VOLUME XX Go Digital - Wipro · VOLUME XX Go Digital >PWYVZL[\W ... The Great Digital Race ......

44

A WIPRO COUNCIL FOR INDUSTRY RESEARCH JOURNAL VOLUME XX Go Digital

Transcript of VOLUME XX Go Digital - Wipro · VOLUME XX Go Digital >PWYVZL[\W ... The Great Digital Race ......

A Wipro CounCil for industry reseArCh JournAl

VOLUME XX Go Digital

Wipro set up the Council for Industry Research comprising domain and technology experts from the organization, to address the needs of customers. It specifically surveys innovative strategies that will help customers gain competitive advantage in the market. The Council, in collaboration with leading academic institutions and industry bodies, studies market trends that provide organizations a better insight into their IT and business strategies.

For more information on the Council, visit www.wipro.com/insights/ or email us at [email protected] can also follow us on twitter@wipro & @wiproinsights

The Great Digital Race

Digital Transformation is everywhere. And you, dear reader, are part of it. Technology has changed in the last decade and is powering a metamorphosis. But this is true only partially. More than the technology, it is your behavior as a customer and as an employee that has set off the tidal wave of transformation. Your lifestyle, your preferences, your needs and desires are at the bottom of a remarkable new way to organize business. Digital Transformation is no longer a buzz word. If you are not running the digital race, you and your business face the very real danger of becoming obsolete. It is important to understand that digitizing goes beyond customer touch points. It is about the effect on the organization’s products, services, processes, people, partners, supply chains and operational philosophies. Some organizations may take months if not years to understand the impact the trend has on their business – and their response to it. By then, it may be too late. This issue of WInsights aims to reduce that risk. Within these pages we look at three key areas that must be urgently addressed: customer experience, operational processes, and business models - all three when transformed through digital technologies aim to bring a metamorphosis in an organization. But you cannot think digital in silos. Successful transformation requires a sweeping vision of what tomorrow’s business will look like. As a business leader you will appreciate the insights shared by digital transformation experts in this issue of WInsights. Industry authorities and our own teams that are engaged in large transformation projects across the world share their views, experience and expertise. I hope that by the time you have absorbed this issue of WInsights, you are raring to take your organization to new digital heights. Here’s wishing you quickly find your digital way through 2015.

Puneet ChandraChief Marketing Officer, Wipro Ltd.

FOREWORD

2

WINSIGHTS Volume XX

Workplace Transformation- Special Feature

Tarun Sharma, VP R&D, Head BMC India & Ukraine Suhas Kelkar, VP & Chief Technology Officer (APAC) BMC

19

Travel Industry Taps Technology To Win Over Customers- A Wipro-Knowledge@Wharton Article

Technology is opening new ways for companies in the travel and hospitalityindustries to engage with customers, raise revenues, and streamline processes.

Bill Martin, Chief Information Officer at Royal Caribbean CruisesElea McDonnell Feit, Former Wharton lecturerDeviprasad Rambhatla, Head of Travel, Transportation and Hospitality Unit, Wipro Ltd

04

CONTENTS

Avinash Rao, Global Head, Wipro Digital

Why ‘Big Bang’ Change Has No Place in Digital Transformation

Digital Transformation is a journey. It goes beyond enabling individual customer touch points such as websites, mobile devices and social platforms - in fact, a Digital Transformation agenda works at the intersection of the front-end customer experience and the back-end digitization of the business.

0814 Internal Customer: The Litmus

Test for Digital Transformation

In a digital world, organizations cannot continue to consume IT in traditional ways and yet hope to succeed - they must transform their workplace along with their processes or perish.

Atul Sood, VP Advanced Technologies & Solutions, Wipro Ltd

Digital Transformaion- Infographic

Digital Transformation is no longer a buzz word. If you are not running the digital race, your business face the very real danger of becoming obsolete. Digitizing goes beyond customer touch points - indeed when Customer experience, Operational processes, and Business models are all transformed through digital technologies your business is reaching towards maturity.

WINSIGHTS Volume XX

3

CONTENTS

Rapid Change: How Simplification Can Make it Simple

Businesses are now realizing the importance of simplification in the businesses, channels, product clusters, measurements, regions, processes and tools they use in order to reduce risk from technological advances, demographic changes, economic shocks, regulatory and environmental issues.

Alexis Samuel, Chief Risk Officer, Head BPE, and Global Managing Partner, Wipro Consulting ServicesKris Denton, Managing Partner, Americas, Wipro Consulting Services, Wipro Ltd

22

Digitize or Perish

In a business where product lifecycles are shrinking and competitive advantage belongs to those who respond in real time, there can be no argument against Digital Transformation.

Srini Pallia, Chief Executive, Retail, Consumer Goods, Transportation & Govt.

38Digital Assurance

In an Everything-Digital environment, businesses must stress on operations that provide accurate, rich and engaging digital content, and distribute it satisfactorily across channels to improve accessibility coupled with a high-end user experience to deliver what every organization wants: digital assurance.

Kumudha Sridharan, VP & Global Head of Testing Services, Wipro Ltd

28

Digital: The New CurrencyNeobanks and digital banks excel in helping customer use the small segments of free time. They have mastered the art of structuring products so that they can be explained without a human interface. So what does the future look like for traditional banks as the new currency goes Digital?

Rajan Kohli, Sr. VP & Global, Head of Banking & Financial, Services, Wipro LtdSushankar Daspal, Practice Head, Digital & Mobile Channels, Banking, Wipro Ltd

31Rapid Change: How Simplification Can Make it Simple

Businesses are now realizing the importance of simplification in the businesses, channels, product clusters, measurements, regions, processes and tools they use in order to reduce risk from technological advances, demographic changes, economic shocks, regulatory and environmental issues.

Alexis Samuel, Chief Risk Officer, HeadBPE, and Global Managing Partner, WiproConsulting ServicesKris Denton, Managing Partner, Americas,Wipro Consulting Services, Wipro Ltd

20

Digitize or Perish

In a business where product lifecycles are shrinking and competitive advantage belongs to those who respond in real time, there can be no argument against Digital Transformation.

Srini Pallia, Chief Executive, Retail, Consumer Goods, Transportation & Govt.

36Digital Assurance

In an Everything-Digital environment, businesses must stress on operations that provide accurate, rich and engaging digital content, and distribute it satisfactorily across channels to improve accessibility coupled with a high-end user experience to deliver what every organization wants: digital assurance.

Kumudha Sridharan, Vice President & Global Head of Testing Services, Wipro Ltd

26

Digital: The New CurrencyNeobanks and digital banks excel in helping customer use the small segments of free time. They have mastered the art of structuring products so that they can be explained without a human interface. So what does the future look like for traditional banks as the new currency goes Digital?

Rajan Kohli, Sr. Vice President & Global, Head of Banking & Financial, Services, Wipro LtdSushankar Daspal, Practice Head, Digital & Mobile Channels, Banking, Wipro Ltd

29

4

WINSIGHTS Volume XX

Bill Martin

Chief Information Officer, Royal Caribbean Cruises

For Bill Martin, the chief information officer (CIO) of Royal Caribbean Cruises Ltd., his two teenage daughters provided the best corporate strategy lessons. In 2012, when he and his family went on a cruise, everybody turned off their phones and put them in an onboard safe.

Then last summer, on a California coast drive, his daughters kept taking photos on their cell phones and sharing them

with friends using apps like Instagram and Snapchat. The big question he gets when choosing a family vacation spot is: “Will I have Internet there?” It’s clear -- no vaca-tion is complete without Internet access.

Martin took that message to Royal Carib-bean’s top management. He explained that today’s younger generation -- a growing market segment for cruise lines -- wants to share vacation experiences in real time.

Elea McDonnell Feit

Former Walton Professor,Knowledge@Wharton

Deviprasad Rambhatla

Head of Travel, Transportation& Hospitality, Wipro Ltd

Travel Industry Taps Technology To Win Over Customers

Technology is opening new ways for companies in the travel and hospitality industries to engage with customers, raise revenues, and streamline processes. Bill Martin, chief information officer at Royal Caribbean Cruises, former Wharton lecturer Elea McDonnell Feit and Deviprasad Rambhatla, Wipro Ltd head of the travel, transportation and hospitality unit, discuss the best approaches in this CIO Series article, produced by Knowledge@Wharton and sponsored by Wipro.

5

What followed is hoped to be a game changer for the $8 billion (2013 revenues) company, which runs 41 cruise ships calling on 490 destinations across 7 continents.Starting in late 2014, the investments Royal Caribbean began making two years ago to boost onboard Internet connectivity will come to fruition. Its newest ships -- Allure of the Seas and the Oasis of the Seas -- will have Internet bandwidth and speeds equal to onshore hotel locations, says Martin.

The Internet project is just one among several technology programs at Royal Caribbean. Another aims to employ data analytics to better understand customer preferences and extract more operational efficiencies. Its recently revamped website, for example, enables easier mobile phone access for browsing and reservations, with continual upgrades planned. A major overhaul of its reservations and pricing systems completed last year is enabling

new combination packages and pricing options.

To roll out the updated Internet, Royal Caribbean in 2012 tapped Harris CapRock, a connectivity specialist for remote envi-ronments, which collaborated with O3b, a provider of high-bandwidth satellite connectivity to “give our guests shore-like connectivity at fiber-like speeds,” notes Martin. He sees it as a big competitive advantage even over other land-based resorts.

The enhanced Internet connectivity will help Royal Caribbean find new ways to exploit analytics on customer preferences. For example, a new call center program supplies agents with key customer informa-tion, such as cruise trip frequency, room

Tapping Analytics

TRAVEL INDUSTRY TAPS TECHNOLOGY TO WIN OVER CUSTOMERS

6

WINSIGHTS Volume XX

class and dining preferences, onboard spending patterns and the like.

“In a cruise line there could be hundreds of customer touch points, and you have to think about whether or not you have good data on those,” says Elea McDonnell Feit, a lecturer at Wharton. She is also executive director of the Wharton Customer Analytics Initiative (WCAI), which helps companies leverage customer analytics.

Feit gets companies started by mapping their customer engagement process on storyboards, which helps them identify customer touch points, gather data around them, and use the business intelligence gleaned to improve customer offerings.

Taking a leaf from the casino industry, Feit says the first step there is to track custom-ers each time they play, using their “rewards cards.” The next step is to measure the data with appropriate systems. The third is to understand customer behavior patterns with analytics, and the fourth stage is to plan “interventions that could change the customer’s path.”

Feit notes that cruise lines could continue to

get data from their customers by engaging them even after they get off the ship. For example, they might offer each customer a free “My Vacation” page on their website. Here, customers could share vacation photos with friends and family and the company could then track the visitors. Deviprasad Rambhatla, head of the travel, transportation and hospitality services unit at Wipro Ltd, says such “social sensing” could provide useful analytics. Social sensing tracks customer behavior through social media platforms like Facebook, cell phones, online gaming consoles, and smart meters or GPS navigation tools in their cars.

In the travel and hospitality industries, roughly 45% of online customer visits are abandoned midway. Using analytics to understand behaviors more clearly, companies could better engage with cus-tomers and potentially convert 15%-20% of the abandoned transactions into sales, Rambhatla says.

Earlier this year, Royal Caribbean unveiled a website that makes it easier for prospec-tive customers to navigate its offerings, especially on mobile platforms like smart-phones and tablets. “That’s how you reach my kids,” says Martin, explaining that the younger generation prefers mobile devices to computers. In social media, the company has introduced features that allow custom-ers to enter ratings for different itineraries and pre-book onboard activities.

Revamped Online Presence

Mobility can help boost satisfaction scores by supplying crew members with data on customer preferences. You can see the customer’s delight when a crew member walks up to with a tablet and recommends his or her favourite drink.”

7

Technology Guideposts

Royal Caribbean also wanted to price services more efficiently. One solution: a “pricing and promotions” tool, unveiled in October 2013, which replaced a 20-year-old reservation system. Martin says the new system allows greater flexibility in target-ing customers with combined offerings. He is also working on a new reservations interface for travel agents.

As Royal Caribbean goes about its technol-ogy programs, Feit offers some words of caution, while Rambhatla points out new possibilities. In data analytics, it is vital for the CIO and the chief marketing officer (CMO) to collaborate, says Feit. “The CIO collects the data that helps the CMO see where there is a problem, but you can’t fix the problem without the CMO’s creativity in how to address the customer’s challenge.”

Companies tracking customer data must also decide whether they want to use “pas-sive or active” methods, says Feit. A typical passive method would be to track cus-tomers’ cell phone usage, usually without their knowledge. Feit advises companies to use active methods to gather data, say, by requiring customers to swipe their card on a machine to get their free towels on a ship deck. “You can run into privacy issues when it is not completely transparent to the customer that you are tracking them,” she says. Rambhatla agrees, and says most companies typically obtain customers’ consent on service agreements.

With processes set to prevent privacy viola-tions, mobility can help boost satisfaction scores by supplying crewmembers with data on customer preferences. “You can see the customer’s delight when a crew member walks up to with a tablet and recommends his or her favorite drink,” Rambhatla says, drawing from an airline client’s experience with analytics and mobility.

He also sees opportunities for hospitality companies to use broadband connectivity to power infrastructure management. For example, a cruise liner could use remotely managed services to run onboard network equipment, computers and even non-computing devices like air conditioners, generators and turbines.

With new speeds for surfing the Internet on the way, Martin now is keeping his “eyes and ears open for new ways of doing things.” He recently acquired Samsung’s latest Gear brand of “wearables” – watches and is testing ways that will allow cruisers to broadcast their experiences in real-time.

TRAVEL INDUSTRY TAPS TECHNOLOGY TO WIN OVER CUSTOMERS

Why ‘Big Bang’ Change Has No Place in Digital Transformation

Last September, Rakuten Bank in Japan launched ‘Transfer by Facebook’ - the first money transfer using Facebook1. The Facebook application is a little friendlier than a routine bank transfer – it comes with a communication tool allowing a message of up to 50 words to be sent with the transfer. A few weeks later, in October, French bank Groupe BPCE launched a cash transfer service via Twitter2.

1Chirag Patel (2014). Rakuten Bank Launched First Money Transfer Service via Facebook in Japan. [online] Let’s Talk Payments. Available at http://letstalkpayments.com/rakuten-bank-launched-first-money-transfer-service-via-facebook-japan/ [Accessed 16 Oct. 2014].

2Eileen Brown (2014). French bank Groupe BPCE launches Twitter cash transfer service. [online] ZDNet. Available at: http://www.zdnet.com/french-bank-groupe-bpce-launches-twitter-cash-transfer-service-7000034712/ [Accessed 16 Oct. 2014].

10

WINSIGHTS Volume XX

The bank’s mobile application allows French bank account holders to transfer a limited amount of money using Twitter without revealing account or bank branch details to the recipient. Banks that have traditionally operated from behind rock-solid walls of privacy and security are, like their customers, going digital. At the same time, new non-bank entrants such as Venmo and Apple Pay, are challeng-ing their core business. This disruption isn’t happening just with banks: we are witnessing the biggest shift in customer lifestyles and business models in the his-tory of mankind. Successful businesses will not transform themselves over night with a big bang. Their digital transforma-tion will be a journey over time through customer journey engineering, iteration, test and learn, and agile development. And each journey will be different with continuous evolution.

Digital evolution is giving rise to remark-able new ways of organizing businesses and addressing customers. Being digital is not about technology but rather about a lifestyle. The relevance of Facebook, the simplicity of Uber, the omnipresence of Google and others have set new ex-pectations and standards for experience in a digital age. Customers want their interactions and experiences with brands, governments and their employers to sup-port their new digital lifestyles.

In turn, businesses are busy trying to re-imagine their products, services, op-erations and business models from their customers’ perspective. They are now investing in creating better experiences

that are aligned with the digital lifestyle of their customers. The buzz is around “Digi-tal Transformation” – only, organizations may take months if not years to figure out what they should be doing and how they should go about it. And while they ponder over their Digital Transformation roadmap, the customer’s lifestyle will have evolved even further. We’ve gone past just simply talking about Digital Transformation in the face of these rapidly changing customer behaviors; it’s time to start getting it done.

It is therefore necessary to understand that Digital Transformation is a larger journey, unique to each business. It goes beyond enabling individual customer touch points such as websites, mobile devices and social platforms. A Digital Transforma-tion agenda works at the intersection of the front-end customer experience and the back-end digitization of the business itself (see Figure 1: Digital Transformation Agenda).

Digital Transformation also means keep-ing the customer informed and empow-ered and changing the way you serve the customer. For many organizations it also implies replacing large hierarchical structures with structures that are more customer centric in shape, digital in form and agile in behavior.

While customers are the reason for embarking on this digital journey, enterprise IT, marketing, operations and other

Digital Transformation Agenda

Avinash Rao

Global Head, Wipro Digital.

11

departments are the ones who need to make it happen. This requires change: moving from well-established and fixed processes to adaptive, iterative and agile ones.

How is a business to achieve this? How long will it take organizations to find and validate the new products or services that their customers want? We believe that this can be done rapidly – often in as little as two days. Two months or even two weeks may be too late. With the type of technology and specialist knowledge available, one can assemble everything and everyone in a room anywhere in the world, complete first hand research, come up with simple but highly creative solutions, go to market with them, build them and have customers use them in under three months.

It is important to be able to build engaging, customer-centric ideas quickly. Instead of giving customers a service that they have

to do (old school), we need to give them services they want to do (new school). Simple bank3 makes a good point of this. The all-electronic bank has no physical branches (it can be accessed online or via a mobile app) and provides powerful reporting of the customer’s saving and spend patterns. It then provides tools that enable better ways to save, budget and spend. These are products and services that go beyond what traditional banks

Digital evolution is giving rise to remarkable new ways of organizing businesses and addressing customers. Being digital is not about technology but rather about a lifestyle.”

WHY BIG BANG CHANGE HAS NO PLACE IN DIGITAL TRANSFORMATION

3Simple (2014). [online] Available at https://www.simple.com/ [Accessed 16 Oct. 2014].

CustomerExperience

CMO, CIO AGENDA COO, CFO & CIO AGENDA

Digitization

Hotspot

“Show up where the customer is at”

“Create seamless & amazing experiences along the customer journey”

“Drive online customer aquisition”

“Enhance cross sell”

“Develop deep insight into customer behaviour”

“Drive digital adoption across customer base”

“Digitize ‘channel to fulfilment’ through Business Service Redesign”

“Deploy new way of working in IT and Operations”

12

WINSIGHTS Volume XX

provide. But more importantly, the inter-action mechanism with customers is dif-ferent. Services such as Simple, Moven4. Rakuten Bank and Groupe BPCE are dis-rupting traditional ecosystems. They are doing this by digging deep into customer journeys and making their interactions relevant by bringing together strategy, technology and design.)

At the core of this approach is the ability to do what appears, at first glance, against the grain of popular level-headed think-ing: ignore best practices and big strat-egy. Instead, businesses must leverage micro-strategy that immediately delivers incremental change relevant to it. The idea is to implement and evaluate ideas quickly, in an iterative manner, throwing in design innovation, enabling technology and optimizing customer journeys as you go along. This means creating a highly adaptive and agile environment that is accustomed to ambiguity and which also supports multi-disciplinary teams.

Such an environment means working with engineers, customers, social anthro-

pologists, data scientists, user interaction specialists, regulatory experts, digital strategists, client IT and business teams. In effect, such a team that depends on real-time customer-relevant research and collaboration serves as a replacement for best practices. It has the powerful abil-ity to re-imagine products, service and process design to deliver value back to the customer.

Is this a risk-free approach? Not really. It takes vision, courage and a willingness to do things differently. Legacy systems, age-old organization models and yes, people, will likely challenge a new approach that requires broad-based change and new thinking. However, because it is an iterative process devoid of ‘Big Bang’ change, the risk is less, controlled and manageable. Businesses will ultimately discover that it is also a process that leads to remarkable breakthroughs. It quickly reveals how ef-fectively moments of truth are being dealt with. And finally, it is a process that is struc-tured around customer needs and therefore lends itself to rapid and successful market place adoption.

4Moven (1014). [online] Available at: https://www.moven.com/ [Accessed 16 Oct. 2014]

At the core of this approach is the ability to do what appears, at first glance, against the grain of popular level-headed thinking: ignore best practices and big strategy.”

13

Source: PwC 16th Annual Global CEO Survey

of global CEOs anticipate an increase in technology investment during 2014

21%

14

WINSIGHTS Volume XX

Does your employer ensure you can find parking easily at every company office you visit, regardless of the location? Nine out of ten people will respond with a “No” to that question (oh, you lucky tenth person!). But imagine this: you go for a meeting to an office other than your own and a simple swipe of your ID card (or even your driving license) at the company parking lot orga-nizes everything for you.

The parking lot system immediately recog-nizes you, directs you to the most conve-nient parking slot, hands you over to the office management system which looks up the available meeting rooms on the campus, provides you the best fit options for meeting rooms on your mobile, lets you select the room you want and automatically updates

the calendar of your colleagues, sending them a message using presence-sensing technology with details of the conference room to head for. Technology has triumphed by making everything happen smoothly. It has helped you move from our existing system of permissions and reservations to a system of direct consumption without human intervention. In the background, multiple systems and networks hum away, orchestrating a series of business rules and access control processes.

This everyday scenario tells us how work-places need to transform in order to en-sure customer delight. Anyone who has struggled to find parking – and who hasn’t – knows that solving this problem will result in happier employees. Let’s abstract this simple scenario for its implications:

• IT can be used in ways that are yet to conceive in order to improve productivity.

• The Internet of Things (IoT), where ev-erything is connected, is reshaping where IT is being deployed and how it is being consumed by organizations.

• IoT is a potent reality that can be har-nessed to transform the organization and deliver a great experience for internal cus-tomers as well.

Atul Sood

Vice President, Advanced Technologies & Solutions, Wipro Ltd

Internal Customers: The Litmus Test for Digitization

In a digital world, organizations cannot continue to consume IT in traditional ways and yet hope to succeed - they must transform their workplace along with their processes or perish.”

15

It is a well-known fact that when organi-zations increase the supply of happiness in the workplace they boost satisfaction, creativity and productivity to improve bottom lines. Researchers have found “strong evidence of directional causality between life satisfaction and successful business outcomes.”1 Organizations are

noting these needs of employees – who constitute their internal customers -- and are acting on them.

A recent article in the Harvard Business Review (HBR) put it well, “The buildings we go to every day haven’t changed as much as the tools we use to get work done.

INTERNAL CUSTOMERS: THE LITMUS TEST FOR DIGITAL TRANSFORMATION

Why Transform For The Internal Customer?

1Positive Intelligence, HBR, January-February 2012: http://hbr.org/2012/01/positive-intelligence/ar/1

16

WINSIGHTS Volume XX

Merging digital communication patterns with physical space can increase the prob-ability of interactions that lead to innovation and productivity.”2 Looked at another way, in a digital world, organizations cannot continue to consume IT in traditional ways and yet hope to succeed. Organizations must transform their workplace along with their processes or perish. More importantly, if you can’t transform the workplace for in-ternal customers, chances are you are even less likely to do it for external customers.

There are three forces underlying the digi-talization of organizations. Understanding these forces makes it simpler to recognize the inevitability of going digital:

Globalization: Employees, vendors, partners and customers are every-

where. Data is crisscrossing digital high-ways and if you are not tapping into this digital data stream you are already losing ground. As an example, today when a salesperson wants to meet a customer, he looks up social media sources before the meeting. No organization can afford to ignore the powerful digital information that is waiting to be tapped.

Personalization: Employees are customers; we need to stop thinking

of them as ‘users’. Just as an organization works at personalizing customer-facing experiences, an organization must per-sonalize employee-facing experiences. Let the digitalized organization present an environment that is suitable for a range of diverse global business, cultural and physical needs of employees.

Collaboration: The workplace is becoming complex; calling for hyper-

specialization. It requires a number of specialists to work together. You need a platform where such teams can collaborate. The HBR article provides an example of a pharmaceutical company where a team responsible for US$1 billion in annual sales found that when a salesperson increased interactions with a coworker in other teams by 10%, his or her sales also grew by 10%.3

With such compelling evidence, where are organizations faltering in their plans for digitalization? The difficulty resides in pockets within an organization. These pockets – such as traditional IT provisioning and outmoded organizational structures -- resist change. For decades these very pockets have been nurtured and strength-ened to become the supporting pillars of business. However, with radical changes in society, technology and customer expec-tations, they need to be re-looked at and re-engineered. The innards of organizations need to respond to these changes in ways that are as yet unfamiliar.

The first organizational pocket impeding change is the way IT has been traditionally

Aligning With New IT Consumption Patterns

2 Workplaces that Move People by Ben Waber, Jennifer Magnolfi, Greg Lindsay, HBR, October 2014: http://hbr.org/2014/10/workspaces-that-move-people/ar/13 ibid

17

INTERNAL CUSTOMERS: THE LITMUS TEST FOR DIGITAL TRANSFORMATION

provisioned. In the past, a small and exclu-sive geek sect (call it the IT Department or the CIO’s Office) set the rules and told the organization what was best for it. This was with good intent. Others did not question this set of organizational IT czars.

Today, users – or more appropriately, ‘inter-nal consumers’ – don’t want to be limited by what the organization’s IT system has to offer. Their markets have evolved, their lifestyles and work methods have evolved and the technology they use in their per-sonal lives has evolved.

Therefore, today’s employee needs to be empowered to select the right tools at the right time, autonomously, in order to improve productivity. Digitalization of orga-nizations is a way to ensure that employees, regardless of their relative position within the organization, have the right set of per-missions and can independently select the tools they want to use at a given moment.

Fortunately, for organizations struggling to keep pace with change, the world is becoming hyper-connected. The IoT is connecting all kinds of sensors, devices, people, databases and analytical engines to go beyond our current notion of con-nectedness which is somewhat limited to desktops, tablets and smart phones.

Data is becoming freely and instantly avail-able and this can be transformational. It can be leveraged to impact customer exper-

ience and also improve operational pro-cesses and business models that support organizations. For example, the IoT can ac-celerate onboarding or training processes, thereby resulting in a faster response to changing markets. This is a compelling reason to consider end-to-end digitaliza-tion of the organization.

The last among the impediments to change is organizational structure. Traditional hierarchical structures have evolved, keep-ing roles and responsibility as the basis, making it painfully slow for people to switch roles or assume different responsibilities. In some instances, these structures have been replaced by the more bureaucratic ‘T’ shaped structure, with individuals demon-strating varying levels of specialization. But neither of the structures solves the problem of collaboration. The reason for this is not difficult to unearth: knowledge and infor-mation travelled slowly, inefficiently and sometimes incoherently between nodes of either structure. This had a negative

Leveraging a Connected World

Creating Innovative Organizational Structures

Just as an organization works at personalizing customer-facing experiences, an organization must personalize employee-facing experiences.”

18

WINSIGHTS Volume XX

bearing on the pace at which organizations could change.

Today, with digitalization, real time data and information can be used to re-structure organizations, making teams behave as if they were part of neural networks that organize and re-organize themselves based on data signals. In business environments where change is rapid, being able to re-structure the organization can make the difference between survival and extinction. Only digitalization can be the backbone for innovative and successful re-structuring.

Creating the perfect customer experience – such as in our example of providing park-ing, meetings rooms and automated calen-dar updates to employees – is crucial for efficiency and success. The forces that are driving the heightened quest for superior customer experiences are globalization, the demand for personalization and the need for collaborative environments in a hyper-specialized world. For organizations to be truly ahead of the curve, they first need to align with new IT consumption patterns, leverage a hyper-connected environment and seek out innovative organizational structures that enable and support the change. Success with implementing these changes within the organization will be the litmus test for how prepared it is to address the external customer.

The Comprehensive View

“When we moved our offices recently, we decided to radically change employee experience. In our new facility we got away from closed-door offices and cubicles to create a much more open layout. When coupled this with more than ample meeting spaces, we essentially went from “my space” (cubicles, offices) to “our space” (closed meeting rooms) and “our space” to “any space” (open and casual collaboration areas). Technology was the key to make this transition happen smoothly and success-fully. We extensively used Wi-Fi networks and obsessed about not using wired connections. We even got rid of all of our desk phones completely. Writable TVs, digital check-in kiosks for meeting rooms, reconfigurable meeting pods and standup col-laboration areas are few of the things we have done in our new facility. With all of these radical changes, employees reported that their work environment experience has certainly improved and they love the new-age, startup like work environment we created for them. And this is just the beginning, we plan to continue to utilize technology to create an even seamless work environment experience for our employees”.

Starting today, the spotlight is on “Customer Centricity”, enabled through workplace empowerment. What makes this possible is globalization enabled by a digital “flat” world. In many digital or-ganizations, Customer Support, IS&T and professional services for global customers are run from remote, but connected knowledge hubs. Product R&D teams and Innovations Centers collaborating globally to bring powerful ideas to life, is a strong testament to the fact that employees are digitally enabled to work from anyplace, anytime, and deliver business value on the move. Today, employ-ees can be as close to customers, irrespective of their physical location and this to me is a great advantage of the digital world!”

WorkplaceTransformation

Tarun Sharma

VP R&D, Head BMC India and Ukraine

Suhas Kelkar

VP & Chief Technology Officer (APAC) BMC

SPECIAL FEATURE

21

Alexis Samuel

Global Managing Partner, Wipro Consulting Services,

Wipro Ltd

Kris Denton

Managing Partner, Americas, Wipro Consulting Services,

Wipro Ltd

Exactly what is your organization capable of creating? The answer to that question is a moment of profound truth.

Most executives will instinctively declare that their organizations are able to produce goods and services for which they have proven competencies with relative ease. This does not explain why several pres-tigious Swiss brands that manufactured watches in an industrial era collapsed in the face of competition from Japanese digital and quartz watches. Or why a com-pany like Kodak that dominated the global photography market for decades sank helplessly when digital photography took off. One of the reasons businesses fail to launch successful new products, even if they are leaders in the segment, is that their legacy businesses have become intracta-bly complex. Change is slow, demanding and, sometimes, devastatingly difficult. As history demonstrates, it can even spell the end of brands that have dominated markets for decades.

Businesses are now realizing the impor-tance of simplification in the businesses, channels, product clusters, measurements, regions, processes and tools they use in order to reduce risk from technological ad-vances, demographic changes, economic

shocks, regulatory and environmental issues.

In retrospect, as a company grows each decision appears sound. But with every subsequent addition, these decisions, solutions, products and services add to complexity. Soon, one end of the organi-zation doesn’t know what the other end is doing. Response lags are high and decay sets in. This is the point at which new busi-ness ideas emerge but the cost of change is inordinately high.

Organizations face a number of questions that need a clear response before change can be initiated on a regular basis to re-main nimble:

• What revenue will the new product gen-erate? What does the financial analysis of the product; customer and supply chain tell us? What are the marketing, pricing and service requirements of the product? • What are the Transport, Finance & Ac-counting, and HR costs associated with the product?

• Which brands/ products must be retired in order to make way for the new product?

• Which products must co-exist? How will older products be managed?

Rapid Change: How Simplification Can Make It Simple

RAPID CHANGE: HOW SIMPLIFICATION CAN MAKE IT SIMPLE

The Logical Response to Complexity

22

WINSIGHTS Volume XX

• Which are the distribution channels that an organization must migrate to so that the new product is a success?

• Which change management practices are required to deliver sustained success?

These are difficult questions to answer. But it remains equally true that there is no good substitute for the reality that successful business transformation requires a holistic approach. The simpler the organization’s structure, processes, measurement metrics and resource allocation mechanism, the faster it can respond to opportunities and market changes.

What is the path an organization must adopt for transformational simplification? Today, digital is emerging as one such strategy that can lead to simplification and help organizations navigate safely to their goals.

Simplification by design is a precursor to an effective journey towards becoming a digital enterprise. This has two imme-diate and obvious outcomes. First, con-flict between actions becomes minimal, thereby eliminating decision deadlocks.Second, simplification allows lean and ag-ile initiatives to realize their full potential.

Simplification allows organizations to go back to the drawing board as often as necessary to re-structure, re-create and re-design themselves and meet unfore-seen challenges. But for this to happen, processes and operational strategies have to be streamlined before going digital (see Figure 1: Value Delivered). When this is not done, there is always the danger of staying misaligned with the enterprise at large.

The irony is that simplification itself isn’t as easy as it sounds! Take the case of a baby food company that has invested years – if not decades – in contracting premium shelf space in retail outlets. Today, it needs to supplement that with a presence in digital market places such as Amazon and eBay. There are enor-mous differences in the two channels. For digital, the baby food company must jockey for a number of new business components. These range from the right display on web pages to lower pricing for online distribution and a completely new shipping model.

With this in mind, an organization is forced to answer a new set of questions:

• Is the digital presence easily discover-able by customers?

• Does the digital display (and information availability) drive customer decisions?

• What are the new user journeys?

Taking A Holistic Approach To Transformation

Simplification Is Not As Easy As It Sounds!

In retrospect, as a company grows each decision appears sound. But with every subsequent addition, these decisions, solutions, products and services add to complexity.”

23

RAPID CHANGE: HOW SIMPLIFICATION CAN MAKE IT SIMPLE

Fig

ure

1: V

alu

e D

eliv

ered

* B

usin

ess

Pro

cess

Exc

elle

nce

| B

usin

ess

Per

form

ance

Man

agem

ent

| E

nter

pris

e P

erfo

rman

ce M

anag

emen

t |

Ent

erpr

ise

Ris

k M

anag

emen

t |

Ser

vice

Inte

grat

ion

and

Man

agem

ent

VA

LUE

DE

LIV

ER

ED

Fin

anci

al a

naly

sis

& u

nit o

f w

ork

driv

en p

roce

ss

targ

etin

g he

lpin

g yo

u al

ign

busi

ness

dr

iver

s to

bus

ines

s pr

oces

ses

Sys

tem

atic

app

roac

h le

vera

ging

dat

a dr

iven

tran

sact

ion

anal

ysis

& p

roce

ss

min

ing

Tre

atm

ent

stra

tegi

esus

ing

leve

rslik

e pr

oduc

tivi

ty,

was

te, v

aria

tion

re

duct

ion,

au

tom

atio

n us

ing

*bpe

, bpm

, epm

, er

m,

agile

, six

si

gma,

le

an, s

iam

Act

iona

ble

road

map

and

pr

ogra

m

man

agem

ent

supp

ort

Enh

ance

mar

ket

Res

pons

iven

ess

& p

ace

ofch

ange

Cre

ate

foun

dati

onF

or b

usin

ess

Res

ilien

ce

Sha

rpen

proc

esse

s F

or e

nhan

ced

Tec

hnol

ogy

enab

lem

ent

Cla

rify

bus

ines

sm

odel

for

shar

edse

rvic

es c

ente

r /

glob

al b

usin

ess

Ser

vice

s

Str

engt

hen

base

line

for

Vir

tual

izat

ion,

B

usin

ess

proc

ess

Out

sour

cing

Red

uce

cost

&

Com

plex

ity

for

Org

aniz

atio

nal

chan

ge

24

WINSIGHTS Volume XX

• What are the new exception paths?

• Do the services associated with the digi-tal channel meet customer requirements with regard to SKUs, payment methods, delivery timelines and service requests?

• What are the new backend processes and operations required?

• What are the existing processes that need to be combined?

• What is the organizational change management effort required?

By now it is amply clear that digital de-mands are different from that of traditional businesses. However, those undertak-ing the simplification exercise should be wary: the exercise should not get waylaid by headcount reduction objectives, else the agenda will get misdirected; and it is important to first decide what part of the business would benefit most from simpli-fication of processes.

This is where sound financial analysis plays a key role. Simplification, improvement and investments must be clearly linked back to bottom line growth. The danger is that sim-plification of processes can get confused with the lowest common denominator of standardization. Commonality in processes for different products/ services, market segments and channels are important but it is essential to also maintain points of differentiation.

Commonality and differentiation do ap-pear to be conflicting. Can an organization do a balancing act so that both can exist within the same framework? Our experi-

ence says they can if an organization maps its simplification strategy with customer journeys. Simplification then automatically becomes a means to deliver consistency in treatment of processes. The challenge, therefore, before organizations is to build resources and a knowledge base that enables consistent delivery.

Organizations are often puzzled by the fact that despite major investments in simpli-fication, the initiative fails. The failure can be attributed to:

Poor understanding of customer journeys. Organizations don’t spend

time and effort on the actual rendition of processes at the customer touch point. They fail to offer customers intuitive, flex-ible, customizable and contextual rendi-tions in order to make their decision-making process simple and quick.

Conflicting objectives of the exercise. Organizations confuse simplifica-

tion with headcount reduction and lose their way.

Organizational change management has hiccups. New digital processes

have differing levels of impact on exist-ing functions/ users. The impact is inad-equately assessed and managed, leading to several failures in meeting customer expectations.

Plans for sun setting existing pro-cesses are unclear and imprecise.

There are no time-bound plans for sun

Preventing the Failure of Simplification

25

setting redundant processes. It is unclear how long old processes will co-exist with newer ones, thus adding to confusion, costs and inefficiencies.

In addition to simplification of processes, organizations need expert guidance on where a particular process must be done. This is to ensure cost efficiencies and to bring the highest available skill levels that contribute to the overall simplification strategy.

The point about where – and by whom -- a process is executed needs emphasis. The resources that execute processes can add considerable value to business outcomes. An organization will often iterate the activi-ties that need to be performed along with a workflow. This can be supplemented by automation. Unfortunately, organizations continue to remain primarily focused on transactions and not on knowledge as a lever of completing a process.

This is illustrated in the easy-to-understand banking process of loan origination. The starting point for all loans is marketing which helps locate and funnel potential customers. When a sufficient number of applicants are delivered by marketing, the applicants get analyzed and evaluated along several parameters such as credit history, employment and educational back ground. But the ‘Yes/ No’ decision to grant the loan is a moment of truth – it requires expertise, something that does not easily lend itself to business rules. There is an element of judgment involved in the deci-sion which lines of code and a computer cannot spit out. This is a critical knowledge step. There is cost and complexity involved in this process. But organizations tend to

view this step as purely knowledge base-dependent. This creates the tendency totask knowledge workers with other duties and responsibilities.

It is easy to see that the total cost of the loan is being masked by the way it is being managed. Could this be done by lesser skilled workers? Can Enterprise Perfor-mance Management (EPM) be combined with Business Process Management (BPM) to accurately measure total cost of the process? And therefore reach financially sound decisions on how the process must be simplified and where it must be executed to maximize returns?

Simplification must be measured across three dimensions: adoption, effectiveness and the efficiency it creates. When these metrics are used to assess the impact of simplification, organizations can auto-matically expect to be headed in the right strategic direction.

Those undertaking the simplification exer-cise should be wary: the exercise should not get waylaid by headcount reduction objectives, else the agenda will get misdirected.”

RAPID CHANGE: HOW SIMPLIFICATION CAN MAKE IT SIMPLE

26

WINSIGHTS Volume XX

Kumudha Sridharan

Vice President & Global Head of Testing Services,

Wipro Ltd

In an Everything-Digital environment, busi-nesses must stress on operations that provide accurate, rich and engaging digi-tal content, and distribute it satisfactorily across channels to improve accessibility coupled with a high-end user experience. This translates into an inordinate focus on infrastructure and application performance, process optimization and stability, usability, design, functionality and security. Together, these deliver what every organization wants: digital assurance.

Digital assurance is vital. It makes a more-than-significant difference to business performance. For example Shopzilla, one of the largest online retailers, unlocked a 7-12% increase in revenue through a 5 second speed up in page loads. The speed up resulted in a 25% increase in page views, leading to improved revenues and a 50% reduction in hardware deployments.

Staples redesigned its website to make it easier for customers to place orders, thereby increasing the likelihood of repeat purchasers. Staples reported that repeat customers had increased from 180,000 to 300,000 over a single quarter after the new design had been tested1.

Digital Assurance

1Michael Wang. Real Usability Success Stories [online]. Great Web Design Tips. Available at: http://www.great-web-design-tips.com/web-usability/78.html [Accessed 13 Nov. 2014].

27

In addition, speed is of the essence. In 2013, during a 34-minute blackout at the Super Bowl, Oreo sent out a Tweet that said, “You can still dunk in the dark.” Some believe that the Tweet resulted in better customer response than the actual Oreo Super Bowl ad that had a multimillion dollar budget2 For Digital Marketing to be agile, systems need to be continuously tested and kept on the ready for a response on scale, else opportunities can be lost.

What this tells us is elementary but often overlooked: digital businesses can achieve considerably more with greater ease than traditional businesses -- but they are also vulnerable to multiple points of failure.

Today industries across the globe are le-veraging innovations in digital technology to reinvent and transform their businesses. They bank on an omni-channel strategy for deeper market penetration. And they use digital content to effectively market their services and products and provide great customer engagement through digital user experience.

The challenge is to do this seamlessly and consistently across platforms, operating systems and device form factors – all of which continue to evolve. In addition, content itself is growing in velocity and formats. Today, rich streaming content is the norm, digital decoupling is being emp-

loyed for effectively managing digital mar-keting operations, and devices and con-sumer actions are unleashing a flood of data that must be assimilated, validated, crunched and put into the feedback loop of businesses. There is no room for error.Testing infrastructure, applications, pro-cess, usability and design, functionality and system security using standardized tools is an effective and essential method to create digital assurance. This insulates systems from unexpected failure.

The strategy of rigorous testing is relevant to internal, employee-facing applications as much as it is to external customer-facing applications. Businesses must therefore ensure they have a 360 degree test strategy that prevents failure at both levels.

Today industries across the globe are leveraging innovations in digital technology to reinvent and transform their businesses. They bank on an omni-channel strategy for deeper market penetration.”

2Oreo’s Super Bowl Tweet: ‘You Can Still Dunk In The Dark’ [online]. The Huffington Post. Available at: http://www.huffingtonpost.com/2013/02/04/oreos-super-bowl-tweet-dunk-dark_n_2615333.html [Accessed 13 Nov. 2014].

DIGITAL ASSURANCE

28

WINSIGHTS Volume XX

Source: Adobe Digital Distress Survey 2013

of staff believe senior management’s digital knowledge is average or less

65%

29

There is something major afoot in the banking business. The organization hav-ing the largest mobile payments user base is not a financial institution. It is a place where consumers go for their daily coffee fix – Starbucks. According to data1 the Starbucks mobile application accounts for 15% of the transactions made in its stores. Today, when Joe Anybody wants to know: “what is the exchange rate between USD and JPY” he is more likely to type that query into a search engine box than go to his bank site.

Why? Because today’s customers are experience oriented and demands con-venience. They have been exposed to a world where a Google Now can pop-up a notification message that alerts them that their package has been shipped with the current commute time home.

Banks have been observing and learning from this – especially the neo (new) banks and digital banks.

In the US, Moven has created a mobile-only offering that provides instant feedback2 on spending in order to help consumers with their finances. Similarly, Bank Simple (“Simple”) provides its customers smarter ways to set goals and track budgets.3 GoBank is focused on customers who

traditionally eschewed formal banking. It is redefining banking with mobile pro-pelled prepaid accounts and clear fees. The distribution mechanism for GoBank is Walmart with its 4300+ stores. ING Direct has demonstrated in multiple geographies that customers love a simple product that offers them attractive rates and is backed

1John Heggestuen (Sep 5, 2014). An Inside Look At The Starbucks App, The Most Successful Mobile Payments System In The US. Business Insider India. Available at: http://www.businessinsider.in/An-Inside-Look-At-The-Starbucks-App-The-Most-Successful-Mobile-Payments-System-In-The-US/articleshow/41807776.cms [Accessed 11 Dec. 2014] 2A Traffic Light For Your Spending (Aug 26, 2014). YouTube. Available at https://www.youtube.com/watch?v=ecgMEXyt_6U [Accessed 11 Dec 2014]3Rachel Giuliani (Jul 25, 2013). 3 Steps to Simplifying your Financial Life with Goals. Simple. Available at https://www.simple.com/blog/3-steps-to-simplifying-your-financial-life-with-goals [Accessed 8 Dec. 2014]

Rajan Kohli

Sr. Vice President & Global Head of Banking & Financial

Services, Wipro Ltd

Sushankar Daspal

Practice Head, Digital & Mobile Channels, Banking,

Wipro Ltd

DIGITAL - THE NEW CURRECY

With increasing product complexity, banks have been forced to increase their marketing spends and in campaigns that help their customers understand the associated risks, costs, lock in periods and returns.”

Digital – The New Currency

Lessons for traditional banks on using technology to engage customers

30

WINSIGHTS Volume XX

by great service. If it means that they have to do everything online, so be it.

There is nothing new about online and mobile banking. So, what has changed between the traditional and neobanks? For traditional banks, online and mobile banking was an “add on” channel. But neobanks such as Moven, Simple, GoBank, ING Direct, Jibun and Ally Bank have built digital businesses from the ground up. Many of these banks do not have a physical branch. Their point of delivery is digital -

online and mobile. Social engagement is integrated into their processes.

Neobanks have leveraged technology ef-fectively to service a growing generation of technology-savvy customers. Central to this use is how they re-imagined the entire customer journey, taking cues from fields as diverse as social media, airlines, retailers and ecommerce implementations. The customer’s end objective guides the journey and all extraneous distractions have been removed.

The neobanks and digital banks excel in helping customer use the small segments of free time. They have mastered the art of structuring products so that they can be explained without a human interface.”

31

Time is Money: Simplification for Sustainability

Traditional banks pick up the gauntlet

What is important is the simplicity of their products, services, processes and touch points. They focus on helping customers achieve their financial goals via advisory and planning and ensuring that custom-ers are not surprised by unexpected fees. These aspects - the astute use of tech-nology, product simplification and fee transparency – are of major concern to traditional banks.

In recent years, with interest rates going down, banks have introduced increasingly complex savings and investment products. These products offer financial capabilities that were restricted to selected clients earlier and came with associated fees and complexity.

On the other hand, digital and neo-banks have aggressively differentiated themselves from traditional banks by creating simple products.

Customers can validate from the online / mobile sites that these products are meant for them. They have access to calculators (for projected returns, fees, etc.) as well as online and video chat with bank repre-sentatives. Once convinced, they open an account – start to finish - without visiting the branch. The neobanks / digital banks excel in helping customer use the small segments of free time for research or for transactions.

Neobanks have mastered the art of struc-turing products so that they can be ex-plained without a human interface. They

have supplemented this by designing customer journeys, technology imple-mentation and processes that complete a transaction in a single easy continuum. The implication of this on traditional banks is straightforward: operating models, prod-ucts, services and IT infrastructure and applications have to be re-calibrated.

The Travelers Checks market offers insights into the change. This market has been in secular decline over the last 5 years with prepaid travel cards and credit cards taking the place of the Travelers Check.

The sharing economy has also caught up. A service from WeSwap enables travel-ers from different countries to directly exchange cash with each other and com-pletely bypass the current banking and bureau-de-change system.

Some traditional bank executives proph-esize that neobanks are doomed because they lack some of the key attributes of traditional banks: product scope, security and privacy. Without these how can a neobanks aspire to become the primary bank across the household?

There is some truth in this argument. The largest of these neo-banks have customer bases in the six digits as compared to the millions of account holders in traditional banks.

For some neobanks people have been waiting for months to get an invitation to sign up. Others lack simple capabilities

DIGITAL - THE NEW CURRECY

32

WINSIGHTS Volume XX

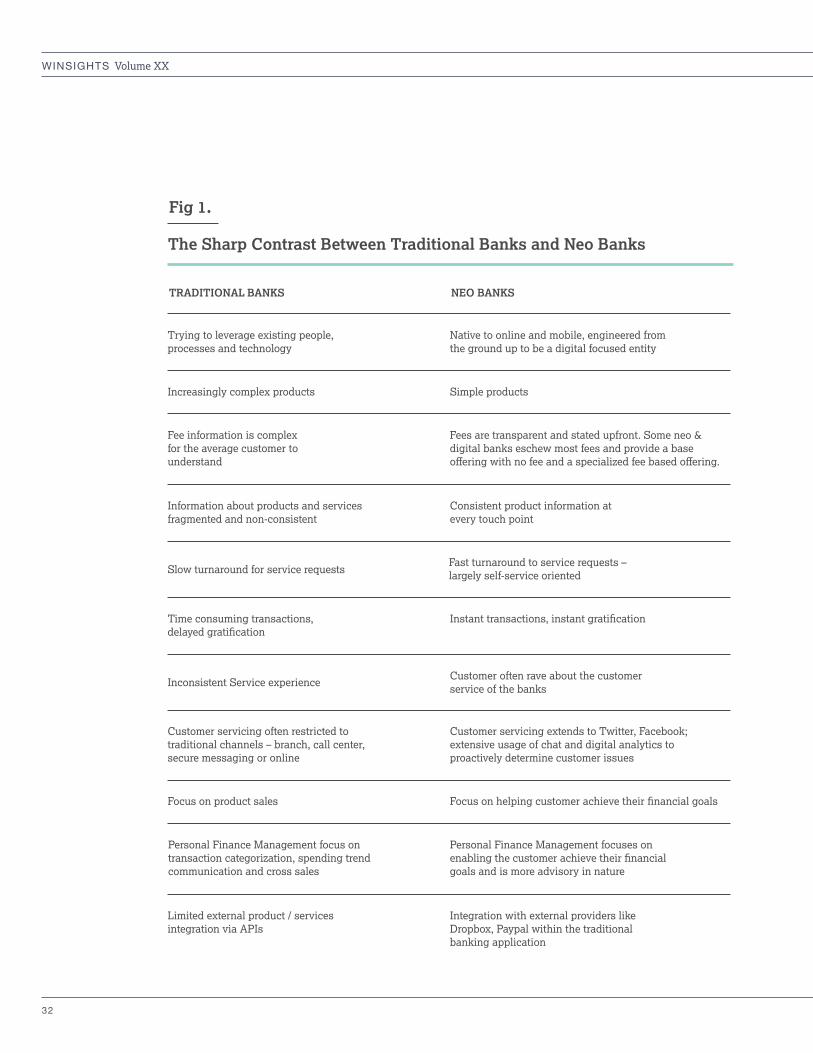

Fee information is complex for the average customer to understand

Fees are transparent and stated upfront. Some neo & digital banks eschew most fees and provide a base offering with no fee and a specialized fee based offering.

Trying to leverage existing people, processes and technology

Native to online and mobile, engineered from the ground up to be a digital focused entity

Information about products and services fragmented and non-consistent

Inconsistent Service experience

Personal Finance Management focus on transaction categorization, spending trend communication and cross sales

Consistent product information at every touch point

Customer often rave about the customer service of the banks

Personal Finance Management focuses on enabling the customer achieve their financial goals and is more advisory in nature

Increasingly complex products Simple products

Slow turnaround for service requests

Customer servicing often restricted to traditional channels – branch, call center, secure messaging or online

Limited external product / services integration via APIs

Time consuming transactions, delayed gratification

Focus on product sales

Fast turnaround to service requests – largely self-service oriented

Customer servicing extends to Twitter, Facebook; extensive usage of chat and digital analytics to proactively determine customer issues

Integration with external providers like Dropbox, Paypal within the traditional banking application

Instant transactions, instant gratification

Focus on helping customer achieve their financial goals

TRADITIONAL BANKS NEO BANKS

The Sharp Contrast Between Traditional Banks and Neo Banks

Fig 1.

33

like Joint Checking accounts. If a customer wants extensive cash operations, the con-venience of a branch is missing from these neobanks. From a product offerings per-spective many neobanks limit themselves to CASA and CD accounts – but, some digital focused banks like ING Direct and USAA offer the full spectrum of products to their customers.

However, from the point of view of security and privacy it is worth noting that neobanks are architected to withstand cyber-attacks and can therefore manage the online/ mo-bile environment better. Neobanks monitor and know when they are being attacked while traditional banks discover they were attacked after the damage has been done as they have built online/mobile banking as an ‘add on’.

Traditional banks also face the challenge that their digital offerings depend on their current legacy systems and processes for fulfillment. These put limits on their flex-ibility. In order to get around this some banks have taken hard choices and offer digital-only products. These products are streamlined and devoid of the complex rules that hobble legacy and grandfathered products. Often, these products are pro-cessed on independent product systems architected for flexibility.

There are other initiatives that traditional banks are taking up. A bank in Poland - mBank - shows the reinvention of a tradi-tional bank. mBank is a part of BRE Bank SA and a member of the Commerzbank Group. In order to get a competitive dif-ferentiation from other Polish and regional banks in Czech and Slovakia it focused on creating the next generation online bank.

DIGITAL - THE NEW CURRECY

34

WINSIGHTS Volume XX

mBank has rebuilt itself on four new pil-lars of Real time Digital Marketing, Direct Banking (reimagined customer journeys, video chat, PFM); mobile banking (including location based services and mobile pay-ments); and Social Engagement (including Gamification, P2P and Facebook applica-tion). It has implemented a Google-like Instant Search for transactions. Money can be transferred to Facebook friends. Leaderboards show how the customer’s savings stack up against others.

The changeover has been so successful that mBank is now becoming the primary brand for the group.

In India which has 100mn monthly active Facebook users4, ICICI Bank is leading the way with Facebook banking. This feature provides customers a secure way to access their banking information from Facebook. In another strategy, a “traditional bank” - BBVA - has acquired Simple for a sum of US$110mn. This is estimated to be about $12005 per account – much higher than the traditional account acquisition metrics of US$200 per account. Simple will run as an organizational unit parallel to the BBVA US.

Research shows that traditional banks are better off going outside to power their in-novation with 72% of survey respondents6 feeling that new market entrants are driv-ing innovation and 52% of respondents7 concerned that legacy business models are inhibiting innovation. This report also highlighted that banks are better off part

nering (76% respondents in favor) outside8 to create the innovation engine.

It is only a matter of time before traditional laggards discover that the gap between them and the new banks has become a threat to sustainability. But the promise of digital is not limited to new entrants. Traditional banks must become customer focused, map their customer journeys and begin to build products and services that can be distributed, sold and managed in a market that is dominated by digital. There are an adequate number of successful examples for traditional banks to emulate.

Why?

Banking on The Future

The difference is significant enough to make CEOs of traditional banks ponder over the question, “Am I doing enough for my organization by way of digital transformation?”

4Here’s looking at you, India. Business Today. Aug 17, 2014, Vol. 23 Issue 16, p46-54.5Jim Bruene (Feb 24, 2014). Why the BBVA Simple Bank Deal is Extraordinary. Available at: http://www.netbanker.com/2014/02/the_importance_of_the_bbva_simple_deal.html [Accessed 11 Dec 2014]6The Payment Innovation Jury Report 2013, Available at http://thefinanser.co.uk/files/129683968-payments-innovation-jury-report.pdf] [Accessed 11 Dec 2014] 7Ibid.8Ibid.

35

Source: 2013, Connecting with Customers Report, LivePerson, Inc.

of companies say that they expect to appoint a Chief Digital Officer

Within the next twelve months

19%

36

WINSIGHTS Volume XX

Srini Pallia

Chief Executive,Retail, Consumer Goods,

Transportation & Govt.

Digitize or Perish

You have watched Julianna Margulies’ character Alicia Florrick on The Good Wife1 almost transform into a politician, donning those glorious suits. There is one suit she wears – muted, chic -- that you especially like. You want to wear it for your next C-suite meeting. You do have a couple of options. You could check Pradux2 or dozens of other similar sites that feature thousands of outfits worn by

stars in sitcoms. Or you could even use a mobile app like the one provided by StyleID3 to search for the clothes you just saw and buy them. Product placement in TV shows was estimated to be a US$8 b industry in 2012, with over 75 percent of US prime-time shows placing products in their episodes4. The effectiveness of product placements can be multiplied several folds by digitizing the customer’s subsequent path-to-purchase. In today’s digital universe, it is possible to completely

New Customer Journeys

37

automate the aspire-research-discover-select-buy process instead of depending on intrusive 1-800 numbers (or even QR codes) appearing on the screen each time a product is shown.

One approach to do this is to embed signals (inaudible to human ears) into the televi-sion episode at points when products are shown. These signals are recognized by an app on the viewer’s mobile device. Based on the signal, the app can automatically pull up the right products, price, colors, sizes, availability, and the various ways to place an order. The viewer can simply tap ‘Save’ for later action or hit the ‘Buy’ button on the app to complete the transaction using pre-stored credit card or bank account details. The viewer could also tap the 1-800 number alongside the product to interact with a service agent. In essence, there is a seamless handover from the television episode to the mobile device and to the e-commerce portal and payment methods.

At the core of this new customer experience is digital transformation. For an increasing number of Retail and Consumer Goods (CG) organizations, Digital Transformation can spell new products and capabilities, new markets, new customers, new points of purchase, new businesses and improved efficiencies; this, in addition to providing existing lines of business a major shot in the arm. Digitizing business processes, operations, supply-chains and customer-facing touch points is providing the tailwind retailers and

CG organizations need to acquire strong leadership positions. A recent 2014 study conducted by Forbes Insights in partner-ship with Wipro Technologies called The race is on5 found that one out of five CG executives, 20%, describe their digital marketing approach as “transformative.”

The study says that these are leaders that have already embraced a broad array of digital strategies: social, mobile, web and analytic tools and technologies transform-ing not only sales and marketing but also

DIGITIZE OR PERISH

In a business where product lifecycles are shrinking and competitive advantage belongs to those who respond in real time, there can be no argument against Digital Transformation.”

1The Good Wife (2014). The Good Wife stars Emmy Award winner Julianna Margulies as Alicia Florrick, a defense attorney. [online] CBS. Available at: http://www.cbs.com/shows/the_good_wife/ [Accessed 23 Oct. 2014]

2[online] Pradux. Available at http://www.pradux.com/ [Accessed 23 Oct. 2014]

3[online] StyleID. Available at https://www.styleid.info/ [Accessed 23 Oct. 2014]

4Stephen Genco, Andrew Pohlmann, Peter Steidl (2013). Neuromarketing for Dummies. [online] Google Books. Available at http://bit.ly/ZOpJiO [Accessed 23 Oct. 2014]

5Forbes Insights-Wipro Technologies (2014). The Race Is On. [online] Wipro. Available at http://www.wipro.com/microsite/consumer-goods-transformation/ [Accessed 23 Oct. 2014]

38

WINSIGHTS Volume XX

the overall business. The study shows thatrelative to Europe (14%), executives from the U.S. are nearly twice as likely to de-scribe their digital marketing efforts as transformative (25%).

Why are more retail and CG organizations not able to leverage digital transformation? The answer could be in the fact that their initiatives are driven in siloes. For success, the strategy must impact a broad swathe of business elements:

• Customer Experience Transformation

• Operational Process Transformation

• Business Model TransformationWhat this means is that once the customer

– in our case the television viewer who wants the sharp suit flaunted by Julianna Margulies in The Good Wife – places an order across any channel (mobile, web, call center, brick-and-mortar), everything along the value chain, from order confirmation to order delivery must be digitized.

Without end-to-end digital transformation that embraces marketing, content dis-semination and re-use, customer interface, order processing, payments, CRM/ cus-tomer history, sourcing, inventory, logistics, and product innovation, fragmented ap-proaches don’t deliver the expected ROI.

This was borne out by our study which said that organizational silos contribute to the challenge of going digital: digital marketing is often organized as a separate function (37%), while e-commerce often operates as a separate business unit (39%). In addition, half of executives surveyed, 50%, reported that in one or more instances, their digital marketing had failed to integrate with es-sential back-end processes.

Integrating Digital Transformation is a critical strategy. The strategy must be aligned with the kinds of demands placed by customers on retailers and CG organi-zations. Today’s customers want not just a seamless experience across channels, but they also want a variety of buying and delivery options.

Customers today don’t want to wait. They don’t mind their orders being fulfilled in bits

Increasing Levels Of Complexity

Focus Areas For Successful Digital Transformation

39

and pieces. Therefore, in several instances of door-step delivery, consolidating orders may not be necessary. In other instances – for example, when a customer wants to pick up the order from a store -- consolida-tion is a key factor in creating a convenient experience. This brings in several degrees of complexity in sourcing, inventory man-agement, packaging and logistics. Now add to this the fact that companies, espe-cially those dealing in cosmetics, clothing, footwear, accessories, and white goods, are adding literally hundreds of product variations to their catalogues every year and it becomes apparent that Digital Trans-formation must cut across the organization to be successful.

Simultaneously, Digital Transformation is accelerating changes in business models. The supply of digital products and services – books, music, movies, graphic designs, etc. -- is growing. These lend themselves to digital delivery and a pay-per-use model with IP Management processes around them. Digital products don’t gain from economies of scale and bring in a new category of micro payments.

Finally, the type of devices customers are using – desktops, laptops, tablets, smart phones, kiosks -- has grown beyond even well-informed forecasts. Not only do customers interact with brands differently across each one of those devices, but applications also behave differently on each device.

A little beyond the present, but looming large, is the reality of the Internet of Things (IoT). Everything and anything – from fork-

lifts to pallets and products – is getting tagged and becoming searchable via RFID or an IP address. How does this impact the Digital Transformation journey of a retail or CG organization? How can it be leveraged to make the customer experience better, to shape new products, to influence buy deci-sions and to bring down operating costs?

In a business where product lifecycles are shrinking and competitive advantage belongs to those who respond in real time, there can be no argument against Digital Transformation. Just like my earlier example with Pradux where consumers are instantly browsing and sharing the hottest trending items they see on TV and in the world. Organizations must re-think their strategies, IT posture and processes in order to make digital part of their DNA.

It is worth noting that the Forbes-Wipro Insights study showed that companies are making substantial investments in digital marketing and related capabilities. The top four overall most frequently cited sets of past investments include social media marketing (70%), shopper and consumer insights (51%), and mobile and customer experience (tied at 47%). The trend is ir-revocable – for the industry it is digitize or perish.

The Digital Future

DIGITIZE OR PERISH

We hope you enjoyed reading “WINSIGHTS”

If you would like to read more, please visit our website

www.wipro.com/insights/— where we regularly publish

our viewpoints and perspectives that can help companies

sustain competitive advantage.

We would love to hear your thoughts and suggestions

that could go a long way in making this journal a valuable

knowledge-sharing tool for senior executives like yourself.

Please write to us at [email protected]

Best Wishes,

Wipro Council for Industry Research

Wipro Ltd. (NYSE:WIT) is a leading Information Technology,

Consulting and Business Process Services company that

delivers solutions to enable its clients do business better.

Wipro delivers winning business outcomes through its deep

industry experience and a 360 degree view of “Business

through Technology” - helping clients create successful

and adaptive businesses. A company recognized globally

for its comprehensive portfolio of services, a practitioner’s

approach to delivering innovation, and an organization wide

commitment to sustainability, Wipro has a workforce of over

150,000, serving clients in 175+ cities across 6 continents.

For more information, please visit www.wipro.com

About Wipro Ltd.

Give us your feedback online

http://www.wipro.com/winsights-feedback/

COPYRIGHT 2015, WIPRO LIMITED