Vivek Chandra - Texas LNG - Relative attractiveness of US LNG exports - Is the threat to Australian...

17

August 2015 www.txlng.com The Relative Attractiveness of US LNG exports – Is the threat to Australian projects real? CONFIDENTIAL Copyright © Texas LNG Brownsville LLC SEAAOC 2015 VIVEK CHANDRA CEO, TEXAS LNG [email protected]

-

Upload

informa-australia -

Category

Business

-

view

659 -

download

1

Transcript of Vivek Chandra - Texas LNG - Relative attractiveness of US LNG exports - Is the threat to Australian...

August 2015 www.txlng.com

The Relative Attractiveness of US LNG exports –Is the threat to Australian projects real?

CONFIDENTIAL

Copyright © Texas LNG Brownsville LLC

SEAAOC 2015

VIVEK CHANDRACEO, TEXAS [email protected]

Ingredients of a ‘Successful’ LNG Project

2

• Reserve life

• NGL Content

• CO2 Content

• Field Access

• Reservoir quality

• Distance from

field to plant

• Upstream costs

• Govt Support

• Security

• Native rights

• Fiscal stability

• Environmental

permits - status

and issues

• Labor costs /

availability

• Technology Risk

• Contractor

Experience

• Infrastructure

required

• Engineering

Stage

• Total Capex/ton

• Overall

complexity

• Operator

Experience

• Partner Experience

• Partner Alignment

• Buyer type (enduser

vs trader)

• Buyer experience

• Marketing stage

UpstreamAbove

GroundTechnical

Company & Market

Not all projects are the same – beware of broad brush!!

US Gulf Coast Projects have most of the important characteristics – and a very large advantage over Australian projects

3

• Long Reserve

life

• Good NGL

Content

• Low CO2

Content

• Easy Field

Access

• Good Reservoir

quality

• Short Distance

from field to

plant

• Low Upstream

costs

• Good Govt

Support

• Good Security

• No Native

rights issues

• Fiscal

stability

• Ease of

Environmental

permits

• Low Labor

costs /

availability

• Low Technology

Risk

• Solid Contractor

Experience

• Limited new

Infrastructure

required

• Advanced

Engineering

Stage

• Low total

Capex/ton

• Low Overall

complexity

• Good Operator

Experience

• Good Partner

Experience

• Good Partner

Alignment

• Buyer type

(enduser vs

trader)

• Good Buyer

experience

• Marketing stage

The US Gulf Coast is really the only source of sufficient incremental volumes that can be delivered at competitive prices

Legacy Projects Expansions ‘Coming Soon’ greenfield

Giant Greenfield Modest Greenfield

US Gulf Coast

4

<$7 /MMBtu >$14 /MMBtu

Unknown!! >$11 /MMBtu~$9-10/MMBtu

Prices are estimated delivered prices to North Asia

Texas LNG is an independent US LNG export project located in Brownsville, Texas which will begin production of 2 MTA of LNG in 2020

We are a credible alternative to the ‘status-quo’ where few LNG suppliers control the market and the customer is taken for granted.

We will encourage flexible terms, no destination restrictions, & delivered prices based on ‘gas-on-gas’ economics and true costs under a transparent tolling pricing model.

Our project will leverage Asian shipyards to reduce capex and thus offer the best price and terms for our tolling customers.

Project total capacity will be 4 MTA, divided in two equal volume Phases. Phase 1 will begin production in 2020.

We will be able to supply LNG at prices competitive to other US Gulf Coast

projects – the lowest costs incremental LNG supplier for global markets

Texas LNG Fact SheetCapacity Phase 1: 2 Million Tonnes per year (MTA) from 2020

Phase 2: 2 MTA additional capacity based on market demand

Export Approvals (DOE) June 2014 (FTA), Non-FTA pending

FERC (Federal Energy Regulatory Commission) Permit Status Pre-Filing commenced on April 14, 2015: Docket No. PF15-14-000Filed Draft Resource Reports 1 & 10 on May 14, 2015All Draft Resource Reports to be filed by 4Q 2015

Engineering & Commercial MilestonesConceptual Design StudyPreliminary Front End Engineering Design (pre-FEED)Front End Engineering Design (FEED)Detailed EngineeringFinal Investment DecisionLNG Production

May 2014June 2014 – October 2014November 2014 – November 2015December 2015 - Late 2016Late 2016 / early 2017 (based on FERC approvals)2020

Engineering Partners Samsung Engineering (also equity partner)

Liquefaction Process Air Products (APCI): Proven C3MR Process

Gas Pre-Treatment Process Honeywell (UOP)

Environmental Advisers Natural Resource Group. LLC

Development Capital Financier Third Point LLC

Financial Advisers BNP Paribas

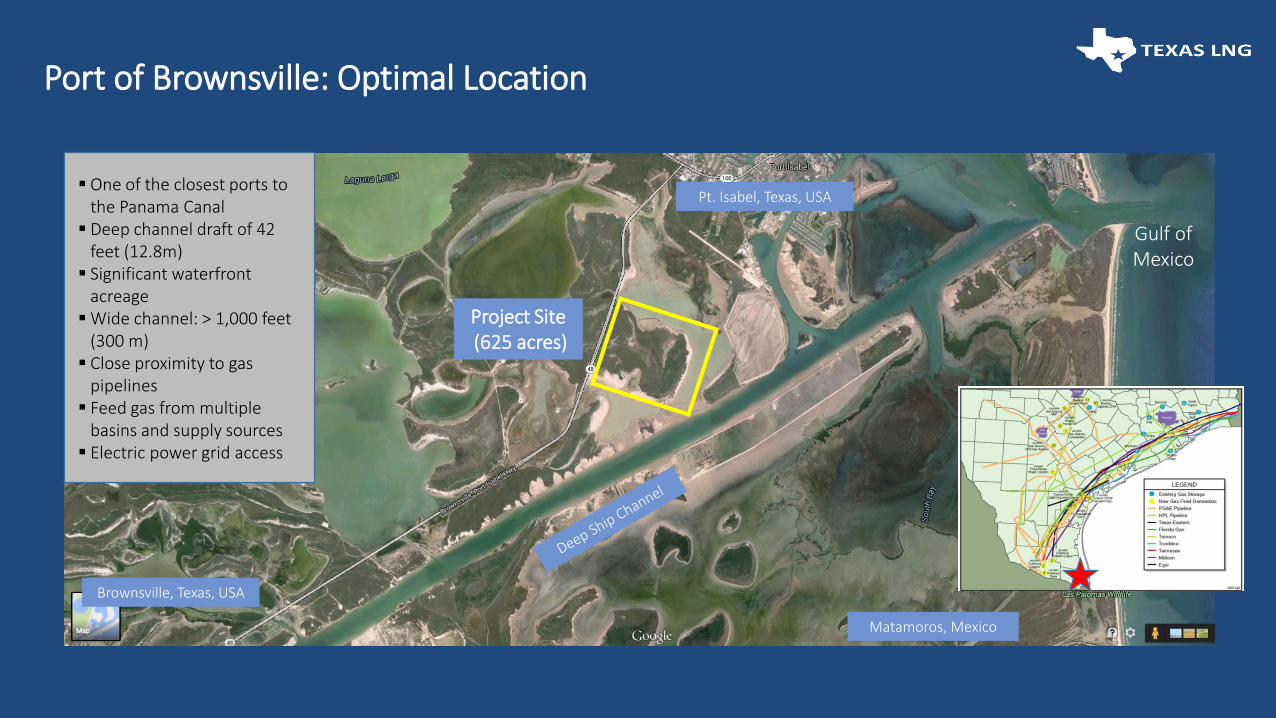

Port of Brownsville: Optimal Location

Brownsville, Texas, USA

Matamoros, Mexico

Gulf of Mexico

Pt. Isabel, Texas, USA

Project Site(625 acres)

One of the closest ports to the Panama Canal

Deep channel draft of 42 feet (12.8m)

Significant waterfront acreage

Wide channel: > 1,000 feet (300 m)

Close proximity to gas pipelines

Feed gas from multiple basins and supply sources

Electric power grid access

Project Concept

Note: This artist impression is a representation of the Texas LNG project and should not be relied upon for any purpose. Actual project configuration may be different than shown in this image.

Samsung Engineering: Equity Owner and Responsible for Project Engineering and Construction

Conceptual Study

Pre-FEED FEED Detailed Engineering

Completed in May 2014

June – Oct 2014.

13,000+ man-hours

Begun in Nov 2014

Estimated: Late 2015

EPC

Estimated: Late 2016/early 2017

Over 100,000 engineering man-hours completed (July 2015) 90+ engineers engaged in Korea and USA.Samsung Engineering will execute the EPC phase on lump-sum basis.Modular construction – most likely in Asia shipyard

Current Phase

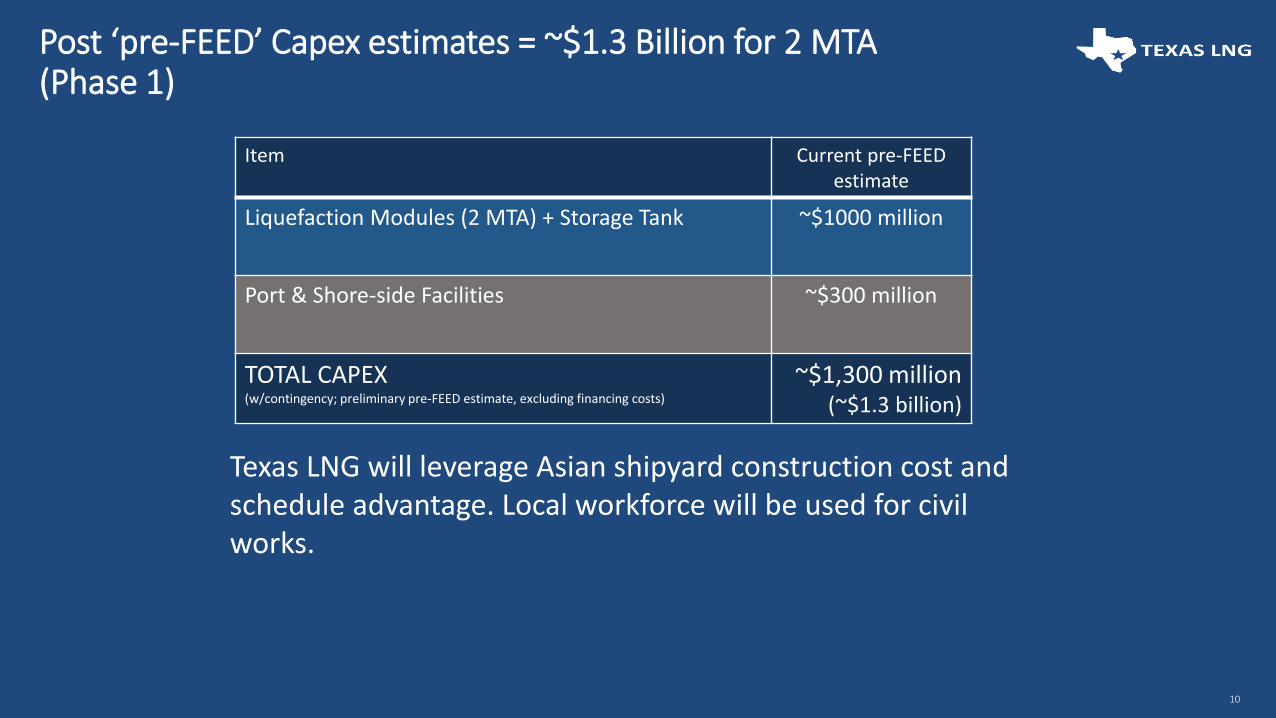

Post ‘pre-FEED’ Capex estimates = ~$1.3 Billion for 2 MTA (Phase 1)

10

Item Current pre-FEED estimate

Liquefaction Modules (2 MTA) + Storage Tank ~$1000 million

Port & Shore-side Facilities ~$300 million

TOTAL CAPEX(w/contingency; preliminary pre-FEED estimate, excluding financing costs)

~$1,300 million(~$1.3 billion)

Texas LNG will leverage Asian shipyard construction cost and schedule advantage. Local workforce will be used for civil works.

Texas LNG = $650 million/MTPA

All Existing ProjectsMainly Future Projects

Source: DB report “US LNG exports: from spectre to emerging reality” Feb 2012

Controlled shipyard environment will reduce Texas LNG’s Capex costs

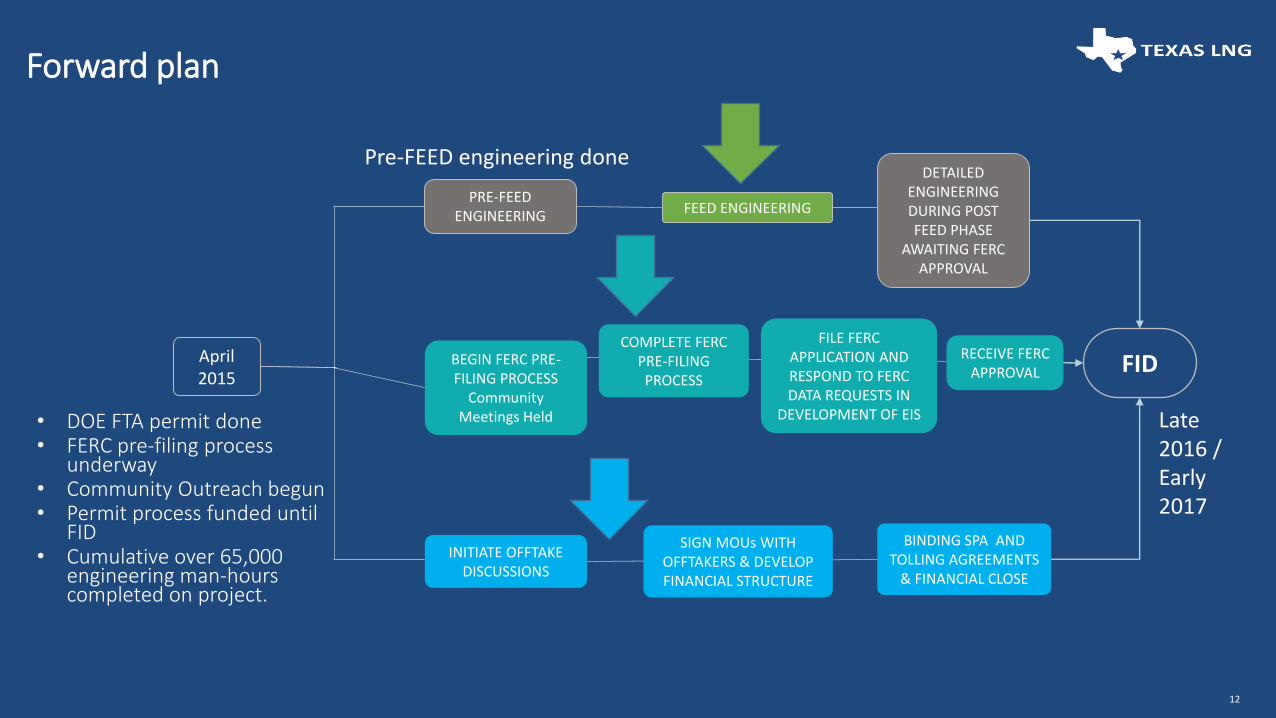

Forward plan

12

COMPLETE FERC PRE-FILING PROCESS

April 2015

BEGIN FERC PRE-FILING PROCESS

Community Meetings Held

PRE-FEED ENGINEERING

FEED ENGINEERING

DETAILED ENGINEERING DURING POST FEED PHASE

AWAITING FERC APPROVAL

RECEIVE FERC APPROVAL FID

• DOE FTA permit done• FERC pre-filing process

underway• Community Outreach begun• Permit process funded until

FID• Cumulative over 65,000

engineering man-hours completed on project.

INITIATE OFFTAKE DISCUSSIONS

SIGN MOUs WITH OFFTAKERS & DEVELOP FINANCIAL STRUCTURE

BINDING SPA AND TOLLING AGREEMENTS

& FINANCIAL CLOSE

Pre-FEED engineering done

Late2016 / Early 2017

FILE FERC APPLICATION AND RESPOND TO FERC DATA REQUESTS IN

DEVELOPMENT OF EIS

Australia (Queensland) $/MMBtu

Liquefaction $ 6.50 Feed Gas @ plant $ 7.00

Shipping Costs $ 1.50 Total Delivered Price $ 15.00

Typical Australia contract terms vs Texas LNG model

13

Texas LNG $/MMBtu

Feed Gas assumed price $ 3.00 Pipeline Tariff* $ 0.40Capacity Fee* (rise with inflation) $ 2.80 Liquefaction Charge* (rise with inflation) $ 0.45

Shipping estimated Asia/ Europe $ 2.10 / $1.25

Total Delivered Price* Asia / Europe $ 8.75 / $7.90

Take or Pay portion

Australian LNG project Take or Pay = $13.50

Take or Pay

Texas LNG’s Take or Pay = $2.80*

Liq

ue

faction

Tolling

Feed Gas

Fe

ed

Ga

sOperating Charge

Shipping

Shipping$

/MM

Btu

Delivered to North Asia: $15/MMBtu Delivered to North Asia: $ 8.75 /MMBtu estimatedDelivery to Europe: $7 .90 /MMBtu estimated

Pipeline

* Texas LNG charges based on current CAPEX and OPEX pre-FEED estimates and may be adjusted as project development continues

To TXLNG

[Pre-Oil Price collapse of 2014/2015]

14

Regional characteristics

Expensive

Labour

High Cost

E&P

Aboriginal

land

issuesUncertain

tax environment

Insistence on

inflexible

contract

terms

High

shipping

costs

Ongoing

drilling and

other

upstream

capex

High

capex/

tonne

costs

Eastern Australia

Western Australia

Well

productivity

inconsistent

Reserves

issues

US Gulf

Coast

*Global LNG Shipping costs have dropped significantly over past 12 months

Oil price

contracts

only

The US LNG exports tidal wave is real – and growing

15

First Phase:Sabine Pass [17]

Second Phase:

Cameron [12]Freeport [13]Corpus Christi [13]Cove Point [5]

Third Phase:Texas LNG [2+2]Trunkline [15]Golden Pass[8]Magnolia [8]Oregon [9]Jordan Cove [6]Others

2015-2016

2017-2019

2020+

Only projects that have begun the FERC process are credible

So, is the US threat to Australian projects real?

16

YES !

Let’s hope that the situation is not be as bad as predicted by a recent Harvard University study that stated…

“after the plunge of oil and LNG prices in Asia, the Australian

LNG chapter risks becoming one of the worst investment stories of the last few decades in the oil and gas sector.”

Source: “Falling Short: A Reality Check for Global LNG Exports" by Leonardo Maugeri, Harvard Kennedy School, December 2014

Disclaimer

Cautionary Statement:

The information and materials in this document are ; Provided for informational purposes only and are subjectto addition, deletion and modification without notice at the sole discretion of Texas LNG LLC and Texas LNGBrownsville LLC.; Not warranted or guaranteed to be correct, complete or up-to-date. The information andmaterials could include technical inaccuracies and other errors. ; Provided “As Is” without any representation orwarranties of any kind. No liability, direct or consequential, of any kind arising from the use of information andmaterials contained in this document or linked website is accepted. ; Not to be considered or to be constitutedas investment advice or as any type of offer, offer, invitation, solicitation or recommendation in relation to thepurchase or sale of any type of financial instruments or security in any jurisdiction.

Any forward looking statements contained in the information and materials in this document are onlypredictions and are subject to risks, uncertainties and assumptions, many of which are outside the control ofTexas LNG LLC or Texas LNG Brownsville LLC or its officers or representatives. These risks, uncertainties andassumptions include commodity prices, currency fluctuations, economic and financial market conditions invarious countries and regions, environmental risks and legislative, fiscal or regulatory developments, politicalrisks, project delay or advancement, approvals and cost estimates. Actual values, results or events may bematerially different to those expressed or implied in this document. Given these uncertainties, readers arecautioned not to place reliance on forward looking statements .

Readers are strongly advised to complete their own investigations to the accuracy and completeness of thecontents of this or any other communication or document, written or oral, provided by or referred to by TexasLNG LLC or Texas LNG Brownsville LLC or its officers or representatives.

17