Wave 5 Trends - GlobalWebIndex - August 2011

47

WAVE 5 TRENDS

-

Upload

globalwebindex -

Category

Technology

-

view

102.698 -

download

0

Transcript of Wave 5 Trends - GlobalWebIndex - August 2011

W A V E 5 T R E N D S

Welcome to Wave 5

Five waves of the GlobalWebIndex research project has revealed for the first time the true picture of internet evolution

globally. Two structural trends are influencing consumers worldwide and are the key drivers behind behavioural trends that

are not only occurring globally but diverge from one another at the local level.

The following, is a summary deck designed for external publication, for the full deck and to understand the data and tool

behind the GlobalWebIndex, please visit globalwebindex.net or email [email protected]

ONE WORLD: MANY INTERNETS

THE POST PC ERA: BREAKING

THE MOUSE BARRIER

• LEAN-BACK: THE RISE OF VIDEO

ENTERTAINMENT ONLINE

• REAL-TIME SOCIAL MEDIA:

TRANSFORMING INTERACTION

• FACEBOOK FATIGUE:

THE GROWING PAINS OF A GLOBAL

PLATFORM

• THE SOCIAL BRAND

• A RENAISSANCE FOR

PROFESSIONAL MEDIA

“The most detailed research

study ever instigated into

the consumer adoption of

the internet”

Jump to

Detail

Delivered in all key internet markets

Waves 1 - 4

Wave 5

Wave 6

Wave 7

Wave 8

Future Waves

Filling a critical knowledge gap

100K+

surveys a

year

3 Waves of

Research

a Year

27 markets

in Wave 5

1000+

variables

to build an

audience

160

questions

on internet

and social

+ + +

Insight CreativityStrategy Planning R O I

+

We Make Data Accessible

Online

Tool

Desktop

Crosstab

Custom

Insight

Agenda

Insight

S U M M A R Y O F W A V E 5 T R E N D S A N D

K E Y P O I N T S

Summary: The internet is diverging

Shift in the way that consumers use

not just the internet but the computer

itself

In the coming months, internet users

across the world believe that the way they

access the internet in Wave 5, is likely to

change from being the PC/laptop to being

a mobile device, either mobile phones or

tablets.

By putting a computer inside the mobile

phone, mobile device manufacturers

started a process that has seen mobile

phones and tablet devices evolve to a

point where people no longer go to the

internet as a separate part of their

everyday lives, but rather, the internet is

evolving to become an integral part of

peoples’ everyday lives. The fact that

mobile devices accompany them at all

times have made this change possible.

Mass market adoption of social media

is driving growing differences between

markets, creating retail / commerce

focused markets and socially focused

ones

Despite being a global platform, that

opens up global content and services to

consumers anywhere in the world, the

internet is actually creating growing

divergence as opposed to

homogenisation.

The internet and in-particular social media

are a reflection of a country and its

peoples. These platforms have in short

created greater localisation and its being

lead by fast growing emerging internet

markets.

This means its increasingly important for

brands to tailor and adjust their strategy to

local markets.

Facebook is no longer the one stop

shop for total internet experience

Despite massive global user growth,

active participation on Facebook is falling

and we are increasingly seeing a slow

down in existing Facebook users. This is

particularly true in the US and other

English speaking countries where

Facebook as been prevalent for longer

and has shifted growth to emerging

markets.

Nevertheless, the potential advertising

revenue is lower in these high-growth

markets because of their relatively

underdeveloped advertising markets.

This, combined with falling engagement in

saturated markets, brings into question

the effectiveness of Facebook as a

branding and advertising channel and

therefore, the exorbitant value investors

have placed on it.

Summary: The Internet is Diverging Into a Global Network of Local Networks

Changes in online content

consumption

The earlier adopters of social media

explored new ways of creating and

sharing online content, however, the

research across the last few waves shows

that now most users focus their

contributions and activities on consuming

and redistributing content.

Wave 5 has highlighted an increasing

divergence in the consumption of online

content across the various markets.

Consumers in newly industrialised

markets of the BRIC countries consume

much more online content than those in

the advanced Western economies such

as the EU 5 and USA.

Consumer engagement with brands

Online consumers want brands to provide

services that fit with their lifestyle. Most

importantly, they want brands to listen to

them and their comments where ever they

are posted whether on a social network

page, company website or micro-blog.

More and more, consumers are expecting

brands to improve their knowledge in

specific areas and to connect them with

other similar-minded brand users.

To drive brand perception, it is now crucial

that brands provide online services that

services the needs of modern consumers

when they want to engage a brand. For

younger, more socially engaged

consumers, this means entertaining them

online with content and services in

addition to driving increased knowledge

around a brand.

Professional content producers will

flourish

Contrary to expectations at the outset, the

rise of social media has led to the

evolution of a retransmission culture

online whereby the content that people

consume is created by professional

sources but filtered and curated by social

means.

Traditional media and news outlets are

still the primary source of news for all

types of people around the world. Instead

of encroaching in the market, social media

has been integrated and used by

traditional media and news channels to

enhance their own content distribution and

reporting.

Nevertheless, social networks now

outrank newspapers as the first source of

news for 16 – 24 year olds globally, but

news websites are still far more widely

used.

S T R U C T U R A L T R E N D 1 :

O N E W O R L D : M A N Y I N T E R N E T S

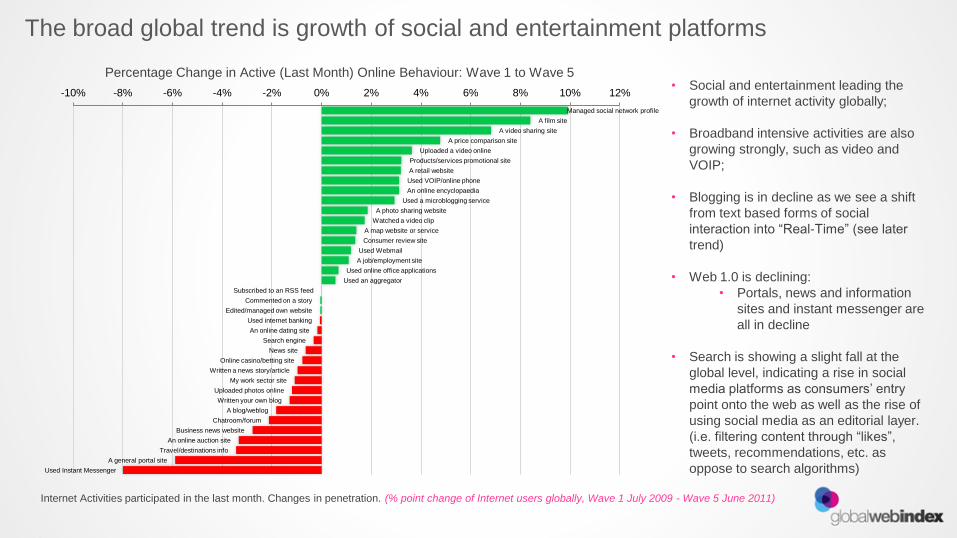

The broad global trend is growth of social and entertainment platforms

Managed social network profile

A film site

A video sharing site

A price comparison site

Uploaded a video online

Products/services promotional site

A retail website

Used VOIP/online phone

An online encyclopaedia

Used a microblogging service

A photo sharing website

Watched a video clip

A map website or service

Consumer review site

Used Webmail

A job/employment site

Used online office applications

Used an aggregator

Subscribed to an RSS feed

Commented on a story

Edited/managed own website

Used internet banking

An online dating site

Search engine

News site

Online casino/betting site

Written a news story/article

My work sector site

Uploaded photos online

Written your own blog

A blog/weblog

Chatroom/forum

Business news website

An online auction site

Travel/destinations info

A general portal site

Used Instant Messenger

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% 12%

Internet Activities participated in the last month. Changes in penetration. (% point change of Internet users globally, Wave 1 July 2009 - Wave 5 June 2011)

• Social and entertainment leading the

growth of internet activity globally;

• Broadband intensive activities are also

growing strongly, such as video and

VOIP;

• Blogging is in decline as we see a shift

from text based forms of social

interaction into “Real-Time” (see later

trend)

• Web 1.0 is declining:

• Portals, news and information

sites and instant messenger are

all in decline

• Search is showing a slight fall at the

global level, indicating a rise in social

media platforms as consumers’ entry

point onto the web as well as the rise of

using social media as an editorial layer.

(i.e. filtering content through “likes”,

tweets, recommendations, etc. as

oppose to search algorithms)

Percentage Change in Active (Last Month) Online Behaviour: Wave 1 to Wave 5

The gap between market leader and laggard is growing in all markets

0%

10%

20%

30%

40%

50%

60%

70%

80%

Wave 1 (Difference Between Leader and Lagard)

Wave 5 (Difference Between Leader and Lagard)

• Looking at a range of internet activities, we can see the

difference between leading and trailing markets in terms

of penetration is growing in 11 out of 16 activities;

• Many of these behaviours are social media, open

platforms, that require little infrastructure and no

payment;

• The open, consumer driven nature of social media has

enabled enthusiastic markets, who are generally newer

to the internet, to adopt and use at a mass scale;

• The large growth in variance in instant messaging is due

to a massive decline in IM usage in many markets;

• Only webmail and internet banking show significant falls

in variance thanks to infrastructure investments in these

services as well as their ubiquity across the world;

• In summary, the internet is not creating a mono-culture

of information and behaviour as some predicted at the

outset. Instead, the cultural fragmentation that existed

offline before the internet now exists online and is visible

in the divergence of online attitudes and behaviour

across the world.

Which of the following have you done online in the past month?. Gap between the leading market and the last. (% difference in users

globally, Wave 1 July 2009 - Wave 5 June 2011)

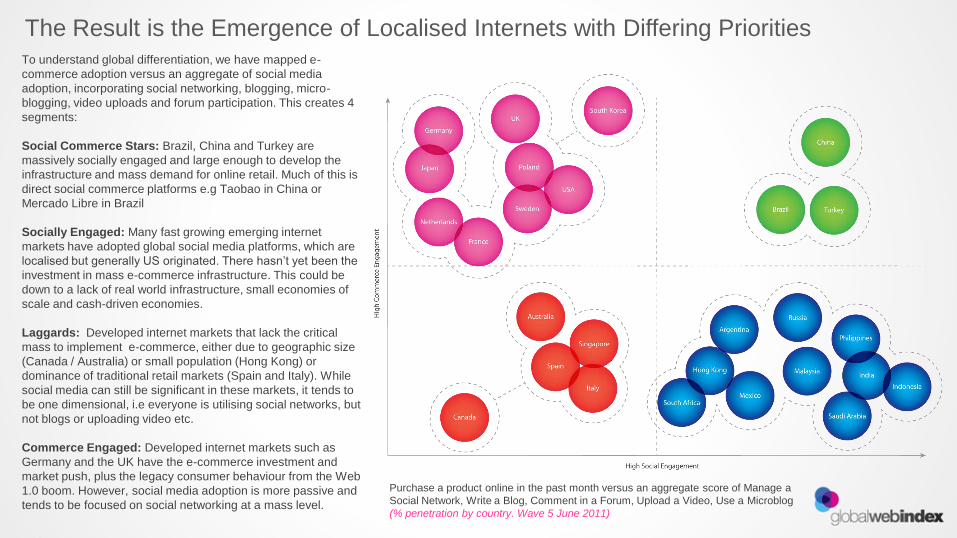

The Result is the Emergence of Localised Internets with Differing Priorities To understand global differentiation, we have mapped e-

commerce adoption versus an aggregate of social media

adoption, incorporating social networking, blogging, micro-

blogging, video uploads and forum participation. This creates 4

segments:

Social Commerce Stars: Brazil, China and Turkey are

massively socially engaged and large enough to develop the

infrastructure and mass demand for online retail. Much of this is

direct social commerce platforms e.g Taobao in China or

Mercado Libre in Brazil

Socially Engaged: Many fast growing emerging internet

markets have adopted global social media platforms, which are

localised but generally US originated. There hasn’t yet been the

investment in mass e-commerce infrastructure. This could be

down to a lack of real world infrastructure, small economies of

scale and cash-driven economies.

Laggards: Developed internet markets that lack the critical

mass to implement e-commerce, either due to geographic size

(Canada / Australia) or small population (Hong Kong) or

dominance of traditional retail markets (Spain and Italy). While

social media can still be significant in these markets, it tends to

be one dimensional, i.e everyone is utilising social networks, but

not blogs or uploading video etc.

Commerce Engaged: Developed internet markets such as

Germany and the UK have the e-commerce investment and

market push, plus the legacy consumer behaviour from the Web

1.0 boom. However, social media adoption is more passive and

tends to be focused on social networking at a mass level.

Purchase a product online in the past month versus an aggregate score of Manage a

Social Network, Write a Blog, Comment in a Forum, Upload a Video, Use a Microblog

(% penetration by country. Wave 5 June 2011)

No such thing as a global online strategy.

Localisation is key online

Social Media presence must be adjusted in each

market

Growing differentiation between markets, creates

opportunities for local players

Online influencers will increasingly emerge from

outside the English language internet

Impact

S T R U C T U R A L T R E N D 2 :

T H E P O S T P C E R A :

W E L C O M E T H E P A C K A G E D I N T E R N E T

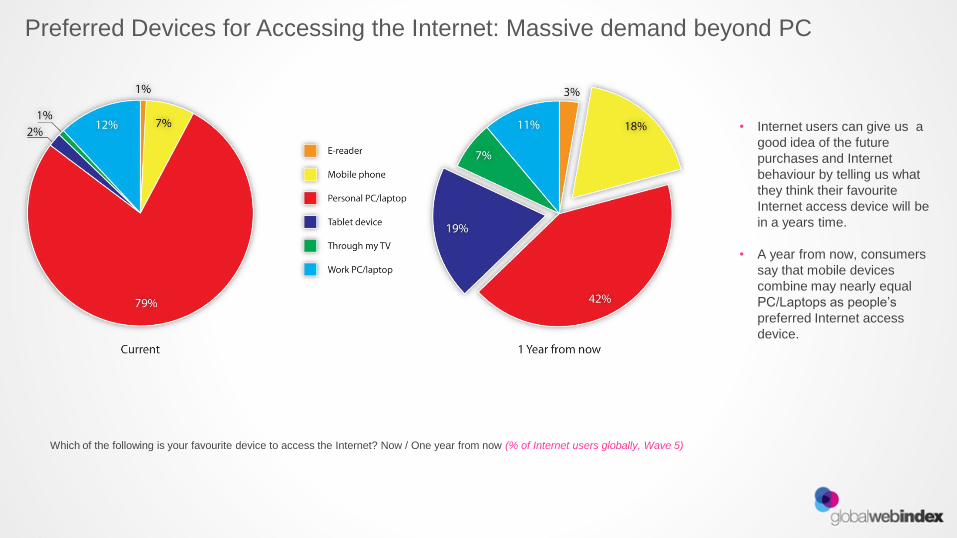

Preferred Devices for Accessing the Internet: Massive demand beyond PC

Which of the following is your favourite device to access the Internet? Now / One year from now (% of Internet users globally, Wave 5)

• Internet users can give us a

good idea of the future

purchases and Internet

behaviour by telling us what

they think their favourite

Internet access device will be

in a years time.

• A year from now, consumers

say that mobile devices

combine may nearly equal

PC/Laptops as people’s

preferred Internet access

device.

Mobile Internet has Already Exploded Globally and Impacting in Home Usage

0%

10%

20%

30%

40%

50%

60%

70%

Wave1 Wave2 Wave3 Wave4 Wave5

Asia Pacific

Europe

Latin America

North America

At home33%

At Work17%

Public Place27%

Whilst Travelling or

Roaming23%

When Accessing Your Mobile, Which is Your Primary Location?

Which of the following have you done on the internet via your mobile phone in the past six

months? – Browsed the internet

(% of internet users globally, Wave 5)

(% of mobile internet users globally, Wave 5)

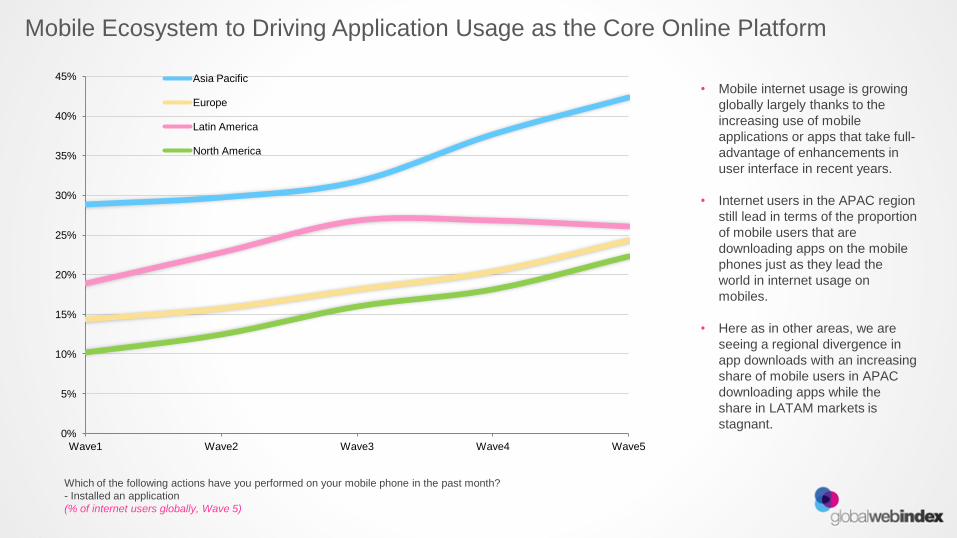

Mobile Ecosystem to Driving Application Usage as the Core Online Platform

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Wave1 Wave2 Wave3 Wave4 Wave5

Asia Pacific

Europe

Latin America

North America

Which of the following actions have you performed on your mobile phone in the past month?

- Installed an application

(% of internet users globally, Wave 5)

• Mobile internet usage is growing

globally largely thanks to the

increasing use of mobile

applications or apps that take full-

advantage of enhancements in

user interface in recent years.

• Internet users in the APAC region

still lead in terms of the proportion

of mobile users that are

downloading apps on the mobile

phones just as they lead the

world in internet usage on

mobiles.

• Here as in other areas, we are

seeing a regional divergence in

app downloads with an increasing

share of mobile users in APAC

downloading apps while the

share in LATAM markets is

stagnant.

Brands must have a multi-platform strategy:

website, mobile site and applications are a must

Packaged platforms reintroduce barriers: Mobile

and tablets are not open consumer driven

platforms. This is an opportunity for brands, who

have the connections and budgets to gain access

Packaged platforms demand that brands think

about creating content. This is particularly true as

internet connected TVs become the norm

Online influencers will increasingly emerge from

outside the English language internet

Impact

Structural Change is Driving a Number of Behavioural Impacts

ONE WORLD: MANY INTERNETS

THE POST PC ERA: BREAKING

THE MOUSE BARRIER

• LEAN-BACK: THE RISE OF VIDEO

ENTERTAINMENT ONLINE

• REAL-TIME SOCIAL MEDIA:

TRANSFORMING INTERACTION

• FACEBOOK FATIGUE:

THE GROWING PAINS OF A GLOBAL

PLATFORM

• THE SOCIAL BRAND

• A RENAISSANCE FOR

PROFESSIONAL MEDIA

B E H A V I O U R T R E N D

T H E R I S E O F T H E “ L E A N B A C K ” W E B

Mass Video consumption is diversifying into multiple internet platforms

16 to 24 25 to 34 35 to 44 45 to 54 55 to 64

Visited a video sharing site 69% 57% 43% 30% 23%

Visited a film site 61% 55% 44% 35% 26%

Watched a full length film 51% 39% 29% 25% 17%

Downloaded free TV shows/film 49% 44% 33% 29% 20%

Visited a Digital content store e.g. iTunes 47% 43% 35% 27% 19%

Stream Personal home videos 42% 31% 22% 16% 10%

Watch on demand TV shows online 40% 35% 29% 27% 24%

Stream Film trailers 31% 25% 17% 11% 7%

Stream Music videos 31% 25% 17% 11% 7%

Listened/Watched a podcast 31% 27% 22% 18% 15%

Streamed a LIVE TV show 25% 20% 16% 11% 9%

Watched a sports program 23% 20% 15% 14% 11%

Download TV show/film via P2P 22% 19% 12% 7% 5%

Watched on demand video clip on a mobile 19% 18% 13% 7% 4%

Paid TV show/film download 14% 13% 9% 6% 4%

Watched live streamed TV on a mobile 9% 8% 6% 3% 2%

Which of the following have you done online in the past month? (% of Internet users globally by age group, Wave 5)

• Globally, younger internet users

are much more active in

consuming content online.

• However, most of the content that

they and older users are enjoying

is not user-generated content but

is professionally produced

content such as full-length

movies and TV shows.

• These same consumers are also

willing to pay for this content, but

the hurdle has been the slow

development of digital content

distribution channels and models.

• This is changing, however, and

promises huge rewards for

content owners as consumers

consume more and more content

online.

Now professional content is driving global differentiation

Which of the following have you done on the Internet in the past month? (% of Internet users in each region, Wave 5)

The difference between the newly

industrialised countries of Brazil, India,

China, and Russia and the advance

Western economies of the EU 5 and

USA in terms of online content

consumption perfectly illustrate the

divergence that is occurring between

all the different internet markets across

the world.

In general, internet users in emerging

markets consume much more content

online. There are, of course, multiple

factors that contribute to this in each

market, but one of the universal factors

is the relative underdevelopment of

traditional media markets in the

emerging countries. As a result, the

quality of online content often

surpasses that which is available

through traditional channels in many

markets.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Global USA EU 5 BRIC

Younger users are the least adverse to paying for content

Which of the following would you consider paying to access online?- None of the above (answer options) (% of Internet users in each market)

• This index chart reveals the proportions

of the Internet population in each country

that would not consider paying for online

content in Wave 5.

• It also shows how averse to buying

online content each age group is

compared to the overall Internet

population.

• The key factor we see is that older

Internet users are generally much less

likely buy content online.

66% 67%

56%

63%

53%

42%

48%

37%41%

28%

Spain France Germany Italy UK USA Brazil India Russia China

16 to 24 25 to 34 35 to 44

45 to 54 55 to 64 Market Average

100

-

+

Consumption of professional video content online

now outstrips consumer created

It is a myth that consumers won’t pay for content

online

Disconnect between the developed media and

content markets in US, UK and Europe and the

consumer demand for content in the emerging

markets. Content producers should look at the

global opportunity

Massive opportunity for brands to build global

content strategy

Impact

B E H A V I O U R T R E N D

R E A L - T I M E S O C I A L M E D I A

The first generation of the Internet

focused on the new ways that

everyone could create and publish

content. As the Internet has

evolved, internet users have moved

more to the consumption and

retransmission of content rather than

producing it themselves.

This is evident when we look at the

fastest growing internet activities

and those with the highest

penetration. Consumption of video

clips on platforms like YouTube and

Dailymotion are among the most

popular internet activities. Micro-

blogging and social networking are

the first and second fastest social

media activities. So much of the

activity on these platforms is

retransmission of content,

retweeting, re-posting of video clips,

etc. and so little is the actual

creation of content. This presents

great opportunities for professional

content creators to harness social

channels to spread their content.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Wave1 Wave2 Wave3

Wave4 Wave5

Micro-blogging and social networking are growing fastest

Which of the following have you done online in the past month? (% of Internet users globally; Wave 1 (September 2009) to Wave 5 (June 2011)

+9%

+10%

+40%

+24%

+2%

+62%

+3%

+6%

+4%

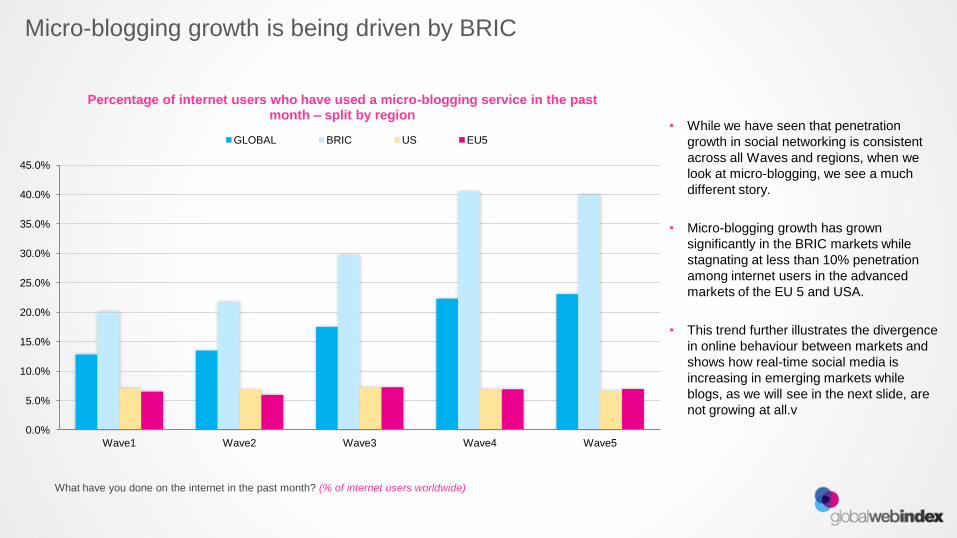

Micro-blogging growth is being driven by BRIC

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Wave1 Wave2 Wave3 Wave4 Wave5

Percentage of internet users who have used a micro-blogging service in the past month – split by region

GLOBAL BRIC US EU5

What have you done on the internet in the past month? (% of internet users worldwide)

• While we have seen that penetration

growth in social networking is consistent

across all Waves and regions, when we

look at micro-blogging, we see a much

different story.

• Micro-blogging growth has grown

significantly in the BRIC markets while

stagnating at less than 10% penetration

among internet users in the advanced

markets of the EU 5 and USA.

• This trend further illustrates the divergence

in online behaviour between markets and

shows how real-time social media is

increasing in emerging markets while

blogs, as we will see in the next slide, are

not growing at all.v

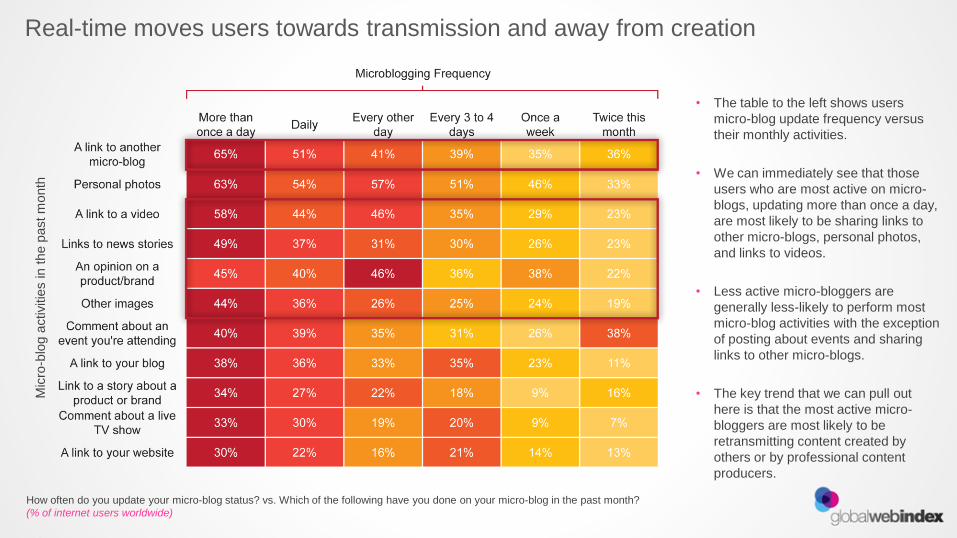

Real-time moves users towards transmission and away from creation

How often do you update your micro-blog status? vs. Which of the following have you done on your micro-blog in the past month?

(% of internet users worldwide)

• The table to the left shows users

micro-blog update frequency versus

their monthly activities.

• We can immediately see that those

users who are most active on micro-

blogs, updating more than once a day,

are most likely to be sharing links to

other micro-blogs, personal photos,

and links to videos.

• Less active micro-bloggers are

generally less-likely to perform most

micro-blog activities with the exception

of posting about events and sharing

links to other micro-blogs.

• The key trend that we can pull out

here is that the most active micro-

bloggers are most likely to be

retransmitting content created by

others or by professional content

producers.

Mic

ro-b

log a

ctivitie

s in t

he p

ast m

onth

Real-time is moving the emphasis away from

creating content to transmitting other peoples

content

Shifts the focus from brands to create rather than

engage consumers to create

Transmitter culture makes journalists, media

owners, content producers and brands more

relevant in the online economy

Mobile devices will turn the internet real-time

Impact

B E H A V I O U R T R E N D

F A C E B O O K F A T I G U E

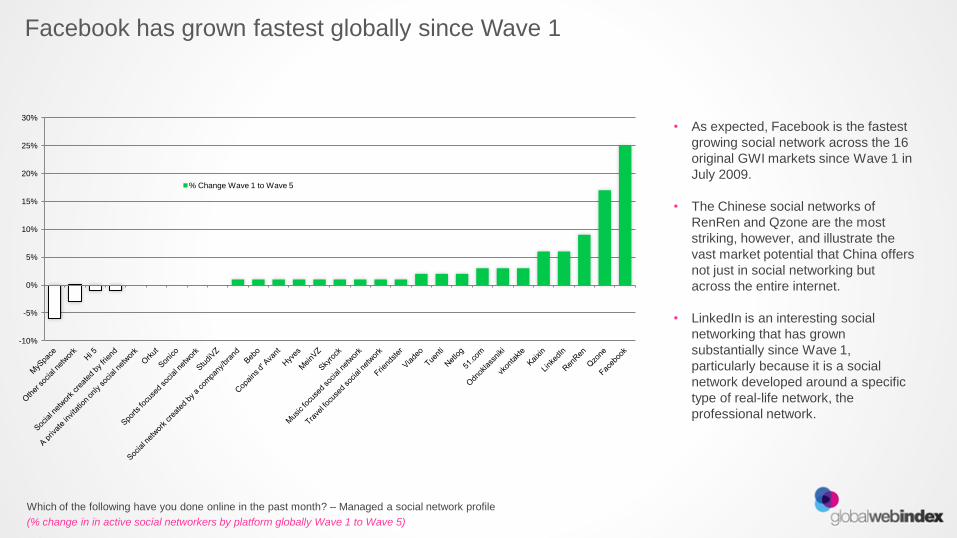

Facebook has grown fastest globally since Wave 1

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

% Change Wave 1 to Wave 5

Which of the following have you done online in the past month? – Managed a social network profile

(% change in in active social networkers by platform globally Wave 1 to Wave 5)

• As expected, Facebook is the fastest

growing social network across the 16

original GWI markets since Wave 1 in

July 2009.

• The Chinese social networks of

RenRen and Qzone are the most

striking, however, and illustrate the

vast market potential that China offers

not just in social networking but

across the entire internet.

• LinkedIn is an interesting social

networking that has grown

substantially since Wave 1,

particularly because it is a social

network developed around a specific

type of real-life network, the

professional network.

However: Broader social networking decline is kicking in

*change based on very low reach <10%

16-24 25-34 35-44 45-54 55-64

Germany -1.6% 4.7% 47.8% 7.1% 62.5%

UK -8.2% -4.7% 17.1% 32.0% 27.8%

Italy 4.9% 35.0% 65.4% 77.3% 75.0%

Spain 48.9% 33.3% 33.3% 70.8% 33.3%

Netherlands 28.1% -10.2% 12.8% 32.0% 114.3%

France 34.6% 11.1% 85.7% 40.0% 110.0%

China 78.8% 112.0% 79.2% 218.2% -28.6%*

Japan 15.4% 4.5% 66.7% 22.2% -33.3%*

USA 2.8% 13.6% 33.3% 16.1% 42.1%

South Korea 156.3% 95.0% 71.4% 58.3% 375.0%

Russia 9.1% 24.5% 42.9% 5.3% 70.8%

India -2.8% 19.4% 17.0% 35.9% 62.1%

Mexico 23.6% 69.0% 71.4% 58.3% 121.1%

Brazil -10.0% 0.0% 15.1% 28.9% 47.4%

Canada 0.0% -1.6% 6.5% -8.3% 31.8%

Australia 4.8% 3.3% 29.7% 36.7% 38.9%

Which of the following have you done online in the past month? – Managed a social network profile (% change in active social networking penetration by market)

• One of the biggest surprises that we

see across the world is the decline in

social network penetration among

younger users in certain markets such

as Brazil, India, and the UK.

• In other markets, however, such as

Spain, South Korea, and China, social

network penetration has seen strong

growth across all age groups.

• In general, the middle age groups are

growing across all countries, and in

many countries, they are the fastest

growing age segments.

• Moving forward, it will be interesting to

examine whether the decreasing

penetration of social networking in

younger age segments is an indicator

of future trends for other age groups.

Massive decline in contribution on Facebook

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Global US US College Educated < 30

• Between Wave1 (July 2009) and Wave 5

(June 2011), there has been a large level of

decline in contribution and active participation

into Facebook

• The hype suggests that with Facebook always

growing its user base, it is quickly becoming

the global social, communication, content and

increasingly purchasing platform. However our

research points to a different story.

• Over time users have began to contribute less

and are increasingly passive. This raises

questions on the quality of user data that often

underpins huge valuation figures. It also raises

questions on whether brands should vest

everything in Facebook pages. This change

suggests they need to diversify

• This decline is most marked in young college

educated Facebook users in the US who were

the original adopters of Facebook. This allows

to forecast a plateau in usage that will spread

into other demographics and markets

Facebook users: Social Network Behaviour / Actions in the past month (% change in active social networking penetration from Wave 1 (July 2009 to June 2011)

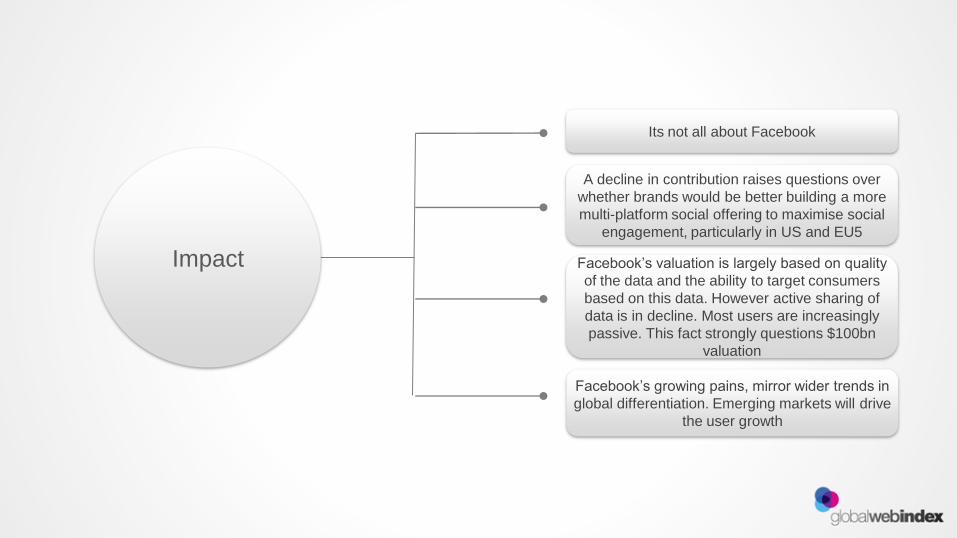

Its not all about Facebook

A decline in contribution raises questions over

whether brands would be better building a more

multi-platform social offering to maximise social

engagement, particularly in US and EU5

Facebook’s valuation is largely based on quality

of the data and the ability to target consumers

based on this data. However active sharing of

data is in decline. Most users are increasingly

passive. This fact strongly questions $100bn

valuation

Impact

Facebook’s growing pains, mirror wider trends in

global differentiation. Emerging markets will drive

the user growth

B E H A V I O U R T R E N D

T H E S O C I A L B R A N D

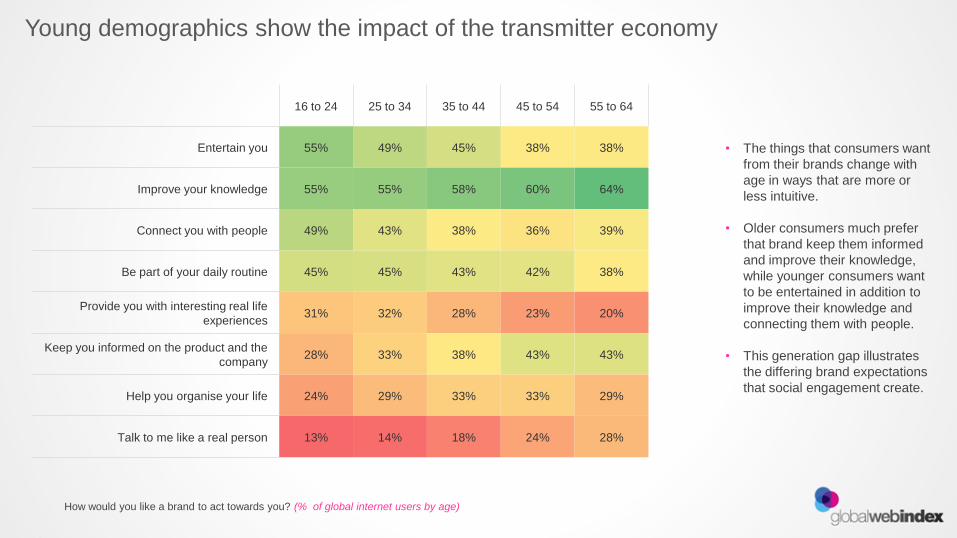

Young demographics show the impact of the transmitter economy

16 to 24 25 to 34 35 to 44 45 to 54 55 to 64

Entertain you 55% 49% 45% 38% 38%

Improve your knowledge 55% 55% 58% 60% 64%

Connect you with people 49% 43% 38% 36% 39%

Be part of your daily routine 45% 45% 43% 42% 38%

Provide you with interesting real life

experiences31% 32% 28% 23% 20%

Keep you informed on the product and the

company28% 33% 38% 43% 43%

Help you organise your life 24% 29% 33% 33% 29%

Talk to me like a real person 13% 14% 18% 24% 28%

• The things that consumers want

from their brands change with

age in ways that are more or

less intuitive.

• Older consumers much prefer

that brand keep them informed

and improve their knowledge,

while younger consumers want

to be entertained in addition to

improve their knowledge and

connecting them with people.

• This generation gap illustrates

the differing brand expectations

that social engagement create.

How would you like a brand to act towards you? (% of global internet users by age)

Social network brand interactions are catching the branded website

0% 10% 20% 30% 40% 50% 60% 70%

Retweeted a branded microblog post

Shared content in a branded community

Asked question to a brand on microblog

Uploaded photo/video to a branded social network page/group

Invited friend to join a branded page/group on social network

Followed branded microblog

Visited branded community

Read branded blog

Chatted with a customer service agent

Visited branded social network group/page

Liked a brand/product

Visit branded website

EU 5 USA BRIC Global

Thinking about all the ways in which you can interact with a brand or company online, which have you done in the past month?

(% of global internet users by age)

• Consumers around the world

still value branded websites

more than any other form of

online marketing and branding

techniques.

• Social marketing techniques are

gaining traction, however, and

liking a brand or product on a

social network is popular among

consumers in all regions in a

relative sense.

Growing demand for one to one relationship and content

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Using microblog/social network pages to provide customer support/service

Becoming your friend in a social network

Creating groups in social networks

Creating blogs to talk about the company and product

Creating a brand community where I can meet new people

Contacting me if I mention the brand on a microblog

Creating videos online featuring the brand

Create applications/online services

Listen to comments on forums/social networks

Wave5 Wave4 Wave3

Which of the following marketing activities would improve your opinion of the participating brand?

(% of global internet users by age)

• Consumers are not bothered

about engaging with brands in a

two-way conversation. What

they want is simply to be

listened to when they need the

brand and for the brand to make

their products and services

readily available where they

are, not where the brand wants

them to be.

• Creating content is also

important, especially for

younger internet users as we

have seen previously.

Consumers react well to high

quality branded content that is

entertaining and engaging.

Social branded channels are close to matching

brand websites in reach

Social media provides a new medium for brands

to engage consumers, but brands must know the

“rules of engagement” and identify what

consumers want from them on these platforms

Their is increasing demand for branded content.

This is a result of the growing demand for a lean

back experience and a result of the transmitter

culture. Brands need a content strategy. The line

between produced content and advertising will

disappear online

Impact

The crucial aspect of social consumer

engagement is to ensure that consumers feel

that their voice is heard online. This doesn’t

necessitate constant two-way conversation but

requires brands to be attentive when that

conversation is wanted

B E H A V I O U R T R E N D

A R E N A I S S A N C E F O R P R O F E S S I O N A L M E D I A

Professionals have never had it so good:

MANY

INTERNETS:

GLOBAL

DIVERGENCE

LEAN BACK

THE POST PC

ERA

REAL TIME

SOCIAL

Global potential for the

distribution of content

Growing rich content

consumption and

willingness to pay

Focus on sharing pro content.

Micro-blogs orientate

consumers to professionals

Package platforms create

the economics to monetise

professional content

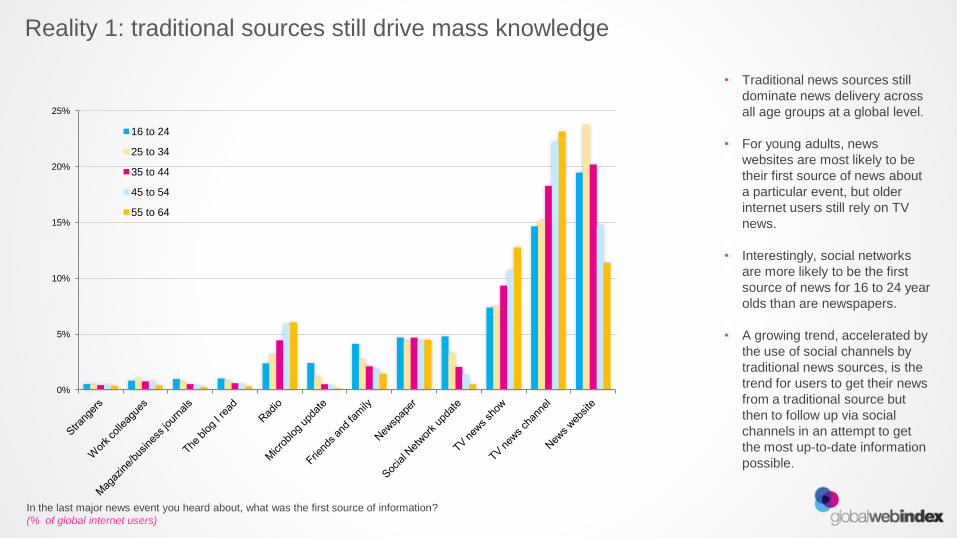

Reality 1: traditional sources still drive mass knowledge

0%

5%

10%

15%

20%

25%

16 to 24

25 to 34

35 to 44

45 to 54

55 to 64

In the last major news event you heard about, what was the first source of information?

(% of global internet users)

• Traditional news sources still

dominate news delivery across

all age groups at a global level.

• For young adults, news

websites are most likely to be

their first source of news about

a particular event, but older

internet users still rely on TV

news.

• Interestingly, social networks

are more likely to be the first

source of news for 16 to 24 year

olds than are newspapers.

• A growing trend, accelerated by

the use of social channels by

traditional news sources, is the

trend for users to get their news

from a traditional source but

then to follow up via social

channels in an attempt to get

the most up-to-date information

possible.

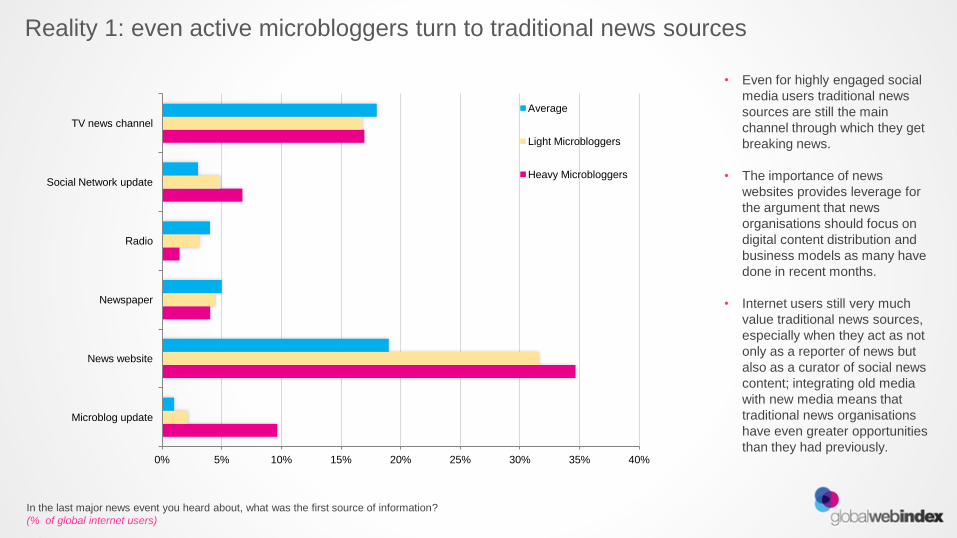

Reality 1: even active microbloggers turn to traditional news sources

0% 5% 10% 15% 20% 25% 30% 35% 40%

Microblog update

News website

Newspaper

Radio

Social Network update

TV news channel

Average

Light Microbloggers

Heavy Microbloggers

In the last major news event you heard about, what was the first source of information?

(% of global internet users)

• Even for highly engaged social

media users traditional news

sources are still the main

channel through which they get

breaking news.

• The importance of news

websites provides leverage for

the argument that news

organisations should focus on

digital content distribution and

business models as many have

done in recent months.

• Internet users still very much

value traditional news sources,

especially when they act as not

only as a reporter of news but

also as a curator of social news

content; integrating old media

with new media means that

traditional news organisations

have even greater opportunities

than they had previously.

Reality 2: traditional TV is not in decline even for heavy social users

22%

33%

21%

12%

7%

6%Less than one hour

1 to less than 2

2 to less than 3

3 to 4

4 to 6

more than 6

Daily micro-bloggers

17%

31%

22%

13%

7%

9%

Daily bloggers

19%

26%

24%

15%

9%

7%

Global Average

How much time do you spend watching TV during a typical day?

(% of internet users by segment)

Social and online must be integrated with offline

strategy

The internet will not replace traditional media,

traditional media will distribute through internet

channels

The internet is becoming more like traditional

media. Packaged platforms, applications etc

enable traditional format with traditional

advertising models

Impact

There is growing demand to build 1 to 1

conversation with brands

E X P L O R E T H E D A T A

g l o b a l w e b i n d e x . n e t

g l o b a l w e b i n d e x @ t r e n d s t r e a m . n e t