Regulation to the Value Added Tax Act the Value Added Tax ...

Value Added Tax and Communications Industry

May 18, 2016

2 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The following information is not intended to be “written advice concerning one or more Federal tax matters” subject to the requirements of section 10.37(a)(2) of Treasury Department Circular 230. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

Notice

3 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda Global VAT Landscape VAT Basics VAT and Telecommunications Industry Puerto Rico VAT introduction (OPTIONAL) Global VAT Challenges

Global VAT Landscape

5 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

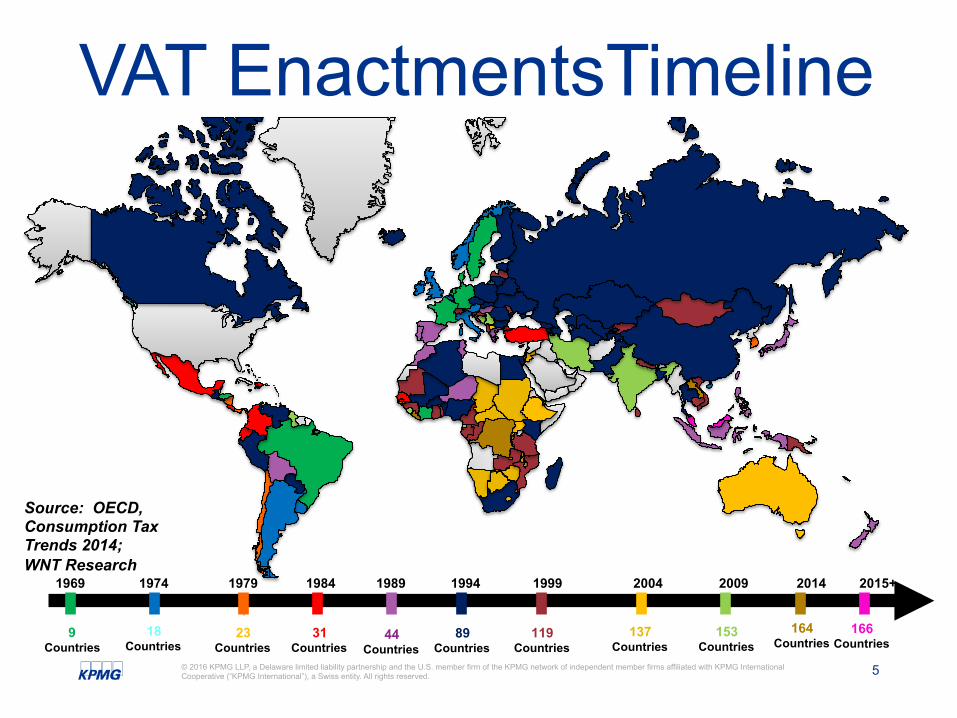

VAT EnactmentsTimeline

1969 1974 1979 1984 1989 1994 1999 2004 2009 2014 2015+

Source: OECD, Consumption Tax Trends 2014; WNT Research

9 Countries

18 Countries

23 Countries

31 Countries

44 Countries

89 Countries

119 Countries

137 Countries

153 Countries

164 Countries

166 Countries

6 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Growing Importance of VAT

VAT is a concern for companies doing business globally Many governments are shifting the emphasis from taxing earnings and gains to taxing consumption Many governments use VAT as first tool in fiscal policy — Reduce to stimulate consumption — Increase to reduce deficits Many governments use VAT as first tool in fiscal policy — Over 160 countries have a VAT regime

- U.S. is only OECD country without VAT - Other countries considering VAT including Gulf Cooperation Council countries

VAT Basics

8 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

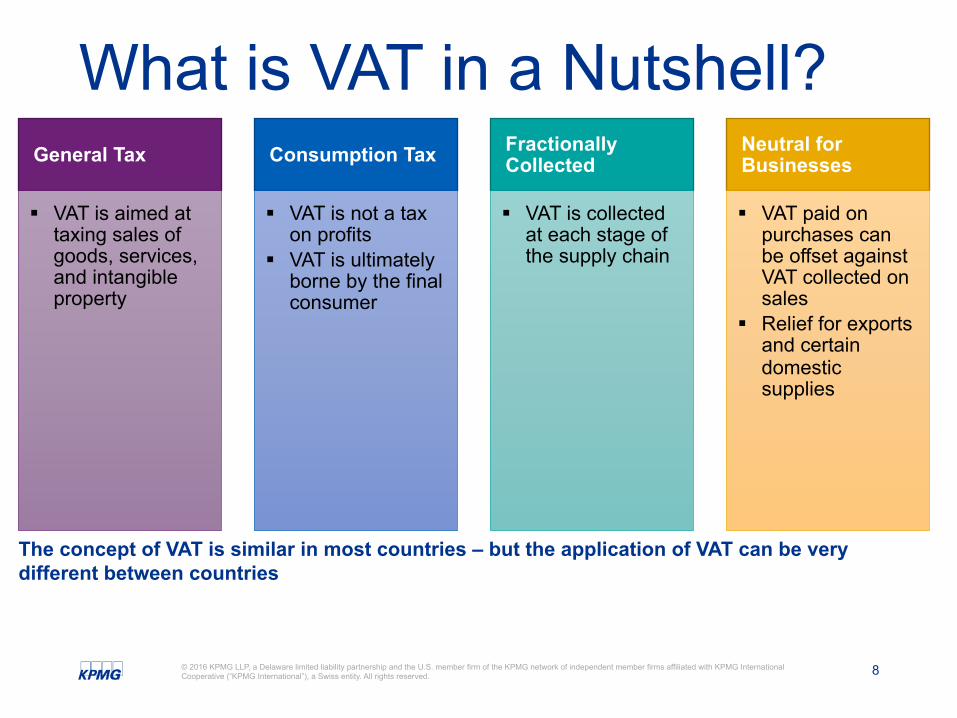

What is VAT in a Nutshell?

The concept of VAT is similar in most countries – but the application of VAT can be very different between countries

General Tax

§ VAT is aimed at taxing sales of goods, services, and intangible property

Consumption Tax

§ VAT is not a tax on profits

§ VAT is ultimately borne by the final consumer

Fractionally Collected

§ VAT is collected at each stage of the supply chain

Neutral for Businesses

§ VAT paid on purchases can be offset against VAT collected on sales

§ Relief for exports and certain domestic supplies

9 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

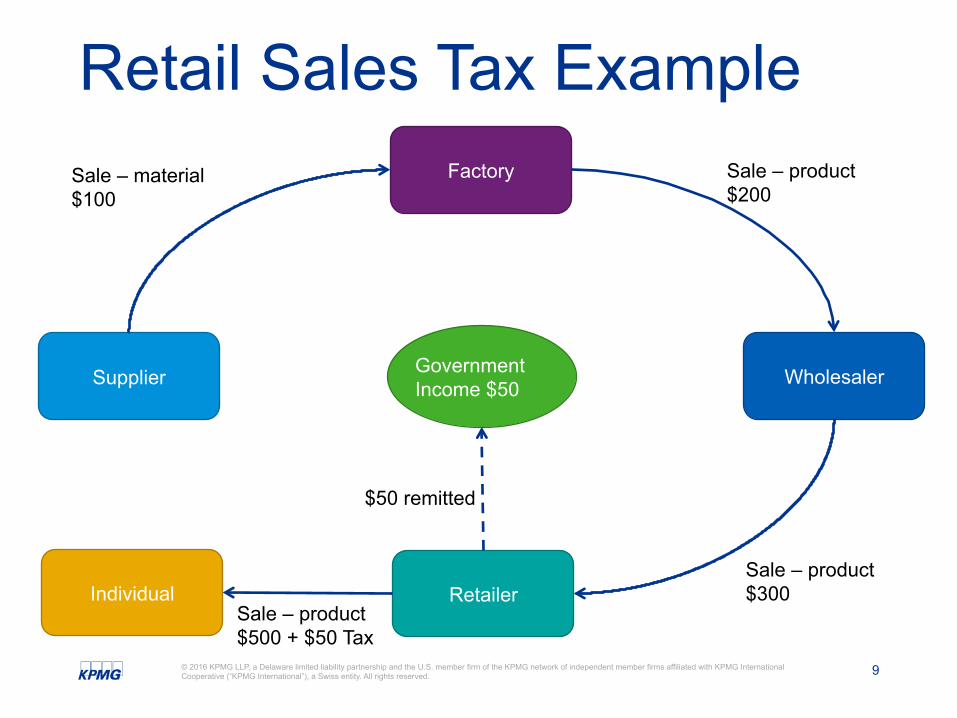

Retail Sales Tax Example

Supplier

Factory

Wholesaler

Retailer

Sale – material $100

Sale – product $200

Sale – product $300

Government Income $50

Individual Sale – product $500 + $50 Tax

$50 remitted

10 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

VAT Example

Supplier

Factory

Wholesaler

Retailer

Sale – material $100 + $10 VAT

Sale – product $200 + $20 VAT

Sale – product $300 + $30 VAT

Government Income $50

$10 remitted

$10 remitted ($20 VAT – $10 credit)

$10 remitted ($30 VAT – $20 credit)

Individual Sale – product $500 + $50 VAT

$20 remitted ($50 VAT – $30 credit)

11 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

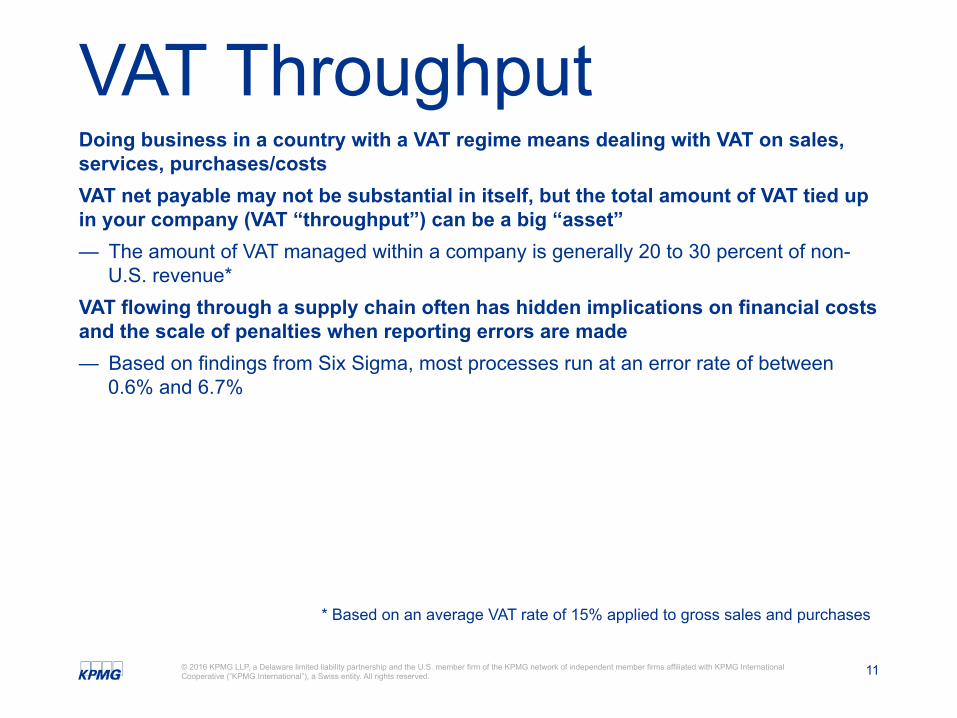

VAT Throughput Doing business in a country with a VAT regime means dealing with VAT on sales, services, purchases/costs VAT net payable may not be substantial in itself, but the total amount of VAT tied up in your company (VAT “throughput”) can be a big “asset” — The amount of VAT managed within a company is generally 20 to 30 percent of non-

U.S. revenue* VAT flowing through a supply chain often has hidden implications on financial costs and the scale of penalties when reporting errors are made — Based on findings from Six Sigma, most processes run at an error rate of between

0.6% and 6.7%

* Based on an average VAT rate of 15% applied to gross sales and purchases

12 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

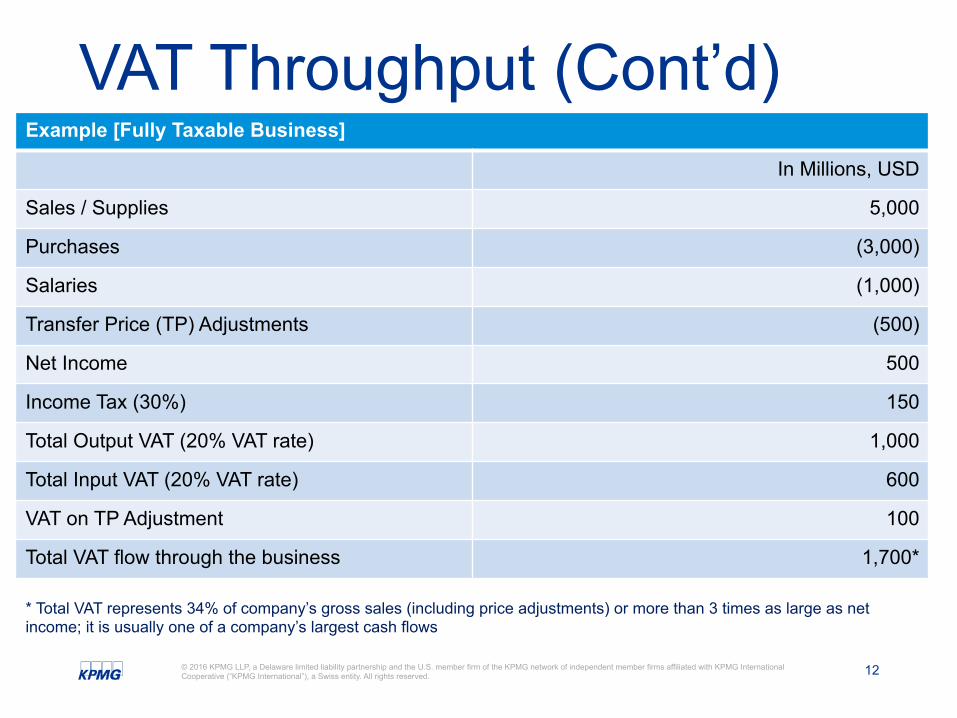

VAT Throughput (Cont’d) Example [Fully Taxable Business]

In Millions, USD

Sales / Supplies 5,000

Purchases (3,000)

Salaries (1,000)

Transfer Price (TP) Adjustments (500)

Net Income 500

Income Tax (30%) 150

Total Output VAT (20% VAT rate) 1,000

Total Input VAT (20% VAT rate) 600

VAT on TP Adjustment 100

Total VAT flow through the business 1,700*

* Total VAT represents 34% of company’s gross sales (including price adjustments) or more than 3 times as large as net income; it is usually one of a company’s largest cash flows

13 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

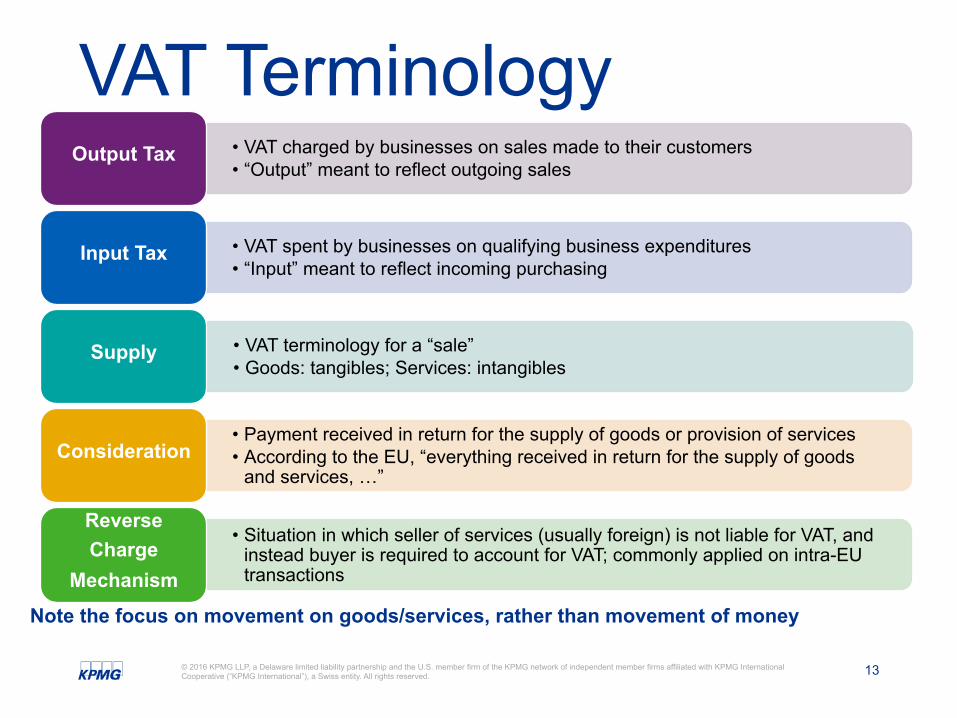

VAT Terminology

Note the focus on movement on goods/services, rather than movement of money

• VAT charged by businesses on sales made to their customers • “Output” meant to reflect outgoing sales

Output Tax

• VAT spent by businesses on qualifying business expenditures • “Input” meant to reflect incoming purchasing

Input Tax

• VAT terminology for a “sale” • Goods: tangibles; Services: intangibles

Supply

• Payment received in return for the supply of goods or provision of services • According to the EU, “everything received in return for the supply of goods

and services, …” Consideration

• Situation in which seller of services (usually foreign) is not liable for VAT, and instead buyer is required to account for VAT; commonly applied on intra-EU transactions

Reverse Charge

Mechanism

VAT and Telecommunications Industry

15 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Global Challenges – Industry perspective

• New markets foray • New product introduction • International structuring • Compliance challenges

16 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

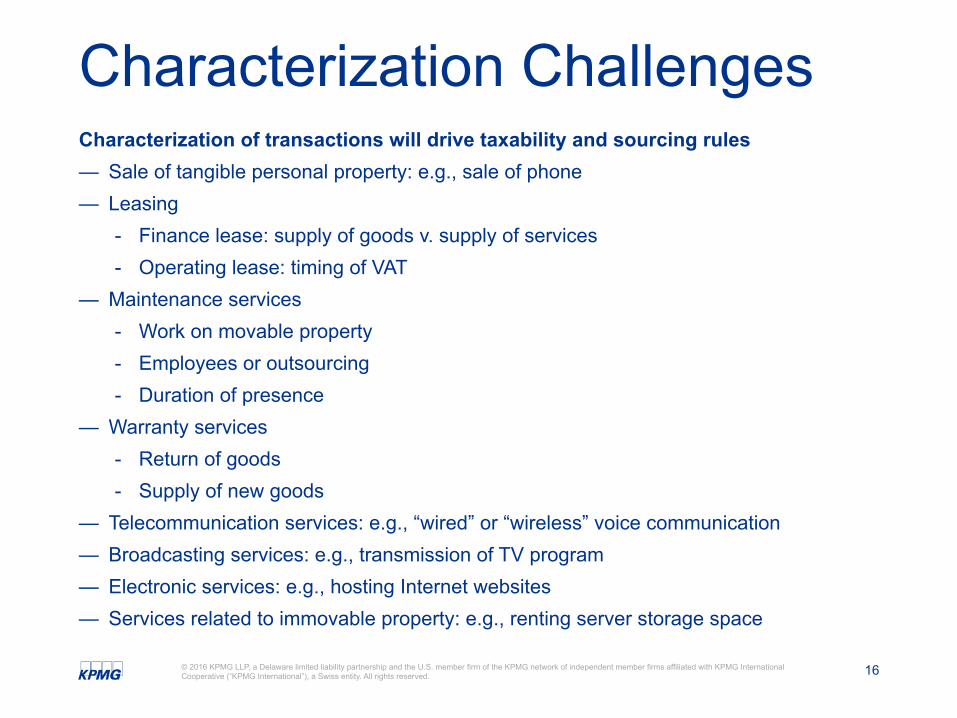

Characterization Challenges Characterization of transactions will drive taxability and sourcing rules — Sale of tangible personal property: e.g., sale of phone — Leasing

- Finance lease: supply of goods v. supply of services - Operating lease: timing of VAT

— Maintenance services - Work on movable property - Employees or outsourcing - Duration of presence

— Warranty services - Return of goods - Supply of new goods

— Telecommunication services: e.g., “wired” or “wireless” voice communication — Broadcasting services: e.g., transmission of TV program — Electronic services: e.g., hosting Internet websites — Services related to immovable property: e.g., renting server storage space

17 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Sourcing Challenges Determining Sourcing — Rules vary across jurisdiction — Origin v. destination v. performance v. use and enjoyment New Rules Relating to Telecommunications, Broadcasting, Electronic (TBE) Services — Based on OECD VAT/GST Guidelines, taxation should occur where customer is

located - Business-to-business (B2B): customer self-assesses VAT under reverse charge

mechanism - Business-to-consumer (B2C): vendor should register for and charge VAT in country

where consumer is established

18 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

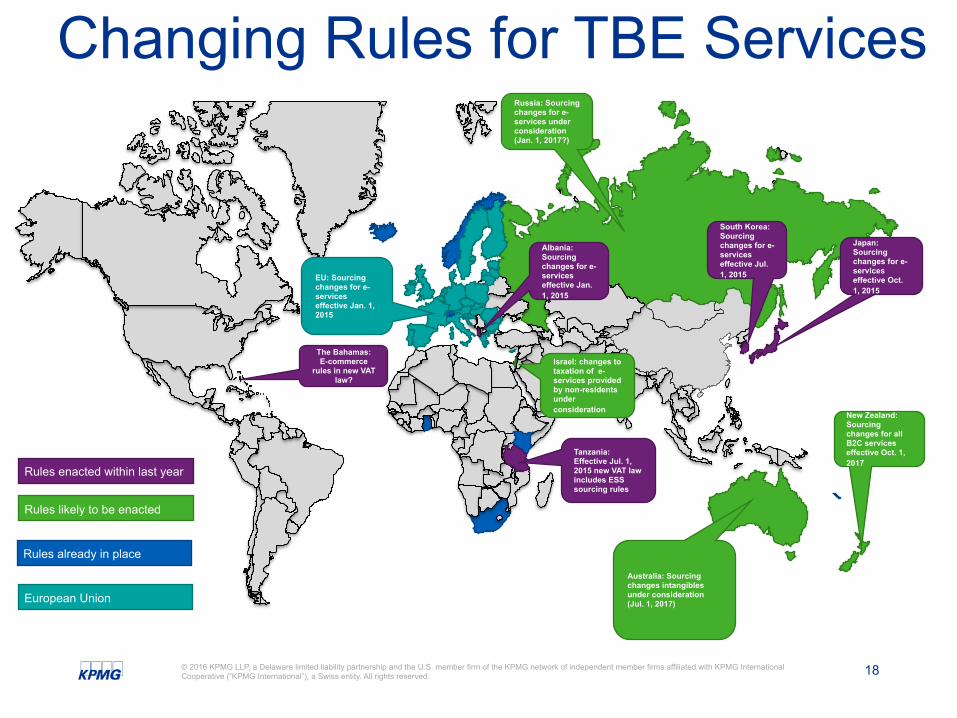

Changing Rules for TBE Services

EU: Sourcing changes for e-services effective Jan. 1, 2015

South Korea: Sourcing changes for e-services effective Jul. 1, 2015

Japan: Sourcing changes for e-services effective Oct. 1, 2015

Australia: Sourcing changes intangibles under consideration (Jul. 1, 2017)

The Bahamas: E-commerce

rules in new VAT law?

New Zealand: Sourcing changes for all B2C services effective Oct. 1, 2017

Albania: Sourcing changes for e-services effective Jan. 1, 2015

Tanzania: Effective Jul. 1, 2015 new VAT law includes ESS sourcing rules

Russia: Sourcing changes for e-services under consideration (Jan. 1, 2017?)

Rules enacted within last year

Rules likely to be enacted

Rules already in place

European Union

Israel: changes to taxation of e-services provided by non-residents under consideration

19 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Broader VAT Issues New revenue streams — Working with new business partners to facilitate new service offerings

- E.g., partnership with car manufacturer to provide internet connectivity in vehicles Nexus / fixed establishment issues — Threshold very low in certain jurisdictions (e.g., new PE rules on e-services in Israel) — Presence of infrastructure and/or personnel Roaming charges — VAT recovery issues on foreign VAT on purchases (e.g., Canada) — VAT recovery issues — Local VAT when onward supplied to customer?

20 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Broader VAT Issues (Cont’d) Customer presence equipment — Vendor maintains ownership? — Cross border movements — VAT recovery issues Cross-border M&A transactions — VAT recovery on transaction/deal costs — VAT on asset transfers? — Registration requirements — VAT implications of new business

Puerto Rico VAT introduction (OPTIONAL)

22 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

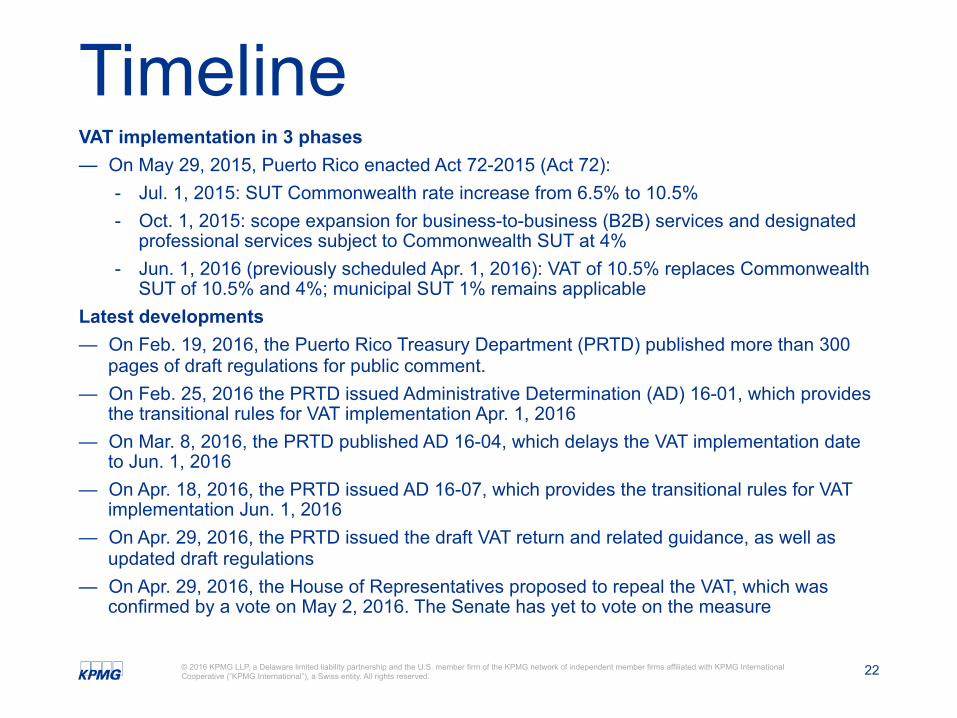

Timeline VAT implementation in 3 phases — On May 29, 2015, Puerto Rico enacted Act 72-2015 (Act 72):

- Jul. 1, 2015: SUT Commonwealth rate increase from 6.5% to 10.5% - Oct. 1, 2015: scope expansion for business-to-business (B2B) services and designated

professional services subject to Commonwealth SUT at 4% - Jun. 1, 2016 (previously scheduled Apr. 1, 2016): VAT of 10.5% replaces Commonwealth

SUT of 10.5% and 4%; municipal SUT 1% remains applicable Latest developments — On Feb. 19, 2016, the Puerto Rico Treasury Department (PRTD) published more than 300

pages of draft regulations for public comment. — On Feb. 25, 2016 the PRTD issued Administrative Determination (AD) 16-01, which provides

the transitional rules for VAT implementation Apr. 1, 2016 — On Mar. 8, 2016, the PRTD published AD 16-04, which delays the VAT implementation date

to Jun. 1, 2016 — On Apr. 18, 2016, the PRTD issued AD 16-07, which provides the transitional rules for VAT

implementation Jun. 1, 2016 — On Apr. 29, 2016, the PRTD issued the draft VAT return and related guidance, as well as

updated draft regulations — On Apr. 29, 2016, the House of Representatives proposed to repeal the VAT, which was

confirmed by a vote on May 2, 2016. The Senate has yet to vote on the measure

23 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

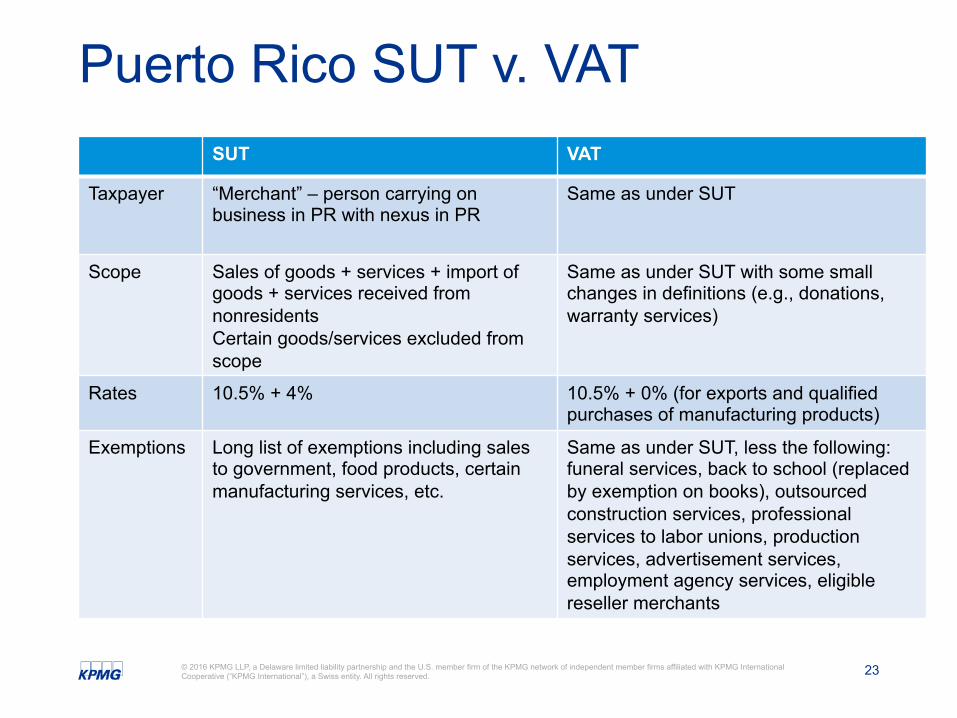

Puerto Rico SUT v. VAT SUT VAT

Taxpayer “Merchant” – person carrying on business in PR with nexus in PR

Same as under SUT

Scope Sales of goods + services + import of goods + services received from nonresidents Certain goods/services excluded from scope

Same as under SUT with some small changes in definitions (e.g., donations, warranty services)

Rates 10.5% + 4% 10.5% + 0% (for exports and qualified purchases of manufacturing products)

Exemptions Long list of exemptions including sales to government, food products, certain manufacturing services, etc.

Same as under SUT, less the following: funeral services, back to school (replaced by exemption on books), outsourced construction services, professional services to labor unions, production services, advertisement services, employment agency services, eligible reseller merchants

24 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

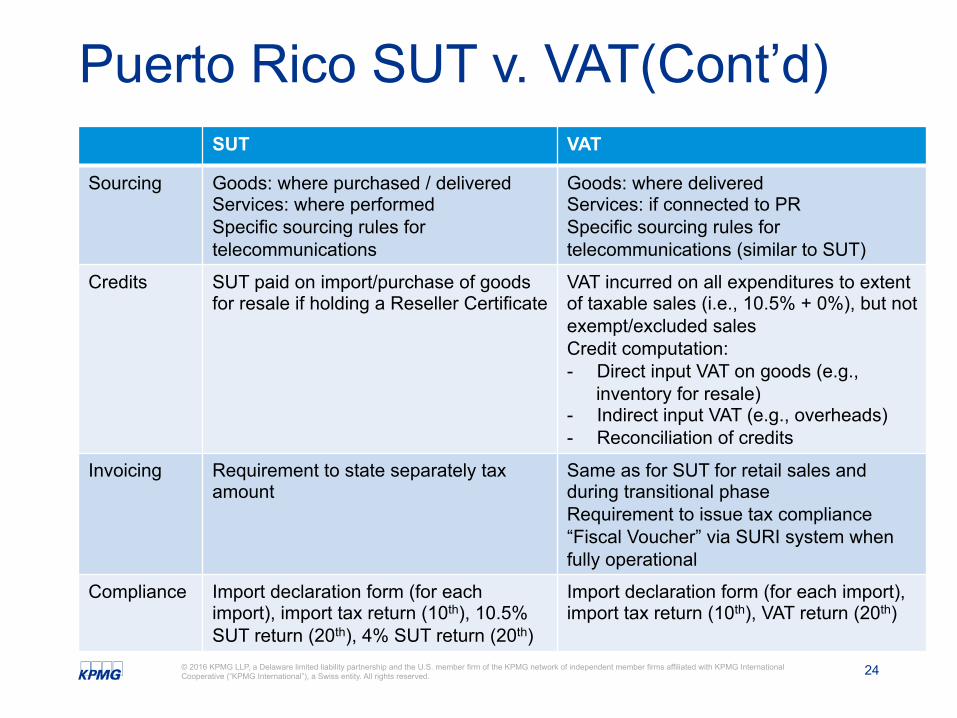

Puerto Rico SUT v. VAT(Cont’d) SUT VAT

Sourcing Goods: where purchased / delivered Services: where performed Specific sourcing rules for telecommunications

Goods: where delivered Services: if connected to PR Specific sourcing rules for telecommunications (similar to SUT)

Credits SUT paid on import/purchase of goods for resale if holding a Reseller Certificate

VAT incurred on all expenditures to extent of taxable sales (i.e., 10.5% + 0%), but not exempt/excluded sales Credit computation: - Direct input VAT on goods (e.g.,

inventory for resale) - Indirect input VAT (e.g., overheads) - Reconciliation of credits

Invoicing Requirement to state separately tax amount

Same as for SUT for retail sales and during transitional phase Requirement to issue tax compliance “Fiscal Voucher” via SURI system when fully operational

Compliance Import declaration form (for each import), import tax return (10th), 10.5% SUT return (20th), 4% SUT return (20th)

Import declaration form (for each import), import tax return (10th), VAT return (20th)

25 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

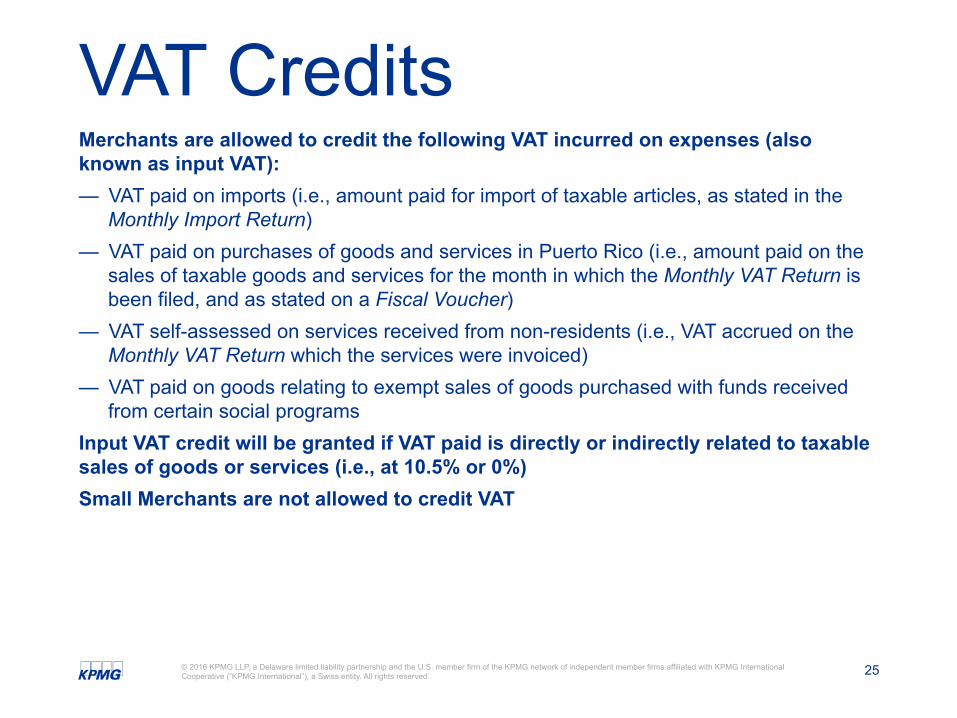

VAT Credits Merchants are allowed to credit the following VAT incurred on expenses (also known as input VAT): — VAT paid on imports (i.e., amount paid for import of taxable articles, as stated in the

Monthly Import Return) — VAT paid on purchases of goods and services in Puerto Rico (i.e., amount paid on the

sales of taxable goods and services for the month in which the Monthly VAT Return is been filed, and as stated on a Fiscal Voucher)

— VAT self-assessed on services received from non-residents (i.e., VAT accrued on the Monthly VAT Return which the services were invoiced)

— VAT paid on goods relating to exempt sales of goods purchased with funds received from certain social programs

Input VAT credit will be granted if VAT paid is directly or indirectly related to taxable sales of goods or services (i.e., at 10.5% or 0%) Small Merchants are not allowed to credit VAT

26 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

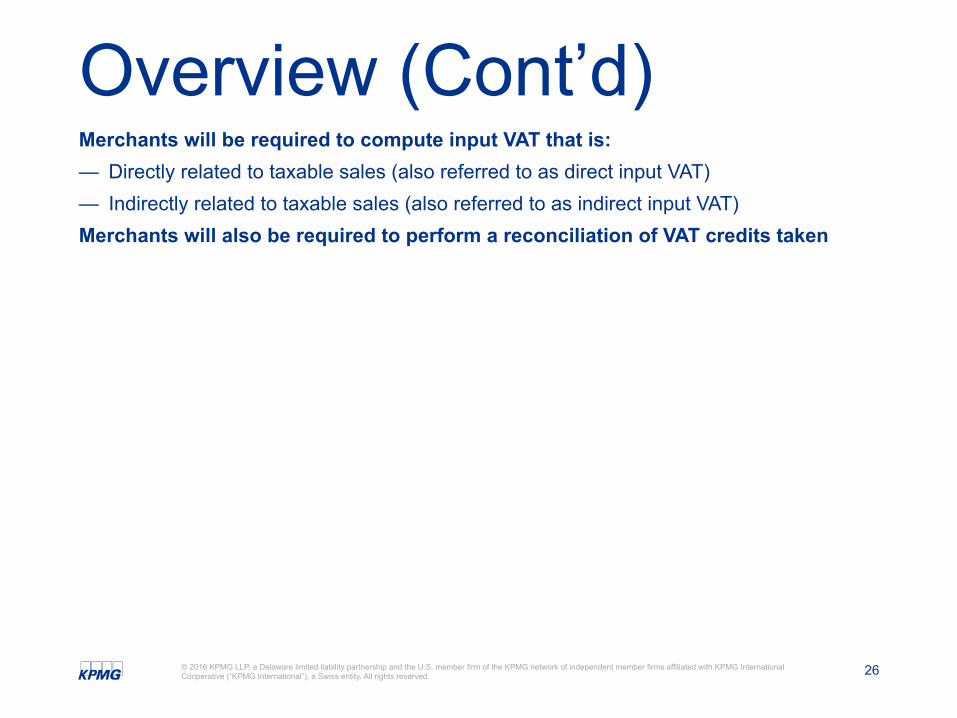

Overview (Cont’d) Merchants will be required to compute input VAT that is: — Directly related to taxable sales (also referred to as direct input VAT) — Indirectly related to taxable sales (also referred to as indirect input VAT) Merchants will also be required to perform a reconciliation of VAT credits taken

27 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

VAT Incurred on Cross-Border Services

Foreign VAT incurred on cross-border services between related parties (as defined by the income tax provision in the Code) may be credited in the Monthly VAT return, limited to: — Foreign VAT amount charged and cannot give rise to a refund — After all adjustments and credit — The non-recoverable amount of self-assessed VAT on services received — The foreign VAT cannot be claimed as a deduction for income tax purposes

28 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Compliance System Sistema Unificado de Rentas Internas (“SURI”) — Registration for VAT

- New Merchants — File application for Merchant Registration Certificate

- Existing Merchants — Validation process

— VAT returns - Preparation and filing on Monthly VAT Return - VAT payment

— PICO remains in use - Import Declaration - Monthly Import VAT Return - SUT returns (for May 2016, adjustments, and specific situations that remain subject

to SUT)

29 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

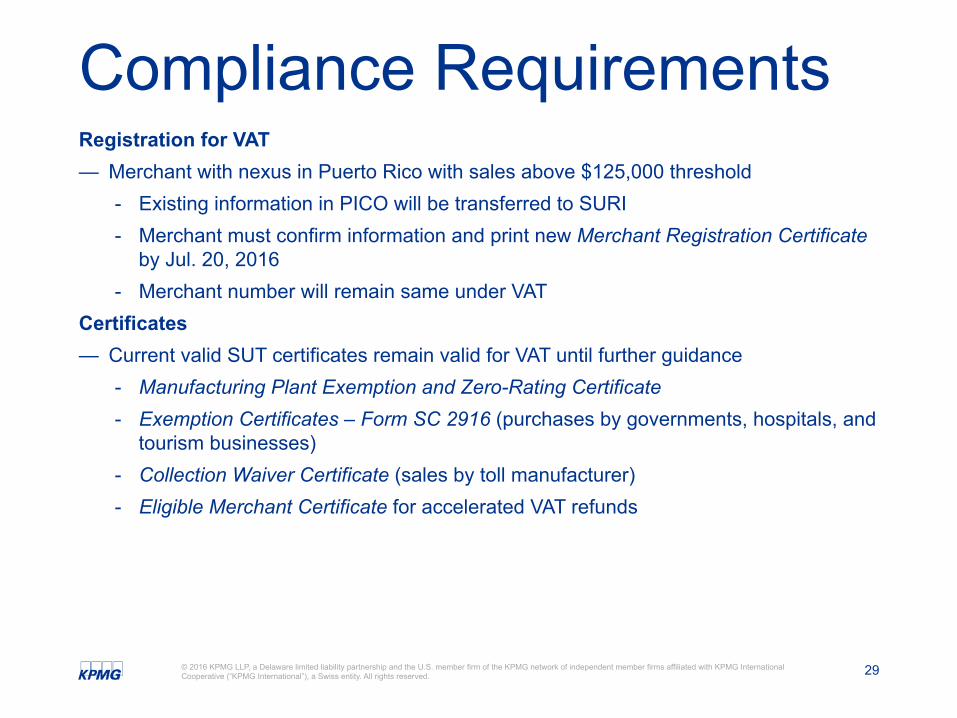

Compliance Requirements Registration for VAT — Merchant with nexus in Puerto Rico with sales above $125,000 threshold

- Existing information in PICO will be transferred to SURI - Merchant must confirm information and print new Merchant Registration Certificate

by Jul. 20, 2016 - Merchant number will remain same under VAT

Certificates — Current valid SUT certificates remain valid for VAT until further guidance

- Manufacturing Plant Exemption and Zero-Rating Certificate - Exemption Certificates – Form SC 2916 (purchases by governments, hospitals, and

tourism businesses) - Collection Waiver Certificate (sales by toll manufacturer) - Eligible Merchant Certificate for accelerated VAT refunds

30 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Compliance Requirements (Cont’d) Other Documentation — Fiscal Voucher, Debit and Credit Notes

- Requirement suspended until SURI fully operational — Invoices issued/received

- Merchants with annual gross receipts of $40,000,000 or more will be required to submit a list to be published by the PRTD detailing VAT incurred on purchases with their Monthly VAT Return

— Shipping documentation and other supporting documentation

31 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

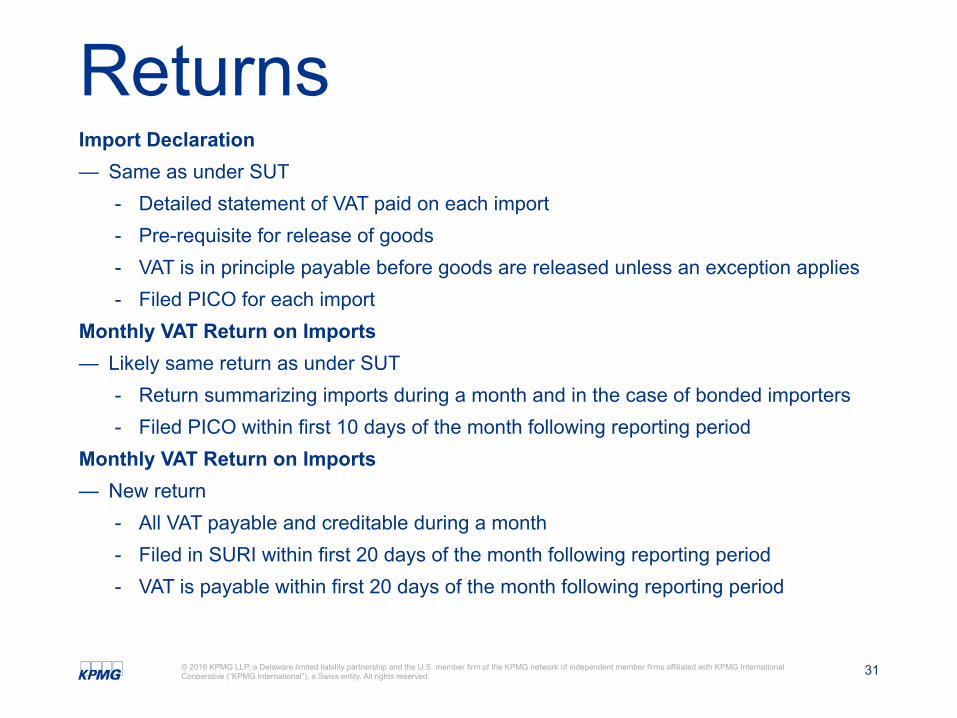

Returns Import Declaration — Same as under SUT

- Detailed statement of VAT paid on each import - Pre-requisite for release of goods - VAT is in principle payable before goods are released unless an exception applies - Filed PICO for each import

Monthly VAT Return on Imports — Likely same return as under SUT

- Return summarizing imports during a month and in the case of bonded importers - Filed PICO within first 10 days of the month following reporting period

Monthly VAT Return on Imports — New return

- All VAT payable and creditable during a month - Filed in SURI within first 20 days of the month following reporting period - VAT is payable within first 20 days of the month following reporting period

Global VAT Challenges

33 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Increase mandatory use of e-invoicing — Brazil, Mexico

- Long standing mandatory e-invoicing requirements — Argentina

- Most businesses now required to use e-invoicing (deadline Mar. 16, 2015) — Colombia

- Introduced broad e-invoicing requirements effective 2018 — Chile, Paraguay, Uruguay

- Expanding compulsory e-invoicing gradually over next years — Peru, Bolivia

- Introduced broad e-invoicing requirements effective 2016 — Italy

- Incentives for using e-invoicing effective Jul. 1, 2016 — China

- Expansion of upgraded VAT invoicing platform effective Aug. 1, 2015 — European Union

- Mandatory for public procurement by 2018

Modernization of VAT Compliance

56

34 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

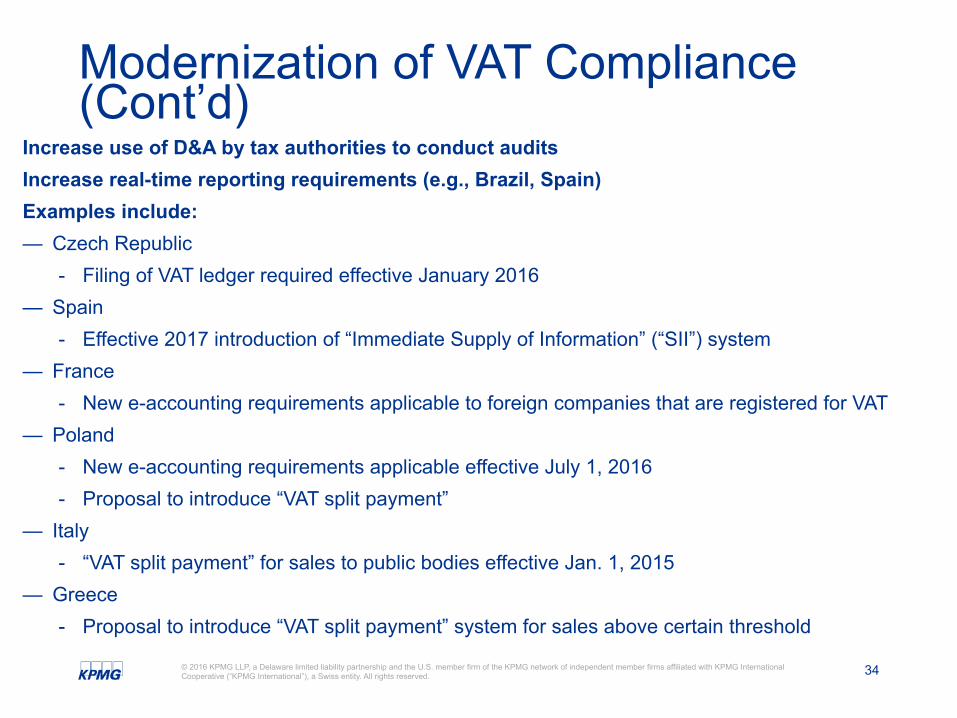

Increase use of D&A by tax authorities to conduct audits Increase real-time reporting requirements (e.g., Brazil, Spain) Examples include: — Czech Republic

- Filing of VAT ledger required effective January 2016 — Spain

- Effective 2017 introduction of “Immediate Supply of Information” (“SII”) system — France

- New e-accounting requirements applicable to foreign companies that are registered for VAT — Poland

- New e-accounting requirements applicable effective July 1, 2016 - Proposal to introduce “VAT split payment”

— Italy - “VAT split payment” for sales to public bodies effective Jan. 1, 2015

— Greece - Proposal to introduce “VAT split payment” system for sales above certain threshold

Modernization of VAT Compliance (Cont’d)

56

35 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

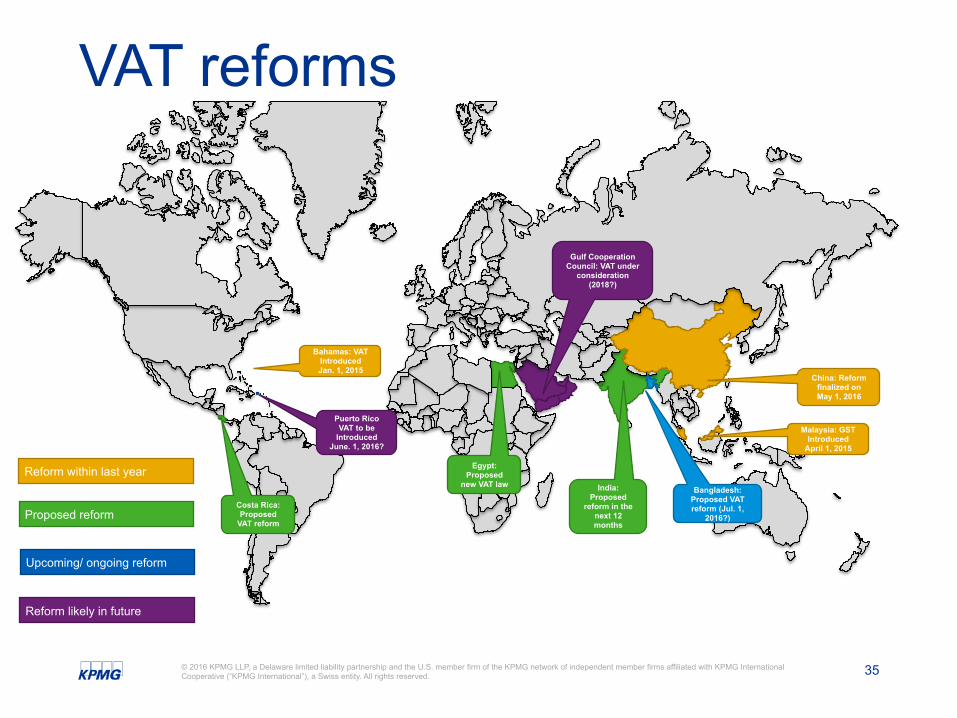

VAT reforms

Gulf Cooperation Council: VAT under

consideration (2018?)

India: Proposed

reform in the next 12 months

China: Reform finalized on May 1, 2016

Malaysia: GST Introduced

April 1, 2015

Bahamas: VAT Introduced Jan. 1, 2015

Puerto Rico VAT to be

Introduced June. 1, 2016?

5

Bangladesh: Proposed VAT reform (Jul. 1,

2016?)

Egypt: Proposed

new VAT law

Costa Rica: Proposed

VAT reform

Reform within last year

Proposed reform

Upcoming/ ongoing reform

Reform likely in future

36 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Liz Bopp, Executive Director - Tax, AT&T Background

Liz is an Executive Director in the AT&T Tax Organization where she has spent the majority of her career. She specializes in transaction taxes and her current role is focused in two areas: (1) tax research, planning and policy which focuses on all new AT&T product and services as well as monitoring changes in existing tax laws and (2) ensuring that all taxes, fees and surcharges are billed correctly to our customers via AT&T’s billing systems. In previous roles, she has done income tax, property tax and payroll taxes for tax compliance and external tax audits.

Liz Bopp

Executive Director, Tax

AT&T Address

Tel: +1 Fax: +1 Cell: +1

Education n Bachelors degree in Biology, Rutgers University n MBA, Marquette University n Masters in Tax, Setton Hall University

37 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

James Freed, Tax Managing Director, KPMG Background James has over14 years of experience advising in indirect tax. Prior to joining KPMG LLP in the U.S. in March 2011, James worked both in the U.K. and the U.S. advising clients on a wide range of indirect tax issues. Professional and Industry Experience James has been an indirect tax advisor for over fourteen years. During that time he has had the opportunity to work on numerous international indirect tax engagements for a wide variety of businesses, including high-tech/eCommerce, manufacturing, agricultural, consumer business, pharmaceutical and international service companies. His work includes provision of global VAT consulting and compliance advice, pre and post M&A work, advice in relation to VAT issues associated with cloud computing service offerings, VAT recovery services, supply-chain restructuring and co-ordination of multinational VAT projects. He also has substantial experience with a variety of indirect tax software solutions, including ERP and ‘tax-engines’. His previous indirect tax experience includes: • Working with a well known retailer on an ongoing basis to advise on the VAT implications relating to expansion into new

markets, the provision of new service offerings and expansion into new manufacturing locations. The services include advice in relation to the emerging e-commerce rules in a number of European and non-European locations. The services also include assistance with VAT compliance in a number of key locations.

• Working with a medical device manufacturer on an ongoing basis to assist it with managing the VAT implications of its expansion into Europe and Asia. The work included advice on numerous technical issues as well as VAT registration, compliance and recovery services

• Working with a global pharmaceutical company to develop its indirect tax operating model. The work included designing a tax operating model, benchmarking this model against its competitors and to subsequently assist with the implementation of best practices around the management of both VAT consulting as well as compliance related tasks. Numerous improvements were identified in order to drive efficiency and reduce cost.

• Working with a number of companies in the food and beverage sector to secure substantial refunds of overpaid VAT from the local tax authorities. The work included devising a methodology to calculate the amount of VAT due from the tax authorities and subsequently negotiating with the tax authorities to secure the appropriate refunds.

Publications and speaking engagements James regularly presents to, and instructs, internal and external clients on international VAT matters.

James Freed

Tax Managing Director, SALT

KPMG LLP 200 East Randolph Drive, Suite 5500 Chicago, IL 60601

Tel: +1 312-665-2627 Fax: +1 312-275-7651 Cell: +1 312-206-3601

Function and specialization

Value Added Tax, U.S. Indirect Tax

Professional associations n Member of the U.K. Chartered Institute of Taxation Languages n English Education n Law Degree, University of Birmingham, U.K. n Chartered Tax Advisor, U.K.

38 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Vinay Mohan, Senior Manager, KPMG Background

Vinay joined KPMG LLP in July 2011 from KPMG in Ireland to take up his current role as Manager in the U.S. Indirect Tax Practice. Prior to joining KPMG in Ireland, Vinay worked with the Indian office of another Big Four in its Global Tax Advisory Services team specializing in Indian Indirect Taxes.

Vinay is based in the Chicago office. He is specialized in international Indirect Taxes and in particular with European VAT and Indian Indirect Tax laws. Vinay has more than 13 years experience in the Indirect Tax field advising clients across a broad range of industries.

Professional and industry experience

Vinay has extensive experience in advising clients on international Indirect Tax issues. He has advised a number of clients in a variety of industries, including pharmaceutical, financial services, technology and telecommunication sector. In particular Vinay has extensive experience in providing advice in respect of supply chains for companies with cross border transactions.

Vinay is also a specialist in Indian Indirect Taxes and works closely with KPMG in India. During his stint in India with another Big Four, Vinay advised clients in varied industry sectors including Manufacturing, Technology and Oil & Gas on Indian Indirect Taxes including Customs, Excise, VAT, Service Tax and Foreign Trade Policy to the extent they dealt with Indian Indirect Tax incentives. Vinay has also advised clients extensively on transition from erstwhile Sales Tax regime to the VAT regime

Specific examples of Vinay’s experience include:

■ Working with a global financial services firm in managing their VAT obligations internationally including assistance in submitting multi million dollar refund claims to UK Revenue authority on exempt financial services previously treated as taxable.

■ Working with several clients in varied industries in gathering country-specific Indirect Tax requirements and validating test environment results during ERP and tax engine implementation projects for Europe, Americas, and ASPAC regions

■ Managing VAT compliance needs for a number of clients through KPMG’s Indirect Tax Compliance Center (“ITCC”)

■ Advising clients including a global pharmaceutical company in implementing complex supply chains in Europe with minimal VAT leakage.

Publications and speaking engagements

— Vinay has undertaken several speaking engagements in Ireland and India.

Vinay Mohan Senior Manager, SALT Global Indirect Taxes Group

KPMG LLP 200 E Randolph Drive, Suite 5500 Chicago, IL 60601 Tel 312 665 1138 Fax 646 417 5762 Cell 917 593 4425 [email protected] Function and specialization International Indirect Taxes (Member of US SALT Practice) Education, licenses & certifications n Bachelor of Commerce, Madras University n Associate Member of Institute of Chartered

Accountants of India

Thank you

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia