Valuation of REIT’s Property in Singapore - pvai.org€¦ · • AMP Capital took over...

39

savills.com.sg Challenges In Valuing REIT’s Properties in Singapore 12 May 2016 By: Cynthia Ng

Transcript of Valuation of REIT’s Property in Singapore - pvai.org€¦ · • AMP Capital took over...

savills.com.sg

Challenges In Valuing REIT’s Properties

in Singapore

12 May 2016 By: Cynthia Ng

Outline

S-REITs

• History & Evolution

• Performance

Current Local Practice for Valuation of

REIT’s Properties

• Standards & Guidelines

• What are We Valuing?

• Factors Affecting Value

• Basis & Assumptions

• Valuation Approaches

• Yields & Discount Rate

• Reconciliation of Valuation

• Valuation Report

Challenges Faced

• Technical Issue

• Economical Issue

• Human Issue

“ Thoughts For The Day”

• Current Practice Sustainable?

• Is Valuation Just “DCF”?

• Role of Valuer

S-REIT

Definition of REIT

• Closed-end funds that pool capital from

retail and institutional investors to invest

collectively in income-producing

properties

• Alternative channel to unlock book values

of the low-yield properties in the portfolios

• Hybrid instrument that combines the

features of RE, stock & bond

Benefits

• Convert relatively illiquid RE into liquid

REIT securities

• Can be traded on SGX – Enjoy tax

transparency status

• Distributions – Tax exemption

• Mandatory & high distribution of income

• Multi-property portfolio

• Regulated by MAS

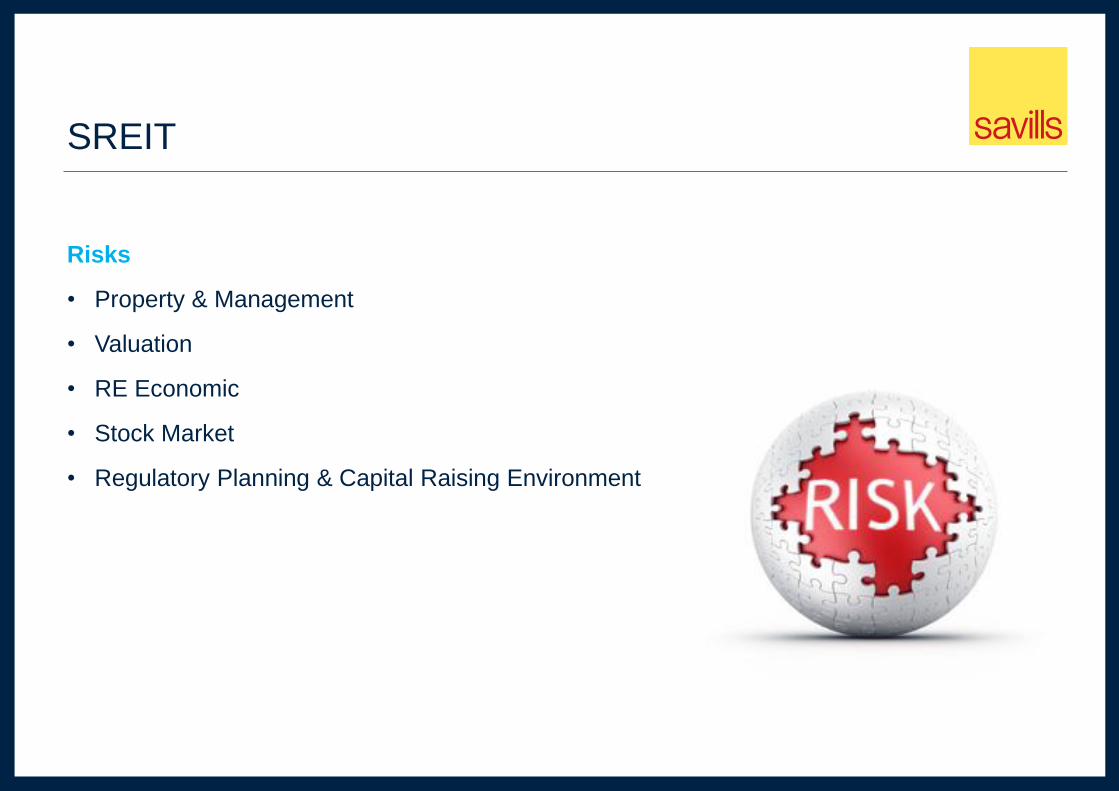

SREIT

Risks

• Property & Management

• Valuation

• RE Economic

• Stock Market

• Regulatory Planning & Capital Raising Environment

Latest Changes to S-REITs

Megers & Acquisitions

• F&N group acquired Allco Commercial REIT in 2008

• YTL Corporate Berhad took over Macquarie Prime REIT in Oct 2008 & renamed to Starhill Global REIT

• AMP Capital took over Macarthurcook Industrial REIT in 2009. Now known as AIMS-AMP Capital Industrial REIT

2015 Budget

Extended income tax exemption to local & foreign sources of S-REIT income received by individual investors for another 5 yrs from 1 March 2015

Stamp duty remission for REITs on purchase of local properties was not extended

MAS Revised Guidelines Jul 2015

Leverage limit increased to 45% of total assets

Asset managers are required to provide justification & disclosure on structure & type of fees charged

S-REITs

Industrial

Commercial/Retail

Hotel

Service Apartment

Hospitality

MAS Guidelines for

Valuation of REITs’ Properties

Interested Party Transaction

REIT to obtain 2 independent valuations of the property, with one to be commission by

the Trustee

In case of purchase, the transacted price can’t be above the higher of the 2 independent

valuations

In case of sale, the transacted price can’t be below the lower of the 2 independent

valuations

Valuation of Assets

To provide full valuation of all properties own by the REIT at lease once a year. However, if

REIT proposed to issue new units for subscription, & the last valuation is more than 6

months, DT valuation would suffice.

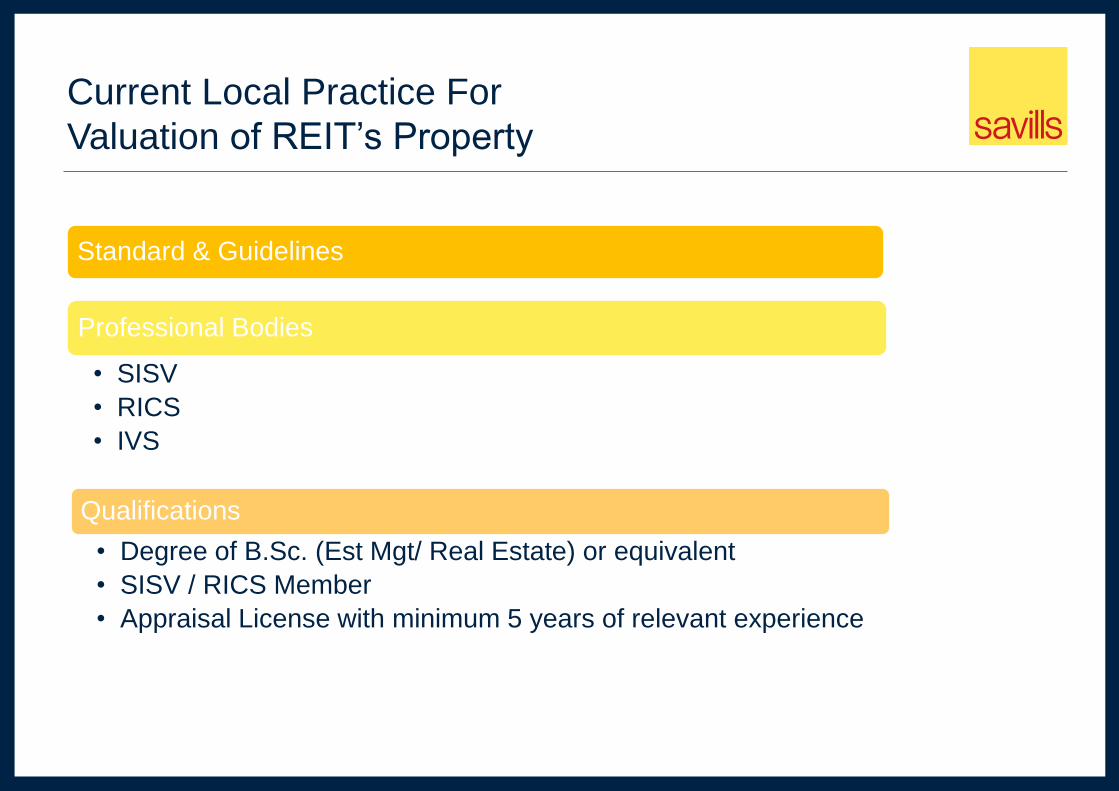

Current Local Practice For

Valuation of REIT’s Property

Standards & Guidelines

What Are We Valuing?

Factors Affecting Value

Basis and Assumptions

Valuation Approaches

Yields & Discount Rate

Valuation Reconciliation

Current Local Practice For

Valuation of REIT’s Property

Qualifications

• Degree of B.Sc. (Est Mgt/ Real Estate) or equivalent

• SISV / RICS Member

• Appraisal License with minimum 5 years of relevant experience

Standard & Guidelines

Professional Bodies

• SISV

• RICS

• IVS

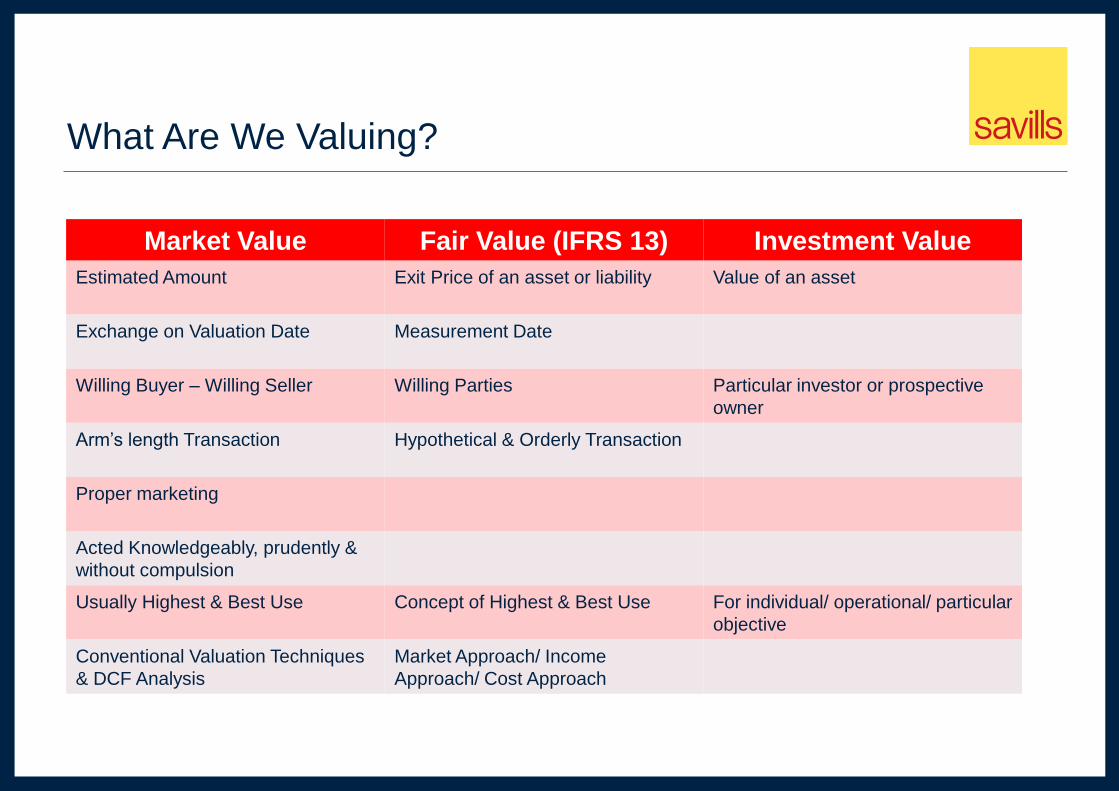

What Are We Valuing?

Market Value Fair Value (IFRS 13) Investment Value

Estimated Amount Exit Price of an asset or liability Value of an asset

Exchange on Valuation Date Measurement Date

Willing Buyer – Willing Seller Willing Parties Particular investor or prospective

owner

Arm’s length Transaction Hypothetical & Orderly Transaction

Proper marketing

Acted Knowledgeably, prudently &

without compulsion

Usually Highest & Best Use Concept of Highest & Best Use For individual/ operational/ particular

objective

Conventional Valuation Techniques

& DCF Analysis

Market Approach/ Income

Approach/ Cost Approach

Valuation of REIT’s Property

Location / Neighborhood

Subject Development/ Property

Financial Performance

Potential

Micro

Economical/ Political/ Environmental/

Social Factors

Indicators (Country Risk, Market Risk,

Currency Risk, Inflation)

Macro

Factors Affecting Value

Valuation of REIT’s Property

Location/ Neighborhood

Accessibility

Linkages

Commercial/ Retail

• CBD - Raffles Place/Marina Bay/Shenton/Robinson/Cecil Street

• Orchard vicinity

• Regional Centre

• MRT Station

Medical Centre

• Near or connected to Hospital

Micro

Valuation of REIT’s Property

Location/ Neighborhood

Industrial

• Industrial Parks

• Link to airport/ port/labour supply

Hotel/Service Apartment

• Mainland vs Sentosa

• Orchard vicinity vs Outlying area

Micro

Valuation of REIT’s Property

Subject Development

Type

Supports/ Facilities Provided

Commercial

• Premium Grade/ Grade A/B

• Green Mark Platinum/ Gold, etc.

Retail

• Shopping Mall vs Shop Unit vs Shophouse

• Tenant mixed/ Anchor tenants

Medical Centre

• Connect to hospital/ health care facility

Micro

Valuation of REIT’s Property

Subject Development

Type

Supports/ Facilities Provided

Hotel

• Class, Band & Management

Service Apartment

• Long-term stay vs Hotel style

Micro

Valuation of REIT’s Property

Subject Development

Industrial

• Use – SR/ Biz Space/ Flatted Factory/ Warehouse/ Data Centre

• Facility/ Specification provided

Micro

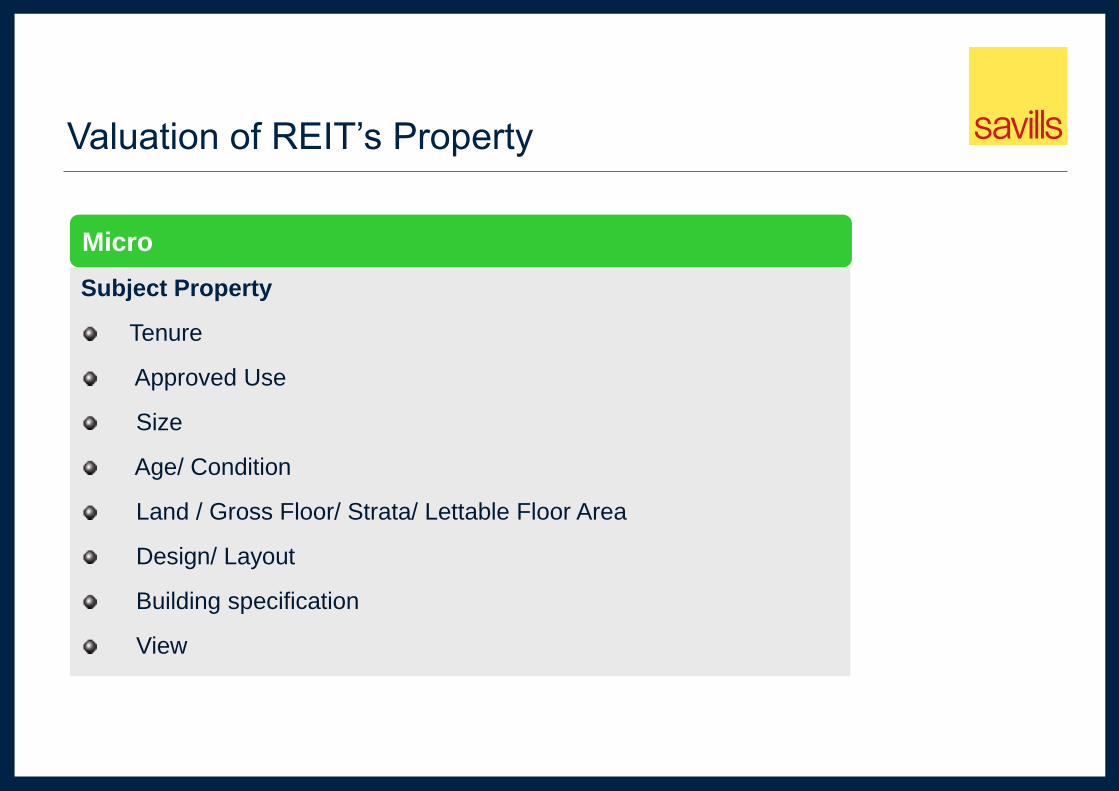

Valuation of REIT’s Property

Subject Property

Tenure

Approved Use

Size

Age/ Condition

Land / Gross Floor/ Strata/ Lettable Floor Area

Design/ Layout

Building specification

View

Micro

Valuation of REIT’s Property

Financial Performance

Gross / Net Revenue

Occupancy

Other Incomes/ Expenses

Special Lease Arrangement

Capex

Micro

Potential

Top Up Tenure

Unused Plot Ratio

Additions & Alterations

Major Upgrading Works

Re-development potential

Valuation of REIT’s Property

Economical

• Demand & Supply

• GDP/ Interest Rate/ Government Bond Rate, Inflation, Consumer Price

Index, Employment Rate, etc.

Political

• Government’s Stability

• Policies/ Measures

Environmental

Social

Macro

Valuation of REIT’s Property

• As Is – VP/ Subject to Tenancies/ Leaseback

• As Is Where Is

• As Is with Potential

• Upon Completion Basis

• Highest & Best Use

Basis of Valuation

• Physical

• Legal

• Planning

• Financial

Assumptions

Valuation of REIT’s Property

Direct Comparison Method

• Compare like with like

• Apply for standard property

• No fixed formula

• Applicable in active market

• Result influenced by market trend

Conventional

Valuation Approaches

What happen if no direct sales

comparable?

Look out for secondary sales

comparable

References/ Benchmarking

Valuation of REIT’s Property

Income Capitalization/Investment

Method

Apply to Income Generating Property

Variable factors – Yield & Net Income

CV = Net Income x Yield

Conventional

Valuation Approaches

Points to take note:-

Actual & Market Rents

Average Expiry Lease

Justification of Cap Rate

Valuation of REIT’s Property

Replacement Cost Method

► Assume Cost = Value

► CV = Land Value + Bldg Cost -

Depreciation

► Estimate of Depreciation –

economical/ functional/ obsolesce

► Apply to Monopoly Property

Conventional

Valuation Approaches

Points to take note:-

Act as a base value of the

property in normal market

Give higher result than DCM

in down market

Current Local Practice For

Valuation of REIT’s Property

Residual Value Method

► RLV = GDV - Development Costs

► Too many assumptions

► Applicable for Property with

Potential / Land / AS IS BASIS for

DEVELOPMENT SITE

Conventional

Valuation Approaches

Points to take note:-

Developer / Investors use

this method to determine

land price

Sensitive Factors –

Efficiency/ Profit/ Expected

Sales Price/ Construction &

Related Costs

Current Local Practice For

Valuation of REIT’s Property

Profit Method

► Applicable to Profitable/ Trading

Potential Property

► Estimate Tenant’s Share can be a

challenge

Conventional

Valuation Approaches

Points to take note:-

Unpopular in local practice

Valuation of REIT’s Property

DCF Analysis

Detailed Investment Method

Off the shelve vs In-House Excel

Required financial background &

knowledge of the relevant trade

Variables that affect the result of

Net Present Value

Discount Rate

Terminal Cap Rate

Growth Rate

IRR

NOI

Valuation Approaches

Points to take note:-

Involved more assumptions,

hence experience is a must

Analysis or Method of

Valuation?

Current Local Practice For

Valuation of REIT’s Property

Yields

Property Yield vs Dividend Yield

Property Yield ≤ Dividend Yield

Initial Yield < Reversion Cap Rate < Terminal Cap Rate

Industrial Yield > Hotel Yield > Retail Yield > Office Yield >

Residential Yield

Discount Rate

Comparable Discount Rate

Weighted Average Cost of Capital (WACC)

Capital Asset Pricing Model (CAPM)

Yields & Discount Rate

Dividend Yield Vs Property Yield

Dividend Yield = Annualised DPU/ Share Price

E.g. S$0.094/ S$1.68 = 5.595%

Dividend Yield

Property Yield = Annualised Rental Income/ Capital Value

Property Yield

???

Correlation

S-REITs (Commercial)

REIT Name Dividend Gross Yield

(1 Mar 16)

Property Yield

CapitaCommercial Trust 6.21%

?

Fraser Commercial Trust 7.62%

K-REIT 6.56%

Mapletree Commercial Trust 7.86%

OUE Commercial REIT 7.44%

S-REITs (Retail)

REIT Name Dividend Gross Yield

(1 Mar 16)

Property Yield

CapitalMall Trust 5.51%

?

Frasers Centrepoint Trust 5.96%

SPH REIT 5.79%

Starhill Global REIT 6.77%

Suntec REIT 6.18%

S-REITs (Industrial)

REIT Name Dividend Gross Yield

(1 Mar 16)

Property Yield

AIMsAmp Cap REIT 8.31%

?

Ascendas 6.10%

Cache Log Trust 9.54%

Cambridge Ind Trust 8.39%

Keppel DC REIT 6.156%

Mapletree Ind Trust 7.09%

Mapletree Log Trust 7.24%

Sabana REIT 8.63%

SoilbuildBiz REIT 8.83%

Viva Ind Trust 9.35%

S-REITs (Hotel & Service Apt)

REIT Name Dividend Gross Yield

(1 Mar 16)

Property Yield

Ascendas H-Trust 8.47%

?

Ascott REIT 7.23%

CDL Hospitality Trust 7.10%

Far East Hospitality Trust 7.43%

OUE HTrust 7.24%

S-REITs (Hospital)

REIT Name Dividend Gross Yield

(1 Mar 16)

Property Yield

First REIT 6.90%

? Parkwaylife REIT 4.92%

Why Dividend Yield is higher than Property Yield ?

Yield Accretive

Low Interest Environment

Investor Hungry of Deals

Valuation of REIT’s Property

Valuation Reconciliation

Average or Weighted Average

Depends on :-

Type of Property

Availability

of Sales

Comparable

Reasonableness

Valuation Report

1. Introduction

2. Property Particulars

3. Title Particulars

4. Town Planning

5. Location

6. Subject Property

7. Occupancy/ Tenancy Details

8. Operating Expenses

9. Property Market Commentary

10. SWOT Analysis

11. Valuation Methodology

12. Reconciliation of Value

13. Valuation

14. Appendix

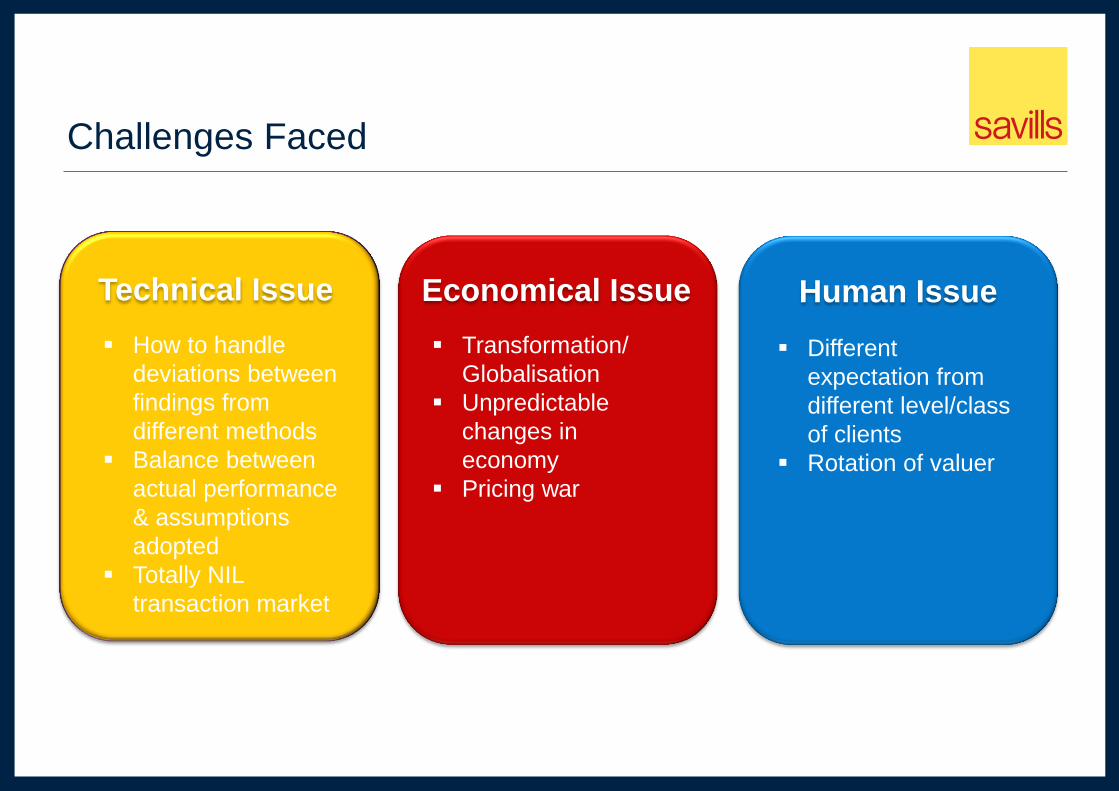

Challenges Faced

Technical Issue Economical Issue Human Issue

How to handle

deviations between

findings from

different methods

Balance between

actual performance

& assumptions

adopted

Totally NIL

transaction market

Transformation/

Globalisation

Unpredictable

changes in

economy

Pricing war

Different

expectation from

different level/class

of clients

Rotation of valuer

Thoughts For The Day

Current Practice Sustainable?

• International standard

• Will X-Valuation take over convention valuation?

Is Valuation Just DCF??

• Skill ability

Valuer’s Role

• Continual professional development

• Ready for change

Advice that gives Advantage.