Value chains coffee_uganda_briefing_note

12

www.iisd.org/gsi © 2012 The International Institute for Sustainable Development Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda Julie Dekens (IISD) and Fredrick Bagamba (MAK) T his briefing note aims to stimulate discussion of policy options for the development of climate-resilient and socially inclusive agro-value chains. It is addressed to decision-makers at all levels in the public and private sectors, especially in commodity-dependent developing countries (CDDCs). The content builds on the results of a pilot initiative on identifying and managing the risks of climate change along the coffee value chain in Uganda. CLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014

-

Upload

dr-lendy-spires-foundation -

Category

Documents

-

view

76 -

download

1

Transcript of Value chains coffee_uganda_briefing_note

www.iisd.org/gsi © 2012 The International Institute for Sustainable Development

Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda

Julie Dekens (IISD) and Fredrick Bagamba (MAK)

This briefing note aims to stimulate discussion of policy options for the development of climate-resilient and socially inclusive

agro-value chains. It is addressed to decision-makers at all levels in the public and private sectors, especially in commodity-dependent developing countries (CDDCs). The content builds on the results of a pilot initiative on identifying and managing the risks of climate change along the coffee value chain in Uganda.

CLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMSBRIEFING NOTE SERIES | FEBRUARY 2014

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 22

KEY POINTS:• A changing climate can affect the entire chain of value-adding activities for

agricultural commodities, from production and processing to marketing and consumption of the final product.

• Sustainable value chain development can only be achieved if all actors along the value chain work together to address climate risks. This means that actors must look beyond their own activities on the value chain to consider how other upstream/downstream actors and activities may be affected by both climate risks and risk management decisions. While such a call for a comprehensive approach to climate adaptation is not new, limited evidence of concrete applications exists in practice. A value chain analysis is therefore proposed for a more integrated approach to climate adaptation.

• Results from a qualitative and participatory analysis of climate impacts on the coffee value chain within Uganda show that climate hazards already negatively affect all actors along the chain, but in different ways and to different extents. Most actors are already making some efforts to minimize the negative impacts but not all responses are sustainable. A lack of communication and trust between and among actors along the value chain particularly hampers climate adaptation.

• Three priority actions are recommended for climate-resilient and inclusive coffee value chain development in Uganda. First, decision-makers should improve networking and partnerships for climate adaptation along the value chain by strengthening existing platforms and structures at all levels and exploring the role of incentives (e.g., standards). Second, the government and the financial services industry need to develop new and flexible financial products to support climate-resilient and inclusive agro-value chains through capacity building and innovative public-private partnerships. Finally, investing in climate-resilient infrastructures such as roads, irrigation systems, storage facilities and telecommunications should remain a top priority to support agro-value chain development in a changing climate.

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 3

BACKGROUNDClimate change undermines inclusive agro-value chains development. Globally, impacts of extreme weather

events such as floods, droughts and hailstorms already undermine the performance of value chains—for example, by leading to losses in agricultural production, the destruction of processing and transport infrastructures, and the deterioration of export earnings.

This trend is expected to continue and worsen as climate change brings more frequent and intense extreme events, shifting rainfall patterns and rising temperatures. For example, reduced rainfall may limit hydroelectricity production, restricting agro-processing capacity and leading to higher production, processing and marketing prices with distributional impacts not only at the farm level but across a broad array of sectors and industries. Extreme weather events could increase the transportation costs. Value chain deterioration has the potential to compromise the achievement of development objectives from local to national levels, particularly affecting poverty reduction and food security efforts. This is a major concern for CDDCs, defined as countries for which at least 60 percent of export earnings depend on commodities. In 2009, CDDCs represented 94 of the 156 developing countries and most were also net food importers.i These countries are particularly vulnerable to climate variability and change because of their reliance on agro-commodities and limited economic diversification capacity.

In addition, even when agro-commodity trade generates benefits at the national level, those benefits do not automatically translate into benefits at the small-scale producers’ level. Farmers (and especially women farmers) tend to lack access to information, credit and markets; depend heavily on middle men who eat into profits; and rely on poor infrastructure—each of which hampers their bargaining power and ability to participate in and benefit from post-farm, value-addition processes. Climate change further accentuates these power asymmetries and inequalities along value chains: those with limited adaptive capacity suffer the most since they have fewer resources with which to minimize negative impacts and/or take advantage of any opportunities associated with climate change.

A value chain approach supports integrated climate risk management. To address these challenges, governments are diversifying their export portfolios and promoting integrated value chain development to better connect producers to markets and increase economic returns to small farmers. Indeed, value chains have emerged as an important place to embed environmental and socioeconomic sustainabilityii because they recognize the interdependency of actors involved in a product value chain, from production to consumption, and the need for comprehensive solutions (i.e., across different levels and sectors). But for value chain development to be truly sustainable over the long term, the exposure and vulnerability of value chain activities to current and expected climatic changes must be reduced.

So far, climate change has largely been addressed along value chains through interventions that seek to reduce greenhouses gas emissions.iii For example, multinational and domestic companies such as Walmart, PepsiCo and Sompo Japan Insurance Inc, to name a few, are already working toward reducing their carbon footprint to achieve sustainable or “green” value chain development.iv These efforts have been mainly driven by increasing pressure from governments, shareholders and customers to reduce carbon dioxide emissions.v The Carbon Disclosure Project, for example, is an international, not-for-profit organization that surveys the largest multinational corporations worldwide to disclose their greenhouse gas emissions on behalf of institutional investors.

In comparison, relatively little has been done to support climate adaptation beyond the production level, along entire value chains. This is presumably due to a combination of factors such as: a lack of understanding of climate change adaptation (including the distinction between adaptation and mitigation and between adaptation and sustainable

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 4

development); the channelling of climate-related finance on mitigation and in emerging economies such as those of China and Brazil rather than in least-developed countries;vi the lack of data and information about future impacts of climate change; inherent uncertainties around information that is available; and the lack of economic and/or costs-benefit analyses on impacts and risk management strategies.

As a result, little is known about the impacts of climate change on value chains at the postharvest stage, including the wider macro-economic implications for a country’s competitiveness, especially in the developing world.vii But to secure sustainable investments in value chain development, governments and other actors need to ensure that climate risks are managed not just at the production level, but also throughout the entire value chain from production to marketing.

THE CASE STUDYAn initiative on climate-resilient coffee value chains (CRCV) was piloted in Uganda. The economy of

Uganda remains largely dependent on a few agro-commodities, which are predominantly rainfed and grown by smallholders with limited external inputs, making the country highly sensitive to risk associated with climate variability and change. During the period 1970–2012, Uganda had the third highest population growth rate (3.3 per cent) and the highest fertility rate (6.1 births per woman) in the world.viii Population increase has caused land fragmentation, a decline in farm sizes, deforestation and swamp encroachment resulting in low incomes and reduced access to local resources (e.g., manure and grass mulch), which further contribute to low soil fertility and low yield. A changing climate puts additional pressure on the country’s development. The government’s development strategy strongly relies on exports to achieve the country’s national Vision 2040 of a “transformed Ugandan society from a peasant to a modern and prosperous country within 30 years” with a focus on commercial agriculture, value addition through agro processing and employment creation along entire commodity value chains.ix While the government also recognizes the threat posed by climate change, the issue is relatively new and climate risk has not yet been integrated into strategic trade documents.x

Against this background, in 2013 the Ministry of Trade, Industry and Cooperatives (MoTIC), Makerere University (MAK) and the International Institute for Sustainable Development (IISD) initiated a six-month pilot initiative to support the integration of climate risks into agro-value chains in Uganda. Specifically, the partners developed a participatory process for exploring the links between climate and the coffee value chain within Uganda as a way of showcasing the range of climate impacts and responses related to a particular agro-commodity.

Coffee remains a major crop in Uganda’s economy. Coffee was selected for this case study because it is a climate-sensitive cropxi that continues to provide the largest share of the total export revenue for the country (i.e., coffee provided 30 per cent of the commodity exports between 2009 and 2010). Coffee production in Uganda has been mostly characterized by high fluctuation and overall stagnation since the 1960s—a trend attributed to climate variability and other factors such as price fluctuation, reduced soil fertility, pests and diseases, and mismanagement. The highest production level was recorded in 1996 with close to 288,000 tonnes compared to more than 94,000 tonnes in 1961 and 186,000 tonnes in 2012.xii The total area of land under coffee has increased modestly from more than 245,000 hectares in 1961 to 310,000 hectares in 2012. Various studies document that farmers already perceive increasing weather uncertainty and changes. Studies on the projected impacts of climate change on coffee in Uganda (and globally) predict negative impacts, particularly for Arabica coffee. However these results need to be further refined and validated. The correlation between climate variability and coffee diseases also needs to be further studied.xiii But clearly all actors along the value chain are already dealing with increasing uncertainties due to climatic and non-climatic factors, and this trend is expected to continue in the future.

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 5

The climate risk analysis was conducted using multistakeholder dialogues along the coffee value chain. The use of a participatory, qualitative approach to climate risk analysis is based on the recognition that perceptions and interpersonal dynamics, including trust relationships, influence the way actors adapt (or not) to a changing climate.xiv To put it simply, if some actors do not perceive climate risk as a major challenge to their activities, it is unlikely that they will take specific actions to address those risks; value chain actors may have similar interests, but a lack of trust between those actors is likely to maintain the status quo and prevent the development of innovative, win-win solutions. The approach also acknowledges that all actors along the value chain are interlinked, answering questions such as: How do actors at a specific level of the chain (e.g., farmers) influence, or not, other actors at the same levels (e.g., input suppliers) or other levels (e.g., exporters)? How do climate hazards combine with other non-climatic risks to affect all value chain actors? Who is affected the most along the chain? The multistakeholder dialogues used in the CRCV initiative mobilized 80 participants representing farm input suppliers, coffee farmers, traders, processors, exporters, and service providers at the production, transformation and marketing stages of the chain. The approach was based on the five-step process described in Table 1.

Table 1: Overall five-step approach of the CRCV initiative

The approach provided a platform for coffee value chain actors to share and learn from each other using “climate dialogue theatres.” Climate dialogue theatres (CDTs) are based on a method that uses drama to promote adult learning on climate adaptation among coffee value chain actors.xv Three CDTs were organized at the production, transformation and marketing levels of the coffee value chain between June and July 2013. The first two CDTs were piloted in Rakai district in the southwestern part of Uganda to build upon previous research conducted by IISD and MAK on coffee and climate risk. The CDT at the marketing level took place in Kampala where most coffee exporters and their service providers reside. CDTs took place “in-situ” (i.e., a coffee-producing village, a processing factory, an exporter warehouse) so that discussions were as concrete as possible.

Steps

1. Engagement (ongoing)

2. Co�ee value chainmapping

3. Climate risk analysis I(horizontal integration)

4. Climate risk analysis II(vertical integration)

5. Reporting and dissemination(ongoing)

Meetings

Literature reviewKey experts meetings

Dialogue theatres at theproduction, transformationand marketing levels

National multistakeholderworkshop

ProposalFinal report and briefs

Raise awareness about the projectand themeSecure ownership and support forprocess

Mapping process, functions, actors,geography, resources, governancestructure and vulnerability toclimate risks

Understanding climate impact andresponses within each segment of the value chain (focus on key actors’perceptions and narratives)

Understanding climate impact andresponse chains across the di�erentsegments of the value chain (focuson risk transmission/distribution asperceived by key actors)

Elaborate and validate resultsSecure key stakeholder ownershipof results

Purpose Methods

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 6

Each CDT was a one-day event organized in the local language with 20 to 25 participants. The term “climate change” was not used unless the participants mentioned it in order to avoid creating confusion and biases in people’s discourse (i.e., confusion between climate variability and climate change; bias towards attributing all changes to climate change). The focus was on current climate hazards and associated current and future potential trends. It was up to the project team to probe participants to understand whether or not the type of changes participants were describing referred more to climate variability or to climate change or both. The CDTs were generally organized into three key sessions: (1) introduction and group formation based on people’s roles along the value chain; (2) issue formulation and prioritization through short story narration in groups (i.e., each group was asked to build a story based on real life experiences around one, or a combination of, climate hazard[s]) and the associated impacts that the group wants to address; and (3) solution identification through rounds of performance and interactive dialogue, where the audience helped each performing group to refine the problem and identify possible alternative solutions.

The process of using CDT contributed to both raising awareness on climate impacts and eliciting the value chain actors’ perceptions of climate impacts and responses. Results from piloting the CDT show that dramatization enhanced learning, especially at the production and transformation levels of the value chain. The level of dramatization decreased at the upstream (marketing level) of the chain. Group participation in their contextual environment also helped to trigger memories about climate impacts and responses at all levels, which facilitated knowledge exchange. Finally, as a result of the CRCV pilot initiative, for the first time in Uganda, climate change issues were integrated into trade-related issues at the ministerial level.

KEY FINDINGSFinding 1: Climate hazards negatively affect all actors along the chain, but in different ways and to different

extents. The impacts of climate hazards are felt across the entire coffee value chain from production to export. All participating actors expressed concern over the perceived impacts of climate hazards (mainly drought, floods and changing rainfall patterns) on their activities. Climate hazards are associated with a reduction in coffee yield and quality through: physiological disruptions of the coffee trees and increased incidences of pests and diseases; the deterioration of coffee seedlings; the disruption of the bean-drying process; and the destruction of inputs and infrastructure for processing and transportation. Indirectly, climate hazards further contribute to reducing incomes through decreases in business activities and services provision and an increase in costs for business and service delivery costs at three levels: production (e.g., increased human labour), transformation (e.g., increased breakdown of processing equipment and machinery due to high moisture content of beans resulting from heavy rainfall) and distribution (e.g., increased vehicle repair costs due to road deterioration from heavy rainfall). Decreasing coffee quality due to climate hazards affects coffee prices and the margins earned by the various actors with impacts for the country’s competiveness on the international market.

It is very hard to generalize differences between the value chain actors in terms of level of exposure and vulnerability to climate hazards because of the complexity of the chain and the diversity of actors in terms of their roles, sizes (in relation to their activities) and locations. However, coffee farmers and processors generally tend to be more vulnerable to the impacts of climate hazards than traders, middlemen and exporters. The results from the pilot study highlight that farmers and processers tend to have limited diversification capacity (e.g., the inability of coffee processing plants to process other commodities), weak organizational capacity (e.g., very limited direct links between farmers and exporters) and face an unfavourable policy environment (e.g., most actors along the chain pass on the losses incurred from climate hazards to farmers in the form of lower coffee bean prices). Thus, vulnerability tends to be more concentrated at the production end of coffee value chains.

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 7

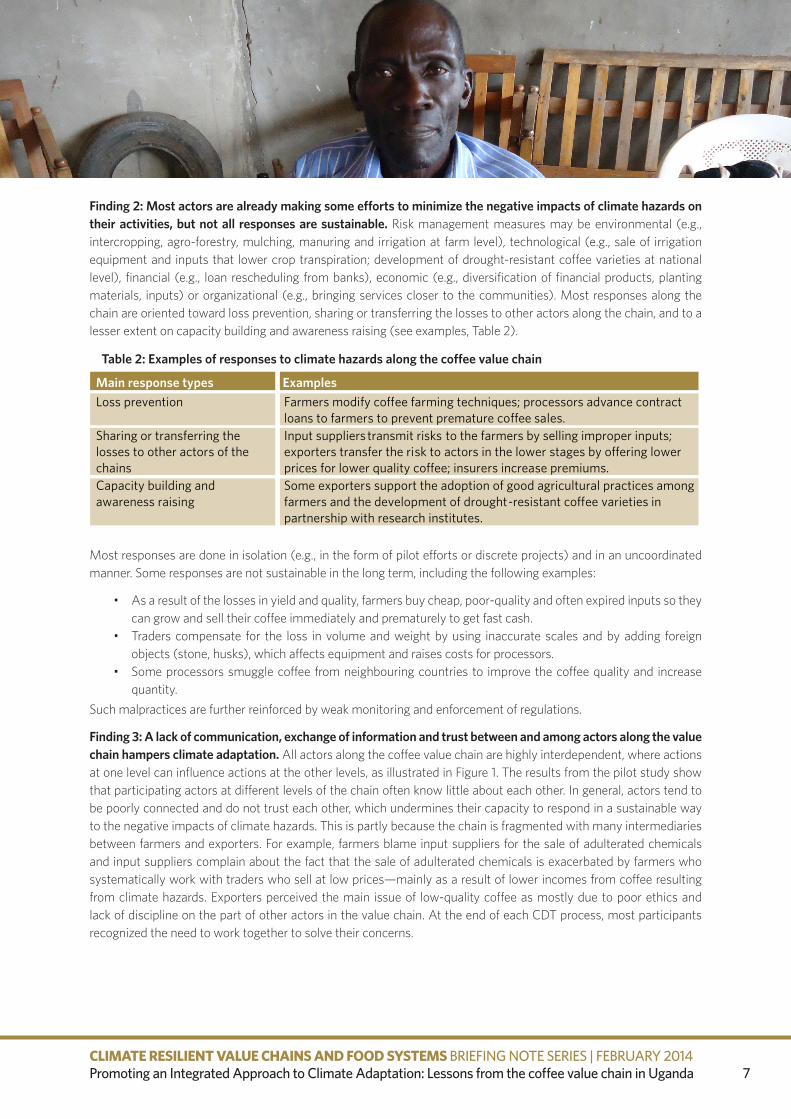

Finding 2: Most actors are already making some efforts to minimize the negative impacts of climate hazards on their activities, but not all responses are sustainable. Risk management measures may be environmental (e.g., intercropping, agro-forestry, mulching, manuring and irrigation at farm level), technological (e.g., sale of irrigation equipment and inputs that lower crop transpiration; development of drought-resistant coffee varieties at national level), financial (e.g., loan rescheduling from banks), economic (e.g., diversification of financial products, planting materials, inputs) or organizational (e.g., bringing services closer to the communities). Most responses along the chain are oriented toward loss prevention, sharing or transferring the losses to other actors along the chain, and to a lesser extent on capacity building and awareness raising (see examples, Table 2).

Table 2: Examples of responses to climate hazards along the coffee value chain

Most responses are done in isolation (e.g., in the form of pilot efforts or discrete projects) and in an uncoordinated manner. Some responses are not sustainable in the long term, including the following examples:

• As a result of the losses in yield and quality, farmers buy cheap, poor-quality and often expired inputs so they can grow and sell their coffee immediately and prematurely to get fast cash.

• Traders compensate for the loss in volume and weight by using inaccurate scales and by adding foreign objects (stone, husks), which affects equipment and raises costs for processors.

• Some processors smuggle coffee from neighbouring countries to improve the coffee quality and increase quantity.

Such malpractices are further reinforced by weak monitoring and enforcement of regulations.

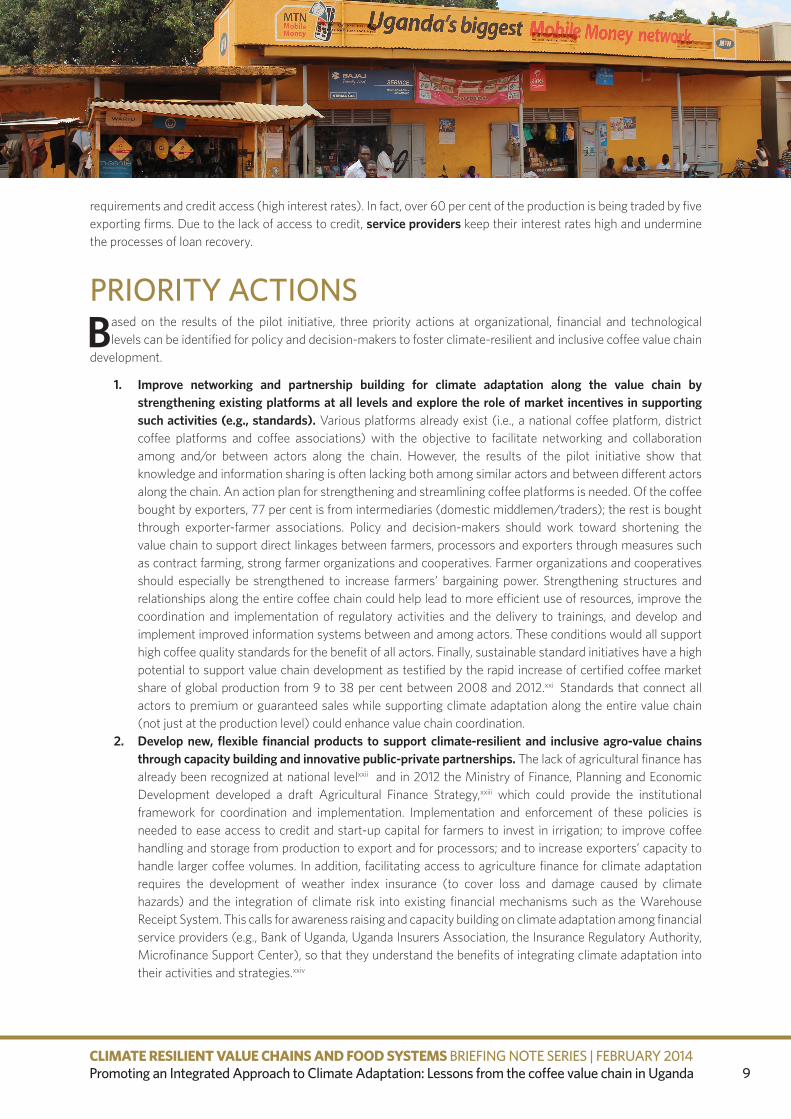

Finding 3: A lack of communication, exchange of information and trust between and among actors along the value chain hampers climate adaptation. All actors along the coffee value chain are highly interdependent, where actions at one level can influence actions at the other levels, as illustrated in Figure 1. The results from the pilot study show that participating actors at different levels of the chain often know little about each other. In general, actors tend to be poorly connected and do not trust each other, which undermines their capacity to respond in a sustainable way to the negative impacts of climate hazards. This is partly because the chain is fragmented with many intermediaries between farmers and exporters. For example, farmers blame input suppliers for the sale of adulterated chemicals and input suppliers complain about the fact that the sale of adulterated chemicals is exacerbated by farmers who systematically work with traders who sell at low prices—mainly as a result of lower incomes from coffee resulting from climate hazards. Exporters perceived the main issue of low-quality coffee as mostly due to poor ethics and lack of discipline on the part of other actors in the value chain. At the end of each CDT process, most participants recognized the need to work together to solve their concerns.

Main response types Examples Loss prevention Farmers modify co�ee farming techniques; processors advance contract

loans to farmers to prevent premature co�ee sales. Sharing or transferring the losses to other actors of the chains

Input suppliers transmit risks to the farmers by selling improper inputs; exporters transfer the risk to actors in the lower stages by o�ering lower prices for lower quality co�ee; insurers increase premiums.

Capacity building and awareness raising

Some exporters support the adoption of good agricultural practices among farmers and the development of drought-resistant co�ee varieties in partnership with research institutes.

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 8

Figure 1: Simplified drought impact chain along the coffee value chain in Uganda

Finding 4: Agriculture financing is a cross-cutting gap for all actors along the chain. The limited access to agriculture finance is perceived as a key barrier by all participating coffee value chain actors and exacerbates the adverse impacts of climate hazards. Despite the decreasing share of the agriculture sector to the country’s GDP, 73 per cent of the population continues to be employed in the agriculture sectorxvi —a trend that is projected to remain in the near future.xvii However, agriculture financing—that is to say, the financing of any agriculture-related activity ranging from production to marketing through savings, credit, insurance and leasingxviii—remains limited. In fact, total agriculture lending by regulated financial institutions and microfinance deposit-taking institutions declined by 21.6 per cent between 2007 and 2010.xix Insurance for crop production is still limited.xx

When farmers experience reduced income due to reduced yields, they tend to buy cheaper inputs and fall into the trap of low quality, low efficacy and further reduction in yields and income. The loans usually have prohibitively high interest rates (between 12 to 36 per cent). Farmers generally register low savings and low loan repayments, which accentuate the negative impacts of climate hazards on their activities. Processors are often constrained by a lack of start-up capital and insurance to cover loss and damage on their infrastructures from climate hazards and high interest rates charged on loans. Few national exporters are involved in coffee marketing due to a lack of initial capital

Drought

Reduced co�eeyield and quality

Increase in pests anddiseases [farmers]

Lower electricitygeneration due to

lower water levels in Lake Victoria

Increased poweroutage

[processors]

Increase inprocessing costs

[processors]Deterioration of

processing equipments[processors]

Reduced income[all actors]

Lower adoption offarm inputs and

increased demandfor cheaper inputs

[farmers]

Pemature co�eeharvesting to get

rapid cash [farmers]

Low loan recoveryrate [farmers]

Increase defaults oninputs bought oncredits [farmers]

Increase of theftamong communities

[farmers]

Distrust betweenfarmers and traders

Distrust amongfarmers

Distrust betweenfarmers and

finance serviceproviders

Distrust betweenfarmers and

processors andexporters

Distrust betweenfarmers and

inputs suppliers

Proliferation ofadultered inputs on

the market[input suppliers]

Adulteration ofco�ee [farmers;

traders]

Reduced marketabilityand competitiveness

[farmers; traders; exporters];damage to the reputation

of Ugandan co�ee[exporters]

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 9

requirements and credit access (high interest rates). In fact, over 60 per cent of the production is being traded by five exporting firms. Due to the lack of access to credit, service providers keep their interest rates high and undermine the processes of loan recovery.

PRIORITY ACTIONS Based on the results of the pilot initiative, three priority actions at organizational, financial and technological

levels can be identified for policy and decision-makers to foster climate-resilient and inclusive coffee value chain development.

1. Improve networking and partnership building for climate adaptation along the value chain by strengthening existing platforms at all levels and explore the role of market incentives in supporting such activities (e.g., standards). Various platforms already exist (i.e., a national coffee platform, district coffee platforms and coffee associations) with the objective to facilitate networking and collaboration among and/or between actors along the chain. However, the results of the pilot initiative show that knowledge and information sharing is often lacking both among similar actors and between different actors along the chain. An action plan for strengthening and streamlining coffee platforms is needed. Of the coffee bought by exporters, 77 per cent is from intermediaries (domestic middlemen/traders); the rest is bought through exporter-farmer associations. Policy and decision-makers should work toward shortening the value chain to support direct linkages between farmers, processors and exporters through measures such as contract farming, strong farmer organizations and cooperatives. Farmer organizations and cooperatives should especially be strengthened to increase farmers’ bargaining power. Strengthening structures and relationships along the entire coffee chain could help lead to more efficient use of resources, improve the coordination and implementation of regulatory activities and the delivery to trainings, and develop and implement improved information systems between and among actors. These conditions would all support high coffee quality standards for the benefit of all actors. Finally, sustainable standard initiatives have a high potential to support value chain development as testified by the rapid increase of certified coffee market share of global production from 9 to 38 per cent between 2008 and 2012.xxi Standards that connect all actors to premium or guaranteed sales while supporting climate adaptation along the entire value chain (not just at the production level) could enhance value chain coordination.

2. Develop new, flexible financial products to support climate-resilient and inclusive agro-value chains through capacity building and innovative public-private partnerships. The lack of agricultural finance has already been recognized at national levelxxii and in 2012 the Ministry of Finance, Planning and Economic Development developed a draft Agricultural Finance Strategy,xxiii which could provide the institutional framework for coordination and implementation. Implementation and enforcement of these policies is needed to ease access to credit and start-up capital for farmers to invest in irrigation; to improve coffee handling and storage from production to export and for processors; and to increase exporters’ capacity to handle larger coffee volumes. In addition, facilitating access to agriculture finance for climate adaptation requires the development of weather index insurance (to cover loss and damage caused by climate hazards) and the integration of climate risk into existing financial mechanisms such as the Warehouse Receipt System. This calls for awareness raising and capacity building on climate adaptation among financial service providers (e.g., Bank of Uganda, Uganda Insurers Association, the Insurance Regulatory Authority, Microfinance Support Center), so that they understand the benefits of integrating climate adaptation into their activities and strategies.xxiv

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 10

3. Investing in climate-resilient infrastructures such as roads, irrigation systems, storage facilities and telecommunications should remain a top priority to support agro-value chain development and build productive capacities in a changing climate. Improving infrastructures to support all the coffee value chain actors and especially the rural coffee growers has already been identified as a priority action in the national export strategy for the coffee sector 2012–2017.xxv For example, the lack of irrigation makes the coffee supply susceptible to drought; heavy rains affect coffee transportation by destroying roads and bridges and increasing the beans’ moisture content during transportation. These impacts can contribute to reductions in the farmers’ yields and access to markets and service provisions, increases in the prices of inputs and decreases in the prices of outputs, which culminate in reduced incomes. However, any sustainable investment in physical infrastructures should ensure that the location, the composition and the design of the infrastructures, among other characteristics, account for the expected increase in frequency and intensity of climate hazards or any potential new climate hazards due to climate change.

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 11

ENDNOTES iUnited Nations Conference on Trade and Development. (2011). Commodities and development report. Overview. Perennial problems, new

challenges and evolving perspectives. Geneva: United Nations. iiSmith, T.M. (2013). Climate change: Corporate sustainability in the supply chain. Bulletin of the Atomic Scientists, 69, pp. 43–52. iiiDasaklis, T.K. & Pappis, C. P. (2013). Supply chain management in view of climate change: An overview of possible impacts and road head.

Journal of Industrial Engineering and Management, 6, p. 4. ivJira, C. & Toffel, M. W. (2013). Engaging supply chains in climate change. Manufacturing and Service Operations Management, pp. 1–19;

United Nations Sustainable Development Platform. (2014). Mitigation of climate change through value chain. Retrieved from: http://sustainabledevelopment.un.org/index.php?page=view&type=1006&menu=1348&nr=835.

vJira & Toffel, 2013, ibid. viPauw, P. & Pegels, A. (2013). Private sector engagement in climate adaptation in least developed countries: An exploration. Climate and

Development, 5(4), pp. 257–267. viiStathers, T., Lamboll, R., & Mvumi, B.M. (2013). Postharvest agriculture in changing climates: Its importance to African smallholder

farmers. Food Security, 5, pp. 361–392. viiiUnited Nations Conference on Trade and Development. (2013). The least developed country report 2013: Growth with employment for inclusive

and sustainable development. Geneva: United Nations. ixNational Planning Authority. (2013). Uganda Vision 2040. Accelerating Uganda’s socioeconomic transformation. Kampala: Ministry of Finance,

Planning and Economic Development. xKey strategic trade documents include the Trade Sector Development Plan, the Diagnostic Trade Integrated Study and the National Export

Strategy all of which are under review in 2013/14. xiSee for examples: F.M. DaMatta et al. (2008), Ecophysiology of coffee growth and production. Brazilian Journal Plant Physiology 19(4),

pp. 485–510; United Nations Development Programme, Bureau for Crisis Prevention and Recovery. (2013), Climate risk management for sustainable crop production in Uganda: Rakai and Kapchorwa Districts. New York, NY: UNDP BCPR.

xiiFAOSTAT. (2014). Home. Retrieved from http://faostat.fao.org/site/291/default.aspx xiiiSee for example: United Nations Development Programme, 2013. (Ibid); L. Jassogne, P. Laderach, P. van Asten, (2013), The impact of

climate change on coffee in Uganda: Lessons from a case study in the Rwenzori Mountains. Oxfam Policy and Practice: Climate Change and Resilience, 9(1), pp. 51–66.

xivSee for example, J.R. Eiser, A. Bostrom, I. Burton, D.M. Johnston,J. McClure, D. Paton, et al. (2012). Risk interpretation and Action: A conceptual framework for responses to natural hazards. International Journal of Disaster Risk Reduction, 1, pp. 5–16.

xvFor more information on the CDT approach, refer to: J. Dekens (2013), Building climate resilient agro-value chains in Uganda: Guide for the climate dialogue theatres. Geneva: International Institute for Sustainable Development.

xviUganda Bureau of Statistics. (2013). The Uganda national household survey 2012/2013. Kampala: Government of Uganda. xviiUnited Nations Conference on Trade and Development. (2013). The least developed country report 2013: Growth with employment for inclusive

and sustainable development. Geneva: United Nations. xviiiMinistry of Finance, Planning and Economic Development. (2012). Agricultural finance strategy: Improving policy coordination, farmer

preparedness and innovation in agriculture finance. Draft. Kampala: Government of Uganda. xixMinistry of Agriculture, Animal Husbandry and Fisheries, 2011. National agriculture policy: Final draft. Kampala: Republic of Uganda. xxWorld Bank & International Finance Corporation. (2013). Doing business report 2014. Washington, D.C.: World Bank and IFC. xxiInternational Institute for Sustainable Development. (2014). State of Sustainability Initiatives (SSI) Review, 2014. Retrieved from: http://www.iisd.org/pdf/2014/ssi_2014.pdf xxiiSee, for example: Ministry of Agriculture, Animal Husbandry and Fisheries (2010), Agriculture sector development strategy and investment

plan – 2010/11–2014/15. Agriculture for food and income security; Republic of Uganda (2007), The Uganda national export strategy 2008–2012. Kampala: Ministry of Tourism, Trade and Industry.

xxiiiMinistry of Finance, Planning and Economic Development. (2012). Agricultural finance strategy: Improving policy coordination, farmer preparedness and innovation in agriculture finance. Draft. Kampala: Government of Uganda.

xxivDekens, J. & Bingi, S. (in print). Why the banking sector should support climate resilient and inclusive agro-value chain development: A case of risk management in the coffee value chain in Uganda. Briefing Note Series on Climate Resilient Value Chains. IISD, MoTIC, MAK and CDKN.

xxvInternational Trade Center. (2012). Uganda national export strategy: Coffee sector export strategy update 2012–2017. Geneva: ITC.

© 2012 The International Institute for Sustainable DevelopmentCLIMATE RESILIENT VALUE CHAINS AND FOOD SYSTEMS BRIEFING NOTE SERIES | FEBRUARY 2014Promoting an Integrated Approach to Climate Adaptation: Lessons from the coffee value chain in Uganda 12

ACKNOWLEDGMENTSThis briefing paper was written by Julie Dekens (IISD) and Fredrick Bagamba (MAK). The authors also acknowledge the contribution of Moses Tenywa (MAK), Norman Ojamuge (MoTIC) and Susan Bingi. We also thank Simbisai Zhanje (CDKN), Caroline Spencer (CDKN), Anne Hammill (IISD) and other anonymous reviewers for providing useful comments. The work was funded by the Climate and Development Knowledge Network (CDKN).

For further information, please contact: Julie Dekens, IISD ([email protected]); Fredrick Bagamba, MAK ([email protected]); or Norman Ojamuge, MoTIC ([email protected]). Information about IISD and its work can be found at www.iisd.org.

This document is an output from a project funded by the UK Department for International Development (DFID) and the Netherlands Directorate-General for International Cooperation (DGIS) for the benefit of developing countries. However, the views expressed and information contained in it are not necessarily those of or endorsed by DFID or DGIS, who can accept no responsibility for such views or information or for any reliance placed on them.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, the entities managing the delivery of the Climate and Development Knowledge Network do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Management of the delivery of CDKN is undertaken by Pricewaterhouse Coopers LLP, and an alliance of organisations including Fundación Futuro Latinoamericano, INTRAC, LEAD International, the Overseas Development Institute, and SouthSouthNorth.

© 2014 Climate and Development Knowledge Network

Photo credits: Photo on page 7 - Martha Mbosa. All other photos - Julie Dekens