Viet Nam Office -...

16

Savills Viet Nam Research Viet Nam Office 2018

Transcript of Viet Nam Office -...

Savills Viet NamResearch

Viet NamOffice 2018

UK,

Irela

nd & Channel Islands124Offices

Europe

117Offices

Middle East & Africa273Offices

Asia Pacific

70Offices

Americas & Caribbean64Offices

AmericasAsia

Pacific

Africa

Europe

35,000 employees across a network of over

600 offices in more than, 60 countries

We will be the real estate adviser of choice in the markets we serve. We do not wish to be the biggest, just the best (as judged

by our clients).

Our values capture our commitment not only to ethical, professional and responsible conduct but to the essence of real estate success, an entrepreneurial value-embracing approach.

GLOBAL NETWORK

2

SAVILLS VIET NAM

Over 22 yearsEstablished in Vietnam since

1995. The 1st International Property Firm in the Country

68,000 sqm leased in 2016

200 mil US$Total value

of residential sales in 2016.

Over 5.2 M sqm Under management in 2016 (over 36 buildings in HCMC and over 18 in Hanoi).

Our Research and Consultancy Services are the most innovative in Vietnam

Number one agency in volume of transactions with over USD 100M transacted each year.

CAMBODIA

DANANG

LAOS

MYANMAR HANOI

HCMC

UK,

Irela

nd & Channel Islands124Offices

Europe

117Offices

Middle East & Africa273Offices

Asia Pacific

70Offices

Americas & Caribbean64Offices

AmericasAsia

Pacific

Africa

Europe

35,000 employees across a network of over

600 offices in more than, 60 countries

We will be the real estate adviser of choice in the markets we serve. We do not wish to be the biggest, just the best (as judged

by our clients).

Our values capture our commitment not only to ethical, professional and responsible conduct but to the essence of real estate success, an entrepreneurial value-embracing approach.

GLOBAL NETWORK

Savills Viet Nam | 3

REGIONAL PERFORMANCE

10.2 9.78.6

97%80%

92%92% 96%

79%

23.5

35.229

48

30.836.5

5.51.61.6

BANGKOK HA NOI HCMC MANILAKL JAKARTA

Occupancy, 2017 Gross rent (US$/m²/mth), 2017Supply (million m²), 2017

PotentialViet Nam is <20% of regional peers.

KEY

4

REGIONAL PERFORMANCE

10.2 9.78.6

97%80%

92%92% 96%

79%

23.5

35.229

48

30.836.5

5.51.61.6

BANGKOK HA NOI HCMC MANILAKL JAKARTA

Occupancy, 2017 Gross rent (US$/m²/mth), 2017Supply (million m²), 2017

PotentialViet Nam is <20% of regional peers.

KEY

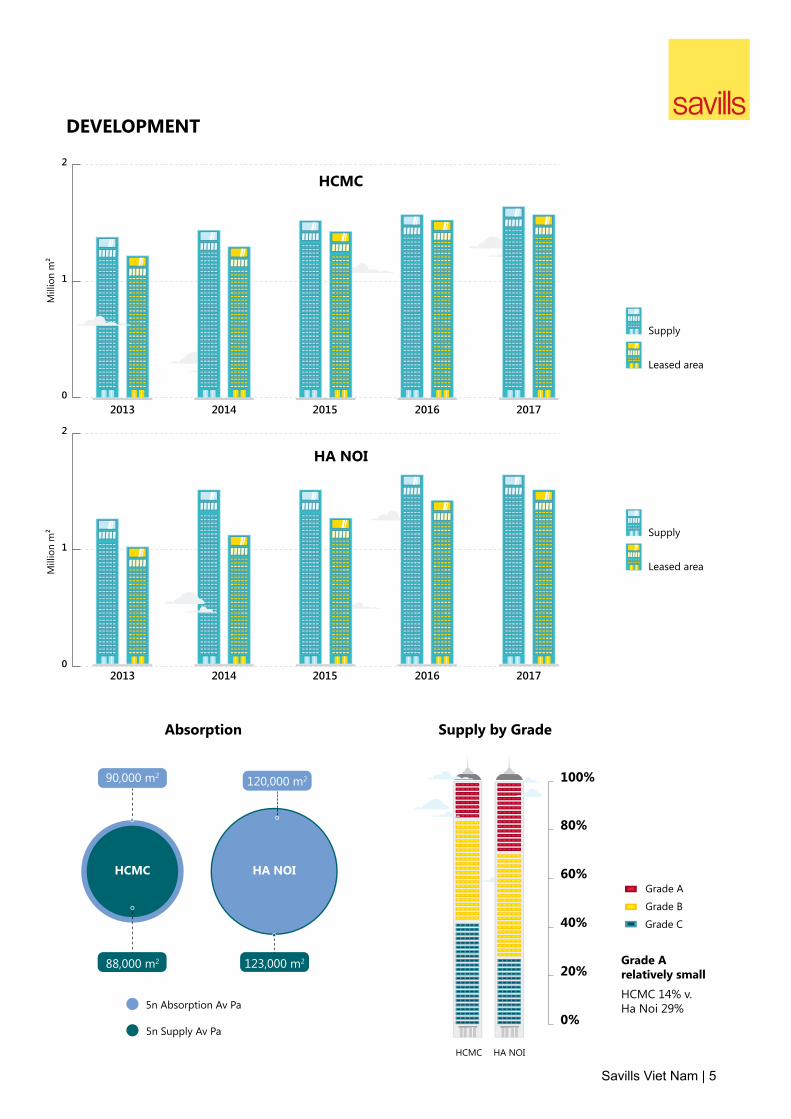

HCMC HA NOI

Grade Arelatively small HCMC 14% v.Ha Noi 29%

0%

20%

40%

60%

80%

100%

Mill

ion

m²

Mill

ion

m²

HCMC

HA NOI

Supply

Leased area

5n Absorption Av Pa

0

1

2

0

1

2

20162013

2015 2016 201720142013

Supply

Leased area

2014 2015 2017

5n Supply Av Pa

HCMC HA NOI

88,000 m2 123,000 m2

90,000 m2 120,000 m2

Grade A

Grade B

Grade C

Supply by GradeAbsorption

DEVELOPMENT

Savills Viet Nam | 5

5 Large Occupiers (>1,000 m²)

Grade A Whole Floor Availability

HCMC: CBD DEMAND

Manufacturing ICTF.I.R.E Consultancy Utilities

2015 2016

21 102017

1

42% 17% 9% 7% 6%

1 2 3 4 5

Leased Area

# Tenants

Averagedeal

Smaller(<500 m²)

Larger(>1,000 m²)

0% 20% 40% 60% 80% 100%

<500 m²

<500 m²

500-1,000 m²

500-1,000 m²

>1,000 m²

>1,000 m²

m²

leased area

of tenants but

leased area

of tenants

m²

6

5 Large Occupiers (>1,000 m²)

Grade A Whole Floor Availability

HCMC: CBD DEMAND

Manufacturing ICTF.I.R.E Consultancy Utilities

2015 2016

21 102017

1

42% 17% 9% 7% 6%

1 2 3 4 5

Leased Area

# Tenants

Averagedeal

Smaller(<500 m²)

Larger(>1,000 m²)

0% 20% 40% 60% 80% 100%

<500 m²

<500 m²

500-1,000 m²

500-1,000 m²

>1,000 m²

>1,000 m²

m²

leased area

of tenants but

leased area

of tenants

m²

Tenants by Industries

Two year take-up ~1,000 m²

2015

2017

31% 12% 9% 4%4% 6% 7% 4% 23%

Manufacturing

ICT

Consultancy

Utilities

Pharmacy &

Healthcare

Mining

Distribution

Others

F.I.R.E

31% 15% 11% 7% 6% 6% 5% 5% 14%

45 44

29 29

85

-5 -6

-17

F.I.R.E Manufacturing ICT Consultancy Utilities Pharmacy &Healthcare

Mining Distribution Others

HCMC: CBD DEMAND

(Thousand m²)

Savills Viet Nam | 7

Finance

Real Estate

Source: GSO

Source: Statistics Offices in Surveyed Countries

Regional F.I.R.E, 2016

Viet Nam F.I.R.E employment

DEMAND: F.I.R.E(Finance, Insurance, Real Estate)

Malaysia

Indonesia

Thailand

Philipines

Viet Nam

100

200

300

400

500

Q1/2017

Thou

sand

jobs

% to

tal e

mpl

oym

ent

F.I.R.E employment:

Q1/2012 Q1/2013 Q1/2014 Q1/2015 Q1/2016

60% in HCMC,Ha Noi

jobs

Philippines (1.7%),Thailand (2%),

Malaysia (3%)

If F.I.R.E employment

doubles in the next 5 years, CBD

demand to catch up?

m² pa

of total employment v.

Employment growth2012-2016

Finance & Insurance

% pa

% pa

Real Estate

0% 1% 2% 3% 4%

8

Source: Swiss Re Sigma 2017

Source: Savills Research & Consultancy;Various sources

DEMAND: BANKS

Insurance Premium Penetration, 2016DEMAND: INSURANCE

Malaysia

Thailand

Philipines

Viet Nam

Bank

s

In CBD prestige towers:

HCMCHa Noi

2015-2020 CAGR 25% paMoF sector development focus

Low penetrationPromising market

> 40 players. Increasing high-end demand

403020100

Local

Foreign

37

11

12

11

19

Indonesia

Philipines

Thailand

Malaysia

Viet Nam

% G

DP

0 1 2 3 4

Non-life

Life

12

24

20

Savills Viet Nam | 9

200

Thou

sand

peo

ple

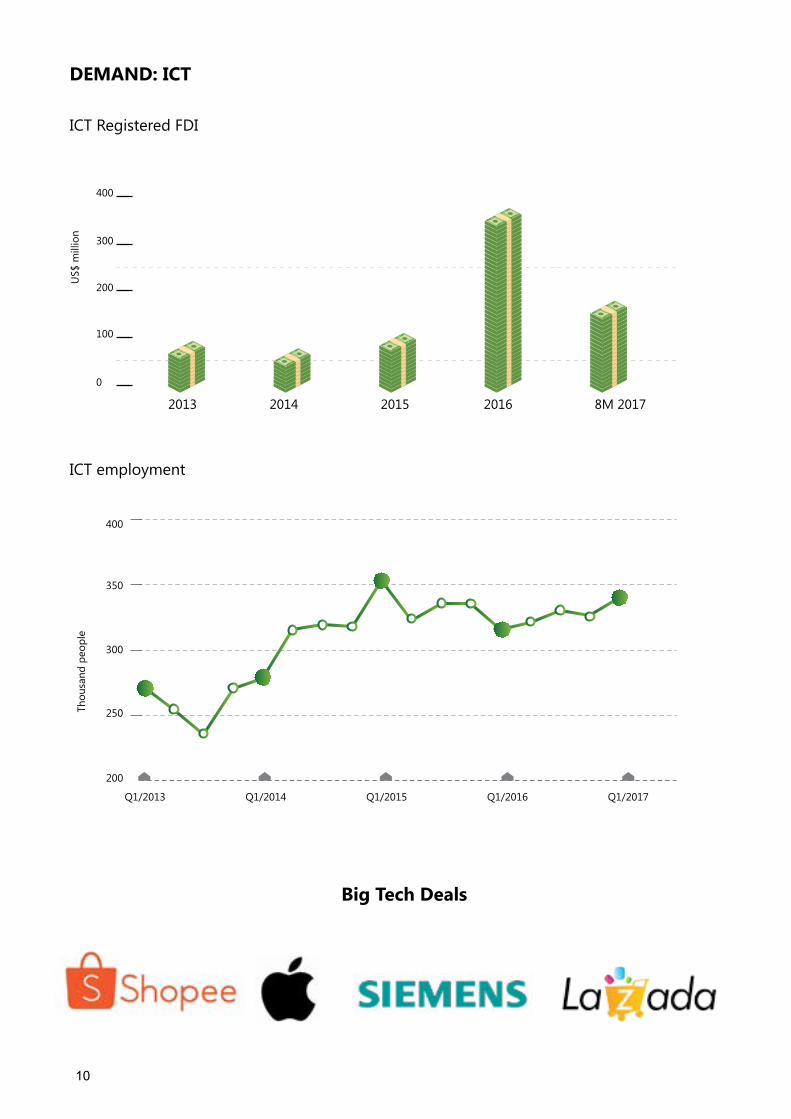

ICT Registered FDI

DEMAND: ICT

2013 2014 2015 2016 8M 2017

US$

mill

ion

ICT employment

250

300

350

400

Big Tech Deals

Q1/2013 Q1/2014 Q1/2015 Q1/2016 Q1/2017

0

100

200

300

400

New establishedbusinesses NEB

NEB registered capitalSource: GSO

20

0

60

80

100

120

thou

sand

bus

ines

ses

200

0

400

600

800

1,000

trillion VND

SMEs ~ 50% workforce

HCMC

Registered capital 85% YoY(National ~ $40B)

New enterprises13% YoY

Domestic

Services and Commerce

2013 201620152014

START UPS

10

New establishedbusinesses NEB

NEB registered capitalSource: GSO

20

0

60

80

100

120

thou

sand

bus

ines

ses

200

0

400

600

800

1,000

trillion VND

SMEs ~ 50% workforce

HCMC

Registered capital 85% YoY(National ~ $40B)

New enterprises13% YoY

Domestic

Services and Commerce

2013 201620152014

START UPS

Savills Viet Nam | 11

Source: Savills Research & Consultancy

A & B

Upcoming

HCMC: FORECAST

LimitedSupply

LowVacancy

RisingDemand

HCMC 3nrent forecast

pa

Onwards

Viettel Tower A

Saigon Centre P2

Deutsches Haus

E. Town Central

Viettel Tower B

M&C Tower

Lancaster NT

Nexus

Viet Capital

289 THD

Sun Project

SJC

BIDV Tower

Golden Hill

Spirit Of Saigon

SATRA TAX

Sabeco

Eximbank

201820192017

20202021

0.0

0.3

0.6

0.9

1.2

1.5

mill

ion

m2

0.0

10

20

30

40

50

US$/m

²/mth

2012 2013 2014 2015 2016 2017 2018f 2019f 2020f

Leased Area Vacant Area Avg. Rent

12

4 levels, $5B cost.9,000 trees, egalitarian.

$5B cost, 15n development.50,000 workers.

18m sodas pa.4 levels, no lifts. HUMANISTIC.Walk and talk. People, Place, Planet

The Avg. Number of Years at Tech Disruptors and Titans

0 0.5 1 1.5 2 2.5

Source: Paysa

10%

80% people

real estate

10%

tech

nolog

y

OFFICE TRENDS

And the reason corporates are so keen to make their offices attractives is:

Source: Savills Research & Consultancy

A & B

Upcoming

HCMC: FORECAST

LimitedSupply

LowVacancy

RisingDemand

HCMC 3nrent forecast

pa

Onwards

Viettel Tower A

Saigon Centre P2

Deutsches Haus

E. Town Central

Viettel Tower B

M&C Tower

Lancaster NT

Nexus

Viet Capital

289 THD

Sun Project

SJC

BIDV Tower

Golden Hill

Spirit Of Saigon

SATRA TAX

Sabeco

Eximbank

201820192017

20202021

0.0

0.3

0.6

0.9

1.2

1.5

mill

ion

m2

0.0

10

20

30

40

50

US$/m

²/mth

2012 2013 2014 2015 2016 2017 2018f 2019f 2020f

Leased Area Vacant Area Avg. Rent

Savills Viet Nam | 13

14

Impacts T H E F U T U R E O F G L O B A L R E A L E S TAT E

Social changeHow new generations are changing the demand for real-estate developments

New technologyThe digital influence on properties, their uses, and the cities we live in

Natural forcesWhy the physical world still has an intimate relationship to land values

Economic trendsHow changes in the world economy will impact the future of real estate

Risk and opportunityin global real estateSavills Global has recently published ‘Impacts: the future of global real estate’ a special publication to mark 10 years after the GFC. Based on the research results in the publication, Savills Vietnam will release a series of statements regarding trends shaping the real estate market in coming years.

To open the series is the statement on rent watch in world cities, where it could be found at HCMC ranked #3 worldwide as Cities most likely to see rental growth.

Read more at: http://sav.li/a2z

Savills.com/Impacts

Global Real Estate 20182 Impacts

savills.com

10 things you need to know about global debt The wealth of ages Abundance and scarcity The fifth age of the city Rates and yields The rise of the NORC Resilient cities How rich was Mr Darcy?

Richard Florida creates a recipe for a better city Professor Carlo Ratti imagines how smart cities will adapt to human needs Linda Yueh discusses how investors should view property cycles Melissa Marsh on building design for the digital age Hank Dittmar champions mixed-use living Plus the real-estate challenges of 2018 and beyond

New technologyThe digital influence on properties, their uses, and the cities we live in

Social changeHow new generations are changing the demand for real-estate developments

Natural forcesWhy the physical world still has an intimate relationship to land values

Economic trendsHow changes in the world economy will impact the future of real estate

Impacts

savills.com

T H E F U T U R E O F G L O B A L R E A L E S TAT E

Issue 01. 2018

Impacts 2018 T

he

futu

re o

f glo

ba

l rea

l esta

te

Savills_Impacts_p1_Cover_v1.4.indd 2 13/11/2017 16:34

Savills Viet Nam | 15

Impacts T H E F U T U R E O F G L O B A L R E A L E S TAT E

Social changeHow new generations are changing the demand for real-estate developments

New technologyThe digital influence on properties, their uses, and the cities we live in

Natural forcesWhy the physical world still has an intimate relationship to land values

Economic trendsHow changes in the world economy will impact the future of real estate

Risk and opportunityin global real estateSavills Global has recently published ‘Impacts: the future of global real estate’ a special publication to mark 10 years after the GFC. Based on the research results in the publication, Savills Vietnam will release a series of statements regarding trends shaping the real estate market in coming years.

To open the series is the statement on rent watch in world cities, where it could be found at HCMC ranked #3 worldwide as Cities most likely to see rental growth.

Read more at: http://sav.li/a2z

Savills.com/Impacts

Global Real Estate 20182 Impacts

savills.com

10 things you need to know about global debt The wealth of ages Abundance and scarcity The fifth age of the city Rates and yields The rise of the NORC Resilient cities How rich was Mr Darcy?

Richard Florida creates a recipe for a better city Professor Carlo Ratti imagines how smart cities will adapt to human needs Linda Yueh discusses how investors should view property cycles Melissa Marsh on building design for the digital age Hank Dittmar champions mixed-use living Plus the real-estate challenges of 2018 and beyond

New technologyThe digital influence on properties, their uses, and the cities we live in

Social changeHow new generations are changing the demand for real-estate developments

Natural forcesWhy the physical world still has an intimate relationship to land values

Economic trendsHow changes in the world economy will impact the future of real estate

Impacts

savills.com

T H E F U T U R E O F G L O B A L R E A L E S TAT E

Issue 01. 2018

Impacts 2018 T

he

futu

re o

f glo

ba

l rea

l esta

te

Savills_Impacts_p1_Cover_v1.4.indd 2 13/11/2017 16:34

16

OUR SERVICES

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

Troy GriffithsDeputy Managing Director

+84 (0) 933 276 [email protected]

Do Thu HangAssociate Director Research Savills Ha Noi

+84 (0) 912 000 [email protected]

Please contact us for further information:

Disclaimer:

Our services are delivered by people who combine entrepreneurial spirit and a deep understanding of specialist property sectors with the highest standards of client care. We help our clients to fulfil their real estate needs – whatever and wherever they are.

ADVISORYSERVICES

Feasibility Studies

Highest and Best Use Study

ValuationConceptual Development Recommendations

Market Research General & Specific

Economic and Demographic studies

AGENCY

Retail Marketing, Agency

OfficeMarketing, Agency and Tenant Services

PROPERTYMANAGEMENTProperty & Asset Management

Pre-Operations Management Consultancy Facility Management

Shopping Centre Management

Property Management Training

HOTEL & LEISUREServiced Apartment Management

Hospitality Research and ConsultancyHotel Investment Brokerage

INVESTMENTStakeholder Engagement Structuring

Strategy Project PositioningAcquisitions and Sales

RESIDENTIALResidential Leasing

Residential Sales Project Sales and Marketing Strategy

International Sales

Development Review

![Viet Cong Fighter - Osprey Warrior 116 - [Vietnam - Nam - Uniforms]](https://static.fdocuments.net/doc/165x107/577cc0f11a28aba71191b085/viet-cong-fighter-osprey-warrior-116-vietnam-nam-uniforms.jpg)