Veritas DGC Inc. Investor Presentation - April 2004.

27

Veritas DGC Inc. Investor Presentation - April 2004

-

Upload

dortha-kelly -

Category

Documents

-

view

221 -

download

0

Transcript of Veritas DGC Inc. Investor Presentation - April 2004.

Veritas DGC Inc.

Investor Presentation - April 2004

2

This presentation contains forward-looking information and

statements within the meaning of the Private Securities Litigation

Act of 1995 concerning among other things, Veritas DGC Inc.'s

prospects and development for its operations all of which are

subject to certain risks, uncertainties and assumptions, including

among other things, changes in market conditions in the oil and gas

industry, prices of crude oil and natural gas, weather conditions,

and the Company's ability to finalize contractual arrangements.

Should one or more of these risks or uncertainties materialize, or

should the assumptions prove incorrect, actual results could vary

materially from those anticipated.

Forward-Looking Information

3

DataLibrary

Land SeismicAcquisition

DataProcessing

Veritas - A Global Provider of Integrated Geophysical Services,

Geophysical Information & Reservoir Solutions

4

Veritas – Company Strategy

Invest in people, technology and operational excellence

Focus on select geographic markets

Manage for free cash flow

Continue to invest in: R&D, Multi-Client data library and differentiating technology

Maintain financial flexibility

Continue to be a leading provider of sub surface information to the global oil and gas industry while

maximizing earnings and cash flow

5

Market Outlook

Flat to slightly improving operating environment

Contract business increasing as a percent of total market

Pricing concerns continue in segments of the contract market

Customer consolidation has slowed

Lower multi-client spending however library shelf sales continue to drive cash flow and profits

More alliance and relationship work being performed

Increasing interest in high margin products and services advanced data processing multi-component data 4D surveys

6

Revenue Mix

FY 2003 First half 2004

11%

29%

33%

27%

12%

24%

37%

27%

Contract Marine Contract Land MC Land MC Marine

$503 $252

($ millions)

Geophysical Acquisition, Data Processing & Reservoir The “Services Business”

8

Our Marine Business

Five 3D vessels, three Viking class, all multi streamer, all chartered

One 2D vessel

Solid streamers deployed on Vantage, Viking 1, Searcher and Viking 2

Focus has shifted to a mix of contract and data library work

Solid Streamers are seen as a major differentiator by many customers for contract work awards

9

Marine Acquisition

CanadaCanada

Gulf of MexicoGulf of Mexico TrinidadTrinidad

BrazilBrazil

North SeaNorth Sea

W. AfricaW. AfricaAsia PacificIndia

10

Our Land Business

Invested in light weight and arctic-specific equipment and standardized on Sercel recording equipment

Developed multi-component recording and processing capabilities

Maintained a high volume of alliance and relationship work

11

Land Acquisition Markets

Alaska Alaska CanadaCanada

USUS

South AmericaSouth America

OmanOman

12

Our Data Processing Business

An order of magnitude improvement in compute price performance

Software and algorithm innovation results in incremental gains in past year

Recent installation of latest 64 bit AMD OPTERON CPU’s

Veritas is an industry leader in sub-surface imaging technology

Multi-Client Data Library“The information business”

14

Multi-Client Business Drivers

Geologic and hydrocarbon prospectivity

Efficient data collection and processing with un-compromised quality and turnaround

Conservative capitalization policy, amortization rates and margin assumptions

Areas with small blocks driven by government licensing rounds

Location, Location, Location

The value of Multi-Client is created by :

15

Key Multi-Client Markets and Assets

CanadaCanadaFoothills 3DFoothills 3DScotia Shelf 3DScotia Shelf 3D

USUSOnshore 3DOnshore 3DGulf of Mexico 3DGulf of Mexico 3D

South AmericaSouth AmericaBrazil 2D & 3DBrazil 2D & 3D

EuropeEuropeUK 2D & 3DUK 2D & 3DNorway 3DNorway 3DFaeroes 2D & 3DFaeroes 2D & 3D

AfricaAfricaNigeria 3DNigeria 3D Asia PacificAsia Pacific

Australia 2DAustralia 2DIndonesia 2DIndonesia 2D

16

Multi-Client Data as of January 31, 2004

189,000 sq km 3D

201,000 km 2D

Book value $348 million

Gross investment $1.3 billion

Life-to-date sales $1.6 billion

Total life-to-date booked margin 40%

Conservative library accounting

17

Multi-Client Revenue

28%

27%

26%

12%

7% 15%

41%24%

13%

7%

Brazil Gulf of Mexico Land West Africa Other

($ millions)

$220 $123

FY 2003 First half 2004

18

Veritas Data Library in the GOM as of 01/31/04

GOM Investment: $500M Sales-to-date: $850M

19

Gulf Of Mexico Lease Expiration 2004-2007

Ref. Lexco Data Systems

20

Multi-Client Revenue Versus Investment

0

50

100

150

200

250

FY2000

FY2001

FY2002

FY2003

FYTD2004

MC Revenue

MC Investment(gross)

Difference

Financial Information

22

Current Capitalization($ in millions)

Cash and cash equivalents $70

Long-term debt Revolving credit facility $0 Term Loan A 27 Term Loan B 114 Term Loan C 40 Total long-term debt 181

Shareholders' equity 485

Total capitalization $666

Debt / total capitalization 27%Net debt / total capitalization 17%

23

Capital Spending

0

10

20

30

40

50

60

70

80

90

100

Other

Processing

Marine

Land

2000 2001 2002 2003 2004 YTD

$ M

illi

on 55

9689

31

14

24

Cash Investments

-100

-50

0

50

100

150

200

250

300Cash Flow fromOperations

Capex

MC Investment(net cash)

Net

2000 2001 2002 2003 2004 YTD

$ m

illio

ns

25

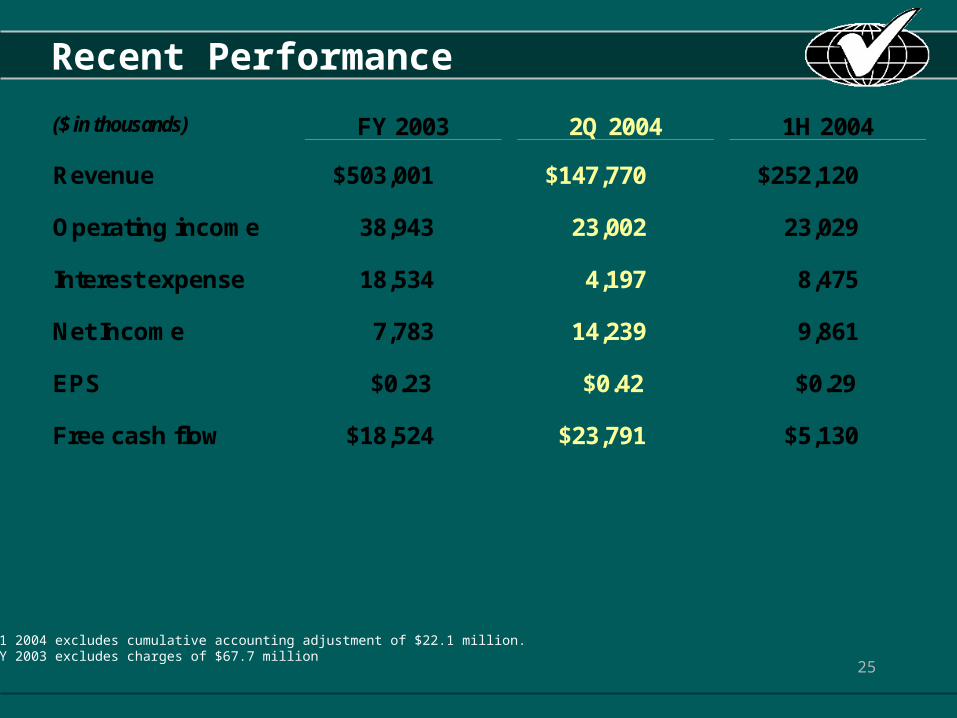

Recent Performance

Note: Q1 2004 excludes cumulative accounting adjustment of $22.1 million.FY 2003 excludes charges of $67.7 million

($ in thousands) FY 2003 2Q 2004 1H 2004 Revenue $503,001 $147,770 $252,120

Operating income 38,943 23,002 23,029

Interest expense 18,534 4,197 8,475

Net Income 7,783 14,239 9,861

EPS $0.23 $0.42 $0.29

Free cash flow $18,524 $23,791 $5,130

26

Why Veritas?

First class technology people and assets

Operating in politically stable areas

Data library sales continue to generate profits

Managed for positive cash flow

Low leverage

A company well positioned for the future

Veritas DGC Inc.

Investor Presentation - April 2004