Value Chain Analysis-Allo - Micro-Enterprise … Chain Analysis.pdf · Chapter-3 SWOT Analysis and...

54

Value Chain Analysis Series: 1 Value Chain Based Approach to Micro-Enterprise Development Value Chain Analysis-Allo Micro Enterprise Development Programme (MEDEP) (MEDEP-NEP/08/006) Bakhundole, Lalitpur February 2010

Transcript of Value Chain Analysis-Allo - Micro-Enterprise … Chain Analysis.pdf · Chapter-3 SWOT Analysis and...

Value Chain Analysis Series: 1

Value Chain Based Approach to Micro-Enterprise Development

Value Chain Analysis-Allo

Micro Enterprise Development Programme (MEDEP) (MEDEP-NEP/08/006) Bakhundole, Lalitpur

February 2010

Contents Chapter-1 Selecting a Value Chain for Promotion 1

1.1 Determining the Scope of Value Chains to be Promoted 1 1.2 Steps in Value Chain Development 2 1.3 Methodology 3

Chapter-2 Value Chain Analysis 5

2.1 Allo Sub-Sector 5 2.2 Mapping the Value Chain 7 2.3 Meso Level Providers of Support Services 10 2.4 Macro Level Enablers 11 2.5 Role of Donors 13 2.6 Market Analysis 13 2.7 Gross Margin, Profit, and Value Addition 18

Chapter-3 SWOT Analysis and Identification of Constraints and Solutions 20

3.1 SWOT Analysis of Allo Sub-Sector 20 3.2 Value Chain Constraints and Possible Solutions 23

Chapter-4 Upgrading the Allo Value Chain 27

4.1 MEDEP Interventions in Allo Value Chain 27 4.2 Strategies for Upgrading the Allo Value Chain 29

Chapter-5 Recommendations 34 List of Tables: Table-1: Support Services provided by Agencies/Organizations at Meso Level 11 Table-2: Ministries and National Organizations and their Role at Macro Level 12 Table 3: Export of Allo Goods by Destination (2007/08) 15 Table-4: World Natural Fibre Production (2008) 17 Table-5: Gross Margin and Profit Analysis at Different Levels of Allo Value Chain 18 Table-6: Strength, Weakness, Opportunity, and Threat (SWOT) 21 Table-7: Constraints, Solutions, and Providers 25 Table-8: Common Facility Centres (CFCs) for Allo Processing 28 List of Charts: Chart-1: Steps in Value Chain Development 2 Chart-2: Value Chain Map (Micro Model) 9 Chart-3: Export of Handicraft Products from Nepal (Textile) 15 Chart-4: Export of Hemp and Allo Goods from Nepal 16 Chart-5: Value Added at Different Functional Levels of Allo Value Chain 19

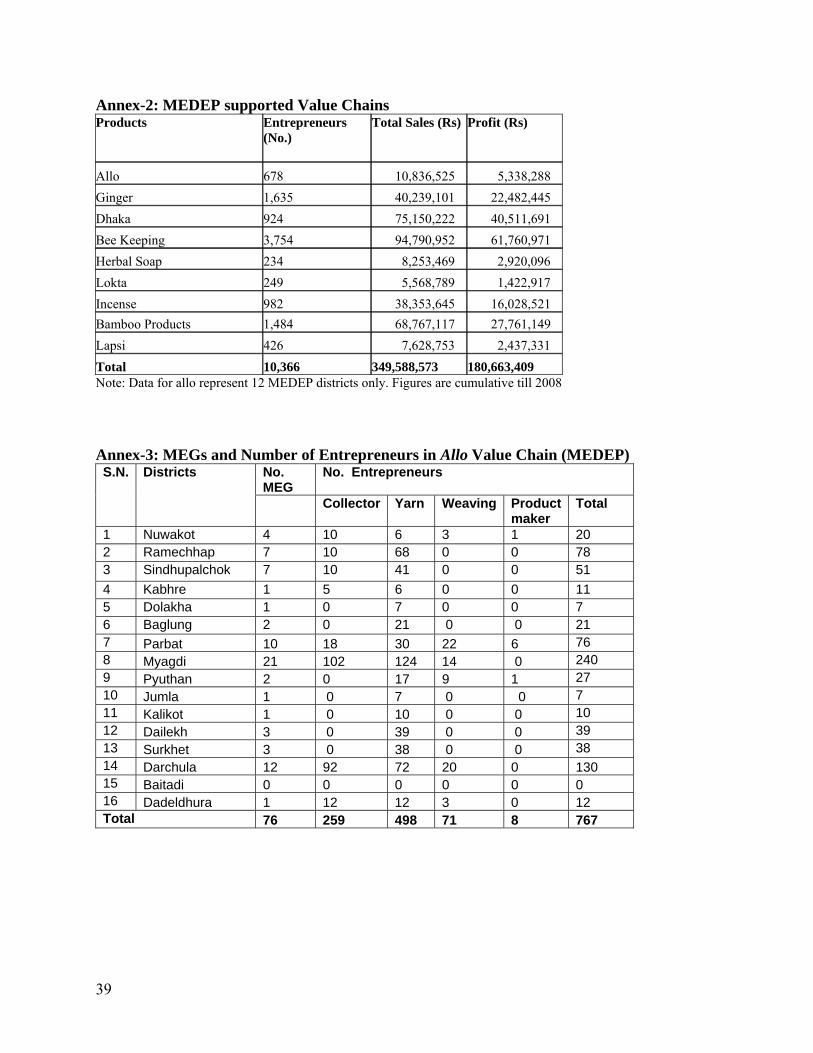

Annexes: Annex-1: Export of Handicraft Goods from Nepal (Time Series) 38 Annex-2: MEDEP Supported Value Chains 39 Annex-3: MEGs and Number of Entrepreneurs in Allo value Chain (MEDEP) 39 Annex-4: Estimated Potential Stock and Current Extraction Level of Allo (MEDEP) 40 Annex-5: Production of Allo yarn and Fabric (MEDEP) 40 Annex-6: List of Selected Input/Equipment Suppliers, Product Makers, Traders and Exporters 41

ii

ACRONYMS BDSPO Business Development Service Providing Organization CFUG Community Forest User Group CSIDB Cottage and Small Industry Development Board DDC District Development Committee DEDC District Enterprise Development Committee DFO District Forest Office DMEGA District Micro Entrepreneurs' Groups Association DoF Department of Forest DoLIDAR Department of Local Infrastructure Development and Agriculture Roads EDF Enterprise Development Fund FECOFUN Federation of Community Forest User Groups Nepal FINGO Financial Intermediary NGO FNCCI Federation of Nepalese Chambers of Commerce and Industry GB Grameen Bank IFAD International Fund for Agriculture Development ILO International Labour Organization LFP Livelihoods and Forestry Programme MDG Millennium Development Goal MEDEP Micro-Enterprise Development Programme MEG Micro Entrepreneurs' Group MFI ` Micro Finance Institution MOAC Ministry of Agriculture and Cooperatives MOFSC Ministry of Forest and Soil Conservation MOEST Ministry of Environment, Science and Technology MLD Ministry of Local Development MOI Ministry of Industry NEDC National Entrepreneurship Development Centre NMEGA National Micro Entrepreneurs' Groups Association OVOP One Village One Product RADC Remote Area Development Committee RMDC Rural Microfinance Development Centre RSDC Rural Self-reliance Development Centre RSRF Rural Self-Reliance Fund SCC Savings and Credit Cooperative SDC Swiss Agency for Development and Cooperation SIYB Start and Improve Your Business SMLE Small, Medium, and Large Enterprises TEPC Trade and Export Promotion Centre UNDP United Nations Development Programme

iii

FOREWORD The Micro Enterprise Development Programme (MEDEP) is a nationally executed project of the United Nations Development Programme (UNDP) under the Ministry of Industry (MoI). The programme is funded by UNDP with additional support from the Australian Agency for International Development (AusAID). MEDEP which is now in its Third Phase (2008-2010) primarily aims at improving the livelihoods of families below the nationally defined poverty level through micro enterprise development. The program emphasizes on inclusion of disadvantaged groups such as indigenous nationalities "janjatis", "dalits", religious minorities, women, and youth as beneficiaries. MEDEP has been working in several commodity sub sectors based on market demand, local resource potential, and needs and demands of target groups. The program is currently active in 36 districts, with total beneficiary number exceeding 40,000. There has been a significant contribution in enhancing the income levels of participating entrepreneurs. The MEDEP approach in value chain is in the process of internalization (especially in Phase-III) although the programme has been active in development of enterprises involving several commodities and products since the last ten years. MEDEP is primarily focused on creating and sustaining micro entrepreneurs through their sustainable integration into the value chains and upgrading activities. A total of ten commodities/products including Allo (Himalyan Nettle) are currently targeted for strengthening the value chains to support higher value addition and enhanced opportunities for income generation for the participants. The present study on Allo has been carried out to identify the weaknesses along the commodity value chain and to design appropriate intervention strategies to energize the whole sub sector. We are hopeful that the study will be useful to all stakeholders in the Allo sub sector. Finally, we would like to offer our thanks to Dr. Bhimendra B. Katwal for completing this important study, field staff of APSO Baglung for their support in data collection and for all stakeholders especially the participants in the sharing workshop for their valuable cooperation. Lakshman Pun, Ph.D. Dhundi Raj Pokharel National Programme Manager National Programme Director February 2010

iv

Chapter-1

Selecting a Value Chain for Promotion

1.1 Determining the Scope of Value Chains to be Promoted Nepal is one of the poorest countries in the world with an estimated 31 percent of the population living below the poverty line. The importance of creating employment opportunities for its growing labour force in the context of poverty alleviation need not be overemphasized. Consistent with the high emphasis placed on poverty alleviation (10th Plan/PRSP, Three year Interim Plan) by the GoN and the MDG of reducing the poverty level population by half between 1990 to 2015, the Micro Enterprise Development Programme (MEDEP), with the support of UNDP has been working to improve the livelihood of poor families through entrepreneurship development. Micro enterprises are increasingly gaining importance in the context of poverty alleviation in Nepal as in other countries. Recently GoN has come up with Micro Enterprise Policy 2064 to facilitate the growth of micro enterprises as defined by the Policy.1 MEDEP programme currently is active in 31 districts with direct beneficiaries exceeding 40,000 persons (65% being women). On an average incremental annual income per participating entrepreneur has been estimated at US$158 (representing an increase of 282% over base).

MEDEP has been working in several commodity sub-sectors based on market demand, local resource potential, and needs and demands of target groups.2 It is now recognized that MEDEP needs to emphasize on a value chain based approach that provides a systematic basis to achieve significant sub sector level impacts. Value chains encompass the full range of activities and services of market actors required to bring a product or service from its conception to its end use and beyond.3 Value chain analysis helps identify the participants at specific functional levels such as primary producers, processors, product makers, retailers, exporters etc including the identification of strengths and weaknesses at each stage. Such analysis provides a sound basis to develop 1 The Policy defines "Micro-enterprise" as any industry, enterprise or other service business, based particularly on agriculture, forest, tourism, mines, and handicrafts, which meets the following conditions:

I. In the case of a manufacturing industry, enterprise involving the investment of fixed capital of not exceeding two hundred thousand rupees, except house and land, and in the case of a service enterprise, an industry, enterprise involving the investment of fixed capital of not exceeding one hundred thousand rupees,

II. The entrepreneur himself or herself in involved in the management, III. A maximum of nine workers including the entrepreneur are employed, IV. It has annual turnover of less than two million rupees, V. If it uses an engine or equipment, the electric capacity of such engine or equipment is less than

five kilowatt. Provided that notwithstanding anything contained above, any industry or enterprise which manufactures liquors, cigarettes or other tobacco products or for the establishment of which approval has to be taken will not be considered as micro-enterprise. 2 Refer to Annex-2 for basic information on the value chains currently supported by MEDEP. 3 Value Chain Program Design: Promoting Market Solutions for MSMEs, Action for Enterprise

appropriate strategies and implement interventions that will contribute to develop the sub sector to its potential level, increase value addition, and to achieve a significant increase in the number of target beneficiaries4.

1.2 Steps in Value Chain Development

The key steps involved in value chain development are as follows (Chart-1):5

Chart-1: Steps in Value Chain Development

MEDEP has recognized value chain development as an appropriate approach to strengthen selected commodity sub sectors such as allo, Dhaka weaving , incense making, orange/sweet orange. The Scoping Study for MEDEP Phase III (Bajracharya 2007) has emphasized that one important dimension where MEDEP needs to focus its

4 MEDEP has specifically targeted ten commodities/products for value chain upgrading based on value chain analyses of the specific sub-sectors. These are:

1. Allo (Himalayan nettle) 2. Ginger 3. Dhaka fabric 4. Honey 5. Herbal soap 6. Lokta (Nepali Paper) 7. Incense sticks 8. Bamboo products 9. Lapsi 10. Orange (Sweet Orange and Mandarin)

5 www.actionforenterprise.org

2

orientation is to ensure business growth through value chain analysis. The commodity value chains selected and currently supported by MEDEP although not based on rigorous and systematic analysis were selected based on available information from secondary and primary sources from field offices, and partner organizations followed by an assessment of market demand, resource potential, and needs and demands of target groups.

The process of value chain selection basically considered the following factors:6

• Market demand/growth potential including unmet market demand • Potential to increase income at rural level • Opportunities for market linkages (internal and external) • Potential for employment generation • Outreach in terms of number of small enterprises • Potential for value addition • Trade potential/competitiveness • External environment (e.g. government policies, taxes etc.)

Considering its potential Allo, has been identified by MEDEP as one of the commodities/products for upgrading through a value chain based approach to benefit large number of resource poor farm families in the remote mountain areas. The value chain analysis of allo is the first one to be conducted by MEDEP for sub sector strengthening and value chain based micro enterprise development. 1.3 Methodology A preliminary value chain development process was initiated by MEDEP by organizing a one-day participatory workshop (12-14 December, 2008) on the targeted sub sectors including allo. The preliminary value chain analysis of allo included participants from Ramechhap, Myagdi, Parbat, Pyuthan and Darchula districts.7 The workshop was useful to make preliminary investigation to identify the weaknesses and constrains involved for the sub sector development. The study is based on detailed information collected from the field in two districts Parbat, and Myagdi. Field Surveys involved interaction with producers/processors, collection of information at enterprise level, and interaction with local facilitators and service providers. Information from Sankhuwasabha was basically obtained through links in Kathmandu and by telephone conversation with Allo Production Club members in Sankhuwasabha. Important actors in the value chain such as traders, product makers, and exporters were contacted for the necessary information for a complete picture of the sub sector value chain. 6 This closely follows the criteria used by GTZ to select sub-sectors for value chain promotion (GTZ , 2008:20). 7 Duwadi, Vrigu, R., and Gurung, Sita, Preliminary Value Chain Analysis Report, Micro Enterpriose Develoment Programme (MEDEP), Pulchowk, Kathmandu, December 26, 2008

3

A sharing workshop was organized on 7 June 2009 where the tentative findings were presented before the stakeholders for their comments and suggestions. The second half of the workshop was entirely devoted to a brainstorming session that focused on the assessment of market based feasible solutions to deal with the various constraints observed in the allo sub sector value chain. The final revised product is now ready before the readers in the present form. It is important to understand that value chain development is a dynamic process and we learn more as we move ahead with the task of implementing the necessary interventions to support in chain upgrading.

4

Chapter-2

Value Chain Analysis 2.1 Allo Sub-sector Allo (Girardinia diversifolia), plant belongs to the “Urticaceae”, the nettle family. Allo known also as Himalayan Nettle is a fibre yielding perennial plant that grows wild between 1,200m to 3,000m. The stem bark of Allo contains fibres with unique qualities, strength, smoothness, and lightness. The ethnic communities in the hills such as Magars (who refer to the plant as Puwa) in West Nepal and the Kulung Rais of Sankhuwasabha district in East Nepal have for centuries extracted and spun these fibres to make ropes, jackets, porter’s head bands or straps, and fishing nets, etc. Allo is harvested mostly from community and government managed forests. The usual harvesting period runs from Kartik (October/November) to Magh (January/February). As the plant grows above 1,200 meters most areas for harvesting are difficult in terms of access, often requiring number of days to travel to forest, harvest allo, and return with load of allo. There is a lack of data on the potential stock of allo that could be harvested on a sustainable basis. Allo as a forest resource is widely available in high mountain districts throughout the length of the country. The main production pockets in terms of commercial scale harvest are located in Sankhuwasabha district in East Nepal, Nuwakot, Ramechhap, Sindhupalchok, and Dolakha in Central region, Parbat, Myagdi, and Baglung in Western mountains, Rukum, Rolpa, Dolpa, Humla, Jumla, Dailekh, and Pyuthan in the mid west part of the country and Darchula, and Dadeldhura in the far west region. A resource inventory of allo is needed for assessing the full production and processing potential of the sub-sector. 8It can be safely assumed that there is a huge potential of allo fibre production, given the fact that fifty mountain districts out of the country's seventy five districts will likely have the annual growing stock of allo in varying degrees.9 A rough estimation based on average per district potential (in mainly accessible areas) of extracting 36.1 metric tons of dried allo bark yields a total volume of 1,805 metric tons.10 This implies that the present level of fibre/yarn production can be increased three to four times, very easily with the possibility of achieving an industry output level of around 1,000 metric tons of allo fibre/yarn production in about two to three years time. Value chain upgrading with the vision to significantly raise the output levels will provide benefit to thousands of poor resource users with an expanded production, processing, and product development in the allo sub sector.

8 A systematic resource inventory of allo is now being undertaken at MEDEP that will provide information on potential stock and sustainable harvest levels of allo in the country. 9 Excluding 20 Terai, two inner Terai (Udayapur, and Surkhet), Kathmandu, Lalitpur, and Bhaktapur districts. 10 Based on assessment of 13 districts, see Annex-4

5

There is probably no way to ascertain the exact number of primary gatherers of allo from community and government forests all over the country. The number of primary gatherers is roughly estimated to be in excess of 8,000 in over 20 districts. Of the total quantity collected significant amount remains at local level meeting the household need for making essential domestic items. The CFUGs have introduced collection rules as in Sankhuwasabha where one user has to pay Rs.15 for a coupon to bring a Bhari (about 30-40 kg) load on back from that community forest (Barakoti and Shrestha, 2008). Allo Processing Allo is processed following the traditional methods practiced since generations. Usually after its harvest the dry plant is soaked in water for a day before peeling is done. Peeling removes the outer bark and leaves the inner bast fibre for further processing. Dried peeled barks are bundled and stored before further processing can be done. The next step involves cooking inner barks in a drum with wood ash to bleach and make it soft. This takes about 2-3 hours. Although cooking with caustic soda takes less time wood ash is preferred as it does not abrade hands, and is easily available. After cooking there is a repetitive process of beating with wooden hammer to soften and extract fibre and washing in clean water usually done in a stream or river. On an average it takes about 2 hours to clean one kg cooked fibre and a lot of firewood (more than 5 kg for one kg of dry bark of allo). The bundles of clean fibre are then left to dry in the sun. The next step involves soaking fibre in water and mixing either with maize flour (more common in west Nepal), or Kamero (locally available white clay) and drying to obtain a white luster. The fibres are then extracted with the help of simple household tools like forceps. About 2 kg of dried fibre is produced with 5 kg of raw bark of allo. Once the soft fibre is obtained it is ready for spinning into yarn. Mostly, the women are involved in all the stages of collection and processing. The spinning is either done with the help of wooden hand spindles locally called "Katuwa", or with spinning wheel "Charka" which has two common variants hand operated "Haate" and foot operated "Khutte". Spinning with hand spindle is slower compared to a wheel, but the hand spindle is preferred, for example by the Kulung women of Sankhuwasabha as it is reported to be handy and suitable for spinning utilizing the leisure time and allows working simultaneously with other activities like looking after animals. Women doing spinning on a part time basis usually produce about 200-250 gm of spun yarn per day. Machine spinning is done by a few large processors based in Kathmandu that supply yarn to the woolen handmade carpet industry. It is estimated that there are over 1,500 persons majority women involved in spinning, and weaving activities. Dyeing of yarn is done with different plant products for making different colours. The locally available plants are utilized for extracting colours for dyeing. In Sankhuwasabha, allo processors use Banmara to make light green or grey colour, Majitho for red, Dar for brown and Dudhilo to make light yellow colour, using bark and/or leaf of these plants with different proportion of copper sulphate, ferrous sulphate and potassium dichromate (Barakoti and Shrestha, 2008).

6

Allo yarn is woven on different types of looms including the traditional back-strap looms. The more common type of handlooms used for weaving requires two persons to fix/set up to start the weaving activity. A weaver on an average is able to weave 3-4 meters of allo cloth in one full day of work. There are two main product lines including allo cloth and products made from woven fabrics and products made as knit wear. A variety of allo based products mostly knitted such as ladies dresses, shawls, and mufflers etc are made particularly by women groups in four VDCs (Bala, Sisuwa, Tamphu, and Mangtewa) of Sankhuwasabha district in East Nepal that are leading in Allo product making. Several other allo products such as jackets, and bags, etc are made from woven fabrics. The range of products is gradually expanding as allo products are gaining in popularity as exportable handicraft goods. Blending of allo with hemp, silk, and cotton is done to produce yarn and fabrics mainly to cater to the export demand. 2.2 Mapping the Value Chain The value chain map generally represents the micro and meso levels of the value chain actors. The basic functions and chain operators including the operational service providers constitute the micro level of the value chain. There are also value chain supporters who are not dealing directly with the product as the chain operators but provide useful support services and are classified under the meso level of the value chain. These include agencies that basically provide the support services benefiting the whole value chain including the common interests of all the value chain actors. Value chain map helps understand the functional levels of the chain and the operators associated with the levels including the linkage at different levels of the chain, thus facilitating the analytical study of the chain with such visual representation. The chain enablers are basically government agencies or public sector agencies responsible for shaping the policy environment, as such are classified as the macro level of the value chain. The allo value chain map (Chart-2) shows the functional levels and chain operators (micro level). As estimated there are over 8,000 primary collectors/gatherers of allo from community/national forests in over 20 districts of the country. Allo Cloth Production Club members in the four VDCs of Sankhuwasabha (Bala, Sisuwa, Tamphu, and Mangtewa) are important actors in the chain especially in production of woven and knitted allo products which are mostly marketed through Fair Trade Shops/exporters based in Kathmandu. MEDEP micro entrepreneurs are mostly involved in spinning and weaving allo fabrics on handlooms either individually or as group using Common Facility Centres (CFCs). The arrows in the map indicate the relationship or coordination between chain operators. The main inputs in allo production and processing are dyes (both chemical and vegetable), caustic soda, and wood ash for bleaching, and maize flour and Kamero (white clay) for softening and fibre separation. Allo processors use very basic types of mostly locally available inputs such as wood ash and Kamero. Most products are not dyed and sold in their natural patterns. Vegetables dyes produced from herbs and forest products

7

rather than chemical dyes are commonly used to dye allo products and these are available locally and also through dealers. These are a number of traders in Kathmandu dealing in the main ingredients used in preparing vegetable dyes such as Majitho, Chutro, Anar ko Bokra, Harro, Barro, Okhar ko Bokra, Khayar, etc. A few manufacturers based in Kathmandui are supplying equipment such as spinning charkhas including foot operated Khuttee charka and wheel charkha, and handlooms. The charkhas cost between Rs 4,500-Rs 5,000 in Kathmandu. Trading activity in allo is both in terms of raw allo and spun yarn. Village based traders collect raw allo or spun yarn from village processors and sale to the large traders based in Kathmandu who are the main suppliers of spun allo yarn to the carpet manufacturers. It is interesting to note that allo yarn is increasingly being used as backing for Tibetan carpets and to weave carpets. Wholesale and retail trading activities are carried out by several handicraft shops including Fair Trade Shops mainly based in Kathmandu in the main tourist areas. The producers affiliated to the Allo Production Club in Sankhuwasabha have well established links with various fair trade shops that source allo products for sale in their outlets and for export. On the other hand the marketing linkages of MEDEP promoted allo entrepreneurs remains weak. The sales outlets of DMEGAs/NMEGA known as "Saugat Grihas" are poorly functioning at present due to weaknesses in terms of managerial capacity as well as inadequate working capital base to procure and market the products of MEs. Most allo processors especially from the remote mountain districts such as Rukum, Rolpa, Dolpa, Humla, Jumla, Dailekh, and Pyuthan depend on the village traders and traders based at Dang and Nepalgunj with some having direct contact with the large Kathmandu based traders to market allo yarn. Due to weak information about prices and market conditions the yarn producers from these remote districts have no option but to sale yarn at the prices offered by the traders who often benefit with huge margins. Carpet industry occupies the prominent position as it uses between 120-160 metric tons of allo yarn, representing over 80 percent of an estimated 150-200 metric tons of total allo yarn production in the country. Allo products are relatively less well known compared to hemp products as export items. There are roughly about 20 traders/exporters mostly Kathmandu based that export some allo based products although not in big quantity and in regular manner.

8

Chart-2: Value Chain Map (Micro Model) ________________________________________________________________________

9

Exporting

Retailing

Product Making

Weaving

Yarn Making

Bark collection

Input supply

Collectors/gatherers (N›8,000)

Allo Club Sankhuwasabha (N=950). Mainly knitted products Kathmandu based (N≥25)

Local traders (N›100)

Carpet industry (N≥50). Uses between 120-160 metric tons of spun allo yarn (in one year) as input in carpet making.

Exporters of allo/hempProducts (N≥25)

Suppliers of cotton, silk, linen, hemp, chemical dyes, Vegetable dyes, and caustic soda

Tourists from US, EU, and Japan Importers (carpets, allo/hemp products) in US, EU, Japan

Handicraft/gift shops/fair trade shops (N≥25)

DMEGA/NMEGA Outlets

Trading

Small processors/Yarn makers (N›1,000)

Large traders (N≥25)

MEG members (N=767) Mainly weaving allo fabrics

2.3 Meso-Level Providers of Support Services The chain supporters are meso level of the value chain with a facilitating role that benefits the chain actors. MEDEP (with the funding support of UNDP and AusAid) has a significant role in the expansion of allo value chain with active entrepreneurship development targeting the poor families, and disadvantaged communities. MEDEP has actively supported allo value chain with its implementation modality based on entrepreneurship development, skill training, appropriate technology, and marketing linkages. It has supported micro entrepreneurs to develop market linkages through their participation in trade fairs, and exhibition. The institutions such as DMEGAs/NMEGA representing the entrepreneurs and BDSPOs/NEDC representing the service providers have a crucial role as supporters and service providers in the allo sub-sector. BDSPOs are NGOs with overall facilitating role with implementation responsibility of MEDEP programme activities including those related to allo in close collaboration with DDC/DEDC which manages the Enterprise Development Fund (EDF), a joint fund of MEDEP contributed and DDC own resource for micro enterprise development in the district. District Forest Office (DFO) plays a key supporting role as regulating agency for the sustainable extraction of forest based resource like allo. DFO regulates trade in NTFPs including allo, lokta, and medicinal plants and herbs. As allo is mostly collected from community forests there is a close coordination between District Forest Offices and CFUGs, the later prepares operational plan of respective community with resource inventory and extraction plan of allo and other forest products. Federation of Handicraft Associations of Nepal (FHAN) is a service oriented non-profit organization of private sector business and artisan community. It helps its members to improve their productivity, explore markets and introduce them to the international arena. It also works as liaison between its members and the Government and Non-Government Organizations. 11 FHAN is making important contribution to develop the country's handicrafts sector by organizing trade fairs/exhibitions domestically and through participation in international trade fairs, providing training, and quality assurance. In 2004 FHAN in collaboration with GoN established Handicraft Design and Development Centre (HANDECEN) to help develop quality products, and venture into product diversification for overall development of Nepalese handicrafts. The centre is providing services related to Traditional & Contemporary Designs, Virtual 3D Products, Prototype Design, Logo & Firm Registration, Research & Development, Training & Seminar, and Consultancy Services. The design centre although currently more focused on Pashmina has the capacity to provide services in improving the design of allo fabrics to suit demand of international markets. Fair Trade Group Nepal (FTG Nepal) is a consortium of fair trading organizations (registered as an NGO in 1996) working with the aim to uplift socio-economic status of underprivileged and

11 The statute of Handicraft Association of Nepal (HAN) in its article 1.4 (i) has defined "handicraft industry" as "an industry that manufactures a product reflecting the country's tradition, art and culture, and/or uses labor intensive specialized skills, and/or uses indigenous raw material and/or resources"

10

marginalized producers of Nepal. FTG Nepal strives to develop collaboration among the fair trading organizations to promote fair trade practices in Nepal. The members of FTG Nepal (16 at present) are providing business support services to their producers. These include providing operating fund for production, small capital investment, design inputs, training, and providing access to the local and international markets. Some FTG Nepal members notably Mahaguthi, Sana Hastakala, Manushi, and Association of Craft Producers/Dhukuti have linkages with several allo producers groups. Such linkages have facilitated sourcing of inputs for the producers' groups and marketing of products. However, majority of allo producers/weavers in different districts still remain outside the ambit of such formal linkages. The experience and institutional capacity of the FTG members can greatly contribute to upgrade the product quality of allo entrepreneurs to meet the requirements of the export market. The following Table-1 lists the different support services provided by agencies and organizations at Meso level of the value chain. Table-1: Support Services provided by Agencies/Organizations at Meso Level Agencies/Organizations Support Services

DFO • Regulates access to national forests for allo and other NTFP extraction • Issues permit (chut purje) to traders to transport semi-processed/processed

allo outside district MEDEP • Social mobilization of target groups (below poverty level)

• Training (entrepreneurship and skill training) • Institutional development (BDSPOs, DMEGA and NMEGA), • Technical and marketing support.

DDC • DEDC coordinates micro enterprise development programme in district • Manages EDF that includes MEDEP and GoN matching funds for micro

enterprise development in the district. CFUG • Prepares Operation Plan of community forest

• Ensures sustainable extraction of allo BDSPOs12 • Overall facilitation for micro enterprise development and provider of services

for micro entrepreneurs supported by MEDEP FHAN/HENDECEN • Promotional activities in domestic and international markets for handicrafts

• Support on product design, research and development FTG-Nepal • Promotion of Fair Trade

• Capacity building of Business Support Organizations, Enterprises, and Producers.

2.4 Macro Level Enablers The government Ministries at macro level help to create a conducive environment in which value chain actors are able to maximize the benefits of participation. GON policies create an enabling environment for micro enterprises to expand. The recent Micro Enterprise Policy-2006 has been instrumental in defining the scope of micro enterprises and has outlined GON policies to support 12 BDSPOs are non-government organizations (NGOs) promoted by and partnering with MEDEP to implement programme components (as service providers) and to facilitative micro enterprise development in the districts covered by MEDEP.

11

the micro enterprises. Besides, MOI, two other ministries MOFSC and MOEST are directly related to the value chain in consideration with a number of Acts and Rules to govern the extraction and management of forest resources and the regulations concerning the environment (such as the requirements for carrying out Initial Environmental Examination (IEE)13 and Environmental Impact Assessment (EIA)14 for resource users. TEPC, a national trade promotion organization under the Ministry of Commerce and Supplies works for promotion of export trade with its role in policy formulation, information dissemination, and related support services. FNCCI is the apex body representing the commercial and industrial sectors with a policy advocacy role on trade and issues related to private sector development. FNCCI actively supports private businesses to showcase their products through the trade fairs and exhibitions. FECOFUN is a national level umbrella organization of CFUGs with basically advocacy role related to the management of community forests. The following Table-2 shows the role of different Ministries and national level organizations in creating an enabling environment for vale chain upgrading. Table-2: Ministries and National Organizations and their Role at Macro Level

Ministries/national level organizations

Role as enabler in value chain promotion

MOI • Implemented Micro Enterprise Policy-2006 • Registration of patent, design, and trade mark (Department of Industry).

MOFSC • Formulation and implementation of policy, and plans related to forest, natural environment, and bio-diversity (Master Plan for Forestry Sector-1989, Forest Act 2049 and Rules 2051, Medicinal Plant and NTFP Policy-2004)

TEPC • Advise GoN in formulating policies for the development and expansion of trade and export.

• Act as information pool by collecting, disseminating and publishing useful trade-related information.

• Simplify the procedures relating to quality control, insurance and transport and enhance support services for export transaction

MOEST • Formulation, implementation, Monitoring & Evaluation of policies, plans and programs pertaining to environment, science and technology.

• Regulatory role in accordance with Environment Protection Act-1996 (Revised on 2008), Environmental Protection Rules 1997 that include provisions for carrying

13 "Initial Environmental Examination" means a report on analytical study or evaluation to be prepared to

ascertain as to whether, in implementing a proposal, the proposal does have significant adverse impacts on the environment or not, whether such impacts could be avoided or mitigated by any means or not.

14 "Environmental Impact Assessment" means a report on detailed study and evaluation to be prepared to

ascertain as to whether, in implementing a proposal, the proposal does have significant adverse impacts on the environment or not, whether such impacts could be avoided or mitigated by any means or not.

12

IEE and EIA. FNCCI • Policy advocacy on trade and issues related to private sector development15.

• Support through trade fairs and exhibitions. FECOFUN • Umbrella organization of community forest user groups with mainly advocacy

role16. 2.5 Role of Donors The key issue of donor intervention is leveraging of resources for wide impacts at the sub sector level. The pertinent questions are: How do development agencies work for systemic change to reach tens of thousands of people rather than apply direct assistance to help a few enterprises or farmers? At which points can leverage be applied to reach the intended systemic change in a sector? (SDC, 2007). Donor resources are best utilized when donors/development agencies intervene in value chains with the potential to upgrade and the outcomes are in the public interest such as improved food security, poverty alleviation, and promotion of environmentally sound practices. In Nepal, donors such as USAID, GTZ, and SNV have been emphasizing on value chain based approach to develop potential sub sectors. Such emphasis by donor agencies has helped create a body of knowledge on the approaches, methodologies, and the practical aspects of strengthening the targeted value chains of a variety of commodities/products. In reference to allo KHARDEP a British aided project identified the potential of allo as one of the sources of income generation for poor farm families in the mountains of East Nepal and provided support to allo producers groups in the late eighties that helped create the opportunity for commercialization of allo. Donor resources are used to support allo chain upgrading in several districts such as the IFAD funded Western Uplands Poverty Alleviation Project (WUPAP) which supports allo value chain participants in selected districts including Bajhang, Bajura, and Jajarkot. With the initiative of RSDC/SDC the allo interest groups in Bajhang have formed a network organization Rilu-Masta Allo Bhangro Sanjal in 2062/63. There is scope for collaboration between MEDEP and WUPAP in common project districts such as Dailekh, Kalikot, and Jumla to strengthen the value chain for the benefit of poor farm families. 2.6 Market Analysis Allo like hemp is an important natural fibre with strong local traditions of spinning and weaving especially among mountain communities and ethnic groups such as the Magars of West Nepal and Kulung Rais of Sankhuwasabha district in East Nepal. Despite being classified as a coarse fabric with husky texture it nonetheless has good demand from tourists who are the main buyers of allo products mainly as gift items. In recent yeas there has been product diversification from the traditional pure allo fabrics to blended fabrics (with silk, cotton, and hemp) to make it more acceptable to customers. New products like ladies dresses and shawls (knitted items) are now

15 FNCCI is currently implementing (jointly with MoAC), the OVOP Programme focusing on sweet orange, lapsi, rainbow trout fish, and Bel. 16 There are a total of 14,389 CFUGs covering 1.2 million hectares of community managed forest land, and over 1.6 million beneficiary households.

13

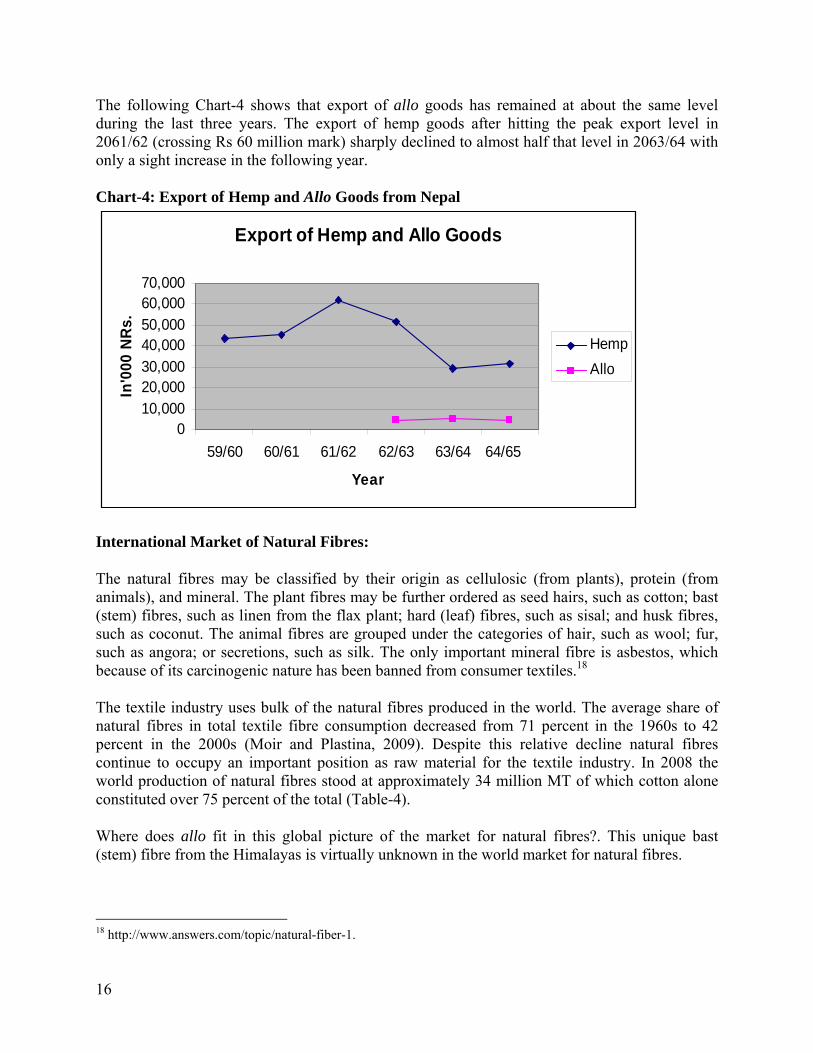

becoming available especially produced by Allo club members in Sankhuwasabha district and these have good export potential. . Allo yarn is one of the main processed products in the value chain. The country’s important carpet industry has now emerged as the main buyer of allo yarn consuming over 80 percent of an estimated total of 150-200 metric tons of spun allo yarn produced in a year17. The remaining quantity of yarn is used for making woven fabrics and other products basically for selling locally to tourists and for export. With rising demand from carpet industry price of allo yarn has remained between Rs 450-Rs 600 per kg, although price of high quality thread for knitting may go above Rs 800 per kg. Presently, export of allo goods in comparison to hemp has remained stable, though at a relatively much lower level whereas export of hemp goods has declined significantly since reaching a peak level in the year 2061/62 (Chart-4). The prevailing market price of hemp yarn is about Rs 150 per kg due primarily to slackness in export demand. The main allo products are shawls (Rs 750-800 per piece), table mats (Rs 300 for set of 6 pieces), ladies dresses (Rs 850-2,500), bags (Rs 600-700 per piece), purse (Rs 70). The price of Allo cloth ranges from Rs 300-350 per meter depending on the width (26” or more). Blended fabrics fetch relatively higher prices such as allo-silk (Rs 700 per metre), and allo-cotton (Rs 350-450 per metre). Most of these products find their markets in overseas countries as handicraft items. In the year 2007/08 (FY2064/65) Nepal exported a total of Rs 2,682.8 million worth of handicraft goods composed of Rs1,463.4 million textiles and Rs 1,219.4 million non-textiles (Annex-1). Within the broad textile category the relative size of allo is quite small in comparison to other textile items (Chart-3). The total export of allo goods was Rs 4.8 million compared to over Rs 60 million of hemp goods exported. Hemp as natural fibre is well known in the international markets as compared to allo which is yet to establish its own individual product identity in the international market for natural fibres as a unique product from the Himalayas. Export of allo products is based on the basis of orders received from importers of natural fibre products and yarn in the overseas countries by exporters based in Kathmandu for specific products which mainly belong to the following two categories:

1. Allo (nettle), hemp, and cotton blended fabrics. Such blending may come in different proportions (such as 31% hemp, 33% allo, and 36% cotton). 2. Natural knitwear consisting mainly of:

• 100% Allo knitwear • Allo and silk twisted knitwear, and • Allo and Linen twisted knitwear.

The main export destination of Nepali allo goods is the US accounting for nearly one third (31.9%) of the total export value of Rs 4.8 million, followed by Sweden (21.2 percent), Japan (17.9 percent), France (6.7 percent), Australia (6.5 percent), and Italy (5.9 percent) as shown in the Table-3. 17 This estimation is based on information collected from value chain operators at different functional levels. As it is difficult to arrive at single acceptable figure the range as given provides a good approximation of the size of allo industry in terms of annual yarn output.

14

Chart-3: Export of Handicraft Products from Nepal (Textile)

Felt SilkWool

Table-3: Export of Allo Goods by Destination (2007/08)

Country Amount (Rs) Percent USA 1,541,974 31.9

Germany 82,620 1.7

Japan 866,313 17.9

Italy 287,749 5.9

UK 160,944 3.3

France 323,698 6.7

Canada 68,476 1.4

Netherlands 41,893 0.9

Australia 314,666 6.5

Sweden 1,027,745 21.2

Finland 58,188 1.2

Others 66,887 1.4 Total 4,841,153 100.0

Source: Nepal Overseas Trade Statistics 2007/08, Trade and Export ProCentre, Pulchowk, Lalitpur, Nepal

15

Pashmina

Cotton Hemp Dhakam

Allo

o

Others

tion

The following Chart-4 shows that export of allo goods has remained at about the same level during the last three years. The export of hemp goods after hitting the peak export level in 2061/62 (crossing Rs 60 million mark) sharply declined to almost half that level in 2063/64 with only a sight increase in the following year. Chart-4: Export of Hemp and Allo Goods from Nepal

Export of Hemp and Allo Goods

010,00020,00030,00040,00050,00060,00070,000

59/60 60/61 61/62 62/63 63/64 64/65

Year

In'0

00 N

Rs.

HempAllo

International Market of Natural Fibres:

The natural fibres may be classified by their origin as cellulosic (from plants), protein (from animals), and mineral. The plant fibres may be further ordered as seed hairs, such as cotton; bast (stem) fibres, such as linen from the flax plant; hard (leaf) fibres, such as sisal; and husk fibres, such as coconut. The animal fibres are grouped under the categories of hair, such as wool; fur, such as angora; or secretions, such as silk. The only important mineral fibre is asbestos, which because of its carcinogenic nature has been banned from consumer textiles.18

The textile industry uses bulk of the natural fibres produced in the world. The average share of natural fibres in total textile fibre consumption decreased from 71 percent in the 1960s to 42 percent in the 2000s (Moir and Plastina, 2009). Despite this relative decline natural fibres continue to occupy an important position as raw material for the textile industry. In 2008 the world production of natural fibres stood at approximately 34 million MT of which cotton alone constituted over 75 percent of the total (Table-4).

Where does allo fit in this global picture of the market for natural fibres?. This unique bast (stem) fibre from the Himalayas is virtually unknown in the world market for natural fibres.

18 http://www.answers.com/topic/natural-fiber-1.

16

Table 4: World Natural Fibre Production (2008)

Type Production '000 MT Percent

Cellulosic Cotton 25,360.8 75.4 Jute and Jute like fibres 3,198.1 9.5 Flax 935.2 2.8 Coir 1,111.3 3.3 Sisal and Agaves 431.0 1.3 Ramie 179.4 0.5 Hemp 75.9 0.2 Sub-total 31,291.6 93.0 Protein Wool 2,191.1 6.5 Silk 156.1 0.5 Sub-total 2,347.2 7.0 Total 33,638.8 100.0

Source: FAO (http://Faostat.fao.org).

Hemp and linen are likely to be closest competitors in the international market for allo as a natural fibre on longer term perspective. However, even with significant upscaling of extraction and processing of allo the total quantity will be nowhere close to the levels of production of linen and hemp. Allo should be promoted as a fibre with unique qualities unlike any other fibre (such as its insulating property), with the added value due to its association with Himalayas and the age old weaving traditions of the poor resource users belonging to the disadvantaged mountain ethnic groups. Establishing a unique identity for Allo may be challenging but it appears that niche markets for unique fibres such as allo do exit in the apparel industry in the developed economies that should be taken advantage of. "Natural fibres face the challenge of developing and maintaining markets while competing with manufactured fibres. In some cases this might involve defining and promoting market niches; in others, conducting research to develop new technologies to facilitate the use of natural fibres in new applications where their natural advantages allow them to compete effectively with manufactured fibres (Moir and Plastina, 2009)." It is encouraging that some initiatives are already underway to promote Nepali allo products in Europe, such as through e-commerce initiative of Karma, an Ecological and Ethical Online shop (www.karmashop.fi). Quality spinning and product development has been initiated on trial basis in collaboration with one of Europe's known fashion houses by Himalayan Wild Fibres, an American private company, which is encouraging for the potential growth of exports of allo products from Nepal provided it leads to availability of new technology for improving the quality of spun yarn.

Exporting fibre rather than spun yarn overseas does not seem to be an attractive option for the future growth of the allo industry. It might be considered an attractive option in the short run as quality of yarn spun overseas using sophisticated technology will be much higher relative to locally spun yarn. However, in this case much of value addition will take place outside the country thus helping little to alleviate poverty in the country by increasing income of the allo entrepreneurs. Hence, for long term competitiveness of allo vis a vis other natural fibres in the international market there must be technological improvements in fibre extraction and spinning

17

to produce high quality yarn locally that could either be exported or used to produce variety of products with good demand in domestic and international markets.

2.7 Gross Margin, Profit, and Value Addition The following Table-5 shows the estimated gross margin, and profit from activities at different functional levels of the allo value chain thread/yarn making, weaving, and product making. One kg of allo yarn fetches a gross margin of Rs 100 and profit of Rs 89 which goes up as it moves to downstream functions such as weaving and production of allo goods. Product making such as allo bags using woven fabric (with one kg yarn and about 3-4 metres of cloth) on an average has a gross margin of Rs 1,775 and profit of Rs 1,665.5 representing 49.3 percent and 46.3 percent respectively of the sales value. Similarly, in carpet making gross margin is calculated at Rs 1,050 with the profit margin of Rs 550 in the production of one square meter of 80 knots carpet. The allo enterprises taking up different functions such yarn making, weaving, and product making including carpet making are profitable at the given level of production technology and management. However, presently the micro entrepreneurs operating individually or as members of MEGs (in the case of MEDEP) are at low level of production scale that affects the total income as allo entrepreneurs. MEDEP supported CFCs are mostly operating well below their production capacity despite favourable demand conditions. The annual average output per weaver was observed to be just 64 meters of allo fabric (worth about Rs 22,000) in one of the CFCs in Saliza, Parbat district. The possible reasons being lack of appropriate skill, equipment and part-time nature of activity. Most women allo entrepreneurs are undertaking production and processing activities as secondary to agriculture to be done during leisure time after household work. Allo entrepreneurs are therefore unable to reap the full benefits (increased family income) of participation in the value chain. An additional factor seemed the practice of involving allo entrepreneurs by BDSPOs as resource persons to train other MEs that might have affected the overall group production efficiency due to the prolonged absence of key member of the group. Table-5: Gross Margin and Profit Analysis at Different Levels of Allo Value Chain (Unit: Rs)

Collection Yarn Making Weaving Product Making Carpet

Sales Revenue Sale 150 500 1,225.0 3,600.0 5,000 Less: Cost of goods sold 150 400 893.0 1,825.0 3,950 Gross Margin 0 100 332.0 1,775.0 1,050 Less: administrative costs 0 0 0.0 36.0 100 Less: Marketing expenses 0 0 12.3 54.0 0 Less: Depreciation 0 11 39.0 19.5 400 Less: Interest on loan 0 0 0.0 0.0 0 Profit 0 89 280.8 1,665.5 550 Gross Margin (%) 0 20 27.1 49.3 21.0 Profit Margin (%) 0 17.8 22.9 46.3 11.0 Note:

1. Calculations based on one kg of allo yarn except for carpet making which represents one sq. meter of 80 knots carpet

2. Collection activity commonly integrates with thread making. However, the above calculation considers collection as a wage earning activity.

18

Value Addition: The net (of intermediate inputs) value added at different levels of operation shows the product making and retailing stage capture the most value in the chain (61 percent). Based on the final retail price of product corresponding to one kg of yarn (Rs. 3,600) the value addition at different stages are calculated to be Rs 150 (4 percent) at collector's level, Rs 350 (10 percent) at the level of yarn making, Rs 900 (25 percent) in weaving activity, and Rs 2,200 (61 percent) at the level of product making. Chart-5: Value Added at Different Functional Levels of Allo Value Chain The shares of added value at different stages arethat chain operators’ incomes can be significantlyadded activities notable to the level of weaving fa

10%

19

Yarn akingM

shown increabrics an

Weaving

in the following Chart-5. It is evident sed through gradual shift to higher value d product making.

25%

Chapter-3

SWOT Analysis and Identification of Constraints and Solutions 3.1 SWOT Analysis of Allo Sub-sector An analysis of the strength, weakness, opportunity, and threat (SWOT) has been conducted for the allo sub sector with respect to the value chain functions such as input supply, production, processing, product making, and trade. The details given on Table-6 make it clear that allo sub sector has high potentiality to grow given the abundance of resource in the form of the highly regenerative allo plant. The processing basically requires inputs that are locally available such as wood ash, Kamero (white clay) and ingredients for preparing vegetable dyes for colouring. The equipment such as charkhas of various designs (for spinning), and looms are manufactured in country. The ethnic communities in the mountain areas such as the Kulung Rais of Sankhuwasabha district in East Nepal have long weaving tradition of allo fabrics as these have a significant place in the rituals. The main weaknesses in the value chain are poorly organized collection and the rudimentary methods of fibre extraction, and spinning which leads to low quality of yarn. Similarly, there is lack of product diversification, and variety in terms of designs. Most allo products are in natural colours with some colouring done by using vegetable dyes. However, the quality of vegetable dyed yarn is poor in terms of consistency and permanence of colours. There are opportunities to strengthen allo value chain by integrating allo producers into the supply chain of the members of FTG-Nepal to benefit from their extensive experience on new product development, and export of handicraft items to the overseas markets. The critical factor seems the need to upgrade the quality of processed fibre and yarn using improved methods and equipment. On a long terms basis allo producers should be able to benefit by establishing a distinct product identity for allo based on collective logo. Threats in the value chain are likely to emerge from quality deterioration by possible mixing with other fibres such as jute and hemp in the absence of effective quality control mechanism and industry code of conduct. In addition competition from relatively cheaper fibres such as hemp, and jute in the natural fibre markets might threaten the growth of allo industry. Over exploitation of resource beyond sustainable limits and excessive use of firewood to process are some of the environmental concerns to potentially act as threats to long term sustainability of the allo industry.

20

Table-6: Strength, Weakness, Opportunity, and Threat (SWOT) Input/Equipment supply Production Processing Product Making TradeStrength • Inputs such as ash,

lime, maize flour, Kamero (white clay) and ingredients for vegetable dyes are available locally.

• Manufacturers of equipment (Charkhas and looms) based in Kathmandu

• Abundantly available in community and government managed forests.

• Long tradition of processing among ethnic communities in the mountain areas.

• Trained (skilled) entrepreneurs to process allo

• Tradition of making allo products

• Locally trained entrepreneurs

• Increasing demand of natural fibre products

• Used as gift items

Weakness • Lack of seed for cultivation on private land.

• Unorganized nature of input supply especially vegetable dyes

• Lack of reliable data on potential sustainable yield from forests

• Poorly organized collection • Difficult to collect in the wild

especially for women • Production areas lack road

access.

• Cooking raw allo takes long time and needs lot of fuel wood

• Rudimentary methods of fibre extraction (labour intensive)

• Needs lot of water for processing

• Low quality of vegetable based colour dyes

• Low quality of spun yarnproduced

• Lack of regularity

on product making

• Lack of skill on making knit wear products

• Lack of product diversification

• Poor quality of spun yarn to meet international standards

Opportunity • Vegetable dyes can be produced using locally available plant resources

• Possibility of cultivating on private farm land.

• Possibility ofimproving quality of spun yarn using motorized charkhas, better extraction methods.

• NGOs/Fair Trade Groups actively involved in new product development

• Increasing awareness and demand forblended fabrics in international markets.

• Establishing identity through collective mark (logo)

• Linking producers' groups to members of FTG-Nepal

• Increasing demand for natural fibres (wild) international markets

21

Threat • Dependent on import of chemicals (dyes) from India

• Over exploitation beyond sustainable harvest levels

• Might lead to deforestation due to increased demand for fuel wood to process allo

• Mixing with jute and hemp might affect quality.

• Competition from relatively cheaper fibres such as hemp, and jute in the natural fibre markets

22

3.2 Value Chain Constraints and Possible Solutions The allo value chain constraints are identified according to the main categories of input supply, technology, market access, organization and management, finance, infrastructure, and policy. This framework provides the basis on which possible solutions can be identified. The solutions selected for interventions should be commercially feasible or market based to the extent possible (except policy and infrastructures) without having to depend on subsidy element. The provision of services should be ensured in a competitive manner implying that there are multiple providers of the products and services required to strengthen the value chain. It has been observed that weak institutional capacity of service provider organizations (BDSPOs) has constrained value chain upscaling in the case of target commodities including allo in MEDEP districts. Institutional weaknesses have mainly manifested in inadequate technical supports for access to appropriate processing technologies and equipment and weak market linkages. As a result many of the MEGs are observed to be functioning quite below the optimal levels with lost opportunities for income generation which could have been avoided by making MEs fully active, rather than the more common situation of semi active or inactive entrepreneurs. Inputs Supply: On input supply the main identified constraints are lack of quality vegetable based dyes for dyeing allo fabrics. Unavailability of seed and knowledge of cultivation practices of allo have also been identified as constraints on the inputs side.

Technology: Allo processing relies on very rudimentary technology carried over since generations resulting in poor quality of fibre and spun yarn. The traditional methods employed in processing yields poor quality fibre which hardly provides the material for producing quality yarn. The capacity of equipment manufacturers to produce appropriate equipment for fibre extraction, and spinning is limited especially in the case of fibre extraction.

Market Access: Marketing continues to be a weak link as producers/processors and not properly linked with traders/product makers, wholesalers/retailers. To facilitate and improve marketing of products produced by micro enterprises MEDEP has been supporting the establishment of sales outlets (called Saugat Grihas) at district, regional and at central level managed by DMEGAs and NMEGA. However, most sales outlets are performing very poorly primarily due to lack of sufficient working capital, and knowledge of conducting business.

Organization and Management: In terms of organizational strength DMEGAs and NMEGA are weak and lacking in professional management. The poor record keeping by members of MEGs is a constraint for monitoring the success or otherwise of the promoted enterprises. BDSPOs/NEDC and DMEGAs/NMEGA are yet to be fully institutionalised and are in need of continued support for their institutional capacity strengthening. Finance: Finance is another weak link in allo value chain development. It is estimated that overall only 23.7% of MEDEP entrepreneurs have access to credit from MFIs. This has resulted mainly from remote location of most enterprises especially so in the case of allo as the established MFIs are not providing services in the remote areas. Moreover, the formal link through ADB/N that existed during Phase-1 of MEDEP was discontinued after ADB/N withdrew

23

from micro-finance sector in 2005 resulting in reduced access to micro credit funds to members of MEGs. As a consequence the new MFIs with whom MEDEP has now entered into partnerships are charging interest rates between 18%-24% which are higher than that previously charged by ADB/N. In the given situation where established MFIs are not extending their coverage to the remote areas, MEDEP has turned its attention to the identification and mobilization of local MFIs such as SCCs, FINGOs, and Rural Development Banks to increase the access of micro-entrepreneurs to credit. The possibility of formation of new SCCs by micro entrepreneurs should be explored. In this regard, MEDEP can collaborate with Nepal Federation of Savings and Credit Cooperative Unions Ltd. (NEFSCUN) the national apex body for Savings and Credit Cooperatives and their District Unions to utilize their expertise in capacity building. Infrastructures: Most allo collection/processing areas are located in remote high altitude areas the road access continues to be a problem. In most production areas due to lack of road access raw/processed allo has to be transported over long distances either by mules or by porters. It still takes almost two days of walk to reach the main allo production areas in Sankhuwasabha from the nearest airport located at Tumlingtar (with flight connections to Biratnagar, and Kathmandu). Moreover, in some remote districts such as Jumla, transporting equipment such as Charkhas is prohibitively costly adding up to 60 percent to the equipment cost due to the high costs of airfreight.

Policy: As a forest product the extraction of allo comes under the regulatory provisions of Environment Protection Act-1996, and Environment Protection Rules 1997 that include the requirements for carrying out Initial Environmental Examination (IEE) and Environmental Impact Assessment (EIA) for forest based enterprises. As per Environment Protection Rules 1997, IIE is required to be undertaken in case of collection of between 5 to 50 tons of forest products other than timber per year, whereas EIA is required for collection of more than 50 tons of forest products other than timber per year. These regulations might affect the establishment of allo processing enterprises as conducting IIE and EIA are likely to be considered as complicated and time consuming. In addition there is also the regulation that restricts establishment of any forest product based enterprise within a distance of one km from the forest in the case of hill areas.

Policy related issues also include regulations on transportation of raw/semi-processed allo outside of district as processors/traders need to obtain the "chut purje" from the concerned District Forest Office (located at district headquarters) which requires number of days of travel in some cases. These rules can and should be simplified especially in the case of product like allo which is highly regenerative and virtually without any adverse effects on the environment in accordance with the NTFP Policy that clearly mentions that the provisions of Environment Protection Act-1996, and Environment Protection Rules 1997 will be reviewed from the perspective of their practicality to help in the commercial development of herbs and NTFPs. The following Table-7, and Table-8 present the constraints by major categories, the identified solutions and the providers.

24

Table-7: Constraints, Solutions, and Providers Type/Category Constraints Solutions Existing/Potential providers Inputs Supply • Inadequate knowledge on

preparation of vegetable based dyes

• Lack of seed supply for cultivation

• Provision of training on vegetable dyes preparation

• Establish nursery for seedling production. • Provide information on cultivation

practices of allo

BDSPOs DFO, CFUG

Technology • Lack of appropriate fibreextraction, and spinningequipment/technology.

• Shrinkage of woven fabrics due tolack of pressing machine.

• Provision of appropriate fibre extraction equipment, and spinning charkhas for quality yarn production

• Provision of training on processing and quality spinning.

• Provision of pressing machine for woven fabrics to avoid shrinkage.

Private manufacturers/dealers of equipment Foreign importers (design) Local handicraft/fair trade shops CSIDB

Market Access • Inadequate marketing linkage of producers with retailers/wholesalers/exporters

• Provision of marketing outlets • Integrate producers' groups into the

supply chain of members of FTG-Nepal. • Provision of information on overseas

markets for export • Increased participation in trade fairs and

exhibition.

DMEGA/NMEGA TEPC/CCIA FNCCI CSIDB

Organization and Management

• Weak institutional capacities of BDSPOs/NEDC and DMEGAs/NMEGA

• Poor record keeping of MEG business

• Lack of organization representing Allo industry.

• Provide training on business plan preparation and record keeping (including product pricing)

• Facilitate formation of an association of allo entrepreneurs.

BDSPOs DMEGA/NMEGA

Finance • Lack of access to credit from MFIs.

• Inadequate working capital of DMEGAs and NMEGA

• Access to credit through formation of Savings and Credit Societies (SCCs).

• Submit the proposal of the programme to DDC and VDC to access the budget.

• Use the revolving fund of CFUG. • Linkage with traders/exporters

FINGOs,/SCCs NEFSCUN CFUG DDC/VDC Traders/Exporters

Infrastructure • Inadequate road access linking production areas to markets

• Provision of road access to major market centres

DDC/VDC, MoLD

Policy • Complex regulations on transport of raw and semi-

• Simplify the regulations on export of raw and semi-processed allo

DoF, DoI

25

processed allo outside district. • Restrictive polices regarding IIE,

EIA and location of forest based enterprise

• Stock of resources not identified. • Lack of policy on registration of

collective mark (logo)

• Simplify the existing provisions of IEE, EIA and location of forest based enterprise

• Inventory taking to determine sustainable harvest level of the resource.

• Formulate policy on collective mark (logo) registration for product identity.

26

Chapter-4 Upgrading the Allo Value Chain

4.1 MEDEP Interventions in Allo Value Chain MEDEP primarily targets families with incomes below the nationally defined poverty level with emphasis on inclusion of disadvantaged indigenous groups "janjatis", "dalits", religious minorities (such as Muslim community), women, and youth as beneficiaries. The entrepreneurship development model is a six step process that encompasses social mobilization, entrepreneurship training, skill training, micro credit, appropriate technology, and Marketing/business counseling. Such a holistic approach differs from conventional skill training based approach to enterprise development. Value chain analysis is now considered an integral part of the MEDEP approach to enterprise development as it provides insights into the existing weaknesses along the specific product value chains that need to be strengthened. Allo is one of the several commodities/products promoted by MEDEP for the benefit of target families in the remote mountain areas, where allo as a resource is abundantly available in the community or national forest and the tradition of allo spinning and weaving exists. There are a total of 767 allo entrepreneurs in 16 districts from Dolakha in the East to Dadeldhura in the West with the combined output of 23 metric tons of yarn (Annex-5). The current extraction and processing level of allo is about 30 percent of potential sustainable yield from community forests that the beneficiaries have access to showing the scope for increasing the output levels to a significant extent (Annex-4). MEDEP is following a holistic approach of entrepreneurship development that targets disadvantaged and poor families to transform them into successful entrepreneurs by their inclusion into the value chain and strengthening their role to maximize the rewards. The specific interventions especially in allo value chain are as follows:

Entrepreneurship Training Entrepreneurship training is provided to potential entrepreneurs using the ILO/SIYB developed Training of Potential Entrepreneurs (TOPE) module followed by Training of Starting Entrepreneurs (TOSE) module for combined duration of about two weeks. There are two more training modules for advanced level training: Training of Existing Entrepreneurs (TOEE) and Training of Growing Entrepreneurs (TOGE). Entrepreneurship training aims to equip potential entrepreneurs with the knowledge and skill needed to run a business.

Skill Training Once the selection of an enterprise is done the next step involves providing the necessary skill for the production, or processing activity. There are over 100 skill based training modules currently available with the programme (on a diverse range of products/commodities including allo). These include modules on Allo Processing (6 months), and Allo weaving (3 months) developed by CSIDB. The topics cover bark extraction from plant, cooking and cleaning bark, fibre extraction, spinning, wefting, warping, setting loom and its operation.

27

.

Establishing Common Facility Centres (CFCs) Common Facility Centres (CFCs) are established to upgrade the working environment for the micro entrepreneurs and help them to gain production efficiency. CFCs are physical structures such as buildings and sheds with appropriate machinery and equipment for use by the group members. Several allo processing CFCs have been established with MEDEP support in different districts (Table-8). The number of MEs (allo entrepreneurs) per CFC ranges from 5 to 29. The average cost sharing is 46.5 percent by MEDEP with the remaining contributed by different agencies such as DDC, CFUGs, DFO, and the community. Table-8: Common Facility Centres (CFCs) for Allo Processing

Cost contribution (Rs.) Name of CFC Location Est. date

Members MEDEP Others Total

Community Building for allo, Cotton, and Dhaka weaving

Beni, Myagdi dist.

2009 7 450,000 460,000 910,000

Allo CFC Kyang (Building)

Kyang/Patichaur, Parbat dist.

2008 14 100,000 420,000 520,000

Allo Processing CFC (Building)

Saliza, Parbat dist.

2007 10 60,000 280,000 340,000

Syawlibang Allo Processing Centre

Sywalibang, Pyuthan dist.

2009 7 25,000 25,000 50,000

Allo Processing Centre Syaulibang, Pyuthan dist.

2009 24 170,000 30,250 200,250

Allo processing centre Naumule, Dailekh dist.

2008 12 129,000 41,100 170,100

Allo processing Bhabani-7, Dailekh dist.

2009 14 414,000 100,000 514,000

Allo processing Khulalabada, Jumla dist.

2009 10 315,000 315,000

Allo processing centre Darchula 2009 10 80,000 17,026 97,026 Allo processing centre Dadeldhura 2006 29 50,000 15,000 65,000 Total 137 1,478,000

(46.5%) 1,703,376 (53.5%)

3,181,376 (100.0%)

Note: Others include: DDC/VDC, CFUGs/DFOs, and community Source: MEDEP-MIS

Appropriate Technology MEDEP has provided appropriate spinning equipment such as foot operated charkas and recently introduced motorized charkhas for allo producers' groups for more efficient and quality spinning. The programme has linked equipment manufacturers (based in Kathmandu) to micro entrepreneurs in districts through the BDSPOs.

Linking MEs to MFIs The programme links micro entrepreneurs to Micro-Finance institutions (MFIs) to help them access credit. Such links continue to be weak due mainly to lack of coverage of many of the remote areas within MEDEP programme districts by MFIs. To expand the reach of financial services to MEs, MEDEP has signed MOUs with 5 GBBs, 4 MDBs, 5 FI-NGOs and more than 30 SCCs,

28

that has contributed to, as one recent study shows extend access to financial services to 61 percent of micro entrepreneurs in the survey districts (CDP-Nepal, 2009).

Market Networking

The institutional set up encompassing Micro Entrepreneur Group (MEG) at local level, and their association at the level of Rural Market Centre called Micro Entrepreneurs Groups Association (MEGA), DMEGA (at district level composed of MEGAs) and NMEGA (at national level composed of DMEGAs) are intended to facilitate market networking from local to national level. Sales outlets at district level, regional level, and at central, level (Saugat Grihas) facilitate marketing of products produced by micro entrepreneurs19. There are a total of 23 sales outlets including 20 district level, two regional level and one at central level. Links with district level government and other offices has helped find market for allo fabrics and products as gift items. Facilitating micro entrepreneurs to participate in trade fairs and exhibitions has immensely helped improve market networking and increase sales volume of ME's products. Many micro entrepreneurs producing allo yarn such as from Pyuthan have now developed links with large traders based in Kathmandu and regularly dispatch allo yarn in small quantities to them by long distance public buses or other means. Training on market networking provided to the outlet operators has helped improve their understanding and capacity to coordinate and develop links with medium and large enterprises. 4.2 Strategies for Upgrading the Allo Value Chain In this section we would focus on the broad strategies to upgrade the allo value chain based on the preceding analysis of the sub sector. There are basically two main considerations in targeting value chain upgrading related to a particular commodity sub sector.

• Inclusion: Increase the number of value chain participants. This is particularly important to expand the possibilities of inclusion of specific target groups such as those below nationally defined absolute poverty level to help alleviate poverty; and

• Upscaling: Scale up production/processing activities to increase the reward of

participating in the value chain. The common indicators are increased volume of production, sales revenue, and profit that show a certain shift from the baseline level to the next higher level that is targeted to be achieved.

19 Sale through Dedicated Outlet-Saugat Griha, Kathmandu Particular Unit Qty sold Amt. Rs Average

Price/unit. Thread Kg 48.5 29,100 600.0Fabrics Meter 121.7 44,725 367.5Products Piece 20.0 9,140 457.0

Source: Saugat Griha, Tripureshwor, Kathmandu

29

In the context of small producers up scaling is mainly achieved through the following two main areas of interventions (Bolwig et al., 2008; Riisgard et. al. 2008)). Strengthening value chain coordination around the production node: Value chain coordination is strengthened either by vertical integration in which an actor performs several functions in the value chain, or through contractualization which simply indicates use of contracts as a mediator of exchange between chain actors. Chain actors can cooperate and enhance fruitful exchanges between them (Vertical contractualization). Similarly, actors in the same position of the value chain can cooperate over such matters as input provision, bulking produce for easy access to markets, identification of potential buyers, as well as product certification (Horizontal contractualization). Upgrading in the production node: The common forms of upgrading in the production node include:

• Improvement in product quality, • Improved efficiency of production process, • Increasing volume of production, • Improving timing of supply • Compliance with mutually agreed upon industry standards.

In view of possible upscaling of MEs activities to help in overall value chain upgrading the main strategies will include: Increased value addition through vertical integration Vertical integration enables MEs to take benefit of the value addition opportunities at different levels of the production and processing stages. These basically include taking up upstream activities to integrate on the input side such as preparation of vegetable dyes using locally available plant resources. Similarly, possible integration on the downstream part of the value chain include product making (knitted products such as dresses, shawls, and mufflers etc) for higher value addition, taking up the retailing function either individually or through producers' marketing outlets (Saugat Grihas) at district, regional and at central level. Improvement in Product Quality The quality of allo yarn needs to be improved to make it less coarse and less husky in texture. This is very critical to the growth of the allo industry in Nepal. The quality of spun yarn can be improved with the introduction of appropriate equipment for fibre extraction, and improved Charkas for quality spinning. Currently, allo yarn produced by most MEDEP entrepreneurs ranges from low to medium in terms of quality (main complaints being presence of knots in yarn leading to breaking up of thread) suitable for use in carpet making but falling short of the quality needed for making knitted/crocheted products. Efforts aimed at improving the quality of spun yarn are going at the moment from value chain participants and stakeholders. Himalayan Wild Fibres, a privately owned company with interest in allo product development for export markets has recently dispatched 300 kg of allo fibre (procured through NMEGA) to Italy for conducting

30