WASHINGTON STATEECONOMIC AND REVENUE FORECAST COUNCIL Economic & Revenue Outlook Presented to...

36

WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL Economic & Revenue Outlook Presented to Washington State National Institute of Government Procurement Steve Lerch Executive Director January 21, 2014 Seattle, Washington

-

Upload

deirdre-edwards -

Category

Documents

-

view

217 -

download

2

Transcript of WASHINGTON STATEECONOMIC AND REVENUE FORECAST COUNCIL Economic & Revenue Outlook Presented to...

WASHINGTON STATEECONOMIC AND REVENUE FORECAST COUNCIL

Economic & Revenue Outlook

Presented toWashington State National Institute of Government

Procurement

Steve LerchExecutive Director

January 21, 2014Seattle, Washington

Economic OutlookJanuary 21, 2014

Slide 2WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Summary

• The U.S. and Washington economies continue to grow, although at a slow pace

• Construction activity has been a big contributor to Washington employment growth; employment is rising in most Washington industries except aerospace and the federal government

• Risks to the forecast are generally from factors outside the state, including a weaker Chinese economy, uncertain federal fiscal policy and possible disruptions to the housing recovery

• State revenue collections have returned to pre-recession levels

Economic OutlookJanuary 21, 2014

Slide 3WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

ERFC Forecast Process

National Economic Forecast

Preliminary Washington State Economic Forecast

Review by Work Group

Review by Governor’s Council of Economic Advisors &

Economic and Revenue Forecast Council

Final National and Washington Economic Forecast

Review by Forecast Council

Final Washington General Fund Revenue Forecast

ERFC and Revenue-Generating Agencies Create Revenue Forecasts

The national economic forecast is based on the Global Insight model

Economic OutlookJanuary 21, 2014

Slide 4WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Three major risks to the forecast

Europe & China

• Hard Landing for China

• Slow growth in Europe

• Reduced Exports

Fiscal Policy

• Debt Ceiling• Budget

Housing• Affordability• Household

formation

Baseline Forecast

Economic OutlookJanuary 21, 2014

Slide 5WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

China’s Economic Growth has Slowed

2005-2011 avg 2012 20130%

2%

4%

6%

8%

10%

12%

14%

China Real GDP Growth

Blue Chip IMF ISI History

Source: Blue Chip, IMF, ISI; data through 2013

Economic OutlookJanuary 21, 2014

Slide 6WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Exports have weakened outside of China

2011 2012 20130%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Annual growth in U.S. exports

China All other countries

Source: WISERTrade; 2013 data through November

Economic OutlookJanuary 21, 2014

Slide 7WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Government expenditures remain weak

2011 2011 2011 2011 2012 2012 2012 2012 2013 2013 2013-2

-1

0

1

2

3

4

5Contributions to Percent Change in Real GDP

Personal Consumption Private Investment Net Exports Govt Exp & Investment

Perc

enta

ge P

oin

ts

Source: BEA; data through 2013 Q3

Economic OutlookJanuary 21, 2014

Slide 8WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Debt ceiling debate created uncertainty

Source: U.S. Treasury; data through January 16, 2014

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-140.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Yield on 1-Month Treasure BillsPerc

ent

Economic OutlookJanuary 21, 2014

Slide 9WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Consumer confidence slowly improves

1980 1985 1990 1995 2000 2005 20100

25

50

75

100

125

150

Index Mich: 1966Q1 = 100, SA

Conf Board: 1985 =100, SA

U Mich Conf Board

Source: University of Michigan; Conference Board, data through December 2013

Economic OutlookJanuary 21, 2014

Slide 10WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Housing affordability is high but falling

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

50

75

100

125

150

175

200

225

Housing Affordability Index, SA

U.S. Washington

Index

Source: Global Insight, WA Center Real Estate Research, ERFC; data through 2013Q3

Affordability is 100 when the median income can just afford the median priced home. Above 100 means the median income can afford more than the median priced home

Economic OutlookJanuary 21, 2014

Slide 11WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Mortgage rates are increasing

2001 2003 2005 2007 2009 2011 20133

4

5

6

7

8

30-Year Fixed Mortgage RatePerc

ent

Source: Freddie Mac; data through December 2013

Economic OutlookJanuary 21, 2014

Slide 12WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Many adults continue to live at home with their parents

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

10

11

12

13

14

41

43

45

47

49

51

Homeownership Rate vs. % Living with Parents25-34 year olds

% living w/parents Homeownership rate

% L

ivin

g w

/ Pare

nts

Hom

eow

ners

hip

Rate

Source: U.S. Census, ERFC, data through 2012

Economic OutlookJanuary 21, 2014

Slide 13WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Euro area GDP has returned to positive growth but risks remain

2010

2010

2010

2010

2011

2011

2011

2011

2012

2012

2012

2012

2013

2013

2013

-6

-4

-2

0

2

4

6

8

10

Quarterly GDP Growth

Italy Germany Euro area

Perc

ent

Change S

AA

R

Source: Eurostat; data through 2013Q3

Eurozone Forecast:

2013: -0.4%

2014: 0.9%

2015: 1.3%

Economic OutlookJanuary 21, 2014

Slide 14WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

U.S. GDP is growing

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

21,000

U.S. Gross Domestic Product

Actuals November forecast

Billions

of

Dollars

Source: ERFC November 2013 forecast; historical data through 2012

Economic OutlookJanuary 21, 2014

Slide 15WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Oil prices are expected to be slightly lower in the near term

2005

2005

2005

2005

2006

2006

2006

2006

2007

2007

2007

2007

2008

2008

2008

2008

2009

2009

2009

2009

2010

2010

2010

2010

2011

2011

2011

2011

2012

2012

2012

2012

2013

2013

2013

2013

2014

2014

2014

2014

2015

2015

2015

2015

2016

2016

2016

2016

2017

2017

2017

2017

25

50

75

100

125

Average Price of Crude Oil

September November

Dollars

per

barr

el

Forecast

Source: DOE, ERFC November 2013 forecast; historical data through 2013Q3

Economic OutlookJanuary 21, 2014

Slide 16WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Washington personal income is expected to increase by 5.2% in 2014

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

100

150

200

250

300

350

400

450

Washington Personal Income

Actuals November forecast

Billions

of

Dollars

Source: ERFC November 2013 forecast; historical data through 2012

Economic OutlookJanuary 21, 2014

Slide 17WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Washington housing permits forecast is lower in the near term

2012 2013 2014 2015 2016 201710

15

20

25

30

35

40

45

50

Washington Housing Permits

September November

Thousa

nds

Source: U.S. Census, ERFC November 2013 forecast; historical data through 2012

Economic OutlookJanuary 21, 2014

Slide 18WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

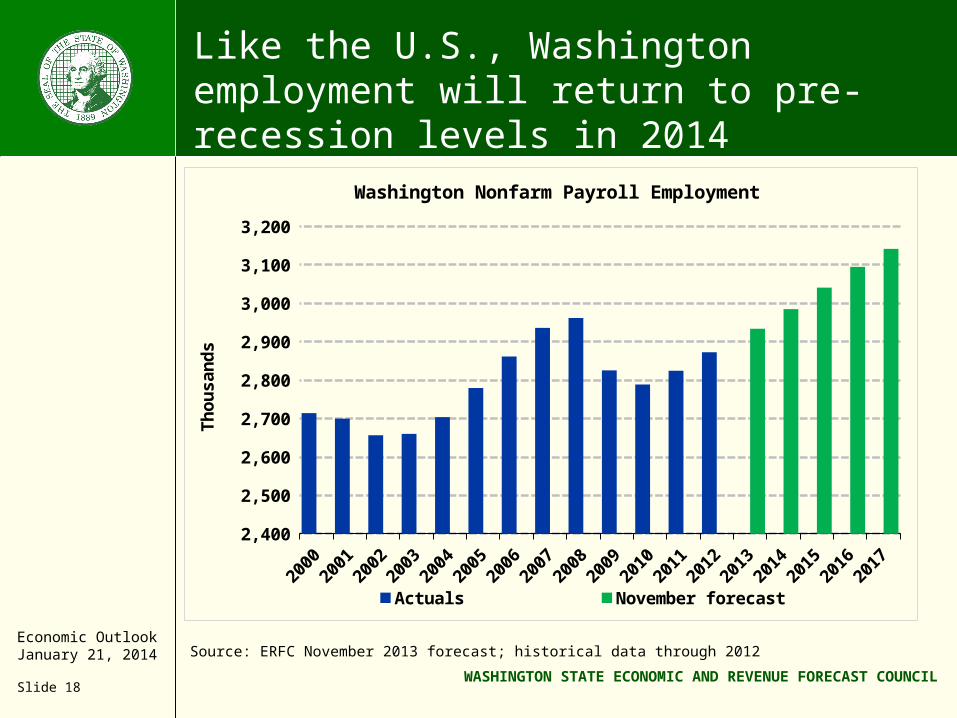

Like the U.S., Washington employment will return to pre-recession levels in 2014

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2,400

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

Washington Nonfarm Payroll Employment

Actuals November forecast

Thousa

nds

Source: ERFC November 2013 forecast; historical data through 2012

Economic OutlookJanuary 21, 2014

Slide 19WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Washington nonfarm employment is up 45,100 so far this year

Whol

e & re

tail

trad

e

Leisure

& h

ospita

lity

Const

ruct

ion

Hea

lth car

e

Emplo

ymen

t ser

vice

s

Man

uf ex

aero

spac

e

Loca

l gov

ernm

ent

Finan

cial

act

iviti

es

Prof/s

cien

tific/te

chnic

al

Softw

are

Aeros

pace

Feder

al g

over

nmen

t

All ot

her-4

-2

0

2

4

6

8

10

12

14

16

2013 YTD employment change

Thousa

nds

Source: Employment Security Dept., ERFC; data through November 2013

Economic OutlookJanuary 21, 2014

Slide 20WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Initial unemployment claims are declining

20062006200720072008200920092010201120112012201320130.5

1.0

1.5

2.0

2.5

Weekly initial claims, 4 week moving average (SA)

Washington U.S.

January

2006 =

1.0

Source: U.S. Dept of Labor/BLS; data through January 4 2014

Economic OutlookJanuary 21, 2014

Slide 21WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Washington manufacturing activity has turned up

2001 2003 2005 2007 2009 2011 201330

35

40

45

50

55

60

65

70

75

80

Institute of Supply Management Index

U.S. Washington

Source: Institute of Supply Management; data through December 2013

An index greater than 50, implies growth

Economic OutlookJanuary 21, 2014

Slide 22WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

After nearly 6 years, Washington employment has still not recovered

0123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960616263646566676869

-200

-150

-100

-50

0

50

100

150

200

250

Washington Employment after Business Cycle Peak

1990-91 2001 2007-09Months

Thousands

Source: WA ESD, ERFC; data through November 2013

Washington remains 20,000 jobs below the start of the recession

Economic OutlookJanuary 21, 2014

Slide 23WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Washington employment will recover slightly faster than the U.S.

2005

2005

2005

2005

2006

2006

2006

2006

2007

2007

2007

2007

2008

2008

2008

2008

2009

2009

2009

2009

2010

2010

2010

2010

2011

2011

2011

2011

2012

2012

2012

2012

2013

2013

2013

2013

2014

2014

2014

2014

2015

2015

2015

2015

2016

2016

2016

2016

2017

2017

2017

2017

0.94

0.96

0.98

1.00

1.02

1.04

1.06

1.08

1.10

Nonfarm Payroll Employment

Washington U.S.

Index, 2013Q

3 =

1.0

Forecast

Date of regaining peak:

WA:

2014Q2

U.S.:

2014Q3

Source: ERFC November 2013 forecast; historical data through 2013Q3

Economic OutlookJanuary 21, 2014

Slide 24WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

…and state personal income will recover slightly faster than the U.S.

2005

2005

2005

2005

2006

2006

2006

2006

2007

2007

2007

2007

2008

2008

2008

2008

2009

2009

2009

2009

2010

2010

2010

2010

2011

2011

2011

2011

2012

2012

2012

2012

2013

2013

2013

2013

2014

2014

2014

2014

2015

2015

2015

2015

2016

2016

2016

2016

2017

2017

2017

2017

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

Real Personal Income

Washington U.S.

Index, 2013Q

2 =

1.0

Forecast

Source: ERFC November 2013 forecast; historical data through 2013Q2

Economic OutlookJanuary 21, 2014

Slide 25WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Aerospace employment is declining

2012 2013 2014 2015 2016 201780

85

90

95

100

Washington Aerospace Employment

Thousa

nds

Source: ERFC November 2013 forecast; historical data through 2012

Economic OutlookJanuary 21, 2014

Slide 26WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Boeing has over 7 years of commercial orders on its books

03 04 05 06 07 08 09 10 11 12 130

400

800

1200

1600

0

1250

2500

3750

5000

Net Orders Deliveries Backlog

Ord

ers

& D

eliveri

es

Back

log

Source: Boeing, data through December 2013

Excludes the military’s new refueling tanker

Economic OutlookJanuary 21, 2014

Slide 27WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Washington construction employment is recovering

1990199019901990199119911991199119921992199219921993199319931993199419941994199419951995199519951996199619961996199719971997199719981998199819981999199919991999200020002000200020012001200120012002200220022002200320032003200320042004200420042005200520052005200620062006200620072007200720072008200820082008200920092009200920102010201020102011201120112011201220122012201220132013201320132014201420142014201520152015201520162016201620162017201720172017100

125

150

175

200

225

Washington Construction Employment

Trend, 1990-2012 Employment

Thousa

nds

Forecast

Source: ERFC November 2013 forecast; historical data through 2013Q3

Economic OutlookJanuary 21, 2014

Slide 28WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Single-family home prices continue to increase

2001 2003 2005 2007 2009 2011 2013-25

-20

-15

-10

-5

0

5

10

15

20

25

Case Shiller Home Price Index, SAYear–over-year percent Change

Seattle Composite 20

Perc

ent

Oct 2013

U.S. is up 13.6%

Seattle is up 13.1%

Source: S&P/Case-Shiller; data through October 2013

Economic OutlookJanuary 21, 2014

Slide 29WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

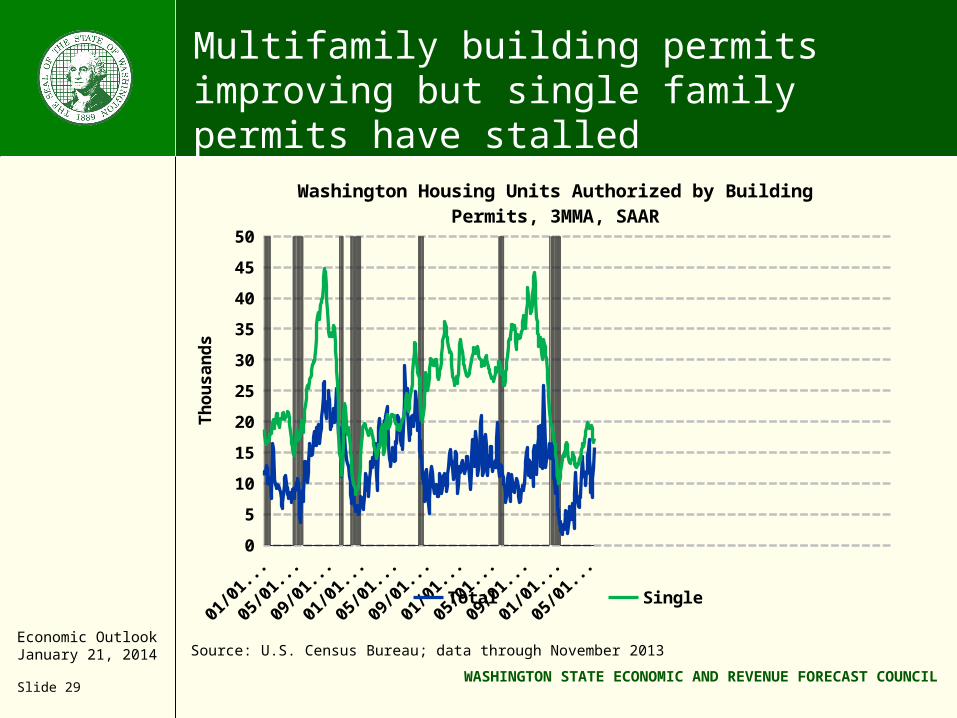

Multifamily building permits improving but single family permits have stalled

1970 1975 1980 1985 1990 1995 2000 2005 20100

5

10

15

20

25

30

35

40

45

50

Washington Housing Units Authorized by Building Permits, 3MMA, SAAR

Multiple Single

Thousa

nds

Source: U.S. Census Bureau; data through November 2013

Economic OutlookJanuary 21, 2014

Slide 30WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Nonresidential activity is trending up but remains volatile

2000 2002 2004 2006 2008 2010 20120

1

2

3

4

5

6

7

8

0

10

20

30

40

50

60

70

80

Nonresidential construction contracts, SAAR, 3MMA

value square feet

Billions

$

Millions

sq. ft

.

Source: Dodge, ERFC; data through November 2013

Economic OutlookJanuary 21, 2014

Slide 31WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Revenue collections have recovered slowly after the last recession

0 1 2 3 4 5 6 7 8 9 10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

-15

-10

-5

0

5

10

15

20

25

30

35

Revenue Act Collections after Business Cycle Peak

1990 2001 2007-09Quarters

Cum

ula

tive G

row

th (

perc

ent)

Source: ERFC; data through 2013 Q3

Revenue Act collections have now exceeded their previous peak reached in Q1 2008

Economic OutlookJanuary 21, 2014

Slide 32WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Revenue from liquor sales has been volatile since privatization

2007 2008 2009 2010 2011 2012 201314,000

16,000

18,000

20,000

22,000

24,000

26,000

Liquor Sales and Liter Taxes, SA

Collections Pre-Privitization Trend

M il li o n s o f d o ll a r s

Source: DOR, ERFC; data through December 2013

Economic OutlookJanuary 21, 2014

Slide 33WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

REET base strengthening along with spikes of large commercial sales

1996 1998 2000 2002 2004 2006 2008 2010 20120

1

2

3

4

5

6

7

8

9

10

Seasonally Adjusted Taxable Real Estate Excise Activity

$Billions

Source: ERFC; Monthly data through December 2013 preliminary

Even after last year’s rush in sales of commercial property due to federal tax changes, large commercial sales are still occurring at an above-average rate

Residential prices and sales volume grew in 2013 but have flattened in recent months

Economic OutlookJanuary 21, 2014

Slide 34WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY1710000

11000

12000

13000

14000

15000

16000

17000

18000

19000

20000$billions

Forecast

8.0% 1.2%

General Fund-State* forecast by fiscal year

(9.6%)(4.1 %)

7.9%

*General Fund-State & Related Funds for FY 07-09, General Fund-State new definition for FY 10-17Source: ERFC forecast, November 2013

1.5%

6.1%

General Fund-State Revenue

2.8%

3.2%

4.1%4.2%

Economic OutlookJanuary 21, 2014

Slide 35WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Conclusion

• We expect the slow pace of economic recovery to continue in both the U.S. and Washington economies

• Washington is still likely to outperform the nation, but by a small margin

• Washington construction activity has been strong but rising mortgage rates could slow the housing recovery

• Other threats to economic recovery include slowing Asian economies and uncertainty around federal fiscal issues

Economic OutlookJanuary 21, 2014

Slide 36WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL

Questions

Economic & Revenue Forecast Council1025 E. Union Avenue, Suite 544Olympia WA 98504-0912

www.erfc.wa.gov360-534-1560