Washington Mutual, Inc.: Maintaining Growth Amidst...

25

Taylor J. Sakamoto, Partner 909-607-2111 [email protected] Liam Patrick, Partner 909-607-75820 James Lloyd, Partner 909-607-6833 Washington Mutual, Inc.: Maintaining Growth Amidst Increasing Integration Costs

Transcript of Washington Mutual, Inc.: Maintaining Growth Amidst...

Taylor J. Sakamoto, Partner 909-607-2111 [email protected] Liam Patrick, Partner 909-607-75820 James Lloyd, Partner 909-607-6833

Washington Mutual, Inc.: Maintaining Growth Amidst Increasing Integration Costs

- Washington Mutual, Inc.-

2

Table of Contents Executive Summary 3 Company Overview Company History 4 Company Description 4 Industry Analysis The Changing State of the Banking Industry 5 The Technological Revolution 5 Consolidation of Financial Firms 5 What is Washington Mutual? A Thrift in Transition 7 Company Financial Services and Products 8 Competitive Landscape Non-Bank Competition 9 Future Threat from Non-Bank Competition 9 Key Competitive Players 10 Gaining Market Share from Industry Heavyweights 11 Geographic Presence 11 Challenging, but Anticipated, Obstacles in New Markets 12 Cross Selling Complimentary Financial Products/Services 12 Cross Selling Through Mortgage Banking Platform 13 Protecting Market Share: Barriers to Entry 13 Break Down Barriers to Entry While Maintaining Market Share 14 2002 Financial Outcome 14 Future Strategy Managing Interest Rate Risk 16 Incorporation of Acquisitions 17 Long-Term Strategy

Conclusion 18

- Washington Mutual, Inc.-

3

Executive Summary Throughout fiscal year 2002, Washington Mutual posted near record profits and further established itself as one of the most dominant players in the American mortgage market. The company found itself the beneficiary of the low interest rate environment, which acted to boost interest income beyond expectations. Additionally, an aggressive growth strategy by means of a recent acquisition spree has thus far paid off, establishing the company in numerous new markets around the nation. Going forward, Blaisdell Consulting believes that there will be two main considerations to concentrate on if Washington Mutual is to continue their strong performance of recent years:

?? Effect of uncertain fluctuations in interest rates ?? Improvement in operational efficiency as a driver for future earnings growth

Although accompanied by the uncertainty of a sluggish American and global economy, these factors should not prove to be terribly difficult to overcome. As a result, Blaisdell Consulting maintains a positive outlook on the future earnings potential of Washington Mutual. For the coming year, in order to address these considerations, we recommend that Washington Mutual focus on:

?? Managing Interest Rate Risk Asset liability management and interest rate options should be employed in order to mitigate interest rate risk that exists in the Balance Sheet, Mortgage Servicing Rights Hedges, and Mortgage Pipeline.

?? Smoothly Integrating Recent and Future Acquisitions An aggressive acquisition strategy has made it imperative that the company maintain tight internal controls over operational costs and efficiency. Full integration must be accomplished before it is advisable that the company pursue further acquisitions in the future.

?? Establishment in New Markets and Long Term Growth By eliminating fees on not only checking accounts, but also other financial products/services, the company will draw in more business flow and a larger customer base, gaining market share from its competitors. Once the company achieves nationwide status, management will be faced with the decision of whether to follow the conglomeration trend witnessed in the banking industry. Their choice will depend on how industry heavyweights manage their conglomerate structure, and if it proves profitable.

We believe that these are reasonable strategic goals for the future that will preserve the profitability that the company has managed to uphold throughout the struggles of the current U.S. market.

- Washington Mutual, Inc.-

4

Company Overview Company History Tracing its roots back to the late 19th century, Seattle -based Washington Mutual has built and maintained a reputation as one of the nation’s premier financial services firms. Originally known as the Washington National Building Loan and Investment Association (WNBLIA), the company incorporated as a result of the wide spread fire destruction witnessed in Seattle’s business district on June 6, 1889. The WNBLIA desired to help the upstart Seattle community rebuild its city. By filing articles of incorporation, the WNBLIA was able to create a safe vehicle for stockholder investing and lending. As a result, the Association was able to provide capital to finance the reconstruction of the young city. Organic growth through the years, accompanied by a series of successful acquisitions pushed the company to go public on March 11, 1983. Over the next six years, the bank would undergo rapid expansion, more than doubling in total size.i Currently, Washington Mutual has total assets of approximately $300 billion. ii Company Description Washington Mutual has operations divided into three main areas: Banking and Financial Services, Home Loans and Insurance Services, and Specialty Finance. Operations revolve around the Home Loans and Insurance Services division, the company’s flagship business line. Through this division, the company sells its mortgage banking services, attempting to develop relationships with clients that will lead to the cross-selling of additional banking and consumer financial services.iii The company is currently attempting to push its operations nationwide with an aggressive acquisition strategy. Historically, Washington Mutual has been a West Coast operation, with heavy market share in the states of Washington, Oregon, and California. However, with over 20 acquisitions within the past 13 years, the company has stretched its presence into 30 states across the continental U.S. Presently, management is making a strong push into the states of New York and New Jersey, attempting to establish an East Coast foundation upon which to expand into the Atlantic states.iv Going forward, management eventually hopes to move away from the company’s mortgage heavy operations towards a more full-service consumer bank orientation.

- Washington Mutual, Inc.-

5

Industry Analysis The Changing State of the Banking Industry The banking industry has undergone extensive changes recently. Once distinctly separated by their functions in the economy, banks and their principal competitors are undergoing a mass consolidation of the financial industry, causing economic roles to now overlap. Legislative proposals from Presidents George Bush and Bill Clinton during the 1990’s has recommended that banks with adequate capital be allowed to offer a wider range of services, affiliate with security broker/dealer firms and investment companies, and enter non financial industries on a limited basis. Continuing this trend, in November 1999, the Financial Services Modernization (Gramm-Leach-Bliley) Act was passed, allowing banks and other financial service firms to combine banking, insurance, and security operations beneath a single roof. As a result, modern banks, as well as financial service providers, are now able to create financial conglomerates that truly fulfill the concept of a one-stop-shop (Example: Citigroup). Consolidation of these once distinct financial industries has made it difficult, if not impossible, to accurately define the landscape of the industry. v Presently, the “modern bank” can be expected to conduct most of the following functions: Loan credit, transaction payments, savings accounts, investment/financial planning, real estate and community development, cash management, merchant banking, investment banking, security brokerage, and risk management. The Technological Revolution Facing higher operating costs, banks and financial service firms have increasingly turned to the use of electronic networks and automation to take over labor-intensive jobs. Such functions include, taking deposits, dispensing payments, and making credit available. This technological trend has been prominent throughout America, with ATMs and POS terminals allowing 24-hour access to deposit/checking accounts, in addition to making payments for goods at stores and shopping centers absolutely electronic in nature. Business can now move faster than it ever has before, with computer networks capable of instantly processing millions of business transactions throughout the entire world. Thus, banking is becoming more of a capital intensive, fixed cost industry and less of a labor intensive, variable cost industry.vi Some believe that the traditional branch banking system and “face to face” transactions will disappear in the near future, eventually to be supplanted by internet commerce. This trend towards full automation will continue as a means to minimize expenditures, as cost per transaction is expected to dramatically decrease with increased volumes of business flow. Consolidation of Financial Firms In order to justify investment in new technology, high volumes of business are required. Consequentially, consolidation has been a major force in the banking/financial services industry. Companies seek to expand their customer base, and increase business flow, through strategic acquisitions, expanding operations into new markets. Clearly reflective of this trend, the total

- Washington Mutual, Inc.-

6

number of small banks in America has dropped by approximately one third since 1980. vii The increasing average size of banks, as well as decreasing bank employment numbers, further testifies to the current consolidation trend. In line with industry consolidation is the growing popularity of the conglomerate corporate structure. Envisioning economies of scale and other operational synergies, banks and financial service firms have been consolidating operations beneath a single roof in an effort to further maximize efficiency. Although faced with enormous integration costs, general consensus appears to be that future benefits far outweigh current expenditures, and the conglomerate structure will eventually dominate the banking industry.

- Washington Mutual, Inc.-

7

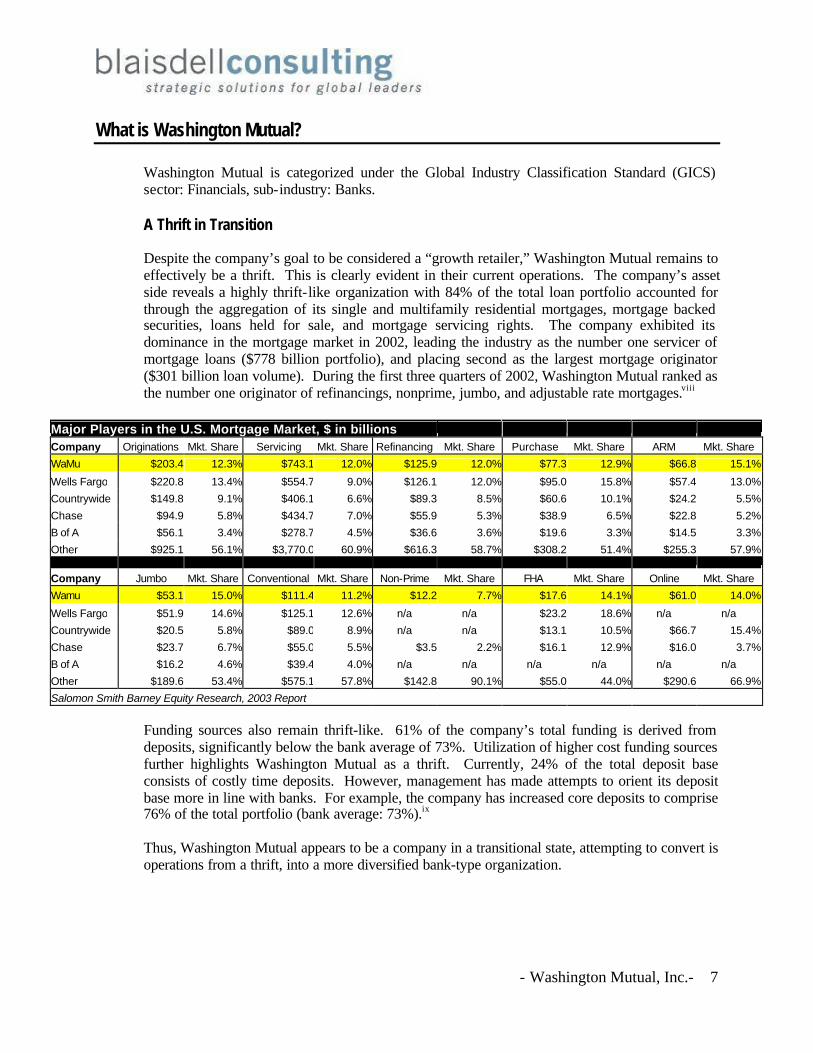

What is Washington Mutual? Washington Mutual is categorized under the Global Industry Classification Standard (GICS) sector: Financials, sub-industry: Banks. A Thrift in Transition Despite the company’s goal to be considered a “growth retailer,” Washington Mutual remains to effectively be a thrift. This is clearly evident in their current operations. The company’s asset side reveals a highly thrift-like organization with 84% of the total loan portfolio accounted for through the aggregation of its single and multifamily residential mortgages, mortgage backed securities, loans held for sale, and mortgage servicing rights. The company exhibited its dominance in the mortgage market in 2002, leading the industry as the number one servicer of mortgage loans ($778 billion portfolio), and placing second as the largest mortgage originator ($301 billion loan volume). During the first three quarters of 2002, Washington Mutual ranked as the number one originator of refinancings, nonprime, jumbo, and adjustable rate mortgages.viii

Major Players in the U.S. Mortgage Market, $ in billions Company Originations Mkt. Share Servicing Mkt. Share Refinancing Mkt. Share Purchase Mkt. Share ARM Mkt. Share

WaMu $203.4 12.3% $743.1 12.0% $125.9 12.0% $77.3 12.9% $66.8 15.1%

Wells Fargo $220.8 13.4% $554.7 9.0% $126.1 12.0% $95.0 15.8% $57.4 13.0%

Countrywide $149.8 9.1% $406.1 6.6% $89.3 8.5% $60.6 10.1% $24.2 5.5%

Chase $94.9 5.8% $434.7 7.0% $55.9 5.3% $38.9 6.5% $22.8 5.2%

B of A $56.1 3.4% $278.7 4.5% $36.6 3.6% $19.6 3.3% $14.5 3.3%

Other $925.1 56.1% $3,770.0 60.9% $616.3 58.7% $308.2 51.4% $255.3 57.9%

Company Jumbo Mkt. Share Conventional Mkt. Share Non-Prime Mkt. Share FHA Mkt. Share Online Mkt. Share

Wamu $53.1 15.0% $111.4 11.2% $12.2 7.7% $17.6 14.1% $61.0 14.0%

Wells Fargo $51.9 14.6% $125.1 12.6% n/a n/a $23.2 18.6% n/a n/a

Countrywide $20.5 5.8% $89.0 8.9% n/a n/a $13.1 10.5% $66.7 15.4%

Chase $23.7 6.7% $55.0 5.5% $3.5 2.2% $16.1 12.9% $16.0 3.7%

B of A $16.2 4.6% $39.4 4.0% n/a n/a n/a n/a n/a n/a

Other $189.6 53.4% $575.1 57.8% $142.8 90.1% $55.0 44.0% $290.6 66.9%

Salomon Smith Barney Equity Research, 2003 Report Funding sources also remain thrift-like. 61% of the company’s total funding is derived from deposits, significantly below the bank average of 73%. Utilization of higher cost funding sources further highlights Washington Mutual as a thrift. Currently, 24% of the total deposit base consists of costly time deposits. However, management has made attempts to orient its deposit base more in line with banks. For example, the company has increased core deposits to comprise 76% of the total portfolio (bank average: 73%).ix Thus, Washington Mutual appears to be a company in a transitional state, attempting to convert is operations from a thrift, into a more diversified bank-type organization.

- Washington Mutual, Inc.-

8

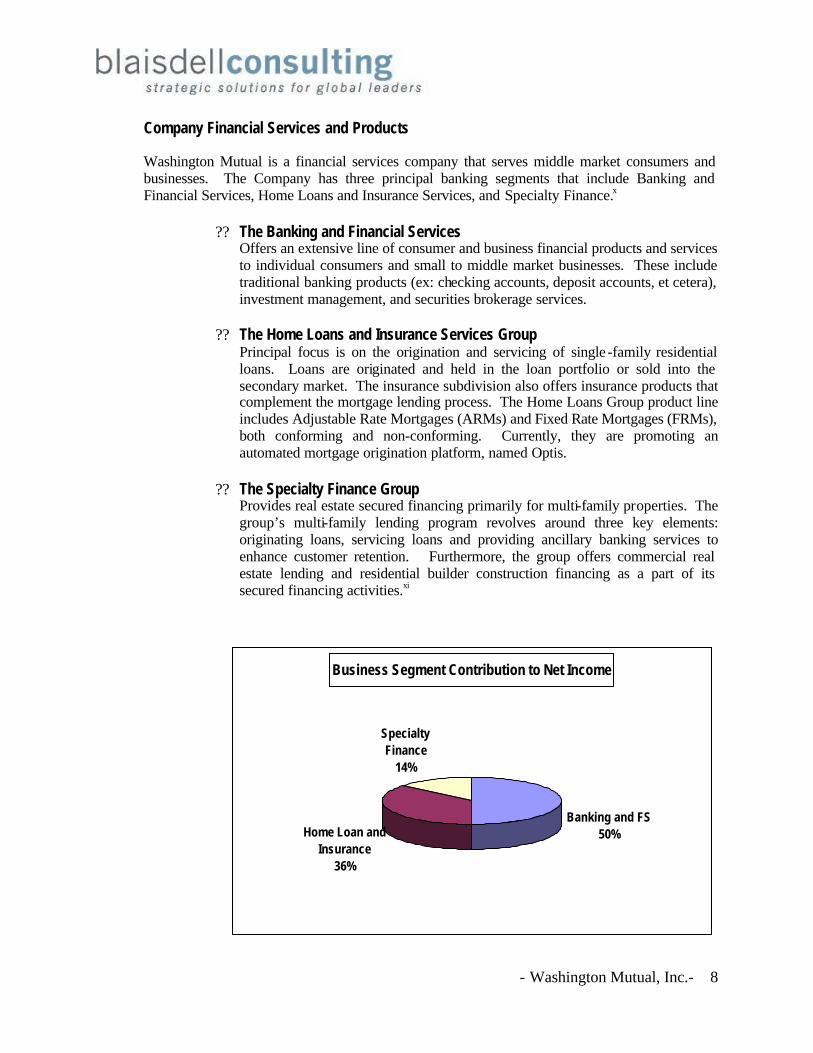

Company Financial Services and Products Washington Mutual is a financial services company that serves middle market consumers and businesses. The Company has three principal banking segments that include Banking and Financial Services, Home Loans and Insurance Services, and Specialty Finance.x

?? The Banking and Financial Services Offers an extensive line of consumer and business financial products and services to individual consumers and small to middle market businesses. These include traditional banking products (ex: checking accounts, deposit accounts, et cetera), investment management, and securities brokerage services.

?? The Home Loans and Insurance Services Group

Principal focus is on the origination and servicing of single -family residential loans. Loans are originated and held in the loan portfolio or sold into the secondary market. The insurance subdivision also offers insurance products that complement the mortgage lending process. The Home Loans Group product line includes Adjustable Rate Mortgages (ARMs) and Fixed Rate Mortgages (FRMs), both conforming and non-conforming. Currently, they are promoting an automated mortgage origination platform, named Optis.

?? The Specialty Finance Group

Provides real estate secured financing primarily for multi-family properties. The group’s multi-family lending program revolves around three key elements: originating loans, servicing loans and providing ancillary banking services to enhance customer retention. Furthermore, the group offers commercial real estate lending and residential builder construction financing as a part of its secured financing activities.xi

Business Segment Contribution to Net Income

Banking and FS50%Home Loan and

Insurance36%

Specialty Finance

14%

- Washington Mutual, Inc.-

9

Competitive Landscape The level and intensity of the competitive landscape in the financial services industry has grown significantly in recent years, as competitors push to offer a broader range of services. In order to expand services and products, banks and other financial service firms are undergoing sweeping changes. Key trends are currently restructuring the industry, pressuring firms to either fall in line or risk losing their market position to a more diversified, efficient competitor. These trends include: Non-Bank Competition Deregulation has created a sort of overlap between financial service firms, intensifying competition between sectors that were once independent. There are currently six chief non-bank competitors that are helping to promote change within the banking industry:xii

?? Insurance Companies and Pensions Plans Providing customers with long term savings plans, risk protection, and credit

?? Mutual Funds Supplying professional cash management and investing services for longer term savers

?? Real Estate Developers and Mortgage Companies Supplying building and construction expertise and construction financing to their customers

?? Check Cashing Firms, Small Loan Vendors, and Finance Companies Supplying customers with access to ready cash and short to medium term loans for everything from daily household and operating expenses to the purchase of appliances and equipment

?? Security Brokers and Dealers Providing investment and savings planning, executing security purchases and sales, and providing credit cards to their customers

?? Credit Unions and other Thrift Institutions Offering customers credit, payments and savings deposit services often fully comparable to what banks offer

Future Threat from Non-Bank Institutions With non-bank institutions attempting to service a broader range of customers’ financial needs, companies have come under pressure to develop more services for the future in order to remain competitive. These non-bank firms represent a sizable threat to the future of Washington Mutual. Their specialization in certain fields may present considerable competition in light of their probable operational efficiency in providing a particular focal product or service. As a result, Washington Mutual has reacted by attempting to expand its financial services and products, trying to orient themselves more as a bank than a thrift. By developing other areas of business and diversifying operations, the company has opened up other avenues of future revenue, protecting itself against market entry by these non-bank institutions.

- Washington Mutual, Inc.- 10

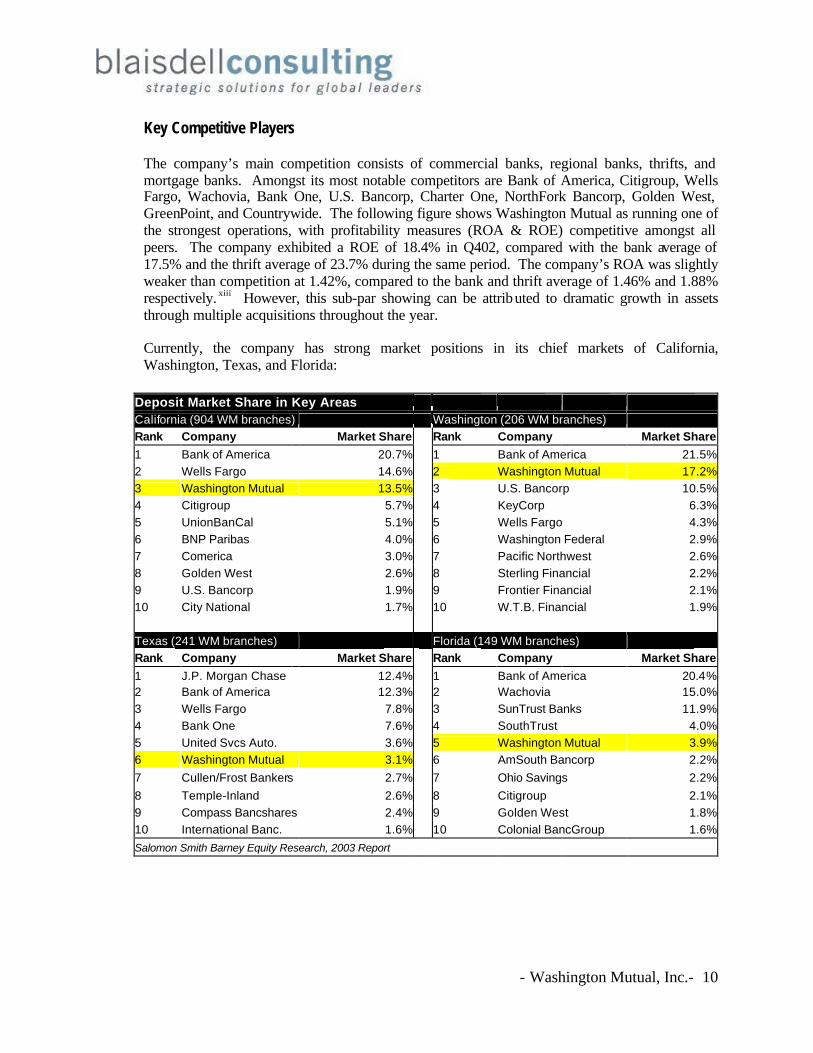

Key Competitive Players The company’s main competition consists of commercial banks, regional banks, thrifts, and mortgage banks. Amongst its most notable competitors are Bank of America, Citigroup, Wells Fargo, Wachovia, Bank One, U.S. Bancorp, Charter One, NorthFork Bancorp, Golden West, GreenPoint, and Countrywide. The following figure shows Washington Mutual as running one of the strongest operations, with profitability measures (ROA & ROE) competitive amongst all peers. The company exhibited a ROE of 18.4% in Q402, compared with the bank average of 17.5% and the thrift average of 23.7% during the same period. The company’s ROA was slightly weaker than competition at 1.42%, compared to the bank and thrift average of 1.46% and 1.88% respectively. xiii However, this sub-par showing can be attributed to dramatic growth in assets through multiple acquisitions throughout the year. Currently, the company has strong market positions in its chief markets of California, Washington, Texas, and Florida:

Deposit Market Share in Key Areas California (904 WM branches) Washington (206 WM branches) Rank Company Market Share Rank Company Market Share1 Bank of America 20.7% 1 Bank of America 21.5%2 Wells Fargo 14.6% 2 Washington Mutual 17.2%3 Washington Mutual 13.5% 3 U.S. Bancorp 10.5%4 Citigroup 5.7% 4 KeyCorp 6.3%5 UnionBanCal 5.1% 5 Wells Fargo 4.3%6 BNP Paribas 4.0% 6 Washington Federal 2.9%7 Comerica 3.0% 7 Pacific Northwest 2.6%8 Golden West 2.6% 8 Sterling Financial 2.2%9 U.S. Bancorp 1.9% 9 Frontier Financial 2.1%10 City National 1.7% 10 W.T.B. Financial 1.9% Texas (241 WM branches) Florida (149 WM branches) Rank Company Market Share Rank Company Market Share1 J.P. Morgan Chase 12.4% 1 Bank of America 20.4%2 Bank of America 12.3% 2 Wachovia 15.0%3 Wells Fargo 7.8% 3 SunTrust Banks 11.9%4 Bank One 7.6% 4 SouthTrust 4.0%5 United Svcs Auto. 3.6% 5 Washington Mutual 3.9%6 Washington Mutual 3.1% 6 AmSouth Bancorp 2.2%7 Cullen/Frost Bankers 2.7% 7 Ohio Savings 2.2%8 Temple-Inland 2.6% 8 Citigroup 2.1%9 Compass Bancshares 2.4% 9 Golden West 1.8%10 International Banc. 1.6% 10 Colonial BancGroup 1.6%Salomon Smith Barney Equity Research, 2003 Report

- Washington Mutual, Inc.- 11

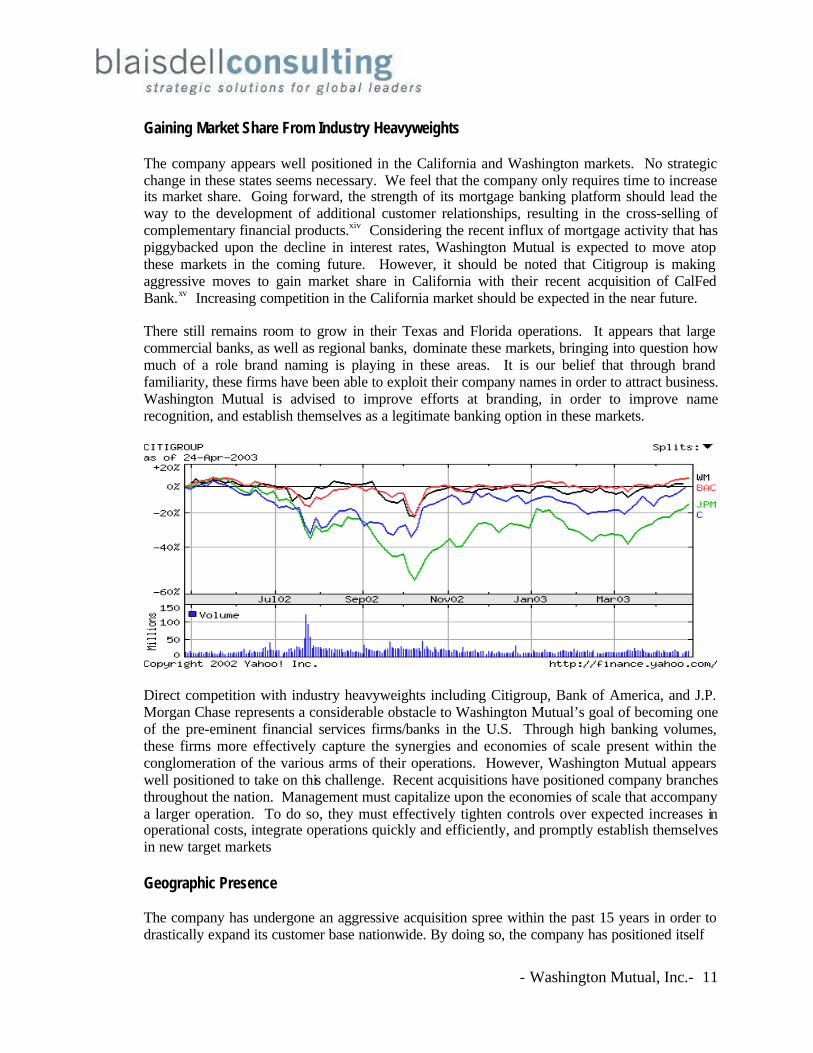

Gaining Market Share From Industry Heavyweights The company appears well positioned in the California and Washington markets. No strategic change in these states seems necessary. We feel that the company only requires time to increase its market share. Going forward, the strength of its mortgage banking platform should lead the way to the development of additional customer relationships, resulting in the cross-selling of complementary financial products.xiv Considering the recent influx of mortgage activity that has piggybacked upon the decline in interest rates, Washington Mutual is expected to move atop these markets in the coming future. However, it should be noted that Citigroup is making aggressive moves to gain market share in California with their recent acquisition of CalFed Bank.xv Increasing competition in the California market should be expected in the near future. There still remains room to grow in their Texas and Florida operations. It appears that large commercial banks, as well as regional banks, dominate these markets, bringing into question how much of a role brand naming is playing in these areas. It is our belief that through brand familiarity, these firms have been able to exploit their company names in order to attract business. Washington Mutual is advised to improve efforts at branding, in order to improve name recognition, and establish themselves as a legitimate banking option in these markets.

Direct competition with industry heavyweights including Citigroup, Bank of America, and J.P. Morgan Chase represents a considerable obstacle to Washington Mutual’s goal of becoming one of the pre-eminent financial services firms/banks in the U.S. Through high banking volumes, these firms more effectively capture the synergies and economies of scale present within the conglomeration of the various arms of their operations. However, Washington Mutual appears well positioned to take on this challenge. Recent acquisitions have positioned company branches throughout the nation. Management must capitalize upon the economies of scale that accompany a larger operation. To do so, they must effectively tighten controls over expected increases in operational costs, integrate operations quickly and efficiently, and promptly establish themselves in new target markets Geographic Presence The company has undergone an aggressive acquisition spree within the past 15 years in order to drastically expand its customer base nationwide. By doing so, the company has positioned itself

- Washington Mutual, Inc.- 12

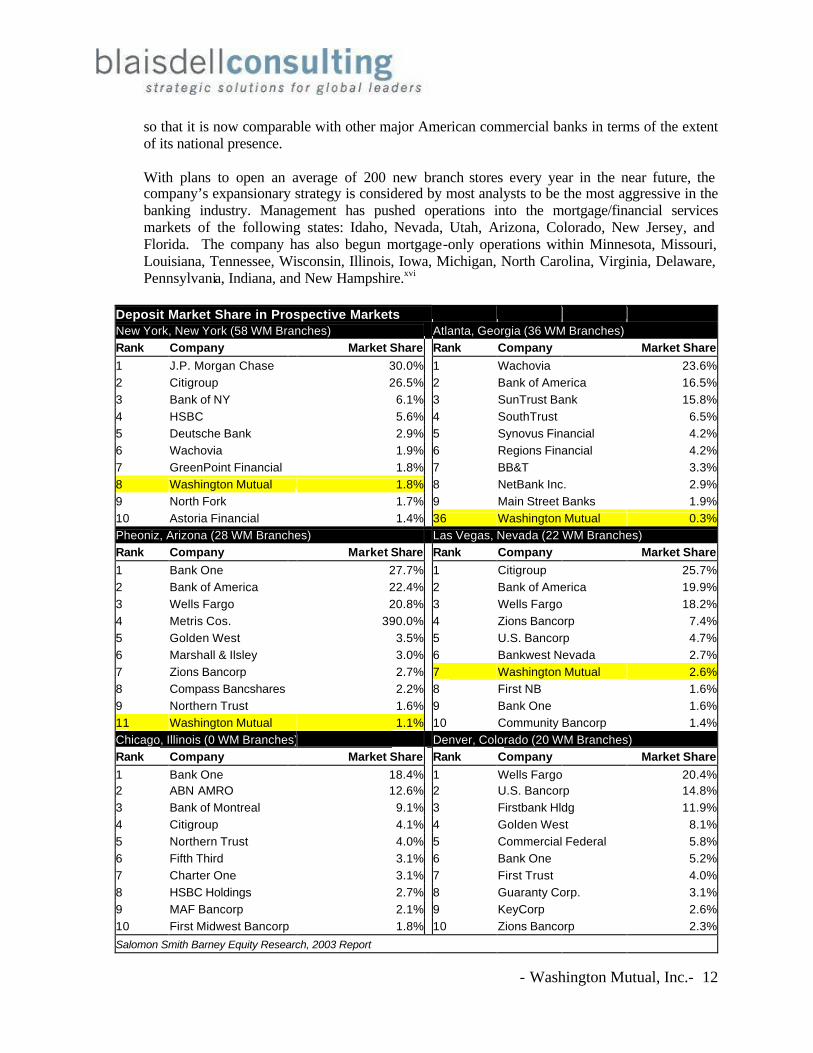

so that it is now comparable with other major American commercial banks in terms of the extent of its national presence. With plans to open an average of 200 new branch stores every year in the near future, the company’s expansionary strategy is considered by most analysts to be the most aggressive in the banking industry. Management has pushed operations into the mortgage/financial services markets of the following states: Idaho, Nevada, Utah, Arizona, Colorado, New Jersey, and Florida. The company has also begun mortgage-only operations within Minnesota, Missouri, Louisiana, Tennessee, Wisconsin, Illinois, Iowa, Michigan, North Carolina, Virginia, Delaware, Pennsylvania, Indiana, and New Hampshire.xvi

Deposit Market Share in Prospective Markets New York, New York (58 WM Branches) Atlanta, Georgia (36 WM Branches) Rank Company Market Share Rank Company Market Share1 J.P. Morgan Chase 30.0% 1 Wachovia 23.6%2 Citigroup 26.5% 2 Bank of America 16.5%3 Bank of NY 6.1% 3 SunTrust Bank 15.8%4 HSBC 5.6% 4 SouthTrust 6.5%5 Deutsche Bank 2.9% 5 Synovus Financial 4.2%6 Wachovia 1.9% 6 Regions Financial 4.2%7 GreenPoint Financial 1.8% 7 BB&T 3.3%8 Washington Mutual 1.8% 8 NetBank Inc. 2.9%9 North Fork 1.7% 9 Main Street Banks 1.9%10 Astoria Financial 1.4% 36 Washington Mutual 0.3%Pheoniz, Arizona (28 WM Branches) Las Vegas, Nevada (22 WM Branches) Rank Company Market Share Rank Company Market Share1 Bank One 27.7% 1 Citigroup 25.7%2 Bank of America 22.4% 2 Bank of America 19.9%3 Wells Fargo 20.8% 3 Wells Fargo 18.2%4 Metris Cos. 390.0% 4 Zions Bancorp 7.4%5 Golden West 3.5% 5 U.S. Bancorp 4.7%6 Marshall & Ilsley 3.0% 6 Bankwest Nevada 2.7%7 Zions Bancorp 2.7% 7 Washington Mutual 2.6%8 Compass Bancshares 2.2% 8 First NB 1.6%9 Northern Trust 1.6% 9 Bank One 1.6%11 Washington Mutual 1.1% 10 Community Bancorp 1.4%Chicago, Illinois (0 WM Branches) Denver, Colorado (20 WM Branches) Rank Company Market Share Rank Company Market Share1 Bank One 18.4% 1 Wells Fargo 20.4%2 ABN AMRO 12.6% 2 U.S. Bancorp 14.8%3 Bank of Montreal 9.1% 3 Firstbank Hldg 11.9%4 Citigroup 4.1% 4 Golden West 8.1%5 Northern Trust 4.0% 5 Commercial Federal 5.8%6 Fifth Third 3.1% 6 Bank One 5.2%7 Charter One 3.1% 7 First Trust 4.0%8 HSBC Holdings 2.7% 8 Guaranty Corp. 3.1%9 MAF Bancorp 2.1% 9 KeyCorp 2.6%10 First Midwest Bancorp 1.8% 10 Zions Bancorp 2.3%Salomon Smith Barney Equity Research, 2003 Report

- Washington Mutual, Inc.- 13

The firm plans to focus on gaining market share in six new cities: New York City, Atlanta, Phoenix, Las Vegas, Chicago, and Denver.xvii Challenging, but Anticipated, Obstacles in New Markets The company will confront typical obstacles in its entry into these new markets. We expect costs associated with its aggressive acquisition spree to rise considerably. The company will meet considerable headwind from attempts at brand naming, and competition from major players already established in the market. If management is able to successfully control costs and improve the operational efficiency of an expanded operations base, then we believe Washington Mutual is well positioned for success in the future. Cross Selling Complimentary Financial Products/Services The cross-selling of complimentary financial products and services is one of the most important keys to successful commercial banking. Banking strategy asserts that initial customer relationships are established through basic banking services and products such as checking and deposit accounts. By first attracting customers with these products, management can then attempt to deepen the relationship by “cross-selling” other of the bank’s services and products, such as mortgage loans, insurance, or credit cards. These complimentary products are highly attractive due to the strong profitability margins that they offer. Ultimately, management would like to have the average customer subscribing to 3-5 of the banks products/services in an effort to maximize business with its current customer base. With mortgage loans, companies are able to enter the market for loan servicing whereby they can either choose to service the loan, or sell it on the secondary market. Sale of loans is beneficial for five key reasons:xviii

1. Opportunity to eliminate lower-yielding loans and replace them with higher yielding assets to obtain better returns when interest rates rise.

2. Replacement of sold loans with more marketable assets increases liquidity, supporting a bank’s cash needs.

3. Removal of credit and interest rate risk from the balance sheet. 4. Faster generation of income by not having to wait for accrual of interest payments. 5. Reduction in assets allowing for a more controlled growth strategy.

Insurance is also viewed as a highly complimentary good for mortgage loans. Homeowners insurance, as well as other typical types of insurance (ie: automobile, life, and health insurance), go hand in hand with the origination of mortgage loans. All represent products the first time homebuyer tends to require, whether it be to look after his own personal welfare, or that of his family. By combining this service with that of mortgage banking, the bank is able to potentially deepen customer relationships through additional cross-selling, capturing higher profits. Cross-Selling Through Mortgage Banking Platform Washington Mutual attempts to cross-sell their products/services through the strength of their mortgage banking platform. The company’s dominance in the mortgage market clearly represents their strongest method of acquiring a broader customer base. In this way, management

- Washington Mutual, Inc.- 14

is following the typical banking strategy in the opposite direction (cross-selling deposit and checking accounts) in an effort to move the firm away from a thrift-like orientation to that of a commercial bank. However, the company also works the strategy in the traditional manner, by attracting customers through its widely successful no-fee checking services. This product is highly popular with the young adult demographic, who at low-income levels, are often times incapable of maintaining a minimum balance. This strategy is a key to the future of Washington Mutual. Since checking and savings accounts are relationship based in nature, they strengthen the likelihood of maintaining business relationships well into the future by capturing customers early on. The bank is currently involved in the insurance business, which is paying dividends as a result of the high activity in the home mortgage market in recent years. Additionally, sale of loans will prove to be an important tool for management, in the case of rising interest rates in the future. Protecting Market Share: Barriers to Entry There are significant barriers to entry for banks and thrifts. Significant capitalization, financing, and federal government accreditation are among many of the requirements necessary to establish a bank or thrift. Additionally, costly physical asset investment and SG&A expenditures would require large amounts of funding in order to begin a company in an already well-defined market. Consequentially, it would be tremendously difficult for a bank start-up to enter any of the financial services/banking markets across the nation. Already established firms may also face considerable barriers to entry into specific financial markets such as mortgage lending, consumer finance, or credit cards. Companies with established footholds in these markets are difficult to displace due to the brand loyalty they have already developed with their customer base. There is also a certain degree of efficiency that is obtained only through the concept of “learning by doing.” In such a case, firms with a history in the market will have an inherent first movers advantage over potential entrants. Furthermore, consolidation has been extensive amongst banks and thrifts. This trend towards consolidation and creation of an all encompassing financial services firm has resulted in the concentration of financial markets in control of a handful of companies.xix Continued consolidation of these markets will further strengthen market position of these firms, acting to heighten any already existent barriers to entry into these markets. Break Down Barriers to Entry While Maintaining Market Share These barriers to entry will work both in favor, and against, Washington Mutual in the coming future. Attempting to disassociate with their current label as a thrift, the company will attempt to gain market position in areas more associated with commercial banks, such as deposit and checking accounts. However, major commercial banks already possess a strong grip on these markets, and are expected to be aggressive in protecting their current position. Washington Mutual’s dominance in the mortgage market makes it highly unlikely that other firms will be able to take a significant share of this market away from them. Ultimately, the company must overcome barriers to entry into commercial banking businesses in order to become the bank

- Washington Mutual, Inc.- 15

that it aspires to be. Concurrently, however, management must also maintain high barriers of entry in the company’s dominated markets in order to protect profitability in these areas.xx

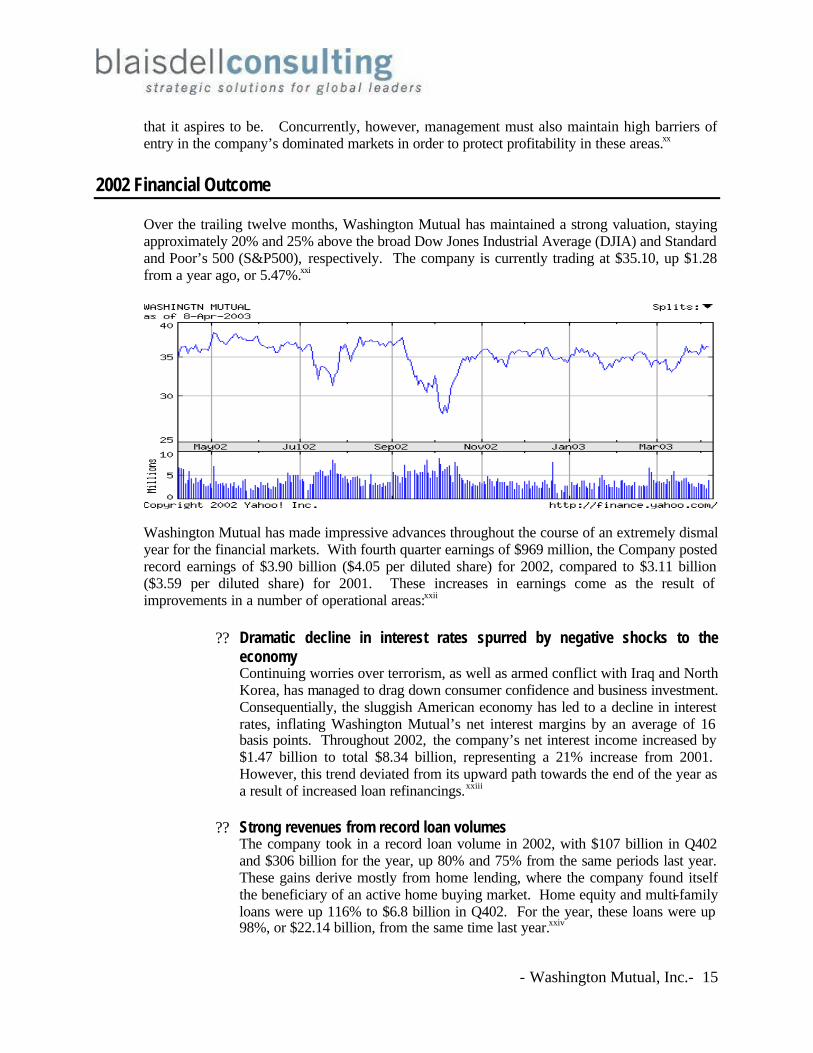

2002 Financial Outcome Over the trailing twelve months, Washington Mutual has maintained a strong valuation, staying approximately 20% and 25% above the broad Dow Jones Industrial Average (DJIA) and Standard and Poor’s 500 (S&P500), respectively. The company is currently trading at $35.10, up $1.28 from a year ago, or 5.47%.xxi

Washington Mutual has made impressive advances throughout the course of an extremely dismal year for the financial markets. With fourth quarter earnings of $969 million, the Company posted record earnings of $3.90 billion ($4.05 per diluted share) for 2002, compared to $3.11 billion ($3.59 per diluted share) for 2001. These increases in earnings come as the result of improvements in a number of operational areas:xxii

?? Dramatic decline in interest rates spurred by negative shocks to the economy Continuing worries over terrorism, as well as armed conflict with Iraq and North Korea, has managed to drag down consumer confidence and business investment. Consequentially, the sluggish American economy has led to a decline in interest rates, inflating Washington Mutual’s net interest margins by an average of 16 basis points. Throughout 2002, the company’s net interest income increased by $1.47 billion to total $8.34 billion, representing a 21% increase from 2001. However, this trend deviated from its upward path towards the end of the year as a result of increased loan refinancings.xxiii

?? Strong revenues from record loan volumes

The company took in a record loan volume in 2002, with $107 billion in Q402 and $306 billion for the year, up 80% and 75% from the same periods last year. These gains derive mostly from home lending, where the company found itself the beneficiary of an active home buying market. Home equity and multi-family loans were up 116% to $6.8 billion in Q402. For the year, these loans were up 98%, or $22.14 billion, from the same time last year.xxiv

- Washington Mutual, Inc.- 16

?? Growth in core deposits The company successfully grew core deposits, with much of the growth coming as a result of expanded customer bases attributable to recent acquisitions.xxv An enlarged deposit base led to the record level of depositor and retail banking fees of $449 million for Q402, up 27% from $353 million from the same time last year. Through all of 2002, depositor and retail banking fees totaled a robust $1.63 billion. xxvi

- Washington Mutual, Inc.- 17

Future Strategy Washington Mutual’s strong performance throughout fiscal year 2002 caps what was a record year in terms of profitability for the firm. Unexpectedly, the company found itself the beneficiary of a number of uncertainties in the marketplace, including American military involvement in the Middle East, as well as lingering worries over terrorism. The drop in rates acted to expand Washington Mutual’s net interest margins which, accompanied by a blossoming home mortgage market (both new and refinanced), acted to boost interest revenue to record levels.xxvii Managing Interest Rate Risk The 2003 outcome may prove to be drastically different from the success witnessed over the course of the past year. With the end of the war with Iraq in sight, as well as reduced fears of terrorism, the American economy seems poised for rebound. As a result, market conditions are anticipated to improve, spurring expectations that the Federal Reserve will increase interest rates.xxviii This will be detrimental to Washington Mutual’s net interest margin. The company’s portfolio mix consists of assets that have a higher duration than its liabilities, creating a “duration gap.” Thus, as rising rates cause company’s liabilities to reprice faster than its assets, the company will experience a compression of its NIM and decline in interest income. Management has already warned of pinched interest margins of 3.00% - 3.25%, down from their peak of 3.79% following the 475 bps cut in rates in 2001. As a result, we predict a significant decline in asset yields as adjustable rate mortgages reprice downwards.xxix On the funding side, interest rates are already at extremely low levels, leaving little room for rate adjustment on key funding sources such as core deposits. This reduces the flexibility of management to expand the NIM, further increasing the likelihood of lower future interest income. As a result of our predictions of future market movements, we advise management to take heavy measures to hedge against rises in interest rates that may result from a market rebound. Management should focus on interest rate risk residing in three areas: (1) Balance Sheet, (2) Mortgage Servicing Rights Hedges and (3) Mortgage Pipeline Fallout.xxx

?? Asset-Liability Management In order to mitigate interest rate risk in the balance sheet, management must maintain tight control over the company’s sensitivity to changes in market interest rates to limit losses in its bottom line net income. It can do so through interest sensitive gap management. This idea essentially concentrates on control over the difference between the volume of a bank’s interest sensitive assets and the volume of its interest sensitive liabilities.xxxi In order to mitigate interest rate risk, the company must reposition its loan and deposit portfolios so that the duration of interest sensitive liabilities and assets proportionately match each other. In so doing, assets will reprice to cover liabilities in a fluctuating interest rate environment.

One method by which Washington Mutual can accomplish this is through the greater employment of time deposits.xxxii Although a costly funding source relative to core deposits, time deposits are advantageous during uncertain interest rate environments due to their definite maturity period and locked in rate. As a

- Washington Mutual, Inc.- 18

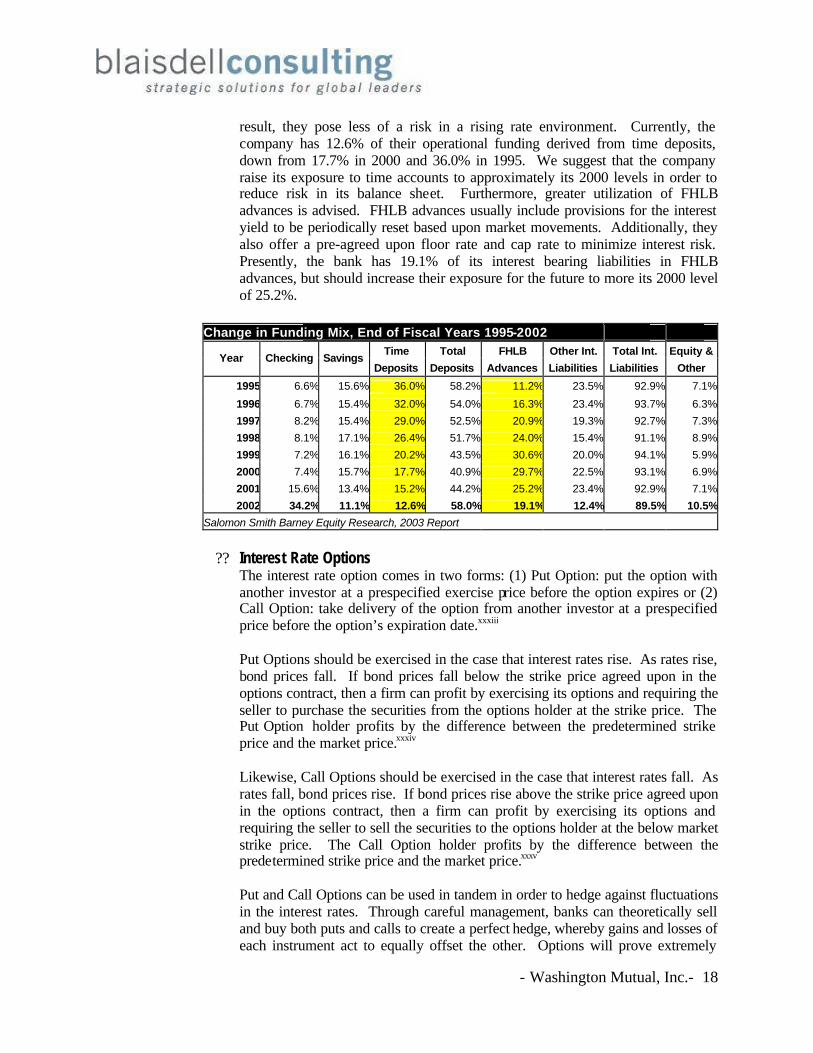

result, they pose less of a risk in a rising rate environment. Currently, the company has 12.6% of their operational funding derived from time deposits, down from 17.7% in 2000 and 36.0% in 1995. We suggest that the company raise its exposure to time accounts to approximately its 2000 levels in order to reduce risk in its balance sheet. Furthermore, greater utilization of FHLB advances is advised. FHLB advances usually include provisions for the interest yield to be periodically reset based upon market movements. Additionally, they also offer a pre-agreed upon floor rate and cap rate to minimize interest risk. Presently, the bank has 19.1% of its interest bearing liabilities in FHLB advances, but should increase their exposure for the future to more its 2000 level of 25.2%.

Change in Funding Mix, End of Fiscal Years 1995-2002

Time Total FHLB Other Int. Total Int. Equity & Year Checking Savings

Deposits Deposits Advances Liabilities Liabilities Other

1995 6.6% 15.6% 36.0% 58.2% 11.2% 23.5% 92.9% 7.1%

1996 6.7% 15.4% 32.0% 54.0% 16.3% 23.4% 93.7% 6.3%

1997 8.2% 15.4% 29.0% 52.5% 20.9% 19.3% 92.7% 7.3%

1998 8.1% 17.1% 26.4% 51.7% 24.0% 15.4% 91.1% 8.9%

1999 7.2% 16.1% 20.2% 43.5% 30.6% 20.0% 94.1% 5.9%

2000 7.4% 15.7% 17.7% 40.9% 29.7% 22.5% 93.1% 6.9%

2001 15.6% 13.4% 15.2% 44.2% 25.2% 23.4% 92.9% 7.1%

2002 34.2% 11.1% 12.6% 58.0% 19.1% 12.4% 89.5% 10.5%

Salomon Smith Barney Equity Research, 2003 Report

?? Interest Rate Options The interest rate option comes in two forms: (1) Put Option: put the option with another investor at a prespecified exercise price before the option expires or (2) Call Option: take delivery of the option from another investor at a prespecified price before the option’s expiration date.xxxiii Put Options should be exercised in the case that interest rates rise. As rates rise, bond prices fall. If bond prices fall below the strike price agreed upon in the options contract, then a firm can profit by exercising its options and requiring the seller to purchase the securities from the options holder at the strike price. The Put Option holder profits by the difference between the predetermined strike price and the market price.xxxiv Likewise, Call Options should be exercised in the case that interest rates fall. As rates fall, bond prices rise. If bond prices rise above the strike price agreed upon in the options contract, then a firm can profit by exercising its options and requiring the seller to sell the securities to the options holder at the below market strike price. The Call Option holder profits by the difference between the predetermined strike price and the market price.xxxv Put and Call Options can be used in tandem in order to hedge against fluctuations in the interest rates. Through careful management, banks can theoretically sell and buy both puts and calls to create a perfect hedge, whereby gains and losses of each instrument act to equally offset the other. Options will prove extremely

- Washington Mutual, Inc.- 19

valuable to Washington Mutual if interest rates rise as expected in the future. With the rise in interest rates and accompanying reduction in interest income, profit from Put Options can minimize the company’s losses in its interest sensitive liabilities portfolio. Such a hedge would prove to be invaluable during a variable interest rate environment.xxxvi Options are the ideal instrument to hedge against the company’s interest rate risk in its MSR hedges, as well as its mortgage pipeline. The MSR portfolio is currently hedged by the heavy use of derivatives and swaps.xxxvii Options should be utilized in order to balance out potential gains or losses in these instruments, incurred as a result of interest rate movements. Additionally, as rates rise, the home-buying market can be expected to dry up, and the company may face severe fallout in its mortgage pipeline. Consequentially, profits will be squeezed as a result of the compression of interest margins and decreased volume of loan origination/refinancing. The purchase of put options would be ideal in this situation, providing some profitability gains to compensate declines in interest income.

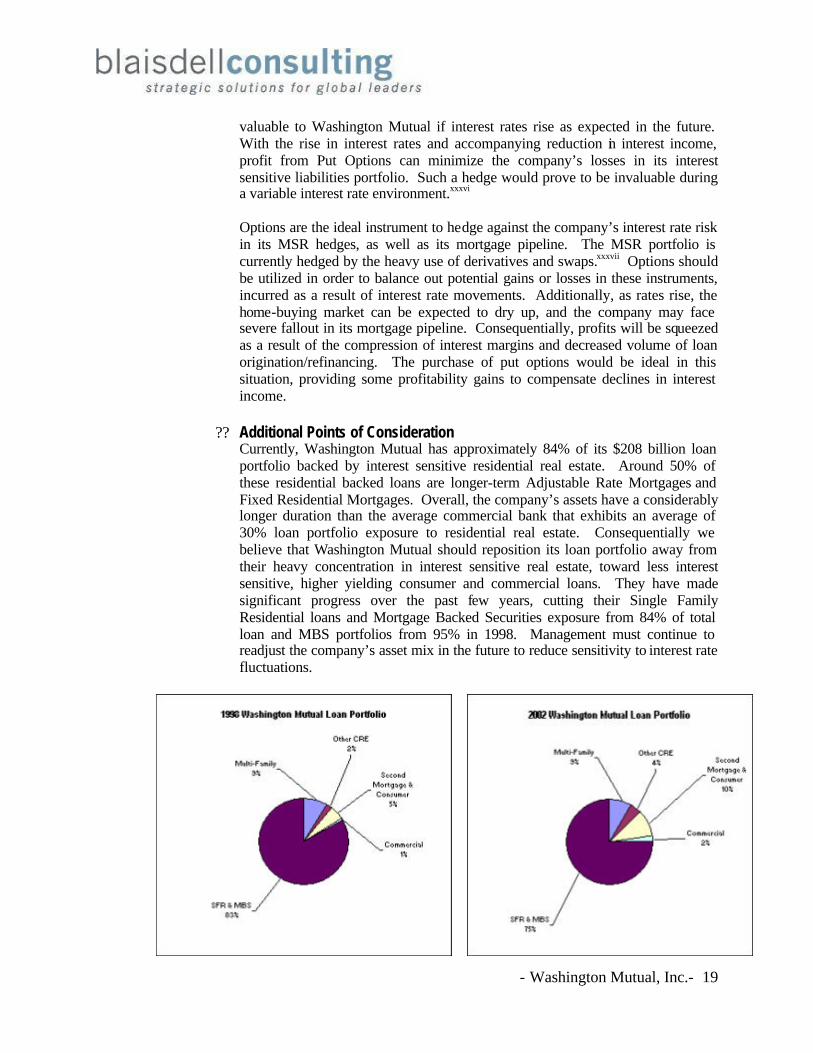

?? Additional Points of Consideration Currently, Washington Mutual has approximately 84% of its $208 billion loan portfolio backed by interest sensitive residential real estate. Around 50% of these residential backed loans are longer-term Adjustable Rate Mortgages and Fixed Residential Mortgages. Overall, the company’s assets have a considerably longer duration than the average commercial bank that exhibits an average of 30% loan portfolio exposure to residential real estate. Consequentially we believe that Washington Mutual should reposition its loan portfolio away from their heavy concentration in interest sensitive real estate, toward less interest sensitive, higher yielding consumer and commercial loans. They have made significant progress over the past few years, cutting their Single Family Residential loans and Mortgage Backed Securities exposure from 84% of total loan and MBS portfolios from 95% in 1998. Management must continue to readjust the company’s asset mix in the future to reduce sensitivity to interest rate fluctuations.

- Washington Mutual, Inc.- 20

Going forward, Blaisdell Consulting also advises management to focus on non-interest income. Emphasis on fee-based income will be a key to keeping operational revenues from declining to unfavorable levels as interest income declines due to compression of the NIM. Washington Mutual has so far been successful in this avenue, growing its deposit base by an annualized rate of over 13% since 1998. Consequentially, depositor and retail banking fees have increased at an annualized rate of 30%. Total fee income has risen to 44%, up from 27%. The company has also managed to squeeze significant levels of fee income from its securities and insurance operations, with analysts anticipating approximately $550 million throughout the course of the coming year.

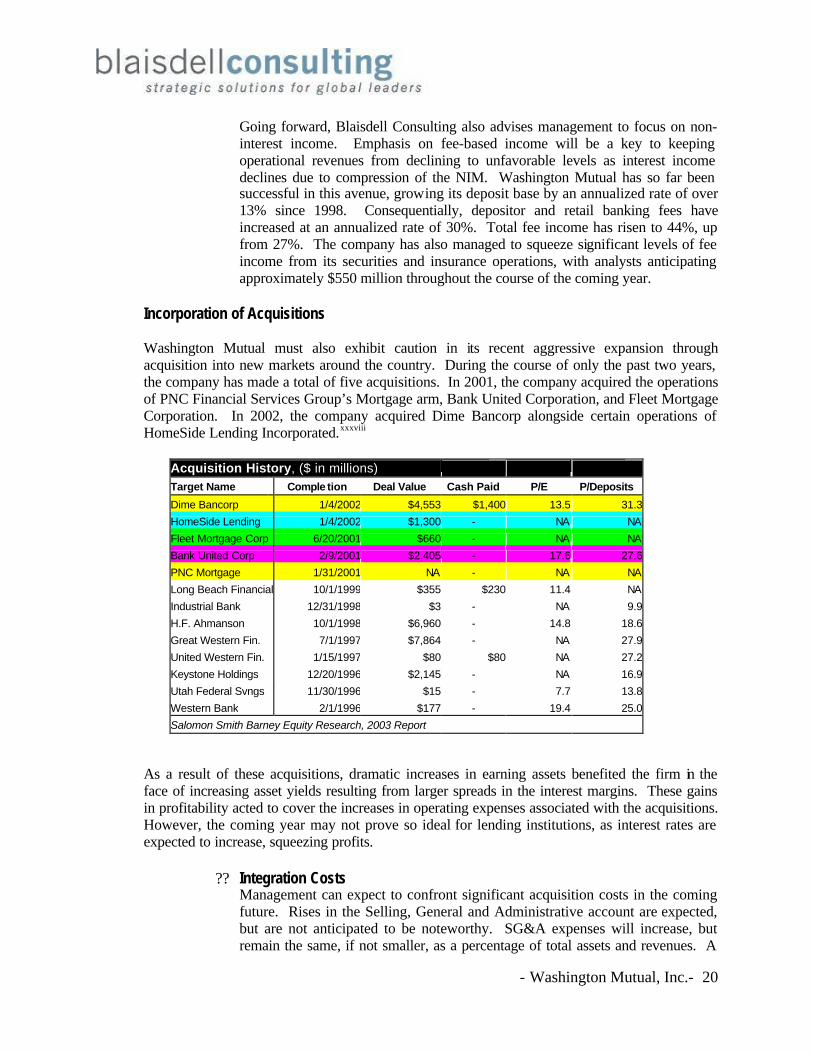

Incorporation of Acquisitions Washington Mutual must also exhibit caution in its recent aggressive expansion through acquisition into new markets around the country. During the course of only the past two years, the company has made a total of five acquisitions. In 2001, the company acquired the operations of PNC Financial Services Group’s Mortgage arm, Bank United Corporation, and Fleet Mortgage Corporation. In 2002, the company acquired Dime Bancorp alongside certain operations of HomeSide Lending Incorporated.xxxviii

Acquisition History, ($ in millions) Target Name Comple tion Deal Value Cash Paid P/E P/Deposits

Dime Bancorp 1/4/2002 $4,553 $1,400 13.5 31.3

HomeSide Lending 1/4/2002 $1,300 - NA NA

Fleet Mortgage Corp 6/20/2001 $660 - NA NA

Bank United Corp 2/9/2001 $2,405 - 17.6 27.6

PNC Mortgage 1/31/2001 NA - NA NA

Long Beach Financial 10/1/1999 $355 $230 11.4 NA

Industrial Bank 12/31/1998 $3 - NA 9.9

H.F. Ahmanson 10/1/1998 $6,960 - 14.8 18.6

Great Western Fin. 7/1/1997 $7,864 - NA 27.9

United Western Fin. 1/15/1997 $80 $80 NA 27.2

Keystone Holdings 12/20/1996 $2,145 - NA 16.9

Utah Federal Svngs 11/30/1996 $15 - 7.7 13.8

Western Bank 2/1/1996 $177 - 19.4 25.0

Salomon Smith Barney Equity Research, 2003 Report As a result of these acquisitions, dramatic increases in earning assets benefited the firm in the face of increasing asset yields resulting from larger spreads in the interest margins. These gains in profitability acted to cover the increases in operating expenses associated with the acquisitions. However, the coming year may not prove so ideal for lending institutions, as interest rates are expected to increase, squeezing profits.

?? Integration Costs Management can expect to confront significant acquisition costs in the coming future. Rises in the Selling, General and Administrative account are expected, but are not anticipated to be noteworthy. SG&A expenses will increase, but remain the same, if not smaller, as a percentage of total assets and revenues. A

- Washington Mutual, Inc.- 21

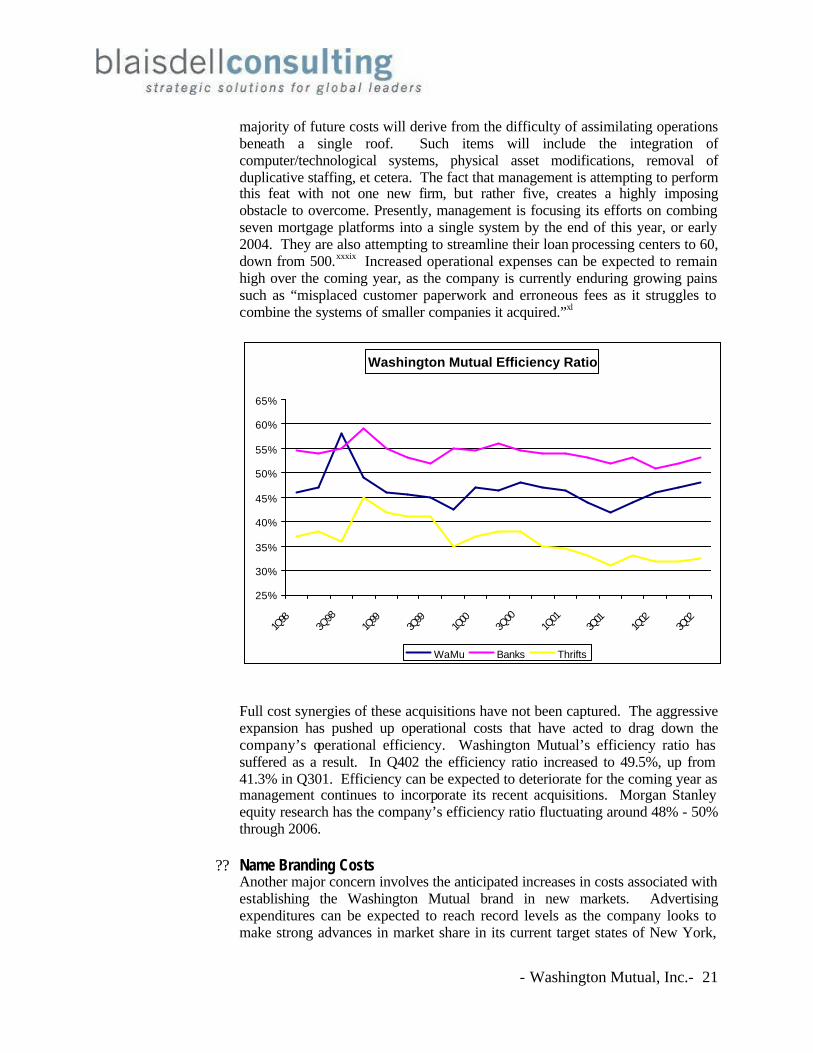

majority of future costs will derive from the difficulty of assimilating operations beneath a single roof. Such items will include the integration of computer/technological systems, physical asset modifications, removal of duplicative staffing, et cetera. The fact that management is attempting to perform this feat with not one new firm, but rather five, creates a highly imposing obstacle to overcome. Presently, management is focusing its efforts on combing seven mortgage platforms into a single system by the end of this year, or early 2004. They are also attempting to streamline their loan processing centers to 60, down from 500.xxxix Increased operational expenses can be expected to remain high over the coming year, as the company is currently enduring growing pains such as “misplaced customer paperwork and erroneous fees as it struggles to combine the systems of smaller companies it acquired.”xl

Washington Mutual Efficiency Ratio

25%

30%

35%

40%

45%

50%

55%

60%

65%

1Q98

3Q98

1Q99

3Q99

1Q00

3Q00

1Q01

3Q01

1Q02

3Q02

WaMu Banks Thrifts

Full cost synergies of these acquisitions have not been captured. The aggressive expansion has pushed up operational costs that have acted to drag down the company’s operational efficiency. Washington Mutual’s efficiency ratio has suffered as a result. In Q402 the efficiency ratio increased to 49.5%, up from 41.3% in Q301. Efficiency can be expected to deteriorate for the coming year as management continues to incorporate its recent acquisitions. Morgan Stanley equity research has the company’s efficiency ratio fluctuating around 48% - 50% through 2006.

?? Name Branding Costs

Another major concern involves the anticipated increases in costs associated with establishing the Washington Mutual brand in new markets. Advertising expenditures can be expected to reach record levels as the company looks to make strong advances in market share in its current target states of New York,

- Washington Mutual, Inc.- 22

Nevada, Illinois, Georgia, Arizona, and Colorado. These branding expenditures can be expected to be a drag on profits in the near term, further increasing total costs related to acquisitions. Thus far, branding has not been a problematic issue for the company. Management has a proven track record in this area, reflected by their success in establishing the Washington Mutual name in new markets across the nation. However, the company must be careful over the next couple of years, maintaining tight controls over increasing costs in the presence of shrinking profits.xli

?? Slow Down Acquisition Activity

These increases in costs might be detrimental if the economy were to improve, consequentially causing a rise in interest rates. Compression of the net interest margin, along with decreased volume of mortgage activity, will slow profitability growth. Management may face a difficult time handling this pinch of their bottom line. Blaisdell Consulting believes the company has been overly aggressive in its operational expansion. Going forward, we would like to see management first get a good grasp over its recent acquisitions before pursuing other M&A opportunities. We feel that with time, the company’s efficiency will improve, as it fully captures cost synergies with its recent acquisitions. However, additional M&A activity in the present time will only further drain the company of cash, and continue to push up costs. This must be avoided if the company is to maintain its financial health amidst a difficult market and shrinking profits.

Long-Term Strategy

In planning for the long-term, Washington Mutual will have to endure further losses in the current period in order to build the foundation that will set the company on course for future profitability. Going forward, Washington Mutual’s chief strategy concentrates on the company’s expansion outside of its robust operations in California, Oregon, and Washington. If the company is to establish itself as one of the preeminent financial firms in the nation, it must first solidify its positions in its recently entered markets, and then continue with its M&A activity to resume company growth nationwide. Washington Mutual will meet significant resistance from its competitors as it attempts to edge into its current target states of Nevada, New York, Colorado, Illinois, Arizona, and Georgia. Blaisdell Consulting believes that the success of this aggressive expansion relies upon the full utilization of the company’s areas of strength. Management will use its mortgage operations, its strongest arm, to lead their growth into these markets, and establish the company name amongst the populace. From there, the company plans on expanding its operational capabilities, cross-selling its other financial products and services to its mortgage customers. In order to become a serious competitor to the major commercial banks around the nation, Washington Mutual must focus on the development of their commercial/retail operations as a means of increasing their customer base.

?? Elimination of Fees on Financial Products/Services To do so, Blaisdell Consulting advises that the company focus on developing “relationship” products such as checking and savings accounts. We feel that the employment of no fee checking accounts will continue to be a highly attractive item, quickly drawing in new customers. The strength behind the company’s no

- Washington Mutual, Inc.- 23

fee checking lies in the distinctive nature of the product. The customer must feel as though he/she is receiving a benefit that can only be obtained through business relationships with Washington Mutual. The offering of no fees is one of those product characteristics that separate Washington Mutual from its competitors. Consequentially, we believe that management should apply this no fee strategy to some of its other financial products and services. An area of particular interest in applying this strategy would be on the company’s network of ATMs. ATM fees, which can go as high as $4.50 for a single transaction, can be a major deterrent to certain customers. The elimination of these fees only acts to increase the attractiveness of Washington Mutual’s products, and should boost business flow in newly entered markets. Additionally, the implementation of this strategy will cause the current client base to restructure and focus on the younger age groups who may not be capable of affording fees. By attracting these customers early on, the company will be able to develop lifetime relationships that will result in future business flow and improved market share. Elimination of fees will act to reduce non-interest income for the firm. This will further drag on profits, which are going to rely more heavily on non interest income in the near-term as rises in interest rates are expected to squeeze the NIM. However, going forward, Blaisdell Consulting believes that the company’s establishment in new markets will produce far greater returns than the fee income loss it will incur over the near term.

?? Follow the Conglomeration Trend? As Washington Mutual expands its presence nationwide, the direction of the company’s future operations comes under question. If management truly desires to be considered amongst the elite banks in the nation, it must consider following the conglomeration trend initiated by financial powerhouses Citigroup, Bank of America, and J.P. Morgan Chase. Although this possibility lies far into the future, it still remains to be an option to be considered. Blaisdell Consulting advises management to continue with a steady organic growth/acquisition strategy after the market has settled and future direction of interest rates is not so uncertain. We are confident in the company’s strength of operations, and their ability to establish a strong market position in any market they enter. Whether or not the firm should attempt to challenge the major conglomerates will be determined with time. If Citigroup and its peers are able to fully integrate all of its operations and capture all accompanying cost synergies, then conglomerates will dominate the future financial markets and Washington Mutual must fall in line. Presently, however, it seems as though conglomerates are facing insurmountable integration costs, and may never fully capture all synergies. In this case, management must learn from others’ past mistakes and maintain operations at a more reasonable level of breadth.

- Washington Mutual, Inc.- 24

Conclusion Going forward, Washington Mutual must mitigate significant interest rate risk through the utilization of options and repositioning of their interest sensitive assets and liabilities. Additionally, a squeeze in future earnings are expected, and so we advise management to slow down acquisition activity in an effort to maintain control over swelling costs amidst a rising interest rate environment. Elimination of fees will expedite the company’s establishment in new markets. Furthermore, the success or failure of the conglomerate structure will determine the future of Washington Mutual.

i Washington Mutual Home Page – Company History – www.washingtonmutual.com ii Yahoo Finance – Washington Mutual Company Profile – www.yahoo.com iii Multex Financial – Washington Mutual Company Description – www.multex.com iv Salomon Smith Barney Equity Research – Washington Mutual 2003 Report v Rose, Peter S. Commercial Bank Management vi Rose, Peter S. Commercial Bank Management vii Rose, Peter S. Commercial Bank Management viii Salomon Smith Barney Equity Research – Washington Mutual 2003 Report ix Salomon Smith Barney Equity Research – Washington Mutual 2003 Report x Multex Financial – Washington Mutual Company Description – www.multex.com xi Multex Financial – Washington Mutual Co mpany Description – www.multex.com xii Rose, Peter S. Commercial Bank Management xiii Salomon Smith Barney Equity Research – Washington Mutual 2003 Report xiv Salomon Smith Barney Equity Research – Washington Mutual 2003 Report xv Citigroup to Buy Parent of CalFed for $5.8 billion – www.bizjournal.com xvi Salomon Smith Barney Equity Research – Washington Mutual 2003 Report xvii Salomon Smith Barney Equity Research – Washington Mutual 2003 Report xviii Rose, Peter S. Commercial Bank Management xix Interview with Professor Gordon Bjork, Claremont McKenna College xx Morgan Stanley Equity Research – Washington Mutual 2003 Report xxi Yahoo Finance –Washington Mutual Company Profile – www.yahoo.com xxii Yahoo Finance – Washington Mutual Company Profile – www.yahoo.com xxiii Washington Mutual 2002 Annual Report xxiv Washington Mutual 2002 Annual Report xxv Lehman Brothers Equity Research – Washington Mutual 2003 Report xxvi Washington Mutual 2002 Annual Report xxvii Salomon Smith Barney Equity Research – Washington Mutual 2003 Report xxviii Lehman Brothers Equity Research – Washington Mutual 2003 Report xxix Lehman Brothers Equity Research – Washington Mutual 2003 Report xxx Interview with Alan Boyce, Portfolio Manager, George Soros Fund xxxi Rose, Peter S. Commercial Bank Management xxxii Interview with Alan Boyce, Portfolio Manager, George Soros Fund

- Washington Mutual, Inc.- 25

xxxiii Rose, Peter S. Commercial Bank Management xxxiv Smith, Gary and Edward Yardeni. Securities Valuation xxxv Smith, Gary and Edward Yardeni. Securities Valuation xxxvi Smith, Gary and Edward Yardeni. Securities Valuation xxxvii Lehman Brothers Equity Research – Washington Mutual 2003 Report xxxviii Yahoo Finance – Washington Mutual Company Profile – www.yahoo.com xxxix Hoovers Online – Washington Mutual to Blend Systems for Faster Expansion – www.hoovers.com xl Hoovers Online – Washington Mutual to Blend Systems for Faster Expansion – www.hoovers.com xli Interview with Alan Boyce, Portfolio Manager, George Soros Fund