Valuation Soccer Players

23

Volume 6, Issue 2 2010 Article 10 Journal of Quantitative Analysis in Sports Valuations of Soccer Players from Statistical Performance Data Radu S. Tunaru, City University, Cass Business School Howard P. Viney, Open University Distance Learning Recommended Citation: Tunaru, Radu S. and Viney, Howard P. (2010) "Valuations of Soccer Players from Statistical Performance Data," Journal of Quantitative Analysis in Sports: Vol. 6 : Iss. 2, Article 10. Available at: http://www.bepress.com/jqas/vol6/iss2/10 DOI: 10.2202/1559-0410.1238 ©2010 American Statistical Association. All rights reserved.

Transcript of Valuation Soccer Players

Volume 6, Issue 2 2010 Article 10

Journal of Quantitative Analysis inSports

Valuations of Soccer Players from StatisticalPerformance Data

Radu S. Tunaru, City University, Cass Business SchoolHoward P. Viney, Open University Distance Learning

Recommended Citation:Tunaru, Radu S. and Viney, Howard P. (2010) "Valuations of Soccer Players from StatisticalPerformance Data," Journal of Quantitative Analysis in Sports: Vol. 6 : Iss. 2, Article 10.Available at: http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

©2010 American Statistical Association. All rights reserved.

Valuations of Soccer Players from StatisticalPerformance Data

Radu S. Tunaru and Howard P. Viney

Abstract

Based upon contingent claims methodology and standard techniques in statistical modelingand stochastic calculus, we develop a framework for determining the financial value ofprofessional soccer players to their existing and potential new clubs. The model recognizes that aplayer's value is a product of a variety of factors, some of them more obvious (i.e. on-fieldperformance, injuries, disciplinary record), and some of them less obvious (i.e. image rights orpersonal background). We provide numerical examples based upon historical statisticalperformance indicators that suggest the value of a soccer player is not the same for all potentialclubs present in a market. In other words this is a special case where the law of one price for oneasset does not function. Our modeling employs the vast database of soccer players' performancemaintained by OPTA Sportsdata; the same database has been used by major clubs in the EnglishPremiership such as Arsenal and Chelsea. From a statistical point of view, our model can beapplied to identify the relative value of players with similar characteristics but different marketvaluations, to explore patterns of performance for individual star players and teams over a run ofgames, and to explore correlations or interactions between pairs of players or small groups ofplayers on the team. Moreover, it offers a tool to value players from a financial point of view usingtheir past performance; hence this model can be also used to inform contractual negotiations.

KEYWORDS: English Premier League, OPTA performance index, team performance, financialvaluation

1. Introduction Many industries are increasingly dependent upon human assets rather than more traditional tangible or intangible assets for the development and maintenance of organizational competitive advantage. However, human assets are vulnerable (Barone et al, 1998, Cherubini and Luciano, 2003, Hung and Liu, 2005), making their control and use difficult, and accurate pricing complex. This is particularly the case in any professional sports industry. This paper describes a framework to enable an analyst to determine a link between the performance of an individual sports player and their financial market value. While the framework illustrated here can be applied more generally, we focus our discussion on the European soccer industry. One of the main reasons for doing this is the availability of a statistical performance index for all players playing in the main soccer leagues in Europe to provide us with a source of rich and consistent data, but also because these leagues are among the highest revenue generating professional leagues within world sport outside of the professional leagues in the USA. European soccer is also an increasingly attractive product across the world, with revenues from TV rights and marketing increasing in particular in Asia and through the global broadcasting of matches via the internet.

Our valuation model is based upon contingent claims methodology and standard techniques in stochastic calculus (Dixit and Pindyck, 1994). This approach is of particular relevance in noisy environments; i.e. uncertain environments where there are many sources of information, and where the value of much of this information is questionable (Childs et al, 2001, 2002, 2004). Our focus is on the Vulnerable Asset (VA), a critical human asset, represented in our paper by a soccer player, who possesses a degree of self-determination over their contractual relationship with their owner, and who has the power to default upon that contractual relationship (the authors, forthcoming).

In this paper, our model is used to determine the financial value of professional soccer players to their existing and any prospective owners. The model attempts to recognize that a player’s value is a product of a variety of factors, some of them obvious (such as on-field performance, injuries, disciplinary record), some of them less obvious (such as image rights, personal background, or language attainment for example). The profusion of variables which may influence the value of a VA such as a professional sportsman is an indication of the noise prevalent within industries of this type. An important aspect of the model is that it permits us to speculate upon the relative value of these playing assets for employers other than the VA’s current employer. Traditional measures of the value of an ‘income-producing asset’ assert that value is a product of market conditions of supply and demand, and hence the value of a methodology

1

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

which provides an evaluation of the asset for both the supplier and the demander is clear.

The paper is organized as follows. In the following section we briefly discuss relevant literature, focusing upon research on prediction within the sporting industries, as well as the application of financial concepts to soccer. We also introduce the source of the data described in this paper. This is followed by a description of the context of the research; namely the European soccer leagues and the English Premier League (hereafter EPL) in particular focusing upon the characteristics of success in these leagues. In Section Four we discuss our model formulation including an extended application of it to explain the value of a soccer player (Thierry Henry) during a specific EPL season, followed by a range of other applications in a variety of situations. This is followed by a brief assessment of the managerial implications of this work, before we draw the paper to a close and establish the future direction of the research. 2. A Brief Review of Relevant Literature We briefly discuss relevant literature in two areas, highlighting some key research on the prediction of results and performance, and upon the application of financial analysis within the soccer industry. We also introduce the Opta Index, which provides us with our data on the soccer players we discuss in this paper. 2.1 Research on Predicting Results and Performance Statistical analysis in the soccer industry initially focused upon finding statistical models for predicting the results of games. Important contributions on this theme can be found in Crowder et.al. (2002), Andersson et.al. (2005) and McHale and Scarf (2007). Dixon and Coles (2002) developed a Poisson regression model that was fitted to English league and cup soccer data from 1992 to 1995. The model was then used to exploit potential misalignments in the soccer betting market using bookmakers' odds from 1995 to 1996. Maher (1982) proposed a model in which the home and away team scores follow independent Poisson distributions with means reflecting the attacking and defensive capabilities of the two teams. Forrest and Simmons (2000a, 2000b) analyzed the predictive information contained in newspaper tipsters' match forecasts, and the performance of the Pools Panel, an official body tasked with providing hypothetical results for matches that were postponed to enable these results to contribute to the various soccer betting pools that dominated the UK betting industry for most of the post Second World War period.

The development of the Opta Database (please see Section 2.3), allowed analysts to establish a direct link between a player’s on-field actions and

2

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

performance, including team results to which they have contributed. Previous studies along this line include those by Barros and Leach (2006), Espitia-Escuer et al. (2006), McHale (2007), and Szczepa�ski (2008). While these studies focused more on the characteristics of individual players another stream of the literature looked at the entire team performance. The idea that performance is a productive function of various inputs has been advocated for soccer analysis since Sloane (1971, 1997). Another seminal paper on this topic is by Carmichael et al. (2000) who considered the linkage between EPL team performance together with the skills and other characteristics of the team members, and the result (a victory or loss) of the match in head-to-head competitions between clubs. Dawson et al. (2000) and Hass (2003) also analyzed the efficiency of the EPL. Ultimately it is the team’s performance that matters and various ways to identify performance drivers for team success have been discussed in Haddley et al. (2000), Crowder et al. (2002), Hirotsu and Wright (2002, 2003), Hope (2003), Barros and Leach (2006), Fitt et al. (2006). Recently, Oberstone (2009) investigated the key factors of success in the EPL by developing a multivariate regression model based on an array of twenty-four pitch actions, collected during the 2007-08 season. One-way ANOVA is used to identify those specific pitch actions that statistically separate the top four clubs from the clubs classified in the middle of the pack and also from the bottom four clubs. Using ANOVA it was possible to identify thirteen pitch actions contributing significantly to the differentiation of the top four clubs from the other clubs. 2.2 Finance and Football Despite the research discussed in Section 2.1, it is surprising to note that there has been very little research to establish a linkage between player or team performance and player or club financial market value. Part of the difficulty perhaps lies with the fact that sportsmen are not tangible assets and valuation is consequently difficult. Paxson (2001) considered a real options view on soccer players, emphasizing the difficulty of decision making when the main assets are the players themselves. Amir and Livne (2005) considered an accounting perspective on football players as intangible assets that might need to be capitalized in a uniform regulatory manner. They failed to detect evidence between the investment in player contracts and future benefits for their clubs. The relationship between future economic benefits and prior investment in soccer players is based on the assumption that the club’s level of production is determined a by current portfolio of tangible assets, such as stadia, commercial shops, TV channels et cetera, and the portfolio of intangible assets, i.e. the soccer players. Forker (2005) discussed some weaknesses of their conclusions emphasizing that their results came from accounting-based tests. These are under

3

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

researched themes and issues such as amortization and economic replacement costs deserve further investigation from an accounting point of view, and there is also a need for econometric tests to be improved. A seminal paper providing a framework for determining a player’s financial value from the dynamics of his performance is Tunaru et al. (2005), and it is upon the methodology proposed in this paper that we intend to draw. 2.3 OPTA Performance Index Opta Sportsdata describe themselves as Europe's leading compiler of sports performance data, with a presence in England, Germany and Italy and a plan to expand to new countries. Opta Index was born in 1996, a football-based version of the successful Coopers & Lybrand cricket statistics. In 2001, Opta Index was purchased by BSkyB, the UK broadcaster, who ran the company until 2003 when SportingStatz purchased the brand. BSkyB continue their association with Opta by retaining a shareholding. The database compiles every touch of the ball during over 2,000 games of soccer a year resulting in over 4,000,000 individual events. Opta provides the full analysis from the EPL, Italy's Serie A, the German Bundesliga, France's Ligue One and the UEFA Champions League. 3. Research Setting To give an idea of the value of Europe’s soccer industry, and of the biggest clubs in particular, it is instructive to quote some figures from the latest Deloitte Football Money report (Deloitte, 2009). This reports that the combined revenue of the 20 highest grossing clubs in Europe (6 from England, 4 each from Germany and Italy, 2 each from Spain and France, and 1 from Turkey) was €3.9b in season 2007-08, a 6% increase on the previous year. This compares to the total revenue from the ‘big five’ European soccer leagues (England, France, Germany, Italy, and Spain) in season 2003-04 of €5.8b, giving an indication of the rapid growth particularly among the elite clubs frequently contesting the UEFA Champions League competition. The largest revenue generating league is the EPL, which Deloitte estimated generated revenues of £1.9b during this season, and it is upon this league that the remainder of the paper focuses. Despite this growth in revenues, the profitability of many EPL clubs is either negligible or negative, with Deloitte suggesting that many leading clubs are essentially ‘not-for-profit’ organizations (Deloitte, 2009: 36) due to their excessive ‘cost of sales’, principally player salaries and transfer fees.

However there is some suggestion that clubs are increasingly aware that this situation, and in particular the share of revenue lost to player wages, is unsustainable. For example, player wages in the EPL accounted for £811m in

4

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

season 2003-04, a rise of 7% on the previous season. This represented a slight decrease in the growth trend, and “well below the astonishing compound annual growth rate of 23% seen in the previous decade” (Deloitte, 2005:7). That season, the average wages/turnover ratio in the EPL was 72%, down from a previous high of 82%, and Deloitte suggest that this proportion was diminishing as clubs were becoming increasingly aware that they must control the amount of revenue paid to their players if they are to retain any form of financial stability (Crawford, 2006). The recent example of EPL side Portsmouth Football Club, where financial security has been severely weakened due to overspending on player salaries without a consummate increase in club revenues is a case in point.

However the share of revenue dedicated to wages is a clear indicator of the extent to which the EPL is dependent upon its players. As we have suggested, the players are VAs, and the competitive advantage of the clubs is directly related to their on-field, and increasingly to their off-field, performance. The dilemma for clubs is that a greater control over cost must be achieved while at the same time maintaining on-field performance, as the principal means of maintaining status.

The professional soccer industry, as with all professional sports industries, exhibit characteristics which indicate their differences from more conventional businesses, while at the same time sharing some key similarities. One key difference is that of organizational purpose, as reflected by key performance indicators. Sports, crucially, possess a more visceral appeal. Supporters of a soccer club (who may or may not also be shareholders) demand entertainment, and are hence customers in a conventional sense. They have relatively little interest in the financial wellbeing of the club and its key shareholders except when the financial wellbeing of the club threatens its long term viability, such as happened with several high profile clubs including Leeds United, Newcastle United, and the aforementioned Portsmouth in the UK, Parma and Fiorentina in Italy, and the Montreal Expos baseball team.

What is so striking about sport is that the main focus of most owners of professional sporting teams is also upon performance measures such as ‘entertainment’ and ‘glory’ rather than upon the bottom line. Indeed, economists have argued that soccer clubs have never been run as pure profit maximisers (Szymanski, 2003; Dobson and Goddard, 2001). Formerly, in the UK at least, club owners had been life-long supporters of their club and prepared to make business decisions that they would never countenance in a more conventional business environment. The success of Blackburn Rovers, in winning the EPL in 1995, was directly attributable to the financial support of Jack Walker, an industrialist whose investment in his club was never intended to yield financial returns of the nature he was accustomed to from operating Walkersteel, his family-owned steel business. In Italy the ‘owner-supporter’ is even more common. For example, prior to being listed on the Borsa Italiana, Juventus of

5

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

Turin was owned and operated by the Agnelli family, owners of the Fiat automobile company.

Add to this recent statements by senior soccer officials (particularly Michel Platini, President of UEFA) that clubs should be penalized for funding their expenditure by a reliance upon debt, and a perspective emerges that suggests that only seeking to manage a football club like a traditional competitive business creates the environment for financial survival and success. Pressures are mounting upon major soccer teams to become more ‘business like’, by which we mean that pressure exists for soccer teams to be aware of the need for the financial side of the club to be run as effectively as possible to support the performance of the sporting side of the club. Indeed, in recent years new types of owners have entered the EPL, many of whom are familiar from US sports (e.g. Malcolm Glazier, owner of the Tampa Bay Buccaneers NFL team owns Manchester United, Randy Lerner, owner of the Cleveland Browns NFL team also owns EPL side Aston Villa, while George Gillett, former owner of NHL team The Montreal Canadiens and Tom Hicks, owner of the Texas Rangers, co-own EPL side Liverpool) and all of whom appear to expect to operate these teams on a more financially rigorous, and business like fashion than traditional EPL owners. This is not universally the case, and the EPL has also seen other new owners, mainly from the middle-east or rapidly developing economies (such as Roman Abramovich at Chelsea or Mansour bin Zayed Al Nahyan at Manchester City), whose investments appear to be motivated by ownership status and is perhaps more akin to old-style owners, but without the local affiliations.

We suggest that the key performance criterion for all soccer teams is the maintenance of status. In arriving at this conclusion we looked at the purpose of a soccer team, and determined that there are several that can be pursued. These are (1) winning competitions, (2) operating profitably or (3) maintaining their status in the hierarchy. In the professional soccer leagues of Europe in the early 21st century, relatively few clubs have the opportunity of winning competitions; for example since its inception in 1992, only four clubs have won the EPL. The numbers of clubs that operate profitably are also relatively low, and the return on investment (ROI) for these clubs would be unacceptable for traditional businesses. This leaves us to conclude that while winning competitions and operating profitably are the purpose of a small group of clubs, the majority of clubs satisfice (Simon, 1957), which we interpret as seeking to maintain their status in the soccer hierarchy even if achieving this goal is at the expense of operating profitably. This is because status can be an extremely valuable commodity, with for example TV revenues which closely reflect a club’s status in the soccer hierarchy for the 20 largest European clubs accounting for 41% (or €1.6b) of total revenue for season 2007/08 (Deloitte, 2009, p.33); these clubs are possibly prioritizing revenue growth over profitability.

6

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

At the same time as status has assumed greater importance, so the resources required to maintain that status have become more expensive to control and use. A variety of factors are important here. They include:

� The changing nature of investment in soccer: numerous clubs have sought to differentiate their sources of revenue and have floated their clubs on stock markets. This has brought into soccer more investors that view clubs more as traditional financial investments than emotional investments, hence a subtle change in the purpose of these clubs;

� The development of meaningful international competition for finance and resources: clubs have always competed on the field for trophies; they now compete off the field for access to players and to funds and revenues. The UEFA Champions League (founded in 1992) was the catalyst for this major change; and

� The rising cost of playing assets: as has been noted (the authors, forthcoming) players are no longer the chattels of clubs, but effectively independent contractors who can sell their skills and expertise into an almost open market (it is not a fully open market due to national employment regulations, but as an effect of the development of trading blocks and legislation to promote the international mobility of labor, and even human rights legislation, this market is becoming much more open). All of these factors have impacted upon each other, and have perpetuated

the growth and importance of each other. Maintaining status now depends upon exploiting the appropriate assets, which requires access to ever greater funds, or the development of a more sophisticated approach in using limited resources to finance the use of those assets. This problem is complicated even further by the fact that the assets in question are vulnerable. 4. Model Formulation It is our contention that statistical analysis of past performance can help develop a model for more accurately determining the financial value of a soccer player. From a modeling point of view what is needed is a variable that is reliable, observable and calculated consistently across discrete but similar activities (such as the 38 games each EPL side plays per season) to allow for appropriate comparisons between the parallel games/events.

Fortunately OPTA Sportsdata, introduced earlier, provides an answer to these requirements. The OPTA Index results from a database where over 400 variables are recorded for all games in a given league such as the EPL. This index encapsulates numerically the individual performance of players and teams. Since the same calculation is made for each player in each game included in the index, one can make relative value calculations and develop methodologies for financial

7

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

value calculation of players and of clubs. As previously noted, we will make extensive use of the valuation formulas established in Tunaru et al. (2005). Their methodology makes an important distinction between valuations made by the incumbent owner of the player’s rights and the potential club that is looking into transferring the player into their team.

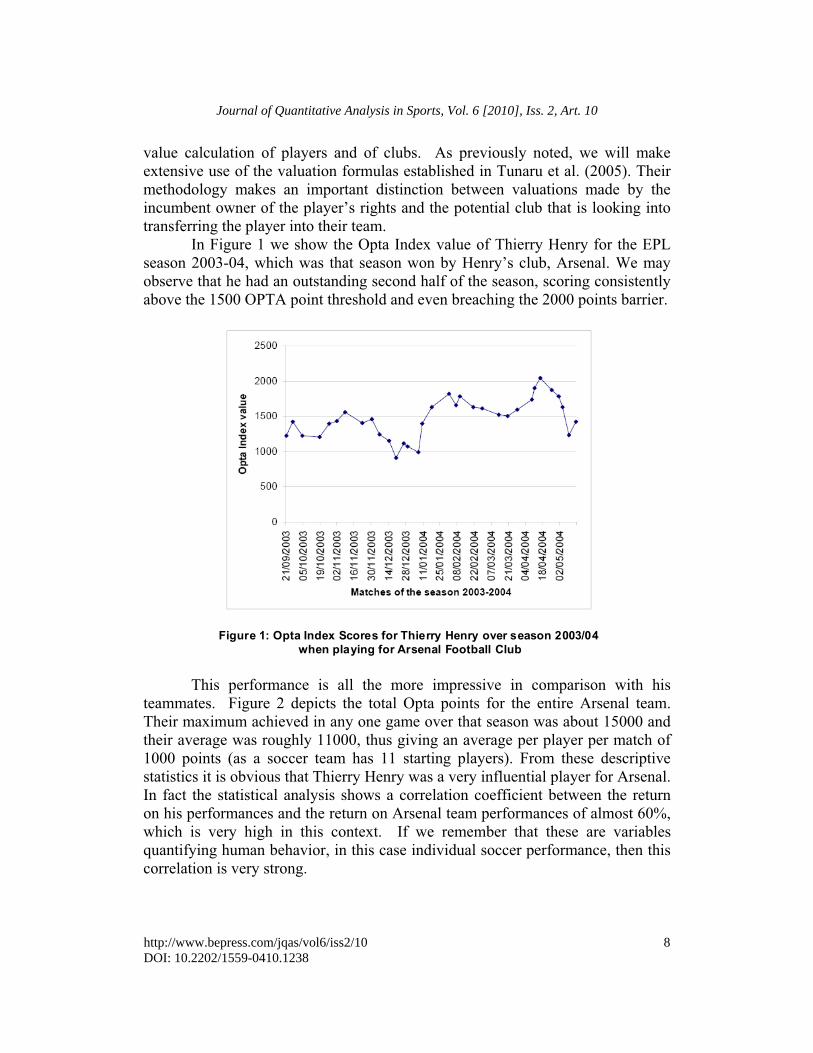

In Figure 1 we show the Opta Index value of Thierry Henry for the EPL season 2003-04, which was that season won by Henry’s club, Arsenal. We may observe that he had an outstanding second half of the season, scoring consistently above the 1500 OPTA point threshold and even breaching the 2000 points barrier.

This performance is all the more impressive in comparison with his

teammates. Figure 2 depicts the total Opta points for the entire Arsenal team. Their maximum achieved in any one game over that season was about 15000 and their average was roughly 11000, thus giving an average per player per match of 1000 points (as a soccer team has 11 starting players). From these descriptive statistics it is obvious that Thierry Henry was a very influential player for Arsenal. In fact the statistical analysis shows a correlation coefficient between the return on his performances and the return on Arsenal team performances of almost 60%, which is very high in this context. If we remember that these are variables quantifying human behavior, in this case individual soccer performance, then this correlation is very strong.

Figure 1: Opta Index Scores for Thierry Henry over season 2003/04 when playing for Arsenal Football Club

8

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

Moreover, Henry missed only one week through injury so the injury arrival rate was estimated as one game per season. The size of the fall in value due to an injury event was taken as 10%. This means that 10 injuries in a season will completely wipe out the value of the player to the owning club. The issue of how much potential value (in terms of the intrinsic value of the player and the value of the player as an asset to his owner) is lost through injuries requires further analysis, as it may be possible to differentiate the potential impact of different types of injuries and their timing, and so add a further level of sophistication to the analysis. Nevertheless the major question in the soccer industry, “How much is a player worth?”, needs deeper consideration.

Tunaru et al (2005) developed a methodology for quantifying dynamically

Henry’s value to his own club. The financial value of a single OPTA point for Arsenal during season 2003-04 was calculated as being £417. There was about an 80% correlation between the turnover of the club, week by week, and the team performance as measured by OPTA. Post 2007 this value will be considerably higher as the club has moved to a new stadium with a much higher capacity and consequently additional revenue generating operations. Figure 3 illustrates the financial market value for Henry and we can see how this monetized value fluctuates with his performance as measured by the OPTA index. The financial value varies between £10m and £20m over season 2003-04 with an average value of £16.33m. It is worth pointing out that this calculation was done from the point of view of his then employers, Arsenal. Hence, based on the statistical analysis of

Op ta A rsenal

0

2 00 0

4 00 0

6 00 0

8 00 0

10 00 0

12 00 0

14 00 0

16 00 0

16/

08/2

003

16/

09/2

003

16/

10/2

003

16/

11/

200

3

16/

12/2

003

16/0

1/2

004

16/0

2/2

004

16/

03/

200

4

16/0

4/2

004

Opta A rs enal

Figure 2. Opta Points for the entire team of Arsenal over the season 2003-04.

9

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

his performance over the season 2003-04 Arsenal should have valued Henry at close to £17 million, in any notional sale to a new employer. In fact, this is exactly the figure for which he was sold to Barcelona in June 2007.

We can expect that the calculation will be different for a potential new employer willing to transfer the player. The reason behind this argument is that if Henry is either transferred to a new club or he is considering defaulting on his current employer by entering into a strategy that is loss making for his current club1, the current club is losing one member of the squad and to keep things the same at least numerically they will have to transfer in a new player from outside. In the soccer industry this may be a problem because similar players may not be available or if they are available they may be more expensive than usual due to market liquidity constraints or the scarceness of appropriately highly skilled assets. This is in essence the basis of our argument that players are vulnerable assets (VAs). For the new employer however, the transfer means that the new 1 The player may decide that his future lies elsewhere and he may refuse to train with his team, refuse to play at his potential and create a state of unrest among his team mates and club fans.

Figure 3. The evolution of Thierry Henry’s financial value to Arsenal Football Club over the entire season 2003-04.

Henry's value for Arsenal

0

5000000

10000000

15000000

20000000

25000000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33

Matches in the season 2003-04

Mar

ket V

alue

Henry's value for Arsenal

0

5000000

10000000

15000000

20000000

25000000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33

Matches in the season 2003-04

Mar

ket V

alue

10

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

club is either increasing the squad by one, or they are placed in a position where they decide to sell one of their players in order to generate the capital needed for the transfer. The difference in the positions vis-à-vis the market creates the difference in the financial value of a player such as Thierry Henry to his current club and any new potential club, everything else being equal.

Henry’s total money contribution (cumulative) via Opta points was £20.3 million during season 2003-04. His value could have been even higher if Arsenal had been able to generate more income from their UEFA Champions League matches. For example an increase of revenue leading to the increase in value of one Opta point to Arsenal to £500 would increase Henry’s value to Arsenal to an average of £19.12m.

Another subtlety is the location of the prospective new employer. If a club is exploring whether or not to sign a player from another club playing in the same national league competition as the player’s current club then the analysis at club level is somewhat simplified because the financial economics of the game are similar and the transaction will be conducted in the same currency. However, if the new club is from a different country then the pricing methodology ought to be adapted to take into consideration issues such as foreign currency exchange rates, and also the financial and economic characteristics of that particular country2.

Human assets are difficult to price in a noisy environment such as the soccer industry. Is the value of a vulnerable asset such as a soccer player the same for all clubs present on the market? In other words does the law of one price function here? Our empirical investigations show clearly that this is not the case. In figure 4 we illustrate in parallel the value of Henry over the season 2003-04 for Arsenal and for another club, in this case Manchester United. It is obvious that Henry’s value would be less for Manchester United. Our heuristic explanation is that if Manchester United were to buy Henry and not sell an existing squad player, they would be adding to their current squad or roster of players while if Arsenal were to sell or lose3 Henry they will be one player short.

2 As an example, until the UK government’s recent decision to increase the upper income tax banding, players playing in France paid higher taxes on their income than their counterparts in the EPL. At the time, taxes in the UK were much lower and therefore it was not surprising that there were so many French players pursuing their careers in the EPL. 3 Players who have reached the end of their contracts are not obliged to sign new contracts, and are able to assume what in US sport is called ‘free agency’ under the Bosman Ruling, named for the Belgian soccer player (Jean-Marc Bosman) who originally took this case to the European Court of Justice.

11

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

0

5000000

10000000

15000000

20000000

25000000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33

Figure 4. The Market Value of Thierry Henry for Arsenal (�) and for ManU (�) with the value of one point equal to £500)

12

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

Let’s consider the same question, although this time for another EPL side, Aston Villa. In 2003-04 the total revenue generated by Aston Villa was £84.4m. Under the (unrealized) assumption that Aston Villa had an identical performance on the pitch with Arsenal it would have meant that one Opta point during that season was worth £200 for Aston Villa. Thus, Aston Villa could not recover the same value from Henry’s performance as would Arsenal, so paying him similar wages to those he received at Arsenal would have resulted in a loss. There are various reasons for this: firstly Aston Villa would have had to transfer him to the club, and there will always be some friction costs because other Aston Villa players may have had to be sold at a discount to enable the transfer and there may well be an accommodation period while the player settles in. However, perhaps more important is the fact that the economic engine of Aston Villa is not comparable with top clubs such as Manchester United and Arsenal.

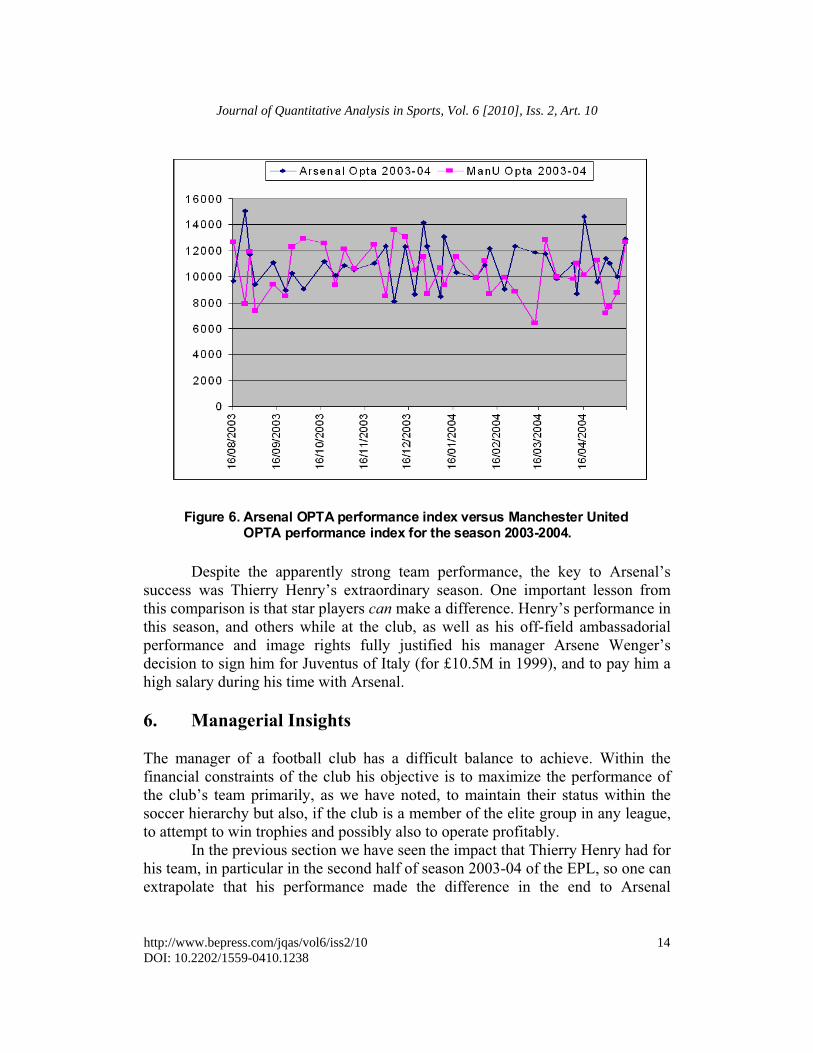

Even in this brief example, we demonstrate that statistical analysis of this nature can be useful to highlight the differential financial contribution such a VA can make, which can assist in determining whether such an investment (i.e. the transfer of a VA from one club to another) is a risk worth taking. 5. Further Insights from Statistical Analysis In this section we show how statistical analysis can extract valuable information about soccer teams and players by looking at the OPTA performance index. In Figure 6 we compare the team index for the EPL champions in season 2003-04 (Arsenal) with their main competitor (Manchester United). It is evident that while Manchester United enjoyed a slightly better first half of the season, Arsenal had a better second half of the season. It is important to remember that in the EPL there is no mid-season break.

There are several points that we would like to point out when comparatively analyzing the performance of the two best teams in season 2003-04 in the EPL. First, both teams seem to have their equilibrium performance level just about 11000 OPTA index points. This implies an average of 1000 OPTA Index points per player per game so players producing well in excess of this threshold are extremely valuable assets for their clubs. Secondly, counting the number of consecutive downward jumps, Arsenal had four runs with two consecutive drops (there is another one that can be easily attributed to noise in data collection) while Manchester United had four runs with two consecutive drops. Arsenal never had a team score below 8000 points while Manchester United had had four such games. Additionally, Arsenal had three games with performances above 14000 points while Manchester United never breached that barrier.

13

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

Despite the apparently strong team performance, the key to Arsenal’s

success was Thierry Henry’s extraordinary season. One important lesson from this comparison is that star players can make a difference. Henry’s performance in this season, and others while at the club, as well as his off-field ambassadorial performance and image rights fully justified his manager Arsene Wenger’s decision to sign him for Juventus of Italy (for £10.5M in 1999), and to pay him a high salary during his time with Arsenal. 6. Managerial Insights The manager of a football club has a difficult balance to achieve. Within the financial constraints of the club his objective is to maximize the performance of the club’s team primarily, as we have noted, to maintain their status within the soccer hierarchy but also, if the club is a member of the elite group in any league, to attempt to win trophies and possibly also to operate profitably.

In the previous section we have seen the impact that Thierry Henry had for his team, in particular in the second half of season 2003-04 of the EPL, so one can extrapolate that his performance made the difference in the end to Arsenal

Figure 6. Arsenal OPTA performance index versus Manchester United OPTA performance index for the season 2003-2004.

14

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

winning the league. Another important factor that should not be overlooked is the frequency and seriousness of the injuries experienced by players in the squad. In Figure 7 we illustrate the week by week total number of injured players for Manchester United in season 2003-04. There is a clear dichotomy between the first half of the season and the second half. The volatility of the number of injuries is much higher for the latter. This suggests that as some players were coming back from injury, other players were getting injured. This creates a problem for the manager who has to consider the probability that players coming back from injury may still need a number of games to get to their standard level of performance and also that changing the team on a frequent basis may be detrimental to the team, by preventing them from developing a deeper understanding between them. It also may help explain Manchester United’s relatively poorer second half to this season.

Another question we can offer commentary upon is ‘does a superstar

player always help a team win competitions?’ Here we use the same tools as utilized above for Thierry Henry but for another interesting case, that of Rio Ferdinand, the current captain of Manchester United who we examine for season 2004-05 of the EPL. His value at the beginning of that season was zero, because in the previous season he received a long ban for missing a drug-test and thus

Man U 2003-04

00.5

11.5

22.5

33.5

44.5

16/0

8/20

03

16/0

9/20

03

16/1

0/20

03

16/1

1/20

03

16/1

2/20

03

16/0

1/20

04

16/0

2/20

04

16/0

3/20

04

16/0

4/20

04

No

of I

nju

ries

Figure 7. The evolution of injuries for the entire Manchester Unitedteam in the 2003-04 season

15

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

played no part in early season games. His transfer from Leeds United (for £30m in 2002) had dwarfed any previous transfer fees for a defender. His off-the-field problems should not take away from his on-the-field performance, should it? Our analysis suggests that this is not the case reinforcing the complexity of valuing a human asset. Even allowing for this initial artificial ranking, his performance during the season was relatively poor, as can be seen from Figure 8.

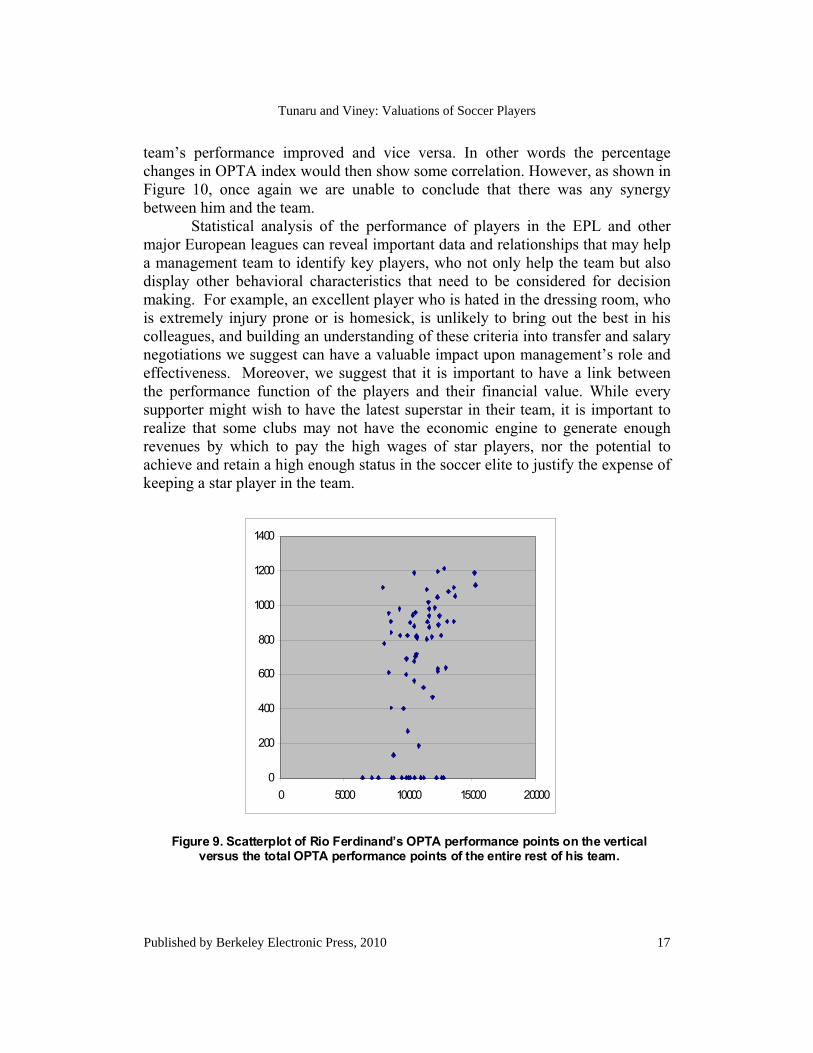

His relative value, as measured by our analysis, never reached £0.6m and this was very low considering his high wages and his transfer fee. As can be seen from Figure 9, there was no correlation between his performance and the team’s performance. The scatter plot shows no association between the levels of his performance and his team’s OPTA index score. This does not necessarily mean that his intrinsic value was low or that he should be dropped from the team. Defenders in soccer take longer to reach their peak and quite often they may be penalized for making a relatively limited number of mistakes during a season. However, his OPTA index scores were consistently so low that one may ask the question whether he justified his high salary by virtue of his poor performances?

One could argue that it possibly was a bad season for the entire team, not just for him. If that was the case then his performances would improve when the

Rio Ferdinand Sterling Value to ManU

0

100000

200000

300000

400000

500000

600000

15/08

/2004

15/0

9/200

4

15/10

/200

4

15/11

/2004

15/12

/2004

15/0

1/200

5

15/02

/2005

15/03

/2005

15/0

4/200

5

15/0

5/200

5

Figure 8. Financial Value of Rio Ferdinand for his club Manchester United through the season 2004-05.

16

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

team’s performance improved and vice versa. In other words the percentage changes in OPTA index would then show some correlation. However, as shown in Figure 10, once again we are unable to conclude that there was any synergy between him and the team.

Statistical analysis of the performance of players in the EPL and other major European leagues can reveal important data and relationships that may help a management team to identify key players, who not only help the team but also display other behavioral characteristics that need to be considered for decision making. For example, an excellent player who is hated in the dressing room, who is extremely injury prone or is homesick, is unlikely to bring out the best in his colleagues, and building an understanding of these criteria into transfer and salary negotiations we suggest can have a valuable impact upon management’s role and effectiveness. Moreover, we suggest that it is important to have a link between the performance function of the players and their financial value. While every supporter might wish to have the latest superstar in their team, it is important to realize that some clubs may not have the economic engine to generate enough revenues by which to pay the high wages of star players, nor the potential to achieve and retain a high enough status in the soccer elite to justify the expense of keeping a star player in the team.

0

200

400

600

800

1000

1200

1400

0 5000 10000 15000 20000

Figure 9. Scatterplot of Rio Ferdinand’s OPTA performance points on the verticalversus the total OPTA performance points of the entire rest of his team.

17

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

This kind of analysis is very important for the manager especially as

players may become more difficult to manage as their status and image grows. Hence being able to pinpoint the qualities of the player and the performance ties with the entire team is imperative in the current environment where spiraling wages and increased revenues are linked, directly or indirectly, to performance. 7. Conclusion and Future Research The OPTA performance index offers a tool to analyze statistically the performance of soccer players and their teams. This is very important for establishing a more realistic assessment of the financial value of players but also for extracting useful information about what determines success on the pitch for a given team or the potential linkages between individual players and their teams. This paper represents a first attempt to highlight the potential we believe this methodology offers.

This area of research is in a nascent phase but with the availability of more accurate information there is scope for expanding this research in several directions. First, we would like to continue our research by undertaking evaluations of entire teams and implicitly of their parent clubs. After all, the clubs main assets are their players. Secondly we would like to develop a ranking tool

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

-0.6 -0.4 -0.2 0 0.2 0.4 0.6

ManU

Ferd

inan

d

Figure 10. Scatterplot of percentage returns of Rio Ferdinand’s OPTA performance points on the vertical versus the percentage returns of total OPTA

performance points of the entire rest of his team.

18

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

that will identify the best and worst teams in terms of their financial performance, rather than the more normal ranking by performance and we can estimate that this ranking may not necessarily coincide with the actual ranking determined by match results. Last but not least we would like to drill-down into the statistical information contained in the OPTA database and identify the unsung heroes. These are the ‘moneyball’ players who make a significant contribution but do not receive either glory or very high financial rewards. References Amir, E. and Livne, G., (2005), ‘Accounting Valuation and Duration of Football

Player Contracts’, Journal of Business, Finance and Accounting, 32(3), pp. 549-586.

Andersson, P., Edman, J. and Ekman, M., (2005), ‘Predicting the World Cup 2002 in soccer: Performance and confidence of experts and non-experts’, International Journal of Forecasting, 21(3), pp. 565-576.

Barone, E., Barone-Adesi, G. and Castagna, A., (1998), ‘Pricing bonds and bond options with default risk’, European Financial Management, 4(2), pp. 231-282.

Barros, C. P. and Leach, S., (2006), ‘Performance evaluation of the English Premier Football League with data envelopment analysis’, Applied Economics, 38(12), pp.1449-1458.

Carmichael F., Thomas D., and Ward R., (2000), ‘Team Performance: The Case of English Premiership Football’, Managerial and Decision Economics, 21(1), pp. 31-45.

Cherubini, U. and Luciano, E., (2003), ‘Pricing Vulnerable Options with Copulas’, Journal of Risk Finance, 5(1), pp. 27-39.

Childs, P.D., Ott, S.H., and Riddiough, T.J., (2001), ‘Valuation and Information Acquisition Policy for Claims Written on Noisy Real Assets’, Financial Management, 30(2), pp. 45-75.

Childs, P.D., Ott, S.H., and Riddiough, T.J., (2002), ‘Optimal Valuation of Claims on Noisy Real Assets: Theory and an Application’, Real Estate Economics, 30(3), pp. 415-443.

Childs, P.D., Ott, S.H., and Riddiough, T.J. (2004), ‘Effects of Noise on Optimal Exercise Decisions: The Case of Risky Debt Secured by Renewable Lease Income’, Journal of Real Estate Finance & Economics, 28(2/3), pp. 109-121.

Crawford, L., (2006), ‘Penalties of a superstar strategy’, Financial Times.

19

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010

Crowder, M., Dixon, M., Ledford, A. and Robinson, M., (2002), ‘Dynamic modeling and prediction of English football league matches for betting’, Journal of the Royal Statistical Society, series D (The Statistician), 51(2), pp. 157-168.

Dawson. P., Dobson. S. and Gerrard, B., (2000), ‘Stochastic Frontiers and the Temporal Structure of Managerial Efficiency in English Soccer’, Journal of Sports Economics. 1(4), pp. 341-362.

Deloitte (2005), Annual Review of Football Finance, London: Deloitte Deloitte, (2009), Football Money League 2009, London: Deloitte Dixit, A.K. and Pindyck, R.S., (1994), Investment under uncertainty, Princeton,

New Jersey: Princeton University Press. Dixon, M. and Coles, S., (1997), ‘Modeling Association Football Scores and

Inefficiencies in The Football Betting Market’, Journal of Royal Statistical Society: Series C, 46(2), pp. 265-280.

Dobson, S. and J. Goddard, (2001), The Economics of Football, Cambridge: Cambridge University Press

Espitia-Escuer, M., and García-Cebrián, L.I., (2006), ‘Performance in sports teams: Results and potential in the professional soccer league in Spain’, Management Decision, 44(8), pp.1020-1030.

Fitt, A.D., Kabelka, M. and Howls, C.J., (2006), ‘Valuation of soccer spread bets’, Journal of the Operational Research Society, 57(8), pp. 975-985.

Forker, J., (2005), ‘Discussion of Accounting, Valuation and Duration of Football Player Contracts’, Journal of Business, Finance and Accounting, 32(3), pp. 587-598.

Forrest D. and Simmons R., (2000a), ‘Forecasting sport: the behaviour and performance of football tipsters’, International Journal of Forecasting, 16, pp. 317-331.

Forrest D. and Simmons R., (2000b), ‘Making up the results: the work of the football pools panel, 1963-1997’, The Statistician 49, pp.253-260.

Haas. D. J., (2003), ‘Productive efficiency of English football teams- a data envelopment approach’, Managerial and Decision Economics, 24, pp.403-410.

Hadley. L., Poitras. M., Ruggiero. J. and Knowles. S., (2000), ‘Performance evaluation of national Football League Teams’, Managerial and Decision Economics, 21, pp.63-70

Hirotsu, N. and Wright, M., (2002), ‘Using a Markov process model of an association football match to determine the optimal timing of substitution and tactical decisions’, Journal of the Operational Research Society, 53(1), pp. 88-96.

20

Journal of Quantitative Analysis in Sports, Vol. 6 [2010], Iss. 2, Art. 10

http://www.bepress.com/jqas/vol6/iss2/10DOI: 10.2202/1559-0410.1238

Hirotsu N. and Wright M., (2003), ‘Determining the best strategy for changing the configuration of a football team’, Journal of the Operational Research Society, 54(8), pp. 878-887.

Hope, C., (2003), ‘When should you sack a football manager? Results from a simple model applied to the English Premiership’, Journal of the Operational Research Society, 54(11), pp. 1167-1176.

Hung. M. and Liu, y. (2005), ‘Pricing Vulnerable Options in Incomplete Markets’, Journal of Futures Markets, 25(2), pp. 135-170.

Maher M.J., (1982), ‘Modeling association football scores’, Statistica Neerlandica, 36, pp. 109-118.

McHale, I., and Scarf, P., (2007), ‘Modeling soccer matches using bivariate discrete distributions’, Statistica Neerlandica, 61(4), pp. 432-445.

McHale, I.G., (2007), ‘Quantitative studies in sport’, The Operational Research Society, Keynote Papers Series.

Oberstone, J., (2009), ‘Differentiating the Top English Premier League Football Clubs from the Rest of the Pack: Identifying the Keys to Success’, Journal of Quantitative Analysis in Sports, 5(3), pp.1-27.

Paxson, D.A., (2001), ‘Real Football Options in Manchester’, in Howell, S., Stark, A., Newton, D., Paxson, D., Cavus, M., and Pereira, J. (eds), Real Options-Evaluating Corporate Investment Opportunities in a Dynamic World, London: Financial Times-Prentice Hall.

Simon, H.A. (1957), Models of man - social and rational, New York: John Wiley and Sons

Sloane. P.J., (1971), ‘The economics of professional football: The football club as a utility maximiser’, Scottish Journal of Political Economy, 8, pp.121-146.

Sloane. P.J., (eds), (1997), ‘The economics of sport’, Economic Affairs. 17. Special issue. pp. 2-6.

Szymanski, S. (2003), ‘The Economic Design of Sport Contests’, Journal of Economic Literature, 41, pp.1137-1187

Szczepa�ski, �., (2008), ‘Measuring the effectiveness of strategies and quantifying players' performance in football’, International Journal of Performance Analysis in Sport, 8(2), pp.55-66.

Tunaru R, Clark, E. and Viney, H., (2005), ‘An Option Pricing Framework for Valuation of Football Players’, Review of Financial Economics, 14(3/4), pp.281-295.

21

Tunaru and Viney: Valuations of Soccer Players

Published by Berkeley Electronic Press, 2010