Virgin Money Broker Lending Guide · 3 Who are we? You probably know the Virgin brand trusted...

43

1 Virgin Money Broker Lending Guide July 18

Transcript of Virgin Money Broker Lending Guide · 3 Who are we? You probably know the Virgin brand trusted...

1Virgin Money Broker Lending Guide

July 18

2

Information in this guide was prepared by Virgin Money (Australia) Pty Limited ABN 75 103 478

prospective borrowers or third parties without the prior written consent of Virgin Money Australia.

Virgin Money (Australia) Pty Limited ABN 75 103 478 897 promotes and distributes the home loans as the authorised credit representative of the credit provider, Bank of Queensland Limited

Policy and does not purport to be a complete statement of Summary of that policy. It must not

credit Assessment Criteria.

Whilst Virgin Money has taken due care in preparing this Guide no warranty is given in relation to the accuracy of this document and neither it, nor any of its related bodies corporate, nor employees, directors or other persons associated with these entities accept liability for any acts or omissions in reliance on this guide.

Important Information

3

Who are we?

You probably know the Virgin brand trusted globally and well-known for shaking things up and providing real alternatives when we think people deserve a fairer go.

At the heart of our value proposition is:

• Placing our people, partners and customers first

• Rewarding genuine loyalty

• Being transparent

passionate about helping people realise bigger possibilities through the delivery of beautifully simple and rewarding financial products, all backed by Virgin

We focus on providing a rewarding proposition and great customer experience.

Our home loans are supported by dedicated Virgin Money broker and customer support teams.

4

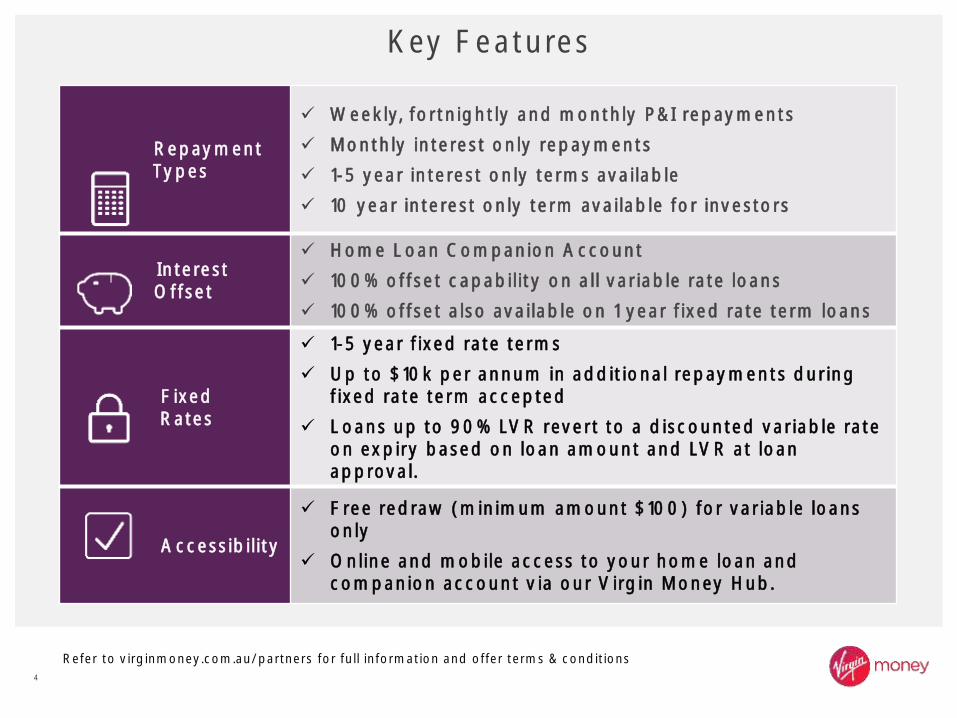

Key Features

Repayment Types

Weekly, fortnightly and monthly P&I repayments

Monthly interest only repayments

1-5 year interest only terms available

10 year interest only term available for investors

Interest Offset

Home Loan Companion Account

100% offset capability on all variable rate loans

100% offset also available on 1 year fixed rate term loans

FixedRates

1-5 year fixed rate terms

Up to $10k per annum in additional repayments during fixed rate term accepted

Loans up to 90% LVR revert to a discounted variable rate on expiry based on loan amount and LVR at loan approval.

Accessibility

Free redraw (minimum amount $100) for variable loans only

Online and mobile access to your home loan and companion account via our Virgin Money Hub.

Refer to virginmoney.com.au/partners for full information and offer terms & conditions

5

Reward Me Home Loan Key Fees

Fee Type Amount

Monthly Fee $10 per loan account (split) per month

Settlement Fee $150

First Valuation Fee $0

Additional Valuation Fee/s (per additional security)

Quoted on application

Additional Security Fee $150 per additional security

Document Variation Fee $200 when change initiated by client

Rate Lock Fee 0.15% of Loan Amount

Construction Loan Fee $250

(covers 4 drawings)

For further information on applicable fees and charges refer to the product key fact sheet available at

www.virginmoney.com.au/partners

Refer to virginmoney.com.au/partners for full information and offer terms & conditions

6

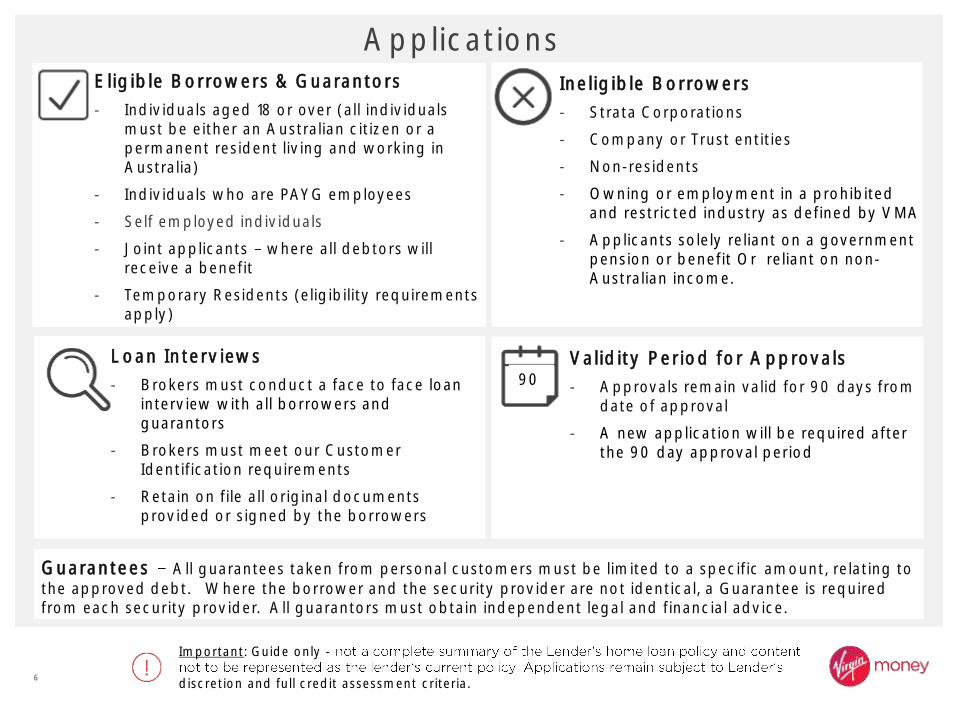

Applications

Loan Interviews

- Brokers must conduct a face to face loan interview with all borrowers and guarantors

- Brokers must meet our Customer Identification requirements

- Retain on file all original documents provided or signed by the borrowers

Ineligible Borrowers

- Strata Corporations

- Company or Trust entities

- Non-residents

- Owning or employment in a prohibited and restricted industry as defined by VMA

- Applicants solely reliant on a government pension or benefit Or reliant on non-Australian income.

Eligible Borrowers & Guarantors

- Individuals aged 18 or over (all individuals must be either an Australian citizen or a permanent resident living and working in Australia)

- Individuals who are PAYG employees

- Self employed individuals

- Joint applicants where all debtors will receive a benefit

- Temporary Residents (eligibility requirements apply)

Validity Period for Approvals

- Approvals remain valid for 90 days from date of approval

- A new application will be required after the 90 day approval period

90

Guarantees All guarantees taken from personal customers must be limited to a specific amount, relating to the approved debt. Where the borrower and the security provider are not identical, a Guarantee is required from each security provider. All guarantors must obtain independent legal and financial advice.

Important: Guide only -

discretion and full credit assessment criteria.

7

Lending Parameters

Loan Purpose

Purchase, Refinance, Construction or Debt Consolidation & Equity Release (Cash Out)

Purposes involving cryptocurrency or refinance of small loan provider debts are unacceptable.

Loan Amounts

Minimum $75,000 / No Maximum without LMI or up to $3m subject to LMI approvalMinimum Loan Split Amount $25,000

Maximum total loan amount of $2.5m for interest only loans (total aggregate borrowings on IO products). Note: for Interest only lending the detailed in application notes.

Genuine Savings

Above 90% LVR Genuine Savings is generally required.

Non-Gen savings can be considered if applications meet certain criteria:

Must be an owner occupied purchase

Repayments must be on a P&I basis

Security must be under 2.2 acres

Term Maximum 30 years

Cross Collateralisation

VMA will look to cross collateralise security over the borrower(s) investment loans where either -- The collateral is either located in a determined higher risk geographic location, or classified as a higher risk property type.- The borrower has four or more investment properties held under residential mortgage

by the Bank. Note: Subject to full credit assessment, other lending criteria may apply.

Important: Guide only -

8

Lending Parameters (Continued)

Maximum LVR

Owner Occupied

98% including LMI for purchases, andconstruction loans with genuine savings.Note: Location restrictions apply

90% + LMI capitalisation for purchase, refinance, purchase of vacant land, and construction loans with non-genuine savings. Note: Location restrictions apply.

80% maximum for interest only loans

Note: LVR > 80% all Owner Occupied loans to be P&I.

Investment

80% maximum no LMI (criteria applies)

90% maximum LVR inclusive of LMI capitalisation (criteria applies)

Note: Maximum LVR for all Investment loans is 90%.

All lending:

• Where LVR is > 90% the NMS (Net Monthly Surplus) required is $200

• If an application includes both interest only and principal and interest loans, the LVR restrictions detailed above will apply where more than 30% of the overall borrowings are interest only

• All housing loans above base LVR 90% must be secured by properties situated in VMA

Important: Guide only -

9

Supporting Documentation Requirements Key Points

Mandatory Requirement

• Provide detailed application notes. Include details of loan & security structure and exist strategy for owner occupied where any applicant is 45 years or older.

• Verification of living expenses. • The latest loan statement for all continuing loans, personal loans or debt and lease/hire

purchase.

Purchases

Contract of Sale:• Fully executed COS (all states except NSW)•

contract and the special conditions.

Funds to complete:• Savings held in applicants name• Statutory Declaration where gift obtained confirming it is non refundable

5% Genuine Savings (LMI loans):• Where in the form of savings must be held for minimum of 3 months in borrower name/s• Where in form of equity (property/shares) must be held owned for at least 3 months

Refinances / Debt Consolidation

Home Loans & Personal Loans:• Most recent 6 months consecutive statements

Credit Cards:• Most recent 3 months consecutive statements

Note: statements can be no older than 3 consecutive months at the date of application

Equity Release / Cash Out

• Personal use <= $50k

• Investment purposes <= $100k

• Car / motor vehicle <= $100k

• Property purchase <= $250k

Note: Must provide detailed commentary on what the funds will be used for in the application submission notes

validation documents are required.

For detailed information on documentation requirements referto the Virgin Money Broker Lending Guide

10

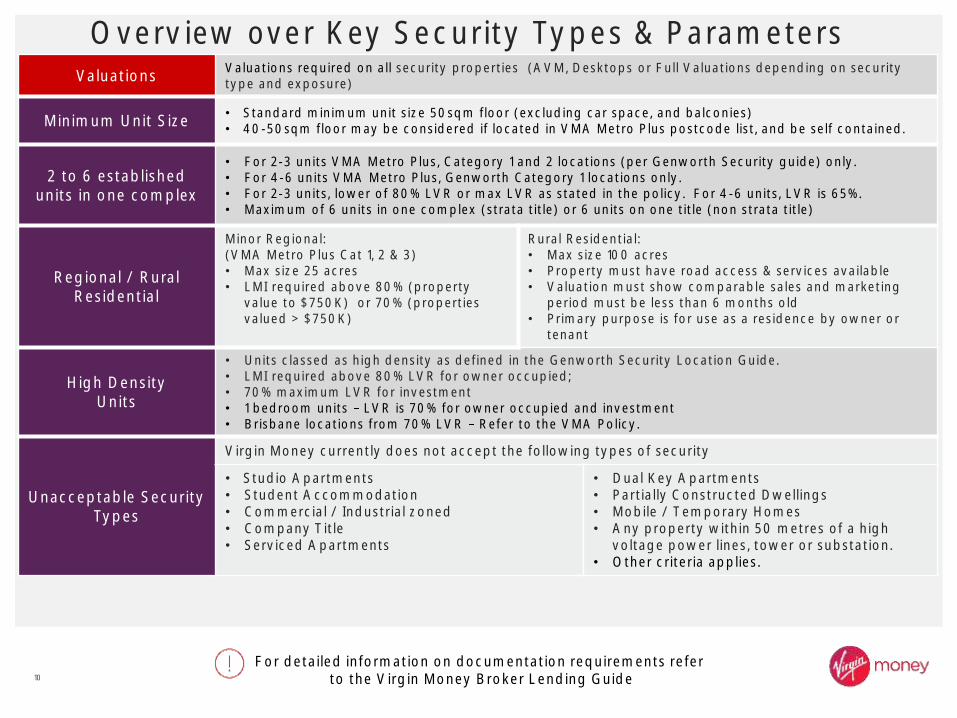

Overview over Key Security Types & ParametersValuations

Valuations required on all security properties (AVM, Desktops or Full Valuations depending on security type and exposure)

Minimum Unit Size• Standard minimum unit size 50sqm floor (excluding car space, and balconies)• 40-50sqm floor may be considered if located in VMA Metro Plus postcode list, and be self contained.

2 to 6 establishedunits in one complex

• For 2-3 units VMA Metro Plus, Category 1 and 2 locations (per Genworth Security guide) only. • For 4-6 units VMA Metro Plus, Genworth Category 1 locations only. • For 2-3 units, lower of 80% LVR or max LVR as stated in the policy. For 4-6 units, LVR is 65%.• Maximum of 6 units in one complex (strata title) or 6 units on one title (non strata title)

Regional / Rural Residential

Minor Regional: (VMA Metro Plus Cat 1, 2 & 3)• Max size 25 acres• LMI required above 80% (property

value to $750K) or 70% (properties valued > $750K)

Rural Residential:• Max size 100 acres• Property must have road access & services available• Valuation must show comparable sales and marketing

period must be less than 6 months old• Primary purpose is for use as a residence by owner or

tenant

High DensityUnits

• Units classed as high density as defined in the Genworth Security Location Guide. • LMI required above 80% LVR for owner occupied; • 70% maximum LVR for investment• 1 bedroom units LVR is 70% for owner occupied and investment• Brisbane locations from 70% LVR Refer to the VMA Policy.

Unacceptable Security Types

Virgin Money currently does not accept the following types of security

• Studio Apartments• Student Accommodation• Commercial / Industrial zoned• Company Title• Serviced Apartments

• Dual Key Apartments • Partially Constructed Dwellings• Mobile / Temporary Homes• Any property within 50 metres of a high

voltage power lines, tower or substation. • Other criteria applies.

For detailed information on documentation requirements referto the Virgin Money Broker Lending Guide

11

Guarantee Lending

Mandatory for all Guarantees

• Available for owner occupied purchases and investment purchases only • Refinancing of existing facilities with guarantor security is subject to review &

assessment• Limited to a specific dollar value• Independent legal and financial advise must be sought

Spousal Guarantee • Guarantor income available for servicing where guarantor is the spouse/partner of

the borrower• Full verification of income in line with validation policy

Family Guarantee

• Security Guarantee only• Guarantor must be an immediate family member (parent or sibling)• Application to be lodged as two separate loans:

1. Customers names utilising the property being purchased as sole security2. Customers & Guarantor utilising the purchase property & guarantor security with guarantee limited to loan amount of second application.

• Servicing - Applicants to demonstrate serving on total debtGuarantors to demonstrate servicing on limited guarantee amount plus their existing commitments

• First mortgage only no second mortgages

Fees• $10 per month per application and loan split• Additional Val fee & Security fee on second application

Important: Guide only -

full credit assessment criteria.

12

Construction Loans

Loan Purpose

• Construction of residential property• Purchase vacant land & construction of residential property (house & land package)• Property Improvements (including renovations)• Contracted Licensed builders only

Maximum LVR

• Maximum 98% including LMI capitalisation, Owner Occupied• Maximum 90% LVR inclusive of LMI where non-genuine savings exist, Investment• Vacant Land 90% LVR inclusive of LMI Note: Other lending criteria and maximum LVR criteria applies., refer to slide 7 & 8 above.

Documentation

• Fixed Price Builders Contract (signed & dated) - the schedule of payments in the contract must be in accordance with relevant state/territory laws and under standard contract terms by the Housing Industry Association or Master Builders Association

• Copy of council approved plans and building specifications• Copy of the builders registration./certification documentation• Copy of the builders Insurance policy with

constructed • Quotes of any work not included in the builders fixed price contract but may be needed for the

valuation e.g. Landscaping

Valuations

Valuations are required at the following stages:1. At initial stage prior to commencement of construction to confirm land value and construction

costings as if complete valuation2. At practical completion (Final Inspection Report) prior to the final loan drawdown3. Progress Inspection Reports will be required for:• Construction of Multiple Dwellings or;• A single residence where the total construction cost exceeds $1M

Progress Payments

• First drawdown must occur within six month from disclosure date.• Progress payments to be in line with State/Territory laws up to a maximum of 75% of the

contract paid up to lock-up stage (80% in WA)• Borrowers contribution to be fully used before the first progress payment• Final drawing must be within 18 months.

Important: Guide only -

full credit assessment criteria.

13

Self Employed Lending Applicants Individual borrowers only (no trust/company borrowers)

Self-Employed Term

Minimum 2 years self-employed

Income Validation

Self-employed income:• Individual - last 2 years personal & business tax returns and Tax Assessment Notices, no more

than 18 months old• Non Individual entities (including Partnerships) - last 2 years personal & business tax returns and

accountant prepared Profit & Loss and financial statements. • Tax status confirmed by Tax Portals and Integrated Client Account Portal for each self -

employed borrower and guarantor.• Must be registered for GST

Note: Applicants with Self-Employed and PAYG Income to provide Accountant confirmation to confirm self-employed entity trading and tax liabilities status.

Servicing Servicing is based on the lower of:

• Average net profit of last two years tax returns; or• Net profit from the most recent tax return

Validating Tax Status

Confirm the taxation status of the self-employed borrowers (personal and business) by either:• A written confirmation from the self-

individual borrower names and/or entity names, taxation year, and status; or• A copy of the business Income Tax Lodgement Status Portal and the Integrated Client Account

Portal; Income Tax Account Portal (companies only); or

• An Australian Tax Office receipt confirming the payment of an outstanding ATO notice.

Note:- Where taxation payments are in arrears, application must be referred to your BDM for full review and assessment. - Tax Assessment Notice / Notice of Assessment (NOA) must be no more than 18 months old.

Important: Guide only -

full credit assessment criteria.

14

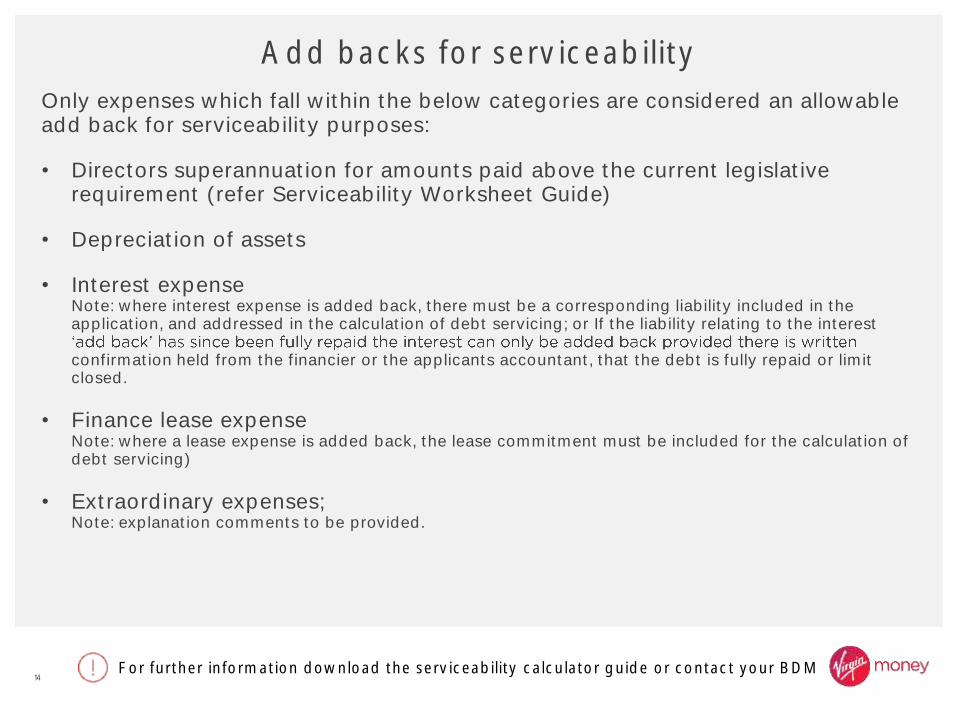

Only expenses which fall within the below categories are considered an allowable add back for serviceability purposes:

• Directors superannuation for amounts paid above the current legislative requirement (refer Serviceability Worksheet Guide)

• Depreciation of assets

• Interest expense Note: where interest expense is added back, there must be a corresponding liability included in the application, and addressed in the calculation of debt servicing; or If the liability relating to the interest

confirmation held from the financier or the applicants accountant, that the debt is fully repaid or limit closed.

• Finance lease expense Note: where a lease expense is added back, the lease commitment must be included for the calculation of debt servicing)

• Extraordinary expenses; Note: explanation comments to be provided.

Add backs for serviceability

For further information download the serviceability calculator guide or contact your BDM

15

Unacceptable add backs can include, but not limited to the following:

• Donations;

• Advertising expenses;

• Capital Losses;

• Bad and doubtful debts;

• Legal expenses;

• Start-up costs;

• Stock replacement or stock write offs;

• Business motor vehicle expenses;

• Club subscriptions / memberships;

Unacceptable Add backs for serviceability

For further information download the serviceability calculator guide or contact your BDM

16Income and Employment

17

Acceptable Primary Income Sources

PAYG Salary and Wages (full time, part time, casual or contract)

Full time or permanent part time• 100% of gross income.

2nd Part time• 80% of a 2nd part-time position with a minimum of 6 months continuous service.

Casual• 80% of gross income up to the equivalent full time job (40 hours per week) where the borrower

can demonstrate a minimum of 6 months continuous service with the same employer.

Employment contract100% of gross income is to be used when calculating serviceability where the borrower can demonstrate:• a minimum of 12 months continuous service with the same employer; and • a minimum of 2 years continuous services in the same occupation.•

Education or Private schools.

PAYG income validation• The most recent payslip being no older than 30 days prior to the application date• Where bank statements are used to validate PAYG income, the latest statement cannot be older

than 30 days prior to the application dateNote: Applicants with Self-Employed and PAYG Income to provide Accountant confirmation to confirm self-employed entity trading and tax liabilities status.

Rental Income

• 80% of gross rental income as validated.

• 70% gross rental commercial property, multiple units and high density units, excluding high density units in prescribed Brisbane locations and properties located in a Mining Town.

• 60% gross rental income for car park space, student accommodation and high density units in prescribed Brisbane locations.

• 50% of gross annual rental income, Serviced apartments/ Holiday rental/ Irregular short term rentals (i.e. Airbnb)

Important: Guide only -

18

Additional Sources of Income

Overtime, Shift allowance and Penalties

80% if the payment is a regular and ongoing condition

100% (essential service industry only) if the payment is a regular and ongoing condition

Note: Essential Services Industry being Ambulance, Police, Fire Service, Medical Doctors, Medical Nursing & Corrective Services

Commission 80% if the payment is a regular and ongoing condition

Permanent Government Pensions (i.e. Veteran Affairs, Disability or Old Age Pension)

100% of payments

Note: Single parent payments are not ongoing hence are not acceptable

Family Allowance (Family Tax Benefit Part A and Part B)

100% of payments where the child is less than 11 years old

Child Support 100% where the child is less than 13 years old

Important: Guide only -

discretion and full credit assessment criteria.

19

Additional Sources of Income

Car Allowance 100% of car allowance

Site Allowance 50% of site allowance, subject to:- and- has been earned over a minimum of two years consecutively.

Investment Income (Interest or dividends)

80% of gross income from the lower of the last 2 years tax returns

Bonus Income80% of the lowest bonus income earned in the last two yearsNote: It must be confirmed as a permanent ongoing condition of their employment and have been earned over a minimum of two years consecutively.

Maternity Leave

100% of Maternity Leave Payment up to 80% LVR, (Employer paid or Government paid working parent payment) subject to no payment gap more than 60 days from end of payment and resumption of employment income

Note: subject to Genworth policy of 50% of employer Maternity Leave Payment and government Paid Parental Leave Payment, refer to full underwriting guidelines.

ProbationaryEmployment

The borrower on probation is allowable if:

Probation is with the same company that the applicant has been continuously engaged with for a minimum of 12 months; or

Their prior employment in the same occupation is greater than 2 years and no more than 4 months break in employment. Prior employment will be confirmed by phone

Important: Guide only -

discretion and full credit assessment criteria.

20

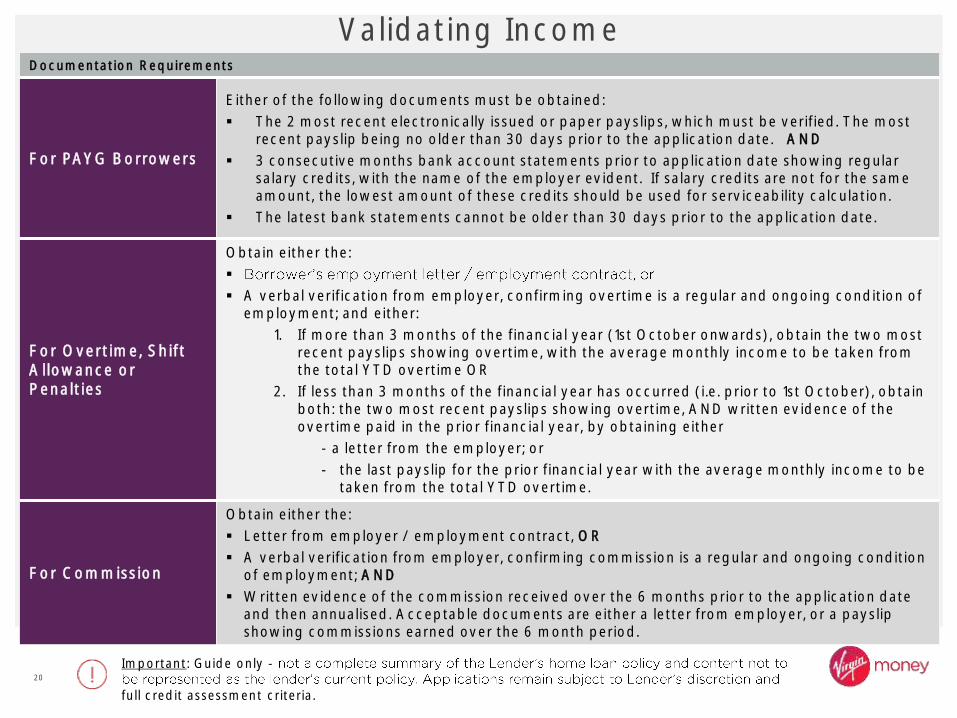

Validating IncomeDocumentation Requirements

For PAYG Borrowers

Either of the following documents must be obtained:

The 2 most recent electronically issued or paper payslips, which must be verified. The most recent payslip being no older than 30 days prior to the application date. AND

3 consecutive months bank account statements prior to application date showing regularsalary credits, with the name of the employer evident. If salary credits are not for the same amount, the lowest amount of these credits should be used for serviceability calculation.

The latest bank statements cannot be older than 30 days prior to the application date.

For Overtime, Shift Allowance or Penalties

Obtain either the:

A verbal verification from employer, confirming overtime is a regular and ongoing condition of employment; and either:

1. If more than 3 months of the financial year (1st October onwards), obtain the two most recent payslips showing overtime, with the average monthly income to be taken from the total YTD overtime OR

2. If less than 3 months of the financial year has occurred (i.e. prior to 1st October), obtain both: the two most recent payslips showing overtime, AND written evidence of the overtime paid in the prior financial year, by obtaining either

- a letter from the employer; or

- the last payslip for the prior financial year with the average monthly income to be taken from the total YTD overtime.

For Commission

Obtain either the:

Letter from employer / employment contract, OR

A verbal verification from employer, confirming commission is a regular and ongoing condition of employment; AND

Written evidence of the commission received over the 6 months prior to the application date and then annualised. Acceptable documents are either a letter from employer, or a payslip showing commissions earned over the 6 month period.

Important: Guide only -

full credit assessment criteria.

21

Documentation Requirements (Continued)

For Self Funded Retirees

Gross income as confirmed by last two annual funds statement (if confirmed as non taxable) or the last 2 years tax returns.

Superannuation and/or investment statements showing current balance.

Family Employment Where the borrower is employed by family or through a family owned or controlled business,

letters of employment or payslips must be supported by minimum last two pay deposits shown in bank statements.

For Maternity Leave Payment

Valid Signed and dated confirmation letter from the employer containing employer name; and ABN (except Government employer), employee name, salary amount and proposed return to work date.

For Self Managed Super Fund Retirees

Last 2 years tax returns with the most recent being no more than 18 months old; and Superannuation and/or investment statements showing the current balance

For Government Pensions

Statement of benefits (not more than 3 months old) issued by CentreLink; orthe Department of Veterans Affairs; or

3 months current bank statements confirming receipt of CentreLink payments.

For Family Allowance (Family Tax Benefit Part A & Part B)

CentreLink Statement of benefits (not more than 3 months old) must be provided by the customer; or

3 months current bank statements confirming receipt of CentreLink payments.Note: Rent Assistance that forms part of the Family Tax Benefit Part A is unacceptable income.

For Child SupportPayment

A copy of the Maintenance Agreement registered with the child support agency; and the 3 most recent months current bank account statements showing regular credits

For investmentIncome (Interest or dividends)

The 2 most recent tax returns no more than 18 months old; and A copy of current account statement or share certificate or CHESS statement.

Bonus Income Copy of letter of entitlement from employer or employment contract; and Letter from employer detailing the bonus amounts received over the past two years, supported

by either a tax return, PAYG payment summary, payslip, or bank statement credit entry.

Important: Guide only -

full credit assessment criteria.

22

Documentation Requirements (Continued)

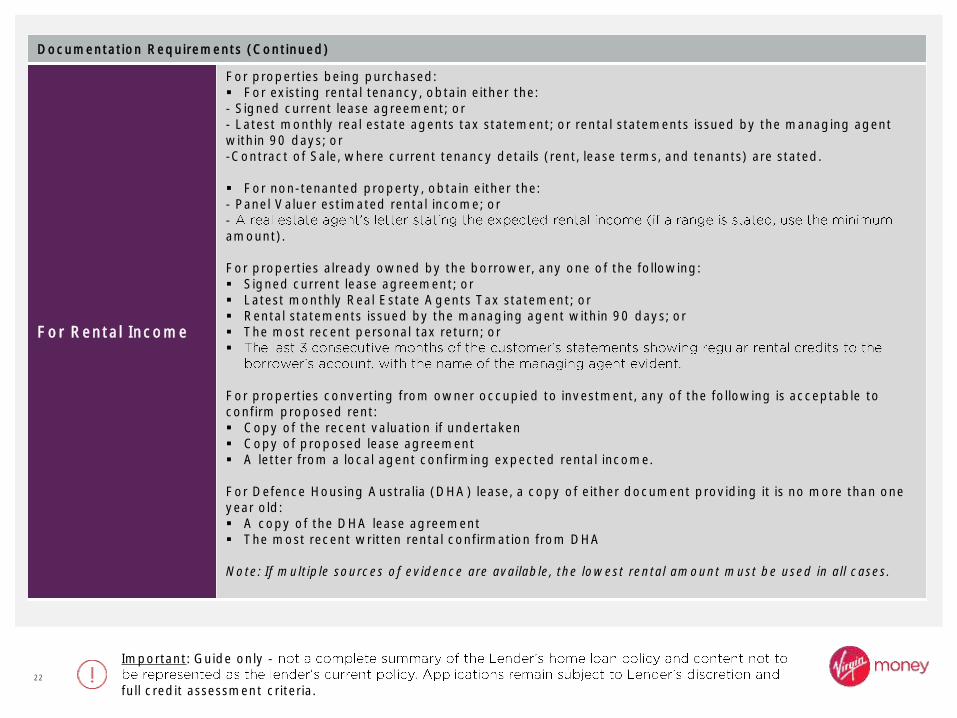

For Rental Income

For properties being purchased: For existing rental tenancy, obtain either the:- Signed current lease agreement; or- Latest monthly real estate agents tax statement; or rental statements issued by the managing agent within 90 days; or-Contract of Sale, where current tenancy details (rent, lease terms, and tenants) are stated.

For non-tenanted property, obtain either the: - Panel Valuer estimated rental income; or -amount).

For properties already owned by the borrower, any one of the following: Signed current lease agreement; or Latest monthly Real Estate Agents Tax statement; or Rental statements issued by the managing agent within 90 days; or The most recent personal tax return; or

For properties converting from owner occupied to investment, any of the following is acceptable to confirm proposed rent: Copy of the recent valuation if undertaken Copy of proposed lease agreement A letter from a local agent confirming expected rental income.

For Defence Housing Australia (DHA) lease, a copy of either document providing it is no more than one year old: A copy of the DHA lease agreement The most recent written rental confirmation from DHA

Note: If multiple sources of evidence are available, the lowest rental amount must be used in all cases.

Important: Guide only -

full credit assessment criteria.

23

Documentation Requirements (Continued)

Serviced Apartments/HolidayRentals

Any one of the following:

Tax return confirming the previous 12 months rental income; or Letter from Managing Agent outlining the expected annual rental income (for properties being

purchased only).

all of the following: the most recent lodged tax return (confirming the previous 12 months rental income) and the most recent Tax Assessment Notice; and the most recent airbnb statement showing receipt of rental within the last 120 days.

Note: The acceptable age of required documentation is in relation to the date of the application. Refer to slide 8 for the required

PAYG income document age.

Important: Guide only -

full credit assessment criteria.

24

Payslip Validation

PAYSLIPS MUST NOT BE HANDWRITTEN & CONTAIN AS A MINIMUM:

1. Borrower Name 2. Employer

Name

4. YTD income figure

3. Employer ABN

(except for Government

Bodies)

Important: Guide only -

full credit assessment criteria.

25

Unacceptable Income

Any form of income not listed in the above sections is considered unacceptable.

Examples of income sources that fall into this category are:

Seasonal income

Entertainment and travel allowances (including any meals, accommodation, offsite, or other such allowances)

Non-permanent allowances (e.g. Higher Duties)

Income from boarders (e.g. owner occupied property)

New start or unemployment benefits, workers compensation, sickness benefits

Any other government benefits or pensions that are not of a permanent nature i.e. single parent payments childcare benefits, or carers payments

Income of a Non-Recurring nature

Cash payments

Leave loading

Rent Assistance

Overseas/Foreign income.

Casuals with less than 6 months employment

Income from cryptocurrency sources

Important: Guide only -

full credit assessment criteria.

Unacceptable Income

26Documentation

27

Supporting Documentation Requirements Key Points

Mandatory Requirement

• Provide detailed application notes. Include details of loan & security structure and exist strategy for owner occupied where any applicant is 45 years or older.

• Verification of living expenses. • The latest loan statement for all continuing loans, personal loans or debt and lease/hire

purchase.

Purchases

Contract of Sale:• Fully executed COS (all states except NSW)•

contract and the special conditions.

Funds to complete:• Savings held in applicants name• Statutory Declaration where gift obtained confirming it is non refundable

5% Genuine Savings (LMI loans):• Where in the form of savings must be held for minimum of 3 months in borrower name/s• Where in form of equity (property/shares) must be held owned for at least 3 months

Refinances / Debt Consolidation

Home Loans & Personal Loans:• Most recent 6 months consecutive statements

Credit Cards:• Most recent 3 months consecutive statements

Note: statements can be no older than 3 consecutive months at the date of application

Equity Release / Cash Out

commentary on what the funds will be used for must be detailed in the application file notes:

• Personal use <= $50k

• Investment purposes <= $100k

• Car / motor vehicle <= $100k

• Property purchase <= $250k

validation documents are required.

For detailed information on documentation requirements referto the Virgin Money Broker Lending Guide

28

Documentation RequirementsValidating Savings, Account Conduct and Expenses

Valid AccountStatements Requirements

Valid Account Statements. Account statements are used for a variety of validation purposes, including validation of identity, account conduct, savings history, income, living expenses, and employment.

Account statements must be either original documentation issued directly by the financial institution or electronically issued documents obtained via internet banking, or internet transaction listing and acceptable as detailed below:

Account statements or electronically issued statements are acceptable if they satisfy all the following requirements:

Display the logo of the bank or other financial institution;

Display the Borrowers name, full BSB and account number; and

Individual transactions are itemised and there is a running account balance.

Internet Transaction listings are acceptable if:

Either:-- Individual transactions are itemised and there is a running account balance. Or,

1. Obtain bank account statement(s) dated within the last 12 months prior to the application date;2. Match the account number on any internet transaction listing to the bank account statement/s provided; and 3. Individual transactions are itemised and there is a running account balanceOr1. Obtain 'Proof Of Account Balance Letter' from other Bank, showing logo and account details;2. Match the account number and account name, on the internet transaction listings to the account details on the 'Proof Of Account Balance Letter'; and 3. Individual transactions on the transaction listings are itemised and there is a running account balance.

Important: Guide only -

full credit assessment criteria.

29

Important: Guide only -

full credit assessment criteria.

Documentation Requirements

Refinancing External ExistingDebt

All Break Costs and Exit Fees;

6 consecutive months for Home Loans, Investment Loans, Personal Loans and Line of Credits;

3 consecutive months for Credit Cards (if paying out credit cards); and

Statements can be no more than three months old at the date of the application.

All statements must meet the Valid Account Statements requirements.

Validating Savings, Account Conduct and Expenses (Continued)

Transaction Account Statements

Most recent 3 months consecutive months of their main transaction account statements prior to the application confirming their transaction history living expenses, and salary credits where the salary and living expenses are transacted through.

Most recent 3 months consecutive bank account statements showing regular salary credits with the name of employer evident.

When a credit card is the only account used for transactions then three months credit card statements will be required.

Account statement/s to be no more than 30 days old at the date of application,

All statements must meet the Valid Account Statements requirements.

30

Validating Savings, Account Conduct and Expenses (Continued)

Genuine Savings

5% genuine equity if mortgage insurance is required;

The equity must be held in the name of at least 1 borrower and can include:

Funds held in a Bank Account or Term Deposit for 3 months or more;

Equity in residential property owned for at least 3 months; or

Shares held for at least 3 months.

be accepted subject to lending criteria.

Note: Rental Payment History cannot be utilised as the sole source of genuine savings .

Non-Genuine Savings

Where the customer cannot demonstrate genuine savings, such applications may be considered if the customer has non-genuine savings and the following is met:

The loan purpose must be for the purchase of a house or unit for owner occupation only;

The security property cannot exceed 2.2ha in area; and

Repayments must be on a principal and interest basis, with no interest only terms available.

The non-genuine savings contribution may consist of:

Gifts, Inheritance, sale of assets, tax refund (Validation must be provided)

Important: Guide only -

full credit assessment criteria.

Documentation Requirements

NB: Borrowers must hold sufficient funds to cover all relevant government fees, duties and charges. The use of borrowed funds from credit providers to pay relevant fees, duties and charges is not acceptable

31

Important: Guide only -

full credit assessment criteria.

Documentation Requirements

Validating Purchases and Funds to Complete

Contracts for Purchase

A fully executed and signed copy of the contract of sale must be obtained.

Note: For NSW a copy of the purchaser's signed contract must be obtained, together with a copy of the fully executed front page from the vendor's contract and the 'Special Conditions'. The details recorded on both copies must be identical.

Funds to Complete Property Purchases

Where the borrower is providing funds to complete a property purchase (in addition to the Bank's lending), the source of these funds must be validated.

The validation requirement is only where the customer contributes an amount above $5,000 to the total purchase.

Note: If the borrower has already paid a deposit for a property purchase prior to the lending application, the source of this does not need to be validated.

External Refinances

For external refinances that require LMI and where the LVR is >80% a current rates notice must be provided together with confirmation of rates being paid up to date.

Confirmation is via, receipt, bank or credit card statement, or letter from the local government authority.

32

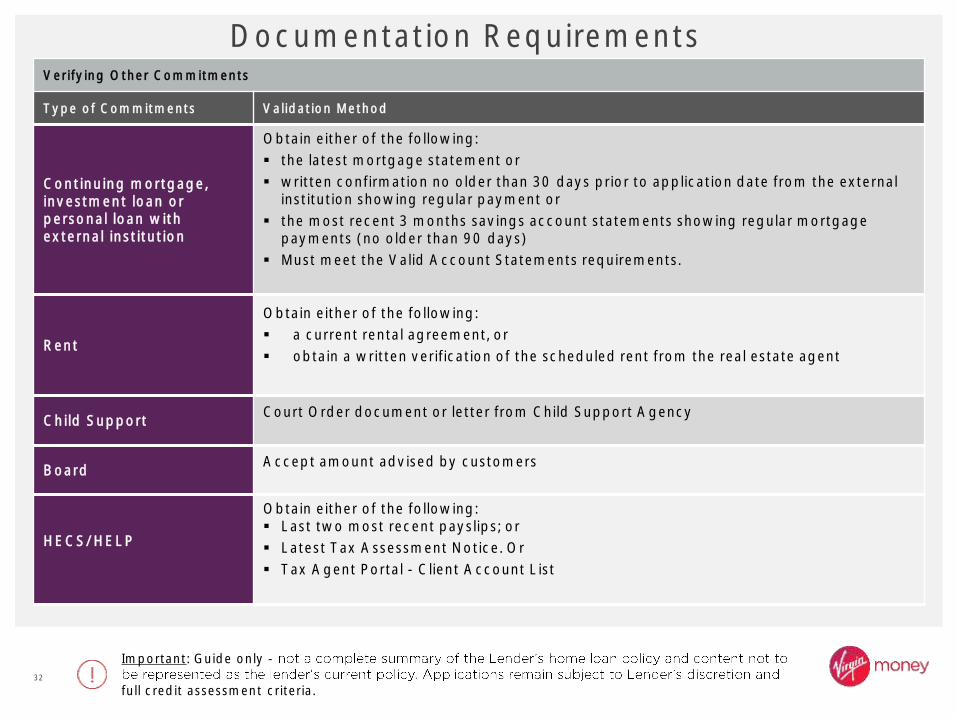

Verifying Other Commitments

Type of Commitments Validation Method

Continuing mortgage, investment loan or personal loan with external institution

Obtain either of the following:

the latest mortgage statement or

written confirmation no older than 30 days prior to application date from the external institution showing regular payment or

the most recent 3 months savings account statements showing regular mortgage payments (no older than 90 days)

Must meet the Valid Account Statements requirements.

Rent

Obtain either of the following:

a current rental agreement, or

obtain a written verification of the scheduled rent from the real estate agent

Child SupportCourt Order document or letter from Child Support Agency

BoardAccept amount advised by customers

HECS/HELP

Obtain either of the following: Last two most recent payslips; or

Latest Tax Assessment Notice. Or

Tax Agent Portal - Client Account List

Important: Guide only -

full credit assessment criteria.

Documentation Requirements

33

Verifying Other Commitments

Type of Commitments Validation Method

Other significant commitments advised by customer

Confirmation letter/invoice or confirm against the bank statements

Leases/Asset Finance: Obtain either of the following:Copy of current lease agreement; or Written confirmation via a statement, letter, or amortisation schedule issued by the Lease/Financer provider in the last 30 days confirming repayments; or Confirm against the last 30 day bank transaction statements.

Novated Leases: Obtain either of the following: A copy of the novated lease agreement; or

Remaining Credit Cards (not being refinanced)

Obtain either of the following:

• The latest credit card statement no older than 30 days prior to application date showing limit, or

• 'Proof of Account Balance Letter' showing other Bank logo, account name, account details, current and available credit card balance.

Body Corporate Levies/FeesOwner Occupied and Investment property expenses. Existing and new properties being purchased

Obtain either of the following:

Copy of latest issued Body Corporate "Notice of Contributions" or similar tax invoice showing levies payable, or

Body Corporate minutes (written) received from independent property managers, or

Contract of Sale (for newly acquired units/townhouses) showing levies payable.

Important: Guide only -

full credit assessment criteria.

Documentation Requirements

34Security

35

SecurityLocation Additional Criteria Property Value

Max LVR without LMI

VMA Metro Plus Postcode list

HousesUp to $3,000,000 80%

>$3,000,000 70%

Units & TownhousesUp to $2,000,000 80%

>$2,000,000 70%

Genworth Security Location Guide:- Category 1 postcode - State/Territory Capital cities only

Houses Up to $3,000,000 80%

>$3,000,000 70%

Units & Townhouses

Up to $1,500,000 80%

>$1,500,000 70%

Genworth Security Location Guide: - Category 1 postcode - Gold Coast Region only

Houses Up to $2,000,000 80%

>$2,000,000 70%

Units & Town housesUp to $1,500,000 80%

>$1,500,000 70%

Important: Guide only -

full credit assessment criteria.

Genworth Security Location Guide:- Category 1 postcode - Regional centres

Houses, Units & Townhouses

Up to $1,500,000 80%

>$1,500,000 70%

Genworth Security Location Guide: - Category 2 postcode - Regional centres

Houses, Units & Townhouses

Up to $750,000 80%

>$750,000 70%

36

Security (Continued)

Location Additional Criteria Property Value Max LVR without LMI

Category 3 postcode: - Regional centres

Houses, Units & TownhousesUp to $750,000 80%

>$750,000 70%

All other postcodes: - Properties in postcodes that are not included in the Genworth Security Location Guide

Houses, Units & Townhouses

Up to $750,000 70%

>$750,000 60%

Rural zoned properties:- VMA Metro Plus - Category 1, 2 & 3

Houses / Dwellings

Up to $750,000 80%

>$750,000 70%

All other postcodes: - Properties in postcodes that are not included in the Genworth Security Location Guide

Houses / Dwellings

Up to $750,000 80%

>$750,000 60%

Important: Guide only -

full credit assessment criteria.

37

Security (Continued)

Security Additional Criteria Property Value Max LVR without LMI

High Density Apartments:Unit is located within

LMI company

Refer to Genworth Security Location Guide.

Full Valuation required to confirm property value

80% Owner Occupied lending

70% Investment lending

High Density Apartments: Units located within Brisbane location

Postcodes: 4000-4006, 4007, 4009-4010, 4032, 4101-4102 & 4169

Full Valuation required to confirm property value

70% LVR without LMI for 1 bedroom apartments

80% without LMI for 2 bedroom apartments

70% Investment lending

1 Bedroom apartments in High Density postcodes

owner occupied and investment properties within the

Full Valuation required to confirm property value

70% without LMI.

Apartment / Unit - Greater than 40 square metres AND less than 50 square metres

Apartment / Unit must be located in a postcode within the

Full Valuation required to confirm property value

80% Owner occupied70% Investment lending

Important: Guide only -

full credit assessment criteria.

38

Security (Continued)

Important: Guide only -

full credit assessment criteria.

Facility Additional Criteria Property Value Max LVR without LMI

Refinanced Owner Occupied Loans

Residential property onlyValuation required to confirm property value

80% without LMI(90% with LMI)

Investment Loans Residential Property onlyValuation required to confirm property. value

80% without LMI 90% includes capitalisation of LMI

39

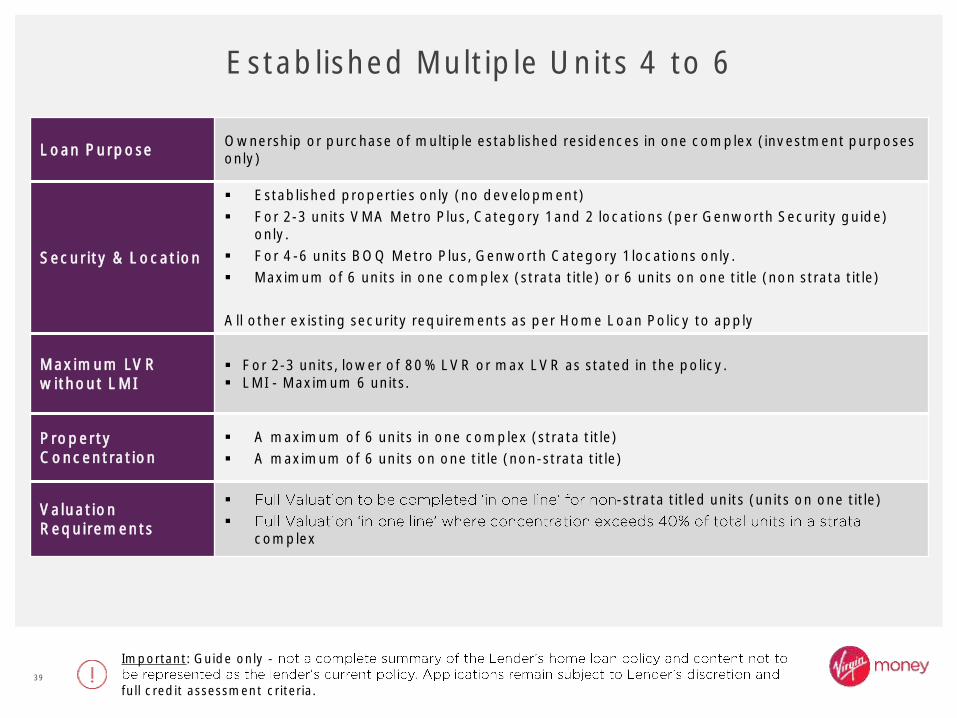

Established Multiple Units 4 to 6

Loan PurposeOwnership or purchase of multiple established residences in one complex (investment purposes only)

Security & Location

Established properties only (no development)

For 2-3 units VMA Metro Plus, Category 1 and 2 locations (per Genworth Security guide) only.

For 4-6 units BOQ Metro Plus, Genworth Category 1 locations only.

Maximum of 6 units in one complex (strata title) or 6 units on one title (non strata title)

All other existing security requirements as per Home Loan Policy to apply

Maximum LVR without LMI

For 2-3 units, lower of 80% LVR or max LVR as stated in the policy. LMI - Maximum 6 units.

Property Concentration

A maximum of 6 units in one complex (strata title)

A maximum of 6 units on one title (non-strata title)

Valuation Requirements

-strata titled units (units on one title)

complex

Important: Guide only -

full credit assessment criteria.

40

Security (Continued)

Notes in relation to security properties:

• Rural zoned vacant land is unacceptable security.

• Primary property purpose must always be as a residence, must be zoned for residential use; and used as a residence by the owner or by a tenant for residential purposes.

• Maximum property size is 40 hectares (100 acres).

• Property must be fully developed with road access and services available including electricity, water, (mains, bore and tank only) and sewerage.

• Income produced from the property must not be the primary source of income to service the debt.

• Excludes property on islands with the exception of islands connected to the mainland by vehicular bridge, (State of Tasmania excluded).

• Full valuation required showing sales evidence and the marketing period must be six months or less.

• Income produced from property must not be the primary source of income to service the debt.

Important: Guide only -

41

Property Valuations

Only one valuation may be ordered for each security property for any one credit application.

Valuation Requirements whentaking security EstablishedDwellings

VMA requires a Full Valuation no more than 3 months old for residential property if the application fits any one of the following criteria:

Total Aggregate Exposure for the Customer Group is $2m or more;

If the postcode of the property is in Category 2, 3 or not in the Genworth Security Location Guide.

Loan to Value Ratio (LVR) > 80%;

Security property is in a non-residential zone, i.e. Rural Residential >5 acres;

Purchase contract is not the result of a sale in the "normal course" with real estate agent involvement. E.g. related private sale;

Any postcode in the listing of prescribed "Mining Towns";

Residential units less than 50 square metres in size;

Purchase of Vacant Land

Other Criteria applies

General Requirements

VMA reserves the right to order a valuation at any time for any transaction.

Virgin Money utilises the following valuation types, AVM's, Desktops, or Full Valuation, subject to acceptable criteria such as property type and attributes, location, and application details.

Important: Guide only -

full credit assessment criteria.

42

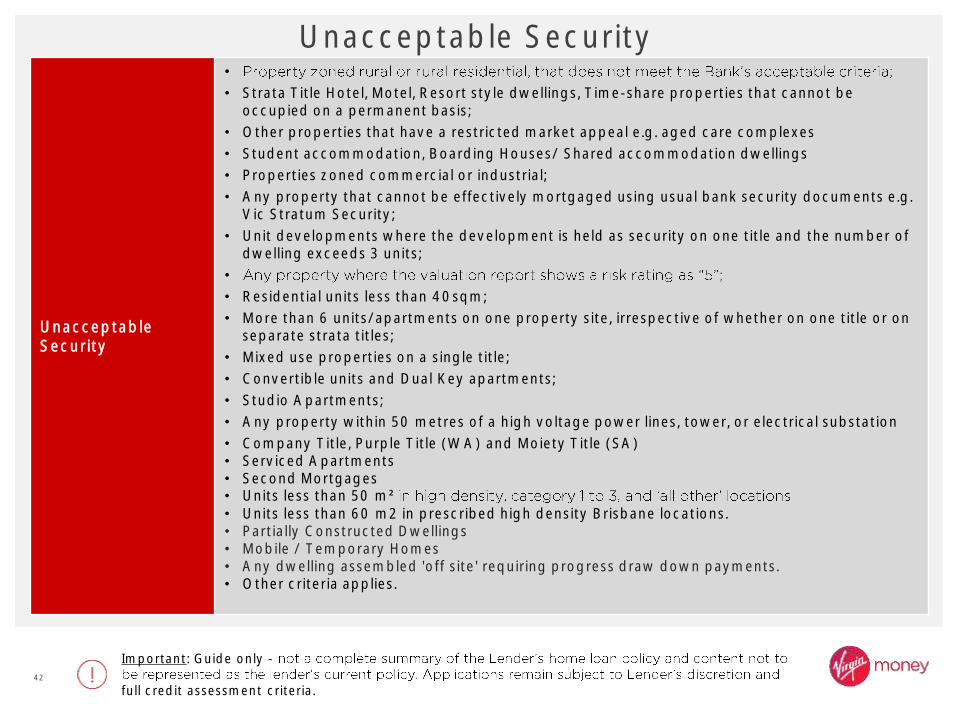

Unacceptable Security

UnacceptableSecurity

•

• Strata Title Hotel, Motel, Resort style dwellings, Time-share properties that cannot be occupied on a permanent basis;

• Other properties that have a restricted market appeal e.g. aged care complexes

• Student accommodation, Boarding Houses/ Shared accommodation dwellings

• Properties zoned commercial or industrial;

• Any property that cannot be effectively mortgaged using usual bank security documents e.g. Vic Stratum Security;

• Unit developments where the development is held as security on one title and the number of dwelling exceeds 3 units;

•

• Residential units less than 40sqm;

• More than 6 units/apartments on one property site, irrespective of whether on one title or on separate strata titles;

• Mixed use properties on a single title;

• Convertible units and Dual Key apartments;

• Studio Apartments;

• Any property within 50 metres of a high voltage power lines, tower, or electrical substation

• Company Title, Purple Title (WA) and Moiety Title (SA)• Serviced Apartments • Second Mortgages• Units less than 50 m²• Units less than 60 m2 in prescribed high density Brisbane locations.• Partially Constructed Dwellings• Mobile / Temporary Homes• Any dwelling assembled 'off site' requiring progress draw down payments.• Other criteria applies.

Important: Guide only -

full credit assessment criteria.

good bye

VIRGIN MONEY AUSTRALIA PTY LTD

Level 8, 126 Phillip Street, Sydney NSW 2000

T 02 8222 8000

virginmoney.com.au