Wake eld Retail,Leisure & Town Centres · PDF fileWake eld Retail,Leisure & Town Centres Study...

164

Wakefield Retail,Leisure & Town Centres Study Wakefield Council August 2013 GVA Norfolk House 7 Norfolk Street Manchester M2 1DW Final Report

-

Upload

vuongkhuong -

Category

Documents

-

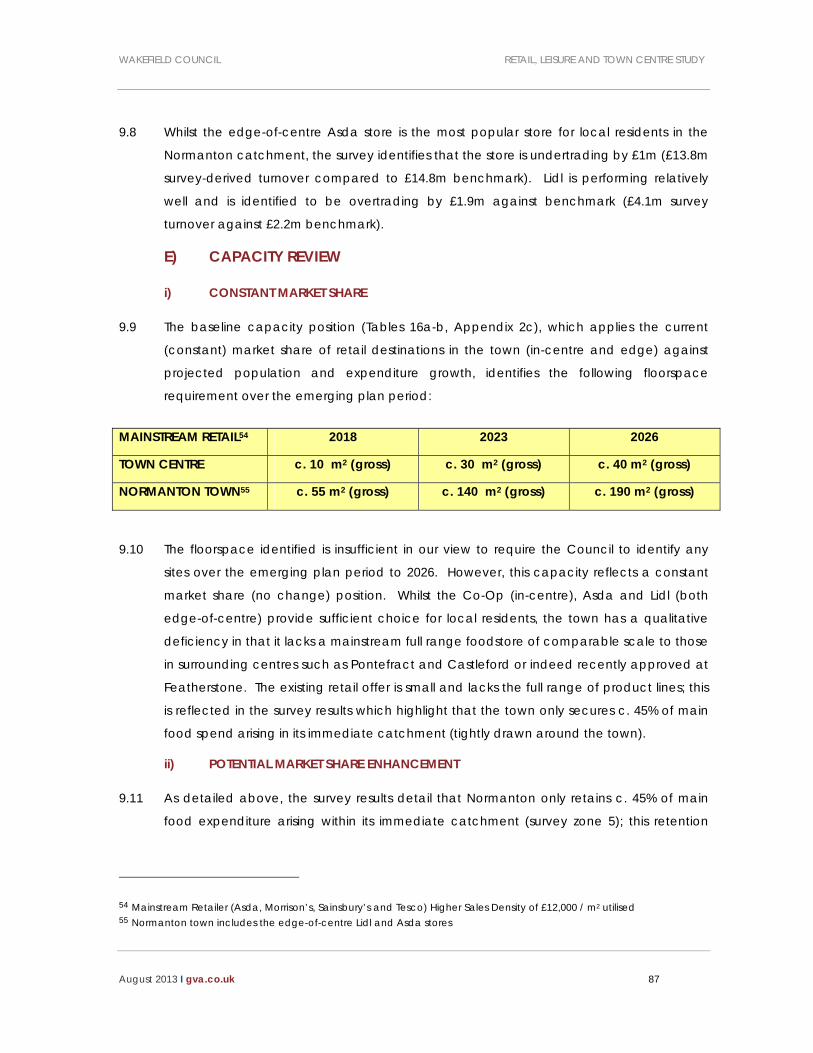

view

221 -

download

4

Transcript of Wake eld Retail,Leisure & Town Centres · PDF fileWake eld Retail,Leisure & Town Centres Study...

Wakefield Retail,Leisure & Town Centres Study

Wakefield Council

August 2013

GVANorfolk House7 Norfolk StreetManchesterM2 1DW

Final Report

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 2

CONTENTS

EXECUTIVE SUMMARY .......................................................................................................... 3

1. INTRODUCTION ........................................................................................................ 9

2. RETAIL AND LEISURE TRENDS .................................................................................. 12

3. PLANNING POLICY FRAMEWORK ......................................................................... 19

4. FLOORSPACE SURVEYS .......................................................................................... 25

5. RETAIL CAPACITY METHODOLOGY ....................................................................... 45

6. COMMITTED SCHEMES ........................................................................................... 51

7. OSSETT / HORBURY ................................................................................................. 55

8. WAKEFIELD CITY ..................................................................................................... 68

9. NORMANTON ......................................................................................................... 85

10. FEATHERSTONE ....................................................................................................... 93

11. PONTEFRACT ........................................................................................................ 100

12. CASTLEFORD ........................................................................................................ 110

13. KNOTTINGLEY ....................................................................................................... 120

14. HEMSWORTH / SOUTH ELMSALL ........................................................................... 127

15. RURAL SOUTH ....................................................................................................... 138

16. OFFICE ASSESSMENT ............................................................................................ 142

17. STRATEGIC RECOMMENDATIONS ....................................................................... 161

APPENDICES

APPENDIX 1 RETAIL CATCHMENT PLAN

APPENDIX 2 CONVENIENCE ASSESSMENT

A) POPULATION AND SPEND DATA B) MARKET SHARE ANALYSIS C) CAPACITY MODELLING

APPENDIX 3 COMPARISON ASSESSMENT

A) POPULATION AND SPEND DATA B) MARKET SHARE ANALYSIS C) CAPACITY MODELLING

APPENDIX 4 TOWN CENTRE FLOORSPACE PLANS

APPENDIX 5 LOCAL SERVICE CENTRE PLANS

APPENDIX 6 LOCAL AND NEIGHBOURHOOD CENTRE PLANS

APPENDIX 7 TOWN CENTRE BOUNDARY PLANS (DEVELOPMENT MANAGEMENT)

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 3

EXECUTIVE SUMMARY GVA was appointed in February 2013 to prepare a district-wide retail, leisure and town

centres study. The study is to inform a Retail and Town Centre Local Plan. The study

establishes current shopping and leisure patters; reviews the vitality and viability of the

main centres; assesses future quantitative and qualitative need; and provides strategic

advice on future needs and appropriate development strategy.

HEALTHCHECK ASSESSMENT

The current floorspace composition of the main centres in the district has been

established by utilising the latest Experian Goad surveys to enable a comparative

assessment. However, given that Goad surveys are not based on adopted town centre

boundaries, GVA has completed new surveys based on saved retail policy area (RPA)

boundaries. The main summary conclusions of the floorspace surveys are as follows:

CENTRE CONCLUSIONS

OSSETT Centre is relatively viable with low vacancy rates. The centre has a predominant convenience and services function with limited comparison retail offer.

HORBURY Centre is relatively viable with low vacancy rates; convenience retail offer and service function is extremely limited. Centre has strong independent (niche) offer.

WAKEFIELD Convenience offer includes mainstream foodstores. Centre has sub-regional comparison retail offer focused on Trinity Walk and Ridings Centre. Vacancies are predominantly within secondary retail areas and potentially reflect a transition period after the Trinity Walk scheme in the city centre opened.

NORMANTON Centre is a viable daily top-up shopping and service destination serving discrete local catchment. Convenience retail offer lacks mainstream anchor. Comparison retail offer very limited.

FEATHERSTONE Traditional linear centre with extremely limited retail offer. Centre requires intervention and possible physical consolidation.

PONTEFRACT Relatively viable town centre with strong convenience offer. Comparison retail offer predominantly orientated towards discount sector. Concentration of food and drink uses (evening economy) focused around historic core.

CASTLEFORD The centre is viable with few vacancies along Carlton Street and Lanes Shopping Centre. Main vacancies are small units in secondary retail areas. Convenience retail offer is limited and comparison offer is orientated towards discount sector. Limited leisure offer which reflects proximity to Xscape regional complex.

KNOTTINGLEY Small town centre which primarily is a large Morrison’s foodstore. The centre has an extremely limited comparison and service function.

HEMSWORTH Relatively viable with edge-of-centre Tesco performing strong anchor function. The comparison retail and service function is relatively limited.

SOUTH ELMSALL Traditional linear high street which may require rationalisation in order to consolidate centre and provide specific area of retail focus. Convenience and comparison retail offer is relatively limited to daily top-up shopping.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 4

On the basis of the floorspace surveys and the recommendations summarised above,

individual plans have been prepared for each respective main centre confirming

potential retail policy area and frontage changes to the existing adopted proposals map.

RETAIL NEED ASSESSMENT

The study is informed by a detailed household telephone survey exercise (1,200 surveys

across 11 catchment zones) and follows the PPS4 practice guidance1 by adopting a step-

by-step approach to quantify needs across the main centres in the district. The emerging

survey results of the Kirklees Retail Study have also been utilised to establish inflow.

All catchment zones are defined on the basis of individual postcode sectors, so as to

generate population and expenditure data from the Experian Micromarketer system.

However, given that Experian population projections (ONS) are based on historic

distribution patterns, a series of measures have been undertaken to reflect the proposed

housing growth and distribution strategy set out in the Council’s adopted Core Strategy

and Site-Specific Policies Local Plan. The latest Experian Retail Planner briefing note (v. 10,

September 2012) was utilised to provide estimates of expenditure growth, sales efficiency

growth and deductions for non-store forms of trading (SFTs).

The main conclusions on retail needs are summarised below:

CENTRE CONVENIENCE COMPARISON

OSSETT The town retains c. 18% of main food expenditure arising within its catchment. Study identifies need for new full-range mainstream foodstore to claw-back expenditure flowing to stores in surrounding centres (Wakefield, Dewsbury etc.).

The town retains just 3.3% of all comparison expenditure arising within its catchment; this reflects extremely limited town centre offer. Study identifies no specific need to plan for new comparison retail given the lack of potential to compete with large centres (Wakefield) and retail park destinations (White Rose).

HORBURY The town performs extremely limited main food shopping function with 2% market share. The study recommends that Council adopt a ‘one-centre’ approach and prioritises a new mainstream foodstore in Ossett given its greater service and retail offer.

The town has a niche local independent comparison retail offer which should be protected. There is limited potential to attract the necessary retailers to deliver a step change in its offer and associated performance. There is no need to plan for new provision.

WAKEFIELD Strong convenience offer with full-range stores in the city centre competing with large stores to the west and south. Rebalancing the network through new foodstores in Ossett and Featherstone would reduce inflows store turnover performance.

Study concludes that no immediate need for Council to plan for new provision over early phase of emerging Local Plan. Future needs should be

City centre performs its intended sub-regional role with strong market share performance from its own catchment and inflows from surrounding areas both within and outside district. City centre performing relatively well in relation to clothing (c. 65% market share from immediate catchment) and is reflective of enhancements which Trinity Walk has delivered.

The study concludes that there is no need for new

1 PPS4 practice guidance on need, impact and the sequential assessment (December 2009)

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 5

determined through update to this study should planned housing growth in the city be achieved.

development in short to medium term given that:

The city centre is still in transitional period after the opening of Trinity Walk scheme where there are some vacant units.

There is extant planning permission for a significant extension to The Ridings Centre.

The Trinity scheme in Leeds city centre allied to planned developments at Barnsley and White Rose likely to further suppress operator demand for representation in Wakefield.

The health and performance of the city centre should however continue to be monitored and a future strategy developed following an update study.

NORMANTON The town as a whole retains c. 45% of main food spend arising within its catchment; there are significant outflows to the out-of-centre Asda at Glasshoughton.

The town has a qualitative deficiency in mainstream foodstore provision and whilst there is potential to increase market share, the identified capacity is insufficient to support a new mainstream store without the relocation of an existing operator (primarily Asda).

Council should investigate commercial operator demand to –up-scale’ and if no genuine interest then no overriding requirement to plan for new provision through early phase of the emerging Local Plan.

The town retains c. 6% of comparison expenditure arising within its immediate catchment; this relatively low performance is reflective of the deficiencies in the existing comparison retail offer.

Limited need is identified on a constant market share basis and it is considered that there is no requirement for the Council to proactively plan for new provision.

FEATHERSTONE The town as a whole retains c. 9% of main food spend arising within its catchment; this reflects the extremely limited retail offer aside from the edge-of-centre Lidl.

The quantitative and qualitative deficiency in provision is to be addressed by the recent approval of a new full-range foodstore on an out-of-centre site in the town. There is subsequently no need identified for a new store in the town.

The town retains c. 4% of comparison expenditure arising within its immediate catchment; most residents visit Wakefield, Pontefract or Junction 32 Outlet.

Limited need is identified on a constant market share basis and it is considered that there is no requirement for the Council to proactively plan for new provision.

PONTEFRACT The town as a whole retains c. 70% of main food spend arising within its catchment; this is in addition to substantial inflows from the Featherstone and Knottingley catchments. There is a degree of leakage (c. 20%) to the out-of-centre Asda at Glasshoughton. The approval of new stores in Featherstone and Knottingley will however reverse current inflows.

Study concludes that there is no need to plan for new convenience provision in Pontefract over the emerging plan period given that existing stores, primarily the edge-of-centre Morrison’s, are found to be under-trading despite inflows from surrounding catchments which are to be reversed.

The town retains 33% of comparison expenditure arising within its immediate catchment. This is in addition to significant inflows from the Featherstone, Knottingley and Hemsworth catchments.

The main out-of-centre retail parks (South Baileygate and Parkside) are predominantly bulky retail orientated and do not compete with the town centre.

Whilst the study identifies a need for new provision in the town centre by the end of the emerging plan period, there is unlikely to be sufficient operator demand due to competition from destinations including Wakefield, Leeds and the Junction 32 Outlet. The Council should monitor the health and performance of the centre as part of a future update.

CASTLEFORD The town centre retains 5% of main food expenditure arising within its immediate catchment; this reflects the extremely limited convenience offer. Whilst edge-of-centre stores (Aldi and small format Morrison’s) claim 8% market share, the out-of-centre Asda store at Glasshoughton is dominant with a 61% market share. The store also draws significant inflows from the Featherstone, Normanton and Pontefract catchments.

The town centre retains 33% of all comparison retail expenditure arising in its immediate catchment. The out-of-centre provision, including Castleford Retail Park, Junction 32 Outlet and Asda Glasshoughton retains a further c. 25%. Leakage is to higher order centres including Wakefield, Leeds and White Rose.

On a constant market share basis, the capacity assessment identifies a limited need for new

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 6

Whilst the dominance of the Asda store (c. £39.1m overtrading) generates an immediate quantitative and qualitative need for new foodstore provision, there is an extant planning permission for a new large foodstore in the town centre. There is consequently no need for the Council to proactively plan for new provision through the emerging plan period.

However, it is critical that the uncertainty relating to the deliverability of the approved scheme is resolved given that resolution to approve by the Council was originally made in late 2006 and that the permission has recently been renewed. If the site is genuinely and robustly proven to not be viable or deliverable then the Council should potentially look for an alternative site given the immediate quantitative and qualitative benefits arising from providing effective competition to the out-of-centre Asda.

comparison retail provision in the town centre over the early to middle phases of the emerging Local Plan. This position is compounded by the turnover claims of the non-food element within the committed foodstore scheme in the town centre which would generate a negative capacity position if realised.

Whilst there is a wider need identified in the town as a whole in the latter phase of the emerging Local Plan (post 2023), the prospects of securing commercial interest to deliver a step change in the performance of the town centre is considered to be particularly limited given the proximity and accessibility of the town to regional comparison shopping destinations including Junction 32 Outlet and Leeds city centre.

KNOTTINGLEY The town centre is dominated by a full-range Morrison’s foodstore which retains c. 64% of main food expenditure arising within its immediate catchment. There are minor outflows to the out-of-centre Asda at Glasshoughton and Aldi at South Baileygate.

Planning permission has recently been granted for a new foodstore in the town which is likely to be occupied by a discount retailer given its proposed layout. This new store will provide competition and choice for local residents.

There is consequently no need for the Council to proactively plan for new convenience provision in the town through the emerging Local Plan period.

The town as a whole, including Morrison’s, only retains c. 10% of comparison expenditure arising within its immediate catchment. Most local residents travel to Pontefract and Castleford to meet their daily comparison shopping needs. Leeds city centre and White Rose are notable destinations for higher order comparison goods such as clothing.

On a constant market share basis, the capacity assessment identifies a limited need for new comparison retail provision in the town centre over the early to middle phases of the emerging Local Plan. As with other comparable centres in the district, there is limited potential to deliver a step-change in the comparison retail offer given the town’s proximity to higher order centres.

HEMSWORTH The town as a whole, including the edge-of-centre Tesco, retains c. 32% of main food expenditure arising within the wider catchment. The Tesco store attracts inflows from the Rural South and Barnsley catchments as well.

The study concludes that there is no quantitative or qualitative need for the Council to plan for new convenience provision in the town over the emerging Local Plan period given that there is an extant planning permission to extend the existing Tesco in the town and that the existing retail offer also includes deep discount stores such as Iceland.

The study, as detailed below, also identifies that a new deep discount foodstore in South Elmsall provides a better spatial solution and would balance the network of centres in the south of the district.

The town as a whole retains just 6% of comparison goods expenditure arising within its immediate catchment; most local residents look towards the sub-regional centres of Wakefield, Barnsley and Doncaster to meet their main comparison retail shopping needs.

Whilst the planned extension to Tesco will enhance the range of comparison retail goods available to local residents, the study concludes that there is a limited need for the Council to proactively plan for new comparison provision over the emerging Local Plan period.

SOUTH ELMSALL The town centre performs a relatively limited main food shopping function with no market share registered. This is reflective of the existing offer within the town centre which is predominantly orientated to top-up shopping (Sainsbury’s Local etc.).

The main provision is the Asda store (former Co-Op) which is located to the west of the town centre in the adjoining settlement of Moorthorpe. The small Asda store retains c. 11% of main food shopping arising within the immediate catchment.

On a constant market share basis, there is a limited

The town retains a similar market share to Hemsworth and it is concluded that there is extremely limited potential to deliver a step-change in its retail offer and associated performance going forward.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 7

quantitative need identified to support new provision. However, the study identifies the potential for achieving a minor increase in the town’s overall market share to 25%. Whilst this market share increase is insufficient to support a new full-range foodstore, a new deep discount foodstore would be a more appropriate strategy response for South Elmsall given that it would enhance choice and competition for local residents by complementing the mainstream Tesco offer at nearby Hemsworth.

LEISURE NEED ASSESSMENT

In addition to establishing where local residents visited for specific retail goods, the

household survey was also structured to obtain information on where people presently go

to pursue their main leisure activities (cinema, ten-pin bowling, health and fitness, eating

out and socialising).

Overall, the survey found that most local residents visited mainstream commercial leisure

locations in Wakefield (out-of-centre Westgate Leisure Park) and Castleford (out-of-

centre Xscape complex). Given competition from surrounding higher order destinations

such as Leeds city centre, the study concludes that there is extremely limited need for the

Council to proactively plan for new commercial leisure provision across the district.

OFFICE NEED ASSESSMENT

An assessment has been undertaken in relation to the relative balance between the

supply of office floorspace and development land and the requirements projected over

the emerging Local Plan period. This assessment has included the consideration of a

range of models to establish requirements over the period, culminating in an identified

need for between 60,390 m2 and 142,030 m2, with demand concentrated within

Wakefield city centre.

Analysis of available office floorspace supply suggests an alignment with this scale of

demand when extant planning permissions are taken into account. Supply is generally

concentrated within Wakefield in floorspace terms, albeit this is in line with evidence

around the strongest market area and historical transactional activity. This relative

balance in supply and demand does place importance on the delivery of extant office

planning permissions over the plan period.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 8

STRATEGIC RECOMMENDATIONS

A proposed district hierarchy is set out in which Wakefield is identified as the sub-regional

centre with Castleford and Pontefract as principal centres. Ossett, Knottingley,

Hemsworth and Normanton are identified as main towns with Horbury, Featherstone and

South Elmsall identified as small towns. Two further tiers are also identified for local centres

and thereafter villages / neighbourhood centres.

Revised retail policy area and frontage boundaries for the main centres in the district are

set out. A locally-set floorspace threshold for impact assessments of 300 m2 is proposed

for larger centres (sub-regional, principal towns and main towns) and 200 m2 for smaller

centres (small towns, local centres and villages).

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 9

1. INTRODUCTION 1.1 GVA was appointed by Wakefield Council in February 2013 to prepare a district-wide

retail, leisure and town centres study. The study is to inform a Retail and Town Centre

Local Plan which will form part of the Council’s Local Development Framework (LDF)

including the adopted Core Strategy and Site Allocations DPDs. The terms of the study

brief are as follows:

To establish current shopping (convenience and comparison) and leisure

expenditure patterns in the district and surrounding localities through commissioning

a new household telephone survey.

Provide a review of the vitality and viability of the main centres (city, town and local

service centres) in the district through completing new floorspace / fascia surveys to

establish centre composition.

To assess the future quantitative capacity and qualitative need for additional retail

and leisure floorspace across the district over the Local Plan period (2026), having

regard to new and planned developments / commitments.

Identify office floorspace provision in the district and capacity to accommodate new

development.

Identify deficiencies in other town centre uses including commercial leisure, tourism

and cultural uses.

To provide strategic advice on the overall future needs and confirm an appropriate

development strategy for the district and its main centres (city, town and local

service centres).

1.2 The study is informed by a detailed household telephone survey exercise which underpins

the quantitative component of the study, identifying the current market share

performance of the main centres and individual stores. The ability to quantify the survey

results in monetary terms enables a detailed understanding of the implications for

potential expenditure growth in relation to existing and planned convenience and

comparison retail floorspace provision.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 10

1.3 The results of the full quantitative analysis and qualitative appraisal along with the

identification of planned and proposed improvements in competing centres, are drawn

together to provide a set of recommendations to enable the Council to proactively plan

for future development.

1.4 However, the conclusions of the study do represent a ‘point-in-time’ assessment of

performance and opportunity. The quantitative need identified should be used to inform

policy which will endure over the short to medium term as required. However, it will be

important that the Council continues to monitor the health of its centres through its

forward planning function, adopting and revisiting the strategy to address changing

circumstances as the Local Plan progresses.

REPORT STRUCTURE

1.5 In accordance with the terms of the Study Brief this report is structured as follows:

PART ONE – BACKGROUND DETAIL AND CONTEXT

SECTION 2 – RETAIL TRENDS; summarises the current market conditions and

developments within the retail and leisure sector.

SECTION 3 – PLANNING POLICY FRAMEWORK; sets out the emerging national and

local planning policy framework which will inform preparation of the Retail and Town

Centre Local Plan.

PART TWO – QUALITATIVE ASSESSMENT

SECTION 4 – HEALTHCHECK ASSESSMENT; assesses the changes in floorspace / fascia

composition within the main centres (city and towns) across the district. The

assessment seeks to comparatively assess and benchmark against Experian Goad

regional averages.

PART THREE – QUANTITATIVE ASSESSMENT

SECTION 5 – RETAIL CAPACITY METHODOLOGY; sets out the methodology

underpinning the quantitative capacity modelling exercise.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 11

SECTION 6 – EMERGING AND COMMITTED SCHEMES; provides an overview of retail

and leisure proposals within and outside of the district which may influence future

retail needs and strategy.

SECTIONS 7 – 15 – CENTRE / CATCHMENT SPECIFIC ANALYSIS; reviews the current retail

performance and market shares of the main destinations (centres and out-of-centre

retail destinations) within and outside of the district in respect to convenience retail,

comparison retail and primary leisure activities. The need / capacity for new

provision within specific centres are identified, having regard to forward growth and

planned / emerging commitments within the district and wider sub-region.

SECTION 16 – OFFICE ASSESSMENT; identifies office floorspace in the district and

capacity to accommodate new development.

SECTION 17 – STRATEGIC RECOMMENDATIONS.

1.6 The next section sets out the current retail and leisure trends which will influence the future

performance of centres and forward strategy.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 12

2. RETAIL AND LEISURE TRENDS 2.1 The study has been commissioned in part to assess the impact of the economic climate

on retail and leisure provision across the district and how the wider economic and social

trends likely to influence both local residents and operator requirements in the future. This

section examines key trends and drivers for change in the retail industry and outlines

those of particular relevance to the district. The review draws on a range of published

data sources including research by Verdict, Mintel and Experian.

ECONOMIC OUTLOOK

2.2 The latest advice published by Experian (Retail Planner 10.1, September 2012) presents a

bleak picture for the economy as the recovery from the recession continues to be weak.

It is anticipated that household spending will continue to be constrained by subdued

disposable income growth and a weak labour market. Pressures on disposable incomes

will limit the extent to which consumers are able to save and consumers will therefore be

more considered with their spending decisions and seeking to achieve best value for

money. In many circumstances, the cost-savings offered by the Internet will be more

readily seized.

2.3 Overall, consumers remain cautious with spending not only on discretionary items but also

on needs, cutting wastage, which will impact on food & grocery volumes. There is an

increased focus on buying efficiently. Big ticket and home-related purchases remain low,

particularly as uncertainty continues to drive house prices and volumes down, as many

are reluctant to move (stagnant housing market and limited availability of finance).

2.4 As the housing market recovery remains slow and uncertain, certain sectors (e.g. home

furnishing and DIY) may benefit from increasing demand as home owners prioritise

renovation of existing property rather than moving. However, it is anticipated that sales

through the town centre will remain weak with online and out of centre retailers

continuing to take a greater share. Space and store numbers in town centre locations

are also expected to decline as retailers drive efficiencies by closing underperforming

space (notable closures include Focus DIY and Comet); these trends are discussed in

more detail below.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 13

THE INTERNET / ‘E-TAILING’

2.5 Consistent with wider economic trends, growth in e-Retail declined in 2009 as a result of

the recession reducing consumer demand. Austerity cuts on the spending ability of the

most prolific online shoppers (35-44 year olds) also had an impact on reduced demand

during this period. Overall the pace of growth in online shopping is set to slow down

significantly as the channel matures and competition increases2.

2.6 Despite overall more modest levels of growth in online shopping, there will continue to

remain reasonable pressure on traditional bricks and mortar retailers. Shoppers are able

to select their own retail mix online and shopping centres and high streets will need to

compete with this choice, which is not only driven by price and range, but also service

and expertise. Online shopping has driven expectations of convenience and service

upwards and customers are expecting more from in-store ambience to tempt them to

make a purchase3. Town centres and high streets will increasingly have to provide a

shopping ‘experience’ that the Internet is unable to match.

2.7 Trends also show that the online and in-store shopping channels are becoming gradually

more blurred as shoppers increasingly research purchases online or in stores which are

increasingly becoming showrooms. According to Verdict, in 2010, 63% of shoppers

researched goods online before purchasing in stores, an increase from 54% in 2007. At

the same time, it is estimated that 29% of consumers researched purchases in store before

buying online, representing a huge increase from 13% in 20074.

NEW TECHNOLOGIES

2.8 Technological advances will continue to drive changes in retailing, with greater

interactions between work, entertainment, social networking and shopping using mobile

devices. Quick Response codes (QR codes) have increased consumer and retailer

interaction and engagement, enabling customers to scan QR barcodes on their mobiles

to gain direct access to the product website, marketing, competitions and product

information. Smartphones provide contactless payment services using Near Field

Communications (NFC) technology. This allows customers to make payments via instore

terminals making the payment process more convenient.

2Verdict Research, “Retail Futures H1 2011 - e-Retail”, March 2011 3Verdict Research, “How Britain Shops: Overall 2011”, March 2011 4Verdict Research, “UK e-Retail 2011”, May 2011

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 14

2.9 Retailers have and continue to develop ‘augmented reality’ technology which will merge

the physical and virtual worlds to allow retailers (such as Ikea and Tesco) to provide an

interactive view of how products such as televisions or furniture, will look in consumers own

homes or provide 3D projections of life size products.

2.10 Fashion retailers including Net-a-Porter and Clarks for example already use augmented

reality technology through pointing smartphones and tablets at an image or

advertisement which triggers video content on the mobile device. This technology brings

static adverts to life and allows consumers to view catwalk runways, video advertisements

and product information, and to make purchases. Augmented reality will provide an

interactive advertising platform for retailers, who will use this technology to break down

the barriers between online and in-store shopping.

2.11 While the Internet and new technologies pose challenges to the high street, retailers are

constantly looking for ways to exploit the trading opportunities available through offering

a multichannel shopping experience. The advantages offered by physical stores, in terms

of the experience and immediacy of products, will see a network of key stores remain a

fundamental component of retailers’ strategies to develop a more coherent and

integrated multichannel proposition.

SALES EFFICIENCY

2.12 An efficiency growth rate represents the ability of retailers to increase their productivity

and absorb higher than inflation increases in their costs (such as rents, rates and service

charges) by increasing their average sales densities. The application of a turnover

‘efficiency’ growth rate is a standard approach used in retail planning studies and in is

accordance with good practice.

2.13 Although hard quantitative evidence is limited, comparison businesses in particular have,

over time, increased sales densities by achieving improvements in productivity in the use

of floorspace. Analysis of past data is difficult as sales densities increases have been

affected by changes in the use of retail floorspace over the last 20 years, with higher

value space-efficient electrical goods replacing lower value space intensive goods, the

growth in out-of-centre retailing, a number of one-off events like Sunday-trading and

longer opening hours and the very strong growth of retail expenditure relative to the

growth in floorspace.

2.14 Following the recession many retailers have struggled to increase or even maintain sales

density levels and, together with other financial problems, have led some retailers into

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 15

closure. With the expectation of weaker expenditure growth, sales density growth is also

expected to be lower than previous estimates, unless retailers accelerate store closures

and more existing retail stock is taken out of use.

2.15 Based on continuing trends towards more modern, higher density stores and the

demolition of older inefficient space, Experian expect relatively constrained efficiency

growth. The scope for sales density increases for convenience goods is more limited as

expanding store portfolios will increasingly overlap with the catchment of existing stores

and result in the cannibalisation of existing sales.

OPERATOR SPACE REQUIREMENTS

2.16 One of the major trends to emerge from the economic downturn has been the decline in

the amount of retail space in town centre locations. This is, in part, a consequence of the

harsh economic conditions forcing out independent retailers whose margins became too

tight to survive and some multiples which have either collapsed or their store portfolios

have shrunk after entering a pre-pack administration. These losses have not been offset

by new developments, as many town centre schemes have been put on hold or revised

downwards in scale. With online presence allowing national coverage, it is expected

that retailers will remain cautious about expansion.

2.17 As retailers cut back on space to improve efficiencies and online becomes a more

important channel, a new model is emerging in town centres. Retailers are moving

towards opening larger flagship stores in strategic locations which are supported by

smaller satellite stores and transactional websites. The larger flagships will accommodate

the fuller range while smaller stores will offer a more select range supplemented by

Internet kiosks allowing access to the wider range.

2.18 This model offers many advantages such as lower property costs, more efficient logistics

and being able to open stores where there is a high level of demand despite there being

space restrictions. Such models are already being trialled by retailers including

Debenhams and House of Fraser. The first House of Fraser.com store, comprising just 140

sqm, opened at Hammerson's Union Square Shopping Centre, Aberdeen in October

2011, followed by a second in Liverpool in November 2011. It is reported that the retailer

will open similar stores in locations with strong web sales, but without a store presence.

Marks & Spencer is also trialling a boutique offer with sample ranges of clothing

combined with online video and ordering capabilities.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 16

OUT-OF-CENTRE PRESSURES

2.19 As retailers opt to develop stores in the most strategic and cost effective locations, there

has been a notable resurgence to out-of-centre destinations which offer the benefit of

lower rents, better space and in most cases, free parking. According to Verdict, out-of-

town is the only channel which has seen store numbers increase consistently since 2000.

BIS report that the number of out-of-centre stores has increased by up to c.1,800 (25%)

since 2000; whilst the number of town centre stores fell by almost 15,000 between 2000

and 2009, the majority of which are likely to have been in ‘high street’ locations.

2.20 John Lewis for example, has developed a number of out-of-town stores through its At

Home format. Reports suggest that the retailer is actively seeking to increase its out-of-

town portfolio. Other retailers including H&M and Primark are also reported to be seeking

to expand their portfolios in out-of-centre locations.

FOODSTORES

2.21 In the convenience sector, the ‘race for floorspace’ has significantly diminished with

Tesco and latterly Sainsbury’s downgrading their respective new store opening

programmes in the short to medium term. The reduction in new store openings has been

coupled with a move away from large stores towards the more traditional convenience

orientated formats. The reduction in store sizes and realignment to predominantly

convenience retail formats has been primarily driven by the increase in online sales of

non-food retail goods.

2.22 Whilst there remains a significant development pipeline (Verdict estimate that between

2010 and 2015 the leading grocers will increase their space by 2 million sqm - almost

double that of the new space opened between 2005 and 2010), the mainstream retailers

are increasing being more selective in terms of future store opening locations and are no

longer acquiring sites in order to restrict competition. Prime sites are now only being

actively considered by the mainstream operators unless it is a ‘once in a generation’

opportunity to achieve representation in a long standing target area.

2.23 The continuing fall out of independents from the market will provide further opportunities

for the expansion of the leading brands. Smaller store formats are becoming more of a

focus as top up shopping is becoming increasingly popular – a response to consumers

being discouraged from travelling long distances by high fuel prices and as more are

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 17

shopping online for staple goods. Following in the path of Tesco and Sainsbury’s, Asda,

Morrison’s and Waitrose are all in the process of expanding smaller concept stores.

2.24 The (limited assortment) discount operators (Lidl and Aldi) are again embarking on a

significant expansion programme (Lidl has announced plans to open a further 60 new

stores in 2013). The proposed expansion programmes are based on the increasing market

share which the discount operators are achieving from middle class shoppers who are

price sensitive but retain a desire for quality produce. Discount operators are therefore

increasing seeking to increase representation in more affluent areas.

THE ROLE OF THE TOWN CENTRE

2.25 The town centre has been the main shopping channel for the last 30 years. However, its

role is set to change dramatically. Emerging trends suggest that it will be used more for

leisure and social activities with more bars, restaurants, food outlets and community

spaces opening in vacant units. The recent announcement by the Government to

enable temporary changes of use from Class A1 to Class A3 amongst others is likely to

precipitate this trend where market demand arises.

2.26 These trends are of major importance to the county’s shopping centres which will need to

adapt to this broader role by broadening their non-retail offer. Data from the Local Data

Company indicates that town centres with more non-retail outlets have seen an

improvement in their performance. Between 2009 and 2011, 114 towns improved their

town centre score and reduced their vacancy rate and of these, 60.5% had a lower

proportion of retail outlets.

2.27 As retailers improve their multi-channel offer, town centre stores will be used more to

support e-retailing with click and collect points and safe drop boxes for customers to

collect their online orders as well as satellite stores opening for customers to make online

purchases. As demand for retail floorspace declines, it is anticipated that more

secondary and tertiary space which suffers from lower levels of footfall, will increasingly

be converted into residential uses.

2.28 In order to ensure that town centres have a viable function moving forwards, it will be

important for the district council to aim to drive footfall to turn around their town centres

and improve dwell time to increase awareness of offers and impulse purchases. This can

be achieved by getting a better understanding of the catchment area and what local

people want, improving the mix of retail and non-retail outlets in the centre to make them

stay longer, and holding commercial, cultural and community events to create a ‘unique

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 18

selling point’ for the town centre to differentiate it from the competition and encourage

people to visit. Councils will also need to promote the wider area, to encourage further

investment in jobs, and in the town centre, to persuade residents to spend their money in

the area and support town centres further.

2.29 Smaller town centres have already been greatly impacted by the pull of larger, higher

order shopping destinations, leading to a higher vacancy rate and weaker performance.

For these centres, it will be increasingly important to create a differentiated offer, tailored

to the local catchment and to encourage residents to shop and socialise more locally.

OVERALL SUMMARY

2.30 It is evident that the traditional high street faces a number of challenges not least from

the tightening of retail spend and changing consumer behaviour but also from increasing

competition posed by the Internet and out-of-centre developments. Whilst the future is

uncertain, in light of the challenge currently faced, strategies which support the high

street are considered ever more vital.

2.31 Whilst the town centre ‘first’ strategy must continue to prevail, strategies in some instances

will need to adopt a degree of pragmatism and at worst consider the process of

managing decline of some centres, particularly secondary ones, given the ongoing

process of consolidation in the retail sector.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 19

3. PLANNING POLICY FRAMEWORK

NATIONAL PLANNING POLICY FRAMEWORK (NPPF)

3.1 National Planning Policy Framework was adopted in late March 2012 and has replaced

Planning Policy Statement 4: Planning for Sustainable Economic Growth. The PPS4

practice guidance on need, impact and sequential assessments does however remain as

an informative tool for both plan making and development management functions.

TOWN CENTRE VITALITY AND VIABILITY

3.2 The NPPF (Section 2) specifies that planning policy should promote competitive town

centre environments and set out policies for the management and growth of centres

over the plan period. Local Planning Authorities (LPAs) are directed to:

Recognise town centres as the heart of their communities and pursue policies to

support their viability and vitality.

Define hierarchies and the extent of town centres and primary shopping areas.

Promote competitive town centres that provide customer choice and a diverse retail

offer which reflects the individuality of town centres.

Retain and enhance existing markets, ensuring they remain attractive and

competitive.

Allocate appropriate in-centre sites which are not compromised by limited site

availability. If it is not possible to ensure a sufficient range of suitable sites,

appropriate edge of centre sites that are well connected to a town centre should be

allocated.

Where town centres are in decline, local authorities should plan positively for their

futures and encourage economic activity.

3.3 The long-standing sequential test is retained in the NPPF albeit that there is increased

emphasis on LPAs to ensure an available supply of sites.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 20

EVIDENCE BASE REQUIREMENTS

3.4 LPAs are directed by NPPF to ensure that their Local Plan is based on adequate, up-to-

date and relevant evidence. In relation to planning to meet business requirements, LPAs

are required to have a clear understanding of business needs within the economic

markets operating in and across their area. LPAs are directed to use the evidence base

to assess (amongst others):

The needs for land or floorspace for economic development, including both the

quantitative and qualitative needs for all foreseeable types of economic activity over

the plan period, including for retail and leisure development.

The role and function of town centres and the relationship between them, including

any trends in the performance of centres; and

The capacity of existing centres to accommodate new town centre development.

3.5 Whilst the NPPF constitutes a material consideration which LPAs should take into account

from the date of publication (late March), the policy provisions and directions of the NPPF

should inform the preparation of plans either through partial review or by preparing a new

statutory development plan.

WAKEFIELD LOCAL DEVELOPMENT FRAMEWORK

3.6 This study is intended to inform the preparation of a Retail and Town Centre Local Plan,

which will form part of Wakefield’s Local Plan. A brief summary of the main adopted

policies within the existing LDF is provided below.

CORE STRATEGY

3.7 The Core Strategy was adopted in April 2009 and sets out the overall strategic direction

for the plan and sets out the framework against which the wider LDF will be delivered.

The main spatial and strategic policies relevant to the retail study commission are as

follows:

Policy CS1 (SCALE AND FUNCTION) supports development that reflects the scale and

function of the main centres of the Wakefield district.

Policy CS2 (RETAIL CENTRE HIERARCHY) sets out a hierarchy for new retail

development and details that Wakefield city centre will remain the largest and

dominant retail centre, performing a sub-regional role, with Castleford and Pontefract

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 21

serving the Five Towns area. The provision of retail and other town centre uses is to be

of an appropriate scale to the size and function of the centre.

Policy CS2 also states that a sequential approach will be taken to assess sites for retail

and other town centre uses, focusing development on city and town centres. Out of

centre retail and town centre uses are only to be permitted where they meet the

requirements of national planning policy.

POLICY CS8 (OFFICE DEVELOPMENT); details that new commercial office

development is to be located at:

i) In Wakefield city centre and in Castleford and Pontefract town centres;

ii) Within the extent of existing office parks at Paragon Business Village, Snowhill,

Wakefield, Calder Park, Denby Dale Road, Wakefield; or

iii) At the Former Prince of Wales Colliery, Park Road, Pontefract.

POLICY CS11 (LEISURE DEVELOPMENT); provides guidance as to the location of new

leisure development, encouraging it towards urban areas. New stadia development

is encouraged at Wakefield and Castleford, alongside new sports village concepts.

DEVELOPMENT POLICIES

3.8 The document was adopted in April 2009 and sets out general development

management policies and the necessary scope of technical work required in support of

planning applications.

CENTRAL WAKEFIELD AREA ACTION PLAN (AAP)

3.9 The Area Action Plan (AAP) was adopted in June 2009 and sets out a detailed strategy

and vision, policies and site allocations for around the Wakefield city centre area.

Relevant policies are set out as follows:

POLICY CW12 states that the focus for substantial new office floorspace will be within

defined Special Policy Areas and along the Emerald Ring. The policy details that the

three major regeneration schemes at Trinity Walk, Merchant Gate and Waterfront will

provide at least 49,000 m2 of Class B1 office floorspace. Small scale office

development is to be permitted outside of these areas, subject to an acceptable

impact on surrounding areas.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 22

POLICY CW13 defines a retail policy area within the city centre where Class A1 retail

development will be permitted and encouraged. The policy area is to provide at

least 53,000 m2 of new retail floorspace in the period to 2016.

Outside of the policy area, significant retail development is only to be permitted

where it would not have a detrimental impact on the vitality and viability of the retail

policy area and is small in scale; serves daily shopping needs; forms part of larger

mixed-use developments; and would not be detrimental to the amenity and

character of the retail policy area.

POLICY CW14 defines primary shopping frontages within the city centre and details

that non-retail uses will permitted at ground floor level, unless they would either:

i) Create a continuous frontage of more than three non-retail uses (classes A3-

A5), or 20 metres of non-retail uses; or

ii) Result in more than 25% of the total length of street frontage in any one street

or of any one block being in non-retail use.

Non-retail uses on corner properties within the Primary Shopping Frontages are to be

allowed in exceptional circumstances but restricted to financial and professional

services and food and drink premises.

POLICY CW15 defines a specialist retail area within the city centre which is to be

maintained and enhanced by opposing comprehensive redevelopment; retaining

active frontages; ensuring no more than a third of the shopping frontage at ground

floor level includes non retail uses; and maintaining and enhancing the public realm.

POLICY CW16 encourages small scale shops as well as restaurant, bars and cafes as

potential uses within the Westgate Yards area.

POLICY CW19 defines Trinity Walk as a special policy area and supports the

development of the site as a vibrant new shopping quarter.

POLICY CW20 defines Merchant Gate as a special policy area to be re-developed as

a new office quarter.

POLICY CW21 defines the Waterfront as a special policy area to be redeveloped as a

mixed use area, including office and residential uses.

POLICY CW22 defines Kirkgate as a special policy area to be redeveloped for uses

including office, retail and leisure development.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 23

POLICY CW23 identifies Ings Road as a special policy area to be redeveloped for uses

including small-scale retail, office and leisure development.

POLICY CW24 identifies Thornes Wharf as a special policy area to be redeveloped as

a mixed use area.

SITE-SPECIFIC POLICIES LOCAL PLAN

3.10 The Site Specific Policies Local Plan was adopted in September 2012 and sets out land

allocations across the district to meet anticipated development needs relating to

housing, employment and mixed use development. It does not include policies and

proposals relating to retailing / town centres and leisure / open space.

WAKEFIELD UNITARY DEVELOPMENT PLAN (FIRST ALERATION)

3.11 The Unitary Development Plan (First Alteration) was adopted in January 2003 and a

number of policies remain ‘saved’. Relevant UDP policies relating to the study are:

POLICY S1 states that retail development will be encouraged and permitted in the

retail area of city and town centres. The policy details that retail development should

be of an appropriate scale to the needs of the area served by these centres.

POLICY S2 states that large retail outlets (foodstores and retail warehouses) which

cannot be accommodated within the defined retailing areas of centres will be

permitted on the fringe of these areas, provided that they lie within the existing urban

area; are readily accessible; do not involve land allocated for other uses; and is of an

appropriate scale.

POLICY S3 permits out-of-centre retail development where there is a clearly defined

need; the type of developed cannot be satisfactorily accommodated in or on the

edge of existing centres and; does not undermine the viability and vitality of existing

centres. Large food / convenience outlets are also only to be permitted within the

main urban areas of Wakefield, Castleford or Pontefract, providing that such

development is on a scale appropriate to serve the needs of the locality.

POLICY S4 encourages the development of local shopping facilities to the serve the

day-to-day needs of their immediate locality.

POLICY S5 sets out a strategy for encouraging public and private sector investment to

provide a better quality retail environment.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 24

POLICY S6 states that non-retail uses will be permitted in town centres, subject to a

variety of restrictions. This includes limiting non-retail uses to A2 and A3 uses only in

primary shopping frontages.

POLICY L1 allocates land for indoor and outdoor leisure facilities.

POLICY L2 encourages new leisure and tourist development. For major travel-

generating uses, such development is to be permitted only in city, town and district

centres or in the case of smaller facilities, in local centres. Outside of such centres,

major leisure development is only to be permitted where there is a clearly definable

need and no other more appropriate sites are available.

POLICIES CAS57 – CA60 sets out retail policy specific to Castleford town centre. Town

centre and primary shopping frontages are defined. Policy CAS60 supports the

provision of new office space in Castleford town centre.

POLICIES NOR32 and N33 set out retail policy specific to Normanton town centre and

define the town centre and primary shopping frontage boundaries.

POLICY FTH28 sets out retail policy specific to Featherstone town centre and defines

the town centre boundary.

POLICIES PNT48 - PNT52 set out retail policy specific to Pontefract town centre and

defines the town centre and primary shopping frontage boundaries. Policy PNT52

permits A2 development with the core retail area and B1 development on establishes

industrial sites or on sites allocated for that purpose in the town centre.

POLICY HEM51 sets out retail policy specific to Hemsworth town centre and defines

the town centre boundary.

POLICY EMS56 - EMS57 sets out retail policy specific to South Elmsall town centre and

defines the town centre and primary shopping frontage boundaries.

POLICIES OH26 – OH28 set out retail policy specific to the town centres of Ossett and

Horbury, and defines the respective town centre boundaries. Policy OH28 identifies

the primary retail frontage in Ossett.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 25

4. FLOORSPACE SURVEYS 4.1 The National Planning Policy Framework states that comprehensive up-to-date monitoring

of town centre performance is essential in enabling local planning authorities to improve

the vitality and viability of town centres and effectively plan for the future.

4.2 The floorspace composition of a centre is a particularly important monitoring tool and in

order to establish the current floorspace composition of the main centres in the district,

the following data sources have been utilised:

EXPERIAN GOAD SURVEYS; Experian has published floorspace plans and

accompanying category reports for most centres in the district. These reports and

plans have been utilised to enable a comparative assessment of a centre against

(comparable) regional benchmarks from the Experian database.

GVA FLOORSPACE SURVEY UPDATES; independent surveys have been completed

given that GOAD centre surveys are based on Experian’s own interpretation of the

true extent of retailing within a centre rather than the town centre boundaries as

defined in an adopted (or emerging) statutory development plan. GVA has

therefore updated the GOAD survey figures to remove all floorspace located beyond

adopted (saved UDP) retail policy areas or in the case of Wakefield city centre, the

adopted AAP retail policy area boundaries.

4.3 In addition to completing detailed floorspace surveys for the main town centres in the

district5, surveys have also been undertaken for the sixteen local centres in the district; the

survey plans for these centres is provided at Appendices 5 and 6 for reference.

OSSETT

EXPERIAN GOAD FLOORSPACE SURVEY

4.4 The latest Experian GOAD survey of Ossett (October 2011) is summarised below; the

GOAD average for comparable centres in the Yorkshire region is also provided to enable

comparative analysis.

5 Wakefield City Centre, Castleford, Pontefract, Hemsworth, Featherstone, Ossett, Normanton, Horbury, South Elmsall and Knottingley

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 26

Retail Sector No.

Outlets % Outlets Floorspace

(sqm) % Floorspace

Ossett Yorkshire & Humberside

Ossett Yorkshire & Humberside

Convenience 13 7.6 7.19 4,264 21.05 12.46

Comparison 43 25.15 29.66 3,921 19.35 29.48

Retail Service 37 21.64 12.23 2,648 13.07 5.38

Leisure Service 31 18.13 19.35 3,800 18.75 18.04

Financial Service 13 7.6 9.13 1,607 7.93 6.41

Vacant 8 4.68 11.28 1,459 7.2 8.67

TOTAL 145 100 100 17,699 100 100

4.5 The main headline findings arising from the Goad data is as follows:

CONVENIENCE; the town centre convenience retail offer is broadly comparable to

the GOAD regional average in terms of the number of outlets (7.6% to 7.19%).

However, the proportion of floorspace within the town centre dedicated to

convenience retail is significantly above the GOAD regional average (21.05% to

12.46%); this reflects the overall limitations of the town centre (limited comparison

retail offer etc.).

COMPARISON; the retail offer in terms of the number of outlets and overall proportion

of floorspace is below the GOAD regional average. This reflects the fact that the

current comparison retail offer in the town centre is limited to daily goods (chemist,

personal items etc.).

VACANT; the town centre had a limited number of vacant units compared to the

GOAD regional average (4.68% to 11.28%). The quantum of vacant floorspace is

however broadly comparable to the Goad average suggesting that the vacant units

at the time of the Goad survey were slightly larger.

4.6 Overall, the GOAD survey indicates that the town centre was relatively viable with few

vacancies. The limitations of the comparison retail offer are highlighted by the survey.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 27

GVA FLOORSPACE SURVEY (AUGUST 2013)

4.7 The floorspace composition of the adopted retail policy area within the town centre is:

Retail Sector Floorspace (sqm gross) Units

Convenience 3,096 15

Comparison 3,468 38

Service6 7,432 81

Vacant 237 4

TOTAL7 14,233 138

4.8 The main differences between the Goad and the GVA update are as follows:

CONVENIENCE; there is a notable difference in convenience floorspace between the

GOAD and GVA surveys; this is due to the exclusion of the Lidl store on Kingsway

which is outside the currently defined retail policy area boundary. There are more

convenience units since the GOAD survey was completed.

COMPARISON; there is a difference of 5 units between the GOAD survey and the

GVA update. The difference in comparison retail floorspace is in the order of 450 m2.

VACANT; the GVA survey identifies a total of 4 vacant units within the town centre;

this is half of the number of vacancies identified in the GOAD survey. The difference

in floorspace is primarily attributable to the Iceland store being vacant at the time of

the GOAD survey.

4.9 Overall, the main differences between the two respective surveys are Iceland re-

occupying a former vacant unit and Lidl being excluded from the GVA survey results due

to its current edge-of-centre location beyond the adopted retail policy area boundary.

In headline terms, it is positive that the vacancies identified in the GVA survey are half of

that identified in the original GOAD survey.

6 Services comprise Retail Services (Class A1), Professional (Class A2), Food & Drink (Classes A3 – A5) and Other Services. 7 Total floorspace excludes Miscellaneous uses

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 28

HORBURY

EXPERIAN GOAD FLOORSPACE SURVEY

4.10 The most recent Experian GOAD survey of Horbury was completed in January 2011; the

main survey results are as follows:

Retail Sector No. Outlets

% Outlets Floorspace (sqm)

% Floorspace

Horbury Yorkshire & Humberside

Horbury Yorkshire & Humberside

Convenience 7 9.59 7.19 1,700 21.18 12.46

Comparison 22 30.14 29.66 2,583 32.18 29.48

Retail Service 14 19.18 12.23 883 11 5.38

Leisure Service 14 19.18 19.35 1,384 17.25 18.04

Financial Service 4 5.48 9.13 399 4.98 6.41

Vacant 7 9.59 11.28 539 6.71 8.67

TOTAL 68 100 100 7,488 100 100

4.11 The survey results highlight the following:

CONVENIENCE; the number of units and quantum of overall floorspace dedicated to

convenience retailing is significantly above the Goad regional averages in both

instances. This primarily reflects the convenience orientated nature of the town

centre retail offer.

COMPARISON; the number of outlets and proportion of floorspace within the town

centre dedicated to comparison retailing is slightly above the Goad regional

average. Given that there is a limited number of national multiple operators

represented in Horbury, the survey results indicate a strong niche local independent

comparison retail offer.

VACANT; there are a total of 7 outlets within the centre which are vacant; this is

below the Goad regional average. Likewise the overall quantum of floorspace which

is presently vacant is below the regional average.

4.12 Overall, the survey results identify that the town centre is viable. The local independent

offer, particularly for comparison retail, appears particularly strong.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 29

GVA FLOORSPACE SURVEY UPDATE (AUGUST 2013)

4.13 The floorspace composition within the adopted retail policy area is as follows:

Retail Sector Floorspace (sqm gross) Units

Convenience 1,747 11

Comparison 910 15

Service8 2,644 33

Vacant 141 2

TOTAL9 5,442 61

4.14 Comparative analysis of the floorspace survey results identifies the following:

CONVENIENCE; there is only a minor difference (increase) in floorspace between the

GOAD and GVA surveys. The GVA survey does however identify four additional units

compared to the GOAD survey; this suggests that units within the town centre have

been re-occupied by convenience retail uses in the period between the two surveys.

COMPARISON; there is a significant difference in comparison retail floorspace

between the GOAD and GVA surveys (c. 2,600 m2 to c. 900 m2). The number of units

has also decreased between the respective surveys (22 to 15 units).

VACANT; the GOAD survey identifies a total of 7 vacant units whereas the GVA survey

identifies only 2. Accordingly, there is a difference in floorspace between the two

respective surveys (decreased from c. 540 m2 to 141 m2).

4.15 Overall, there is a significant difference in comparison retail provision between the GVA

and GOAD surveys. This suggests that the units may have been re-occupied. It is our

view that the town centre is relatively viable with a niche comparison retail offer

(independent orientated) complementing its daily food shopping and services function.

8 Services comprise Retail Services (Class A1), Professional (Class A2), Food & Drink (Classes A3 – A5) and Other Services 9 Total floorspace excludes Miscellaneous uses

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 30

WAKEFIELD

EXPERIAN GOAD FLOORSPACE SURVEY

4.16 The latest GOAD survey of Wakefield city centre was undertaken in August 2012. The

survey results against the Yorkshire regional average is provided below for comparison.

Retail Sector No.

Outlets % Outlets Floorspace

(sqm) % Floorspace

Wakefield Yorkshire & Humberside

Wakefield Yorkshire & Humberside

Convenience 41 5.86 7.19 22,418 13.78 12.46

Comparison 208 29.71 29.66 56,782 34.91 29.48

Retail Service 74 10.57 12.23 7,107 4.37 5.38

Leisure Service 127 18.14 19.35 22,102 13.59 18.04

Financial Service 59 8.43 9.13 8,278 5.09 6.41

Vacant 135 19.29 11.28 27,843 17.12 8.67

TOTAL 644 100 100 144,530 100 100

4.17 The Goad survey results indicate the following:

CONVENIENCE; whilst the number of outlets within the city centre is slightly below the

Goad regional average, the quantum of floorspace is above; this is primarily

attributable to the large Sainsbury’s (Trinity Walk) and Morrison’s (Ridings Centre).

COMPARISON; whilst the city centre has experienced a significant quantitative

expansion in its retail offer with the completion and subsequent opening of the Trinity

Walk scheme, the number of outlets is comparable to the Goad regional average.

The quantum of floorspace (as a proportion of the overall city centre) is however

substantially above the Goad regional average.

VACANT; both the number of units and overall quantum of floorspace are

significantly above the Goad regional average. The higher than average vacancy

rates are likely to reflect a number of national and local economic factors including

the ongoing adverse economic climate, the city centre retail offer settling down after

the Trinity Walk scheme has become fully established and the presence of traditional

retail stock in the more secondary areas of the town centre which are in some

instances becoming increasingly obsolete in commercial terms (demand etc.).

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 31

4.18 Overall, the survey results show that the city centre retail offer (convenience and

comparison) is relatively well balanced and in line with the Goad regional average. The

service offer is broadly comparable to the regional average whilst vacancies do begin to

raise some concerns, particularly in relation to secondary areas of the centre.

GVA FLOORSPACE SURVEY UPDATE (AUGUST 2013)

4.19 GVA has updated the GOAD survey to take account of floorspace (including upper and

ground floors) and fascia changes since mid 2012. Given that the Goad survey includes

areas outside of the adopted retail policy area boundaries (as defined by the Central

Wakefield AAP) such as the southern extent of Kirkgate (towards rail station), western

extent of Westgate, Lower Warrengate and northern extent of Northgate, the survey

results show significant changes, as follows:

Retail Sector Floorspace (sqm gross) Units

Convenience 18,026 40

Comparison 48,258 179

Service10 23,122 203

Vacant 16,352 103

TOTAL11 105,758 525

4.20 Whilst there has not been a significant time lapse since the GOAD survey was completed

in mid 2012, the main differences between the two respective surveys are as follows:

CONVENIENCE; whilst the number of units is similar for both surveys (c. 40 units), there is

a significant difference in floorspace with GOAD identifying c. 22,400 m2 (gross)

whereas the GVA survey identifies c. 18,000 m2 (gross).

COMPARISON; there is a major difference in the number of units between the two

surveys with GOAD identifying 208 and GVA identifying 179. There is a significant

difference in the amount of comparison retail floorspace between the two surveys (c.

56,800 m2 (gross) to c. 48,300 m2 (gross)); this is due in part to the exclusion of the

southern extent of Kirkgate which is beyond the existing defined retail policy area.

VACANT; the GOAD survey identifies a total of 135 units which are presently vacant

whereas the GVA survey identifies 103 units. There is also a significant difference in

10 Services comprise Retail Services (Class A1), Professional (Class A2), Food & Drink (Classes A3 – A5) and Other Services 11 Excludes floorspace defined as Miscellaneous

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 32

vacant floorspace with GOAD identifying c. 27,800 m2 (gross) and GVA c. 16,350 m2

(gross)). The differences in both surveys is primarily attributable to the GOAD survey

extending beyond the existing adopted retail policy area.

4.21 Given that the Trinity Walk scheme within the city centre has only been trading since May

2011, it is difficult to definitively conclude whether the vacancy levels are a result of the

quantitative and qualitative enhancement to the current retail offer, the current

economic climate or differences in the survey area utilised (GVA floorspace figures solely

based on adopted retail policy area boundaries).

4.22 Whilst there are some vacant retail units within both Trinity Walk and Ridings Centre, it is

particularly apparent that there are a significant number of smaller historic units on the

outer parts of Westgate and Kirkgate in particular.

EDGE-OF-CENTRE / OUT-OF-CENTRE RETAIL PROVISION

4.23 Whilst there are two large mainstream foodstores within the city centre (Sainsbury’s Trinity

Walk and Morrison’s Ridings Centre), there are also a number of foodstores located

outside. A large format Morrison’s store is prominently located on Dewsbury Road to the

west of the city centre whilst a recently re-opened Sainsbury’s store is located at Ings

Road to the south. A large freestanding Asda store at Sandal serves the far southern

extent of the city and the surrounding rural hinterland.

4.24 In terms of comparison retailing, there are a number of retail warehouse parks to the

south of the city centre including Westgate (bulky orientated including operators such as

ScS and Pets at Home), Ings Road (Matalan, Homebase and B&M) and Cathedral (B&Q,

Argos Extra and Carpetright) retail parks.

4.25 The main commercial leisure offer in Wakefield is also located outside the city centre at

Westgate Leisure Park; occupiers including Cineworld and Gala Bingo.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 33

NORMANTON

EXPERIAN GOAD FLOORSPACE SURVEY

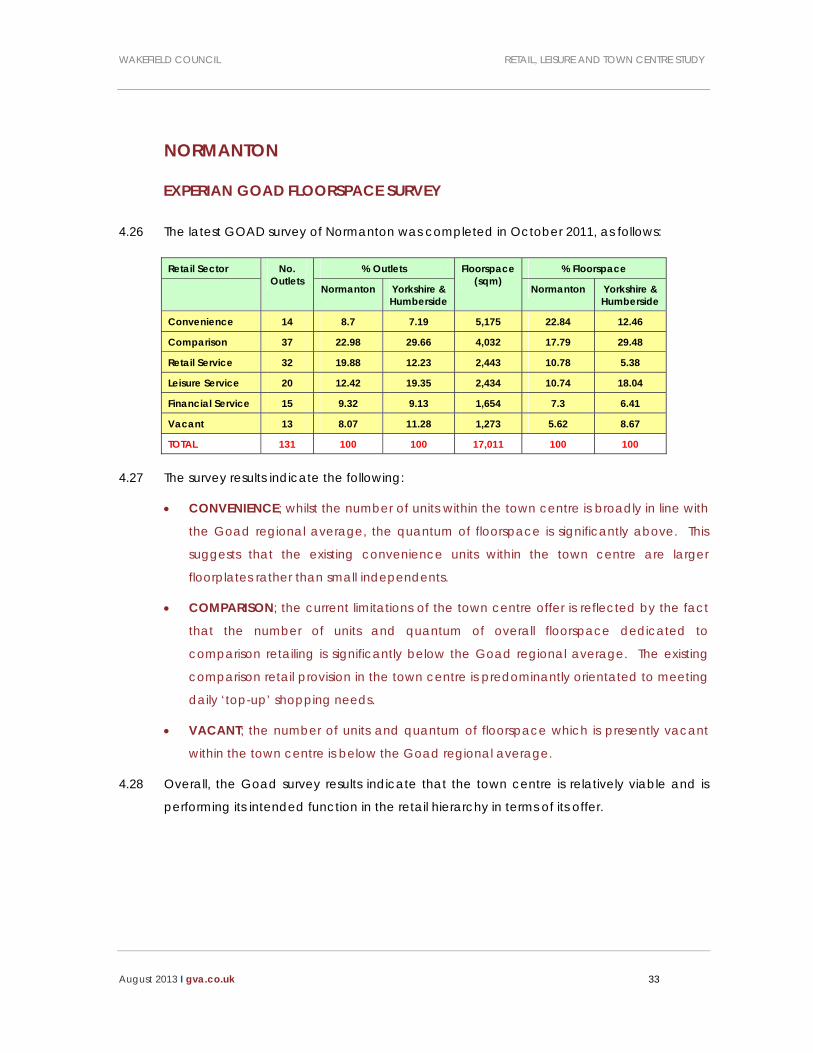

4.26 The latest GOAD survey of Normanton was completed in October 2011, as follows:

Retail Sector No. Outlets

% Outlets Floorspace (sqm)

% Floorspace

Normanton Yorkshire & Humberside

Normanton Yorkshire & Humberside

Convenience 14 8.7 7.19 5,175 22.84 12.46

Comparison 37 22.98 29.66 4,032 17.79 29.48

Retail Service 32 19.88 12.23 2,443 10.78 5.38

Leisure Service 20 12.42 19.35 2,434 10.74 18.04

Financial Service 15 9.32 9.13 1,654 7.3 6.41

Vacant 13 8.07 11.28 1,273 5.62 8.67

TOTAL 131 100 100 17,011 100 100

4.27 The survey results indicate the following:

CONVENIENCE; whilst the number of units within the town centre is broadly in line with

the Goad regional average, the quantum of floorspace is significantly above. This

suggests that the existing convenience units within the town centre are larger

floorplates rather than small independents.

COMPARISON; the current limitations of the town centre offer is reflected by the fact

that the number of units and quantum of overall floorspace dedicated to

comparison retailing is significantly below the Goad regional average. The existing

comparison retail provision in the town centre is predominantly orientated to meeting

daily ‘top-up’ shopping needs.

VACANT; the number of units and quantum of floorspace which is presently vacant

within the town centre is below the Goad regional average.

4.28 Overall, the Goad survey results indicate that the town centre is relatively viable and is

performing its intended function in the retail hierarchy in terms of its offer.

WAKEFIELD COUNCIL RETAIL, LEISURE AND TOWN CENTRE STUDY

August 2013 I gva.co.uk 34

GVA FLOORSPACE SURVEY UPDATE (AUGUST 2013)

4.29 GVA has updated the Goad survey to take account of floorspace and fascia changes

since late 2011; the survey results are as follows:

Retail Sector Floorspace (sqm gross) Units

Convenience 2,790 13

Comparison 3,453 37

Service12 3,908 54

Vacant 585 11

TOTAL13 10,736 115

4.30 The main differences in the survey results (taking account of the defined adopted retail

policy area boundaries) are as follows:

CONVENIENCE; there is only a difference of 1 unit between the two respective

surveys. The floorspace figures are however significantly different with GOAD

identifying 5,175 m2 (gross) and GVA 2,790 m2 (gross). The difference is due to the

existing Lidl and Asda stores being located outside of the defined retail policy area