Way2wealth Steel 27Sep10

29

Indian Steel Scenario Indian Steel Scenario Sep 2010 Sep 2010 Way2Wealth Way2Wealth making investing simpler, more understandable and profitable making investing simpler, more understandable and profitable. .

-

Upload

nishant-pathak -

Category

Documents

-

view

217 -

download

0

Transcript of Way2wealth Steel 27Sep10

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 1/29

Indian Steel ScenarioIndian Steel ScenarioSep 2010Sep 2010

Way2WealthWay2Wealthmaking investing simpler, more understandable and profitablemaking investing simpler, more understandable and profitable..

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 2/29

Commodity Update

9

9 Manufacturin

Indian Economy

9 Agriculture

9 Inflation & Interest Rates

9 Trade

9 FII & Credit Growth

9 Indian Steel Scenarioaw a er a – eserves, ro uc on ra e

9 Crude Steel – Capacity & Production

9 Consumption – Sector & Product

–

9 Global Steel Scenario

9 Domestic Steel Balance Sheet

9 Steel Companies under focus

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 3/29

Indian Economy – Manufacturing

- --

12.0

16.0

20.0

IIP Index Grow th

20.0

30.0

40.0

50.0

0.0

4.0

8.0

10.0

0.0

10.0

Manufactur ing (%-YoY) Other Manufactur ing (%-YoY)

4.0

Jul-02 Jul-03 Jul-04 Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10

Source:MOSPI

¾ Indian manufacturing growth remain positive via strong growth in capital goods and moderategrowth in consumer goods & Others

20.0

Jul-02 Jul-03 Jul-04 Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10

Source:MOSPI

¾ Strong order book, expansion mode by major Corporates amid optimistic consumerism augur well

with steady IIP growth with Metal, Automobile and SME enterprises in focus

¾ Latest IIP growth of 13 percent induced higher volatility and moving forward base effect & higher

¾ Despite hiccups, moving forwards from higher interest rates & uncertain global markets; Govt

additional spending on supplementary demand for grants coupled with higher outlay for

Infrastructure Capex, keep IIP to remain above/around +8.5 percent

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 4/29

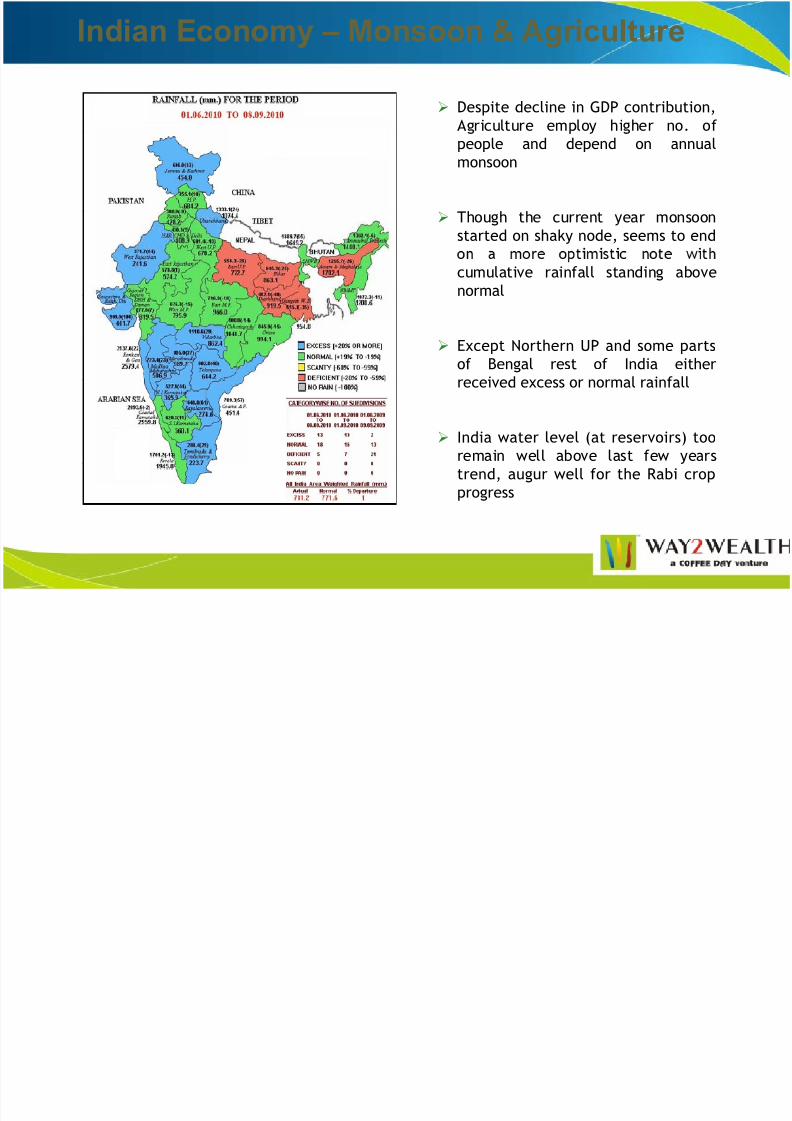

Indian Economy – Monsoon & Agriculture

¾ Despite decline in GDP contribution,Agriculture employ higher no. of

people and depend on annual

monsoon

¾ Though the current year monsoon

started on shaky node, seems to end

cumulative rainfall standing above

normal

¾ Except Northern UP and some parts

of Bengal rest of India either

received excess or normal rainfall

¾ India water level (at reservoirs) too

remain well above last few years

trend, augur well for the Rabi crop

progress

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 5/29

Indian Economy – Inflation & Interest rates

-

5.0

10.0

15.0

20.0n a - ey n eres a es

7

8

9

10

10.0

5.0

0.0

WPI Total WPI Prim ArtiWPI Manf WPI Fuel & power

3

4

5

6

¾ Though moderating off late, overall inflation remain above the double digit levels thanks to Non

.

Aug-07 Feb-08 Aug-08 Feb-09 Aug-09 Feb-10 Aug-10 29/02/2008 31/08/2008 28/02/2009 31/08/2009 28/02/2010 31/08/2010

CRR Repo Cut Off Rev Repo Cut Off Source: RBI

oo n a on

¾ Despite ease in food prices, strong demand, higher MSP and market based energy prices expected

to leave inflation a stubborn thorn in the months to come

¾ Moderation in IIP, good harvest and base impact to lower the inflation only by the end of the

year/fiscal period

¾ Credit/capital growth, energy imports and overall firmness in food prices made RBI change policy

stance towards controlling & anchoring inflation

’ ,

Nov’10

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 6/29

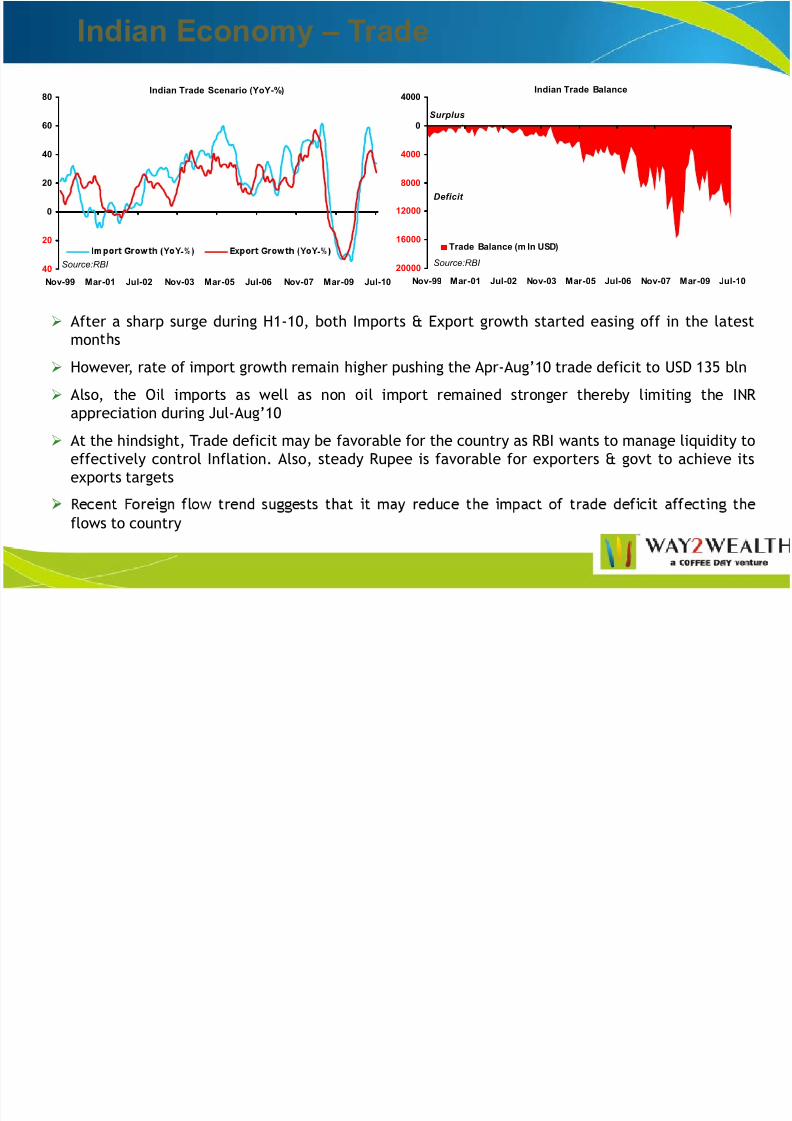

Indian Economy – Trade

Indian Trade Scenario (YoY-%)

40

60

80Indian Trade Balance

4000

0

4000

Surplus

20

0

20

- -

16000

12000

8000

Trade Balance (m ln USD)

Deficit

40

Nov-99 Mar-01 Jul-02 Nov-03 Mar-05 Jul-06 Nov-07 Mar-09 Jul-10

Source:RBI 20000

Nov-99 Mar-01 Jul-02 Nov-03 Mar-05 Jul-06 Nov-07 Mar-09 Jul-10

Source:RBI

¾ After a sharp surge during H1-10, both Imports & Export growth started easing off in the latest

mon s

¾ However, rate of import growth remain higher pushing the Apr-Aug’10 trade deficit to USD 135 bln

¾ Also, the Oil imports as well as non oil import remained stronger thereby limiting the INR

appreciation during Jul-Aug’10

¾ At the hindsight, Trade deficit may be favorable for the country as RBI wants to manage liquidity to

effectively control Inflation. Also, steady Rupee is favorable for exporters & govt to achieve its

exports targets

flows to country

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 7/29

Indian Economy – Capital Flows & Credit

Net Foreign Investme nts - 3M Avg

1000

1500

2000

25003000

-

2

4

6

2

3

3

2000

1500

1000500

0

500

Net FII (Mln USD)

6

4

2

0

1

1

Total Food Non Food

Apr-06 Feb-07 Dec-07 Oct-08 Aug-09 Jun-10 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10

Source:RBI

¾ Both FII & FDI continue to remain strong & Positive so far during FY10-11, while availability of other

forms of fund raising by corporate India could let credit growth remain slower

¾ Credit growth has picked up significantly from its recent lows to 18-20 percent levels with

expectations of the trend to remain upbeat as govt borrowing would be lower in H2

¾ Key concerns to credit growth is the increasingly direct access of credit by corporate in the primary

debt market coupled with fall in deposit growth.

¾ If deposit growth doesn't pick up to 17-18 percent levels then it may impede the credit growth given

the deficit systemic liquidity

¾ However, the money growth and overall optimism in the underlying economy augur well for the pick

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 8/29

Indian Economy – Capital Flows & Credit

2008-09 2009-10 2010-11 F

Real GDP 6.70 7.40 8.30

IIP 2.75 10.3 10.8

WPI 8.46 3.17 6.50

9.6

9.0

6.7

7.4

8.3

8

10

CPI 8.93 11.9 10.0

PLR 12.8 11.8 13.0

91-181 TB Yield 7.09 - 7.15 3.53 - 4.33 4.5 - 5.5

10 Yr G Sec Yield 7.6 7.2 8 2

4

6

Source: RBI, W2W Estimates

¾ Rise in investments, better than expected monsoon and GoI emphasis on creation of infrastructureaugur well for the Indian growth momentum to move from cyclical to structural

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 E 2010-11 F

Source:RBI, W2W Estimates

¾ However, normalizing incentives, monetary policy amid weaker external consumer call for

moderation during Q3 of FY 2010-11

¾ Upbeat in sentiments from monsoon, steady to upswing in the job market amid softer lending

-

¾ Despite ease in Food inflation (largely statistical) pick up in demand, limited capacity in short term,

firm commodity prices globally is expected to keep the inflation higher in the current cycle

¾ Emergence of a new crisis and untimely policy/inability to balance inflation/growth momentum are

t e ey r s to t e a ove out oo

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 9/29

Commodity Update

9 Indian Economy

9 Manufacturing

9 Agriculture

9 Inflation & Interest Rates

9 Trade

9 FII & Credit Growth

9

9 –Indian Steel Scenario

,

9 Crude Steel – Capacity & Production

9 Consumption Sector & Product

9 Demand Scenario – Em hasis On Infrastructure

9 Global Steel Scenario

9 Domestic Steel Balance Sheet

9 Steel Price Outlook

9 Steel Companies under focus

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 10/29

Indian Steel: Iron Ore - Reserves

14630Haematite

India Iron Ore Reserves

Source: JPC, in mln t

25249Total

10619Magnetite

¾ Ukraine, Russia, Australia, China and Brazil hold significant share in global Iron Ore reserves with

proven Iron content

¾ India’s share in global Iron Ore reserve base stand at +6 percent, equals to +25.2 bln tons spread

across Karnataka, Jharkhand, Orissa and Chhattisgarh

¾ India’s resources of iron ore are classified under Haematite–14.6 bln t and Magnetite-10.6 bln t

¾ India produces Iron Ore in all marketable products, like lumps, concentrates, pellets, powder and

sinter

¾ Beneficiation and Pelletization remain low in the Indian Iron Ore industry, which otherwise can

improve the quality

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 11/29

Indian Steel: Iron Ore - Production

314

257

200

250

300

350

20

25

30 Production Share of Iron Ore - India

62%

15%

0%

6.4 6.1

8.2

0

50

100

150

0

5

10

23%

- - - - -

Production (mln t) Production Growth (%-YoY)Source: JPC, W2W Source: JPC, W2W

¾ Amid absence of any new mining project, Indian Iron Ore production is largely driven by the

growth/demand for exports over the last decade

ue o prox m y an qua y na rema ne arges mpor er on spo mar e as s an a n urn

let the Indian Iron Ore production to register a CAGR growth of 16 percent during FY 2004-10

¾ Restriction on export (quality/tax), allocation of fresh mining and clampdown on illegal mining

expected to result in slower to steady pace of production during 2010~2013

¾ 62 percent of the Indian iron Ore production is of medium quality (Iron content between 62~65

percent), while high quality Ore production stand at 23 percent

¾ Our analysis shows that during 2010-15, the Indian Iron ore production is likely to register a CAGR

growth of +7 percent amid strong growth in domestic steel capacity

¾ As a result of which, we foresee limited export growth of Iron Ore in the future (2~3 years)

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 12/29

Indian Steel: Coal - Reserves

¾ North America, Russia, China and Australia hold major share in the global Coal reserves, while’

¾ India’s proven coal reserves stand at 105.8 bln tons (8 percent of the global reserves) with little

Coking coal (key for Iron & Steel) reserves ~ 4 percent of 105.8 bln tons

¾ Further Indian coal reserves contain high Ash content (avg~34.1)with low Carbon (avg~31.6)&

a or c va ue avg~

¾ Further majority of the Industry/production is in the hands of public sector companies limiting the

innovation/advancement in the process of production

¾ Thou h the NMDP-2008 su est ease in minin / roduction ermits recent develo ments across ke

producing states may keep the production growth below the targets

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 13/29

Indian Steel: Coal – S&D & Imports

India Coal Scenario - S&D Growth

15.0

20.0

25.0

Production Growth

Consumption Growth

130

150

170

190

Import Requirements

(mln t)

5.0

10.0

30

50

70

90

0.0

2000-01 2003-04 2006-07 2009-10 2012-13 FSource: MoC, W2W Research

10

2000-01 2004-05 2008-09 2012-13 FSource: MoC W2W Research

¾ Upcoming projects in Power Generation, Cement and Iron & Steel are expected to keep thedomestic consumption of coal at a scorching pace

¾ On the other hand, the current production trend and policy suggest the domestic supply to remain

below the consumption and thereby open the door for significant rise in coal/coke imports

¾ Iron and Steel sector is expected to drive the demand by an average +10 percent, Power Sector and

~

¾ However, the pace of production may alter (probably on the higher side) as the mining policy

towards fuel mineral is expected to change over the due course

¾ Despite ‘major’ steel players are integrated and are scouting for resources elsewhere, the average

global coal prices are expected to remain higher during 2010-12

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 14/29

Indian Steel: Crude Steel – Capacity

93

80

73

112

21

16

80

100

120

15

20

25

7366

60

86

1850

60

70

80

90

10

12

14

16

18

20

9

0

20

40

0

5

1010

0

10

20

30

2004-05 2006-07 2008-09 2010-11 E 2012-13 F

0

24

6

8

- - - - -

Crude Capacity (mlnt) Capacity Growth (%-YoY)Source: JPC, W2W

¾ An expanding consumer market make India a place for host of steel companies to set up

manufacturing capacities

Finished Steel Production Crude Steel Prod Growth (%-YoY)

Source: JPC, W2W

m suppor ve po cy rom o , e omes c s ee sec or as a rac e a s agger ng nves men o

about USD 238 billion, during 2008-10 consisting 222 MoUs signed

¾ Majority of the new capacities are of brown field (74 percent) and are coming up across Orissa,

Jharkhand, Chhattisgarh, Karnataka and West Bengal

¾ Although the industry is exhibiting positive growth, it is facing some major challenges also in terms

of regulatory barriers in land acquisition, raw material availability and other issues

¾ The best case scenario suggest that Indian crude steel capacity to register a CAGR growth of 11.4

percent during 2010-13 reaching 112.3 mln tons

¾ As a result of expanding capacities, Indian crude steel production would also register a CAGR growthof 10.7 percent during 2010-13 to reach +97 mln tons

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 15/29

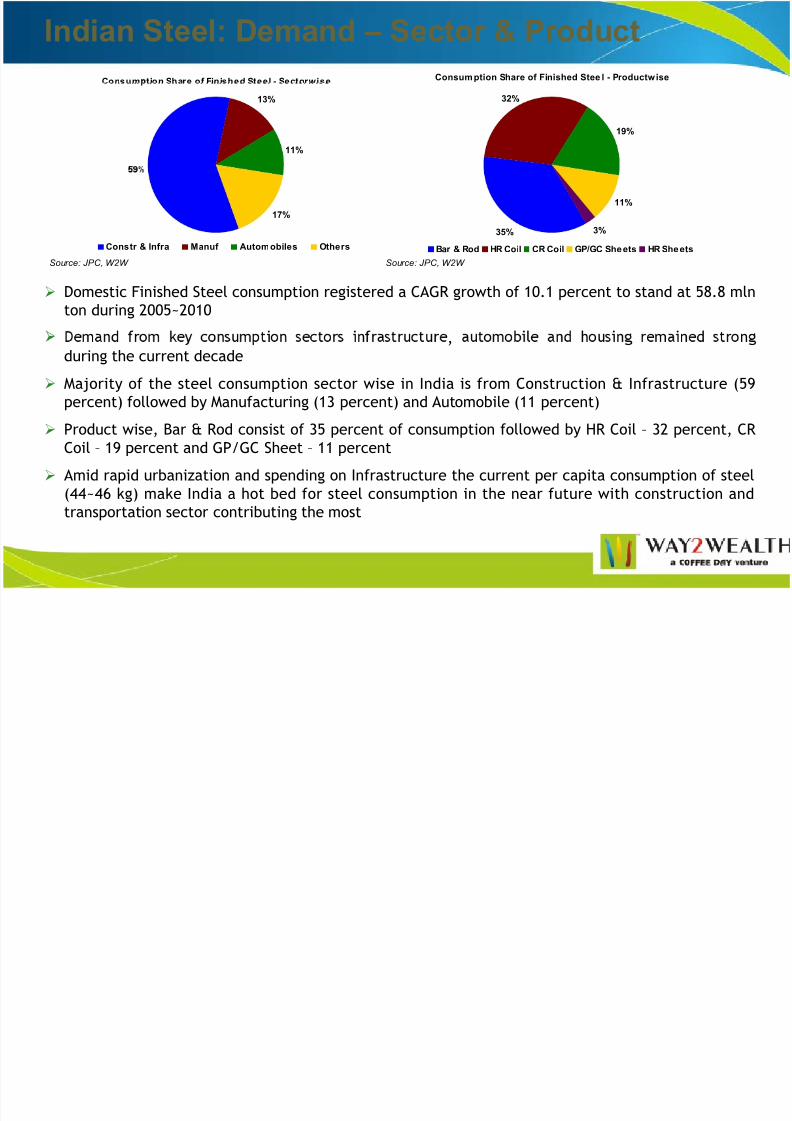

Indian Steel: Demand – Sector & Product

Consum tion Share of Finished Steel - Sectorwise Consumption Share of Finished Stee l - Productwise

13%

11%

19%

32%

17%

Constr & Infra Manuf Automobiles Others

35%

11%

3%

Bar & Rod HR Coil CR Coil GP/GC Sheets HR Sheets

Source: JPC, W2W Source: JPC, W2W

¾ Domestic Finished Steel consumption registered a CAGR growth of 10.1 percent to stand at 58.8 mln

ton during 2005~2010

,

during the current decade

¾ Majority of the steel consumption sector wise in India is from Construction & Infrastructure (59

percent) followed by Manufacturing (13 percent) and Automobile (11 percent)

¾ Product wise, Bar & Rod consist of 35 percent of consumption followed by HR Coil – 32 percent, CR

Coil – 19 percent and GP/GC Sheet – 11 percent

¾ Amid rapid urbanization and spending on Infrastructure the current per capita consumption of steel

(44~46 kg) make India a hot bed for steel consumption in the near future with construction and

transportation sector contributing the most

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 16/29

Indian Steel: Demand – Infrastructure

Infrastructure¾ The basic facilities, services, and installations - of a country or community - such as transportation

network, communications systems, water, power lines, Roads & Buildings and Other public

institutions is considered essential for enablin roductivit of an econom and re uire hu e

initial investments

¾ During early 80’s infrastructure was defined primarily with respect to the nation’s public works and

.

According to Dr. C. Rangarajan Commission, Infrastructure in India include,

¾ Railways (Tracks, Signalling systems, Stations etc)

oa s r es

¾ Airports, Runways and Other facilities

¾ Electricity (T&D)

¾ Pipelines (water, energy and other)

¾ Port facilities

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 17/29

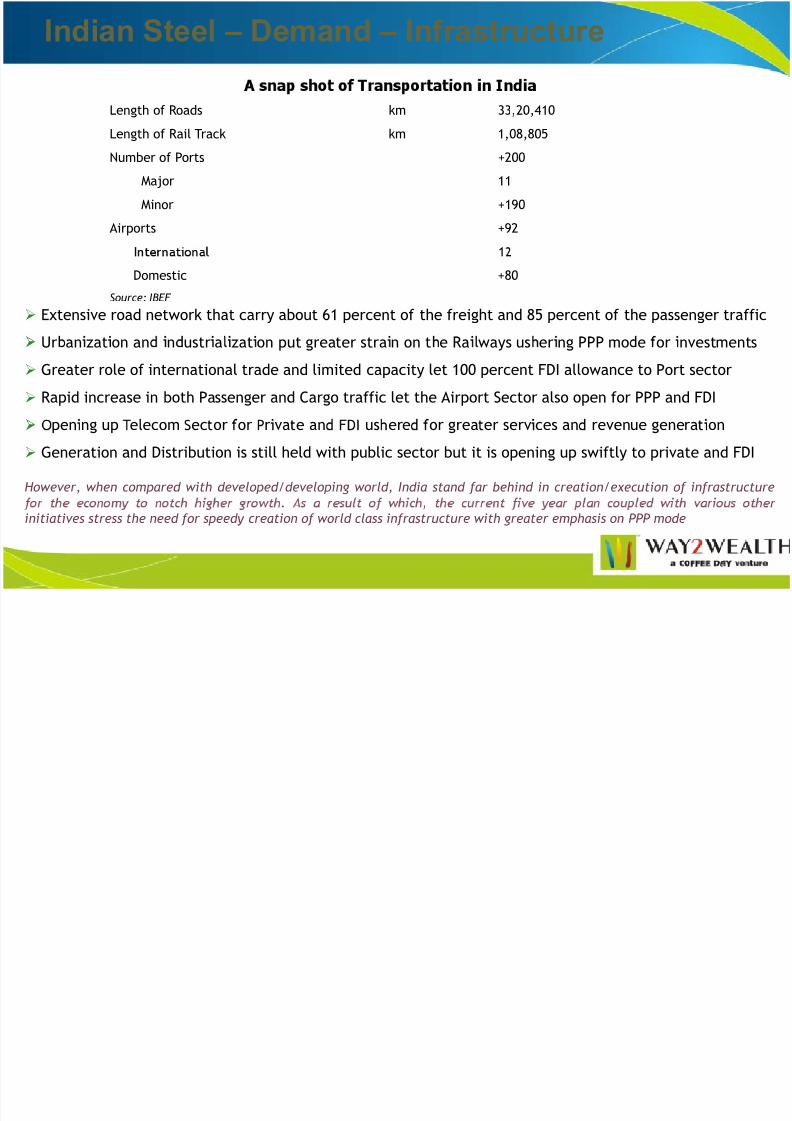

Indian Steel – Demand – Infrastructure

Length of Roads km 33,20,410

Length of Rail Track km 1,08,805

Number of Ports +200

Major 11

Minor +190Airports +92

Domestic +80

Source: IBEF

¾ Extensive road network that carry about 61 percent of the freight and 85 percent of the passenger traffic

Ur an zat on an n ustr a zat on put greater stra n on t e Ra ways us er ng PPP mo e or nvestments

¾ Greater role of international trade and limited capacity let 100 percent FDI allowance to Port sector

¾ Rapid increase in both Passenger and Cargo traffic let the Airport Sector also open for PPP and FDI

pen ng up e ecom ec or or r va e an us ere or grea er serv ces an revenue genera on

¾ Generation and Distribution is still held with public sector but it is opening up swiftly to private and FDI

However, when compared with developed/developing world, India stand far behind in creation/execution of infrastructure

. ,

initiatives stress the need for speedy creation of world class infrastructure with greater emphasis on PPP mode

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 18/29

Indian Steel – Demand – Infrastructure

-

80

100

120

140-

3.3

3.0

2.6

1.92

3

3

4

20

40

60

Actual Outla USD bln Pro ected Outla USD bln

1.0

1

1

2

0

2003-04 2005-06 2007-08 2009-10 2011-12Source: Planning Commiss ion

¾ Total lanned outla for infrastructure for 11th FYP um ed b 138.9 ercent to USD 514 bln from

2003-04 2005-06 2007-08 2009-10 2011-12Private Sector Contribution to Infrastructure (as a % of GDP)

Source: Planning Commission

USD 218 bln during the 10th FYP

¾ However, hurdled by various policy issues in identifying, granting and allocating finances, the

expenditure is expected to be lower than the projected/assumed outlay

,push the overall spending on infrastructure from current 7 percent of GDP to +8.5 percent of GDP

by 2012

¾ Despite all the above, India still need to spend more than USD 1 trillion on infrastructure by 2020

,

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 19/29

Indian Steel: Demand – Infrastructure

¾ Power generation and Distribution continue to’

India - Investments Into Infrastructure

8.49

followed by Roads & Telecom

¾ However, under the 11th FYP Sea Ports &

Airways increased the share of investments

with sli ht decline in the Road and Rail4.8

5.9

7.5

.

5

6

7

8

¾ PPP mode of operations and increased

allocation in the planned investments augur

well for infrastructure growth2

3

4

2003-04 2005-06 2007-08 2009-10 2011-12

As a % of GDPSource: Planning Commission

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 20/29

Indian Steel: Demand – Infrastructure

Planned Expansion of Roads

60000

80000

100000

Power Generation (MWh)

15000

20000

25000

Thermal Hydro

Nuclear Total

0

20000

40000

Target (in km)

0

5000

10000

- - - - - - -

Source: Planning Commission

Planned Expansion of Port Capacity1300

- - - -Source: Planning Commission

¾Near term targets for road, power and portremain higher when compared to the 10th FYP

700

900

1100¾ Achieved targets so far remain low in Road and

Power, while the capacities at ports are

increasing

¾ Elsewhere rivate artici ation in housin

300

500

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Port Capacity (mln t)

Source: Planning Commission

urban facilities and telecom continue to

increase the capacities

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 21/29

Indian Steel: Demand – Infrastructure

As infrastructure inadequacies would constitute a significant constraint in realizing the potential

growth of the economy an ambitious programme of infrastructure investment has been developed

for the 11th FYP

¾ RGGVY – Rajiv Gandhi Grameen Vidyutikaran Yojana – Electricity Distribution

– –

¾ JNNURM – Jawaharlal Nehru National Urban Renewal Mission – Urban Infrastructure

¾ AIBP – Accelerated Irrigation Benefit Programme – Irrigation and Canal Development

¾ NHDP – National Highways Development Programme – Roads

¾ NMDP – National maritime Development Programme – Ports

¾ MRTS – Mass Rapid Transport Systems – Urban Transport

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 22/29

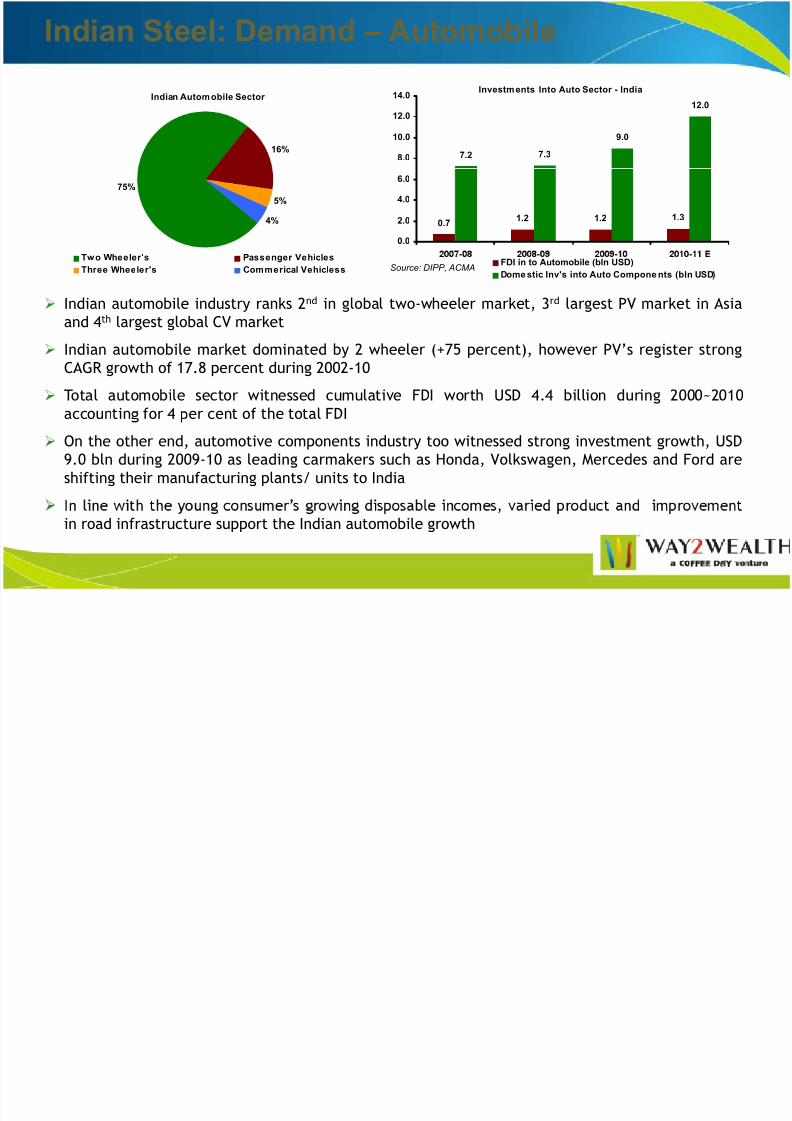

Indian Steel: Demand – Automobile

Investments Into Auto Sector - India

7.2 7.3

9.0

12.0

8.0

10.0

12.0

14.0Indian Automobile Sector

16%

0.71.2 1.2 1.3

0.0

2.0

4.0

6.075%

5%

4%

- - - -FDI in to Automobile (bln USD)

Domestic Inv's into Auto Compone nts (bln USD)Source: DIPP, ACMA

Two Wheeler's Passenger Vehicles

Three Wheeler's Commerical Vehicless

¾ Indian automobile industry ranks 2nd in global two-wheeler market, 3rd largest PV market in Asia

and 4th largest global CV market

¾ Indian automobile market dominated by 2 wheeler (+75 percent), however PV’s register strong

CAGR growth of 17.8 percent during 2002-10

¾ Total automobile sector witnessed cumulative FDI worth USD 4.4 billion during 2000~2010

accountin for 4 er cent of the total FDI

¾ On the other end, automotive components industry too witnessed strong investment growth, USD

9.0 bln during 2009-10 as leading carmakers such as Honda, Volkswagen, Mercedes and Ford are

shifting their manufacturing plants/ units to India

’ ,

in road infrastructure support the Indian automobile growth

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 23/29

Indian Steel: Final Demand – Sector wise

2009-

10 2012-13 F CAGR GrowthAutomobile 6.5 10.3 16.7

Construction 23.5 33.2 12.2

Indian Finished Stee l Consumption & Grow th

7265

59

79

10.310.310.750

60

70

80

90

10

12

14

16

. . .

Manufacturing 7.1 9.1 8.8

Railways 3.2 3.9 6.0

Other Manf 3.9 4.6 5.3

Others 12.2 14.8 6.7 0

10

20

30

40

0

2

4

6

8

Source: MoS, W2W Research, in mln tons finished steel

¾ Automobile & auto components, Construction, Household Appliances (white goods) and-

2004-05 2006-07 2008-09 2010-11 E 2012-13 F

Domestic FS Consum ption Consumption Growth (%-YoY)

Source: JPC, W2W Research

¾ Assuming Indian GDP to register an average GDP growth of +8.32 percent during 2010-13,

domestic finished steel consumption estimated to grow at a CAGR of +9 percent to reach +79 mln

tons

¾ However, steady consumer at matured economies and any unforeseen spillover of risks can limit

the above estimated growth

¾ The same is expected to register a higher CAGR growth of +9.2 percent to reach +82 mln tons if

the external and internal economy remain robust and intensity of consumption increase with

growth

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 24/29

Steel: Global Dynamics

Raw Material

¾ Above cash cost prices over the last few years and significant amount of Capex to boost Iron ore miningcapacity & production in the medium term (6~8 months)

¾ Global Iron ore production set to register a CAGR growth of 5.7percent with incremental gains coming from

India China and Latin American countries

¾ Global coking coal production continue to suffer mild set back in short term (3~6 months) with majority of

the new capacities are coming up with execution risks¾ During 2011-12, global Iron ore prices would trend south steadily, while Coking Coal prices would remain

firm from the current levels

Supply

¾ Global supply of finished steel remain well balanced with emerging Asia add on new capacities, while thatof the matured economies increases the operating rate.

¾ After China & India, Japan, Korea and Taiwan continue to add the production gains

¾ Longs production remain strong across South Asia, while flat and semis production to remain strong in China

Demand ¾ Strong demand coming from emerging Asia and concentrated in India and China

¾ Demand remain robust from transportation, house hold appliances amid steady demand from

infrastructure, construction and housing

,

across

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 25/29

Indian Steel: Balance Sheet

2008-09 2009-10 2010-11 E 2011-12 F 2012-13 F

Finished Steel Production 57 60 66 73 86

Imports 5.8 7.2 7.7 5.7 6.2

o a upp y

Domestic FS Consumption 53 59 65 72 79

Exports 4.0 3.2 4.0 4.7 5.5

S&D Balance 5.1 4.9 4.6 1.8 7.0

Source: MoS, W2W Research, In mln tons

¾ Demand is estimated to remain robust & above production, resulting domestic S/D to remain

balanced in the short run

¾ However as demand would outpace during Q4-10 CY to Q2-11 CY Indian S/D would turn tight,

¾ As new capacities comes up with execution risk amid high dependency on key raw materials, the

average steel prices are set to move steadily higher during 2010-12

¾ Average domestic Mild Steel Ingots ( Mandi Gobindgarh) prices are likely to move higher

y13.5~16.8 percent n FY 10 15~18 percent n FY 11

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 26/29

Indian Steel: Technical Scenario 1

ee ngo s on nuous ar on

40000

3

5

30000

35000

B[A]

[C](5)(3)

31,000

27,000

20000

250004

(1)

[B](4)

(2)

23,000

15000

Jan-07 Nov-07 Sep-08 Jul-09 May-10

A

Source:Bloomberg,Way2Wealth Research

¾ We believe, steel has entered B primary wave correction and the current upwards correction is

expected to conclude at ` 31,000 in next couple of months

¾ As it is forming a wedge pattern, initially steel can correct back to ` 23,000, which would be the

opportunity for longs to accumulate for subsequent targets of ` 27,000 & ` 31,000 subsequently

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 27/29

Indian Steel – Outlook & Strategy

Global S/D to remain

steady in medium term

Asian S/D to remain

As prices are

supported by raw

material firmness in

the short run and

As raw material pricesare expected to calm

down in medium term

investors should also

Steel tighter in the medium

term

Indian demand to

outpace the supply in

ec n ca y, s ee oo s

attractive at the base of

22000-24000 levels,

which gives opportunity

for an upside target of

-

demand in the

medium term,

Go LONG on Steel

Long GHZ @ INR

~

expose emse ves o

gain from the volumetric

growth besides price

growth. Go LONG on

steel majors like TATA &

Supply to remain firm in

As Iron ore prices are

expected to ease down

globally albeit with

robust demand growth in

Iron Ore

concerns over new

mining and trade

Supply to remain healthy

with new production

,

companies may witness

slower revenue growth.

However short term

strength and volatility in

However, as industry try

to converge from long

term contracts to

quarterly with

the best of the available

stocks for gains

Look for building Long

in SESA GOA on

volatility intact

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 28/29

Indian Steel: Stocks in Focus

COMPANY PRODUCTS

Tata Flat Lon Tube and Wire

JSW HR, CR, Galvanized Sheet

Sesa Goa Iron Ore, Pig Iron & Coke

NMDC Iron Ore

Adhunik Metallic Medium Integrated company

Raj Ratan Global Wire

Kalyani Pig Iron, Steel, Tube

Maharashtra Seamless Pipes & Tubes

7/30/2019 Way2wealth Steel 27Sep10

http://slidepdf.com/reader/full/way2wealth-steel-27sep10 29/29

Thank you

Research Department

Premise A, 15th Floor, Chandramukhi Building, Backbay Reclamation,

Nariman Point (near Inox Theatre), MUMBAI : 400021

Phone: 022 4019 2900, Fax: 022 40192939