Volatility term structure and estimation of yield curve ... · Volatility term structure and...

26

Volatility term structure and estimation of yield curve: Inferring their connections and movements Ana Maria A, ChirinosLeañez ¥ Miriam Maita Bolívar This version: October 2012 Abstract: This paper estimates yield curve under forward interest rates and its conditional variance for two types of markets; domestic and external debt market, using monthly data from January 2004 to December 2011 and from April 2005 to December 2011, respectively. Yield curve is estimated using the parametric model proposed by Nelson Siegel (1987) and the conditional variance is computed under stochastic volatility model characterization (EGARCH). We find the vast majority of estimations displayed an upward sloping yield curve in each market, excluding recession periods in which yield curve showed downward sloping pattern. At the end of the sample humped shaped was exhibited. Other findings reveal yield curve parameters of long term component (level) could be mainly connected to economic fundamentals and market risk expectations at the same time (CDS and EMBI). While short term component of the yield curve (slope) might be affecting by price variables (nominal depreciations of non - official exchange rate, expansions in oil prices and inflation). Additionally, short term bonds are more volatile compare to other maturities horizons, especially those instruments issued in external debt market. Finally, positive economic performance could reduce conditional variance of bond returns in both markets. Key words : yield curve, volatility term structure, conditional variance, Venezuelan bond market, local debt market, foreign debt market, Nelson-Siegel model, investors’ expectations, level, slope and curvature JEL classification code: C13, C21, G12, N26 ¥ Economic Analyst of the Research Department at Central Bank of Venezuela and Professor of Universidad Católica Andres Bello, [email protected] Economic Analyst of Economic Analysis Department at Central Bank of Venezuela, [email protected]

-

Upload

nguyenxuyen -

Category

Documents

-

view

220 -

download

0

Transcript of Volatility term structure and estimation of yield curve ... · Volatility term structure and...

Volatility term structure and estimation of yield curve: Inferring their connections and movements

Ana Maria A, ChirinosLeañez¥

Miriam Maita Bolívar

This version: October 2012

Abstract:

This paper estimates yield curve under forward interest rates and its conditional variance for two types of markets; domestic and external debt market, using monthly data from January 2004 to December 2011 and from April 2005 to December 2011, respectively. Yield curve is estimated using the parametric model proposed by Nelson Siegel (1987) and the conditional variance is computed under stochastic volatility model characterization (EGARCH). We find the vast majority of estimations displayed an upward sloping yield curve in each market, excluding recession periods in which yield curve showed downward sloping pattern. At the end of the sample humped shaped was exhibited. Other findings reveal yield curve parameters of long term component (level) could be mainly connected to economic fundamentals and market risk expectations at the same time (CDS and EMBI). While short term component of the yield curve (slope) might be affecting by price variables (nominal depreciations of non - official exchange rate, expansions in oil prices and inflation). Additionally, short term bonds are more volatile compare to other maturities horizons, especially those instruments issued in external debt market. Finally, positive economic performance could reduce conditional variance of bond returns in both markets. Key words: yield curve, volatility term structure, conditional variance, Venezuelan bond market, local debt market, foreign debt market, Nelson-Siegel model, investors’ expectations, level, slope and curvature JEL classification code: C13, C21, G12, N26

¥ Economic Analyst of the Research Department at Central Bank of Venezuela and Professor of Universidad Católica Andres Bello, [email protected] Economic Analyst of Economic Analysis Department at Central Bank of Venezuela, [email protected]

2

Introduction hilarious

Which are the main factors driving shape of yield curve and volatility term structure

(VTS)? Are these representing market expectations? Is there any difference between

VTS and term structure of interest rates (TSIR) depending on the type of market in

which bonds are issued (local market or foreign market)?

An extensive body of the literature has analyzed common factors that affect yield curve

(Litterman and Scheinkman 1991, Dielbod-Li 2005, Pérignon and Villa 2006).

Nevertheless, a new trend of financial researches have focused on the second moment of

this financial indicator (Benito and Novales 2005, Diaz et al. 2010b and Jareño and

Tolentino 2011), as a new mechanism of extracting information for risk portfolio

management, and predicting future movements of interest rates.

For Venezuelan economy, levels of government bonds issued either local or foreign

markets have increased from 2006 onwards (an average growth of 39% and 12%

respectively), motivating empirical research regarding fixed income securities. In this

context, Chirinos and Moreno (2009), and Maita (2011) build the TSIR using

parametric approaches for a small group of debt securities. They find that different

shapes of the yield curve are attributed to variations in three elements: level, slope and

curvature (Litterman and Scheinkman (1991)). However, to the best of our knowledge,

there is no previous empirical research that has addressed volatility term structure for

Venezuelan debt market (domestic-foreign) or associated the possible factors that

generate its movements, and yield curve variations.

Purposes of this research are threefold: First we estimate yield curve under parametric

characterization (Nelson Siegel, 1987) including a wide spectrum of bonds for both

market during a recent period (2004-2011). Second, using EGARCH model, we

compute conditional variance of term structure of interest rates under instantaneous

forward rates. After that, and with the intention to reduce dimensionality of volatility

across maturities of bonds selected, we apply principal components analysis (PCA) to

obtain the main representative volatility factors. Third, we connect a group of

macroeconomic variables with the main unobservable factors of the yield curve and

3

volatility, with the purpose to establish conjectures concerning possible variables driven

movements on yield curve and VTS.

Determining changes in volatility term structure and its interrelations with yield curve

are relevant to comprehend investors’ expectations, which are a useful tool for policy

makers. Nowadays, this tool of analysis has become in an alternative way, especially

after financial crisis, of understanding a fraction of the intrinsic movements of financial

market.

This paper is divided into five sections: First section describes theoretical framework

used to estimate yield curve and compute conditional variance. Second section explains

the estimation methodology. Third one characterizes features of the data, while fourth

section shows empirical results. Finally last section summarizes main concluding

remarks.

1. Theoretical Framework 1.1 TSIR estimation

Extensive approaches of the estimation of term structure of interest rates have been

applied by financial literature1, including stochastic term structure models and affine

term models (Vasicek 1977, Cox, Ingersol and Ross 1985, Hull and White 1990, among

others) and the parametric or parsimonious representations. These characterizations

summarize the key hypothesis behind fixed income analysis2. First group of models are

built under the main assumption that interest rates follow a stochastic process. However,

issues arise to fit observed yield data and in terms of computational tractability for

empirical scenarios. Such problems are dealt under parametric models, since they

provide good fit with a minimum level of requirements for empirical applications.

Having said that, we decide to estimate Nelson Siegel (NS) model, which is the typical

characterization of parsimonious modelling of the interest rates. Specifically, we

compute yield curve using instantaneous forward interest rates (rates at which contract

1See Chirinos and Moreno (2010) for an extensive description 2Expectation hypothesis theory ( Fisher, 1930), market segmentation theory ( Culbertson, 1953), preferred habitat theory (see Modigliani and Sutch, 1966) and liquidity preference theory ( Hicks, 1946).

4

are negotiated at future dates)3. Since doing so, it is possible to separate short, medium

and, more important, long expectations of investors that are imbedded in the yield

curve.

Under NS model instantaneous forward rate is given by following function:

where T denotes maturity, f(t,T) is the forward rate for period [t,T], and ,,, 210

are the coefficients to be estimated4. Terms of equation (1) can be interpreted in the

following fashion: 0 measures long-term component (positive constant) and it is

frequently associated to indicators of economic fundamentals. The second term,

T

exp1 , is related to the component of the short term. This coefficient can be

monotonically decreasing or increasing depending on the sign of 1 . The third

component

TT

exp2 is the medium term component, responsible of generating

the hump shapes and U shapes that the term structure can exhibit. The parameter

depends on the rate at which the forward rate achieves its asymptotic value ( 0 ) and

must be positive since it is a time constant variable.

The main advantage of this model is to capture all the possible shapes that yield curve

usually can exhibit over the time (monotonic, hump and even S shapes).

According to Dai and Singleton (2000) a considerable fraction of movements and

shapes of yield curve are mainly attributable to unobservable factors called level, slope

3From a theoretical perspective, spot rates are often used to construct the yield curve. This concept tends to be understood as the yield to maturity. Nevertheless both concepts differ. The yield to maturityis the internal rate of return at time t on a debt security with maturity s = t + T. The rates r(t,T) considered as function on T will be referred as the continuously compounded spot rates. It can be shown that

),(log1

),( TttPT

Ttr T>0, where P is the corresponding bond price for the period [t,T].

4In their original version Nelson-Siegel (1987) implement ordinary least-squares to estimate equation (1)

since the parameter is settled in a range of values. As mentioned, this paper estimates the time constant parameters.

These authors do estimate and compute equation (1) for a reasonable range of values for this parameter. In contrast to this, and following Svensson (1997), we determine all the parameters of the model.

(1)

TTT

Ttf expexp),( 210

5

and curvature. Diebold and Li (2002) find that parameters of Nelson Siegel model can

be interpreted as such latent factors, where 0 is the level, 1 the slope and 2 is

curvature. From now on, we use this result to refer to these parameters

1.2 Volatility Estimation Understanding the way and the reasons why fixed income returns change, is crucial to

comprehend movements of yield curve and somehow investors’ strategies as well.

During decades, this have been one of the main proposes of asset prices and risk

management literature. In fact, during nineties, financial researches have dealt with

uncertainty in asset returns analysis through time-varying variance models; this means

the autoregressive conditional heteroskedasticity (ARCH) by Engle 1982, and its

generalized extension (GARCH) by Bollerslev, 1986. These models were developed to

satisfy the uncertainty regarding fluctuations of asset returns.

Both characterizations improve volatility forecast compared to constant variance

models. However, non negative restrictions on the parameters must be imposed in order

to preserve positive variance estimations, which in some cases, implies large

computations to satisfy the restrictions imposed. Besides, ARCH models require a

considerable amount of lags to capture the nature of volatility in a parsimonious way,

but this does not imply that nonnegative constraints will be satisfied. Additionally, these

models are unable to detect, the well known, leverage or “asymmetric” effect imbedded

in asset price variations. Such effect occurs when an unexpected drop in prices (bad

news) increases predictable volatility more than proportionally than an unexpected rise

in prices (good news) of similar magnitude (Black Scholes, 1976). In consequence,

literature has extended original GARCH models in order to consider an asymmetric

representation5. One of these models is the exponential GARCH (Nelson, 1991). Under

this characterization conditional variance is defined in the following way:

5See Bollerslev et al. (1992) for a more extensive discussion of stochastic volatility models.

(2) 2

)log( logj-t

j-t

1j-t

j-t

11

22

q

jj

q

jj

p

i

itit

ttt z )1,0(~ Nzt

6

2Where is the conditional variance at time t, that is function of three elements:

mean (w), p lags of conditional variance (GARCH term), q lags of standardized news

(ARCH term) and q leverage terms. Logarithmic form of equation (2) leads to avoid

negative variance from the sign of coefficient β. Besides measures the leverage

effects of asset returns, such effect appears when 0 , which implies that a negative

value of this term implies negative shocks has more impact on volatility that positive

shocks, the asymmetric effect occurs when 0

2. Data

Data used for local debt market, includes Venezuelan treasury bills and government

bonds negotiated during January 2004 to December 2011 and denominated in local

currency (Bolívares), this means internal public debt. This set of instruments includes a

combination of periodic and not periodic interest payments. In the case of treasury bills

pay not periodic interest payments and their maturity range goes from 91, 105, and 182

and to 364 days. In the case of government bonds, we consider fixed coupon bonds

(Títulos de interésfijo -TIF) and variable coupons instruments (Vebonos). Interest

payments of variable coupon bonds are indexed to treasury bills of 91 days. For these

last debt instruments, cash flows are computed assuming a future rate of 12%, obtained

from historical analysis of domestic coupons bonds. Data selected for this market

includes 72 Vebonos, 29 TIF and an average of 20 treasury bills instruments. Spectrum

of maturity for these types of securities is not superior to 15 years.

On the other hand, we use monthly data from April 2005 to December 20116 in external

market. In this market, debt securities are mainly fixed coupon instruments issued by

Venezuelan government and denominated in US$ dollars; which represents a portion of

its external public debt. Data selected includes a set of 14 bonds with a maturity horizon

around 30 years.

For both markets, information regarding debt instruments includes: clean prices, yields

to maturity, coupon rates, coupon payment dates and maturities. Such variables were

obtained from Reuters (external debt market), and Sistema de Custodia Electrónica de

Títulos -SICET (local debt market). All trading negotiations refer to secondary market

6Sample of each market differs since we consider as estimation requirement at least an amount of 10 bonds to estimate yield curve, and this conditions is fulfill for foreign debt market after 2005. We consider necessary, at least, 10 instruments since NS characterization requires a minimum set of 4 observations.

7

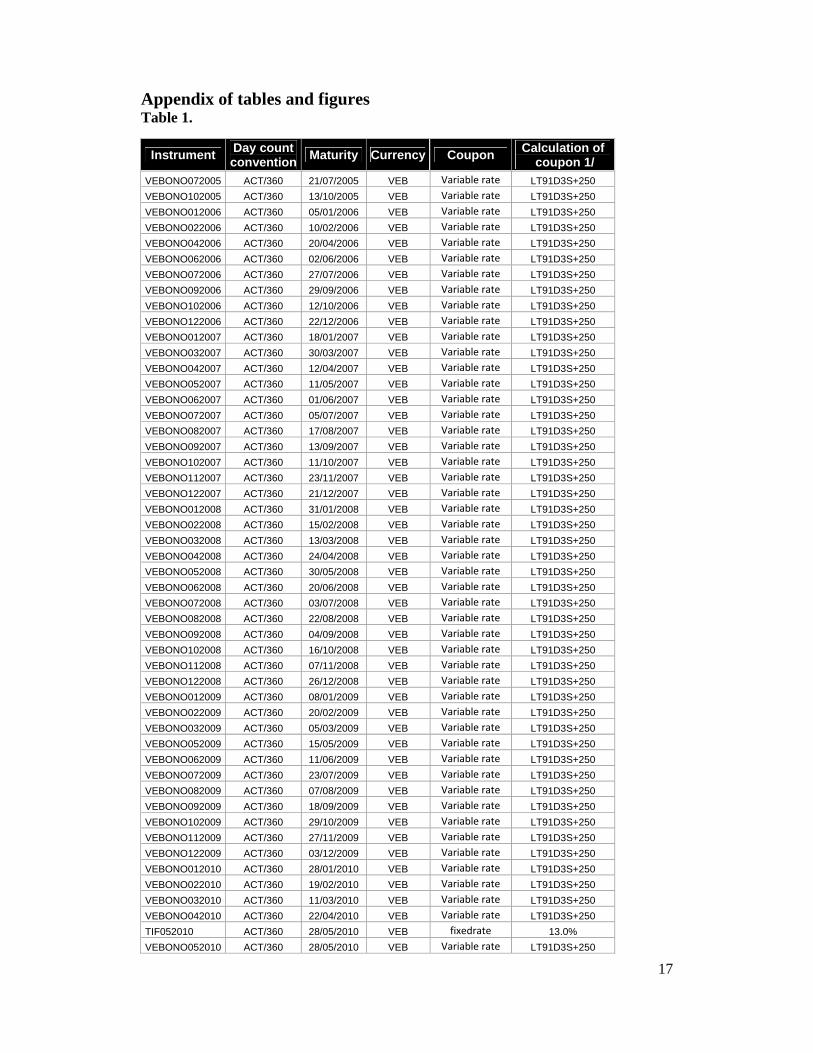

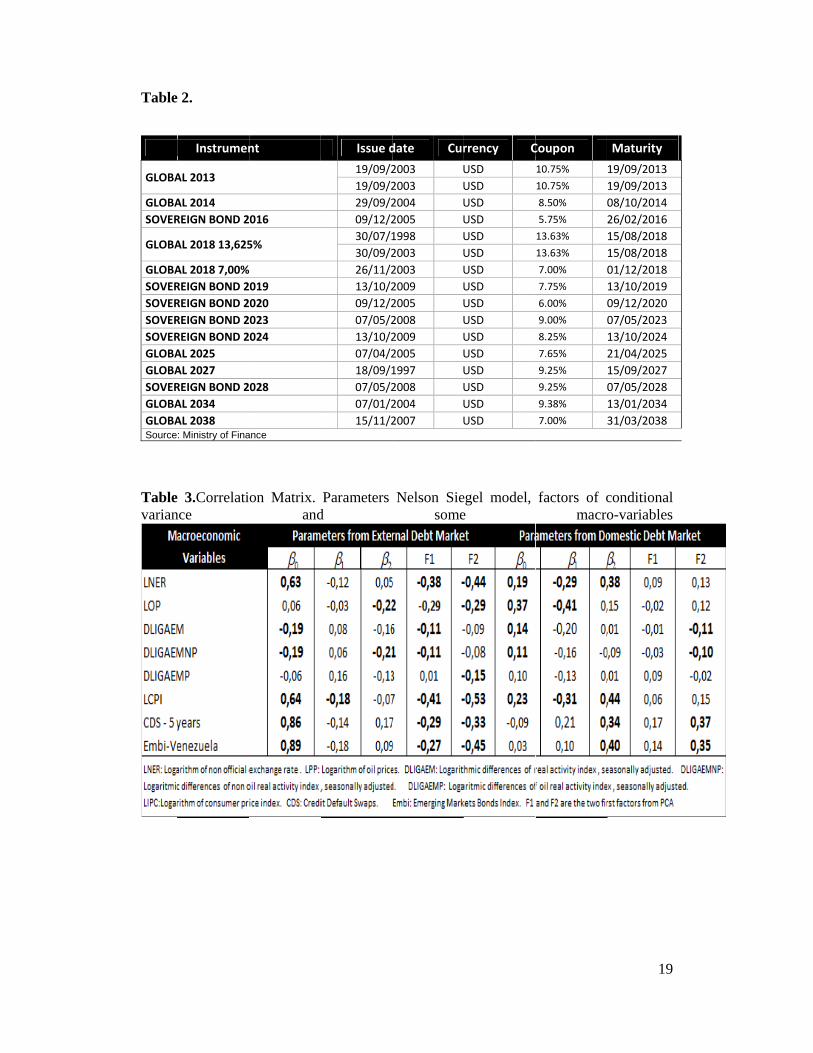

transactions. Table 1 and table 2 show main features of data used ranked by time to

maturity.

3. Estimation methodology In order to estimate equation (1) we apply a non-linear least-squares regression

technique to fit the cross- sectional set of monthly data for the markets evaluated7.

Fitting procedure is computed under an optimization problem (i.e. minimization of

squared errors between observed and estimated yield) with an initial set of parameters

for the coefficients to be estimated. The assumptions used to select the ranges of starting

values are the following: 0 represents yield of the bond with longest term to maturity

in the data sample; 1 is the difference of the yields between the longest and shortest

term to maturity; 2 is the associated to yields of bonds with medium-term to maturity

and is the average maturity of bonds in medium term. 0 and were constrained to be

positive as the model predicts.

Optimization mechanism requires error minimization yields, defined as the difference of

the equation (1) respect to historical observed yields. Even when optimization do not

minimize price errors, along the estimation procedure we compute, after each iteration,

cash flows related to every instrument and theoretical prices8 for the different

parameters of NS model. In this way, we simultaneously obtain the theoretical price

associated to the forward rate that minimizes yield errors.

To guarantee accuracy of the final results, different (increasing) numbers of replications

were considered through the algorithm of Gauss Newton. Once forward rates are

estimated under equation (1), we determine conditional variance according to equation

(2) for cross sectional dataset of two markets. In this fashion, we get conditional

volatility, for each instrument associated to a specific maturity. In short, this leads us to

7As alternative techniques, Maximum Likelihood Estimator (MLE) or Generalized Method of Moments (GMM) can be also applied 8

),(),(1

TtDCFTtPN

tNN

, where CF are the cash flows of the Nth bond and D (t,T) is the discount

function.

8

obtain volatility term structure. For comparative purposes, we reduce dimensionality of

conditional variance across the amount of bonds considered and maturities; using its

representative factors through principal components analysis (PCA). Finally, we

compare these factors representing volatility and parameters 0 , 1 , 2 with a group of

macroeconomic variables, to infer their possible interrelations and the reasons that

generate movements on yield curve and the volatility of term structure.

4. Empirical results 4.1 TSIR analysis and parameters from NS This section analyzes the term structure in terms of the shapes of the yield curve y and

its variance, providing conjectures of their different shapes exhibited, depending on the

market in which they were traded and issued. For the whole sample (both markets) we

find three types of yield curve: upward sloping, downward sloping, and humped yield

curves9. Description of different periods related to these patterns is summarized in the

following paragraphs of this section.

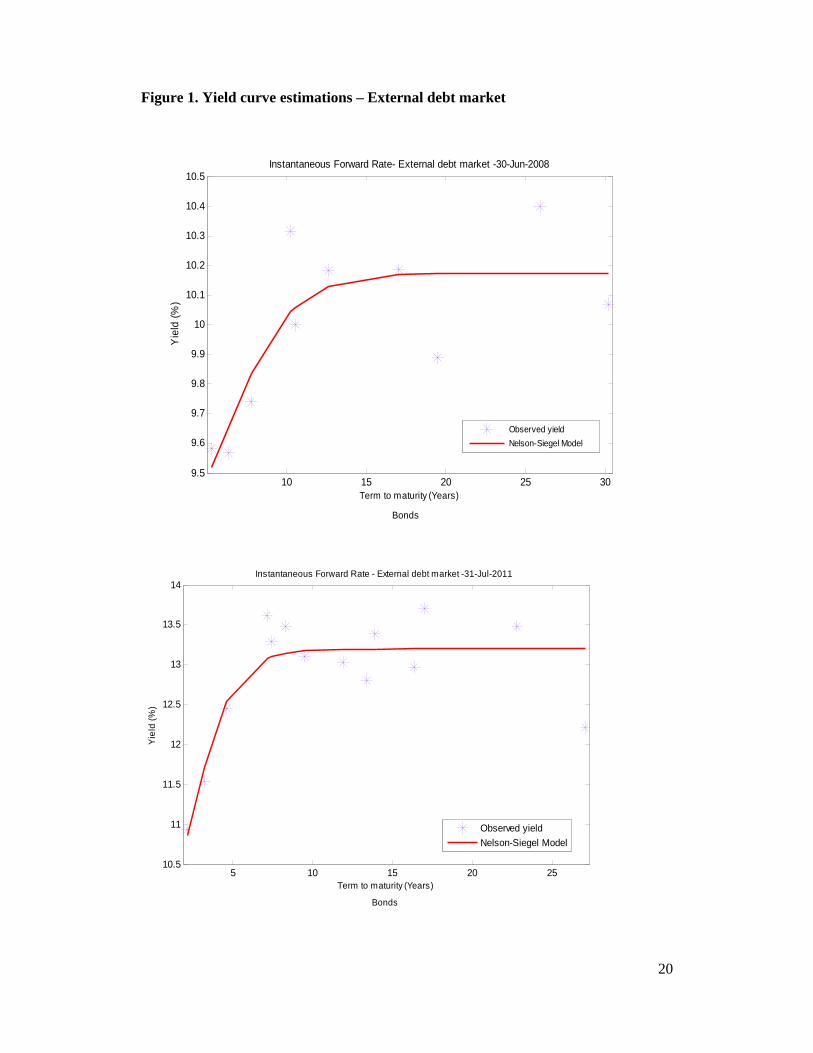

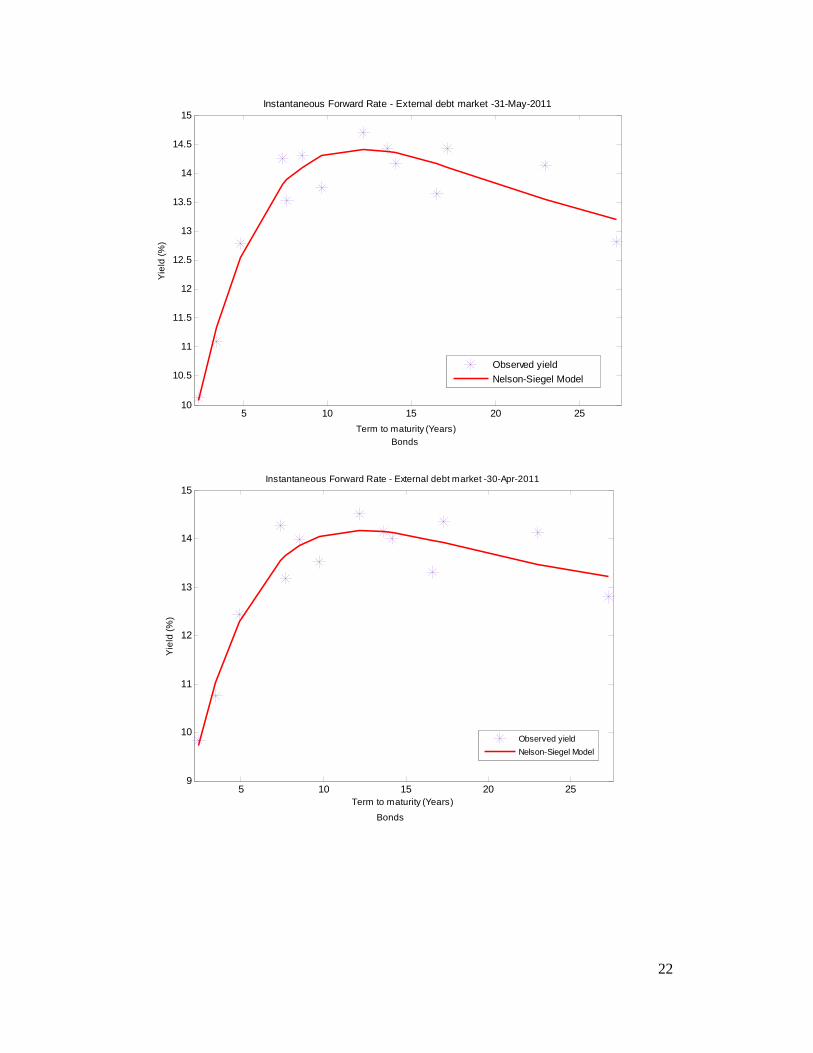

For external debt, during May 2005- September 2008, a positive or normal pattern was

exhibited by yield curve. Domestic debt market replicated this fashion from July 2005

to June 2008. Presence of “positive” yield curves would corroborate expectation

hypothesis theory, that claims that forward rates increase along maturities and those are

always higher than future spot rates. However, one can argue that bond holders are so

risk adverse, that they invest in short term maturities, and the only way we able to hold

long term bonds if they get a risk premium in exchange to face higher levels of

exposure10. Additionally and using the theory of term premium (captured by the slope

of term structure, i.e. spread of long term and short term interest rates) and its positive

relation with economic growth and inflation rate (Fama 1990, Miskin 1990a, and

Estrella and Mishkin, 1996).So, upward sloping yield curve would be reflecting

Venezuelan bond holders’ expectations about economic growth in the future and

inflationary pressures. Indeed, empirically speaking, the period mentioned for positives

yield curve coincides with GDP annual growth rates above 5% accompanied with 9Even when extended version of Nelson- Sigel model ( Svensson, 1994) was formulated to captured the “humped” yield curves, the application of the original Nelson Siegel characterization was able to reproduce them. 10 This theory is called liquidity preference; see Hicks (1946) for more details.

9

variations of consumer prices index (CPI) around 20%. It seems that there exist

elements to infer that such economic performance could have been extracted from the

information imbedded in yield curve.

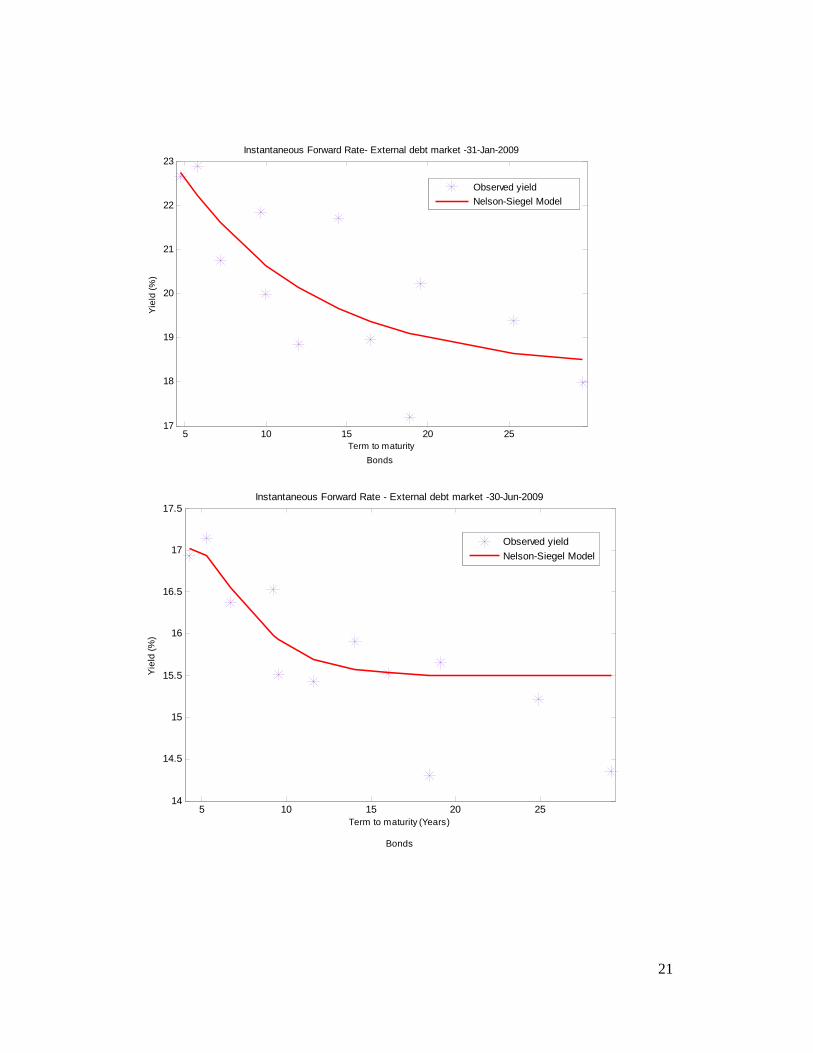

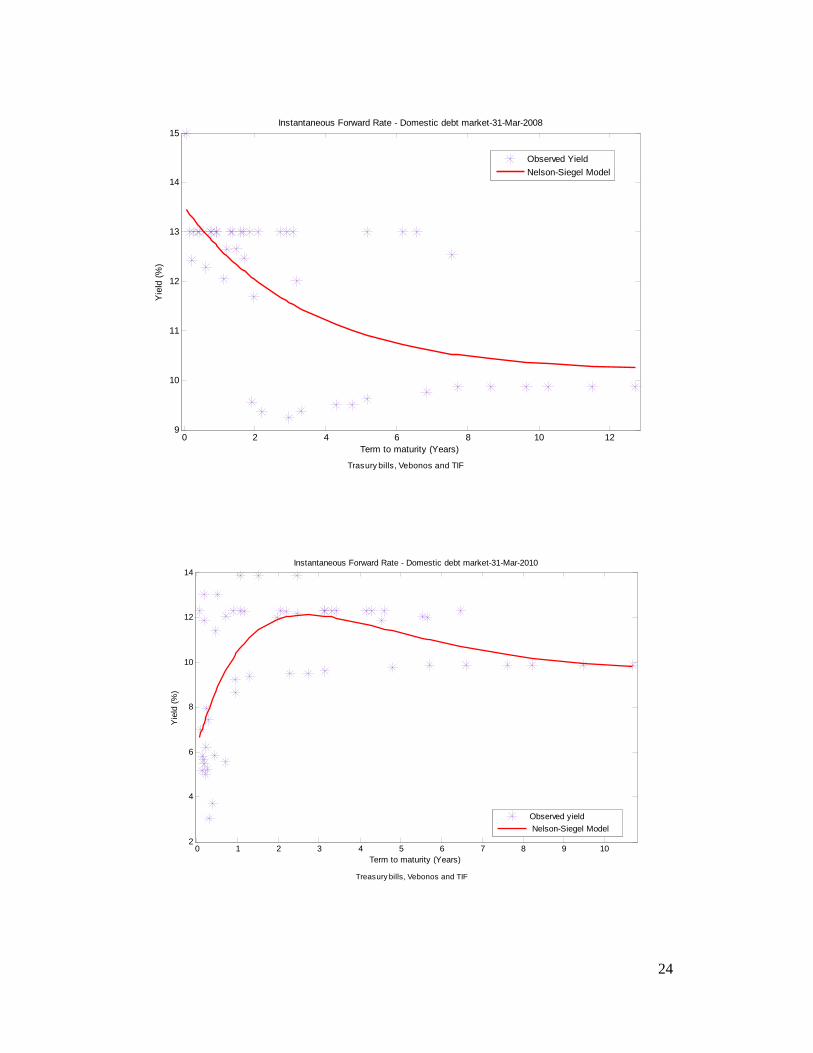

However, in the period October 2008 - July 2009, foreign yield curve reverted its

positive sloping pattern into an inverted one. In the domestic debt market this type of

curves is replicated during February 2008 to August 2009. Theoretically a downward

sloping yield curve occurs when short-term yields exceeds long term rates. These curves

are commonly used as leading indicator of future recessions. In fact, it does not seem

fortuitous that these periods of time occur during the fall of oil prices (May 2008) and

the global financial collapse (September 2008). Even when Venezuelan economic

contraction effectively occurred during the first term of 2009, it is possible to argue that

traders anticipated the negative impact that contraction of oil market would be

generating on real sector due to dependence on oil exports.

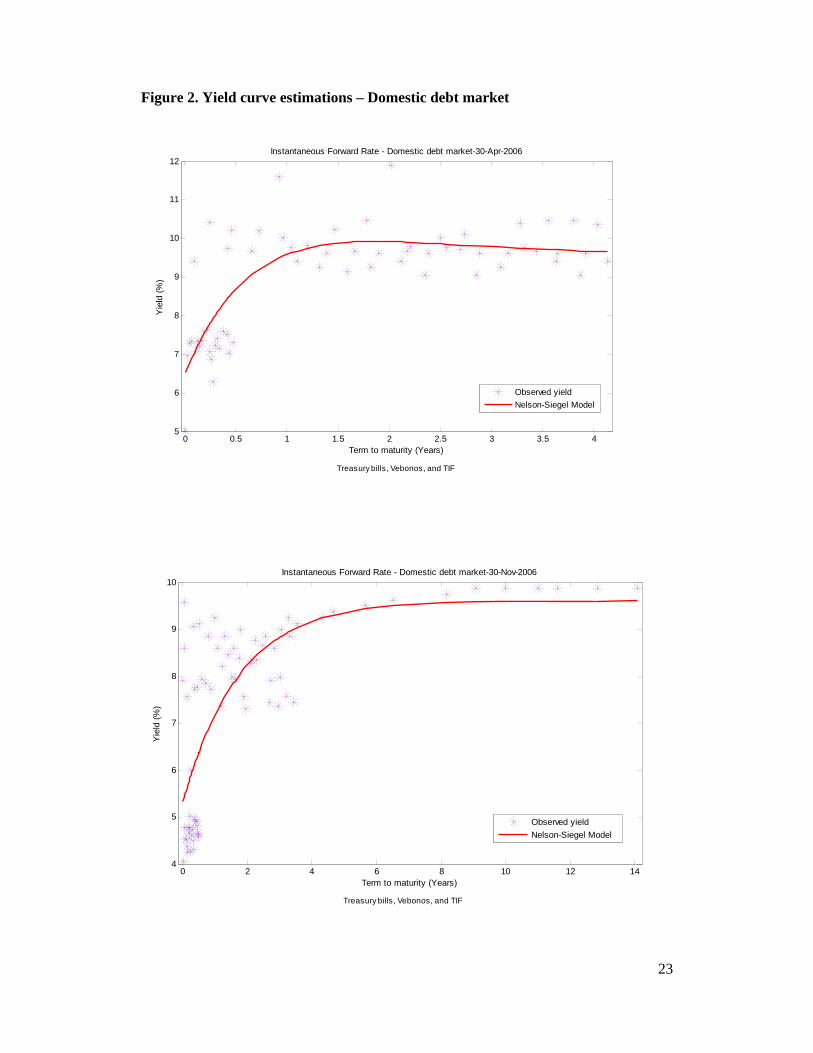

On the other hand, last type of pattern showed by the yield curve was the “humped”

shaped. A key issue is that this pattern appears mainly for the shortest maturities, to

then decrease from mid-term to long term maturities. For external debt market, such

“humped” behavior is presented in two periods: November 2009 - February 2010, and

August 2010 - January 2011. This is because long term bonds (30 years) in this market

were more liquid and had stable returns over time than short term bonds, which reported

the highest variations of their yields.

For domestic debt market, humped yield curves appeared from January 2009 to the end

of the sample. For this market, humped pattern was associated to maturity of four years;

where the hump achieved its maximum value to start to decline for the rest of

maturities. Such feature is mainly attributable to the borrowing strategy implemented by

the National Public Credit Office during 2009-2010, in where financial instruments

were issued around 4 years of maturity.

Figure 1 and figure 2 shows all the patterns described in this section.

10

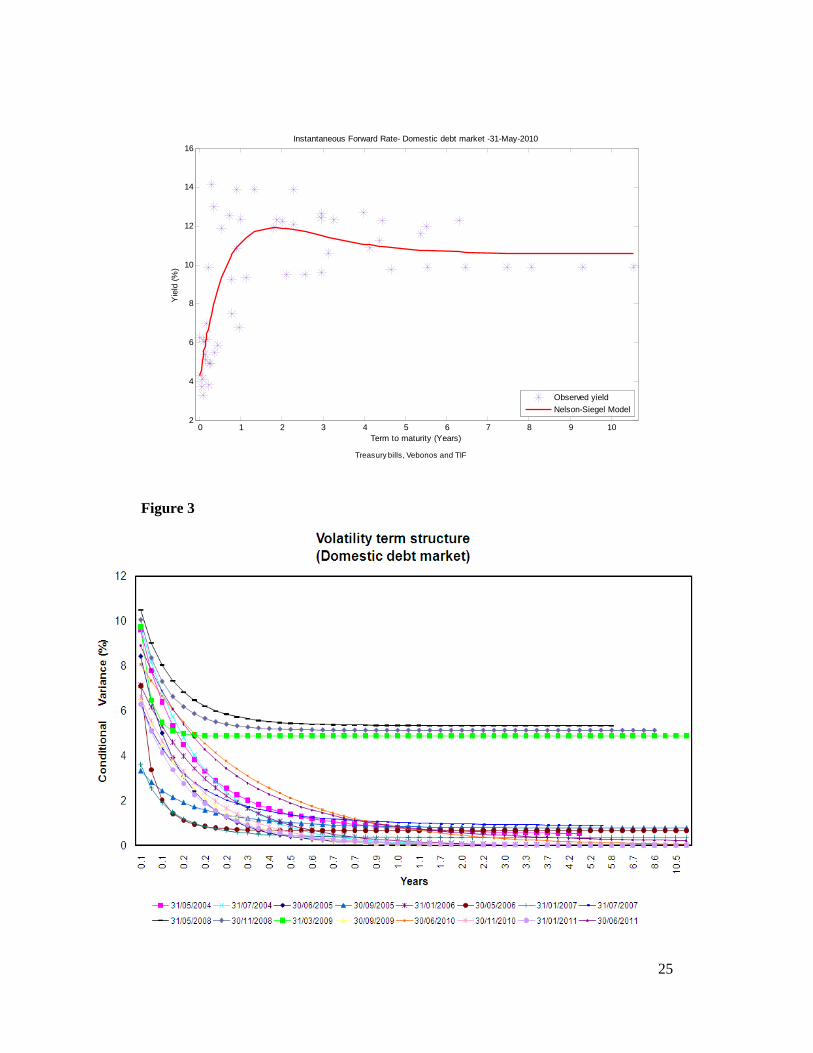

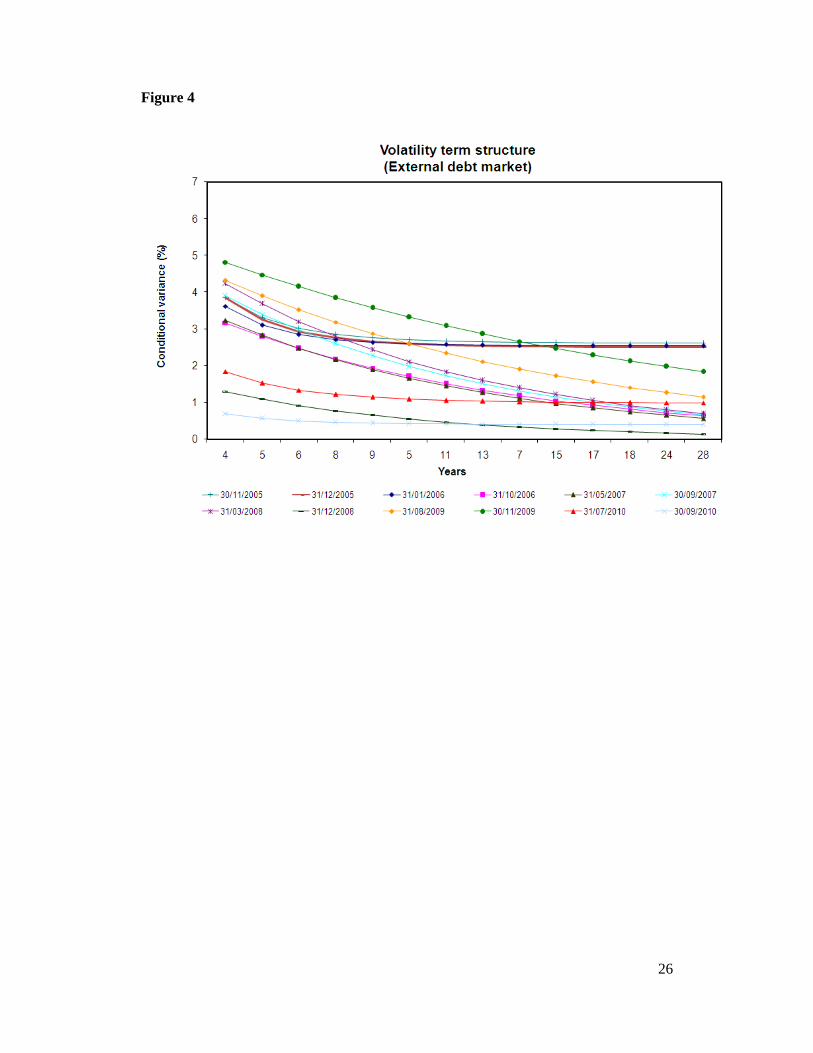

4.2 Volatility term structure

The second moment of the TSIR was computed using EGARCH (1,1) model. Results

reveal some similar characteristics regarding volatility term structure for both markets.

External market results’ along the whole sample indicates that bonds with maturity

inferior than 12 years are more volatile than long term bonds (16 – 30 years of term to

maturity). We emphasize the period October 2008 - July 2009, in which yield curves

were downward sloping, the entire structure of observed yields increased abruptly (

from 14% to 19% ) across all maturity spectrum, especially more than proportional for

those short term debt securities (figure 3). This effect modified the magnitudes of

conditional variance for all bonds outstanding. However, it was reverted in 2009, when

observed bond returns recovered their initial trend (10% -13 % in average).

On the other hand, conditional variance, for short term bonds (less than 3 years) issued

on domestic market are superior that variance of long term bonds. Indeed, this feature is

replicated along the sample as well (figure 4). As shown in external debt market, during

2008 and the beginning of 2009, the level of conditional variance rises across

maturities. For both markets, as argued in previous section, the fall in oil prices could

explain the unexpected fluctuations in bond returns. Nevertheless, domestic

instruments, historical yields did not return to their previous levels as external debt

market did.

So, it seems that independently the type of market considered, in terms of second

moment of TSIR, debt securities instruments with short term to maturity have a high

conditional variance. However, when both markets are compared between them, since

maturity horizons differ, if we abstract of negotiation conditions, short term bonds from

foreign market would be equivalent to long term bonds of domestic market. Under this

scenario and using the basis of financial foundations; long term bonds tend to show

stable returns across time. These debt instruments display a VTS superior to the

expected for the maturity associated.

11

4.3 Parameters from NS, principal components analysis (PCA) of VTS and some

macro variables

Previous section has analysed, how the shapes and movements of yield curve are

interrelated with VTS, but the underlying set of possible variables that make changes on

both financial indicators are still missing in the analysis. In this context arises the

typical question regarding macroeconomic factors driven their variations. Literature has

tried to generate a macroeconomic interpretation of yield curve (Litterman and

Scheinkman 1991, Bliss 1997, Wu 2001,Dielbod-Li 2005, Pérignon and Villa 2006).

The last purpose of the research is to establish different signals respect the variables that

promote variations on these financial indicators. We do not pretend to statically

determine a model to reproduce such movements, instead we just conjecture the

potential relations among a selection of macroeconomic variables, parameters of NS

model, and conditional variance of forward rates. In order to do so, as mentioned in

section 3, dimensionality of conditional variance must be reduced. So, we shrink the

range of maturities and number of bonds for each type of market using PCA. Previous

researches, Novales and Benito (2007) and Diaz et al. (2010), apply same analysis for

Spanish debt market. For Venezuelan case, and to our knowledge, this is the first

approximation applied to debt market. Using PCA, we select the two first factors (F1,

F2) for each market that account around 98 % of accumulative variance for both

markets, and they represent the volatility of instruments of short and medium term.

Using these factors, we compute a correlation matrix (Table 3), taking into account

parameters estimated from NS ( 210 ,, ), and some macroeconomics and financial

variables. Financial variables selected are: Credit Default Swap (CDS) and Emerging

Market Bond Index (EMBI). Both variables refer to investors’ expectations about

economic performance and government financial health. Economic variables selected

and showed statistically significant relations are: non official exchange rate (NER), oil

prices (OP), and indexes for: monthly real activity (IGAEM), monthly real oil activity

(IGAEMP), monthly real non - oil activity (IGAEMNP), and the consumer price index

(CPI). Variables coming from real sector are expressed in logarithmic differences, while

variables associated to prices (exchange rate, oil prices, and CPI) are included in

logarithmic levels.

12

Establishing the degree of lineal association, we find that long term component ( 0 ) of

foreign market is positively correlated with CDSand EMBI (89% and 86%

respectively). These variables are common referred as reflecting the implicit risk in the

conditions of debt market; it is possible conjecture that movements in the level of yield

curve could be mainly associated to changes in the market valuation of financial

conditions for Venezuelan government. Besides, this parameter for foreign debt market

is moderate correlated with positive changes in non- official exchange rate (63%) and

CPI (64%). These lineal relationships are remained in direction but they decrease in

magnitude for local debt market (19% y 23% respectively). For the Venezuelan

economy and due to the existence of exchange control rate, depreciations that occur in

non- official market are directly translated into the returns of the instruments negotiated

in debt market. The link of 0 with changes in CPI has been previously pointed out by

Wu (2003). According to this author and since this unobservable parameter refers to the

long term expectations, movements in expected inflation rate would finally alter real

long term interest rates and influence the level of yield curve. In few words, as a result

of high inflation expectations, agents anticipate the rise in interest with the intention of

mitigate the effects of future inflation pressures.

Besides, its links with price variables, there exists lightly relationship between 0 and

the real sector. Magnitudes of this relationship are partially similar for both markets;

however, sign of direction is the opposite. In foreign market, long term component and

productive sector are related in a negative way. Intuition behind this is the following:

Since the level can be considered as a proxy of credit risk, adverse economic conditions

will exacerbate expectations of a poor financial performance of government sector.

Nevertheless, in internal debt market the association is essentially positive; clamming

that under economic growth scenarios returns of instruments increase, shifting the level

of yield curve as a whole.

Even, when oil prices do not show high correlation with foreign long term parameter, as

we can expect, it does for domestic market. A boost in oil prices would tend, ceteris

paribus, to shift the level of yield curve as the rest of real variables do.

On the other hand and for both markets, the short term component of yield curve ( 1 ) is

negative affected by inflationary pressures. As mention in section 1, this last parameter

13

is well known as the slope of yield curve, which means that periods with high inflation

rates would shift down slope of term structure of interest rates. Therefore, not only

positive variations in prices contract slope of yield curve, depreciations of non official

exchange rate, and the increment in oil prices, cause the same outcome in the local debt

market. In short, changes of price variables impact slope of yield curve for the

Venezuelan debt market.

Foreign medium term component ( 2 ), that measures curvature and steepness of yield

curve, is negative related with oil prices (22%), i.e. during episodes of drop in oil prices

humped shapes are more likely to occur. This could explain the presence of this

characteristic in external market at the end of 2008, when oil prices abruptly declined

after a period of expansion. In the case of domestic, external variables (non- official

exchange rate, CDS and EMBI) and prices could be driven changes in the curvature of

yield curve, and they would reproduce a steeper yield curve as well. Besides, we figure

out that humps, in the internal market, are more likely to take place for short term

maturities while in the external market such humps are linked to medium term

instruments.

Regarding the factors (F1 and F2) extracted from conditional variance, the factor of

short term volatility (F1) of foreign market, is negative correlated with all the variables

in table 3. However, the strongest correlation comes from non- official exchange rate

and CPI. Relevant is the small relationship between this factor and real sector variables,

which implies that under economic expansions volatility of foreign short term debt

instruments is reduced, due to expectations of Venezuelan bond holders improves and

the speed at which instruments are traded with arbitrage opportunities purposes

declines. These relationships, excluding real variables, remain for the factor of medium

term volatility (F2) of foreign debt market. Although, F2 for domestic market,

reproduce correlations of similar magnitude than factor of short term volatility of

external market for real variables; contractions in real production volatility of medium

term bonds increases. Therefore, this factor shifts its value as a result of a greater credit

risk.

14

Different from the results found by Diaz et al. (2010), in which factors of conditional

variance are equivalent to the unobservable components of NS model, for the

Venezuelan case, these relationships are negligible.

5. Concluding remarks

The versatility of term structure and its ability to connecting the puzzling associations

between macroeconomic variables and financial systems is one of the arguments to

argue why this indicator is continuously used by analyst and policy makers. After

consequences of subprime crises, financial world found another way of extracting

information regarding investors’ expectations, through the volatility of the yield curve.

When we analyze Venezuelan debt market comparatively is relevant the way how the

patterns exhibited by yield curve are shared for external and domestic debt instruments,

during analogous period of time. Even when is true, that negotiation conditions of debt

instruments differ across market, investors expectations’ of their bond holders seem to

follow same tendency and be caused by the same factors. Remaining question is

whether both markets simultaneously share invertors.

Alternatively, at the beginning of the sample the vast majority of the estimations

displayed an upward sloping fashion coinciding with periods of economic expansion.

However, during the financial distress, drop in oil prices and contractions of Venezuelan

economic, representatives yield curve exhibited a downward sloping pattern while

humped yield curve characterized both market at the end of the sample used. These

movements of yield curve encourage the continuous conjectures of relationships

between real sector of the economy and shapes of yield curve. In this context, it does

not seem random that long term component of NS is strongly connected to the

economic fundamentals and variables related to financial risk (CDS and EMBI).

Besides, a shift down of slope of yield curve could be linked to depreciations, inflation

and oil price expansions, while steepness of yield curve is mainly driven by changes in

prices and external sector variables. It means that factors that alter slope of yield curve

are associated to price variables.

15

In addition, debt instruments of short term are more volatile than long term bonds.

Nevertheless, short term bonds from external debt market have a higher conditional

variance than their equivalent instruments, in terms of maturity, from domestic market.

In this sense, expansions of real sector would reduce volatility of debt securities in both

markets, i.e. under better economic performance, investor’s expectation improves and

the fluctuations of instruments traded decreases.

Finally, the naïve relationships discussed here are far away from being conclusive.

Evidently, there still remains an open questing that must to be dealt in further research

about incorporating in an appropriate statistical and mathematical representation,

macroeconomic elements for the estimation of yield curve and VTS.

References Black, F and Scholes, M (1973): “The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 72, pp. 637-659. Bollerslev, T.(1986). Generalized autoregressive conditional heteroskedasticity.Journal of Econometrics, 31, pp. 307-327. Bollerslev T, Chou R, Kroner, K. (1992). ARCH modelling in finance.Journal of Econometrics, 52, pp. 5-59. Benito, S. and Novales, A. (2005).A factor analysis of volatility across the term structure: the Spanish case, mimeo. Cox, J., Ingersoll, J and Ross, S (1985): An Intertemporal General Equilibrium Model of Assets Prices. Econometrica, 53, pp. 363-384. Chirinos, A. and Moreno, M. (2010). Estimation of the Term Structure of Interest Rates: The Venezuelan Case. Central Bank of Venezuela, Working paper series N° 119 (forthcoming) Culbertson, J.M. (1957). The Term Structure of Interest Rates. Quarterly Journal of Economics, 71, 485-517. Diaz, J. and Ibáñez, A (2006): Estimation with Applications of Two Factors Affine Term Structure for Mexico, 1995-2004, mimeo. Díaz A, Jareño F, Navarro E. (2010b). A Principal Component Analysis of the Spanish Volatility Term Structure.International Research Journal of Finance and Economics, 49, pp. 150-155.

16

Díaz A, Jareño F, Navarro E. (2011a). Term Structure of Volatilities and Yield Curve Estimation Methodology.Quantitative Finance, 11 (4), pp. 573-586. Diebold, F. and Li, C. (2005).Forecasting the term structure of government bond yields.Journal of Econometrics, 130, pp. 337-364 Engle, R. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of U.K. inflation.Econometrica, 50, 987–1008 Estrella, A. and Mishkin, F. (1996): Predicting U.S. recessions: Financial variables as leading indicators, Research Paper 9690. Federal Reserve Bank of New York. Fisher, I. (1930) Theory of Interest, New York, Macmillan. Jareño, F. and M. Tolentino (2011). The US volatility term structure: A principal component analysis. Journal of Business Management, 6(2), pp. 615-626. Kozicki, S (1997): Predicting real growth and inflation with the yield spread. Economic Review, Federal Reserve Bank of Kansas City, issue Q IV, pages 39-57. Litterman. R. and Scheinkman, J.(1991). Common Factors Affecting Bond Returns.Journal of Fixed Income, 1(1), pp. 54-61 Maita, M (2011). Estimación de una curva de rendimientos para los bonos de la deuda pública interna en Venezuela, mimeo. Modigliani, M and R. Sutch (1966).Innovations in Interest Rate Policy.American Economic Review, 56, 178-197. Nelson, C. R. and A. F. Siegel (1987). Parsimonious modelling of yield curves, Journal of Business, 60, 473-89. Perignon, C. and Villa, C. (2006).Sources of time variation in the covariance matrix of interest rates.Journal of Business, 79(3), 1536–1549 Svensson, L. (1994): Estimating and interpreting forward interest rates: Sweden 1992-1994, CEPR Discussion Paper Series, No 1051, October (also: NBER Working Paper Series, No 4871). Wu, Tao. (2003). What makes the yield curve move?. FRBSF Financial Letter, 15, June 6.

17

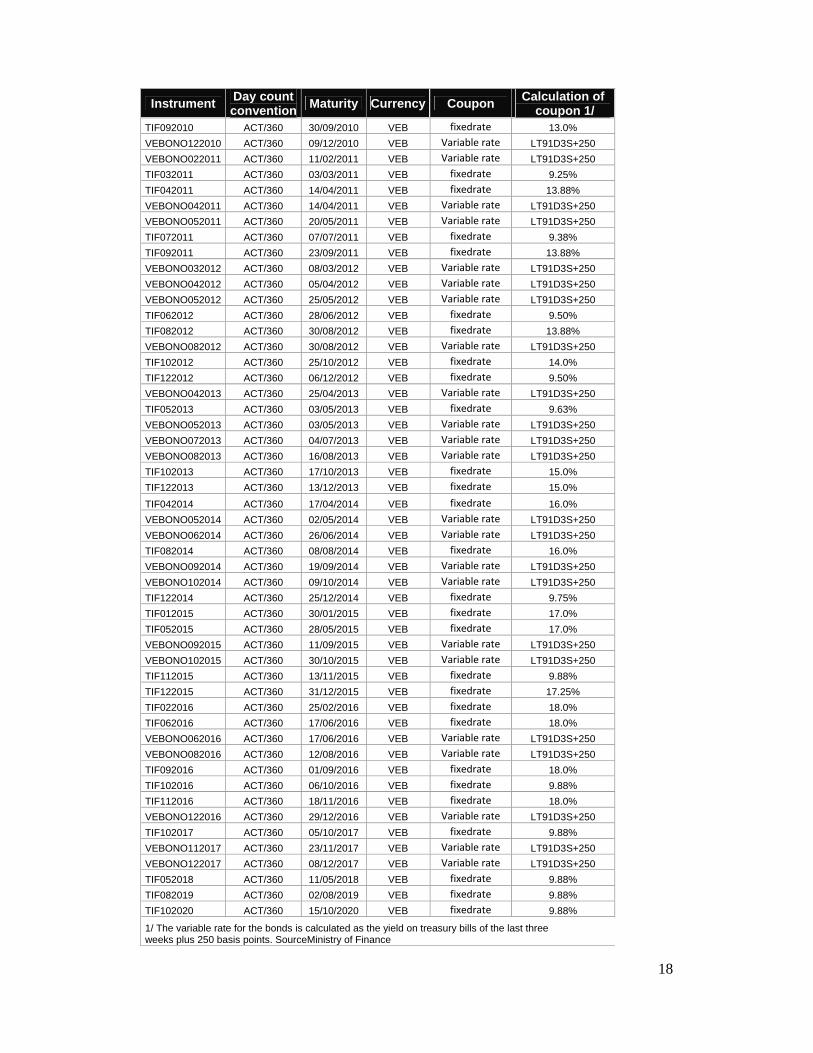

Appendix of tables and figures Table 1.

Instrument Day count convention

Maturity Currency Coupon Calculation of

coupon 1/

VEBONO072005 ACT/360 21/07/2005 VEB Variable rate LT91D3S+250

VEBONO102005 ACT/360 13/10/2005 VEB Variable rate LT91D3S+250

VEBONO012006 ACT/360 05/01/2006 VEB Variable rate LT91D3S+250

VEBONO022006 ACT/360 10/02/2006 VEB Variable rate LT91D3S+250

VEBONO042006 ACT/360 20/04/2006 VEB Variable rate LT91D3S+250

VEBONO062006 ACT/360 02/06/2006 VEB Variable rate LT91D3S+250

VEBONO072006 ACT/360 27/07/2006 VEB Variable rate LT91D3S+250

VEBONO092006 ACT/360 29/09/2006 VEB Variable rate LT91D3S+250

VEBONO102006 ACT/360 12/10/2006 VEB Variable rate LT91D3S+250

VEBONO122006 ACT/360 22/12/2006 VEB Variable rate LT91D3S+250

VEBONO012007 ACT/360 18/01/2007 VEB Variable rate LT91D3S+250

VEBONO032007 ACT/360 30/03/2007 VEB Variable rate LT91D3S+250

VEBONO042007 ACT/360 12/04/2007 VEB Variable rate LT91D3S+250

VEBONO052007 ACT/360 11/05/2007 VEB Variable rate LT91D3S+250

VEBONO062007 ACT/360 01/06/2007 VEB Variable rate LT91D3S+250

VEBONO072007 ACT/360 05/07/2007 VEB Variable rate LT91D3S+250

VEBONO082007 ACT/360 17/08/2007 VEB Variable rate LT91D3S+250

VEBONO092007 ACT/360 13/09/2007 VEB Variable rate LT91D3S+250

VEBONO102007 ACT/360 11/10/2007 VEB Variable rate LT91D3S+250

VEBONO112007 ACT/360 23/11/2007 VEB Variable rate LT91D3S+250

VEBONO122007 ACT/360 21/12/2007 VEB Variable rate LT91D3S+250

VEBONO012008 ACT/360 31/01/2008 VEB Variable rate LT91D3S+250

VEBONO022008 ACT/360 15/02/2008 VEB Variable rate LT91D3S+250

VEBONO032008 ACT/360 13/03/2008 VEB Variable rate LT91D3S+250

VEBONO042008 ACT/360 24/04/2008 VEB Variable rate LT91D3S+250

VEBONO052008 ACT/360 30/05/2008 VEB Variable rate LT91D3S+250

VEBONO062008 ACT/360 20/06/2008 VEB Variable rate LT91D3S+250

VEBONO072008 ACT/360 03/07/2008 VEB Variable rate LT91D3S+250

VEBONO082008 ACT/360 22/08/2008 VEB Variable rate LT91D3S+250

VEBONO092008 ACT/360 04/09/2008 VEB Variable rate LT91D3S+250

VEBONO102008 ACT/360 16/10/2008 VEB Variable rate LT91D3S+250

VEBONO112008 ACT/360 07/11/2008 VEB Variable rate LT91D3S+250

VEBONO122008 ACT/360 26/12/2008 VEB Variable rate LT91D3S+250

VEBONO012009 ACT/360 08/01/2009 VEB Variable rate LT91D3S+250

VEBONO022009 ACT/360 20/02/2009 VEB Variable rate LT91D3S+250

VEBONO032009 ACT/360 05/03/2009 VEB Variable rate LT91D3S+250

VEBONO052009 ACT/360 15/05/2009 VEB Variable rate LT91D3S+250

VEBONO062009 ACT/360 11/06/2009 VEB Variable rate LT91D3S+250

VEBONO072009 ACT/360 23/07/2009 VEB Variable rate LT91D3S+250

VEBONO082009 ACT/360 07/08/2009 VEB Variable rate LT91D3S+250

VEBONO092009 ACT/360 18/09/2009 VEB Variable rate LT91D3S+250

VEBONO102009 ACT/360 29/10/2009 VEB Variable rate LT91D3S+250

VEBONO112009 ACT/360 27/11/2009 VEB Variable rate LT91D3S+250

VEBONO122009 ACT/360 03/12/2009 VEB Variable rate LT91D3S+250

VEBONO012010 ACT/360 28/01/2010 VEB Variable rate LT91D3S+250

VEBONO022010 ACT/360 19/02/2010 VEB Variable rate LT91D3S+250

VEBONO032010 ACT/360 11/03/2010 VEB Variable rate LT91D3S+250

VEBONO042010 ACT/360 22/04/2010 VEB Variable rate LT91D3S+250

TIF052010 ACT/360 28/05/2010 VEB fixedrate 13.0%

VEBONO052010 ACT/360 28/05/2010 VEB Variable rate LT91D3S+250

18

Instrument Day count convention

Maturity Currency Coupon Calculation of

coupon 1/ TIF092010 ACT/360 30/09/2010 VEB fixedrate 13.0%

VEBONO122010 ACT/360 09/12/2010 VEB Variable rate LT91D3S+250

VEBONO022011 ACT/360 11/02/2011 VEB Variable rate LT91D3S+250

TIF032011 ACT/360 03/03/2011 VEB fixedrate 9.25%

TIF042011 ACT/360 14/04/2011 VEB fixedrate 13.88%

VEBONO042011 ACT/360 14/04/2011 VEB Variable rate LT91D3S+250

VEBONO052011 ACT/360 20/05/2011 VEB Variable rate LT91D3S+250

TIF072011 ACT/360 07/07/2011 VEB fixedrate 9.38%

TIF092011 ACT/360 23/09/2011 VEB fixedrate 13.88%

VEBONO032012 ACT/360 08/03/2012 VEB Variable rate LT91D3S+250

VEBONO042012 ACT/360 05/04/2012 VEB Variable rate LT91D3S+250

VEBONO052012 ACT/360 25/05/2012 VEB Variable rate LT91D3S+250

TIF062012 ACT/360 28/06/2012 VEB fixedrate 9.50%

TIF082012 ACT/360 30/08/2012 VEB fixedrate 13.88%

VEBONO082012 ACT/360 30/08/2012 VEB Variable rate LT91D3S+250

TIF102012 ACT/360 25/10/2012 VEB fixedrate 14.0%

TIF122012 ACT/360 06/12/2012 VEB fixedrate 9.50%

VEBONO042013 ACT/360 25/04/2013 VEB Variable rate LT91D3S+250

TIF052013 ACT/360 03/05/2013 VEB fixedrate 9.63%

VEBONO052013 ACT/360 03/05/2013 VEB Variable rate LT91D3S+250

VEBONO072013 ACT/360 04/07/2013 VEB Variable rate LT91D3S+250

VEBONO082013 ACT/360 16/08/2013 VEB Variable rate LT91D3S+250

TIF102013 ACT/360 17/10/2013 VEB fixedrate 15.0%

TIF122013 ACT/360 13/12/2013 VEB fixedrate 15.0%

TIF042014 ACT/360 17/04/2014 VEB fixedrate 16.0%

VEBONO052014 ACT/360 02/05/2014 VEB Variable rate LT91D3S+250

VEBONO062014 ACT/360 26/06/2014 VEB Variable rate LT91D3S+250

TIF082014 ACT/360 08/08/2014 VEB fixedrate 16.0%

VEBONO092014 ACT/360 19/09/2014 VEB Variable rate LT91D3S+250

VEBONO102014 ACT/360 09/10/2014 VEB Variable rate LT91D3S+250

TIF122014 ACT/360 25/12/2014 VEB fixedrate 9.75%

TIF012015 ACT/360 30/01/2015 VEB fixedrate 17.0%

TIF052015 ACT/360 28/05/2015 VEB fixedrate 17.0%

VEBONO092015 ACT/360 11/09/2015 VEB Variable rate LT91D3S+250

VEBONO102015 ACT/360 30/10/2015 VEB Variable rate LT91D3S+250

TIF112015 ACT/360 13/11/2015 VEB fixedrate 9.88%

TIF122015 ACT/360 31/12/2015 VEB fixedrate 17.25%

TIF022016 ACT/360 25/02/2016 VEB fixedrate 18.0%

TIF062016 ACT/360 17/06/2016 VEB fixedrate 18.0%

VEBONO062016 ACT/360 17/06/2016 VEB Variable rate LT91D3S+250

VEBONO082016 ACT/360 12/08/2016 VEB Variable rate LT91D3S+250

TIF092016 ACT/360 01/09/2016 VEB fixedrate 18.0%

TIF102016 ACT/360 06/10/2016 VEB fixedrate 9.88%

TIF112016 ACT/360 18/11/2016 VEB fixedrate 18.0%

VEBONO122016 ACT/360 29/12/2016 VEB Variable rate LT91D3S+250

TIF102017 ACT/360 05/10/2017 VEB fixedrate 9.88%

VEBONO112017 ACT/360 23/11/2017 VEB Variable rate LT91D3S+250

VEBONO122017 ACT/360 08/12/2017 VEB Variable rate LT91D3S+250

TIF052018 ACT/360 11/05/2018 VEB fixedrate 9.88%

TIF082019 ACT/360 02/08/2019 VEB fixedrate 9.88%

TIF102020 ACT/360 15/10/2020 VEB fixedrate 9.88%

1/ The variable rate for the bonds is calculated as the yield on treasury bills of the last three weeks plus 250 basis points. SourceMinistry of Finance

Table

GLOBA

GLOBA

SOVER

GLOBA

GLOBA

SOVER

SOVER

SOVER

SOVER

GLOBA

GLOBA

SOVER

GLOBA

GLOBASource

Table varian

2.

Instrumen

AL 2013

AL 2014

REIGN BOND 2

AL 2018 13,625

AL 2018 7,00%

REIGN BOND 2

REIGN BOND 2

REIGN BOND 2

REIGN BOND 2

AL 2025

AL 2027

REIGN BOND 2

AL 2034

AL 2038 : Ministry of Fina

3.Correlatince

nt

016

5%

019

020

023

024

028

ance

on Matrix. and

Issue d

19/09/2

19/09/2

29/09/2

09/12/2

30/07/1

30/09/2

26/11/2

13/10/2

09/12/2

07/05/2

13/10/2

07/04/2

18/09/1

07/05/2

07/01/2

15/11/2

Parameters d

date Cur

2003 U

2003 U

2004 U

2005 U

1998 U

2003 U

2003 U

2009 U

2005 U

2008 U

2009 U

2005 U

1997 U

2008 U

2004 U

2007 U

Nelson Siesome

rrency C

USD

USD

USD

USD

USD

USD

USD

USD

USD

USD

USD

USD

USD

USD

USD

USD

egel model, e

Coupon

10.75%

10.75%

8.50%

5.75%

13.63%

13.63%

7.00%

7.75%

6.00%

9.00%

8.25%

7.65%

9.25%

9.25%

9.38%

7.00%

factors of cmacro

19

Maturity

19/09/2013

19/09/2013

08/10/2014

26/02/2016

15/08/2018

15/08/2018

01/12/2018

13/10/2019

09/12/2020

07/05/2023

13/10/2024

21/04/2025

15/09/2027

07/05/2028

13/01/2034

31/03/2038

conditional o-variables

20

10 15 20 25 309.5

9.6

9.7

9.8

9.9

10

10.1

10.2

10.3

10.4

10.5

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate- External debt market -30-Jun-2008

Observed yield

Nelson-Siegel Model

Bonds

Figure 1. Yield curve estimations – External debt market

5 10 15 20 2510.5

11

11.5

12

12.5

13

13.5

14

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - External debt market -31-Jul-2011

Observed yield

Nelson-Siegel Model

Bonds

21

5 10 15 20 2517

18

19

20

21

22

23

Term to maturity

Yie

ld (

%)

Instantaneous Forward Rate- External debt market -31-Jan-2009

Observed yield

Nelson-Siegel Model

Bonds

5 10 15 20 2514

14.5

15

15.5

16

16.5

17

17.5

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - External debt market -30-Jun-2009

Observed yield

Nelson-Siegel Model

Bonds

22

5 10 15 20 2510

10.5

11

11.5

12

12.5

13

13.5

14

14.5

15

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - External debt market -31-May-2011

Observed yield

Nelson-Siegel Model

Bonds

5 10 15 20 259

10

11

12

13

14

15

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - External debt market -30-Apr-2011

Observed yield

Nelson-Siegel Model

Bonds

23

Figure 2. Yield curve estimations – Domestic debt market

0 0.5 1 1.5 2 2.5 3 3.5 45

6

7

8

9

10

11

12

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - Domestic debt market-30-Apr-2006

Observed yield

Nelson-Siegel Model

Treasury bills, Vebonos, and TIF

0 2 4 6 8 10 12 144

5

6

7

8

9

10

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - Domestic debt market-30-Nov-2006

Observed yield

Nelson-Siegel Model

Treasury bills, Vebonos, and TIF

24

0 2 4 6 8 10 129

10

11

12

13

14

15

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - Domestic debt market-31-Mar-2008

Observed Yield

Nelson-Siegel Model

Trasury bills, Vebonos and TIF

0 1 2 3 4 5 6 7 8 9 102

4

6

8

10

12

14

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate - Domestic debt market-31-Mar-2010

Observed yield

Nelson-Siegel Model

Treasury bills, Vebonos and TIF

25

Figure 3

0 1 2 3 4 5 6 7 8 9 102

4

6

8

10

12

14

16

Term to maturity (Years)

Yie

ld (

%)

Instantaneous Forward Rate- Domestic debt market -31-May-2010

Observed yield

Nelson-Siegel Model

Treasury bills, Vebonos and TIF

26

Figure 4