Volume 1 : Issue 4 : 2014 Executive Monitor · Executive Monitor Financial Services Banking The...

22

Executive Monitor Financial Services Volume 1 : Issue 4 : 2014

Transcript of Volume 1 : Issue 4 : 2014 Executive Monitor · Executive Monitor Financial Services Banking The...

Executive MonitorFinancial Services

Volume 1 : Issue 4 : 2014

2

Executive MonitorFinancial Services

Global Industry Trends The financial services landscape has been disrupted by a variety of factors over the last decade. In general, while the overall economy is more stable than ever since the financial crisis hit, it remains unpredictable, and recovery continues to be uneven across regions. Economic and credit growth is sluggish, and despite rising profits in financial services, the sector still faces capital restraints, including smaller budgets and staff, which are carryovers from cutbacks made during the downturn. Mounting regulatory pressures and rapid changes in the digital landscape could negatively impact the industry if it does not find ways to innovate and turn risks into growth opportunities. With a shifting landscape in the US in Washington, executives must prioritize compliance along with profitability goals. In order to do so, they are beginning to hire more in-house staff to manage the rising workloads that accompany new regulations as well as leverage technology, particularly big data, to increase efficiency in fulfilling regulatory requirements.1

The financial services industry must also adroitly evolve and utilize new technologies to create better experiences for their customers. However, they must execute these digital initiatives carefully to ensure that they do not become vulnerable to data breaches.

Executive Summary

After years of instability stemming from the economic crisis of 2008-2009, financial markets are bouncing back. While many regions are still in repair, some governments have instated new regulations to help facilitate stability and growth. As the middle class expands in the developing world, there is a newly found need for banks and financial services firms to support their requirements. This has stimulated growth in several emerging market economies. FinTech, especially, has expanded considerably in the last few years compared to other, more traditional segments of the industry. Executives will continue to face regulatory challenges in the years ahead, and will need to find creative ways to continue on the path of recovery.

“Recovering economies, shifting regulatory environments and a massive influx of technology have reinvigorated the war for talent in the financial services sector. Talent acquisition has become the differentiator for companies to take market share. This has resulted in a continuous challenge for organizations to attract and retain top performers beyond offering better compensation.” Trina Gordon, President & CEO, Boyden World Corporation

1 http://www.cgma.org/magazine/news/pages/20138297.aspx?TestCookiesEnabled=redirect

3

Executive MonitorFinancial Services

Banking

The banking sector is undergoing a transformation, but has a cautiously optimistic outlook as it navigates uncharted territory. The growth rate in the sector is slow but steady in the face of new changes in healthcare as well as regulatory changes, which are the leading challenges for many bankers. In fact, according to Corp! Magazine, 55% of bankers rank federal oversight as their top obstacle.2

Banks will have to shift their approach to reach their digitally empowered customer bases. While a significant portion of customers still prefer to visit a bank’s branch, the brick-and-mortar locations where banks traditionally conduct business will have to change in order to keep up with consumer needs and efficiently allocate financial resources.3 This will involve rethinking the function of brick-and-mortar spaces and considering closing down, relocating, and/or downsizing some locations, as some banks have already done. Beyond these changes, banks have also started altering the nature of services offered at branches. According to Bankrate, tellers no longer solely conduct transactions; they also sell bank products and services.4 Some bank branches have even introduced “intelligent ATMs,” which offer more transaction services than the traditional ATM and use video screens to connect customers to live tellers.

The online and mobile banking space also provides huge opportunities for growth. Eight out of 10 customers use online banking at least once a month, and since 2012, there has been a 50% increase in mobile banking.5 Forrester predicts that the mobile payments market will grow to $90 billion by 2017 from only $12.8 billion in 2012.6 In order to seize this opportunity, banks must compete with the likes of PayPal, Venmo, and other apps that allow peer-to-peer money transfers for a low rate or at no cost. Mobile wallet usage also presents another growth opportunity for the banking industry, despite its struggle to gain widespread adoption in the last few years. The introduction of Apple Pay in October of this year may be the push the industry has needed. Moving forward, banks may also need to find ways to use social media as a vehicle for delivering a better customer experience and educating consumers about new products.

Investment Banking

Since the Great Recession, investment banks have undergone extensive restructuring while rebuilding their reputations and strengthening their balance sheets. Though the future is still somewhat uncertain, analysts report a positive outlook, reflected in a surge of M&A activity in 2014 after a lull from 2009 to 2013. According to David Solomon, co-head of the investment banking division at Goldman Sachs, the rise in M&A transactions indicates that companies now find themselves in a position to pursue greater growth opportunities.7 In addition, IPO activity is at its highest level since 2000, with most recent deals trading successfully.

Investment banks respond to new regulations in ways that change their longstanding approaches to credit, market and portfolio risks.8 For example, many players in the industry are restructuring or completely abolishing their cash equity business, while the commodities industry has been shaken by players being forced to completely leave the space. According to Accenture, the focus now is on strengthening the balance sheet instead of high levels of return on equity.9

“The overall landscape of the financial services industry has had to change with tighter regulations and to meet the demands for transparency and accountability from shareholders. This has created new positons and growth in areas such as compliance, finance and legal. With technology driving product, data and customer acquisition as well as cybersecurity are the areas we see most growth across the industry.” Jeanne Branthover, Leader of Boyden’s Global Financial Services Practice and Managing Partner, Boyden New York

2 http://www.corpmagazine.com/finance/banking-industry-faces-new-financial-landscape-a-candidate-driven-marketplace/ 3 http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-Consumer-US-Retail-Banking-Survey.pdf 4 http://www.bankrate.com/finance/banking/new-age-of-consumer-banking-3.aspx 5 http://www.accenture.com/us-en/Pages/insight-retail-banking-survey-interactive-infographic.aspx 6 http://techcrunch.com/2013/01/16/forrester-u-s-mobile-payments-market-predicted-to-reach-90b-by-2017-up-from-12-8b-in-2012 7 http://www.goldmansachs.com/our-thinking/trends-in-our-business/investment-banking/solomon-2014/index.html 8 http://www.strategyand.pwc.com/global/home/what_we_do/industries/financial_services/fs_key_trends/46791703 9 http://www.strategyand.pwc.com/global/home/what_we_do/industries/financial_services/fs_key_trends/46791703

4

Executive MonitorFinancial Services

The aforementioned notwithstanding, investment banks will also have to create digital solutions to respond to other developments, such as an increased demand for on-the-go services and data transparency by clients, as well as the desire for faster communication by stakeholders.10

Wealth Management and Private Banking

The wealth management sector is at an inflection point, where it must transition from its customary reactiveness to become proactive and reassess its business models and service offerings. This past year has been positive for the sector, with wirehouses such as Bank of America Merrill Lynch, Wells Fargo Advisors, and Morgan Stanley Wealth Management making up a greater portion of the overall revenue at their corresponding banks.11 However, in order to stay competitive in the marketplace, wealth managers must continue to create new ways to interact with customers while also balancing the legal restrictions and financial costs of compliance.

Although the reputation of wealth managers has improved since the downturn, firms continue to labor to regain client trust and increase satisfaction. In order to accomplish this, they must consider clients’ current risk-averse management styles. Since the downturn, clients have shifted their allocated assets into safer, more transparent products (see figure below) such as fixed income or cash related.12 These shifts are expected to return to normal in the mid- to long-term, however.

“Despite the uptick in M&A activity, investment banks continue to be forced to bow to regulatory and political pressure to change. We have already seen several high profile investment banking and capital markets management moves into pivotal global management positions within asset and wealth management groups of the larger global banks. The knock-on effect of such management changes and the inherent regulatory pressures mean the necessary mix of buy- and sell-side DNA within the buy side is evolving quickly; cross asset class and hybrid structured products professionals are being attracted by opportunities within traditional buy-side firms, managed platforms and fund of funds firms as they invest in their own product capabilities.” John Burr, Partner, Boyden UK

Source: http://www.strategyand.pwc.com/media/file/US_Wealth_Management_Survey.pdf

10 http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-Digital-Disruptions-Investment-Banking.pdf 11 http://www.investmentnews.com/article/20141017/FREE/141019929/wealth-management-a-growing-force-in-bank-fortunes 12 http://www.strategyand.pwc.com/global/home/what-we-think/reports-white-papers/article-display/wealth-management-survey- trends-emerging

5

Executive MonitorFinancial Services

In addition to responding to changing client behaviors, wealth managers must also handle new client expectations to create a personalized experience.13 Fewer clients are interested in the traditional commoditized services, so firms must offer segment-specific value propositions based on the client’s goals and investment personality. According to EY, there is an underlying trend in the wealth management marketplace of moving away from simply chasing returns, so that the marketplace will instead buy into customized solutions that investors can choose based on their individual goals. For example, these goals can consist of mirroring benchmarks, asset-liability matching and/or managing assets around a target date or goal (e.g., buying a house or funding an education).14

Unlike other financial services sectors, the wealth management sector is less susceptible to disruption over the next couple of years. For the most part, traditional channels such as face-to-face (in branch), phone, and email interactions are viewed as most vital by clients (see figure below), while digital channels remain a complementary part of the client experience. That said, digital channels should remain on the sector’s radar, as the use of mobile devices to trade is expected to increase over the next couple of years. Mobile trading’s share of DARTs in 2013 was 9%, and this number is expected to rise to 21% by 2016 and 38% by 2018.15

Source: http://www.ey.com/GL/en/Industries/Financial-Services/Asset-Management/2014-Wealth-Management-Survey

“Large financial companies continue to invest heavily in talent for their private wealth divisions. Other units, including asset management, draw more revenue, though wealth management remains the most profitable. With tighter regulation, we have seen increased demand for talent in various compliance areas, including anti-money laundering. Talent acquisition in compliance is surpassing client development, which has traditionally been the most active area of hiring in the sector.” Andrew Reese, Partner, Boyden New York

13http://www.pwc.com/gx/en/banking-capital-markets/private-banking-wealth-management-survey/index.jhtml?WT.ac=vt-wealth 14http://www.ey.com/Publication/vwLUAssets/EY-Global_wealth_and_asset_management-industry-outlook/$FILE/ey-global-wealth- and-asset-management.pdf 15http://wealthmanagement.com/mutual-funds/gallery-top-trends-wealth-management#slide-8-field_images-475181

6

Executive MonitorFinancial Services

Firms will also need to use both traditional and digital channels to increase transparency, another critical issue for wealth managers. Given risk-averse attitudes, clients require greater access to investment portfolios as well as more information on how to make the best investments. Thus wealth managers need to determine how to best communicate the information clients seek. Asset Management

In 2013, the global asset management industry had its best performance since the crisis. Profits were strong and reached record levels of $68.7 trillion - up 13% since the end of 2012. Upward trends are forecasted to continue. By 2020, PwC predicts that global assets under management will increase to $102 trillion, growing at a 6% compounded annual rate.16 However, the industry is still facing challenges and must develop a long-term strategy to evolve with shifting markets and conditions.17

Though outlooks are relatively positive, net revenues are still less than they were before the financial crisis and new issues now shape asset management and its operating costs. For example traditional, actively managed core assets remain vulnerable and have lost share in the global pool as specialties and solutions continue to dominate net flows. Furthermore, asset managers are still trying to figure out ways to navigate the increasingly complex and costly regulatory changes, which will involve building and scaling new functionality for accelerated central clearing, among other challenges.

Source: http://www.pwc.com/gx/en/asset-management/publications/pdfs/pwc-asset-management-2020-a-brave-new-world-final.pdf

“Among asset manage-ment companies, regulatory change, geopolitical instability, changes to distribution models and product offerings, demographic change, due diligence, transparency, and technological advancement have all combined to separate the ‘true players’ in terms of talent acquisition. Companies continue to upgrade demands on their own performance as asset managers seek deeper and longer-term client relationships in an increasingly competitive landscape.” Ken Rich, Partner, Boyden New York

16 http://www.pwc.com/gx/en/asset-management/publications/pdfs/pwc-asset-management-2020-a-brave-new-world-final.pdf 17 https://www.bcgperspectives.com/content/articles/financial_institutions_global_asset_management_2014_steering_course_growth/

7

Executive MonitorFinancial Services

Additionally, asset managers must find ways to embrace the digital and data revolution to better connect with Wall Street, engage customers, mine data for information on clients and potential clients, and improve operational efficiency as well as regulatory and tax reporting. 18 19

Insurance

Despite experiencing a relatively good year in 2013, insurers face greater pressure to maximize profits and value for shareholders in the face of historically low interest rates and new regulations. Capital management has become a huge challenge and insurance companies have had to rethink strategies for building revenues and increasing profits. Many have adopted traditional cost-cutting measures to sustain themselves in the short term, but will have to take additional innovative steps to grow in the long term. For instance, insurers will have to increase their flexibility in fixed-income allocations, adopt a more holistic approach to portfolio construction, redefine what is liquid and illiquid, adjust equity allocations, and find ways to capitalize on disintermediated lending markets.20

Insurance companies are also focusing on finding better ways to meet client needs and expectations. Advances in technology are helping them do this, and also empowering consumers to compare and/or purchase insurance products from virtually anywhere. But given that choosing the right type of insurance is difficult to do without the guidance of an advisor, it is not foreseeable that online resources will or should ever replace trained professionals. Consequently, insurers should find ways to make the digital experience an extension of the traditional client experience, not a substitute for it.

Financial Technology (FinTech)

Financial technology or FinTech, the segment of the technology startup scene disrupting financial services across various sectors, has grown exponentially over the last few years and is expected to continue this upward trend. Global investment in financial technology went from under $930 million in 2009 to nearly $3 billion in 2013 (see figure below).

“Dynamics and ever-evolving new risks are forcing executives to be nimble and adjust their roles to build a foundation for long-term success and survival. The ubiquitous influx of third-party capital, disruption to the marketplace, and the response of (re)insurers and the brokerage community are placing heightened value on senior executives who understand the strategic use of capital and alignment with their clients’ strategic thrusts.” Erik Matson, Partner, Boyden New York

Source: http://www.accenture.com/Microsites/fsinsights/capital-markets-uk/Documents/Accenture-Global-Boom-in-FinTech-Investment.pdf

18 http://www.slideshare.net/TheBostonConsultingGroup/global-asset-management-2014 19 http://www.valuewalk.com/2014/02/pwc-aum-100-trillion-2020/ 20 https://www.blackrock.com/institutions/en-us/literature/whitepaper/global-insurance-industry-outlook-2014-the-year-ahead.pdf

8

Executive MonitorFinancial Services

FinTech has been responsible for the disintermediation of banking services such as peer-to-peer lending, money transfers, equity investment, loans, fundraising, and even asset management. The rapid success of FinTech is perhaps attributable to its non-threatening nature (at least in comparison to large banks) combined with consumer preferences for conducting financial transactions digitally. In today’s financial services marketplace, new small- to medium-sized players can compete with large incumbent players. To keep up, many banks have set up venture funds to fund technology startups and have partnered with them.21

This new age of financial services also offers great opportunities to leverage big data for risk management and a more personalized customer experience. FinTech can easily gather customer data and use advanced analytic tools for credit evaluation and account monitoring to unlock new sources of available capital with greater accuracy.22 Additionally, the information gathered can be used to individualize and enhance the customer experience from a client’s computer, tablet or smartphone.

Executive Hiring Trends Careers in financial services have lost much of their allure and prestige in the last decade, especially in the United States and Europe. Since the economic downturn, political and media scrutiny have taken a toll on the industry’s reputation, and the industry has had to reduce financial rewards due to lower returns and new rules on compensation.23 However, now that the greater economy and the industry are recovering, companies have an opportunity to transform and upgrade their businesses with talented executives leading the way and ensuring the industry’s resilience.

Since the aftermath of the financial crisis, which resulted in the loss of thousands of jobs in the industry, the hiring environment in financial services has improved considerably. According to a survey of investment professionals conducted by the CFA Institute and the US Bureau of Labor Statistics (BLS), the outlook for jobs in the financial services industry is positive. The CFA survey found that 40% of investors believe the outlook for jobs will improve, 42% believe it will stay the same, and only 18% believe it will deteriorate. The BLS, however, projects that jobs in the industry will increase at a modest annual rate of 0.9% through 2022.24

Leaders and senior managers, including computer scientists, IT professionals and compliance professionals, who can effectively manage regulatory and digital disruptions at all levels are in highest demand. According to PwC’s Annual CEO Survey, most CEOs in the industry (more than 70%) currently see cyber insecurity as a key threat to their company’s growth prospects. They are also concerned about overregulation (80%), and think that technology will transform their business (86%).25 Firms will need to find talent at senior levels capable of guiding the evolving workforce that will eventually deal with these issues.26 According to the CFA Institute, many firms are taking longer than usual to fill these positions.27 But in order to secure this critical talent, firms may have to go above and beyond traditional recruitment and deploy new practices.28

“The FinTech space has ramped up considerably in 2014. Whereas a few years ago, banks were fighting with other banks for technology talent, now the war for talent is often happening between pure tech companies and banks. The competition for talent is fierce in cyber-security, machine learning and big data analytics, where financial institutions are using these technologies to build new customer bases and simultaneously blunt threats from state-sponsored hacking and credit card fraud. These new roles have enormously benefited customers, while at the same time creating jobs within a banking subsector that 10 years ago just didn’t exist.” John Budriss, Partner, Boyden New York

21http://blogs.wsj.com/digits/2014/08/04/banks-lure-FinTech-startups-with-venture-funds/ 22http://www.slideshare.net/ourcrowd/20140729-fin-tech-webinar-zack-miller 23http://www.oliverwyman.com/content/dam/oliver-wyman/global/en/files/insights/financial-services/2014/Jan/Oliver%20Wyman_ State%20of%20Financial%20Services%20Industry%202014.pdf 24http://blogs.cfainstitute.org/investor/2014/08/28/poll-whats-your-outlook-on-job-growth-in-the-financial-services-sector/ 25http://www.pwc.com/gx/en/ceo-survey/index.jhtml# 26http://www.internationalfinancemagazine.com/article/Recruitment-trends-for-2014-in-financial-services.html27http://blogs.cfainstitute.org/investor/2014/08/28/poll-whats-your-outlook-on-job-growth-in-the-financial-services-sector/ 28http://www.forbes.com/sites/danschawbel/2013/11/05/top-8-workplace-trends-in-the-financial-services-industry/

9

Executive MonitorFinancial Services

Nearly half of CEOs say that finding talent with the right skills is a challenge and a “serious threat to their company’s growth.” One quarter of CEOs say that because of a lack of the right talent, they have had to “cancel or delay a strategic initiative over the past year.” Firms will therefore have to offer more incentives to draw executives in, especially with competition from other industries, particularly technology.30 A significant amount of talent that was once drawn to the financial services industry is now flocking to technology, which has less stringent regulation and a reputation for offering employees diverse working arrangements and flexibility, such as more personal time and the opportunity to work remotely. Additionally, a greater percentage of companies may want to consider increasing monetary incentives for executives. Some changes are already taking place, and financial executives reported higher average salary increases (3.3%) than the average business marketplace (3%) in 2014,31 Furthermore, according to a Mercer survey, lower pay will be linked to performance at many firms. Realistically, it is too soon to tell whether higher fixed compensation will be more attractive to employees and whether limiting the effectiveness of compensation as a management tool will positively influence performance.32

Another notable new trend challenging the financial services industry is the high turnover of millennials. This group tends to see the financial services industry as a “stepping stone to other career options” and only 10% plan to stay at their job long term, compared to 18% of millennials in other industries. In large part this occurs because millennials find themselves working many more hours than they expected. Consequently, many companies have had to change their strategic planning and have experienced slower than expected expansion. CEO Outlook

CEOs from banking and capital markets firms are more positive about the global economy than their peers in other sectors, with more than half (56%) saying they expect overall conditions to improve over the next year. And, more than half say they plan to increase headcounts over the next year as well. They recognize rapid changes in the market and agree that technology is the “most important transformational trend” that faces their sector. Nearly six in 10 of these CEOs also say the speed of technological change is a threat to their growth. In addition, they are skeptical that IT is well prepared to make the changes necessary, with only 36% expressing confidence. They also believe cyber insecurity is a threat to growth, and at 70%, they believe so more than CEOs from all other sectors.

As noted in PwC’s Annual CEO Survey, “Success in this market demands leaders who can manage through uncertainty and complexity as they seek to deal with regulatory change while preparing for the future. This in turn demands a clear sense of who their key customers and markets are going to be in five years’ time and what investments and changes will be needed to respond. It also requires a forward-looking view on how regulation will interact with the other transformational trends in areas such as cost, returns and the ability to meet customer expectations.” 33

“In Paris, recruitment of senior executives is increasing in asset management. Experienced proposal managers and senior product specialists are in demand as mid-sized companies develop new products for debt funds and private equity investments, and strengthen their distribution teams. On the corporate banking side, professionals with ECM or DCM expertise are in demand to cover mid-cap and upper mid-cap companies. In commercial banking, client assignments have increased for Chief Data Officers and technology specialists.” Florence Soulé de Lafont, Managing Partner, Boyden France

“CEOs in financial services are recognizing the impact of a rapidly changing competitive landscape. Those that will win will capitalize on this transformation. Today’s financial services CEO needs to focus on technology, talent, big data/analytics and cybersecurity, and also have the capacity and desire to innovate. Since the crisis we are seeing a different profile for successful leaders in the financial services sector. The market now demands a leader who can manage through uncertainty and complexity.” Jeanne Branthover, Leader of Boyden’s Global Financial Services Practice and Managing Partner, Boyden New York

30http://blogs.wsj.com/moneybeat/2014/01/22/talent-wars-four-ways-banks-can-compete-with-tech-firms/ 31http://www.grantthornton.com/issues/library/survey-reports/tax/2014/Financial-executive-compensation-survey.aspx 32http://www.mercer.com/content/dam/mercer/attachments/global/webcasts/140715_WB_the_latest_on_executive_remuneration_in_ financial_services.pdf 33http://www.pwc.com/gx/en/ceo-survey/2014/industry/banking-capital-markets.jhtml

10

Executive MonitorFinancial Services

34http://www.pwc.com/gx/en/ceo-survey/2014/industry/asset-management.jhtml

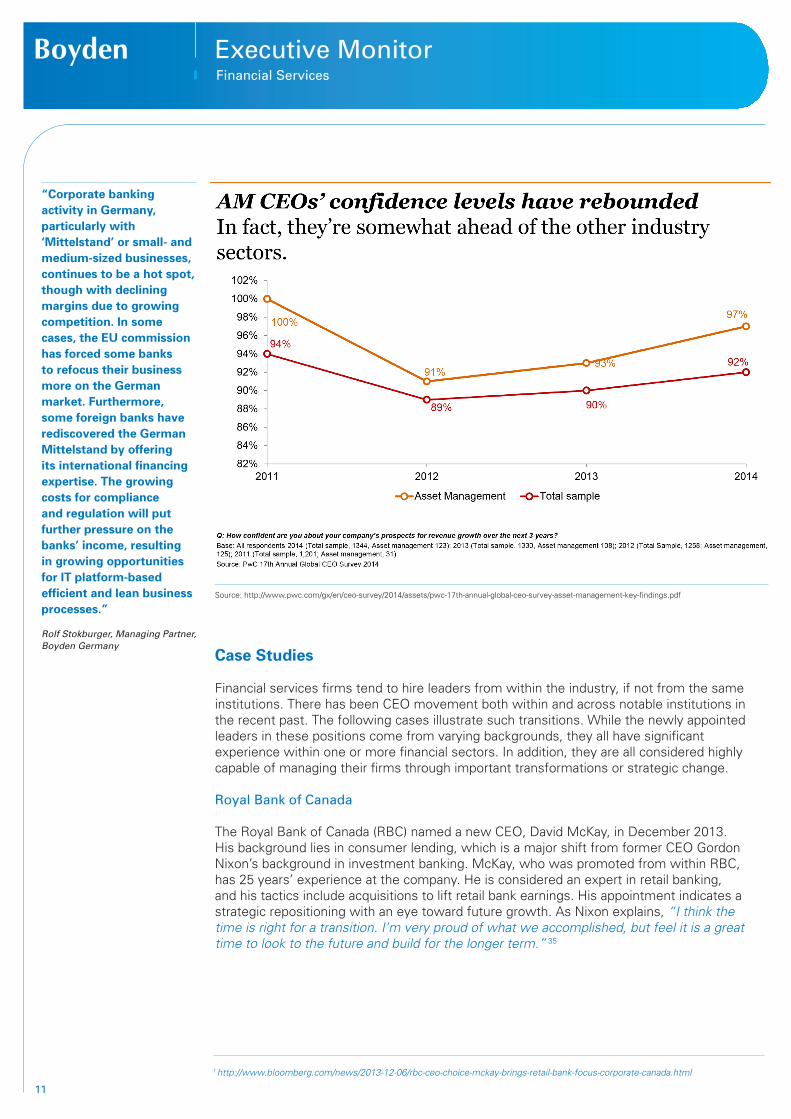

CEOs in asset management are particularly optimistic about the future, especially compared to their sentiment at this time last year. Today, nearly all (97%) expect revenue growth and are more upbeat about the overall economy, with more than half believing the economy will improve over the next 12 months. They are also making investments in talent; nearly six in 10 asset management CEOs plan to expand their workforce in the next year. Additional funding in technology and new strategies for M&A further highlight their optimism. Technology is, however, seen as a double-edged sword. “I think technology is both an opportunity and a threat. I think ultimately money will be increasingly digitalized and there will be many new entrants to the payment system in terms of money transfer,” says Douglas Flint, Chairman, HSBC Holdings Plc. “There’ll be many, many people with large customer bases who’ll want to get into the business of financial services. So I think digitalization of money is only going to expand.” Despite their positivity, asset management CEOs do have some concerns; among them are overregulation (80%), slow growth in developed economies (80%) and fiscal austerity (78%).34

Source: http://www.pwc.com/gx/en/ceo-survey/2014/industry/banking-capital-markets.jhtml

11

Executive MonitorFinancial Services

Case Studies

Financial services firms tend to hire leaders from within the industry, if not from the same institutions. There has been CEO movement both within and across notable institutions in the recent past. The following cases illustrate such transitions. While the newly appointed leaders in these positions come from varying backgrounds, they all have significant experience within one or more financial sectors. In addition, they are all considered highly capable of managing their firms through important transformations or strategic change. Royal Bank of Canada

The Royal Bank of Canada (RBC) named a new CEO, David McKay, in December 2013. His background lies in consumer lending, which is a major shift from former CEO Gordon Nixon’s background in investment banking. McKay, who was promoted from within RBC, has 25 years’ experience at the company. He is considered an expert in retail banking, and his tactics include acquisitions to lift retail bank earnings. His appointment indicates a strategic repositioning with an eye toward future growth. As Nixon explains, “I think the time is right for a transition. I’m very proud of what we accomplished, but feel it is a great time to look to the future and build for the longer term.” 35

Source: http://www.pwc.com/gx/en/ceo-survey/2014/assets/pwc-17th-annual-global-ceo-survey-asset-management-key-findings.pdf

“Corporate banking activity in Germany, particularly with ‘Mittelstand’ or small- and medium-sized businesses, continues to be a hot spot, though with declining margins due to growing competition. In some cases, the EU commission has forced some banks to refocus their business more on the German market. Furthermore, some foreign banks have rediscovered the German Mittelstand by offering its international financing expertise. The growing costs for compliance and regulation will put further pressure on the banks’ income, resulting in growing opportunities for IT platform-based efficient and lean business processes.” Rolf Stokburger, Managing Partner, Boyden Germany

1 http://www.bloomberg.com/news/2013-12-06/rbc-ceo-choice-mckay-brings-retail-bank-focus-corporate-canada.html

12

Executive MonitorFinancial Services

Fidelity Investments

Fidelity Investments, America’s second largest fund manager, named Abigail Johnson as its new CEO in October 2014. Johnson already serves as President of the company, and will take over the post of CEO from her father, who has been in the role since 1977. The executive change was the “widely anticipated next step” in Johnson’s eventual succession within the company.

Johnson is one of very few female CEOs in the industry, and her net worth has now climbed to $13.3 billion, according to Forbes. She is also ranked 34th on Forbes’ list of the World’s 100 Most Powerful Women. While no one is surprised that Johnson has taken over the company, many are confident, given her commitment to the firm since 1988 and the “keen eye for detail” and talent for “executing a strategic plan” she has shown to possess. 36 37 Bank of Portugal

In September 2014 Eduardo Stock da Cunha was named as the new CEO for Novo Banco (the successor to Banco Espirito Santo), following the resignation of its three top managers. The Bank of Portugal plans to sell off Novo Banco to recover state bank loans. Stock da Cunha is an experienced international banker, and has worked with lenders including Santander and Lloyds in the UK, Portugal, Spain, and the US. His experience uniquely qualifies him to steer the bank through its next chapter.38

Executive Compensation

Executive compensation in the financial services industry has come under tough scrutiny. Many say that the financial crisis was partly “caused by excessive short term risk-taking encouraged by a bonus culture.” Investors in particular have criticized and even rejected compensation plans at some of the world’s largest banks this year. Despite changes since the financial crisis, many are still unsatisfied with efforts by financial services firms and demand further modifications, especially in the US and UK.39

According to the Mercer Global Financial Services Executive Compensation Survey, nearly eight in 10 financial services organizations say they expect an impact on executive compensation due to difficult market conditions this year. The chart on the following page indicates the changes that have been put in place. At the top ranks “strengthened the linkage between performance management and compensation.” Only two in 10 firms do not anticipate making changes due to the current market environment.40

“Leadership focus is on profitability with solvency issues of the banking system now stabilized. As a result of banking sector consolidation, low loan demand and near-zero interest rates have increased demand for executives in the technology and digital sectors. In addition, private equity funds are creating management structures and hiring in Spain as PE firms buy companies in consumer finance, retail and real estate.” Carlos Dafauce, Partner, Boyden Spain

“Regulatory pressures within wealth manage-ment and private banking in Europe will have significant impact. MiFID II will compel regulated firms to be completely transparent about their charging structures. With the emergence of several online institu-tional and retail trading platforms, we are already seeing more of a digital execution-led strategic focus from larger traditional wealth managers in order to compete with very credible, lower-cost new entrants in this space.” George Nice, Partner, Boyden UK

36 http://online.wsj.com/articles/abigail-johnson-named-ceo-of-fidelity-investments-1413226082 37http://www.forbes.com/sites/moiraforbes/2014/10/13/power-woman-abigail-johnson-named-ceo-of-fidelity-investments/ 38http://www.reuters.com/article/2014/09/14/us-portugal-bes-idUSKBN0H90RG20140914 39http://www.cnbc.com/id/101714765#. 40http://www.mercer.com/content/dam/mercer/attachments/global/webcasts/140715_WB_the_latest_on_executive_remuneration_in_ financial_services.pdf

13

Executive MonitorFinancial Services

Global Industry Trends Europe The Eurozone GDP is expected to grow, albeit slowly, throughout the end of 2014 and into 2015 at a slightly higher rate, after two years of decline. The rate of recovery will look different for each country across the region; Germany, Ireland and Spain have a relatively positive outlook, whereas France, Belgium and the Netherlands (countries which have been slow to change) project slower growth. Unemployment, which is expected to stabilize this year, will remain high at approximately 12%. Assets under management are expected to increase by 6.6% through the end of this year, and then by 24% over five years. In addition, “risk appetite continues to improve”: multi-asset funds should grow over the next few years.42

The European Union appointed a new Commissioner for Financial Stability, Financial Services and Capital Markets, Jonathan Hill of Britain, in October 2014. Hill pledges to strengthen Eurozone financial institutions and “curb the ‘risk-taking and short-termism’ in capital markets.”

United Kingdom

The United Kingdom’s financial services sector is not only a global leader, but a huge regional employer. There are over 34,000 businesses in the country providing financial services, employing millions of people. Overall, 7% of employment in the UK is attributed to this sector. London “dominates as a global financial center,” but other cities in the country are also very strong, including Edinburgh, Glasgow, Leeds, and Manchester.43

A serious challenge the UK financial sector faces is a very low level of public trust in its institutions. As the chart on the following page illustrates, only one third of UK consumers surveyed trust retail banks, and all other financial institutions score even lower. Because of this lack of confidence, the public is also concerned about things like poor returns on savings, unfair fees, risky investments by institutions, security of personal details, business ethics and more.

“The Dutch banks, including ABN AMRO which is expected to go public again next year, have passed the ECB Stress Test comparatively well. This helps in reestablishing public confidence and the reputation of the sector. Following the financial crisis, banks and insurers are slowly hiring again. Management with expertise in IT, e-finance, big data and compliance are especially in demand. However, the upward trend is jeopardized by Dutch government regulation of bonuses, which maximize performance-related income to 20% of fixed annual salaries. This risks a ‘brain drain’ of highly talented Dutch investment bankers, who might move to foreign banks or shift to corporates or the consulting industry.” Joost Goudsmit, Managing Partner, Boyden Netherlands

41http://www.ey.com/Publication/vwLUAssets/EY-FS-Eurozone-Spring-2014/$FILE/EY-FS-Eurozone-Spring-2014.pdf 42http://www.ey.com/Publication/vwLUAssets/EY-FS-Eurozone-Spring-2014/$FILE/EY-FS-Eurozone-Spring-2014.pdf43http://www.prospects.ac.uk/accountancy_banking_and_finance_sector_overview.htm

14

Executive MonitorFinancial Services

Middle East and Africa

The Middle East has one of the fastest-growing banking and capital markets sectors in the world, and like many other regions, is in a period of transformation and change. Similar to the trends taking place in Africa, the population in general is younger and more educated than before. Firms in the region are investing in initiatives to increase diversity in products and services, as well as adhere to regulatory requirements for developing secure financial systems in order to keep up with international peers.

Each country’s financial sector is in a different phase. Some nations, including many of the Gulf Cooperation Council (GCC) countries, have a more developed banking sector that is efficient and profitable on its own, PwC notes, whereas others are dominated by public sector banks. In most areas in this region, the banking sector is “highly concentrated” as the three largest banks account for at least 65% of total commercial bank assets. As a result, new banks have a difficult time entering this market.45

Currently, Africa’s financial services sector makes up 10% of the continent’s collective GDP. If growth rates remain constant this could reach 20% in the next 10 years, mostly attributable to retail banking. This growth will also “create new jobs, establish a formal identity of millions of market participants, and provide greater safety than predominant cash-based systems.” As illustrated in the following chart, African countries are divided into four groups of financial services markets. Established Markets include only South Africa and Mauritius. Morocco, Egypt, Tunisia and others are “Forging Ahead”, whereas Kenya, Algeria and Libya are still considered “Next Movers.” Finally, countries like Ethiopia, Sudan and others are still in transition.46

“The strong local and regional banks are pushing aggressively to gain market share and upgrade their talent pool. The regional institutions are achieving this by attracting executives leaving multinationals which are not expanding in the region due to different priorities in other parts of the world. We expect to see more involvement from governments and banks in the Gulf Region to accelerate development in underdeveloped markets in MENA and Sub-Saharan Africa.” Magdy El Zein, Managing Partner, Boyden Middle East

44http://www.pwc.co.uk/financial-services/financial-services-risk-and-regulation/how-financial-services-lost-its-mojo.jhtml 45http://www.pwc.com/m1/en/industries/banking-capital-markets.jhtml 46http://www.howwemadeitinafrica.com/five-trends-driving-africa%E2%80%99s-economic-growth/12795/

Source: http://www.pwc.co.uk/financial-services/financial-services-risk-and-regulation/how-financial-services-lost-its-mojo.jhtml

15

Executive MonitorFinancial Services

China

China’s financial services sector, akin to many other industries in China, has grown tremendously over the past decade. This expansion has drawn many international companies to the country and this trend should continue as “the industry’s prospects in China remain attractive, and much more alluring than they are almost anywhere else.” The next few years will bring significant changes, and firms will have to adapt to structural shifts.

As the next chart indicates, China’s retail banking market will likely become the second largest in the world within the next year. However, industry reports suggest that retail banks must work to improve profit per customer, as well as focus on the following objectives:

• Building better primary relationships with customers• Creating smarter and more focused acquisition strategies• Developing low-cost and scalable operating models 47 Despite its rapid growth, China is currently in a transitional period in which the government is pushing for greater controls over state-owned firms. In addition, these companies face pressure to restructure and significantly reduce salaries for state employees and executives alike.48 Nevertheless, CEOs in banking and capital markets believe China is the most important market to watch closely over the next year, followed by the US. Asset management CEOs also believe China is a priority over the next year and that it leads emerging economies in terms of growth (31%).49 50

Source: http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-Tipping-Point.pdf

47http://www.mckinsey.com/insights/financial_services/winning_strategies_for_chinas_financial-services_sector 48http://dealbook.nytimes.com/2014/10/14/longtime-chief-leaves-c-i-c-c-a-major-chinese-investment-bank/?_php=true&_ type=blogs&_r=0 49http://www.pwc.com/gx/en/ceo-survey/2014/assets/pwc-17th-annual-global-ceo-survey-banking-capital-markets-key-findings.pdf 50http://www.pwc.com/gx/en/ceo-survey/2014/assets/pwc-17th-annual-global-ceo-survey-asset-management-key-findings.pdf

16

Executive MonitorFinancial Services

Singapore

Singapore’s role as a prominent financial services market, both regionally in Asia and globally, is indisputable. While the country is only home to approximately five million residents, it has over 200 banks, more than 500 entities in the asset management industry, and the world’s fourth largest foreign exchange market. More than 180,000 people are employed by Singapore’s financial services sector, which makes up 12% of GDP for the country.51

Recruitment at all levels in the financial services industry has been growing for the past few quarters, and is expected to continue through 2015. The country has made a conscious effort to focus on local talent rather than hiring foreigners, which is reflected in new policies; this could “highlight the skills shortage [in Singapore]...and is likely to have a significant impact on the hiring of middle-income employees.” 52 Australia

Australia’s sophisticated financial services sector and strong economy position the country well as a financial hub. Australia faced few challenges associated with the global financial crisis and has had a nearly steady growth rate over the past five years.53 This is due in part to China’s continuous imports of Australian iron ore, coal, and other minerals. China is Australia’s primary trading partner; however, exports have dropped this year as the Chinese economy slowed, causing Australian commodity prices to fall by 12%.54 Trust has also waned, especially in international markets, and firms must re-engage customers as well as increase profits.55

Sydney, Australia’s most populous city, has vast potential as a leading financial services hub. The sector employs 180,000 people in New South Wales, and generates 5% of Australia’s annual GDP. However, FinTech is proving slow to catch on: The rise of new technologies here has caused an overlap with traditional financial services, potentially disrupting big local employers. Sydney’s financial services firms must deal with the challenge and embrace FinTech if they are to continue to succeed internationally. As a report from The Committee for Sydney notes, “Traditional financial services institutions are investing in technology innovation, rethinking their business models and even collaborating with FinTech firms.” 56

“Singapore continues to move up the value chain. The economic environment is very friendly to high value-added businesses and we are increasingly seeing global head-quarter functions being set up here in addition to numerous regional hubs. Often a global board member of a multinational company will be based in Singapore so they can offer other board members a firsthand view of developments in Asia.” Roger Wilson, Managing Partner, Boyden Singapore

Source: http://www.mckinsey.com/insights/financial_services/winning_strategies_for_chinas_financial-services_sector

51http://www.jdsupra.com/legalnews/singapore-one-of-asias-key-financial-c-70450/ 52http://www.channelnewsasia.com/news/singapore/hiring-in-banking/1412158.html 53http://www.pwc.com.au/industry/financial-services/about-us.htm 54http://www.businessweek.com/articles/2014-09-25/australian-economy-changes-as-commodity-exports-to-china-slow 55http://www.ibisworld.com.au/industry/default.aspx?indid=1740 56http://www.smh.com.au/nsw/sydney-struggling-to-keep-up-as-technology-challenges-financial-services-industry-20141006-10qoza.html

17

Executive MonitorFinancial Services

Canada

Canada remained strong throughout the duration of the financial crisis, and continues to enjoy this resiliency through 2014. The country has earned a reputation in the global community for its stability. Despite this, there are some challenges the country must face, including an evolving regulatory environment, and downward pressure on return on equity. 57

On its own, Canada’s financial services sector is strong; however the country struggles to compete with its global counterparts, especially in terms of innovation: “83% of financial services corporations in Canada see innovation as a key driver of success, but one third find it very challenging to build an innovative culture because they are unable to find the right talent and have trouble measuring return on investment.” 58

Source: http://www.pwc.com/ca/en/banking-capital-markets/publications/pwc-canadian-banks-2014-en.pdf

“In Canada, the leaders of practically all of the federal financial bodies—the central bank, banking regulator, export credit agency and federal housing corporation–have backgrounds in business and economic development. They have long histories of proactively encouraging economic growth and investment balanced by prudent risk management. That orientation, coupled with the balance-the-budget approach of the federal government, reflects the overall prudent sentiment in the country. Overregulation is therefore unlikely to materialize to the extent that some currently fear.” Ron Robertson, Managing Partner, Boyden Canada

57http://www.pwc.com/ca/en/banking-capital-markets/canadian-banks.jhtml 58http://business.financialpost.com/2013/12/02/canadas-financial-services-sector-struggling-to-keep-up-with-global-innovation-report/

18

Executive MonitorFinancial Services

Latin America

Latin America is one of the least saturated financial services markets in the world. However, a growing middle class and an increase in average household income are paving the way for increased opportunities in the region. Banks in Mexico have begun lending small amounts of money to low-income consumers as a first step.59

Global banks are eager to lend to the region, however doing so requires the expertise of local partners. Interestingly, Chinese lenders have taken the lead, already committing $75 billion to development goals in Latin America since 2005. As growth continues, there will likely be increased demand for loans and project bonds, especially in countries that have a mature debt capital market like Chile. Brazil, which is hosting the Olympics in 2016, should expect to see an increase in project financing.60

Conclusion

The financial services industry continues to grow. However, despite its ongoing recovery and expansion, especially in select regions, there is no shortage of challenges that executives must be prepared to address in order to ensure progress. Regulatory reform, structural changes within the industry, and an increased focus on technology will all be key areas of focus for the C-Suite in the near and somewhat longer term. In addition, fluctuations in both regional economies and the global economy will necessarily influence the state of the industry. In some cases, a shortage of talent also poses issues, as do continued scrutiny and suspicion concerning executive compensation.

“Latin America is definitively a growth market that is demanding additional and more sophisticated financial services and products. The Pacific Alliance free trade agreement, which includes Mexico, Colombia, Peru and Chile, is boosting GDP growth and higher income per capita. This demands more investment banking activity to fund projects and more fund managers to manage private pension funds, which in turn are creating long-term instruments of up to 30 years or longer. While Brazil has slowed, industry players are still widely viewing it as a mid-term growth market. Many financial international leaders are present and competition for talent remains high in the region.” John Byrne, Managing Partner, Boyden Chile

59 http://americasmi.com/en_US/expertise/articles-trends/page/the-latin-american-consumer-of-2020#sthash.C9A79HhZ.dpuf60 https://www.bnymellon.com/_global-assets/pdf/solutions-index/the-opportunity-for-lending-in-latin-america.pdf

19

Executive MonitorFinancial Services

Sources Blackrock (2014). “2014: The Year Ahead.” https://www.blackrock.com/institutions/en-us/literature/whitepaper/global-insurance-industry-outlook-2014-the-year-ahead.pdf.

PwC (2014). “About Financial Services.” http://www.pwc.com.au/industry/financial-services/about-us.htm.

Accenture (2013). “A Critical Balancing Act: US Retail Banking in the Digital Era.” Banking 2020 Thought Leadership Series. http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-Consumer-US-Retail-Banking-Survey.pdf.

Adewunmi, Femi. How We Made It in Africa. (10 Oct. 2011). “Five Trends Driving Africa’s Economic Growth.” http://www.howwemadeitinafrica.com/five-trends-driving-africa%E2%80%99s-economic-growth/12795/.

PwC (2014). “Asset Management 2020 A Brave New World.” http://www.pwc.com/gx/en/asset-management/publications/pdfs/pwc-asset-management-2020-a-brave-new-world-final.pdf.

Accenture (2011). “At the Tipping Point: Financial Services in Africa Comes of Age.” http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-Tipping-Point.pdf.

PwC (2014). “Banking & Capital Markets.” http://www.pwc.com/m1/en/industries/banking-capital-markets.jhtml.

Reuters (14 Sept. 2014). “Bank of Portugal Picks New CEO for BES Successor Novo Banco.” http://www.reuters.com/article/2014/09/14/us-portugal-bes-idUSKBN0H90RG20140914.

Barboza, David. The New York Times (14 Oct. 2014). “Longtime Chief Leaves C.I.C.C., a Major Chinese Investment Bank.” DealBook. http://dealbook.nytimes.com/2014/10/14/longtime-chief-leaves-c-i-c-c-a-major-chinese-investment-bank/?_php=true&_type=blogs&_r=0.

Accenture (2014). “The Boom in Global Fintech Investment.” http://www.accenture.com/Microsites/fsinsights/capital-markets-uk/Documents/Accenture-Global-Boom-in-Fintech-Investment.pdf.

PwC (2014). “Canadian Banks 2014.” http://www.pwc.com/ca/en/banking-capital-markets/canadian-banks.jhtml.

Strategy& (2014). “Capital Markets/Investment Banking.” http://www.strategyand.pwc.com/global/home/what_we_do/industries/financial_services/fs_key_trends/46791703.

Oliver Wyman (2014). “The Challenges Ahead: The State of the Financial Services Industry 2014.” http://www.oliverwyman.com/content/dam/oliver-wyman/global/en/files/insights/financial-services/2014/Jan/Oliver%20Wyman_State%20of%20Financial%20Services%20Industry%202014.pdf.

Collins, Dean. JD Supra Business Advisor (9 Oct. 2014). “Singapore: One of Asia’s Key Financial Centres.” http://www.jdsupra.com/legalnews/singapore-one-of-asias-key-financial-c-70450/.

20

Executive MonitorFinancial Services

Corpart, Guillaume. Americas Market Intelligence (Sept. 2012). “The Latin American Consumer of 2020.” http://americasmi.com/en_US/expertise/articles-trends/page/the-latin-american-consumer-of-2020#sthash.C9A79HhZ.dpuf.

Accenture (2014). “Digital Disruptions in Investment Banking.” http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-Digital-Disruptions-Investment-Banking.pdf.

Accenture (2 Dec. 2013). “Digital Revolution Is Transforming US Retail Banking – Interactive Infographic.” http://www.accenture.com/us-en/Pages/insight-retail-banking-survey-interactive-infographic.aspx.

Einhorn, Bruce. Bloomberg Business Week (25 Sept. 2014). “Australian Economy Changes as Exports to China Slow.” http://www.businessweek.com/articles/2014-09-25/australian-economy-changes-as-commodity-exports-to-china-slow.

Etherington, Darrell. TechCrunch (16 Jan. 2013). “Forrester: U.S. Mobile Payments Market Predicted To Reach $90B By 2017, Up From $12.8B In 2012.” http://techcrunch.com/2013/01/16/forrester-u-s-mobile-payments-market-predicted-to-reach-90b-by-2017-up-from-12-8b-in-2012/.

EY (Spring 2014). EY Eurozone Forecast. http://www.ey.com/Publication/vwLUAssets/EY-FS-Eurozone-Spring-2014/$FILE/EY-FS-Eurozone-Spring-2014.pdf.

IBISWorld (July 2014). “Finance in Australia: Market Research Report.” http://www.ibisworld.com.au/industry/default.aspx?indid=1740.

Grant Thornton (30 May 2014). “Financial Executive Compensation Survey 2014.” http://www.grantthornton.com/issues/library/survey-reports/tax/2014/Financial-executive-compensation-survey.aspx.

PwC (Feb. 2014). “Fit for the Future 17th Annual Global CEO Survey.” http://www.pwc.com/gx/en/ceo-survey/2014/assets/pwc-17th-annual-global-ceo-survey-banking-capital-markets-key-findings.pdf.

PwC (Feb. 2014). “Fit for the Future 17th Annual Global CEO Survey: Key findings in the asset management industry.” http://www.pwc.com/gx/en/ceo-survey/2014/assets/pwc-17th-annual-global-ceo-survey-asset-management-key-findings.pdff.

Forbes, Moira. Forbes (13 Oct. 2014). “Power Woman Abigail Johnson Named CEO of Fidelity Investments.” http://www.forbes.com/sites/moiraforbes/2014/10/13/power-woman-abigail-johnson-named-ceo-of-fidelity-investments/.

Wealthmanagement.com (17 Jan. 2014). “Gallery: Top Trends in Wealth Management.”

Bankrate (2014). Geffner, Marcie. “6 Signs of a New Age of Consumer Banking.” http://www.bankrate.com/finance/banking/new-age-of-consumer-banking-3.aspx.

PwC (2014). “Global CEO Survey.” http://www.pwc.com/gx/en/ceo-survey/index.jhtml.

PwC (2014). “Global CEO Survey: Asset Management.” http://www.pwc.com/gx/en/ceo-survey/2014/industry/asset-management.jhtml.

PwC (2014). “Global CEO Survey: Banking & Capital Markets.” http://www.pwc.com/gx/en/ceo-survey/2014/industry/banking-capital-markets.jhtml.

21

Executive MonitorFinancial Services

Ernst & Young (2014). “Global Wealth and Asset Management Industry Outlook.” http://www.ey.com/Publication/vwLUAssets/EY-Global_wealth_and_asset_management-industry-outlook/$FILE/ey-global-wealth-and-asset-management.pdf.

Grind, Kirsten. The Wall Street Journal (13 Oct. 2014). “Abigail Johnson Named CEO of Fidelity Investments.” http://online.wsj.com/articles/abigail-johnson-named-ceo-of-fidelity-investments-1413226082.

Channel NewsAsia (13 Oct. 2014). “Hiring in Banking, Financial Services Sector to Expand for next Half-year: Hays.” http://www.channelnewsasia.com/news/singapore/hiring-in-banking/1412158.html.

PwC (2014). “How Financial Services Lost Its Mojo - and How It Can Get It Back.” http://www.pwc.co.uk/financial-services/financial-services-risk-and-regulation/how-financial-services-lost-its-mojo.jhtml.

Reuters (29 May 2014). “Investors Reject Bank CEO Pay Plans.” http://www.cnbc.com/id/101714765.

The Wall Street Journal (4 Aug. 2014). Irrera, Anna. “Banks Lure Fintech Startups With Venture Funds.” http://blogs.wsj.com/digits/2014/08/04/banks-lure-fintech-startups-with-venture-funds/.

The New York Times (7 Oct. 2014). “Jonathan Hill, Nominee to Oversee E.U. Financial Sector, Makes Fresh Appeal to Lawmakers.” http://www.nytimes.com/2014/10/08/business/international/jonathan-hill-nominee-to-oversee-eu-financial-sector-makes-fresh-appeal-to-lawmakers.html?_r=1.

Mercer (15 July 2014). “The Latest Executive Remmuneration in Financial Services.” http://www.grantthornton.com/issues/library/survey-reports/tax/2014/Financial-executive-compensation-survey.aspx.

The New York Times (14 Oct. 2014). “Longtime Chief Leaves C.I.C.C., a Major Chinese Investment Bank.” http://dealbook.nytimes.com/2014/10/14/longtime-chief-leaves-c-i-c-c-a-major-chinese-investment-bank/?_php=true&_type=blogs&_r=0.

Miller, Zack, and Mick Weinstein. Ourcrowd (30 July 2014). “Investing in Fintech: Trends in Financial Technology for Investors and Entrepreneurs.” http://www.slideshare.net/ourcrowd/20140729-fin-tech-webinar-zack-miller.

Prospects (2014). “Overview of the Finance Sector in the UK.” http://www.prospects.ac.uk/accountancy_banking_and_finance_sector_overview.htm.

BNY Mellon (2014). “The Opportunity for Lending in Latin America.” https://www.bnymellon.com/_global-assets/pdf/solutions-index/the-opportunity-for-lending-in-latin-america.pdf.

Ovsey, Dan. Financial Post (2 Dec. 2013). “Canada’s financial services sector struggling to keep up with global innovation: report.” http://business.financialpost.com/2013/12/02/canadas-financial-services-sector-struggling-to-keep-up-with-global-innovation-report/.

PwC (2013). “Private Banking and Wealth Management Survey.” http://www.pwc.com/gx/en/banking-capital-markets/private-banking-wealth-management-survey/index.jhtml?WT.ac=vt-wealth.

22

Executive MonitorFinancial Services

Bloomberg (6 Dec. 2013). “RBC New CEO McKay Brings Consumer Bank Focus: Corporate Canada.” http://www.bloomberg.com/news/2013-12-06/rbc-ceo-choice-mckay-brings-retail-bank-focus-corporate-canada.html.

International Finance Magazine (Apr. 2014). “Recruitment Trends for 2014 in Financial Services.” http://www.internationalfinancemagazine.com/article/Recruitment-trends-for-2014-in-financial-services.html.

Rhonemus, Brian. Corp! Magazine (27 Feb. 2014). “Banking Industry Faces New Financial Landscape A Candidate Driven Marketplace.” http://www.corpmagazine.com/finance/banking-industry-faces-new-financial-landscape-a-candidate-driven-marketplace/.

Shawbel, Dan. Forbes (5 Nov. 2013). “Top 8 Workplace Trends In The Financial Services Industry.” http://www.forbes.com/sites/danschawbel/2013/11/05/top-8-workplace-trends-in-the-financial-services-industry/.

Goldman Sachs (Dec. 2013). “Themes in Investment Banking.” http://www.goldmansachs.com/our-thinking/trends-in-our-business/investment-banking/solomon-2014/index.html.

Turner, Matt. The Wall Street Journal (22 Jan. 2014). “Talent Wars: Four Ways Banks Can Compete with Tech Firms.” http://blogs.wsj.com/moneybeat/2014/01/22/talent-wars-four-ways-banks-can-compete-with-tech-firms/.

Tysiac, Ken. CGMA Magazine (9 July 2013). “How Regulatory Challenges Are Affecting Financial Services Industry.” http://www.cgma.org/magazine/news/pages/20138297.aspx?TestCookiesEnabled=redirect.

Strategy& (19 May 2010). “U.S. Wealth Management Survey: Trends and Emerging Business Models.” http://www.strategyand.pwc.com/global/home/what-we-think/reports-white-papers/article-display/wealth-management-survey-trends-emerging.

VanDeren, Julia. Enterprising Investor (20 Aug. 2014). “Poll: What’s Your Outlook on Job Growth in the Financial-Services Sector?” http://blogs.cfainstitute.org/investor/2014/08/28/poll-whats-your-outlook-on-job-growth-in-the-financial-services-sector/.

Wade, Matt. The Sydney Morning Herald (7 Oct. 2014). “Sydney Struggling to Keep Up As Technology Challenges Financial Services Industry.” http://www.smh.com.au/nsw/sydney-struggling-to-keep-up-as-technology-challenges-financial-services-industry-20141006-10qoza.html.

McKinsey & Company (Nov. 2012). “Winning Strategies for China’s Financial-services Sector.” http://www.mckinsey.com/insights/financial_services/winning_strategies_for_chinas_financial-services_sector.