Vattenfall Q2 2012 results · 4 | Conference Call | 31 July 2012 Lower electricity futures prices...

25

Vattenfall Q2 2012 results Øystein Løseth, CEO and Ingrid Bonde, CFO Conference Call, 31 July 2012

Transcript of Vattenfall Q2 2012 results · 4 | Conference Call | 31 July 2012 Lower electricity futures prices...

Vattenfall Q2 2012 results Øystein Løseth, CEO and Ingrid Bonde, CFO

Conference Call, 31 July 2012

2 | Conference Call | 31 July 2012

Q2 Highlights

• Stable net sales from continuing operations • Operating profit in Q2 2012 significantly higher than the negative result in Q2

2011- 2011 result influenced by the large negative effect of the write-down of German

nuclear assets • Underlying operating profit from continuing operations was almost on par with

Q2 2011 - Lower prices were compensated by 9% higher production volumes (hydro and

nuclear) and lower costs • Cost reduction programme ahead of plan

- As of 30 June, SEK 5 billion achieved• Compensation for closure of German nuclear power plants

- Request for the institution of arbitrage proceedings filed at ICSID, Washington, and constitutional complaint to German Federal Constitutional Court

• Application to Swedish Radiation Safety Authority (SSM) to specify terms for new nuclear reactors

3 | Conference Call | 31 July 2012

Decline in Nordic spot prices / Improved hydro balance

• Sharp decline in Nordic spot prices Q2-12 vs. Q2-11

• Nordic hydrological balance still strong (+9.6 TWh at the end of Q2)

• German and Dutch spot prices declined but to a lesser extent

Monthly Spot Average Hydrological balance

15

25

35

45

55

65

75

85

Jan-1

0Apr-

10

Jul-1

0Oct-

10

Jan-1

1Apr-

11

Jul-1

1Oct-

11

Jan-1

2Apr-

12

Jul-1

2

Nord Pool Spot EPEX APX

0

200

400

600

800

1000

-60

-40

-20

0

20

40

System Price Hydro Balance 200720032002 2004 2005 2006 2008 2009 2010 2011 2012

EUR/MWh TWh SYSSEK/MWh

-24.6

40.4 (53.6)

EPEX

-45.6

28.4 (52.2)

Nord PoolEUR/MWh APX

Q2-12 (Q2-11) 45.1 (54.4)

% -17.0

4 | Conference Call | 31 July 2012

Lower electricity futures prices

• Electricity futures prices decreased Q2-12 vs Q1-12 on all Vattenfall markets- Mainly due to lower spot and commodity

prices and lower economic sentiment in Europe

• Lower coal and oil prices Q2-12 vs. Q1-12 • Fairly stable gas prices • CO2 prices still below 10€/ton

Electricity futures prices Commodity prices

0

20

40

60

80

100

120

140

Jan-1

0Mar-

10May

-10Ju

l-10

Sep-10

Nov-10

Jan-1

1Mar-

11May

-11Ju

l-11

Sep-11

Nov-11

Jan-1

2Mar-

12May

-12Ju

l-12

0

10

20

30

40

50

60

70

Oil (USD/bbl), Brent Front M onth Coal (USD/t), API 2, Front YearEmission allowances CO2 (EUR/t), Dec 07-11 Gas (EUR/M Wh), NBP, Front Year

EUR/MWh USD EUR

35

40

45

50

55

60

65

Jan-1

0Apr-

10

Jul-1

0Oct-

10Ja

n-11

Apr-11

Jul-1

1Oct-

11Ja

n-12

Apr-12

Jul-1

2

NP 13 NP 14 EEX 13EEX 14 APX 13 APX 14

5 | Conference Call | 31 July 2012

Higher generation output, higher heat and gas sales

• 9% higher electricity generation output (41.1 TWh in Q2/12 vs 37.7 TWhin Q2/11)- Hydro power generation increased due to high reservoir levels - Nuclear generation increased due to timing of audits and shorter

unplanned outages in Q2 2012• Higher heat and gas sales due to colder weather

TWh TWh

1.1

10.611.6

17.8

0.9

7.1

10.2

19.5

0

5

10

15

20

25

Fossil Nuclear Hydro Wind & other

Q2 2012: 41.1 Q2 2011: 37.7

6,5

8,9

6,47,2

0123456789

10

Heat sales Gas sales

Q2 2012 Q2 2011

6 | Conference Call | 31 July 2012

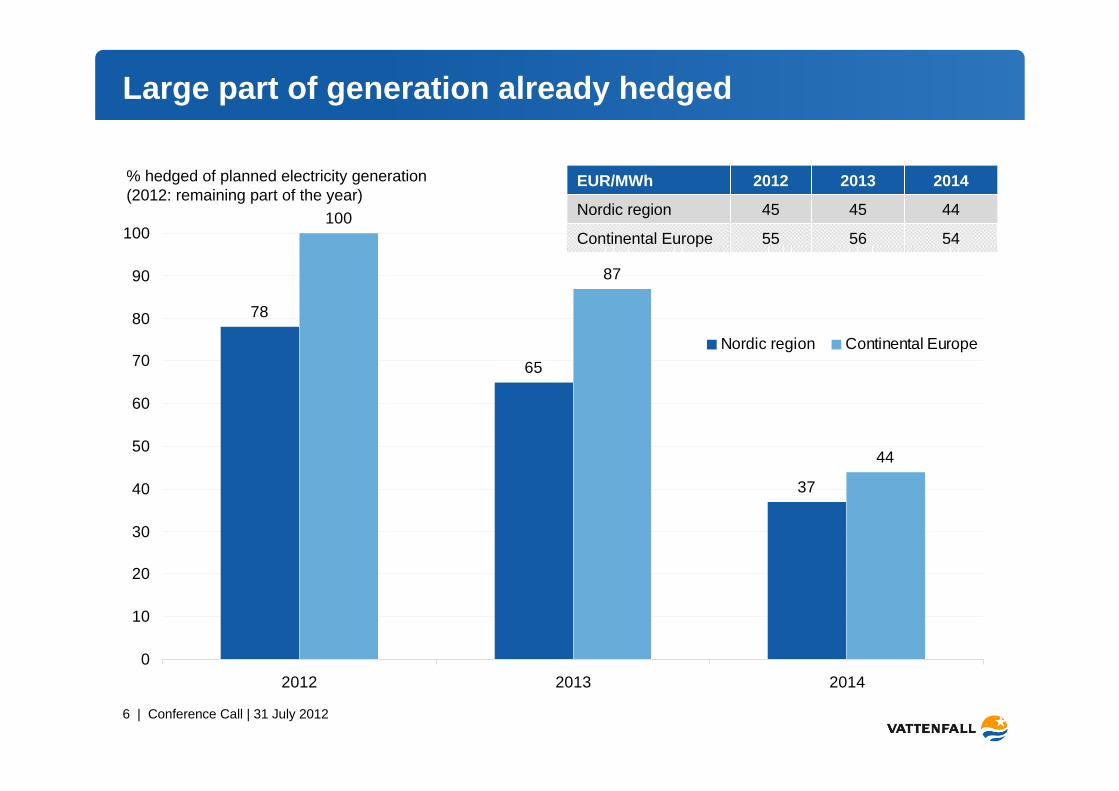

78

65

37

100

87

44

0

10

20

30

40

50

60

70

80

90

100

2012 2013 2014

Nordic region Continental Europe

Large part of generation already hedged

55

45

2012

56

45

2013

54

44

2014EUR/MWh

Nordic region

Continental Europe

% hedged of planned electricity generation(2012: remaining part of the year)

7 | Conference Call | 31 July 2012

Application to Swedish Radiation Safety Authority

• Vattenfall has made an application to Swedish Radiation Safety Authority, SSM, to specify terms for new nuclear reactors

• Vattenfall wants to ensure continuous production of base-load energy, with low CO2-emissions, when existing nuclear reactors are to be phased out (2025-2035)

• The application is necessary for Vattenfall to investigate conditions set by SSM. It is a multi-step process which takes several years to complete

• No decision has been made within Vattenfall to replace old reactors with new reactors

• Any potential future investment will be decided on a cost versus revenue basis. If profitable, Vattenfall wants to have the option to replace reactors

8 | Conference Call | 31 July 2012

Assessment starts now in order to have the option for replacement power

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14

New law in place

15

Replacement power in operation

16

Optionally investment

Analysis of the conditions, requirements and processes for a complete basis for decision

Project planning for new plant

Erection and commissioning of a new plant

Stepwise decision process

Year

FinancialsIngrid Bonde, CFO

10 | Conference Call | 31 July 2012

Q2 2012 Financial highlights

--3,235877Profit after tax

-35.66,1253,947Cash flow (FFO)

-12.7141,089**123,207Net debt

-1,590

5,382

-3,239

12,566

40,443

Q2 2011

-3,204

4,818

4,775

9,730

36,703

Q2 2012MSEK Change (%)

Net Sales -9.2

EBITDA -22.6

EBIT -

Underlying EBIT* -10.5

Financial items, net -101.5

* Underlying profit: EBIT excluding Items affecting comparability

** As of 31 December 2011

11 | Conference Call | 31 July 2012

Underlying EBIT per operating segment

-7.4

Change (%)

3,905

Q2 2011

3,616

Q2 2012MSEK

Generation

• Underlying EBIT decreased by 289 MSEK

- Lower achieved prices

- Higher volumes

- Lower O&M costs

-24.0

Change (%)

1,607

Q2 2011

1,222

Q2 2012MSEK

Distribution and Sales

--

Change (%)

61

Q2 2011

-24

Q2 2012MSEK

Renewables

• Underlying EBIT decreased by 385 MSEK

- Divestment of Polish, Finnish and Belgian operations

- Improved profitability within B2C

• Underlying EBIT decreased by 85 MSEK

- Lower achieved prices

- Poorer wind conditions in the UK

12 | Conference Call | 31 July 2012

23.7

7.2

-1.0

17.7

+1.0 -1.4

16.5

8.6

9.1

-1.1 +1.3

EBIT H12011

IAC UnderlyingEBIT H1

2011

Electricityprice

Electricityvolume

Costs Structure Other UnderlyingEBIT H1

2012

IAC EBIT H12012

Development of underlying EBIT H1 2012

bn SEK

13 | Conference Call | 31 July 2012

H1 2012 Financial highlights

271.33,96814,732Profit after tax

-8.818,28116,664Cash flow (FFO)

-12.7141,089**123,207Net debt

-3,483

17,676

8,603

29,498

92,311

H1 2011

-5,658

16,493

23,731

33,556

85,697

H1 2012MSEK Change (%)

Net Sales -7.2

EBITDA 13.8

EBIT 175.8

Underlying EBIT* -6.7

Financial items, net -62.4

* Underlying profit: EBIT excluding Items affecting comparability

** As of 31 December 2011

14 | Conference Call | 31 July 2012

Cash flow development Q2 2012

bn SEK

+0.5

-2.4

-3.8

8.4

-0.5

-3.2

4.5

Cash f low fromoperations

MaintenanceCapex

Free cash flow Grow thinvestments

Divestments Cash f low fromfinancing activities

Cash flow for theperiod

15 | Conference Call | 31 July 2012

Key credit metrics

• FFO Interest cover decreased to 4.3 (x)

• FFO/adjusted net debt increased to 23.4%

• Adjusted net debt/EBITDA decreased to 2.7 (x)

• Gross debtdecreased by SEK 4.6 bn to SEK 165.7 bn

• Net debtdecreased by SEK 17.9 bn to SEK 123.2 bn

• Adjusted net debtdecreased by SEK 19.5 bn to SEK 156.5 bn

Comparison with 31 December 2011

3.22.7Adj.net debt/ EBITDA (x)

21.7

27.1

4.8

FY 2011

23.4

32.2

4.3

Q2 2012Key credit metrics

FFO Interest cover (x)

FFO/net debt (%)

FFO/adj. net debt (%)

0

50

100

150

200

250

30.06

.2010

30.09

.2010

31.12

.2010

31.03

.2011

30.06

.2011

30.09

.2011

31.12

.2011

31.03

.2012

30.06

.2012

For calculation of adjusted net debt, see Appendix page 23

Rolling 12 months values

16 | Conference Call | 31 July 2012

Vattenfall’s key strengths:

• Strong owner, clear operating mandate• Diversified production portfolio, competitive low cost production assets

(hydro, nuclear, lignite). Low CO2 exposure in the Nordic market.• Good geographical base and strong market positions (Northwestern

Europe)• Strong liquidity position• Prudent hedging policy• Large end-customer base• Significant share of regulated business• Proven execution ability (divestments, cost reduction, re-organization)

Concluding remarks

Q&A

Appendix

19 | Conference Call | 31 July 2012

+1.5-1.0

8.6

-3.2

4.8

-0.5+0.3

5.4

-0.90.1

4.8

EBIT Q2 2011 IAC UnderlyingEBIT Q2 2011

Electricityprice

Electricityvolume

Costs Structure Other UnderlyingEBIT Q2 2012

IAC EBIT Q2 2012

Development of underlying EBIT Q2

bn SEK

20 | Conference Call | 31 July 2012

Strong liquidity position

36,391Available liquidity

-5,923Unavailable liquidity*

42,314Reported cash, cash equivalents & short term investments

25,767Short term investments

16,547Cash and cash equivalents

SEK millionGroup Liquidity

As of 30 June 2012

918Within 180 days

334Within 90 days

SEK millionDebt maturities**

*German nuclear ”Solidarvereinbarung” 2,987, Margin calls paid (CSA) 1,088 and others 1,848**Excluding loans from minority owners and associated companies

21 | Conference Call | 31 July 2012

Committed credit facilities

33,080Total undrawn

10,709EUR 1 300 millionMulti option Facility (12-month rolling)

EUR 2 550 million

Line size

22,371RCF (maturity Jan 2016)

Amount available SEK millionCommitted credit facilities

As of 30 June 2012

22 | Conference Call | 31 July 2012

Bonds issued under EMTN-programme

57%

Margin calls (CSA)5%

Loans from associated companies

6%

Loans from minority shareholders

7%

NPV of liabilities to Nuon shareholders

17%

Bank loans and other 3%

Hybrid capital5%

Breakdown of gross debt

• All public debt issued by Vattenfall AB• The debt portfolio has no currency exposure that

has an impact on the income statement. The debt in foreign currency is either swapped to SEK or booked as a hedge against net foreign investments.

• No structural subordination

Total debt 30 June 2012: SEK 165.7 billion (EUR 18.9 billion)

9,92118,710Total

01,710SEK 15 bn Domestic CP

2,000

15,000

Size(MEUR)

0

9,921

Utilization(MEUR)

Debt issuing programmes

EUR 15 bn Euro MTN

EUR 2 bn Euro CP

23 | Conference Call | 31 July 2012

Development of reported and adjusted net debt

*Of which: German nuclear ”Solidarvereinbarung” 3.0, margin calls paid (CSA) 1.1 and others 1.8

-141.1-123.2Net debt

0.60.2Loans to minority owners of foreign subsidiaries

17.425.8Short-term investments

11.316.5Cash and cash equivalents

-170.4-165.7Total interest-bearing liabilities

-8.0-9.5Other liabilities

-10.2-11.2Liabilities to minority shareholders

-10.5-9.6Liabilities to associated companies

-30.5-27.4Present value of liability pertaining to acquisition of subsidiaries

-99.2

-8.8

June 302012

-102.3Bond issues and commercial papers and liabilities to credit institutions

-8.9Capital Securities

Dec 312011

Net debt(bn SEK)

-176.0-156.5= Adjusted net debt

22.936.4= Adjusted cash, cash equivalents & short-term investments

-5.8*-5.9*Unavailable liquidity

28.742.3Reported cash, cash equivalents & short-term investments

-198.9-192.9= Adjusted gross debt

9.810.4Liabilities to minority owners due to consortium agreements

7.58.0Margin calls received

3.33.7Cross currency swaps

-18.5-18.4Provisions for nuclear power (net)

-12.5-12.3Mining & environmental provisions

-22.5-23.0Present value of pension obligations

4.4

-165.7

June 302012

4.450% of Hybrid capital

-170.4Total interest-bearing liabilities

Dec 312011

Adjusted net debt(bn SEK)

24 | Conference Call | 31 July 2012

Vattenfall debt maturity profile

These figures differ from the reported interest bearing liabilities as loans from associated companies, minority owners, margin calls received (CSA) and valuation at fair value are excluded and currency derivatives for hedging debt in foreign currency are included.

Including Hybrid capital

141.1123.2Net debt (SEK bn)

3.93.6Average interest rate (%)

5.55.8Average time to maturity (years)

3.9

30 June 2012

4.3

31 Dec 2011

Duration (years)

MSEK

Hybrid capital

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038

Undrawn back-up facilities

Includes deferred payments for Nuon shares (MEUR):July 2013: 1,179.5July 2015: 2,071.3

25 | Conference Call | 31 July 2012

Financial targets and outcome Q2 2012

2.1 times3.5-4.5 timesCash flow interest coverage after maintenance investments

15.7%*15% on average equityReturn on Equity (RoE)

40-60%

Single A category rating

Target

40% (SEK 4.4 bn)

Moody’s: A2, negative outlookS&P: A-, stable outlook

Q2 2012Key Ratio

Credit rating

Dividend pay-out

* Rolling 12 months values