Vishak_2256- Dissertation final doc - reduced size

61

Page No. 1 Dissertation Report On Feasibility Study to own a marine spread Submitted in partial fulfillment of the requirement of Executive Masters in Business Administration (EMBA) Operations Specialization Submitted By: ‐ Mentored By: ‐ Prof. Krishnan Subramanian Vishak Gopi Mr. Nihar Kumthekar Roll No. 2256 EMBA 22

-

Upload

vishak-gopi -

Category

Documents

-

view

149 -

download

0

Transcript of Vishak_2256- Dissertation final doc - reduced size

PageNo.1

DissertationReportOn

FeasibilityStudytoownamarinespread

Submittedinpartialfulfillmentoftherequirementof

ExecutiveMastersinBusinessAdministration(EMBA)

OperationsSpecialization

SubmittedBy:‐MentoredBy:‐Prof.KrishnanSubramanian

VishakGopiMr.NiharKumthekar

RollNo.2256

EMBA22

PageNo.2

DECLARATION

Iherebydeclare that thematter included in thisdissertationreportentitled “FeasibilityStudy toownamarinespread”,istheresultofstudyandinterviewscarriedoutbyme.Ifurtherdeclarethatthisismyoriginalworkandhasnotbeenpublishedanywherebefore.ThisProjectworkhasbeencarriedoutforthesolepurposeofsubmissioninpartialfulfillmentofExecutiveMastersinBusinessManagement(EMBA)inOperationsManagementatSPJainCenterofManagement,Dubai.

VishakGopi

RollNo.2256

EMBABatch22

SPJainSchoolofGlobalManagement

Block5

AcademicCity

Dubai,UAE

Theaboveistruetothebestofmyknowledgeandinformation

ProjectMentorIndustryMentor

Prof.KrishnanSubramanian Mr.SubhashNair

Mr.NiharKumthekar

PageNo.3

ACKNOWLEDGEMENT

Iwouldliketothankandexpressmysinceregratitudetoallthepeoplewhohaveassistedmewiththisreport.Especially:

Mr.NiharKumthekarforhisinterestandcontinuousguidancealongwithmotivationandtheinvaluableadvisethroughoutthetimedurationofthisprojectandProf.Krishnanforprovidingvaluableinsight.

Mr.SubhashNair,Director,TechnomakOffshoreandSubsea,forbeingmyindustrialmentorforhisvaluableinsightonthistopicinspiteofhisbusyschedule.

IwouldalsoliketothankallmyprofessorsatSPJAIN(Dubai)fortheircontributioninbroadeningmythinkingprocessandthinkoutofthebox.

IalsotakethisopportunitytothankmybatchmatesfromEMBA22forteachingmetheimportanceofteamworkandcollaboration.

Finally,Iwouldliketothankmyfamilyforsupportingmedevelopasagoodindividualandacompleteprofessional.

VishakGopi

24.05.2015

PageNo.4

EXECUTIVE SUMMARY

AsperrecentstudyitisestimatedthatJackupbargesarehavinghighdemandinoffshoreindustryespeciallyinshallowwater

AbuDhabioffshorehasmanyupcomingprojectsandmakesitanideallocationtotargetinthisregion.SincethecompanyhasalreadyregisteredwithmajoroilcompaniesinAbuDhabiforvariousworks,itwillbeeasytogetqualifiedaJack‐upvessel.

Therearemanycompetitorsinthisfield.Butthereareveryfewcompetitorswhoownavesselandcapabletodoalltheoffshorebrownfieldandgreenfieldworks.OwningaJack‐upbargewillenableTechnomaktobidandwinEPCIprojects.

ThisreportisonthestudymadebymeonthisissuewhethertoownaJack‐upbargeoraworkbargeorconvertaJack‐upRigorCharterthevessel.Iftheanswerisbuyingthenweneedtoknowwhichtypeofvessel?

MyanalysisshowsthatitisfeasibletoownaJack‐upbarge.Therevenuegeneratedisbasedonthedataavailableinthemarket.Thedecisionnottogoforanothertypeofvesselorcharterisalsodetailed.Thus,therecommendationisownaJack‐upbarge.

PageNo.5

TABLEOF CONTENTS

DECLARATION..........................................................................................................................................................................2

ACKNOWLEDGEMENT..........................................................................................................................................................3

EXECUTIVE SUMMARY.............................................................................................................................................................4

LISTOFFIGURES.....................................................................................................................................................................7

LISTOFTABLE.........................................................................................................................................................................8

INTRODUCTION.......................................................................................................................................................................9

COMPANYBACKGROUND..................................................................................................................................................10

BUSINESSMODEL............................................................................................................................................................11

OFFSHOREOPERATIONS..............................................................................................................................................12

MARINESPREAD..............................................................................................................................................................12

MARINESPREADINFORMATION...................................................................................................................................13

OFFSHOREWORKINGBARGE[Option‐1]..............................................................................................................13

JACK‐UPBARGE/LIFTBOAT[option‐2]...............................................................................................................14

CONVERTJACK‐UPDRILLRIGTOJACK‐UPWORKACCOMODATION/BARGE[option‐3]..............15

SERVICESTOBEOFFERED..........................................................................................................................................15

WHOARETHECUSTOMERS?.....................................................................................................................................16

VALUEPROPOSITION.....................................................................................................................................................16

PROBLEMSTATEMENT......................................................................................................................................................17

LITERATUREREVIEW.........................................................................................................................................................18

GROWTHFACTORSANDCHALLENGES.................................................................................................................21

DEMOGRAPHICFACTORS.............................................................................................................................................22

OILDEMAND......................................................................................................................................................................23

MOTORIZATIONINASIANCOUNTRIES.................................................................................................................24

FUELECONOMYIMPROVEMENTS...........................................................................................................................25

UPSTREAMCOSTINCREASE.......................................................................................................................................26

USSHALEOILPRODUCTIONOUTLOOK.................................................................................................................27

UNCERTAINITYINRESERVEESTIMATION..........................................................................................................29

POTENTIALFORWELLDRILLING............................................................................................................................30

OTHERCONSTRAINTS...................................................................................................................................................31

NORTHAMERICABECOMESTHELEADERINOILPRODUCTION...............................................................32

BIOFUELS...........................................................................................................................................................................33

DEEPWATERPRODUCTION.......................................................................................................................................34

PageNo.6

IRAQIPRODUCTIONGROWTHPROPSECTS.........................................................................................................35

OPEC’SBALANCINGROLE............................................................................................................................................37

GTL‐CHALLENGEFORTHEOILMARKETAFTER2020...................................................................................38

INFLUENCEOFDOLLAREXCHANGERATE..........................................................................................................39

OILPRICESFORECAST..................................................................................................................................................40

OILREFINERYPROJECTSINMIDDLEEAST.........................................................................................................41

RESEARCHOBJECTIVES.....................................................................................................................................................42

RESEARCHMETHEDOLOGY........................................................................................................................................43

PRIMARYRESEARCH......................................................................................................................................................43

SECONDARYRESEARCH...............................................................................................................................................44

PROJECTSCOPE.....................................................................................................................................................................44

VESSELSNOTINCLUDEDINTHEFLEET...............................................................................................................44

LIMITATIONS.....................................................................................................................................................................45

FINDINGANDANALYSIS....................................................................................................................................................45

PRIMARYRESEARCH......................................................................................................................................................45

FINDINGS.............................................................................................................................................................................46

TENTATIVELYASEDONPRIMARYRESEARCH[IDI]WITHCUSTOMERS...............................................46

SECONDARYRESEARCH...............................................................................................................................................47

PORTER’SFIVEFORCES................................................................................................................................................49

SWOTANALYSIS...............................................................................................................................................................50

DECISIONTREEFORSETTINGUPMARINEOPERATION...............................................................................51

RECOMMENDATIONS..........................................................................................................................................................52

MANAGERIALIMPLICATIONS.........................................................................................................................................52

SUPPLIERS..........................................................................................................................................................................52

VESSELCOST......................................................................................................................................................................53

INFRASTRACTUREREQUIREMENT.........................................................................................................................53

HUMANRESOURCEREQUIREMENT........................................................................................................................53

COMPETITORS...................................................................................................................................................................54

PROJECTEDPROFIT&LOSSSTATEMENTFORFIVEYEARS.........................................................................55

BREAKEVENANALYSIS................................................................................................................................................56

THEWAYFORWARD......................................................................................................................................................56

TIMEFRAMEFORPROJECTEXECUTION...............................................................................................................57

CONCLUSION...........................................................................................................................................................................58

BIBLIOGRAPHY......................................................................................................................................................................59

APPENDIX.................................................................................................................................................................................60

PageNo.7

LISTOFFIGURES

Figure1VALUEPROPOSITION........................................................................................................................................17

Figure2FACTORSAFFECTINGOILPRICE..................................................................................................................22

Figure3DEMOGRAPHICFACTORSAFFECTINGOILPRICE................................................................................23

Figure4OILDEMAND.........................................................................................................................................................24

Figure5MOTORIZATIONCURVES.................................................................................................................................25

Figure6FUELCONSUMPTIONBYNEWCARS..........................................................................................................26

Figure7UPSTREAMCOSTINCREASEINOILEXPLORATIONANDPRODUCTION....................................27

Figure8OILPRODUCTIONINNORTHDAKOTA......................................................................................................29

Figure9AVERAGEBAKKENWELLPRODUCTIONCURVE.................................................................................30

Figure10FORECASTOFNUMBEROFWELLS........................................................................................................31

Figure11FORECASTOFSHALEOILPRODUCTION..............................................................................................32

Figure12FORECASTOFPRODUCTIONOFLIQUIDHYDROCARBONINNORTHAMERICA.................33

Figure13FORECASTFORGLOBALBIOFUELPRODUCTION.............................................................................34

Figure14DEEPWATERPRODUCTIONFORECAST...............................................................................................35

Figure15FORECASTOFOILPRODUCTIONINIRAQ............................................................................................36

Figure16dYNAMICSOFOPECSHAREINGLOBALPRODUCTION..................................................................37

Figure17HISTORYOFGTLPROCESS..........................................................................................................................39

Figure18DYNAMICSOFBRENTOILPRODUCTION.............................................................................................40

Figure19BRENTPRICEFORECAST.............................................................................................................................41

Figure20LARGESTNEWOILREFINERYPROJECTSINTHEMIDDLEEAST..............................................42

Figure21PORTER’SFIVEFORCESMODEL...............................................................................................................49

Figure22DECISIONTREE.................................................................................................................................................51

Figure23RACICHART.......................................................................................................................................................57

Figure24GANTTCHART..................................................................................................................................................58

PageNo.8

LISTOFTABLE

Table1COMPARISONOFVESSELS,THEIRDAYRATEANDOPERATINGEXPENSES............................46

Table2ANALYSISBASEDONPORTERSFIVEFORCES.........................................................................................50

Table3SWOTANALYSIS....................................................................................................................................................51

Table4PROFIT&LOSSSTATEMENT...........................................................................................................................55

Table5PROJECTTIMEFRAME.......................................................................................................................................57

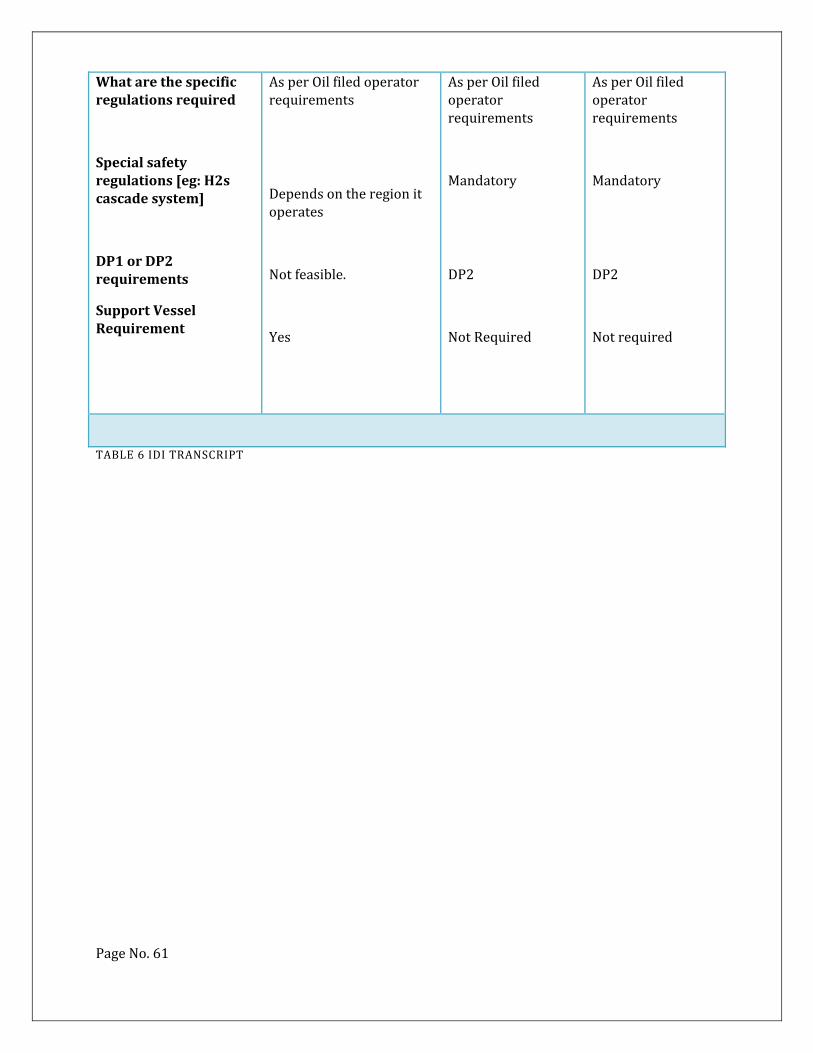

Table6IDITRANSCRIPT....................................................................................................................................................61

PageNo.9

INTRODUCTION

About56percentof theworld'soil reservesand36percentof theworld'snaturalgas

reservesareintheMiddleEast.

2011 saw UAE as the world's eighth largest oil producer, churning out an average

productionvolumeof2.813millionbarrelsperday.

UAEcomesfourthinthetopglobalexporters’ league,exportingaround81percentof its

total production. The UAE exports around 2.32 million barrels of crude oil each day to

predominantlyAsianmarkets.

The UAE holds theworld's sixth largest proven oil reserves of approximately 98 billion

barrelsandseventhlargestgasreservesof213trillioncubicfeet.

Almost one‐third of the top 20 largest oil and gas projects in the Middle East under

executionarenowtakingplaceintheUAE'sboomingupstreamsphere.

TheAbuDhabi InternationalPetroleum InvestmentCompany in July2012 inaugurateda

pipeline via Fujairah to a refinery in Pakistan that completely bypasses the Strait of

Hormuz.The1.8million‐barrel‐per‐daycrudeoilpipelinerunsfromHabshaninAbuDhabi

toFujairahandensuresthesecurityoftheUAE'soilproductionandexportstotheworld.

Theenergy investmentneeds in theMiddleEastandNorthAfricaregionover theperiod

2012 through to 2016 is expected to reach US$ 525 billion, with most of the energy

investments being in the Arabian Gulf, according to The Arab Petroleum Investment

Corporation.

Around600,000barrels per daywill be neededover thenext decade tomeet theUAE's

infrastructure, business and investment needs reiterating UAE's continued reliance on

technology, equipment and expertise in the oil & gas sector, to service its own

consumption.

PageNo.10

The above details describe the growing potential of Abu Dhabi Oil & Gas market and

modification/maintenanceofexistingfacilityaswellasthenewfacilitydevelopmentsare

mandatorytogrowingmarketdemand.

COMPANYBACKGROUND

TECHNOMAKisanintegratedEngineeringDesignFabricationErectionCompanygearedto

serve the growing needs of offshore, Oil and Gas marine Power, Metallurgy and

InfrastructureprojectrequirementsoftheMiddleEast,Africa,FarEast,EuropeandIndian

Sub‐Continent.

As an ISO 9001‐2008, ISO 14001‐2007 & OHSAS 8001‐2007 certified company,

TECHNOMAK is committed towards maintaining high safety, quality and environmental

standards and continuous improvement of the efficiency by encouraging teamwork and

creating a positive work environment .The prime focus of the company is on customer

satisfactionandbuildingalongtermandsolidbusinessrelationshipbyadoptingthebest

internationalstandardsandpracticesprevalentintheindustry.

TECHNOMAKhasa fully fledgedfabricationfacilitymeasuring1millionSq. ft.andawell

experiencedworkforceof730inUAE,620inIndiaandareintheprocessofrecruitinga

similarstrengthofemployeesinQatarimmediately.TECHNOMAKhasalreadyestablished

itsstrongpresenceinchallengingassignmentsintheMENAregion&Indiansubcontinents

Themissionofthecompanyistocatertotheneedsofthecustomersthroughsafe,

reliable and environmentally sound means thereby achieving new landmarks and

engravingthecompany’snameinthelistoftop‐notchcompanies.

Company is headed by a group of professional engineers with strong and hands on

experience in the field of ship building and ship repair, offshore structure design and

fabrication,Oil&Gaspipelines,TurnkeyandShutdownprojects.Thiswouldaddvalueto

thesuccessfulprojectexecution.

PageNo.11

Equipped with professional management, technically skilled workforce and full‐fledged

fabricationfacilitymeasuring1,000,000sqftarea,TECHNOMAKhasprovenitscapability

tomeetthechallengeswithinthescheduledtimeframes.

Our fabrication yard and workshops are situated in Hamriyah Free Zone. The

fabricationfacilityatInnerHarbourarea,HamriyahFreezoneisstrategicallylocated

toenableeasyloadoutandtransportationoffabricatedmodules.

Equippedwithacomprehensiverangeofsupportfacilityandsolidengineeringbackups,

TECHNOMAK is capable of providing full range of heavy engineering fabrication,

constructionandconsultancyservicesforshipbuilding,shiprepair,andvesselmodification

andupgradationandOil&Gasindustry.

BUSINESSMODEL

TheCompanyservesmajorsectorsincluding:

x ArchitecturalandStructuralSteelFabrication&Installation.

x OffshorestructuresandplatformsFabrications.

x Offshore&SubseabrownfieldProjects

x Pipelineprojects&Equipmenterections

x Petrochemicals,Refineries&Powerplantsshutdown

x ShipbuildingandShiprepair

x Tankfabrication&Erectionjob

x HVAC,MEP&InteriorsProjects

TECHNOMAKbelievesinthephilosophyofbuildingbondsbeyondbusinessandalways

upholdscustomersatisfactionwin‐winrelationship,continuousimprovement,teamwork

andachievingoperationalexcellence&growthwhiledeliveringvaluetothecustomers,

employeesandthecommunity,astheguidingprinciples.

PageNo.12

OFFSHOREOPERATIONS

Technomakhasstartedtheiroffshoreinstallationprojectsinthelastquarterof2013.Sofar

TechnomakcompletedoneoffshoreInstallationprojectanditwasthefirstkindofproject

incompanyhistory.Afterthatprojectthemanagementwasspeedinguptheprocessto

startanewdivisionfocusingoffshorebrown‐fieldandInstallationprojects.Company

targetssmallandmediumrangeofoffshorebrownfieldaswellasGreenfieldprojects.The

targetedworksare;

TopsideStructuralworks

TopsidePipingworks

TopsideMechanicalworks

TopsideElectricalandInstrumentationworks.

TopsideblastingandPaintingworks

MARINESPREAD

Besides looking at the businessmodel it is important to understandwhat rolewill be

playedbyamarinespreadinwinningandsuccessfullyexecutingtheproject.Themarine

spread can be a offshore working barge, Jack‐up barge, a rig converted into working

barge.Theinvestmentwouldbeintherangeof$10mto$100mdependsontheageand

typeofthevessel.Alternativelywecancharterthevesselforaparticularprojectorcan

charteronyearlyleasebasis.Tocharteravesselforshorttimeisverydifficultandmost

of the vessels are working on long‐term charters. Also the mobilization cost for the

vesselsareveryhighandwon’tbeviable formostof theshort termprojects.Ontopof

thatgettingasuitablevesselforcriticalprojectsontimeisverydifficult.Alsotheclient’s

firstprioritieswillgenerallygoestothecontractorshavingtheirownvessel.

PageNo.13

MARINESPREADINFORMATION

OFFSHOREWORKINGBARGE[OPTION‐1]

Thephotographshowsatypicaloffshoreworkbarge.Itconsistsofaccommodationinthe

rangeof150to300pax.Itwon’tbeselfpropelled.Suchkindofbargessupportspreadfor

mobilizationaswellasanchorhandling.Thesebargescanbeanchoredoffshorewith6to8

anchors.Tospreadtheanchors itrequiresanchorhandling tugboats.Andtheseanchors

mooringhavegotweatherlimitationsaswell.Whenweatherpicksupthebargehastobe

movedawayfromthefield.Thataffectstheoffshoreworkingdaysaswell.Ontopofthat

suchconventionaltypeofanchoringisnotacceptingtheoilcompaniesandthereisalways

risk that the anchors may damage subsea pipelines. But this type of vessel has good

stability, large deck space for storage and other works and cheaper compared to other

types.

PageNo.14

JACK‐UPBARGE/LIFTBOAT[OPTION‐2]

Thesetypesofbargesareselfelevatingandthesearecategorizedbasedonthewaterdepth

it can operate. The oil companies prefer such kind of barges to work near offshore

platforms because of safety. This can work in any weather. These types of vessels are

generally small in size.Therewillbe limitation inaccommodationspace,deckspaceand

cranecapacityaswell.Thecostofsuchbarges ishighcomparedto floatingworkbarges.

Butthedemandforsuchbargesisveryhighandgettingaprojectwithsuchbargeswon’t

bedifficult.

PageNo.15

CONVERTJACK‐UPDRILLRIGTOJACK‐UPWORKACCOMODATION/BARGE[OPTION‐3]

ThesekindsofRigsareusedfordrillingtheoilwells.Itconsistsofaccommodations,cranes

anddrillingunit.Thedrillingunitscanberemovedandcanbeconvertedintojack‐upwork

barge. The old rigs are available for sales in different part of the world. The cost for

mobilization,conversionsetcareconsideredinthefeasibilitystudy.

SERVICESTOBEOFFERED

Belowisthelistofservicesthatwillbeoffered

1. Allsortoftopsideworks.

2. Cranecapacityintherangeof250MTto400MT.

3. Accommodationfor150to300men.

4. Subseadivingworks

PageNo.16

5. Subseainstallations,tie‐ins.

WHOARETHECUSTOMERS?

OilfieldoperatorssuchasADMA,ZADCO,DubaiPetroleum,QatarPetroleum,Soudi

Aramco,Shell,MaerskOilQatar,OXY,Chevronetcarethetargetedcustomers.However

thecharteragentsandEPCcontractorsaretheothertargetedcustomersforwhomthe

vesselcanbegivenforlongtermorshorttermcharters.

VALUEPROPOSITION

Ourswillbeoneoftheonestopsolutionsforourclientrequirements.Includingthevessel,

fromdetaildesigntojobcompletionandwecanprovidealltypesofpumpsforthe

customer.Wewillbefocusingonleveragingourlocationbyprovidinggoodservicetoour

customers.Thus,easylogistics,costeffectivenessandcloseproximityisthevalue

propositionthatwewillbeofferingtoourcustomers.

PageNo.17

PROBLEMSTATEMENT

Tostartwithoffshoreoperations,Technomaktargetingthesmallinstallationprojectsin

thebeginning.Butthemajorchallengeistoownamarinespread[whichcanbeaoffshore

workingbarge, Jack‐upbarge, a rig converted intoworkingbargeetc.].The investment

wouldbeintherangeof$10mto$100mdependsontheageandtypeofthevessel.Else

wecancharterthevesselforaparticularprojectorcancharteronyearlyleasebasis.To

charter a vessel for short time is very difficult andmost of the vessels areworking on

long‐termcharters.Alsothemobilizationcostforthevesselsareveryhighandwon’tbe

viable formost of the short term projects. On top of that getting a suitable vessel for

criticalprojectsontimeisverydifficult.Alsotheclient’sfirstprioritieswillgenerallygoes

to the contractors having their own vessel. The following diagram shows the major

challenges

OURST

RENGTHS

GOODENGINEERING

EXPERIENCEDOFFSHORE

MARINESPREAD

ValueProposition

CustomerSatisfaction

Customerswillbeabletoexecutetheirprojectwithminimalinterfaces

Customerscangetoffshoreserviceandvesselunderoneroof

Customerscangetgoodcompetitivepricesincethevesselandexecutionteambelongstooneteam.

FIGURE1VALUEPROPOSITION

PageNo.18

LITERATUREREVIEW

WhyMiddleeastmarket?(Gas,2014)

About56percentoftheworld'soilreservesand36percentoftheworld'snaturalgas

reservesareintheMiddleEast.

2011 saw UAE as the world's eighth largest oil producer, churning out an average

productionvolumeof2.813millionbarrelsperday.

UAEcomesfourthinthetopglobalexportersleague,exportingaround81percentofits

totalproduction.TheUAEexportsaround2.32millionbarrelsofcrudeoileachdayto

predominantlyAsianmarkets.

PageNo.19

TheUAEholdstheworld'ssixthlargestprovenoilreservesofapproximately98billion

barrelsandseventhlargestgasreservesof213trillioncubicfeet.

Almost one‐third of the top 20 largest oil and gas projects in theMiddle East under

executionarenowtakingplaceintheUAE'sboomingupstreamsphere.

TheAbuDhabiInternationalPetroleumInvestmentCompanyinJuly2012inaugurated

apipelineviaFujairahtoarefinery inPakistanthatcompletelybypassestheStraitof

Hormuz. The1.8million‐barrel‐per‐day crude oil pipeline runs fromHabshan inAbu

Dhabi toFujairahandensuresthesecurityof theUAE'soilproductionandexports to

theworld.

The energy investment needs in the Middle East and North Africa region over the

period 2012 through to 2016 is expected to reach US$ 525 billion,withmost of the

energy investments being in the Arabian Gulf, according to The Arab Petroleum

InvestmentCorporation.

Around600,000barrelsperdaywillbeneededoverthenextdecadetomeettheUAE's

infrastructure,businessandinvestmentneedsreiteratingUAE'scontinuedrelianceon

technology, equipment and expertise in the oil & gas sector, to service its own

consumption.

UAEplanstobuildaliquefiednaturalgasbunkerstationinFujairahtomeet15%ofit's

increasingdemandongasbecauseofindustrialexpansion.

HowbigistheMiddleeast’soilandgasindustry?Howquicklyisitgrowing?(Nagraj,

2014)

Theworld’s largestoilproducer is theMiddleEast.ThoughSaudiArabiacontinues tobe

the region’s largest oil producer, Iraq displays one of the biggest growth rates in

production.

TheoilandnaturalgassectorintheMiddleEastwillrequireatotalof$1.6trillionofnew

investmentoverthenexttwoandahalfdecades.

Howwillthediscoveryofshaleintheusaffecttheregionaloilandgasmarket?

PageNo.20

Theuprising of light tight oil in theUSwill play amajor role inmeeting global demand

growthoverthenextdecade.However,theMiddleEastbeingtheonlylargesourceoflow‐

costoilwillmostcertainlyremainat thecentreof the longer‐termoiloutlook, capturing

mostoftheexpectedgrowthinglobaloildemand.

Whatarethemainchallengesthattheindustryfaces?

MiddleEasternoilproducersareencountering challengesof competitionandof growing

demandfromdomesticmarkets.Energyuseintheregionwillgrowby77percentby2035,

doublethe increase inproductionaccordingtothe latestestimates fromBP,whichcould

putpressureongovernmentsthatdependonoilexportrevenue

WiththeMiddleeastmarketsfocusingonrenewableenergy,howwilltheoilandgas

industryfareinthelongterm?

Duetohavingthelargestoilandgasreservesintheworld,onemightquestionwhetherthe

MiddleEast is the rightadvocate for renewableenergy.However,withoutstandingsolar

and wind conditions across the region, an increasingly tight gas market and a growing

recognition that hydrocarbon reserves could be put to better use other than generating

electricity, renewable energy is attracting unprecedented attention in the region. The

significantinvestmentbytheregionalcountriesisatestimonialtothefocus.

ThisisB2Bmarketinginallaspectsandtheprojectswhichwearetargetingisfromtheend

clients[oilfieldoperatorseg:ADMA,MAERSK,ZADCO,DP,QP,QGetc.]Thereisalways

highdemandforoffshoreworkingbarges/jack‐upbarges.Thevesselhastomeetthe

criteria’s/guidelinesofthefiledoperators.SuchguidelinesforADMA(OPCO,31.12.2004)

andMAERSK(MAERSKOIL,2011)shallbefollowedtoselectthevesselortheinvestment

requiredtomodifythevesseltomeetsuchguidelines.Therearelotsofprojectscomingup

inoil&Gasindustry,especiallyinthisgulfregion.(ZADCO,2014)Themostofthepipelines

arelaidin1970’sanditisagingnow.Theselinesaretobereplaced.Newfileddevelopment

projectsarealsocomingupinOman,RAK,Abudhabietc.Thesevesselscanbegivento

othercompaniesoncharteraswellforprojectspecificoroffshoreaccommodation

purpose.

PageNo.21

Afeasibilitystudyshouldbeabletoanswerthesemainquestions:

Idealtypeofvessel?[WorkBarge/Jack‐upbarge/Rigconverttoajack‐upworkbarge]

BuyorCharter?

MarketPotential?

Isitworthgoingahead?

GROWTHFACTORSANDCHALLENGES

Globaloilpricedynamicsaresubjecttomanyfactors,principallythebalanceofsupplyand

demand, the macroeconomic and geopolitical situation, the dynamics of the US dollar

exchangerateandconditionsoftheglobalfinancialmarkets.Technologicalbreakthroughs

make it possible to develop huge resources. The increase in unconventional oil and gas

productionintheUSservesasagoodexample.TakingintoaccounttheUSoilproduction

progressmany analytical agencies lower their long‐term oil price forecasts. At the same

time a number of trendswill support oil prices in themedium term. In this outlookwe

wouldliketospecifythesetrendsandcriticallyanalyzeanumberofchallengesthattheoil

industryfacenowadays.(Lukoil)

Growthfactors:

•Populationgrowth,urbanization

•MotorizationinAsia

•Growingcostsofexplorationandproduction

•OPECpolicy

•Dollardepreciation

Principalchallenges:

•IncreaseofunconventionaloilproductioninNorthAmerica

PageNo.22

•IncreaseofoilproductioninIraq

•Deepwatershelfproduction

•Biofuelsproductiongrowth

•Gastoliquids(GTL)expansion

FIGURE2FACTORSAFFECTINGOILPRICE

DEMOGRAPHICFACTORS

Our planet’s population will continue to grow rapidly. Between 2010 and 2025 global

populationwillgrowbymorethan1.1blnpeople.Thegreatestpopulationgrowthwillbe

registeredindevelopingcountries,whileinthedevelopedcountriespopulationwillremain

relativelystable.Highratesofpopulationgrowthareexpected, firstofall, inIndia,which

willbecome theworld’smostpopulouscountryby2020.Explosivepopulationgrowth is

also forecasted for the African countries where it will be the result of improvement in

socio‐economicconditionsandqualityofmedicalservices.Alongwithpopulationgrowth,

developing countrieswill experience themovement of the rural population to the cities,

PageNo.23

knownasurbanization.According to theestimatesofMckinseyGlobal Institute,by2025

440citiesindevelopingcountrieswillcontributeuptohalfoftheglobalGDPgrowth.

Atthesametimethelevelsofconsumptionwillgrow.Itisexpectedthatby2025thesizeof

the urban consumer class will grow by 1 bln people and the overall middle class will

amounttomorethan50%ofthetotalglobalpopulation.Themaingrowthwillcomefrom

developingAsiancountries.Urbanizationandgrowthoftheconsumerclassindeveloping

countrieswill, inturn,promotedemandforrealestate, infrastructure,cars,hi‐techgoods

and,asaresult,energyresources.(Lukoil)

FIGURE3DEMOGRAPHICFACTORSAFFECTINGOILPRICE

OILDEMAND

Demand for liquid hydrocarbons will continue to grow. Global demand for liquid

hydrocarbonswillcontinuetogrowannuallyby1.2%onaverageandwill,inourestimate,

reach 105 mb/d by 2025. The greatest surge in oil demand will come from the

transportation sector, for which oil is the principal energy source (over 90%).

Consumption of liquid hydrocarbons will increase in developing countries where the

transportation industry is undergoing rapid growth. Analysts expect to see significant

PageNo.24

growth in the number of cars as well as the development of sea, air and railway

transportation.

In addition to this, growth in demand for oil in developing countries will be further

encouragedbytheindustrialsector,inparticular,thepetrochemicalindustry.Atthesame

time, consumption of liquid hydrocarbons in developed countries will remain relatively

stable due to low rates of economic growth and further improvements in fuel economy.

Despitestablegrowthrates,oil’sshareintheglobalconsumptionofenergyresourceswill

gradually decrease, because of substitution for other energy sources in such sectors as

powergenerationandhousing.(Lukoil)

FIGURE4OILDEMAND

MOTORIZATIONINASIANCOUNTRIES

Themotorizationofthepopulationindevelopingcountriesisoneoftheprincipalfactors

behind the future growth in demand for oil. Today developing countries are severely

laggingbehinddevelopednations in termsof thenumber of carsper 1,000people, thus

creatingconditionsforsignificantgrowthinthesizeofglobalcarownership.Intheforecast

period, themostnoticeable increase incarownershipwill takeplace inChina,whosecar

PageNo.25

markethasalreadyenteredanintensivegrowthstage.Intoday’sChinathenumberofcars

per1,000peopleis40.By2025thisfigurewillbecloseto200,whichwillmeananincrease

of220millioncarsfortheperiodof2010‐2025.

Significantgrowth incarownershipwillalsoberegistered in Indiaandotherdeveloping

Asiancountries.By2025large‐scalegrowthofcarownershipwillbegininAfrica.Freight

cars and truckswillmake a strong contribution to the growth in consumption ofmotor

fuels.Thetotalnumberofsuchcarsisexpectedtogrowby140mlnby2025.Accordingto

ourestimates,theaggregateglobalcarfleetwillgrowby670mlnduringtheperiod2010‐

2025.Thiswillleadtoanincreaseinfuelconsumptionof9mb/d.(Lukoil)

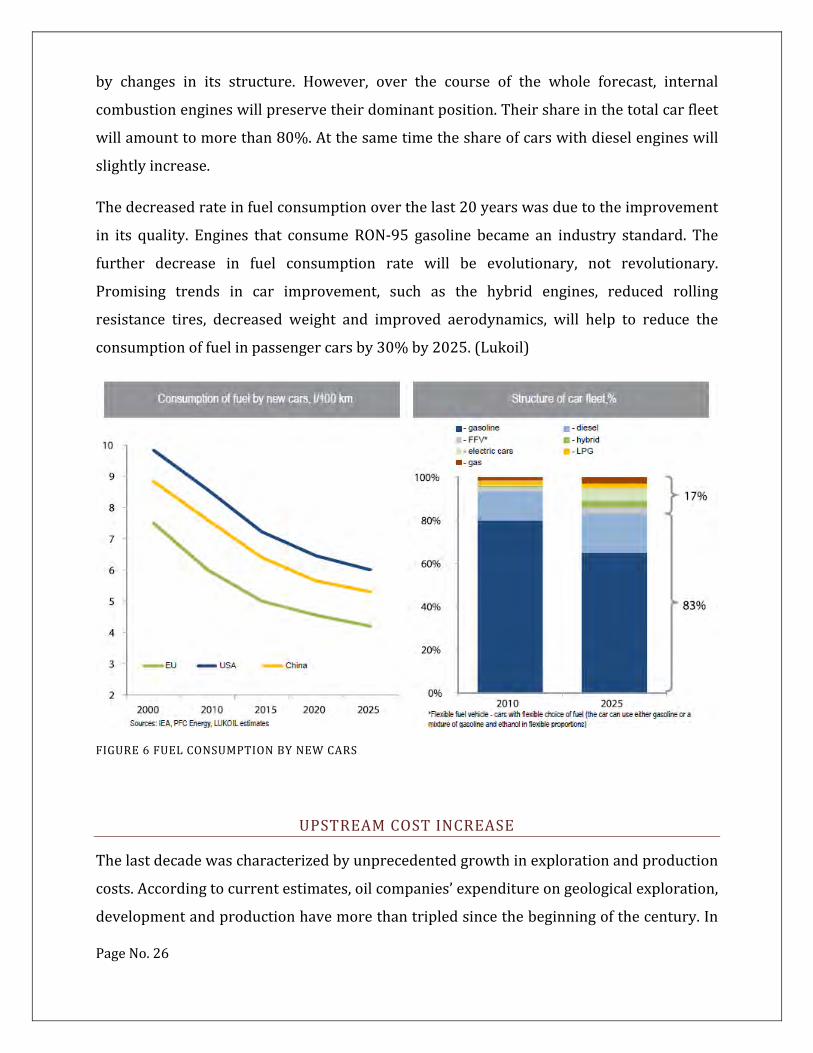

FIGURE5MOTORIZATIONCURVES

FUELECONOMYIMPROVEMENTS

We are currently observing a sustained trend towards decrease of fuel consumption in

passengercars.This ishappeningforanumberofreasons: thedesignsofcarbodiesand

enginesareimproving,thequalityofenginefuelisgettingbetterandhybridtechnologies

arebeingimplementedmoreoften.Growthinthesizeofthecarfleetwillbeaccompanied

PageNo.26

by changes in its structure. However, over the course of the whole forecast, internal

combustionengineswillpreservetheirdominantposition.Theirshareinthetotalcarfleet

willamounttomorethan80%.Atthesametimetheshareofcarswithdieselengineswill

slightlyincrease.

Thedecreasedrateinfuelconsumptionoverthelast20yearswasduetotheimprovement

in its quality. Engines that consumeRON‐95 gasoline became an industry standard. The

further decrease in fuel consumption rate will be evolutionary, not revolutionary.

Promising trends in car improvement, such as the hybrid engines, reduced rolling

resistance tires, decreased weight and improved aerodynamics, will help to reduce the

consumptionoffuelinpassengercarsby30%by2025.(Lukoil)

FIGURE6FUELCONSUMPTIONBYNEWCARS

UPSTREAMCOSTINCREASE

Thelastdecadewascharacterizedbyunprecedentedgrowthinexplorationandproduction

costs.Accordingtocurrentestimates,oilcompanies’expenditureongeologicalexploration,

developmentandproductionhavemorethantripledsincethebeginningofthecentury.In

PageNo.27

manyways the increase in costs is tied to thedepletionof the conventionaloil resource

base.Thegrowingdemandforhydrocarbonsforcescompaniestodevelopunconventional

and highly costly reserves. The companies are producing oil from deepwater shelves,

operatinghighviscosityoilfieldsandextractingoilfromtightreservoirs.Intoday’smarket

about 15mb/d have commercial production costs above $70/bbl. for example, shale oil

projectsintheUSonaverageareprofitableat$80/bblcostofoil.

Therefore,even ifdemandforoil fallssignificantly, itsequilibriumprice isunlikely tostaybelow

$70‐80/bbl for long.Futuregrowth inproductionwillprimarilycomefromthedevelopmentand

operationofunconventionalreserves.From2010‐2025over70%oftheincreaseinthesupplyof

liquid hydrocarbonswill come from the use of hi‐tech productionmethods and alternative fuels

suchasnatural gas liquids (NGL),GTL/CTLandbiofuel. Thegreatest increase inproductionwill

come from the deepwater shelf, tight oil reservoirs in theUS and heavy crude fromCanada and

Venezuela.WealsoexpectanincreaseintheproductionofNGL,primarilyintheMiddleEastandin

theUS.(Lukoil)

Figure7UPSTREAMCOSTINCREASEINOILEXPLORATIONANDPRODUCTION

USSHALEOILPRODUCTIONOUTLOOK

The development of horizontal drilling and hydraulic fracturing technologies havemade

profitable a significant amount of unconventional hydrocarbon reserves in the United

States.Thisbeganwiththeactiveproductionofshalegaswhichledtothecollapseofspot

PageNo.28

gasprices.Highoilprices in2011‐2012forcedmanycompaniestostartactivedrilling in

unconventionalreservoirscontainingliquidhydrocarbons.In2011thenumberofdrilling

oil rigs in theUSexceeded thenumberofgas rigs.Thegrowth inshaleoilproduction in

2011‐2012wasveryimpressive.OilproductionattheBakkenformationinNorthDakota

increasedmore than7.5 timesandamounted to589,000b/d in2012.Eagle fordplay in

Texasalsobecameasiteofexplosivegrowthinliquidhydrocarbonproduction.

In2012theaggregatevolumeofoilproductionfromunconventionalreservoirsintheUSis

estimatedtohaveequaled1.2mb/dy.Thetransportationandrefininginfrastructurewas

unprepared for such production growth and that led to a decrease in US oil prices. The

average spread between Brent and WTI oil amounted to $17/bbl in 2011‐2012, while

severalyearsbeforeWTIsoldatapremiumincomparisontoBrent.(Lukoil)

PageNo.29

FIGURE8OILPRODUCTIONINNORTHDAKOTA

UNCERTAINITYINRESERVEESTIMATION

Shaleoilreservesarecharacterizedbylowpermeability.Hydraulicfracturingtechnologyis

used to improve the oil inflow.Well flow rates in shale formations are characterized by

highdeclineratesinthefirstyearofproduction‐generallytheyamountto60‐70%ofthe

maximumflowrate.Shaleoil reserves in theUShaveundergoneseveral revisions in the

lastfewyears.In2008theUSGeologicalsurvey(UsGs)estimatedrecoverableoilreserves

attheBakkenformationat3,65bln.In2013theUSGSincreasedthereservesestimateto

7,4blnbbl.In2011ContinentalResourcesvaluedrecoverablereservesat20blnbbl.The

principalinstrumentofreserveestimationisproductioncurveanalysis,whereproduction

curvesarederivedfromtheactualdataofapproximatewellflowrates.Whentheperiodof

awell’soperationissmall,forecastsfordifferentproductioncurvesmayvarysignificantly.

Themajority ofwells in theBakken formation currently only have data for 3‐4 years of

actualoperations,leadingtosignificantdiscrepanciesinexistingestimates.

The value of the estimated ultimate recovery (EUR) depends on the chosen method of

calculation and data available. Estimates may significantly vary for different groups of

wells, depending on the quality of formation, hydraulic fracturing technology and other

factors.Hence,anoverestimationofshaleformationreservesispossible.(Lukoil)

PageNo.30

FIGURE9AVERAGEBAKKENWELLPRODUCTIONCURVE

POTENTIALFORWELLDRILLING

Whenforecastingshaleoilproduction,itisnecessarytotakeintoaccountthepotentialfor

well drilling. Themaximumnumber ofwellswill dependon theproductive area of land

suitablefordrillingandonwellspacing.Accordingtothecurrentestimates,themaximum

number ofwells that can be drilled at theBakken formation inNorthDakota is 33,000‐

39,000.Asthedensityofwellspacinggrows,EURdecreases,andthisshouldalsobetaken

into account when forecasting future production. Intensifying shale oil production by

increasingratesofdrillingwillleadtofastreservedepletion.

Accordingtoourestimates,dailyoilproductionof2mbattheBakkenformationisunlikely

tobesustainable,becauseinthiscasethedrillingpotentialwillbedepletedby2022‐2025.

ThemostlikelyscenarioofBakkenformationdevelopmentisthatitreachesaproduction

levelnothigherthan1.5mb/dby2020.Tosupportconsistentlyhighlevelsofproduction

companieswillhavetocontinueincreasingthenumberofactivedrillingrigs,leadingtothe

needtohiremoredrillingcrews.Accordingtothe2012pollconductedbyNationalOilwell

PageNo.31

Varco, theavailabilityofqualifieddrilling crews isoneof theprincipal challenges forUS

drillingcompanies.Itispossiblethatanothersubstantialconstrainttothegrowthinshale

oilproductionintheUSwillbeashortageofhydraulicfracturingcrews(Lukoil)

FIGURE10FORECASTOFNUMBEROFWELLS

OTHERCONSTRAINTS

Shale oil production requires the use of large quantities of water. Hydraulic fracturing

requires5‐19mln litersofwater.Thismaybecomeanimpediment incertainproduction

regions. There are also certain concerns regarding the environmental safety of shale oil

production.When hydraulic fracturing is underway at a shallow depth, companies may

inject chemical reagents into the ground waters. There may also be problems with the

disposalofusedchemical solutions. Inaddition, expertsnote that shaleoilproduction is

associated with the emission of methane and other dangerous compounds into the

atmosphere.

Some experts express concern that the use of hydraulic fracturing may lead to rock

movement and deformation, and this, in turn, can provoke landslides and restrict

construction. Considering this list of constraints,we forecast that shale oil production in

theUSwillamountto3.9mb/dby2025.Shaleoilproductiongrowthisexpectedprimarily

atthemostdevelopedformationsinBakkenandEagleford.Takingintoaccountwellflow

PageNo.32

rates, thepaceofdrillingand theproductivearea, themost intensivegrowth inshaleoil

production in the US will take place in the next 5‐10 years. After that production will

stabilize.(Lukoil)

FIGURE11FORECASTOFSHALEOILPRODUCTION

NORTHAMERICABECOMESTHELEADERINOILPRODUCTION

ForthenextdecadeNorthAmericawillremaintheleaderintermsofgrowthofproduction

of liquidhydrocarbons.By2025 theaggregatevolumeof liquidhydrocarbonandbiofuel

productionintheUSandCanadawillamountto19mb/d,thussignificantlyreducingthe

region’sdependencyonoil imports. Justseveralyearsagofewbelievedthatsuchgrowth

wouldbepossible in a regionwith consistentlydecliningproduction at brownfields.But

large‐scale deployment of innovative technologies has forced many to review their

evaluations.

TheUnitedStateswillcontinuetoincreaseliquidhydrocarbonproductionwiththehelpof

shale oil, the development of deepwater shelf and growth in NGL production In Canada

production growthwill primarily depend on the oil sands. By 2025 production of high‐

viscosity oil in Canada will reach 3.6 mb/d, which is 1.7 mb/d more than this year.

PageNo.33

Production growth in Canada may be significantly constrained by logistics and

environmentalconcerns.(Lukoil)

FIGURE12FORECASTOFPRODUCTIONOFLIQUIDHYDROCARBONINNORTHAMERICA

BIOFUELS

According to our estimates, the rapid growth in biofuel consumption that theworld has

beenexperiencingsincethemid‐2000sisunlikelytoberepeated.Europeanbiofuelshave

highproductionthecostanduntilrecentlyhavebeendevelopedwiththehelpofsubsidies.

InGermany,forexample,thecostofbiodieselproductionisalmosttwotimeshigherthan

thecostofproductionof regulardiesel fuel.Thecrisis,however, is forcing theEuropean

governments tocutbiofuelsubsidyprogramsand,asaresult,manyEuropeanproducers

are experiencing losses. In addition to this, the European Commission has proposed to

lowerthetarget levelof1stgenerationbiofuelconsumptionto5%ofthetotalvolumeof

motorfuelconsumption,whilethecurrenttargetlevelis10%.Ifthissuggestionispassed,

itwillhaveanegativeeffectontheconsumptionofbiofuelsinEurope.

PageNo.34

TheUnitedStatesistheworld’slargestbiofuelproducer,butthesituationthereisalsofar

from optimistic. It was believed earlier that the development of biofuels is a strategic

necessitycapableofdecreasingAmericandependencyonimportedoil.Butthegrowthin

productionofunconventionalhydrocarbonshasreducedtherolethatbiofuelsweremeant

toplayintheprovisionofAmericanenergysecurity.Manyexpertsdoubtwhetherbiofuel

productionisjustifiablefromanenvironmentalpointofview,since,asarule,productionof

fuelfromcropsrequiresfossilfuels.Takingthestatedcircumstancesintoaccount,wehave

aratherconservativeviewoffuturebiofuelprospects.(Lukoil)

FIGURE13FORECASTFORGLOBALBIOFUELPRODUCTION

DEEPWATERPRODUCTION

Astraditionalonshorereservesaredepleted,offshoreresourcesareplayingagreaterrole

insupplyingthegrowingdemand.Thegrowinginterestinshelfresourcesisillustratedby

thefactthatoverthelast20yearsthenumberoflargeshelfdiscoverieshasbeengreater

thanthenumberofbigonshorediscoveries.Today,provenoffshorereservesarevaluedat

280blnbbl,whileshelfproductionamountsto30%oftheglobalproduction.Technological

development helps oil companies to increase the depth of offshore fields. About 27%of

PageNo.35

shelfproductioniscurrentlyatadepthof300mandmoreandwithtimethisshareissetto

grow.Today,technologyallowsproducerstodrillatdepthsthatexceed3,000m.However,

developmentofsuchreservesrequiresmultimillion‐dollarinvestments

TheaccidentattheDeepWaterHorizondrillingplatformintheGulfofMexicohasforced

manycompaniestoreviewtheirapproachtosafetymeasuresduringshelfdrilling.Thiswill

lead to growing operating costs for offshore projects. The high tax burden in certain

countries, such as Angola and Nigeria, will also lead to growth in production costs.We

estimatetheoilpriceforprofitabledevelopmentofdeepwaterreservesshouldbeatthe

level of $50‐90/bbldependingon the regionofproductionandwaterdepth.Despite the

highcostofproductionandoperatingrisks,deepwaterproductionwillcontinuetogrow.

After2015,whenanumberofnewlargefieldswillbeput inoperation,weexpecttosee

significantproductiongrowth.(Lukoil)

FIGURE14DEEPWATERPRODUCTIONFORECAST

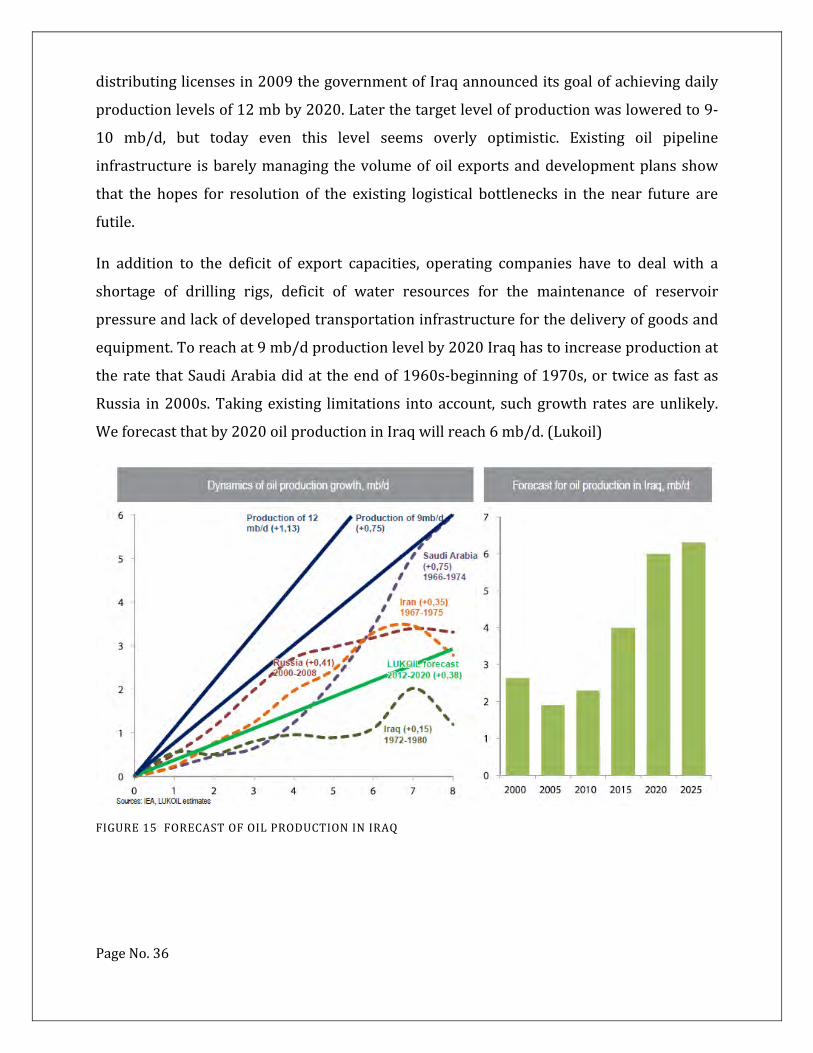

IRAQIPRODUCTIONGROWTHPROPSECTS

Iraq remains themost promising region in termsof conventional oil production growth.

Despitethecountry’s impressiveprovenreservesthatamountto143blnbbl,production

levels remain relatively low ‐ and in 2012 amounted to 3.1 mb/d. In the process of

PageNo.36

distributinglicensesin2009thegovernmentofIraqannounceditsgoalofachievingdaily

productionlevelsof12mbby2020.Laterthetargetlevelofproductionwasloweredto9‐

10 mb/d, but today even this level seems overly optimistic. Existing oil pipeline

infrastructure isbarelymanagingthevolumeofoilexportsanddevelopmentplansshow

that the hopes for resolution of the existing logistical bottlenecks in the near future are

futile.

In addition to the deficit of export capacities, operating companies have to deal with a

shortage of drilling rigs, deficit of water resources for the maintenance of reservoir

pressureandlackofdevelopedtransportationinfrastructureforthedeliveryofgoodsand

equipment.Toreachat9mb/dproductionlevelby2020Iraqhastoincreaseproductionat

theratethatSaudiArabiadidattheendof1960s‐beginningof1970s,ortwiceas fastas

Russia in2000s.Takingexisting limitations intoaccount, suchgrowth ratesareunlikely.

Weforecastthatby2020oilproductioninIraqwillreach6mb/d.(Lukoil)

FIGURE15FORECASTOFOILPRODUCTIONINIRAQ

PageNo.37

OPEC’SBALANCINGROLE

Today OPEC countries control about 42% of global oil production. Thanks to their

coordinated actions, cartel members are capable of rapidly reacting to changes in the

market situation by introducing production quotas. Such actions helped to stabilize oil

pricesratherquicklyduringtheglobalfinancialcrisisof2008.Oilpricesactasadecisive

factor for thebudgetrevenueplanningofOPECcountries.Asaresultof theArabSpring,

thebudgetaryobligationsofcertaincartelmembershavegrownsignificantly.Accordingto

existingestimates,thebreakevenpricethatallowsSaudiArabiatobalanceitsbudgetwas

about$78/bblin2012.

The probability of further budget expenditure needed to stimulate the economy and

implementinfrastructureprojectsisquitehighforthenext2‐3years.Forexample,Saudi

Arabia’s budget for 2013 envisions an increase of 19%. Therefore it should come as no

surprisethatSaudirepresentativesregularlyvoiceapriceof$100/bblasthetargetlevel.

In the medium term, as production by independent producers, especially the US and

Canada, grows, OPEC members will limit the growth of their own production, thus

supportingtheglobaloilpricesatnecessarylevels.(Lukoil)

FIGURE16DYNAMICSOFOPECSHAREINGLOBALPRODUCTION

PageNo.38

GTL‐CHALLENGEFORTHEOILMARKETAFTER2020

One of the most promising alternatives to oil fuels is GTL technology. This technology,

based on the synthesis of liquid fuels from coal ormethane, had been used back in the

1940s in Germany, which experienced a shortage of oil during World War II. GTL

technologymakes itpossible torefinemethanefromnaturalgas intoawidespectrumof

products, the most important of which are diesel fuel and kerosene with improved

environmentalcredentials.Today,revivalof interest inthistechnologyisaresultbothof

thestricterenvironmentalrequirementsformotorfuelsandofthepossibilityofoperating

gas fields in regions lacking gas transportation infrastructure. The largest active GTL

projecttodayisPearlGTL.Сurrentmarketpricesmakeitprofitable.

TheonlyprojectcurrentlyunderconstructionistheEscravosGTLinNigeria.Therelatively

smallnumberofactiveandplannedprojects isa resultof thehighcostsofbuildingGTL

refineries.OverthenextfewyearsGTLtechnologywon’tpresentaseriouschallengetothe

oil industry. But beyond this time the situation may radically change due to further

developmentofmethaneconversionmethods.Amongthepromisingmethodsisthemicro

channel technology that makes it possible to substantially reduce the physical size of

reactors, leading to a reduction in capital investments in construction. We believe that

development of GTL technologymay have a significant influence on the oilmarket after

2020.ShouldGTLtechnologygainlarge‐scalecirculation,it’spossiblewe’llseethespread

betweenoilandgaspricesnarrowing.(Lukoil)

PageNo.39

FIGURE17HISTORYOFGTLPROCESS

INFLUENCEOFDOLLAREXCHANGERATE

SinceoilpricesaredenominatedinUSD,thedynamicsoftheAmericancurrency’sexchange

rate will influence global oil prices. As a rule dollar depreciation leads to growth in oil

prices,while dollar appreciationdoes the opposite. The influence of the dollar exchange

rateonoilpricescanbeillustratedbycomparingthedynamicsofoilpricesinUSDwithoil

prices,denominatedinSwissfrancsandgold.Overtheperiodof2000‐2012,thepriceofoil

denominated inUSD increased3.9 times,while thepriceofbarreldenominated inSwiss

francsonlygrew2.2 times,while thepriceofoildenominated ingoldactually fell. If the

dollarwastightlytiedtothegoldstandard,thepriceofoiloverthelastdecadewouldbe

practicallyunchanged.

Overthelastdecadewehavebeenseeingatrendtowardsdollardepreciationagainstother

globalcurrencies.InmanywaysthisisaresultofUSmonetarypolicy.Depreciationofthe

dollar stimulates the US economy by having a positive influence on exports. Alongwith

economicgrowth,thecurrenciesofdevelopingcountries,especiallytheonesfromtheAsia

Pacific region, are appreciating.Most likely this trendwill continue in themedium term,

encouraginggrowthinoilprices.(Lukoil)

PageNo.40

FIGURE18DYNAMICSOFBRENTOILPRODUCTION

OILPRICESFORECAST

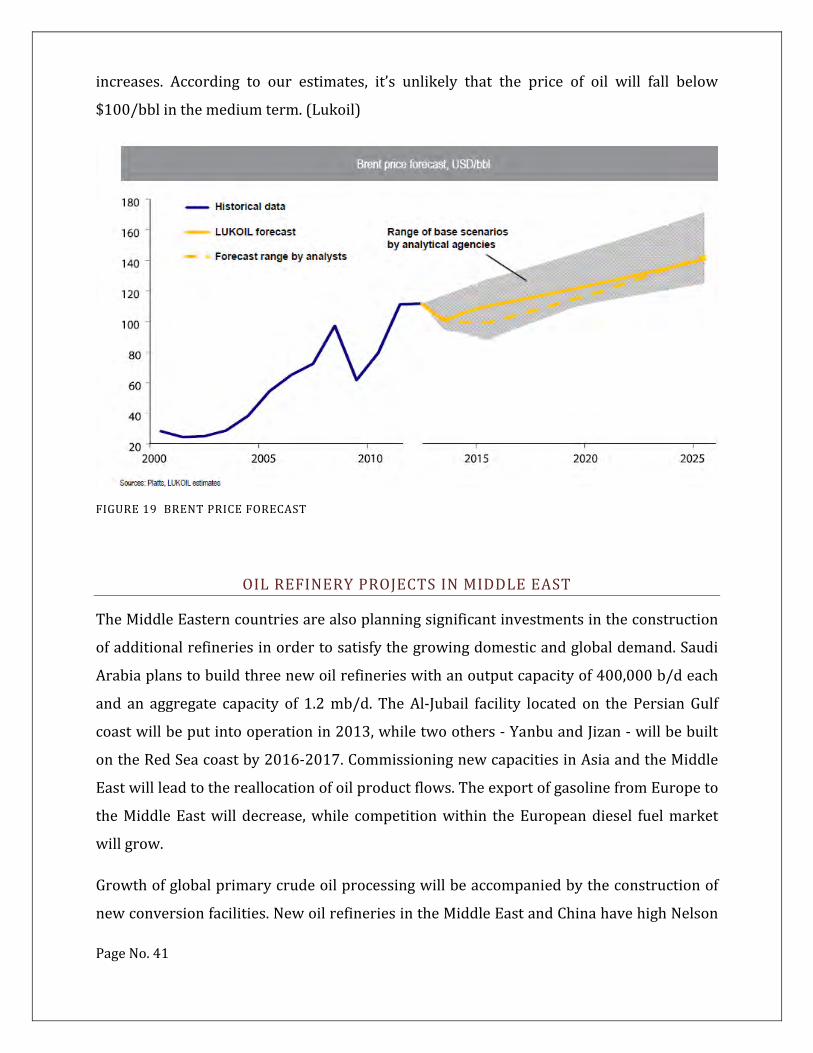

PopulationgrowthandhighratesofautomotivegrowthinAsiawillencourageanincrease

in oil consumption in the medium term. Growing demand and the natural decline of

production from conventional oil fields will require the development of new reserves.

Recently therehasbeenasteady trend towardsanescalation inE&Pcostswhichcanbe

explainedbythedepletionofconventionalfields.Astheincreaseinproductionwillbefrom

highcostsourcessuchasdeepwaterfields,high‐viscosityoilandoilfromtightreservoirs,

the production costs will continue to grow. Taking into account the high cost and

technological achievements in oil production, biofuelswill not have serious stimulus for

growthinproduction.

The increase inoilproduction inNorthAmericawillbegradualwhichwill allowmarket

playerstoadjusttochanges.Medium‐pacedincreaseinoilproductionisexpectedinIraq

where the planned production probably won’t be reached due to technological and

infrastructuralshortage.OPECwillstrivetokeeppricesabove$100/bbltomeetitsbudget

commitmentsastheindependentproducersincreasetheirproduction.Aboveall,thetrend

towards US dollar depreciation is one of the important factors that influence oil price

PageNo.41

increases. According to our estimates, it’s unlikely that the price of oil will fall below

$100/bblinthemediumterm.(Lukoil)

FIGURE19BRENTPRICEFORECAST

OILREFINERYPROJECTSINMIDDLEEAST

TheMiddleEasterncountriesarealsoplanningsignificantinvestmentsintheconstruction

ofadditionalrefineriesinordertosatisfythegrowingdomesticandglobaldemand.Saudi

Arabiaplanstobuildthreenewoilrefinerieswithanoutputcapacityof400,000b/deach

and an aggregate capacity of 1.2mb/d. TheAl‐Jubail facility located on the Persian Gulf

coastwillbeputintooperationin2013,whiletwoothers‐YanbuandJizan‐willbebuilt

ontheRedSeacoastby2016‐2017.CommissioningnewcapacitiesinAsiaandtheMiddle

Eastwillleadtothereallocationofoilproductflows.TheexportofgasolinefromEuropeto

theMiddleEastwill decrease,while competitionwithin theEuropeandiesel fuelmarket

willgrow.

Growthofglobalprimarycrudeoilprocessingwillbeaccompaniedbytheconstructionof

newconversionfacilities.NewoilrefineriesintheMiddleEastandChinahavehighNelson

PageNo.42

complexity Indices and this implies that they have extensive conversion capacities. For

EuropeanoilrefineriestheaverageNelsonIndexequals7units,butforthenewcapacities

intheMiddleEastandAsiathisfigureamountsonaverageto10units.Constructionofnew

conversioncapacitieswillcontinuetotakeplaceindevelopingcountries.Themostpopular

productionprocesseswill includehydrocrackingunitsused forproductionofdiesel fuel

and high quality motor oils, catalytic cracking units used for production of high octane

gasolineandthecokingunitthatallowsheavyresiduestoberefinedintopetroleumcoke

withproductionofadditionallightoilproducts.(Lukoil)

FIGURE20LARGESTNEWOILREFINERYPROJECTSINTHEMIDDLEEAST

RESEARCHOBJECTIVES

TounderstandtheOil&Gasmarketpotentialgrowth.

Tounderstandthesuitablemarinespreadconsideringmarketdemand.

Tounderstandtheimplicationsinvestment,operatingcostandreturn.

Tocheckthefeasibilityofowningamarinespread.

Tounderstandtheadvantagesanddisadvantagesofchartering.

PageNo.43

Tokeepthebusinesssustainableandprofitable.

RESEARCHMETHEDOLOGY

This isdoneby interviewing thedecisionmakers invariouscompaniesand interviewing

experiencedoil&gasprofessionals.Thisistogaugeandunderstandthedemandofmarine

spread in Middle East and other part of the globe. Also, it will give an idea about the

company’s budget and economic conditions of themarket by giving a clearer picture on

demandandpotentialtowincontractsaswellascompetition.

PRIMARYRESEARCH

Primaryresearchisdonetofindoutthesuitablemarinespreadtoownandadvantagesand

disadvantagesofowningamarinespread.

Whatisthebasicoperationalrisk.ThispartoftheresearchisdonewithvariousOperation

managersofMarinecompanieswhichareoperatingtheirvesselsmostlyinMiddleEast.

Primaryresearchinvolvesthein‐depthinterviewwithkeypersonnelinvariousOil&Gas

companies .It gives the information regarding the upcoming projects, competitions,

potentialcompetitors,updatedmarineregulationsandsafetyrequirementstooperatethe

vessel.Thisresearchwillhelpusinfindingoutthedemandforthemarinespread.

Belowmentionedarethestakeholderswhowillbeinterviewedforgainingdeeper

understandingabouttheOil&Gasindustryandmarketdemandconditions.

VesselOperators‐The interviewwillbe1‐1andwillbean IDIwhichmeansan InDepth

InterviewbasedonQualitativeResearchQuestionnaire.Thistypeofaninterviewwillhelp

usgainmoreinsightonhowtheoperationsareruntooperateamarinespreadandwhat

are their futureplans in termsofnewbuildvesselwhichgivesan insight for themarket

demand.

Customers‐Oil&GasfieldOperators.Variouskeyprofessionalswhoworksforthemajor

oil field operators in Middle East are interviewed to understand their needs and

PageNo.44

requirementswithrespect to themarinespread.Tounderstandwhat is themostcritical

factor, in terms of HSE and marine regulations for them in order to give business to a

company.

SECONDARYRESEARCH

WehavecollectedthedatafromvariousreadingmaterialsavailableonOil&Gasindustry

presentinpublishedbooksaswellasonline.Thisdatahashelpedusindetermining

varioustrendsinoil&Gasindustry,Oilpricevariation,Oilproductiondemandetc.We

requiredtoknowthepast,presentandfutureprojects.

PROJECTSCOPE

Basedontheresearchmethodologythefindingscollectedbasedontheanalysisdonewill

helpusintakinganinformeddecisionwhethertogoforwardwithbuyamarinespreadup

or not. Based on the investment and assumptive return as per other operatorswe have

forecasted Profit and loss for the organization. We have used past project data and

assumptive returnby the competitorshowever these are all basedon thepast thus it is

necessarytofactorinmacroeconomicconditionsaswell likepolitical,currency,oilprice

inflationrisksetc. HoweverMiddleEastmarkethas lowriskscomparedtootherpartof

theGlobe.ThedemandfortheVesselinotherpartoftheGlobeandareaslikeEastAfrica,

NorthSeaandvariousreducestheriskofthismarket.

VESSELSNOTINCLUDEDINTHEFLEET

OIL & GAS operators mostly have restrictions to use conventional mooring barges to

operate near the Offshore platforms. It has got potential risk for the subsea pipelines.

Anchordrag,misspositioningofanchorswillresultsindamagingthesubseapipelines.In

additiontothattheweatherdowntimesforsuchvesselsareveryhigh.HencetheOilfiled

operatorsprefersJack‐upbargesforthetopsidemodificationworksaswellasothersubsea

work. Henceconventionalmooring bargesareeliminated fromtheFleet.For theGreen

PageNo.45

fieldprojects,tolaynewpipelines,theconventionalmooringbargesrequiredandthatshall

beconsideredlaterstageofthebusiness.

LIMITATIONS

OneofthemajorlimitationsfortheJack‐upbargesarelimitationinoperatingindeepsea.

Theleglengthofthejack‐upgovernstheoperatingdepth.SincetheMiddleEastoilfields

areshallow,wedidn’tanticipateanythreatinoperatinginthispart.

FINDINGANDANALYSIS

PRIMARYRESEARCH

Theprimaryresearchontherequirementsforselectthemarinespreaddivertedtothe

initialinvestment,potentialdayratesandOperationalcosts.Itinvolvedin‐depthinterview

withtheoperationalmanagerofvariousmarineoperators.

Comparisonofdifferenttypesofvesselandtheiradvantageanddisadvantagesaregiven

below.

Sl.No. Issues

Accommodations‐workBarge[OPTION‐1]

Buy/buildJack‐upbarge[OPTION‐2]

Convertdrillrigtoaccommodation‐workbarge[OPTION‐3]

1Operatingmode Afloatmode Elevatedmode Elevatedmode

2Metoceaneffect

Direst,therewillbesitedowntimesforHs>1.5

In‐derect,nositedowntimeduetoheavyseas

In‐derect,nositedowntimeduetoheavyseas

3Monsoondowntime Yes

No,roundtheyearoperation

No,roundtheyearoperation

4 Operatingcost

More,duetomooringspread&moredowntime Less Less

5Mobilizationcost

More,duetomooringspread Less Less

6Initialinvestment Low VeryHigh High

7Assetre‐salevalue Low High High

PageNo.46

8 Marketratesupto30,000US$/day

upto75,000US$/day

upto65,000US$/day

9Initialinvestment* 15mto25mUSD 60mto100mUSD 45mto55mUSD

TABLE1COMPARISONOFVESSELS,THEIRDAYRATEANDOPERATINGEXPENSES

FINDINGS

TentativelybasedonPrimaryresearch(IDI)arementionedbelow.

Interviewer:Myself

Interviewed:MukeshNair‐OperationsManager(MubarakMarine)

Mr.Ron–Director(LivingstoneLiftboats)

JeffJackson‐OperationsManager(AquaDive)

Jack‐upbargesarethehotcakeinMiddleEastMarket

ThereisdeficiencyofJack‐upbargesinthisMarket.

TheOffshorecompaniesowningaJack‐upbargeisveryfew.

OilfieldOperatorsprefersEPCcontractorswiththeirownvessel.

Minimalinterfacesintheproject.

Owningavesselwillenablethecompanytogivecompetitivebidsincethemajor

costfactorfortheoffshoreprojectsarethemarineunits.

MarineUnitswillenablethecompanytowinbidsirrespectiveofcompetition.

ManyofthevesseloperatorsfailingtoqualifythestringentrequirementofOil

fieldoperatorslikeADMA,ZADCOetc.Sinceourcompanyisalreadyqualifiedfor

differentworks,itshouldn’tbeaproblemforustogetitthrough

TENTATIVELYASEDONPRIMARYRESEARCH[IDI]WITHCUSTOMERS

Interviewer:Myself

Interviewee:Mr.RahulRajan(HSEdesignhead,ADMA)

Mr.Byron(SeniorProjectEngineer,MOQ)

Vishak Gopi

Text Box

Vishak Gopi

Text Box

PageNo.47

Mr.Anish(PrincipleSurveyor,DNV,Abhudhabi)

ThereisagoodneedforJack‐upvessel

Mostoftheavailablevesselsareagingnow.15yearsistheallowableageofthe

vesseltooperateinmostoftheoilfields.

It’sagoodideatohaveafleetalongwiththeotherservicesourcompanyoffers.

Mostofthesubseapipelinesandplatformarebuiltin1970’sandmostofthem

areagingnow.

Thepipelinesaretobereplaced.Topsidepipingtobereplacedorupgradedfor

higherdesignpressure

Mostofthetopsidepipingaredesignfor3250psiandithastobeupgradedto

3600psitoincreasetheoperatingpressureandhenceproduction.

Thereisanupcomingtenderforconductorpiperepairofover100wellhead

towersandboatlandingreplacementofover100platformsinAbhudhabioil

field.

SECONDARYRESEARCH

Secondaryresearchwasaccumulatedthroughvariousliteraturesavailableonlineand

otherwise.

HereisimportanttoscantheMACROECONOMICfactorsspecifictoOil&Gasindustry,

MiddleEast.

P‐PoliticalItisimportanttoknowthatMiddleEastispoliticallyverystable.The

Governmentisverystableandfocusesonoilproductiongrowth.

(Source:ArabianBusiness.com,2007)

E‐EconomicallyMiddleEastOil&Gasmarketisboomingthoughataslowerpace.About

56percentoftheworld'soilreservesand36percentoftheworld'snaturalgasreserves

areintheMiddleEast.2011sawUAEastheworld'seighthlargestoilproducer,churning

outanaverageproductionvolumeof2.813millionbarrelsperday.UAEcomesfourthinthe

Vishak Gopi

Text Box

PageNo.48

topglobalexportersleague,exportingaround81percentofitstotalproduction.TheUAE

exportsaround2.32millionbarrelsofcrudeoileachdaytopredominantlyAsianmarkets.

Almostone‐thirdofthetop20Oil&GasprojectsintheMiddleEastunderexecutionarein

UAE.(SourceGas,2014)

S‐Social‐ThesocialenvironmentinMiddleEastisveryhealthy.Expatriatesfromvarious

partsoftheglobeprefertoworkintheMiddleEast.Todevelopanexperiencedworkteam

foroffshoreoperationswouldn’tbeamajortask.OurcompanyoperatesinFreezone,and

thegovernmentbelievesinmakinggoodrelationshipwitheachotherforthegrowthofthe

business.

T‐Technologically‐MiddleEast,especiallyUAEisverysimilartootherEuropean

countries.Peoplehaveaccesstoallthenewtechnologicgadgetsandtherearemanylocal

andmultinationalcompaniesrunningtheiroperationswhichrequiregoodqualityproducts

andservices.

E‐Ecological‐UAEgivesspecialfocusoncleanlinessandsafeguardingitsnaturalbeauty.

SharjahFreezonehasalwaysrunaggressivecampaignstotakecareoftheecologicalaspect

oftheenvironment.

L‐Legal–SharjahHamriyahfreezonewasfoundedorestablishedoveradecadeandover

6000variouscompaniesareoperatingfromHFZ.Itprovidestheoptionof100%

ownershiptotheexpatslivingintheUAE.HFZgivesprioritiestothecompaniesregistered

inHFZintermsofberthallocation,permissionforthevesseltoenterandgoout,pilotage

servicesetc..

PageNo.49

PORTER’SFIVEFORCES

FIGURE21PORTER’SFIVEFORCESMODEL

(Source:PortersFiveforces,2013)

AsperPortersfiveForcesModelfollowinghasbeenestablished

Throughouttheanalysiswewillbegaugingiftheenvironmentisfeasibleforabusiness

liketooperateamarinespreadbasedonthefactorsmentionedaboveinfigure21.

Threatofnewentrants‐Threatofentrantscanbementionedasaveragesinceitisneither

veryhighnortoolow.Since,MiddleEastOil&Gasmarketisgrowingandmanyprojects

arecomingup,severalcompaniesareeyeingexpansioninincreasingtheirfleet.However

thereisdeficiencyinJack‐upinthemarket.Henceifthecompanyisowningajack‐upand

providesgoodserviceandbuildsupgoodrelationshipwiththecustomersthenthethreat

fromnewentrantscanbefurtherreducedtoagreatlength.

BargainingPower–Sincethecompanyalreadyhasgotexperiencedprojectexecution

teamandalreadyprovidinggoodservicetotheclients,theadditionofmarinespreadwill

definitelyelevatethebargainingpowerofthecompany.

ThreatofSubstitutes‐ThreatofsubstitutesisverylesssinceJack‐upbargescanbe

replacedwithJack‐upbargesonly.Todeployanewteamreplacinganexistingcompany

familiarwiththefieldandsafetynormsisnoteasytaskfortheclients.

PageNo.50

Rivalryamongcompetitors‐Competitionatthemomentisverylowsincethereis

deficiencyofsuitableAck‐upbargesinthemarket.Experienceinprojectexecution,HSEis

themajorfactorcompetitivenessinOil&Gasindustry.Thusfocusongoodandsafeservice.

VeryHighHighModerateLowVeryLow

12345

Threatofnewentrants 4

BargainingPowerofSuppliers 2

BargainingPowerofBuyers 4

ThreatofSubstitutes 5

RivalryAmongCompetitors 3

TABLE2ANALYSISBASEDONPORTERSFIVEFORCES

SWOTANALYSIS

Strength

ExperiencedTeam

Inhousecapabilitytooperate

Opportunities

Enablethecompanytowinprojectsbyattracttheclientswithmarinespread

Lessoperatingcostcomparedtothecompetitors.

C

Weakness

Newoperatorswhichwilltaketimetoestablishitselfasabrand

Threats

Verylowcompetitionentrybarrier

Contractorsliketodealwithexperiencedmarineoperators.

PageNo.51

TABLE3SWOTANALYSIS

DECISIONTREEFORSETTINGUPMARINEOPERATION

Figure22DECISIONTREE

Therevenueiscalculatedbasedonthedayrateofthestandardjack‐upbargesvsaverage

operational daily expense. Considering strong growth of 300 charter days and yearwill

giveanetreturnof15.5miland weakgrowthof250charterdaysayearwillgiveanet

returnof11.5mil.

Five year operation will enable the company to achieve break even in good growth

scenario.

Whereascharteringoptionwillgiveanominalcommissionof10%marginondayratesand

stronggrowthwillgive1.05milreturnsinanyearcomparedtoaweakgrowthof0.63mil

peryear.

ThedayrateofJackupis70000USDperday

Average operating cost 15000 USD per day considering operating crew charges and

maintenancecost[IncludingFuelOil,LubeOil,FreshWateretc].

Thestronggrowthconsidered300daycharterperyearirrespectiveoflongtermorshort

termcharters.250charterdaysperyearconsideredforweakgrowth.

Jack–UpBarge

Buy

Charter

StrongGrowth.300charterdaysanyear

StrongGrowth.150day

WeakGrowth.250days/year

WeakGrowth.90days

21‐5.48=(15.5mil)

17.5‐5.48=(12.02mil)

1.05mil

0.63mil

PageNo.52

Forthepresentcharteringoptioncompanyfollowsatariffof10%marginondayratesand

whicheventuallygives1.05mil revenueperannum ina stronggrowth scenariowhereas

0.63milincaseofweakgrowthscenario.

RECOMMENDATIONS

Now that findings encourage us going forwardwith own amarine spread. The required

specificationstobesetinthebeginning.Thenextchallengeistofindasuitablevesselinthe

market for sale and compare its cost to build in house. Since the company is capable of

manufacture a Jack‐up internal price comparison and committed work load shall be

analyzedandthemanagementwilltakeacallonbuyfromoutsideorbuiltin‐house.

MANAGERIALIMPLICATIONS

OntheabovefindingsandanalysistheorganizationneedtogoforwardwithowntheJack

upBarge.Sincethecompanyownthequay‐sidefacilityandJettyitwon’tbedifficulttoget

theberthtoanchortheJackupbarge.Theadditionalcostwillbetheoperationalcostas

mentionedintheprimaryresearchfindings.

SUPPLIERS

TheJackUpbargecanbebuiltin‐houseorbuyoutfromthemarket.TheavailableJackupbargesinthemarketasfollows

Livingstone360

AquaDiveII

WorkBoatInternational

RodsonUniversalPteLtd

Force3Offshore

PageNo.53

VESSELCOST

Livingstone360costs–USD80‐100mil

AquadiveII‐USD50‐60mil

InthisstudyUSD100milinvestmentconsideredeithertobuyLivingstone360classliftboatorUSD100miltobuiltin‐houseaJack‐upbargewhichisconsideredtobeaperfectoneinthismarket.

INFRASTRACTUREREQUIREMENT

Thelistofinfrastructurerequired:

Jetty–75meter Waterfrontequipmentstoragearea–2500Sq.Meter Officespace‐20person

Sincethecompanyalreadyhavingthemanpoweranddedicatedshiprepairdivision,themaintenanceofthevesselshallbedoneinhouse.

HUMANRESOURCEREQUIREMENT

ListofPersonnelrequirement[BargeOperation]:

BargeSuperintendent‐1nos BargeEngineer‐2nos BargeMaster–1nos FirstEngineer‐4Nos SecondEngineers‐6Nos Technicians‐12Nos StoreKeeper/Logistic‐1Nos Seamen‐8Nos Medic‐1nos

Note:TheEmployeesforbargeoperationshallbeoncontractbasisandtheirsalaryincludedinoperationalexpenses.

ListofPersonnelrequirement[OnshoreSupport]:

MaintenanceManager‐1nos[300,000AEDperannum]

PageNo.54

OperationsManager‐1nos[300,000AEDperannum] BusinessDevelopmentManager–1nos[300,000AEDperannum] FinanceManager‐1[300,000AEDperannum] ContractsManager‐1[300,000AEDperannum] ProjectManager‐1[300,000AEDperannum] Project/FieldEngineers‐2Nos[240,000AEDperannum] DesignEngineer/NavalArchitects‐2Nos[240,000AEDperannum] HRassistant‐1Nos[75,000AEDperannum] Secretory‐2Nos[75,000AEDperannum] Documentcontroller‐1Nos[75,000AEDperannum] Officeboy‐1Nos[48,000AEDperannum]

Themaintenance,finance,HR&Admin,Logistics,andSecurityetcshallbeutilizedfromtheexistingteam.

COMPETITORS

ItisalsoessentialtoknowaboutthecompetitorsinthismarkettogoforwardwiththeideatoownaJack‐upbarge.Thelistofcompetitorsisasbelow:

GMS ALROUMIGENERALTRADINGESTABLISHMENT ALMANSOORIPRODUCTIONSERVICES BINJABRMARINEEST. EMIRATESWESTERNOILWELLDRILLINGANDMAINTENANCECOMPANYLLC GENERALPETROLEUMSERVICESEST GULFAUTOMATIONSERVICES&OILFIELDSUPPLIES(GASOS) GULFMARINESERVICES MARIDIVE&OILSERVICES MUTAWAMARINEWORKSL.L.C. SCHLUMBERGERMIDDLEEASTS.A. TARGETENGINEERINGCONSTRUCTIONCO.LLC UNIARABENGINEERING&OILFIELDSERVICES ZAKHERMARINEINTERNATIONALINC. NATIONALPETROLEUMCONSTRUCTIONCOMPANY(NPCC) NATIONALPETROLEUMCONSTRUCTIONCOMPANY(NPCC) ALSHOUMOUKHINTERNATIONALSERVICES(SISCO) WHITESEASHIPPINGLLC STANFORDMARINESERVICESLLC WELLSTECHNIC EMDADLLC(exALBAWARDIEST) KHALIDFARAJSHIPPING

PageNo.55

ABUDHABIPETROLEUMPORTSOPERATINGCOMPANY(IRSHAD) ESNAAD HALLIBURTONWORLDWIDE BOSKALIS MUTAWAGROUP GPC AQUAMARINE LIVINGSTONE

PROJECTEDPROFIT&LOSSSTATEMENTFORFIVEYEARS

Year1 Year2 Year3 Year4 Year5Charterrevenue[300days/year]

21,000,000 21,000,000 21,000,000 21,000,000 21,000,000

Operatingcost[Includingmarinecrew]

5,475,000 5,748,750 6,036,188 6,337,997 6,654,897

GrossProfit 15,525,000 15,251,250 14,963,813 14,662,003 14,345,103GeneralandAdminExpenses

RentalofPremises 60,000 63,000 66,150 69,458 72,930

Salaries,allowances&bonuses[Onshoreteam]

900,000 945,000 992,250 1,041,863 1,093,956

Sales&MarketingExpenses Travelling/businessmeeting

50,000 50,000 50,000 50,000 50,000

TenderFee 30,000 30,000 30,000 30,000 30,000Others 50000 50000 50000 50000 50000TotalS&M 130,000 130,000 130,000 130,000 130,000PBDIT 14,435,000 14,113,250 13,775,413 13,420,683 13,048,217PBIT 12,035,000 11,713,250 11,375,413 11,020,683 10,648,217Profit/LossBeforeTaxation 9,035,000 8,713,250 8,375,413 8,020,683 7,648,217

LessTaxation 0 0 0 0 0

Profit/LossAfterTaxation 9,035,000 8,713,250 8,375,413 8,020,683 7,648,217

NetProfit[USD] 9,035,000 8,713,250 8,375,413 8,020,683 7,648,217TABLE4PROFIT&LOSSSTATEMENT

PageNo.56

BREAKEVENANALYSIS

Contribution=SellingPrice[Dayrate]–VariableCost=70000‐15000

BreakEvenPointofcharter=FC/Contribution

BreakEvenPoint=6565000/55000

=120Charterdays

THEWAYFORWARD

Fromthepastfewyearswehavebeenfacingchallengetofindasuitablevesseltobidandwintheoffshoreprojects.Ontopofthegainfromthecharterrevenuethemajorpotentialgainwouldbe theprofit fromtheoverallproject.Theproject shallbe takenas the lumpsum for a said duration and with the effective project management the days saved inschedulewouldaddthemajorprofitmargin.

Thereispotentiallongtermcharteravailablewithmajoroil&gasoperatorsin

Abudhabi,theprojectcalled“conductorpiperepair”forover100wellheadplatformsand“Boat landing replacement” for over 100 platforms. Since Technomak had successfullycarriedouttheConductorrepairoffivewellheadtowersasapilotproject,thatwouldhelpuswinningthecontract.