Veni, Vidi, Vici - Iowa Actuaries Club Vidi, Vici February 14, 2016 Act The power to decide Actuaa l...

35

Principle-Based Reserves Veni, Vidi, Vici www.pwc.com February 14, 2016 Act The power to decide Actuarial Services

Transcript of Veni, Vidi, Vici - Iowa Actuaries Club Vidi, Vici February 14, 2016 Act The power to decide Actuaa l...

Principle-Based ReservesVeni, Vidi, Vici

www.pwc.com

February 14, 2016

ActThe power to decide

Actuarial Services

PwC 2PwC

Principle-Based ReservesAgenda

• PBR Summary and Timeline

• Where to start

• Implementation aspects

- Exclusion tests and grouping

- Net premium, deterministic and stochastic reserves

- Assumptions

- PBR actuarial report

- Governance

- Tax reserves

• Company Initiatives

2

PwC 3PwC

Principle-Based Reserving (PBR)A fundamental change in statutory reserves

• VM-20 Reserve Concepts

- Reserve calculation will be based on own company experience

- Method based on principles and guidance (not formulaic)

- Margins added to each assumption for conservatism

• Requires a significant amount of effort

- PBR reserve is the greatest of a net premium reserve, deterministic reserve and stochastic reserve

- Current valuation systems may not be easily adapted to PBR

- Extensive reporting and documentation requirements

• As of June 30th, forty-five states1 have adopted PBR legislation (Models 808 and 820) representing 79.5% of gross premium – NY has indicated a 2018 adoption

• January 1, 2017 will be the effective date

3

Excludes territories

PwC 4

PBR: How VM is being implemented

Revised Standard Valuation Law* references the

NAIC valuation manual

* Enacted by state legislation

Valuation ManualValuation ManualVM-01 – Definition of TermsVM-01 – Definition of Terms

VM-02 – Minimum NF Mortality & InterestVM-02 – Minimum NF Mortality & Interest

VM-05 – NAIC Model Standard Valuation LawVM-05 – NAIC Model Standard Valuation Law

VM-20 – Requirements of PBR for Life ProductsVM-20 – Requirements of PBR for Life Products

VM-21 – Requirements for PBR for VAVM-21 – Requirements for PBR for VA

VM-22 – Requirements for PBR for non-VAVM-22 – Requirements for PBR for non-VA

VM-25 – Health Insurance Reserves – Minimum RequirementsVM-25 – Health Insurance Reserves – Minimum Requirements

VM-26 – Credit Life & Disability Reserves RequirementsVM-26 – Credit Life & Disability Reserves Requirements

VM-30 – AOM RequirementsVM-30 – AOM Requirements

VM-31 – PBR Report Requirements for Business subject to PBRVM-31 – PBR Report Requirements for Business subject to PBR

VM-50 – Experience Reporting RequirementsVM-50 – Experience Reporting Requirements

VM-51 – Experience Reporting FormatsVM-51 – Experience Reporting Formats

VM-M – Appendix M Mortality TablesVM-M – Appendix M Mortality Tables

VM-A – Appendix A RequirementsVM-A – Appendix A Requirements

VM-C – Appendix C Actuarial GuidelinesVM-C – Appendix C Actuarial Guidelines

VM-G – Appendix G Corporate Governance Requirements for PBRVM-G – Appendix G Corporate Governance Requirements for PBR

Update

d b

y N

AIC

Adoption

PwC

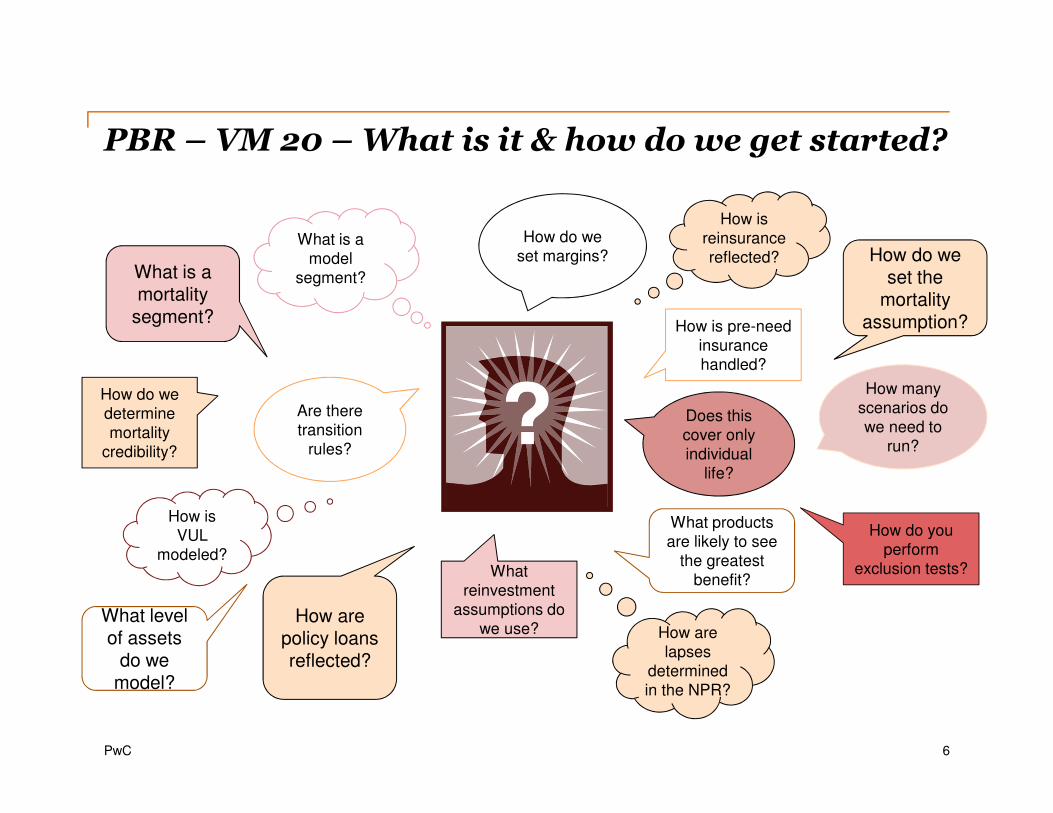

Where do I start?

5

PwC 6

PBR – VM 20 – What is it & how do we get started?

What is a mortality

segment?

How do we set margins?

How is VUL

modeled?

How is pre-need insurance handled?

What products are likely to see

the greatest benefit?

Does this cover only individual

life?

How are lapses

determined in the NPR?

How do we determine mortality

credibility?

How do we set the

mortality assumption?

Are there transition

rules?

What is a model

segment?

How do you perform

exclusion tests?

How are policy loans reflected?

How many scenarios do we need to

run?

How is

reinsurance reflected?

What reinvestment

assumptions do we use?

What level of assets

do we model?

PwC 7PwC

Valuation SystemsValuation system selection has been a particular discussion point

amongst clients

NPR

• Need to model NPR/CRVM at a seriatim level

Deterministic

• ALM model with some element of iteration to solve for starting assets

• Needs to be able to capture exclusion test

Stochastic

• ALM model needs to support stochastic modeling in an efficient manner

• Needs to capture exclusion test

Assets

• Model needs to model the assets you are holding

• Also need to model reinvestment assumptions

7

PwC 8PwC

VM-20 ValuationsCertain Implementation Considerations

VM-20 Areas of

Focus

VM-20 Reserve

Grouping

PBR Actuarial Report/

Governance

Tax Reserves

8

7

1

2

3

4

Net Premium Reserve

Stochastic ReserveDeterministic

Reserve

Mortality Assumption

5

6

Exclusion

Tests

PwC 9PwC

VM-20 Reserve Groups

VM-20 Reserve

Grouping

1

2

Exclusion

Tests

9

PwC 10

Minimum Reserve Under PBRDetermined by comparing reserves computed under 3 basesCould Hold Max[NPR, DR + DPA, SR + DPA]

• Minimum reserve

• Prescribed assumptions

• Seriatim

• Cash value floor

• Calculate if fail deterministic or stochastic exclusion tests or ULSG or employ clearly defined hedging strategy

• Gross premium reserve

• Mix of best estimate and prescribed assumptions

• Determined in aggregate under single scenario

• Discount rate = path of net asset earned rates for model segment

• Calculate if fail stochastic exclusion test or employ clearly defined hedging strategy

• Greatest present value of accumulated deficiency

• Mix of best estimate and prescribed assumptions, including dynamic policyholder behavior

• Determined in aggregate, multiple scenarios

• Discount rate is prescribed = 105% of 1-year Treasury rate

• Equals average of highest 30% of resulting reserves (CTE 70)

Net Premium Reserve (NPR)

Stochastic Reserve (SR)

Deterministic Reserve (DR)

DPA = Due & Deferred Premium Asset

PwC 11PwC

Reserve = max (NPR, DR+DPA,

SR+DPA)

Does the product have a clearly defined hedging

strategy?

Does the company choose to model stochastic reserves?

Does the product pass the SET?

No

No

Is the product ULSG or Term?

Yes

Yes

Yes

Reserve = max (NPR,

DR+DPA)

Does the company choose to model deterministic reserves?

Does the company pass the DET?

No

No

Yes

Yes

Yes

No

Reserve = NPR

Decision Tree for Determining Required Reserve Computations

No

PwC 12PwC

Reserve Grouping – Term & ULSGLATF has proposed limits on grouping related to these two products

All other life products can

be grouped together

PBR covers all life

insurance as defined by

SSAP 50

Other

Calculate the maximum of

NPR, DR and SR

ULSG is deemed to fail

DET by default

ULSG

Calculate the maximum of

NPR, DR and SR

Use of DET suspended in

2017

Term

12

PwC 13PwC

VM-20 Reserve Method

Net Premium Reserve, Deterministic Reserve, and Stochastic Reserve

3

4

Net Premium Reserve

Stochastic ReserveDeterministic

Reserve

5

13

PwC 14PwC

Net Premium Reserve – Term & ULSGGeneral

Different elements for Term & ULSG

When determining the NPR

Lapse ratesMethodology

Common elements for Term & ULSG

When determining the NPR

2001 or 2017 CSO Mortality Interest rate formula*

* Minor differences exist

VM-20 Net premium reserve is fully prescribed

• The net premium reserve calculation differs for term and ULSG

• Higher interest rate for term without non-forfeiture benefits and UL with secondary guarantee (SG)

• Unique formulas for term with and without shock lapses and for UL with and without SG

• Lapses are a component of the methodology

• Higher expense allowance than current CRVM

• Actuarial present value of benefits equals the PV of future benefits, including death, endowment, and cash surrender benefits. Future benefits are before reinsurance and policy loans.

PwC 15PwC

Deterministic ReserveGeneral• Seriatim reserve

• Cash flows discounted at Net Asset Earned Rate for scenario #12 of the 16 scenarios defined for SERT

• Gross Premium Reserve (GPR) defined as the actuarial PV of:

• Reflects prudent estimate assumptions

• If simplifications, approximations, or modeling efficiency techniques are employed, a company must be able to demonstrate that the seriatim reserve is not materially different than the grouped reserve for the DR calculation.

Plus

� Future death benefits and cash surrender benefits,

� Future expenses, excluding FIT, � AV in separate account at valuation date, and� Policy loan value at valuation date, including

accrued interest if loans are modeled

Minus

� Future gross premiums and/or other applicable revenue,

� Future net separate account transfers, � Future net policy loan cash flows, if policy

loans are explicitly modeled, � Future net reinsurance discrete cash,� Future net reinsurance aggregate cash flows

allocated, and� Future derivative liability program net cash

flows (cash received minus cash paid)

PwC 16PwC

Stochastic ReserveGeneral

• For a given risk subgroup, the stochastic reserve is calculated by reflecting:

- The aggregate of the Greatest Present Value Accumulated Deficiency (GPVAD) for each scenario, where the Accumulated Deficiency is defined as the negative of the projected assets

- PVs are calculated using prescribed discount rate equal to 105% of the scenario specific one-year treasury rate

- Scenario reserve = Starting assets + GPVAD

- The stochastic reserve is the CTE 70 of the scenario reserves

• Add together the stochastic reserves for each risk type subgroup for which the reserve held is the Max[NPR, DR+DPA, SR+DPA]

• Term and ULSG stochastic reserves need to be calculated separately

PwC 17PwC

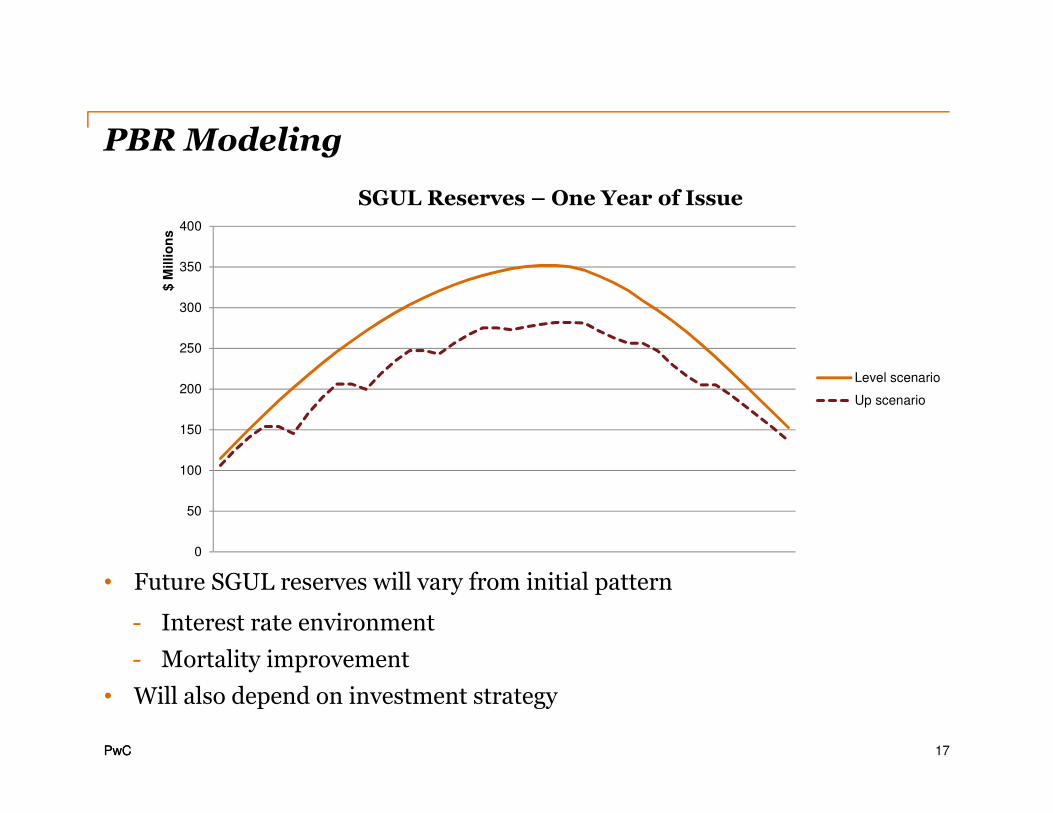

PBR Modeling

• Future SGUL reserves will vary from initial pattern

- Interest rate environment

- Mortality improvement

• Will also depend on investment strategy

0

50

100

150

200

250

300

350

400

$ M

illio

ns

SGUL Reserves – One Year of Issue

Level scenario

Up scenario

PwC 18PwC

Projection of reserves for term block

18

-100,000

0

100,000

200,000

300,000

400,000

500,000

600,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Aggregate STAT reserves - Rsv = 0 after LT Period

XXX - 2001 CSO XXX - 2017 CSO NPR Deterministic

PwC 19PwC

Deterministic & Stochastic Reserves – Assumption

Assumption

6

19

PwC 20PwC

Assumptions – General

Explicit margins

• Determine independently for each material assumption initially, and then, if applicable, adjust to take into account that risk factors are not normally 100% correlated.

• Must demonstrate reasonableness of the adjustment.

• Reflect magnitude of historical fluctuations in the risk factor

• Apply method consistently each year. Permitted to change method but must disclose the rationale and modeled reserve impact.

Prudent estimate assumptions

• Anticipated experience plus a margin

• Based on relevant and statistically credible available company experience or other relevant and statistically credible experience

• Apply credibility theory if applicable

• Provide margins for uncertainty, including adverse deviation and estimation error, such that the greater the uncertainty the larger the margin and resulting reserve

• Periodically sensitivity test to understand materiality of prudent estimate assumptions on the minimum reserve. Update less frequently if impact is immaterial and assumption is not changing.

• Requires appointed actuary review of emerging experience to set anticipated experience assumption.

Material assumptions

Prescribed

• Mortality

• Interest

• Equity returns

• Defaults

• Reinvestment spreads

Prudent estimate

• Morbidity

• Expenses

• Lapses

• Partial withdrawals

• Loans and

• Option elections

Types of assumptions

• Prescribed

• Stochastically Generated

• Prudent estimate assumptions

PwC 21PwC

PBR Actuarial Report/Governance

PBR Actuarial Report/

Governance

7

21

PwC 22PwC

VM-31 PBR Actuarial Report

� Two major parts to the report. The overview must be filed with the domiciliary commissioner by April 1 each year.

Overview Section

• Key statistics by product type

• Description of material risks

• Part 1 and Part 2 Section 1 of the annual statement blank

• Reliance statements

• Summary of valuation assumptions and margins for each major PBR product line

• Summary of modelling methodology for assets, liabilities and reinvestment assumptions (including any management action)

• Description of how materiality is determined as it relates to decisions, information, assumptions, risks, or other elements of PBR. Relate to % of surplus, % of reserves, or $ value.

• Certification paragraph that reserves comply with VM-05 and VM-20 and that assumptions and margins are prudent estimates.

Other Sections

• Summary of results

• Documentation of assumptions

• DET & SET

• Describe model segments

• Describe validation of model calculations

• Describe mortality segments & rationale for policy selections

• Describe rationale for credibility method

• Provide experience study results every 3 years for mortality and policyholder behavior

• Describe policyholder behavior margins and sensitivity test used to determine the margins

• Describe how changes in NGE impact policyholder behavior

• Describe changes in anticipated experience assumptions or margins since last PBR Actuarial Report

PwC 23PwC

PBR Governance

Company Management Board of Directors

Review PBR Reports

Resolve Management

Questions

Determine direction to rely on PBR valuations

Provide general

oversight

Senior Management

Qualified Actuary

Oversee PBR

valuation function

Adopt internal controls

over PBR valuations

Ensure validation,

appropriateness of PBR inputs,

studies, and results

Report to Board at

least annually

Ensure adequate resources

Oversee PBR calculations

Review assumptions, methods, and

models

Review internal standards for

valuation processes, controls, and

documentation.

Provide PBR summary report

to board and senior

management

Provide annual opinion on asset

adequacy of PBR and non-PBR balances

Cooperate with auditors and regulators.

Disclose unresolved PBR

issues.

PwC 24PwC

Tax Reserves

Tax Reserves

8

24

PwC 25PwC

PBR Tax ConsiderationsOverview of Tax Reserves for Life Insurance Contracts

Straightforward framework, devil in the details

• Federally Prescribed Reserve based on

- CRVM in effect when the contract was issued

- Prevailing mortality tables

- Prevailing interest rates (AFR if greater)

- No deficiency reserves

• Cap equals statutory reserve

• Floor equals contract net surrender value

• Calculations are performed contract-by-contract

25

PwC 26PwC

PBR Tax ConsiderationsTax issues presented by PBR

Some issues already identified (but not answered) by IRS

• For Net Premium Reserve

- How will reserves be computed for companies that elect 3-year transition and other special rules?

• For Deterministic Reserve

- Will IRS allow a Gross Premium Reserve methodology?

- What are prevailing mortality tables if company uses own mortality?

• For Stochastic Reserve

- Will IRS allow reserve that is not seriatim?

- How will factors that are not prescribed be taken into account?

26

PwC 27PwC

PBR Tax ConsiderationsTax issues presented by PBR, cont’d

Some issues already identified (but not answered) by IRS

• For Cap on deductible reserves

- Will IRS treat Stochastic and Deterministic Reserves as life insurance reserves despite use of non-prescribed factors?

- Same issue for testing whether a company is taxed as a life or nonlife company?

• For Life Insurance Contract qualification

- What are prevailing mortality tables in situations where a company may use its own experience rather than industry tables?

27

PwC 28PwC

PBR Tax ConsiderationsFurther IRS Guidance?

Prospects are limited

• IRS provided interim guidance on AG 43 in 2010, highlighted a number of issues but did not follow up

• In response to industry requests, IRS and Treasury Department’s Priority Guidance Plan anticipates guidance on both Life PBR and AG 43, in particular concerning the treatment of stochastic reserves

• As a practical matter, limited resources at IRS and Treasury mean it is possible – even likely – there will be no tax guidance concerning the implementation of Life PBR

28

PwC 29PwC

Company Initiatives Related to PBR

29

PwC 30PwC

Challenges in Implementing PBRTechnical requirements

Companies face many technical issues in implementing PBR including:

• Scoping – performance of deterministic and stochastic exclusion tests

• Assumption setting – based on own company or industry experience, or prescribed amounts

• Margin setting – for each of the major assumptions based, in part, on sensitivity testing

• Scenario generation – for asset and liability modeling

• Asset modeling – including current portfolio and reinvestments

• Liability modeling – of dynamic policyholder behavior

• Grouping – of experience and model cash flows

30

PwC 31PwC

Challenges in Implementing PBRCompany functions impacted

Company actuaries are not the only resources impacted by PBR:

• Financial reporting – additional reporting and disclosures

• Investments – modeling assets and strategies

• Information technology – access to data and computing power

• Risk management – assumption governance and model validation

• Executive management – oversight and Board communications

It is necessary to communicate with and engage many stakeholders in order to effectively implement PBR

31

PwC 32PwC

Challenges in Implementing PBRManagement information

Financial planning and analysis will be very different under PBR:

• Statutory profit signatures under PBR will be different

• Potential for more volatility in statutory earnings (and capital)

• Company business plan projections may have to incorporate stochastic processes

• Key performance indicators and attribution analyses will be very different under PBR

• Senior management and the Board are likely to need additional instruction on changes in potential profit emergence, increased volatility and range of expected outcomes

32

PwC 33PwC

Something for everyone!

• Executive Management: Provide oversight and resources

• Financial Reporting: Changes to the Statutory Blanks to incorporate PBR

• Finance: Forecast and explain changes in statutory reserves, more volatility in statutory earnings and surplus

• Investment Accounting: Investment data requirements; potentially more portfolios / segments

• Tax: Tax reserves during transition and after implementation of PBR

• Investments: Investment policy development and monitoring

• Risk Management and Governance: Validation of PBR models. Assumption and margin governance.

• Internal Audit: Review of processes and controls

• Product Development: Product changes, “right-sized” reserves with greater future uncertainty

• Information Technology: New data requirements, processes, computing capacity

• Human Resources: Race for experienced actuarial talent

• Valuation: Aggregate, calculate, articulate, repeat

PBR Business Implications

PwC 34PwC

Modeling Considerations for Implementation

1. Product combinations under PBR and how this fits within a company’s investment allocation framework

2. Companies struggling with modeling reinsurance (especially YRT), reinvestments, simplified underwriting and dynamic lapse experience

3. Strategic decisions have focused on tax reserves and product grouping

4. Limitations of current valuation, modeling, and administrative system

5. Margin setting (and evaluation of the conservatism of total margins) has been a focus of many clients as management approaches PBR

Common issues for PBR implementers

PwC 35

Thank you

Contacts

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. PwC refers to the US member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Jeff [email protected](414) 212-1715

Alexandre [email protected] (312) 298-3216