VENEZIA - Eurac Research · 2018-03-22 · •Tourism and other activities are all components of a...

16

Mara Manente Director, Ciset-University Ca’ Foscari, Venice VENEZIA: …. A SUSTAINABILE OR UNSUSTAINABLE BEAUTY?

Transcript of VENEZIA - Eurac Research · 2018-03-22 · •Tourism and other activities are all components of a...

Mara ManenteDirector, Ciset-University Ca’ Foscari, Venice

VENEZIA:

…. A SUSTAINABILE OR UNSUSTAINABLE BEAUTY?

VENEZIA: A SUSTAINABILE OR UNSUSTAINABLE BEAUTY?

Nome, data

Historical

Centre

Lido

Mestre-

Marghera

Municipality: 261.000 Inhabitants

Historical Centre: 54.400 Inhab.

(-1000inh per year)

Nome, data

SUMMARY

1. Big attraction: the numbers of tourism

2. The phenomenon of excursionism and the “touristregion”

3. The cost – benefit balance: negative externalities

4. The competitive profile

5. Strategic priorities

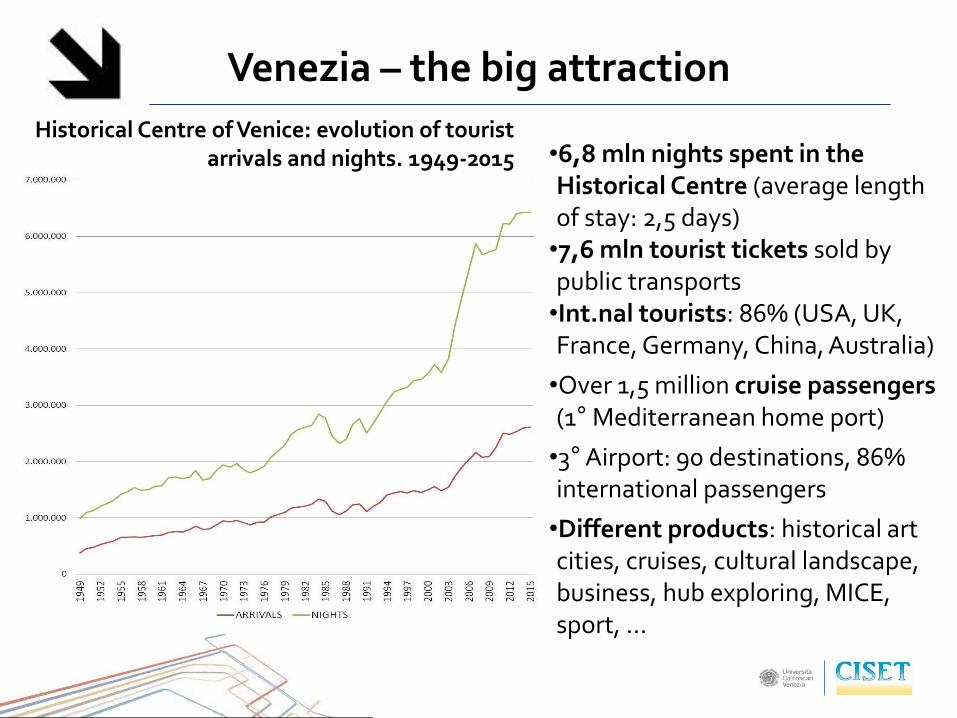

Venezia – the big attraction

Historical Centre of Venice: evolution of tourist arrivals and nights. 1949-2015 •6,8 mln nights spent in the

Historical Centre (average length of stay: 2,5 days) •7,6 mln tourist tickets sold by public transports•Int.nal tourists: 86% (USA, UK, France, Germany, China, Australia)

•Over 1,5 million cruise passengers (1° Mediterranean home port)

•3°Airport: 90 destinations, 86% international passengers

•Different products: historical art cities, cruises, cultural landscape, business, hub exploring, MICE, sport, …

Venezia – the whole attraction

•Over 25 million estimated visitors per year (less than 55.000 inhabitants)

•3,4 million from the green area: tourists that sleep outside Venice but their main destination is Venice

•2 bln euro the estimated overall tourist revenue

JESOLO

NOVENTA

SCORZE’

STRA’

MONSELICE

SOTTOMARINA

Coastal axis

Riviera

Mirano area

Terme euganee

PiaveTerraglio

Coastal axis

MOBILITY AXES

MESTRE

45 MINUTES

45 MINUTES45 MINUTES

45 MINUTES

45 MINUTES

Source: CISET

Venezia and its relevant tourist region

Venezia – the “cultural” experience

Tourists• 70% are first time visitors (50% in other cities)• Strong incidence of extra EU demand (USA, Australia, Canada, Japan, Brazil...)• Limited knowledge of the territory around Venice and of the city itself

(preference for traditional itineraries: bus terminal-railway station, Rialto bridge, St. Mark square)

• Good willingness to pay, medium-high expenditure

MAIN PRODUCT/SEGMENT

The experience in Venice• Focus on the magic atmosphere of the city and on its iconic value, but the image is

generic• Few visits to museums (1 entrance per visitor in Venice, on average)• Tourists generally require a very similar experience, independently from their

profile/willingness to pay • Also among same-day visitors, an important share require similar experience

High turnover of visitorsHigh dependence on un-differentiated markets

NEGATIVE EXTERNALITIES IN AN URBAN ENVIRONMENT

• …

• crowding out of other urban functions and a more complex “second level” crowding out, when activities related to cultural, high-quality visits are replaced with others selling cheap, mass flow oriented goods

• congestion in terms of time (70% of flows concentrated in 4 hours) and places (34% public space used by tourists, static image related to the big attractions and iconic values)

• visitors pay for the support services, but the costs for the maintenance of the primary attractions lie mainly on the residents …. AND

•The fiscal mechanism cannot completely bridge the gap

THE COST/BENEFIT BALANCE

Competitive profileThe “icon”cities: Venice, Florence, Bruges

GENERAL

•Tourism plays a driver role: mono-culture

•The city IS the attraction: just a few sites are recognized, but the potential of the resources is not completely exploited

•Reduced differentiation of tourism demand by motivation

•No peculiar development or change to lead them out of their side-line role in the next 20 years

BRAND INDICES

• Powerful tourist brands, strongly attracting international demand,

• Presence in other sectors (politics, economics, culture, fashion, etc. ) considered not so significant in the last 30 years

•Urban life perceived as ‘static’ and not exciting (pulse)** The two super-index have been conceived to be assimilable to Anholt City Brand Index in order to

compare resuls

THE ‘ULTIMATE’ CITIES (1)

• Generally compete on many touristmarkets (business, conventions, city breaks, cultural tourism, events, etc.),

• Are drivers of different networks ofmobilities at local and internationallevel

• Their offer can satisfy differenttargets

• Tourism and other activities are allcomponents of a complex project ofurban development

• Consolidated and global “brand” representing not only tourism, butalso cultural, politica, finacial, etc role(cfr. Anholt City Brands Index )

London, Paris, Barcelona, Rome

0

0,2

0,4

0,6

0,8

1

Role of International

tourism demand

Variety of socio-

demographic segments

Variety of tourist

activities/experiences offered

Significance of core

resources and attractors

Competitiveness of

accommodation supply

Relative cost of city for

tourists

Presence of the city

Pulse of the city

Potential o f the city

London Paris Barcelona Rome

SOURCE: CISET, Osservatorio delle città d’arte, Analisi di benchmark delle principali città italiane, con Mercury, Doxa e Censis, per conto di DipartimentoTurismo.- Presidenza del Consiglio dei Ministri; Minghetti, Montaguti, “Cities to play: Outlining Competitive Profiles for European Cities”

THE “YOUNG TRENDY” CITIES

Less established role as global tourist destinations Rapid development of touristflows in the last years mainly due to their:Perceived brand: “youth and

liveliness”Increasing city presence at

international levelHigh value attributed to the

pulse of the city

Prague, Istanbul, Sevilla

0

0,2

0,4

0,6

0,8

1

Role of International

tourism demand

Variety of socio-

demographic segments

Variety of tourist

activities/experiences offered

Significance of core

resources and attractors

Competitiveness of

accommodation supply

Relative cost of city for

tourists

Presence of the city

Pulse of the city

Potential o f the city

Prague Istanbul Sevilla

SOURCE: CISET, Osservatorio delle città d’arte, Analisi di benchmark delle principali città italiane, con Mercury, Doxa e Censis, per conto di DipartimentoTurismo.- Presidenza del Consiglio dei Ministri; Minghetti, Montaguti, “Cities to play: Outlining Competitive Profiles for European Cities”

Strengthening the diversification of the economicsectors (avoid tourism mono-culture) and sustaintourism business to “hybridise” (e.g. with creativeindustry)

Working on the traveller’s choice mechanism andbuying model (Tour Operators, guides, blogs, socialnetworks, influencers, …) by informing, guiding, sellingexperiences tailor-made and by increasing loyalty

Priorities (1)

The sustainability and competitiveness of the destination stay inits capacity to attract new market segments, to increase thesignificance of core attractions and make tourism a componentof a complex project of urban development:

Qualifying the market demand and its behavior to avoid thestandardization and trivialization of the tourist experience

Enhancing the visitor-friendliness of the destination by

•implementing a strategy for tourism management atmetropolitan level

• strengthening communication and information channels

•diversifying the offer and quality of complementarytourist services

• focusing on the internal and external accessibility

•planning a strategy of attractions and events relevant tothe targeted markets during all year

…… priorities (2)

Diversifying the supply chain according to the ''experienceapproach“ through the rediscovery of multifacetedconnections with the lagoon and the “terraferma” along theexiting mobility axes in order to avoid the “Gran Canal view”approach

System of Intelligence - Monitoring sustainability (e.g. ETISToolkit for sustainable destination management) - Monitoringeffectiveness and efficiency of policies for tourism

…… priorities (3)

Many Thanks!Mara Manente

CISET - Università Ca’ Foscariemail:

[email protected]@unive.it

URL: http//:www.unive.it/ciset

@ilCISET

@ manente03

![[drupalday2017] - Venezia & Drupal. Venezia è Drupal!](https://static.fdocuments.net/doc/165x107/58d13cdb1a28ab455d8b50d5/drupalday2017-venezia-drupal-venezia-e-drupal.jpg)