value chain analysis of fisheries sector for rodrigues

85

VALUE CHAIN ANALYSIS OF FISHERIES SECTOR FOR RODRIGUES June 2012 REPORT/RAPPORT : SF/2012/18 European Union Funded by

Transcript of value chain analysis of fisheries sector for rodrigues

VALUE CHAIN ANALYSIS OFFISHERIES SECTOR FOR RODRIGUES

June 2012

REPORT/RAPPORT : SF/2012/18

EuropeanUnion

Funded by

Implementation of a Regional Fisheries Stategy For The Eastern-Southern Africa And Indian Ocean Region

10th European Development FundAgreement No: RSO/FED/2009/021-330

“This publication has been produced with the assistance of the European Union. The contents of this publication are the sole responsibility of the author and can in no way be taken to the views of the European Union.”

Implementation of a Regional Fisheries StrategyFor The Eastern-Southern Africa and India Ocean Region

Programme pour la mise en oeuvre d'une stratégie de pêche pour laregion Afrique orientale-australe et Océan indien

Value Chain Analysisof Fisheries Sector

For RodriguesSF/2012/18

Soobaschand Sweenarain

EuropeanUnion

Funded by

Implementation of a Regional Fisheries Stategy For The Eastern-Southern Africa And Indian Ocean Region

10th European Development FundAgreement No: RSO/FED/2009/021-330

“This publication has been produced with the assistance of the European Union. The contents of this publication are the sole responsibility of the author and can in no way be taken to the views of the European Union.”

Table of content Preface.......................................................................................................................... 5

Acronyms...................................................................................................................... 6

Acknowledgement.............................................................................................................. 8

Summary...................................................................................................................... 10

1. INTRODUCTION............................................................................................................ 24 1.1. Value Chain Assessment............................................................................................. 24

1.2. Rodrigue Island.......................................................................................................... 25

1.3. Methodology.............................................................................................................. 26

2. OVERVIEW OF FISHERIES SECTOR OF RODRIGUES.......................................28

2.1. Fisheries Policies......................................................................................................... 28

2.2. Fisheries Administration............................................................................................. 28

2.3. Recent Studies on the Fisheries Sector........................................................................30

2.4. Fisheries Infrastructure...............................................................................................30

2.4. Supporting Organisationd..........................................................................................30

3. SUPPLY CHAIN ANALYSIS............................................................................ 35

3.1. Key Determinants.......................................................................................................35

3.2. Large Net Fishery........................................................................................................36

3.3. Off-lagoon Hand Line (HL) fishery.............................................................................. 40

3.4. Non Motorised BT and HL fishery............................................................................... 42

3.5. Octopus Fishery.......................................................................................................... 45

3.6. Extended off-lagoon HL (chilled) fishery..................................................................... 48

3.7. FAD Fishery................................................................................................................. 51

4. MARKET STRUCTURES AND MARKETING FUNCTIONS........................................52

4.2. Market Price of Fresh Fish...........................................................................................53

5. VALUE CHAINS..................................................................................................56

5.1. Value Chains of LN fishery......................................................................................... 56

5.2. Value chains of Off-lagoon Hand line fishery............................................................. 57

5.3. Value chains of octopus fishery................................................................................. 58

5.4. Value chains of off lagoon (chilled fishery)............................................................... 59

6. SPORT FISHERY.................................................................................................. 61

7. CONCLUSIONS.................................................................................................. 62

7.1. Production functions.................................................................................................. 62

7.2. Marketing functions............................................................. ..................................... 62

7.3. Processing and value added activities.........................................................................63

8. RECOMMANDATION........................................................................................65

8.1. Policy advocacy...........................................................................................................65

8.2. Development of new extended artisanal (chilled) fisheries......................................... 65

8.3. Promote investment in infrastructure and equipment................................................ 65

8.4. Strengthen financial supports.....................................................................................65

8.5. Strengthen existing value chains.................................................................................65

APPENDX 1................................................................................................................................ 66

APPENDX 2................................................................................................................................ 68

APPENDX 3................................................................................................................................ 69

APPENDX 4................................................................................................................................ 71

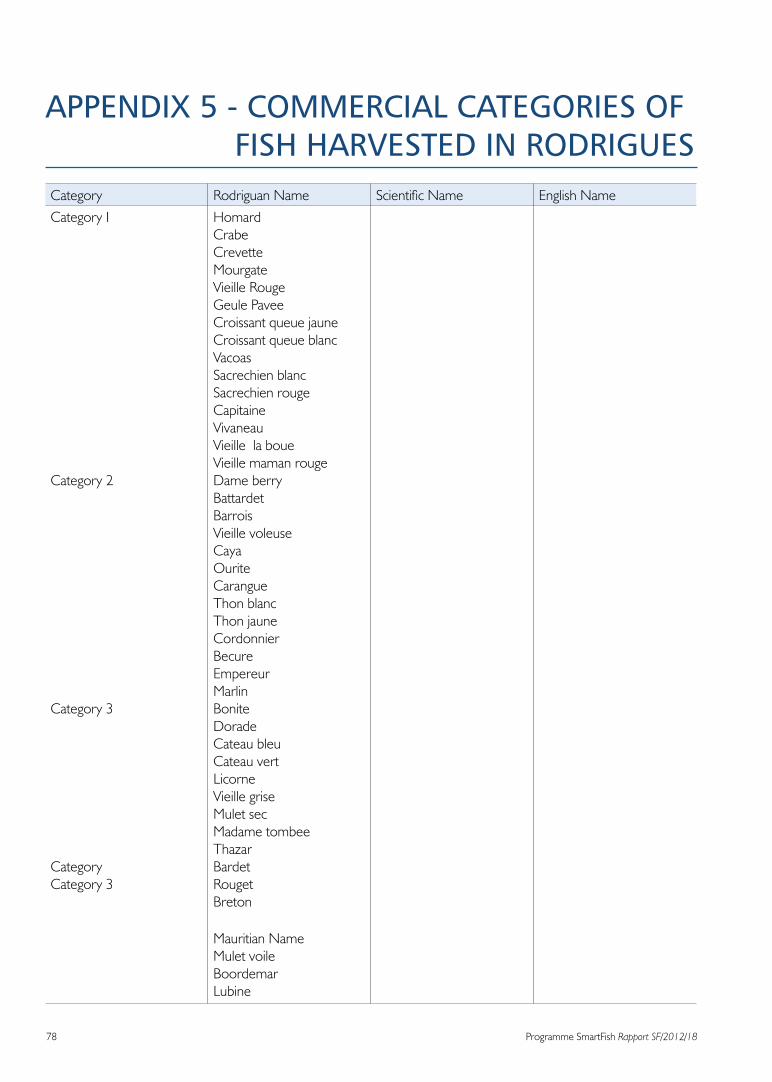

APPENDX 5................................................................................................................................ 77

APPENDX 6................................................................................................................................ 79

APPENDX 7................................................................................................................................ 80

Programme SmartFish Rapport SF/2012/18 7

PREFACE

This Value Chain Analysis for the artisanal fisheries on the island of in Rodrigues complements a report of similar focus, prepared for Mauritius. Within the broader framework of the IOC SmartFish Programme (Implementation of a Regional Fisheries Strategy for ESA-IO programme), under the Regional Trade component, this report has been prepared to assist with a better understanding of the situation in the artisanal fishery from an economic and value perspective. This will allow for objective planning for potential interventions to assist in the move towards a more market driven and sustainable fishery that will enhance and contribute to the growing demand for fish in the country as well as investigate and enhance the ability to export beyond Rodrigues to markets in the region, specifically Mauritius, and Réunion are identified specifically.

This report looks closely at the different types of fishing methods within the artisanal sub-sector, such as the hand-line (motorized and non-motorized) fishery, the basket trap fishery, the large net fishery as well as the on-foot fishery. It provides a detailed analysis of performance in terms of typical business models for each unit and makes assessments of performance with respect to catch potential and capacity /over-capacity vs. stocks. Ultimately the impact on the local fishing communities, as well as the broader issue of increasing demand in the region is addressed and how to re-model and empower the artisanal fishery to better serve the economy, as well as the local population. Recommendations for short-term interventions are made to inform the many stakeholders of what works and what doesn’t work so well and a view to the future for everyone’s benefit.

Regionally, small island artisanal fisheries, as well as regional coastal artisanal fisheries are all dealing with issues of over-capacity and depleted stocks in coastal lagoons, as well as deciding how to ensure future productivity of the sector where local fishers derive a significant part of their livelihoods from fishing. This report will contribute to the regional knowledge in this regard and inform other initiatives to be planned regionally under the SmartFish programme.

Programme SmartFish Rapport SF/2012/188

ACRONYMS

BT Basket TrapBWA Bad Weather AllowanceC A Competent AuthorityCOP Cost of ProductionCPFD Catch Per Fisherman DayCPUE Catch Per Unit EffortCSA Close Season AllowanceCSO Central Statistics OfficeCSP Consumer Sale PriceDBM Development Bank of MauritiusEEZ Exclusive Economic ZoneEPMU Economic Planning and Monitoring Unit ESA – IO East-Southern Africa - Indian OceanEU European UnionFAD Fish Aggregating DeviceFFC Federation of Fishermen CooperativesFLS Fish Landing StationFPS Fisheries Protection ServiceFRTU Fisheries Research and Training UnitHACCP Hazard Analysis and Critical Control PointsHL Hand LineHN Harpoon NetHP Horse PowerICT Information and Communication TechnologyIFAD International Fund for Agricultural DevelopmentIFRS Implementation of Fisheries Regional StrategiesIOC Indian Ocean CommissionKg KilogrammeLFC Local Fisher CommunityLN Large NetMARS Marine and Agricultural Resources SupportMC Marketing CostMCS Monitoring, Control and SurveillanceMID Maurice Ile DurableMM Marketing MarginMOFR Ministry of Fisheries and RodriguesMP Marketing ProfitMRC Mauritius Research CouncilMSY Maximum Sustainable YieldNGO Non-Governmental OrganisationsPM Profit MarginPSP Producer Sale PriceRGF Rodrigues General Fishing Co. Ltd.RRA Rodrigues Regional AssemblyRs Mauritian RupeeSEMPA South East Marine Parks AuthoritySIDPR Sustainable and Integrated Development Plan for RodriguesSME Small & Medium Sized EnterprisesSN Shrimp NetSTE Short Term Expertise

Programme SmartFish Rapport SF/2012/18 9

Mt Metric TonneTC Total CostVAT Value Added TaxVCA Value Chain AnalysisWSP Wholesale Price

Programme SmartFish Rapport SF/2012/1810

ACKNOWLEDGEMENTS

Special thanks to:

• Mr. M. Jeetoo, Officer-in-Charge of the Economic Planning and Monitoring Unit (EPMU) and his staff for their valuable guidance and logistic supports.

• Mr. Sylvio Perrine, Scientific Officer, Fisheries Research and Training Unit (FRTU) and his team of enumerators for

their cooperation during the field works.

• Mr. Edouard J Darkson, Manager and the Members of Board of Rodrigues General Fishing Co. Ltd for providing operational and financial information on their activities

• Mr. Raffaut Renolph, Education Officer, Shoal Rodrigues for his assistance in documentary research on Large Net and octopus fisheries

• All those stakeholders of the fisheries sector who have voluntarily shared information of a private and confidential nature to enable this study to be realized.

Programme SmartFish Rapport SF/2012/18 11

LAYMAN’S SUMMARY

The Value Chain Assessment (VCA) of the fisheries sector for Rodrigues aims at examining the existing value chains and analysing the opportunities and constraints for its future development. Value chains help to maximise revenue flow in the fisheries sector through judicious utilization of scarce resources, processing, value addition, efficient marketing and distribution. In Rodrigues fishing has evolved over time from subsistence to commercial fisheries in an opportunist way in the absence of the basic infrastructural, extension and marketing facilities. Consequently the existing value chains of the local and regional (Mauritian) markets are either marginal or exhausted. Intensive fishing and overcapitalisation in the lagoon has led to the depletion of the sedentary fish stocks and damages to marine ecosystems. Open access, or the inexistence of a management framework, has contributed to impoverishment of local fisher folks. Paradoxically there are significant untapped fish stocks in the off-lagoon and deep-sea areas around the island that can lift up the fisheries sector as a major cluster of the regional economy. It is recommended to chart out an integrated action plan to marshal the development of extended artisanal and small scale fisheries with due emphasis on export oriented value chains.

RÉSUMÉ DES NON-INITIÉS

L’analyse des chaînes de valeur du secteur de la pêche de Rodrigues vise à examiner les chaînes de valeur existantes et d’évaluer les perspectives ainsi que les contraintes pour son développement futur. Les chaînes de valeur aident à optimiser les flux de revenus des produits de la mer grâce à une meilleure utilisation des ressources rares, la valorisation, et de commercialisation. A Rodrigues, le secteur de la pêche a évolué au fil du temps de façon opportuniste, en absence des infrastructures de base et des structures de marché. Par conséquent, les chaînes de valeur existantes tant sur les marchés locaux qu’à l’export (mauricien) sont aléatoires ou épuisées. La pêche intensive et des surinvestissements dans la petite pêche ont conduit à l’épuisement des stocks de poissons sédentaires dans le lagon et des dégâts importants aux écosystèmes marins. Le libre accès ou l’inexistence du cadre de gestion a contribué à l’appauvrissement des communautés des pêcheurs. Cependant, il existe des stocks de poissons encore sous-exploité au large du lagon et en haute mer autour de l’île ce qui peut hausser le secteur de la pêche comme un pilier de l’économie régionale. Il est recommandé d’élaborer un plan d’action intégré pour agencer le développement d’une pêcherie intermédiaire orientée vers les chaînes de valeur à l’export.

EXECUTIVE SUMMARY

The Value Chain Assessment (VCA) of the fisheries sector for Rodrigues Island is sponsored by the Implementation of a Regional Fisheries Strategies for the Eastern South Africa and Indian Ocean SmartFish Programme (IRFS ESA-OI) under the aegis of the Indian Ocean Commission (IOC) and funded by the European Fund. It is a step forward in the fine-tuning and implementation of the Sustainable and Integrated Development Plan for Rodrigues (SIDPR), 2009 by the Fisheries Commission of the Rodrigues Regional Assembly (RRA), which is within the framework of the new Fisheries Master Plan and the Mauritius Ile Durable (MID) project of the Central Government. A VCA of the small scale or artisanal fisheries requires a business oriented approach whereby the various components of the value chain - fishing, processing and marketing are viewed as enterprises or cost centres. Although in-bound and out-bound logistics are external factors of a value chain, they are of critical importance for the efficiency of the core activities.

Programme SmartFish Rapport SF/2012/1812

Production

Formally the fisheries sector of Rodrigues comprises 1,410 registered fishers and 1,821 fishing boats while the total fish production is approximately 1,600 Mt. The gross annual revenue generated by the various types of fishing activities (excluding the sport fishery) is estimated at Rs 174 Million on the basis of a mean producer sale price of Rs 109/ kg. It represents an annual income of Rs 123,688 per registered fisher (Rs 10,307 per month). The tendency to err on the side of short term economic needs of fishers instead of long term conservation or sustainability has led to further overexploitation and depletion of the coastal fishery resources. There must be no compromise whatsoever on doing away with open access/common property rights and laissez faire in coastal marine fisheries.

Chart 1: Total Catch 1997 - 2010 in metric tonnes

Given that a fishing boat carries 3 to 4 fishing crew, there are potentially 5,823 active fishers (including 330 on-foot fishers mostly fisherwomen) in the sector. Therefore the net annual income of a fisher operating in the lagoon can fall as low as Rs 29,950, meaning that approximately Rs 132 million (75 %) of the gross income does not benefit the registered fishers.

An additional production of approximately 3,200 Mt of fresh fish would be necessary to accommodate 5,823 fishers with a mean annual income of Rs 90,000 on the basis of a minimum household income of Rs 7,500 per month. Fisheries expansion is plausible off-lagoon and high seas around Rodrigues. It is indicated that 70% of highs seas fish resources in the Western Indian Ocean are unknown or unexplored. The FAD fishery can potentially yield 1000 Mt of tuna and large pelagics annually on the basis of 60 Mt per FAD (Lojac H’meur, 1989 and C. Roullot, 1991). It is proposed to chart out a performance based fisheries development plan with a targeted increase in marine fish production of 5,000 Mt in the short and medium terms. Development initiatives of RGF off-lagoon HL fishing fleet and the IFAD-MARS extended artisanal fishing fleet have to be supported by an enabling environment at all levels.

Fisheries statistics are not reliable due to an out-dated sampling, data collection and processing system in addition to a shortage of human and technical resources at the FRTU. Apparently the actual production is much higher, since the 2005 Annual Fisheries Bulletin has not been published. Administrative records maintained by the FPS on registered fishers, fishing boats and fishmongers have to be consolidated into a computerised data-base that can be useful for fisheries management purposes.

Programme SmartFish Rapport SF/2012/18 13

Marketing

In marketing, raw fish is considered as a non-branded fast moving consumer product. Traditional fishing enterprises just sell their catch and do not “market” them. They must be trained in marketing to increase their revenue and to obtain a fair share of the value added in the supply chain.

The flow of market information is essential to promote a fair and transparent market mechanism. An increase in supply of raw fish may depress prices on the local markets due to the limited purchasing power of consumers. To enhance value chains of fresh/chilled fish it is important to develop export markets. Effective demand for high quality chilled fish in Mauritius arises from local markets for direct consumption and from the seafood hub’s processing for re-export. Two major hurdles have to be removed in order to link local chilled fish value chains in Rodrigue to the Mauritian seafood hub, namely cost effective transportation (sea and air) logistics and compliance to international sanitary and health standards and HACCP alignment. Reunion Island can also be targeted as a prospective market for raw fish and fish products.

Marketing infrastructure is virtually non-existent on the island. Raw fish is sold on the beach (at fish landing stations (FLS)) or on the roadside. There are no sheltered FLS that can be used for handling, sorting and grading of fish prior to sale. Simply by improving the landing facilities (better sorting and grading of raw fish by commercial category) can increase the revenue of a fishing enterprise by 5 to 10%.

Market Price by Product Segment - Year 2011 ( Rs/Kg) which chart2

Programme SmartFish Rapport SF/2012/1814

Existing FLS have to be renovated and operationalized at the earliest in close collaboration with the Local Fisher Communities (LFC). More FLS have to be set up in major fishing villages.

The supply chain of fresh fish is short and geographically limited because the product is highly perishable. To extend the shelf life of the product it is crucial to enforce adequate handling and preservation practices along the supply chain. The use of isotherm boxes, flexible containers and ice flakes is necessary to enhance the value chain of high value fish species on local and export markets. The implementation of world class food safety, quality and traceability standards in the seafood sector is a pre-condition for export oriented market development.

Chilled fish value chains are economically more attractive for artisanal and semi-industrial fisheries of insular states as compared to frozen raw fish. For instance the difference between consumer prices of chilled and frozen fish is approximately 2:1. Efficient downstream logistics have to be developed. A refrigerated supply chain is more appropriate for industrial or large scale fisheries due to its high initial investments. In the artisanal fisheries, refrigeration is rather a means of preservation of last recourse for unsold fish. A local practice of using domestic refrigerators or cold rooms to store fresh fish is hazardous to public health. An extension of the Competent Authority in Rodrigues will be necessary for capacity building in world class food safety, quality standards and HACCP alignment in the local seafood sector.

Marketing Channel Flow Chart

1st Grade Fish

Other Grades Fish

(LN, BT/HL)

Octopus Collectors Process/Exporters

Cottage Processors

Fish Traders

Fish Hawkers

Fish Markets

Hotels & Restaurants

End Consumers

Export to Mauritius

Programme SmartFish Rapport SF/2012/18 15

Processing and Value added activities.

Value chains in processing and value added operations in the fisheries sector are minimized for the following reasons:

i) Scarce supply of raw fish; ii) Inadequate technical and financial support; iii) Absence of handling and preservation practices for raw fish; iv) Non-compliance with international sanitary and health standards and to HACCP;v) Restricted markets: local consumers and visitors; vi) Lack of fisheries infrastructure such as FLS, ice-flake plants, etc.; vii) Absence of out-bound logistics for export of chilled products;viii) Lack of entrepreneurial and management skills.

A few examples of value added (chilled) fish products are given below:

• Value added (vacuum packed) fish fillet / loin, cubes, slices, whole and gutted;• • Semi processed fish ball, burgers, sausages and paste;• • Ready-to-cook marinated, smoked, pre-cooked (traditional recipes), pickles.

Value Chain of Chilled FishActual

Fishing Units(6 fishing boats)

Fishing Units(6 fishing boats)

Fish TerminalSorting /grading

Cleaning / packaging

Ice flakes &Containers

Processing UnitValue added

Products(HACCP aligned)

Ice FlakeUnit [500kg/day]

Processing[Cleaning, Gutting,

Slicing, packing]

Cold Storage[Blast Freezer,

Cold & Chill Room]

MarketingFishmongers

End Consumers

Exports to MRU

Local Markets

Export MarketsMauritius / Reunion

(Re-exports)

Octopus Collector – cum –Exporter

Programme SmartFish Rapport SF/2012/1816

From the above, it can be concluded that the fisheries sector can be improved as the driving force of the local economy such as in the small island states of Seychelles, Maldives, Hawaii or Finland. There should be an ambitious and performance oriented development and management plan to resolve the problem of conservation of the lagoon ecosystems, marshal a concerted action plan to develop export-oriented small scale and extended chilled fisheries in the off-lagoon and high-seas around the island.

The existing extension services must be upgraded to provide adequate support to stakeholders in product development, fish handling and preservation of fish, up-grading of existing fishing boats, demonstration of new fishing techniques, exploration of new off-lagoon fisheries, entrepreneurial skills in fishing, processing, marketing, business management skills, project facilitation and mentoring.

Local leadership and community based management capabilities have to be developed in LFCs to ascertain their active participation in voluntary compliance to Monitoring, Control and Surveillance (MCS) of coastal fisheries, fish handling and preservation practices, shared management of fisheries infrastructure.

There is a strong political determination to create an enabling business environment in Rodrigues. These efforts have to be seen in the fisheries sector through the development of crucial infrastructure facilities such as FLS, an integrated fishing terminal, export logistics for chilled fish and fish products, promotion of export market development, private local and foreign investments, joint venture, strategic alliances and domestication of foreign fishing and processing companies.

Programme SmartFish Rapport SF/2012/18 17

Recommendation

1. Policy advocacy:

i) To establish coastal fisheries management to encompass effective monitoring, control and surveillance (MCS) measures.

ii) To enforce food safety and quality practices for fish and fish products sold on the local markets and for exports.

iii) To regulate and monitor the activities of amateur, leisure and game fishers (including on-foot fishers) in the coastal fishing zones.

2. Development of extended artisanal (chilled) fisheries: FAD and open-sea tuna, tuna-like and large pelagic fisheries and Deep-sea demersal fishery

i) Direct Investment, transfer of technology, technical assistance

ii) Motorization of traditional crafts, use of more efficient fishing techniques, fish prediction data, application of GIS and remote sensing etc.

iii) Extension and facilitation services: training, re-skilling and mentoring

iv) Transfer of technology and capacity building in quality assurance

v) Fisheries exploration and testing of more efficient fishing technologies.

3. Promote Investment in Infrastructure and Equipment

i) Air-freight logistics to enable export of chilled fish products

ii) Fishing Landing Station (FLS) and fish markets in major regional fishing centres

iii) Integrated fishing port, ice flake machinery, isotherm/cool room

4. Strengthen Financial Supports

i) Suitable loan for asset and working capital finance for fisher folk, artisanal processors and traders;

ii) Promote banking and saving culture

iii) Provide financial literacy, entrepreneurial skills (pricing and costing) and business management.

5. Strengthen existing value chains

i) (Strategic alliance / partnership) Partial processing of local catch and final processing in other markets

ii) Second and third cycle of processing activities (ready-to-cook and ready to eat products)

iii) Product Research and Development

iv) Opening of export markets

v) Marketing Intelligence to obtain real time market information.

Programme SmartFish Rapport SF/2012/1818

RÉSUMÉ EXECUTIF

Cette étude des filières du secteur de la pêche de Rodrigues est mise en oeuvre par le programme « Implementation de Stratégies des Pêches pour les pays sud-est Africains et l’océan Indien », communément appelé « SmartFish » sous les auspices de la Commission de l’océan Indien et financé par l’Union Européenne. Elle est un pas en avant vers l’adaptation du secteur de pêche au Plan de Développment Soutenu et Intégré de Rodrigues, 2009 par la Commission des pêches et l’Assembée Régionale de Rodrigues aussi bien qu’elle s’insère au Plan Directeur des pêches et le projet Maurice – Ile Durable (MID) du governement central.

L’analyse des filières dans le secteur de la pêche implique une approche d’entreprenariat comprenant des différentes composantes de la filière de l’amont en aval – pêche, transformation/valorisation, et la commercialisation comme des activités économiques à part entière. Bien que les logistiques - en amont et en aval - sont considérés comme des facteurs externes de la chaîne de valeurs, ils jouent un rôle important dans la compétitivité des activités primaires.

Production

Officiellement le secteur des pêches de Rodrigues comprend 1410 pêcheurs professionnels et 1821 pirogues de pêche alors que les captures annuelles sont estimées à 1600 tonnes. Le revenu global généré par les différentes activités de pêche (excluant la pêche sportive) s’élève à 174 million de roupies moyennant un prix de 109 roupies le kilo à la première vente. Ceci représente un revenu moyen de 123, 688 roupies par an par pêcheur professionnel soit 10,307 roupies par mois. Le choix de focaliser sur les gains à court terme au lieu d’une exploitation à long terme et durable a mené à l’épuisement des ressources halieutiques et à la dégradation de l’écosystème marin. Il ne devrait pas avoir un compromis pour se défaire l’approche de libre accès or une politique de laissez-faire dans le secteur de la pêche locale.

Tableau 1: Captures totale - 1997 - 2010 en tonnes

Programme SmartFish Rapport SF/2012/18 19

Sachant qu’une embarcation de pêche emploie de 3 à 4 pêcheurs, Il aurait potentiellement environ 5,823 pêcheurs actifs (incluant 330 pêcheurs à pieds qui sont principalement des femmes pêcheurs) dans le secteur. De ce fait, le revenu annuel par pêcheur en activité dans la pêcherie peut baisser jusqu’à 29,950 roupies, c›est-à-dire que plus de 132 million de roupies, soit 75 % du revenu du secteur de la pêche ne profite pas directement les pêcheurs professionnels.

Autrement, il faudrait une production additionnelle d’environ 3,200 tonnes pour assurer un revenu décent aux 5,823 pêcheurs actifs sur la base d’un revenu moyen de 90,000 roupies par an soit 7,500 roupies par mois. L’expansion des pêcheries hors-lagon et en haute mer autour de Rodrigues est plausible. Plus de 70% des ressources en haute mer dans l’océan Indien occidental est encore méconnu et sous-exploité. Le réseau de DCP déployé au tour de Rodrigues peut produire 1000 tonnes de gros pélagique par an soit 60 tonnes par DCP (Lojac’Hmeur , 1989 et Roulet 1991). Donc, il est proposé d’élaborer un plan de développement de la hauturière pour augmenter la production de poisson de 5,000 tonnes à court et moyen termes. Les initiatives de société étatique « Rodrigues General Fishing Co. Ltd » et le projet IFAD -MARS pour le développement d’une pêcherie intermédiaires se cadrent bien dans cette nouvelle vision et doivent être soutenues par un environnement macroéconomique adéquat.

Les statistiques de pêche ne sont pas fiables et le système d’échantillonnage, de collecte et de traitement est dépassé ainsi les ressources humaines et techniques de la FRTU sont inadéquates. Il est certain que les captures réelles sont nettement supérieures que préconisent les statistiques de pêche. Les statistiques de pêche ne sont pas publiées depuis 2005. Aussi les données administratives recueillies par le Service de Protection sur les pêcheurs professionnels, les embarcations de pêche, les vendeurs de poisson doivent être consolidées en une base de données aux fins de gestion de la pêcherie.

La commercialisation

Le poisson frais est un produit « basic » qui se vend bien. Les pêcheurs traditionnels ne se préoccupent pas pour la vente de leurs captures et ne font aucun effort de marketing. Ils doivent être sensibilisés et formés pour mieux valoriser et commercialiser des produits de la pêche en vue d’accroître leurs revenus tout en assurant une distribution équitable des valeurs entre les différents acteurs de la filière. La diffusion des informations commerciales sur les produits de la pêche est essentielle pour assurer des transactions justes et transparentes. Une hausse de production de poisson peut faire chutée le prix sur les dans le secteur du «Seafood Hub». Deux obstacles majeurs devront être surmontés pour connecter la filière de pêche rodriguaise au secteur du «Seafood Hub» de Maurice notamment, efficience du fret (maritime et aérien) et le respect des normes sanitaires et d’hygiène. La Réunion marchés locaux à cause du pouvoir d’achat limité des consommateurs. Il est impératif de développer des exportations si on tient à valoriser les produits de la pêche. Il existe une demande croissante des poissons de qualité pour la consommation directe sur les mauriciens mais aussi pour la transformation peut aussi bien s’intéressée les produits de la pêche de Rodrigues. Les infrastructures à terre sont quasiment inexistantes. Le poisson est vendu aux débarcadères ou au bord de la route. Il n’y a pas des endroits abrités pour travailler – le tri par espèce et par taille, le lavage - avant la commercialisation vente. Simplement en améliorant le traitement à terre, il est possible d’augmenter le revenu à la première vente de 5 à 10 %.

Programme SmartFish Rapport SF/2012/1820

Tableau 2 : Prix par catégorie commerciale de poisson - 2011 ( Rs / kilo)

Les débarcadères existants doivent être rénovés et mis en opération en collaboration avec les organisations des pêcheurs les plus vite. D’autres débarcadères devront être aménagés dans les principaux centres de pêche. Le circuit commercial des produits de la pêche est court et limité géographiquement parce que ce dernier est hautement périssable. Pour mieux préserver ces produits on devra utiliser des caisses isothermes et des paillettes de glace pour tout le long de la chaîne de distribution. Ceci est également un impératif pour la valorisation des produits de la pêche. Le respect des normes sanitaires et de qualité et traçabilité internationales est la basse pour le développement des marchés à l’export.

Le développement des filières « fraîches » dans les pêcheries artisanales et intermédiaires est économiquement plus attrayant pour les petits états insulaires par rapports aux filières «surgelées». Par exemple le prix à la consommation du poisson frais est presque le double que le surgelé. Cependant, il est important de développer des logistiques appropriés au long de la chaîne de distribution. La filière surgelée est plus approprié à la pêche industrielle qui manipule des volumes relativement plus conséquents. L’usage de congélation dans la pêcherie artisanale est principalement un moyen de préservation du dernier recours pour les invendus. Pour des raisons sanitaires et la protection de la santé publique, il est interdit de commercialiser du poisson préservé dans des congélateurs domestiques comme du poisson frais. Il serait bien de créer une antenne de l’Autorité Compétente à Rodrigues afin de développer des capacités locales dans mise en œuvre des normes sanitaires et de qualité internationales dans le secteur de la pêche.

Programme SmartFish Rapport SF/2012/18 21

Filières commerciales des produits de la pêche locale

Transformation et la valorisation des produits de la pêche

La valorisation des produits de la pêche à Rodrigues est marginalisée pour les raisons suivantes: i) Pénurie de poisson (carence de l’offre); ii) Manque de moyens techniques et financiers; iii) Absence de la bonne pratique des normes sanitaires et d’hygiènes ;iv) Inexistence des normes sanitaires et de qualité internationales ;v) Marchés locaux restreints (limités aux consommateurs locaux et visiteurs étrangers) ;vi) Manque d’infrastructures macroéconomiques et des débarcadères aménagés ; vii) Manque de logistique approprié pour l’export des produits frais ;viii) Manque d’initiative des opérateurs économiques.

Quelques exemples des produits frais de pêche à valeur ajoutée

• Emballage sous vide du poisson avec ou sans tête éviscéré, des filets, des tranches, des cubes ;

• Produits prêt à cuire : boulette de poisson, burgers, saucisses, patte de poisson ;

• Filets et/ou tranches marinés aux épices locaux ; poisson fumé, des recettes traditionnelles.

Poisson de Grade 1

Poissons DiversCasiers, Sennes..

Ourites Collecteurs ExportateursTraitement

Cottage Processors

Intermédiaires

VendeursAmbulants

Poissonneries

Hôtels & Restaurants

Consammateurs

Exports/Maurice

Programme SmartFish Rapport SF/2012/1822

La filière locale de poisson frais (sous glace)

Actuel

Potentiels

De ce qui précède, on peut conclure que le secteur de la pêche peut contribuer davantage au développement socio-économique de Rodrigues comme dans le case des autres petits états insulaires à l’instar des Seychelles, Maldives, Hawaii ou la Finlande. Pour ce faire il faudra mettre en place un plan d’action ambitieux axé sur le développement durable des pêcheries intermédiaires hauturières en mettant en exergue la valorisation et l’exportation des produits de la pêche de qualité.

Les services d’appuis au secteur de la pêche devront s’adapter aux besoins réels des acteurs de la filière dans les domaines suivant: le traitement et la préservation post capture, l’amélioration des pratiques de pêche, l’exploration des nouvelles pêcheries hors-lagon, la formation en gestion d’entreprise de pêche, la transformation des produits de la pêche. Désormais ils devront agir comme des facilitateurs aux opérateurs économiques du secteur.

Il est important de promouvoir le sens de leadership et la responsabilisation des communautés des pêcheurs afin qu’elles puissent participer activement dans le contrôle, la gestion et la surveillance de leurs zones de pêche et la gestion des infrastructures de pêche à terre en accord avec les autorités locales.

Il existe une volonté politique pour créer un environnement macroéconomique adéquat pour dynamiser l’économie locale. Dans le secteur de la pêche, ces efforts devront être perçus dans la mise en place dans le développement des infrastructures de pêche appropriées dans les principaux centres de production ; un complexe de pêche au port pour entreprendre la transformation, le conditionnement et le stockage des produits de pêche destinés à l’export; attirer des investissements locaux et étrangers ; proposer des joint-ventures aux entreprises de pêche, de transbordement, et de transformation étrangères pour s’implanter à Rodrigues.

Production[6 bat. de pêche]

Production[6 bat de pêches]

+Autres bateaux

Maison des PêcheursPointe Monier

TraitementprimaireTri/ gradage/ lavage

Machine à glaceConteneur réfrigéré

TransformationValeur ajoutéeBonne pratique

d’Hygiène)

March à glace[500 Kg/jr]

Transformation[Evisceration

Lavage, Emballage)

StockageChambre Froide

Blast Freezer Cold & Chill

VentePoisonneries Détaillants

Consommateurs

Exports to MRU

Marches locaux

ExportsMauritius / Réunion

(Re-exports)

Collecteur / Exportateurs - Ourites

Programme SmartFish Rapport SF/2012/18 23

7.4. Recommandations

1. Encadrement institutionel

iv) Pour la mise en œuvre d’un programme de suivi, de contrôle et de gestion de la pêche côtière. ii) Pour l’application des normes sanitaires et les bonnes pratiques d’hygiène pour le traitement, le stockage et la commercialisation des produit frais de la pêche.

iii) la réglementation des activités de la pêche plaisancière (amateurs / non-professionnels) et sportives dans les zones côtières

2. Promouvoir le développement d’une pêcherie intermédiaire axée sur les gros pélagiques au tour des DCP et les poissons de fond sur le bancs au large.

vi) Attirer des investissements, le transfert de technologies et l’assistance technique ;

vii) La motorisation des embarcations de pêche et la vulgarisation des techniques de pêches appropriées, l’usage des technologies de pointe dans la recherche des bancs de poissons;

iii) La formation et/ou le redéploiement des pêcheurs professionnels

iv) Transfert de technologies en matière de traitement, la valorisation les respects des normes sanitaires et de qualité ; v) L’exploration des nouvelles pêcheries et l’essai de nouvelles techniques de pêche

3. Renforcement des infrastructures et des logistiques

i) Le fret aérien pour l’exportation des produits de la pêche vers Maurice.

ii) Des complexes de pêche dans les principaux centres de production de l’ile.

iii) Un port de pêche équipé en vue de consolider le développement de l’industrie de la pêche et le concept de Seafood Hub à l’instar de Maurice.

4. Financement adapté

iv) Des prêts / crédits adaptés pour le financement des équipements et le fond de roulement des activités de pêche hors-lagon, de transformation et de commercialisation.

v) Développer une culture bancaire et d’épargne parmi les acteurs de la pêche pour les rendre plus accessible aux sources de financement formel.

vi) Formation dans la gestion financière d’une entreprise – le plan de financement, la trésorerie, le revenu, les frais fixes et variable etc…

Programme SmartFish Rapport SF/2012/1824

5. Renforcement des filières existantes

i) Exportation des produits partiellement transformés pour subir la transformation finale sur place. (Par exemple, un accord commercial un transformateur dans le Seafood Hub à Maurice)

ii) Fabriquer les produits transformés (prêt-à-cuisiner et prêt-à-manger ) pour le marchés spécifiques ( niches : hôtels/ restaurants/ traiteurs) ?

iii) Recherche et Développement des produits et des marchés à travers les institutions nationales telles que le FiTEC, Entreprise Mauritius, les Fédération des Cooperatives …

iv) Ouverture vers de nouveaux marchés – exhibition dans les foires internationales et régionales, partenariat stratégiques avec des gros importateurs / distributeurs.

v) Création d’un système d’information sur les marchés ciblés des produits de pêche . (Intelligence en marketing)

25Programme SmartFish Rapport SF/2012/18

1.0 Introduction1.1 Value Chain Assessment

The Value Chain Assessment (VCA) of the fisheries sector for Rodrigues Island is sponsored by the Implementation of Regional Fisheries Strategies for the Eastern South Africa and Indian Ocean SmartFish Programme (IRFS ESA-IO) under the aegis of the Indian Ocean Commission (IOC) and funded by the European Fund (EU). It is a step forward in the fine-tuning and implementation of the Sustainable and Integrated Development Plan for Rodrigues (SIDPR), 2009 by the Fisheries Commission of the Rodrigues Regional Assembly (RRA), which is within the framework of the new Fisheries Master Plan and the Mauritius Ile Durable (MID) project of the Central Government.

This study1 has been highlighted in the Budget Speech 2012 - “Take-Off towards Sustainable Modernisation of Rodrigues” 2 of the Regional Government. It looks into the operating value chains of the fisheries sector and explores new opportunities and constraints in the dynamic environment of fish trade with a national and global perspective as an implicit strategy to enhance socio-economic benefits from judicious utilization of scarce fish stocks. A synopsis of the fundamentals of Sustainability is illustrated in the diagram below.

Chart 1: Sustainability Diagram

The world is a globalised market. International trade of seafood constitutes many new opportunities and challenges for all countries particularly the insular states of the Western Indian Ocean. Protectionism is giving way to free trade and yet, non-tariff standards, certifications and voluntary labelings are imposed on imported fish and fish products by developed countries (Ponte 2006). The seafood sector of developing countries is also vulnerable to cheap imports from other develping and emerging economies. Therefore the national stakeholders are bound to review their strategies to boost up their competitive edge4 on the local markets and to capture new market shares in industrialised and emerging

1 The Terms of Reference is given in Appendix 12 Under the heading ‘Revitalising the fishing Industry page 13-153 Sustainability is the capacity to endure. For humans, sustainability is the long-term maintenance of well being, which has environmental, economic, and social dimensions, and encompasses the concept of stewardship, the responsible management of resource use.4 In 2009 the FAO and NORAD have initiated a comprehensive value-chain analysis of international fish trade with particular emphasis on small scale sector in developing countries to follow up the study on the impact of international fish trade on local food security as FAO Fisheries Technical Paper 456, 2004.

Economic

Social Ecological

Affordability Feasibility

Acceptability

SUSTAINABILITY

Introduction

26 Programme SmartFish Rapport SF/2012/18

economies. Modern Information and Communication Technology (ICT) makes real time market information accessible worldwide. Market forces do not lead de-facto to sustainable exploitation and conservation of biological resources unless consumer behaviours are motivated by the principles of sustainability through effective awareness building at all levels – local, regional and global.

Globalization has also streamlined the normal business of states whereby the public sector emerges as regulator and facilitator to fast track a business friendly environment, equal opportunities for all and social justice. The private sector is empowered as the growth engine. Innovative financial concepts such as Public-Private Partnerships have become instrumental in the procurement of economic infrastructure and efficient logistics to connect local industries to international trade. This policy framework is also relevant for the development of the fisheries sector of an insular economy.

From a marketing perspective, fish is an end product and/or an intermediate input in the supply chain to produce value added fish and fish products for end consumers. No enterprise irrespective of type or scale is immuned or isolated from international trade. Self employed actors in the fisheries sector are in fact household or micro enterprises that have to be empowered by all means to build a resilient business enterprise at the grass-roots level of the national economy.

Fish stocks are part of the biogical wealth of a nation and their economic rent5 is a function of their respective value chain or maximisation of value added. Common property rights or open access is the main cause for depletion of fish stocks and degradation of the marine ecosystem in coastal fisheries. It negates value chains and degenerates into a vicious circle of poverty and the paradox of miseries in the midst of plenty among the fisher communities. Actually coastal fisheries feed everyone – the traders, processors, exporters and consumers – except the fishers.

The methodology of VCA6 was initially devised as an analytical tool to examine efficiency at each sequence of the value chain of an industrial or marketing function. This method is currently applied to assess the value added or profitability of seafood industries and to study the economic viability of specific projects. In small scale fisheries, VCA can be instrumental in promoting judicious utilization of scarce fish stocks through appropriate product and market development. The main objectives of this study for the fisheries sector of Rodrigues include:

• Appraisal of the different value chains operating in the fisheries sector and their enabling environment using a systemic approach.

• An analysis of the supply chains– production , processing, marketing - to assess the revenue flow and economic efficiencies.

• Evaluation of future value chain opportunities and constraints of the fisheries sector within the perspectives of future fisheries development and management policies.

• Recommendations to ascertain sustainable development of the fisheries sector as a driving force for socio-economic benefits of the regional economy.

1.2 Rodrigues Island

Rodrigues Island forms an integral part of the Republic of Mauritius. In 2002 it achieved an autonomous status for administrative and political powers with the setting up of the Rodrigues Regional Assembly (RRA). The local executive exercises the same powers as a Regional Government presided by a Chief Commissioner, who is the direct interlocutor of the Central Government regarding Rodriguan affairs.

5 David Ricardo argued that economic rent accrues on the basis of unequal ownership/access or control over an existing scarce resource. This is contrary to open access and common property rights over natural resources.

6 The value chain concept was introduced 25 years ago by Michael Porter in his 1985 best-seller, Competitive Advantage: Creating and Sustaining Superior Performance. A value chain is defined as a chain of activities whereby products pass through all activities of the chain in sequence and at each activity the product gains some value. The chain of activities gives the products more added value than the sum of added values of all activities.

27Programme SmartFish Rapport SF/2012/18

Located at the heart of the Indian Ocean some 650 km North East of Mauritius, Rodrigues Island has a total land surface area of 108 km² (18 km long and 8 km wide) and a coast line of 80 km. It is completed encircled with coral barriers nestled with shallow beds extending out up to 10 km at some places. The surface area of the lagoon is approximately 240 km². It enjoys a tropical climate with temperatures varying between 28°C and 35°C during summer, which coincides with the cyclone season (November - April) and between 18°C and 27°C in winter. In 2008 the population was at 37,700 with a growth rate of 1.19 % per annum. It accommodates about 40,000 Mauritian and foreign visitors, mainly from Réunion Island every year (CSO, 2010). Regular sea-links between Mauritius and Rodrigues is ensured by two mixed cargo-cum-passenger vessels (MV Mauritius Pride and MV Mauritius Trochetia) on a weekly basis. The trip lasts between 24 to 36 hours depending on sea conditions. Also, Air Mauritius provides 2 to 5 daily services.

The fisheries sector is a major productive sector of the Rodriguan economy. As at November 2011, it employed 1,410 registered fishers including 330 fisherwomen, who are involved mainly in the octopus fishery. Approximately 2,000 non-registered full time and subsistence fishers 7 3 are also engaged in fishing on a full or part-time basis. Over the past 5 years, 400 registered fishers have relinquished their fishing cards in exchange for some financial compensation. It is most likely that they have gone back to fishing as non-registered fishers. There are 1,821 registered fishing boats out of which 70% are traditional canoes using oars and sail. Their activities are limited to the lagoon. Most registered fishers are not owners of fishing assets; they are in fact fishing workers.

In 2010, the annual catch was estimated at 1,609 Mt and consisted of 1,225 Mt from the lagoon fisheries including 273 Mt of octopus and 384 Mt from the off-lagoon. Fish and fish products are the main source of protein diet for Rodriguans and the per-capita fish consumption is about at 20 Kg per year. The fisheries statistics do not include the portion of daily catch held for household consumption commonly called “carri”.

The fisheries sector is also a major source of export earnings with an annual export of approximately 145 Mt of frozen octopus to Mauritius. Harvest of octopus has declined drastically over the past decade due to over fishing and degradation of the marine ecosystem. In spite of intensive efforts of the regional Government, the development of off-lagoon and FAD fisheries has not achieved expected results. There is an apparent political will on the part of RRA to marshal a rational management and development plan for the fisheries sector.

1.3 Methodology

1.3.1 Business analysis of the fisheries sectorA VCA of small scale or artisanal fisheries requires a business oriented approach whereby the various components of the value chain - fishing, processing and marketing are viewed as enterprises or cost centres. Although in-bound and out-bound logistics are external factors of a value chain, they are of critical importance for the efficiency of core activities.

The main objective of an enterprise in the fisheries sector is to earn normal profits84

or a surplus of income over operating costs. Net income is the source of livelihood for the economic actor and for maintenance of capital assets employed in the trade. It is important to differentiate between a fishing enterprise (owner of fishing capital) and a fishing worker or labour. The majority of registered fishers cannot be considered as fishing enterprises because they do not own the fishing capital – fishing boats whether motorized or not. Normally the harvested fish belongs to the boat owner and the fishing workers are remunerated by pre-agreed amount per kg or a share of the net income. However an on-foot fisher is assumed to be an individual enterprise because the latter is solely responsible of her/his fishing operations. The administrative registries held by the FPS do not permit to identify ownership of fishing boats by:

7 Hardman et al , 2007

8 Profit is the surplus of revenue over the total operating cost including non-cash items such as depreciation of the capital assets. It is the best known measure of success in an enterprise

Introduction

28 Programme SmartFish Rapport SF/2012/18

• Registered active fishers • Non-registered professional • Registered fishmongers • Subsistence/amateur / leisure fisheries.

1.3.2. Components of the Rodriguan Fisheries SectorThe fisheries sector comprises predominantly marine coastal fisheries95. Semi-industrial and industrial fisheries do not exist. The main types of fishing activities are as follows:

• Large Net fishery (LN)• Off-lagoon Hand line fishery (HL)• Non-motorized Basket Trap (BT) and Hand line (HL) fishery • Octopus fishery • Off-lagoon Hand line (chilled) fishery• Shrimp Net (SN) fishery

1.3.3. Fish preservation and value added activities The value chains are limited to:

• Frozen octopus • Dried octopus • Packed of dried and grilled octopus • Packed octopus pickles • Dried salted fish

Frozen octopus is the main export product of the fisheries sector. The use of refrigeration is a primary mean of preservation of raw octopus rather than value added process. The production of dried octopus and dried-salted fish has declined significantly mainly because of scant supply. Value added products made from dried octopus are promising value chains for the cottage /micro enterprises.

1.3.4. Marketing Structures and ChannelsThere are 3 private companies engaged in export of frozen octopus. Generally fresh fish is sold to end consumers and/or fishmongers at landing stations. There are approximately 40 regular and full-time fishmongers in addition to some 35 seasonal vendors who are active mainly during large net (LN) fishery. Some non-licensed fishmongers were also identified during field works.

1.3.5. Data collectionThe VCA requires detailed financial/economic data of enterprises involved at the different sequences of the value chain. These data were scant and had to be collected by a primary survey of stakeholders. Fisheries Statistics and time-series data of fish market prices for the year 2010 (unpublished) were obtained from the FRTU. They were verified / cross-checked through direct interviews and discussion with reliable operators. Site visits were effected to all fish landing stations (FLS), processing and storage units of the island. Group discussions were organized with fishers, indigenous fish processors, fishmongers, logistic providers and NGO involved in the fisheries sector.

1.3.6. Data processing and analysisBasic cost accounting methods were used to process and analyze the collected data. They were then applied in a business model devised for each trade to assess economic performance in terms of revenue flow, cost of production, net income of fishing enterprise and fishing workers. A minimum income criterion of Rs 7,500 per month was used to perform break-even analysis on individual and small scale enterprises.

9 Small scale fishing activities performed within 12 nautical miles from the coast.

Overview of the Fisheries Sector of Rodrigues

29Programme SmartFish Rapport SF/2012/18

2.0 OVERVIEW OF THE FISHERIES SECTOR OF RODRIGUES2.1. Fisheries Policies

Most coastal fisheries in the Western Indian Ocean are overexploited and fish stocks on the high seas are harnessed by distant waters fleet from EU and South East Asian countries10.6The Central and Regional Governments are both committed to achieve sustainable management and development of their marine fish resources as a prerequisite to enhance economic growth and social welfare of the population.

The existing social welfare policies in favour of the fisher communities are unique and reputedly over generous. They have contributed undeniably to overfishing and degradation of the coastal marine ecosystem. There is an emergency to provide appropriate supports and incentives to shift the fishing efforts from the lagoon to off-lagoon and high-sea fisheries. Value chain development in the fisheries sector aims at enhancing revenue flow and employment through judicious utilization of scarce fish resources, product and market development and seamless integration to the macro-economic environment.

The Fisheries and Marine Resources Act 2007, promulgated in May 2008 provides a policy framework for fisheries conservation and management. At time of writing, a new Fisheries Master Plan for Mauritius and Rodrigues is awaiting approval of the Cabinet. The Sustainable and Integrated Development Plan for Rodrigues 2009, which has been approved by the RRA constitutes a blueprint for the sustainable development of the fisheries sector of Rodrigues. The 2012 Budget of RRA acknowledges the essential role of the fisheries sector and makes adequate provisions to streamline the sector towards sustainable growth. Implementation of the IFAD-MARS Programme for the development of extended artisanal fisheries is an ambitious project that is expected to create a spin-off effect.

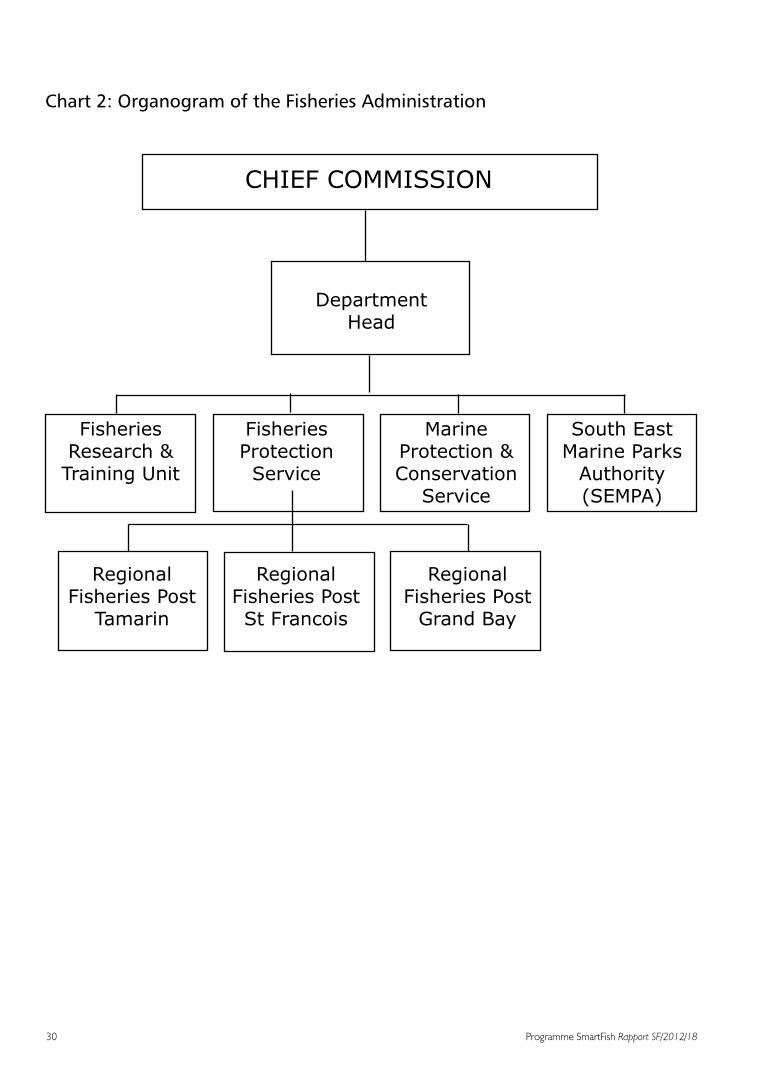

2.2. Fisheries Administration

The fisheries sector of Rodrigues is under the responsibility of the Fisheries Commission and is chaired by the Chief Commissioner.

10 FAO Fishery Technical paper 495 – The State of World highly migratory, straddling and other high seas fishery resources and associated species.

30 Programme SmartFish Rapport SF/2012/18

Chart 2: Organogram of the Fisheries Administration

CHIEF COMMISSION

DepartmentHead

Fisheries Research &

Training Unit

Fisheries ProtectionService

Marine Protection & Conservation

Service

South East Marine Parks

Authority (SEMPA)

RegionalFisheries Post

Tamarin

RegionalFisheries Post St Francois

RegionalFisheries Post

Grand Bay

Overview of the Fisheries Sector of Rodrigues

31Programme SmartFish Rapport SF/2012/18

2.3. Recent Studies on the Fisheries Sector

Recent studies in the fisheries sector (non-exhaustive) that have provided valuable resources to this mission are listed below:

• Assessment of Current data for the Octopus Resource in Rodrigues – African Journal of Marine science presented by J Anderson, S. Perrine et al , 2010.

• Sustainable and Integrated Development Plan for Rodrigues, KPMG / UNDP , 2009• Study of Fish Handling and Preservation in Mauritius and Rodrigues, HBL Appavoo & Associates, 2007• Socio-economic Study of the Fishing Community – Case Study of Rodrigues , University of Mauritius, 2007• Large Net Fishery Assessment, Shoal Rodrigues 2006

2.4. Fisheries Infrastructure

There are only 4 Fish Landing Stations (FLS) located at Pointe Aigle, Tamarind, St. Francois and Grand Bay but they are not in use. FLS are in reality unsheltered/traditional fish landing sites in main fishing villages that have been designated for local fisheries administration and data collection.

The FAD programme dates back to 1994 and presently there are 16 FADs in the northern regions of the island. These FADs have not been visited / maintained by the research and training vessel, MV Rodriguez for the past six months due vessel mechanical problems.

There are two institutional fish markets on the island, one at Mont Lubin and the other one is at Bazar de Port Mathurin. A third one is operated by Rodrigues General Fishing Co. Ltd (RGF)111 at Pointe Monier.

The main processors / exporters of frozen octopus are equipped with isotherm vans, blast freezers and cold rooms. RGF has an ice flake production unit of 500 Kg per day that supplies its own fleet of 6 off-lagoon hand-line fishing boats. There is no standard practice for handling and preservation of fresh, chilled, frozen fish and fish products.

2.5. Supporting Organisations

2.5.1. Extension services

Since 2000, the FRTU has imparted ad hoc training in navigation, fishing technology, sanitary and health on board, first aid, basic meteorology and cooperative organisation to some 800 registered fishers. The IFAD-MARS Programme has provided training to 50 registered fishers in entrepreneurial skills including book keeping and business management. The 2012 budget has made provision to train an additional 200 registered fishers in off-lagoon fisheries by next year.

In spite of the various training programmes in the fisheries sector the development goals have not been achieved. It is important to assess the effectiveness of those training programmes and to plan for capacity building in an integrated and performance based approach.

2.5.2. Financial support

Finance is the life blood of an enterprise. Financial resources have been made available to the fisheries sector through the Development Bank of Mauritius (DBM), the Empowerment Funds, the SME Partnership and commercial banks to fisheries sector. However, the development of the fisheries sector has been retarded due to inherent mismatch 11 RGF is a fully RRA owned private limited company that has been set up to operationalize the fisheries terminal commonly known as “Maison des Pêcheurs “ at Pointe Monier and a fleet of six 9.5 m long fibreglass fishing boats engaged in off-lagoon hand line (chilled) fishery.

32 Programme SmartFish Rapport SF/2012/18

between financial requirements of fishing entrepreneurs and pre-requisites of the lenders. For instance, the loan ceiling provided by DBM to registered fishers to purchase fishing equipment (boat and engine) is Rs 200,000. This amount of loan is insufficient to invest on an adequate fishing unit to operate off-lagoon. In fact the DBM financial scheme led to overcapitalization in the lagoon fisheries and depletion of the fish stocks. Most borrowers were unable to pay back their loans due to a decline of their revenue. Other obstacles to the access of finance in this sector are informal transactions, low financial literacy and the absence of a savings culture. Therefore, there is an urgent need for suitable financial facilities embedded with adequate extension and facilitation supports to ensure the launching of the off-lagoon fisheries.

2.5.3. Technical Expertise of MRC

The Mauritius Research Council (MRC) has set up a regional office at the RRA to assist in the experimental phase of seaweed culture in Rodrigues. This institution can assist the fisheries sector by undertaking various socio-economic audits and creating/re-activating LFCs to partner in future fisheries management plan.

2.5.4. Regional and International Cooperation

The IFAD/MARS programme is a break-through in the development of an extended artisanal chilled fishery in Rodrigues. A fleet of five 15 metre long fishing boats are to be delivered to the RRA soon.

The SmartFish programme of the IOC / EU can be sought for technical expertise in fish trade and fisheries management, as well as other small support for the fishery. 2.5.5. Empowerment and Capacity building

The mission of the Federation of Fishermen Cooperatives (FFC) of Rodrigues is to unite the fisher folks into cooperative societies as a prerequisite to work collectively towards their socio-economic empowerment. The FFC has modernized its management style to invigorate dormant fisher cooperatives and to propel new ones. The task is not made easier as most fishers are averted to any form of cooperative or association in their economic life. It is playing a crucial role in providing an organisational framework to 6 fisher cooperatives that have been designated to operationalize the newly built IFAD/MARS fishing boats. The FCC is also keen in developing local and regional fish marketing and distribution networks.

Shoal Rodrigues is doing a commendable work in marine conservation, awareness building and follow up of the LN and octopus fisheries. It has been instrumental in the establishment of the South East Marine Parks Authority (SEMPA) as a pilot project.

2.5.6. Fish Resources

Western Indian Ocean, Zone 51 of the FAO accounted for 5.2 % of global landing in 2005. 24 % of fish stocks have no room for expansion, 2% have some room for further expansion while the status of 73% of fish stocks are still unknown or unexplored. Most coastal fish stocks of the region are considered to be fully exploited. While the coastal fisheries within 12 nautical miles are harvested by the coastal states, the most lucrative oceanic fisheries are harvested mostly by distant waters fleets from EU and South Eastern Asian countries12.2.

The total annual catch of the fisheries sector topped 2,000 Mt in 1999 and declined ever since reaching its lowest point of 1,000 Mt in 2005/06, then picking up again with the development of off-lagoon fisheries, to revolve around 1,600 Mt today (as shown in Chart 1). Since the 1990s the production of octopus has declined by nearly 50% to stagnate below 300 Mt per year over the past 6 years. This is mainly due to overfishing and serious damage caused to the marine habitats. Octopus is a ready cash product and the decrease in productivity has a direct impact on the livelihood of the fisher communities, particularly the “piqueuse d’ourites”.

12 Regional assessment of World fisheries, Oceana, May 2008.

Overview of the Fisheries Sector of Rodrigues

33Programme SmartFish Rapport SF/2012/18

The experiment of FAD fisheries since 1994 has failed to spin-off into an alternate fishery to relieve the lagoon ecosystem. Actually there is a network of 16 FADs in the northern areas of the island. They are mostly exploited by game fishers that indirectly confirm the presence of fish on these FAD13.3 An evaluation of past development initiatives is necessary to understand their lacunae and to chart out a rational action plan.

Chart 3: Total Catch 1997 - 2010 in metric tonnes (Mt)

Over the past 3 years (2008 - 2010) a new trend is observed in the sector whereby the total catch from the lagoon is declining and is compensated by a gradual increase in production of the off-lagoon fisheries. This trend has to be enhanced further. There is no sign of recovery in the octopus fishery. The FAD is yet to be adopted by the off-lagoon fishers. Data on the sport fishery is not collected.

2.5.7. Fishers

Besides 1,410 registered active fishers (FPS – Nov 2011) including 330 fisherwomen, there is a large number of unregistered full-time, seasonal and amateur fishers. As shown in the charts below, nearly 60 % of registered fishers operate in the lagoon in spite of the declining catch rate. They are not equipped to fish off-lagoon. Most fishers involved in off-lagoon fishing are located in the northern region because the channels are safe and the fishing areas are sheltered. The shrimp net (SN) fishery accounts for 13 licence holders who operate mainly around the islets, namely Coco Island. They are also multi-geared like other fishers.

13 Catch per fisherman day on the FAD was estimated at 60kg by Lojac H’meur (Fishieries Expert), 1994

34 Programme SmartFish Rapport SF/2012/18

2.5.8. Fishing Equipment

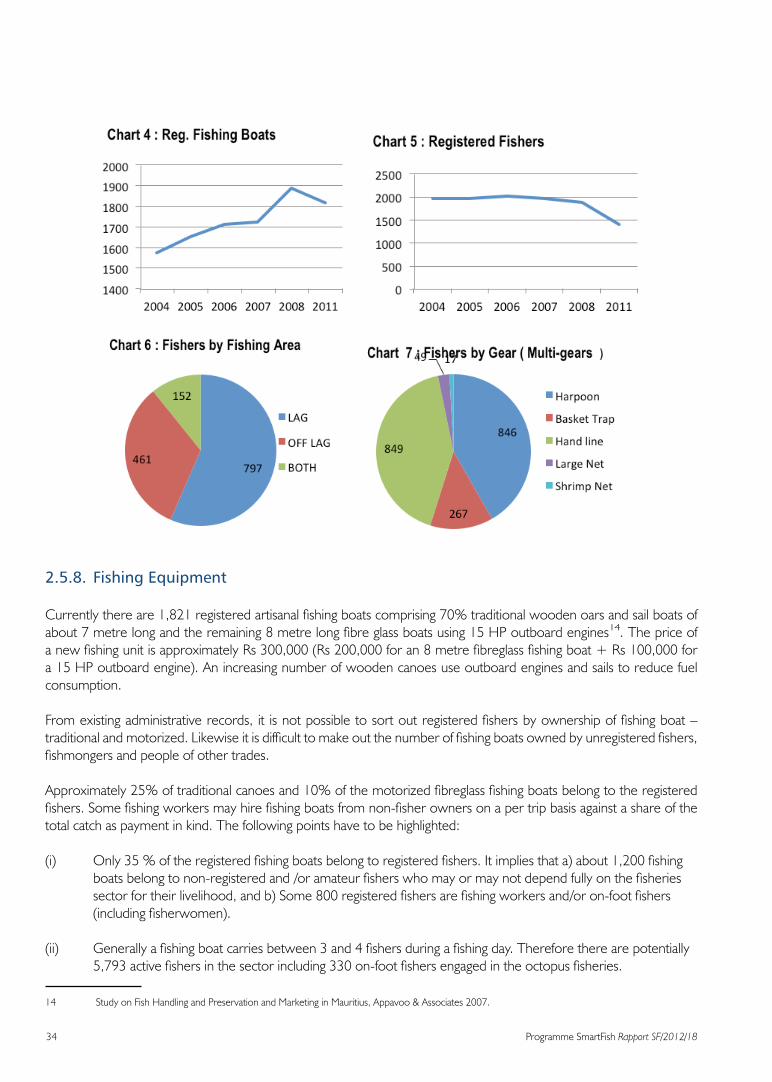

Currently there are 1,821 registered artisanal fishing boats comprising 70% traditional wooden oars and sail boats of about 7 metre long and the remaining 8 metre long fibre glass boats using 15 HP outboard engines14.1The price of a new fishing unit is approximately Rs 300,000 (Rs 200,000 for an 8 metre fibreglass fishing boat + Rs 100,000 for a 15 HP outboard engine). An increasing number of wooden canoes use outboard engines and sails to reduce fuel consumption.

From existing administrative records, it is not possible to sort out registered fishers by ownership of fishing boat – traditional and motorized. Likewise it is difficult to make out the number of fishing boats owned by unregistered fishers, fishmongers and people of other trades.

Approximately 25% of traditional canoes and 10% of the motorized fibreglass fishing boats belong to the registered fishers. Some fishing workers may hire fishing boats from non-fisher owners on a per trip basis against a share of the total catch as payment in kind. The following points have to be highlighted:

(i) Only 35 % of the registered fishing boats belong to registered fishers. It implies that a) about 1,200 fishing boats belong to non-registered and /or amateur fishers who may or may not depend fully on the fisheries sector for their livelihood, and b) Some 800 registered fishers are fishing workers and/or on-foot fishers (including fisherwomen).

(ii) Generally a fishing boat carries between 3 and 4 fishers during a fishing day. Therefore there are potentially 5,793 active fishers in the sector including 330 on-foot fishers engaged in the octopus fisheries.

14 Study on Fish Handling and Preservation and Marketing in Mauritius, Appavoo & Associates 2007.

Overview of the Fisheries Sector of Rodrigues

35Programme SmartFish Rapport SF/2012/18

vii) Technically there are 1,821 fishing boats for 1,410 registered fishers with an annual production of 1,600 t. There is a surplus of approximately 1,351 fishing boats, mostly fishing in the lagoon. It is crucial to determine the number of boats that can be modified and adapted to off-lagoon fisheries.

2.5.9. Fishing Gears The main fishing gears used in the fisheries sector are briefly described below.

• Harpoon (HN): It is a long spear-like instrument used by on-foot fishers to catch octopus during low tides in Rodrigues. The fishing technique is not more destructive to marine ecosystem as compared to other gears used in the artisanal fisheries. The absence of strict management regulations is the main cause for the depletion of the stock of octopus and degradation of the marine ecosystem.

• Large Net (LN): It is consisted of a net of up to 500 m long and 5 m wide with regulated mesh size used to encircle reef fish in the lagoon. The fishery is restricted to licence holders and a close season of 5 months every year – from the first day of October to the last day of February is enforced. Since 1996 the Government has introduced a buy-back scheme to reduce the number of large nets due to its destructive effects on the coral reefs.

• Basket Trap (BT): It is a baited passive and close-end basket made of galvanized steel mesh or bamboo anchored in the inner lagoon to trap reef fish. A basket trap can potentially hold up to 100 kg of fish. It is a popular fishing method among the artisanal fishers. The fish caught by basket traps is mainly Licorne and Cordonier

• Hand line (HL): It is a single nylon line held in the hands with up to 3 baited hooks used to catch demersal/bottom fish such as Red Snappers, Vacoas, Sacrechien and Capitaine. It is a selective fishing method that harvests high market value fish. It is practiced in the lagoon and off-lagoon.

• Shrimp Net (SN): The fishing gear consists of a net basket fixed to a stick used to catch shrimps in shallow waters around the islets namely Coco Island. The fishery is restricted licence holders only. Actually there are 11 active SN fishers in Rodrigues.

Most fishers are polyvalent as most fishers use HL and BT regularly. The following examples show the complexity of fishing activities in Rodrigues:

(i) During low tides, about 12 - 16 days per month around the year, most fishers catch octopus in the early morning before setting out for their regular trade (HL and BT).

(ii) During LN fishing (March to September) a large number of HL and BT fishers migrate to LN fishery seasonally and during close season the LN fishers will also perform other fishing activities.

(iii) A trait of specialisation is observed in the off-lagoon HL fishery as the fishers focus on a single fishing method.

36 Programme SmartFish Rapport SF/2012/18

3.0 SUPPLY CHAIN ANALYSIS

In this section the operating cost and revenue flows of the fishing activities is studied. It is useful is determining the cost of production, value added, wages of fishing crew and net income of fishing enterprises.

3.1 Key determinants and assumptions

The transactions are predominantly small-scale and informal. Accounting records and economic data are not available. Business models were created from data collected through a primary survey.

3.1.1 Product and Market Segments

Fish is composed of a wide range of value products ranging from low value to high value, depending on the species, quality, size and so on. Fish species are clustered into commercial categories according to marketing practices15. 1 Market price of each commercial category was collected at various levels of the marketing channels namely, Producer Sale Price (PSP), Whole Sale Price (WSP) and Consumer Sale Price (CSP).

Table 1: Price Survey of fish (Rs / Kg) – November 2011

Products / Markets PSP WSP CSPProduct Segment 1Product Segment 2Product Segment 3Miscellaneous fish

140 100 80 60

150 110 90 70

18013011090

3.1.2 Effective fishing days

Fishing activities depend on sea and weather conditions. They are more intense and productive during summer (7 months) than winter (5 months). Generally fishers are willing to go out for fishing everyday if weather conditions allow. A fishing trip last for 8 to 10 hours and sometimes more than one trip is performed in a single day. Night fishing is also frequent. To determine a realistic number of effective fishing days per year, bad weather day records16 of the FPS were cross-checked by a primary survey in the 3 main fishing regions of the island. The mean fishing day per year for the island is held at 200 (North: 266, South: 168 and South East: 168). The sea conditions in the southern regions are more severe than the northern part.

3.1.3 Catch Per Unit Effort (Productivity)

The Catch Per Unit effort (CPUE) data of the FRTU was cross-checked and complemented by primary surveying. Formal catch data does not include fish kept by fishers for household consumption commonly called “carri”. This “carri” varies between 1.5 kg (winter) and 2.5 kg (summer) per fishing day. In the LN fishery fish is also used as payment in kind to fishing workers and it is approximately 5 kg per fishing day. The impact of the above indigenous practices on the revenue flow is also examined.

15 A list of main fish species harvested by the local fisheries and their classification according product and market segmentation is given in Appendix 2 16 Bad weather days are recorded by the Fisheries Protection Service for the purpose of computation of Bad Weather Allowance payable to registered fishers.

Supply Chain Analysis

37Programme SmartFish Rapport SF/2012/18

3.1.4 Other pertinent assumptions

• A monthly income of Rs 7,500 is assumed as an income threshold of the fisher household or the opportunity cost of fishing labour. It is treated as a fixed cost while performing break even analysis.

• The fishing units / enterprises are considered as on-going businesses and the value of the fishing capital is estimated at actual cost.

• Various allowances such as BWA and CSA provided by the Government to registered fishers are not included in the business models.

• Fishing is mainly a cash business that falls outside the formal or banking network. Payment in kind is converted into

money terms and included in the business model.

• A registered fisher does not require a fishmonger licence to sell his/her catch direct to end consumers.

• There is no Value Added Tax (VAT) on fish and fish products.

• The net income estimates of the fishing enterprise are after provision for depreciation and other non-cash items unless otherwise stated.

• The cost of apparent damages cause by fishing practices to marine habitats is not included in the costing (an in-depth economic assessment.

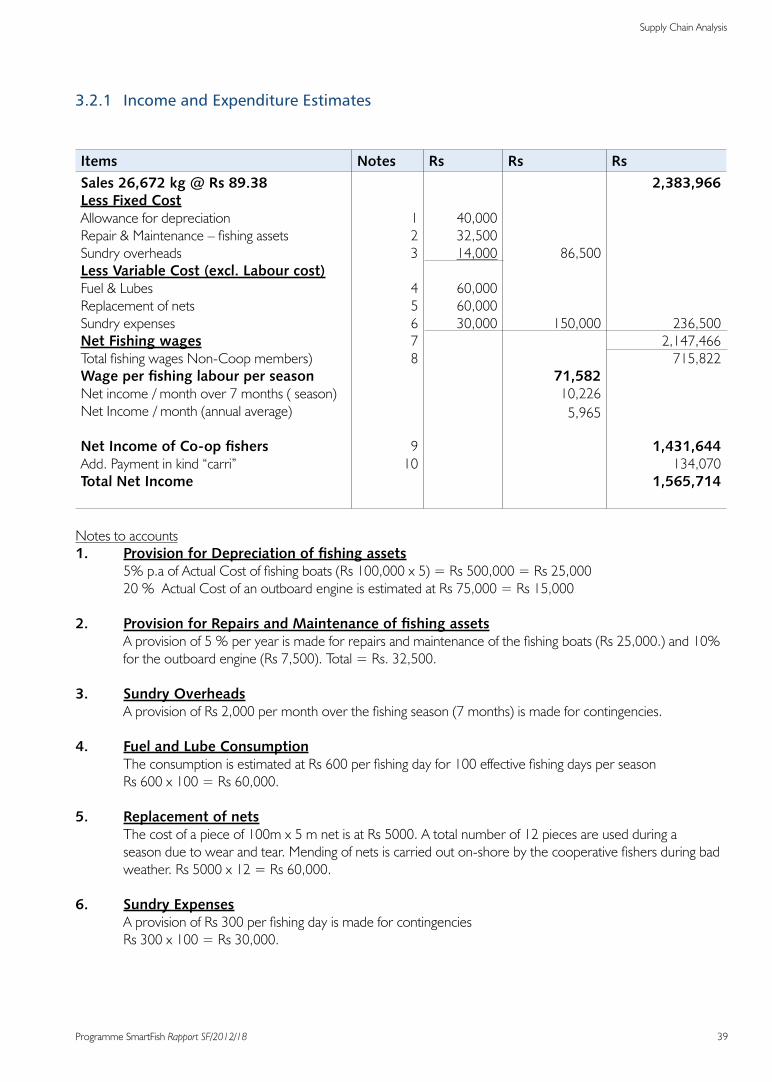

3.2 Large Net Fishery

In Rodrigues there are 6 cooperative societies and one individual large net licence holders. Customarily a large net fishing enterprise consists of up to 5 fishing boats with a least one motorized boat to haul the net and 20 fishers. Other key determinants and assumptions are discussed below:

(i) There is several net income sharing practices in the fishery. However for the purpose of this case study the distribution of net income between cooperative fishers and casual fishers is assumed at a 2:1 ratio.

(ii) The 2010 total catch for the LN fishery was at 186.7 Mt (FRTU). The mean catch per fishing unit is assumed at 26.7 Mt, which is equal to a mean catch per fishing unit per fishing day of 266 Kg.

(iii) A fishing unit comprises 1 motorized + 4 non-motorized fishing boats and 20 fishers including 10 cooperative and 10 casual /non registered fishers

(iv) Number of effective fishing days is assumed at 100 during the season;

(v) Fish kept for “carri” varies between 1.5 kg and 2.5 kg per fisher per fishing day (are not included in the official fisheries statistics).

(vi) The length of net varies between 300 and 500 m long. Approximate 10 – 12 nets are replaced during a fishing season. The cost per unit is Rs 5,500.