Uttam Galva Steels Limited - Sify.comim.sify.com/sifycmsimg/jan2010/Finance/14926454_Ut... · Uttam...

16

Uttam Galva Steels Limited BUY Target Price:133.00 CMP: Rs.119.25. Market Cap: Rs.14292.11mn. Date: 6 Jan,2010. Key Ratios: Particulars FY08 A FY09 A FY10E FY11E OPM(%) 10 8 10 10 NPM(%) 4 2 3 3 ROE(%) 17 12 14 15 ROCE(%) 14 12 13 13 P/BV(x) 0.60 1.09 1.49 1.27 P/E(x) 3.45 8.97 10.96 8.60 EV/EBDITA(x) 2.96 3.72 3.69 3.36 Debt Equity(x) 1.48 1.71 1.59 1.46 Key Data: Sector Steel Face Value 10.00 52 wk. High/Low (Rs.) 142.00/25.30 Volume (2 wk. Avg.) 1.20 BSE Code 513216 SYNOPSIS • We initiated the coverage of Uttam Galva Steels Ltd and set a target price of Rs.133. for medium to long term gains. • Uttam Galva Steels Limited is one of the largest manufacturers of cold rolled steel ("CR") and galvanized steel (GP) in Western India. • The Company is into the business of procuring hot rolled steel ("HR") and processing it into CR and further into GP and Colour Coated Coils. • The Company has expanded and modernized its operations at Khopoli which have increased its cold rolling capacity to 1million MT per annum • The revenue of the company for the quarter ended on Sept 30 th decreased 19% YoY while profit increased 2% YoY. • The topline of the company are expected to grow at a CAGR of 16% over 2008A to 2011E. Share Holding Pattern: V.S.R. Sastry Vice President Equity Research Desk 91-22-25276077 [email protected] Dr. V.V.L.N. Sastry Ph.D. Chief Research Officer [email protected]

Transcript of Uttam Galva Steels Limited - Sify.comim.sify.com/sifycmsimg/jan2010/Finance/14926454_Ut... · Uttam...

Uttam Galva Steels Limited

BUY Target Price:133.00

CMP: Rs.119.25. Market Cap: Rs.14292.11mn.

Date: 6 Jan,2010.

Key Ratios:

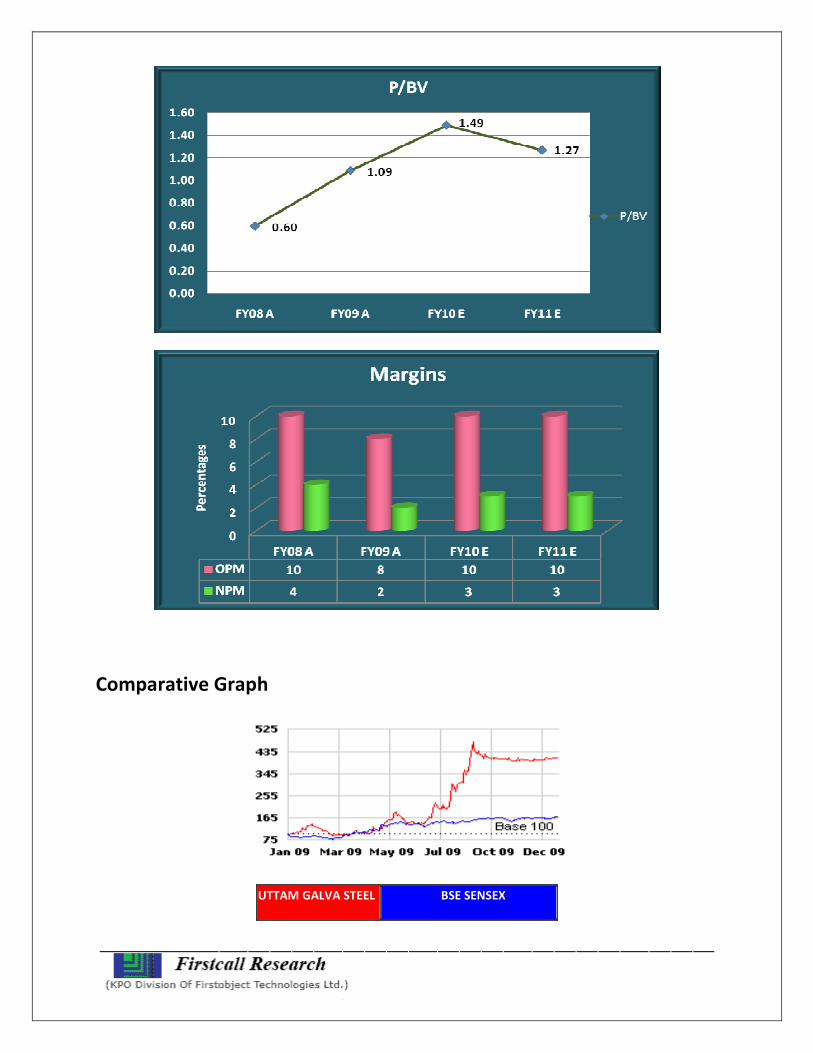

Particulars FY08 A FY09 A FY10E FY11E

OPM(%) 10 8 10 10

NPM(%) 4 2 3 3

ROE(%) 17 12 14 15

ROCE(%) 14 12 13 13

P/BV(x) 0.60 1.09 1.49 1.27

P/E(x) 3.45 8.97 10.96 8.60

EV/EBDITA(x) 2.96 3.72 3.69 3.36

Debt

Equity(x)

1.48 1.71 1.59 1.46

Key Data:

Sector Steel

Face Value 10.00

52 wk. High/Low (Rs.) 142.00/25.30

Volume (2 wk. Avg.) 1.20

BSE Code 513216

SYNOPSIS

• We initiated the coverage of Uttam Galva Steels Ltd

and set a target price of Rs.133. for medium to long

term gains.

• Uttam Galva Steels Limited is one of the largest

manufacturers of cold rolled steel ("CR") and

galvanized steel (GP) in Western India.

• The Company is into the business of procuring hot

rolled steel ("HR") and processing it into CR and

further into GP and Colour Coated Coils.

• The Company has expanded and modernized its

operations at Khopoli which have increased its cold

rolling capacity to 1million MT per annum

• The revenue of the company for the quarter ended

on Sept 30th decreased 19% YoY while profit

increased 2% YoY.

• The topline of the company are expected to grow

at a CAGR of 16% over 2008A to 2011E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

Table of Content

Investment Highlights ................................................................................................................................... 3

Peer Group Comparison ................................................................................................................................ 5

Financials ....................................................................................................................................................... 9

Charts .......................................................................................................................................................... 11

Outlook and Conclusion .............................................................................................................................. 13

Industry Overview ....................................................................................................................................... 13

Investment Highlights

• Results Updates (Q2 FY10)

The bottomline of the company for the quarter increased 2% yoy that is Rs.217.70mn from

Rs.212.60mn of same period of last year. Total revenue for the second quarter stood at

Rs.11025.60mn from Rs.13617.30 which is 19% decreased than that of a year ago period.

EPS for the quarter stood at Rs.1.82 per equity share of Rs.10.00 each.

Expenditure of the company decreased 22% YoY to Rs.9982.10mn from Rs.12748.70mn of

same period of last year. Interest expenses for the quarter stood at Rs.388.4mn. OPM &

NPM for the quarter stood at 9% and 2% respectively.

Quarterly Results - Standalone (Rs in mn)

As at Sep - 09 Sep - 08 %Change

Net Sales 11025.60 13617.30 (19)

Net Profit 217.70 212.60 2

Basic EPS 1.82 1.87

Equity Capital 1198.50 1139.70

• Uttam Galva to rope in Arcelor Mittal as co-promoter

Uttam Galva Steels has announced that the board of the company has approved a co-

promotion agreement amongst the company, Arcelor Mittal Netherlands BV and the

promoters of the company.

Following the development, Arcelor Mittal Netherlands BV, part of the largest steel

producer of the globe -- Arcelor Mittal -- will become a co-promoter of the Miglani family-

promoted steel producer. The agreement contemplates that the Articles of Association

(AoA) of the company would be amended to incorporate the rights and obligations of the

parties in the agreement.

• Uttam Galva gets Bombay HC’s approval for scheme of arrangement

Uttam Galva Steels has received a green signal from the Bombay High Court (HC) for the

scheme of arrangement between Shree Uttam Steel and Power and the company on

August 7, 2009. Apart from this, the HC, Goa Bench has also given its nod for the scheme

on August 17, 2009.

As per the scheme of arrangement, the power division of Shree Uttam Steel and Power will

be demerged into the company. The proposal for the same was approved by the board of

the company in January this year.

• Uttam Galva Bags ‘All India Star Exporter’ Award

Uttam Galva Steels Limited, India’s leading manufacturer - exporter of value added steel,

has bagged it’s 13th consecutive ‘All India Star Exporter’ award for Export Excellence from

the Engineering Export Promotion Council (EEPC), Ministry of Commerce & Industry.

• Uttam Galva hikes product prices by Rs 2000 a tonne

Uttam Galva Steels has decided to hike prices of its galvanized steel products by Rs 2,000

per tonne, effective from August 15. Apart from this, the company is also going to increase

the prices of its cold-rolled products by equal proportion.

The move follows sharp increase in the prices of Zinc, a key input used in the production of

galvanized steel, on the London Metal Exchange (LME) by $400 per tonne to $1,900 level

and scarcity of hot-rolled (HR) coil which is used as a raw material in cold-rolled products.

• Uttam Galva plans for capacity expansion

Uttam Galva Steels is planning to invest Rs 400 crore for boosting its production capacity

and for adding new product mix in the next one year. The investment will be funded

through a mix of internal accruals and debt.

The company is looking at adding value to its existing product mix and doubling the

capacity of its service centre to 40,000 tonne a month. The company’s steel service centre,

located close to its plants in Khopoli, Maharashtra, has a production capacity of 20,000

tonnes presently. It is also setting up a captive power plant having a capacity of 60 MW

near its steel plant for an investment of Rs 300 crore.

Company Profile

Uttam Galva Steels Limited is one of the largest manufacturers of cold rolled steel ("CR") and

galvanized steel (GP) in Western India.

The Company is into the business of procuring hot rolled steel ("HR") and processing it into CR

and further into GP and Colour Coated Coils. In Galvanized coils it specializes in making ultra

thin sheets, which could be as low as 0.13mm thickness. The excess capacity of CR which is not

used for galvanizing is converted to value added grades in Cold Rolled Closed Annealed

("CRCA") coils, cut to length sheets and also sold as Full Hard CR in the overseas markets.

More than 50% of the Company's products are currently exported to over 142 countries

worldwide and it has a customer base in many advanced markets such as Australia , France ,

Germany , Greece , UK and the USA to name a few. In the Indian market, the Company has

established itself as a major player for the supply of CRCA to manufacturers of automobiles,

white goods, general engineering and drums & barrels segment. The Company is also a large

supplier of galvanized coils and sheets to the construction industry.

In domestic market, the company has clientele namely Mahindra & Mahindra, Bajaj Auto, Bajaj

Tempo, Piaggio TATA Motors, Godrej, Daewoo, Anchor, Bharat Heavy Electricals (BHEL), Larsen

& Turbro, Compoton Greaves, Kirloskar Copeland etc.

The Company's manufacturing facilities are located at Khopoli, in the state of Maharashtra,

India, which are close to Nhava Sheva and Mumbai ports. This provides the Company with easy

access to imports of HR coils and also for exporting its products. A close proximity to the ports

gives the Company the advantage of lowering its transportation costs. The Company's domestic

sales are also within the radius of 500 km from its manufacturing facilities to domestic

companies.

The Company has expanded and modernized its operations at Khopoli which have increased its

cold rolling capacity to 1million MT per annum as of March 2009. The Company has also

increased its GP capacity to 750,000 MT per annum as of March 2009. The Company has also

added a new colour coated line (Uttam Spectrum) with a capacity of 90,000 MT per annum as

of March 2009. Due to its high quality products and brand image in the market, the Company

expects that its increased volumes will be easily absorbed into the domestic and export

markets.

The Company now has an entire range of cold rolling Reversible mills i.e. 20-Hi, 6-Hi, 4-Hi and

newly commissioned twin stand 6-Hi mill. It is now in a position to process HR coils of different

grades, thicknesses and widths and is able to meet virtually the entire thickness/width range of

CR/GP/GC coils for various end-use sectors. A significant portion of the Company's CR coils and

GP/GC, coils/sheets are in the higher value added thin gauge segment.

Business Division

With two hundred and fifty acres of land and more than 100 000 sq. meters of covered shed,

Uttam Galva Steel plant is tucked between a hillock and a large lake in the beautiful

surroundings of Western Region of India, near Kohopoli, which is 100 KMs away from the city of

Mumbai, India.

The plant has facility of cold rolling HR coils, with a capacity of 1,000, 000 Tons/Year and

Galvanizing of 750 000 Tons/Year. It does additional value addition of color coating on CR or

Galvanized coils.All these facilities are also supported by a service center, which tailor makes

the coils to customer requirements by slitting & cutting and by delivering sheets/ coils to

customer specifications

• Coil Roll Mill-

This unit includes one 4-hi mill, two 6-hi mills (One Twin Stand) and one 20 Hi mill which

manufactures products having thickness ranging from 0.15mm to 2.5mm and a width up to

1650 mm.

• Galvanising Mills-

Company’s 1650mm Super Galvanising Line is the widest line in India. It manufactures

products having thickness between 0.13mm to 3mm.

• Colour Coating Lines-

Company’s color coating line has installed capacity of 90,000 ton/year.

Products

• CR & CRCA

o The Cutting Edge of Technology

• Galvanizing

o Galvanized Plain Products (GP)

o Galvanized Corrugated Products (GC)

• Color Coated Products

o Prepainted Steel

Peer Group Comparison

Name of the

company

CMP

(As on 6

Jan, 2010)

Market

Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E

(x)

P/BV

(x) Dividend(%)

UTTAM GALVE

STEEL LTD 119.25 14292.11 8.79 13.56

1.09 -

TATA STEEL 641.95 569547.1 40.78 15.74 2.34 160

MONNET ISPAT 390.45 18725.2 43.60 8.96 1.56 50

JINDAL STEEL 723.30 673234.5 13.85 52.22 12.43 550

Key Concerns

• There exists threat with regard to short supply of raw material (mainly due to limited

producers offering raw material) & non-tariff barriers like safe guard duties being

considered to be imposed by Indian Government discouraging import of raw material at

International price levels which is low compared to Domestic prices.

Financials

12 Months Ended Profit & Loss Account (Standalone)

Particulars FY 08 A FY 09 A FY 10 E FY11 E

(Rs.Mn) 12m 12m 12m 12m

Net Sales 31,558.40 43,716.40 44372.15 48809.36

Other Income 21.1 4.3 4.09 4.90

Total Income 31,579.50 43,720.70 44376.23 48814.26

Expenditure -28,549.90 -40,070.80 -40112.4 -43928.42

Operating Profit 3,029.60 3,649.90 4263.81 4885.84

Interest -1,138.80 -1,656.30 -1556.92 -1634.77

Gross Profit 1,890.80 1,993.60 2706.89 3251.07

Depreciation -647.6 -923.7 -1136.2 -1249.8

Profit before Tax 1,243.20 1,069.90 1570.74 2001.30

Tax -4.6 -11.9 -267.0 -340.2

Profit after Tax 1,238.60 1,058.00 1303.71 1661.08

Extraordinary Items - -56.3 - -

Net Profit 1,238.60 1,001.70 1303.71 1661.08

Equity Capital 1,139.70 1,139.70 1,198.50 1,198.50

Reserves 5,955.70 7,099.40 8,403.11 10,064.19

EPS 10.87 8.79 10.88 13.86

Quarterly Ended Profit & Loss Account (Standalone)

Particulars Mar 09 A June 09 A Sep 09 A Dec 09 E

(Rs.Mn) 3m 3m 3m 3m

Net Sales 11,139.10 10,733.30 11,025.60 10694.83

Other Income 1.00 3.3 0.1 0.10

Total Income 11,140.10 10,736.60 11,025.70 10694.93

Expenditure -10,095.10 -9,704.10 -9,982.10 -9682.64

Operating Profit 1,045.00 1,032.50 1,043.60 1012.30

Interest -347.5 -340.2 -388.4 -407.82

Gross Profit 697.50 692.30 655.20 604.48

Depreciation -254.4 -275.8 -277.7 -288.81

Profit before Tax 443.10 416.50 377.50 315.67

Tax 82.8 -70.8 -159.8 -53.66

Profit after Tax 525.90 345.70 217.70 262.01

Extraordinary Items -56.3 - - -

Net Profit 469.60 345.70 217.70 262.01

Equity Capital 1,139.70 1,139.70 1,198.50 1198.50

EPS 4.12 3.03 1.82 2.19

*A=Actual, E=Estimated

Charts

Comparative Graph

UTTAM GALVA STEEL BSE SENSEX

Outlook and Conclusion

• At the current market price of Rs.119.25, the stock trades at a P/E of 10.96x and 8.60x for

FY10E and FY11E respectively.

• On the basis of EV/EBDITA, the stock trades at 3.69x and 3.36x for FY10E and FY11E

respectively.

• Price to Book Value of the stock is expected to be at 1.49 and 1.27 respectively for FY10E and

FY11E.

• The Net sales of the company are expected to grow at a CAGR of 16% over 2008 to 2011E.

• Uttam Galva Steels is planning to invest Rs 400 crore for boosting its production capacity and

for adding new product mix in the next one year. The investment will be funded through a

mix of internal accruals and debt.

• We expect that the company will keep its growth story in the coming quarters also. We

recommend ‘BUY’ in this particular scrip with a target price of Rs.133.00. for Medium to

Long Term Gains.

Industry Overview

The Indian steel industry entered into a new development stage from 2005–06, resulting in

India becoming the 5th largest producer of steel globally. Producing about 55 million tonnes

(MT) of steel a year, today India accounts for a little over 7 per cent of the world's total

production.

India is the only country across the world to post a positive overall growth in crude steel

production at 1.01 per cent for the January-March period of 2009. The recovery in steel

production has been aided by the improved sales performance of steel companies. The steel

sector grew by 5.3 per cent in May 2009.

Significantly, state-owned steel maker, Steel Authority of India (SAIL), which reported a net

profit of US$ 571 million in January-June 2009, has become the most profitable steel company

globally, beating steel majors such as ArcelorMittal, Posco, Bao Steel and Nippon in the half

yearly profits.

Production

Steel production reached 28.49 million tonne (MT) in April-September 2009. Further, India,

which recorded production of 22.14 MT of steel during April-August 2009, is likely to emerge as

the world's third largest steel producer in the current year, according to Goutam Kumar Basak,

Executive Secretary, Joint Plant Committee (JPC).

The National Steel Policy has a target for taking steel production up to 110 MT by 2019–20.

Nonetheless, with the current rate of ongoing greenfield and brownfield projects, the Ministry

of Steel has projected India's steel capacity is expected to touch 124.06 MT by 2011–12. In fact,

based on the status of memoranda of understanding (MoUs) signed by the private producers

with the various state governments, India's steel capacity is likely to be 293 MT by 2020.

Consumption

India accounts for around 5 per cent of the global steel consumption. Almost 70 per cent of the

total steel used is for kitchenware. However, its use in railway coaches, wagons, airports, hotels

and retail stores is growing immensely.

India's steel consumption rose by 5.7 per cent to 26.49 MT in the first six months of the current

fiscal over the same period a year ago on account of improved demand from sectors like

automobile and consumer durables.

A Credit Suisse Group study states that India's steel consumption will continue to grow by 16

per cent annually till 2012, fuelled by demand for construction projects worth US$ 1 trillion.

The scope for raising the total consumption of steel is huge, given that per capita steel

consumption is only 35 kg – compared to 150 kg across the world and 250 kg in China.

Steel players like JSW Steel and Essar Steel are increasing their focus on opening up more retail

outlets pan India with growth in domestic demand. JSW Steel currently has 50 such steel retail

outlets called JSW Shoppe and is targetting to increase it to 200 by March 2010. They expect at

least 10-15 per cent of their total production to be sold by their retail outlets.

Essar Steel which currently has over 300 retail outlets across the country, plans to set up 5,000

outlets of various formats soon. It expects to sell 3MT of steel through the retail route in two

years.

Exports

Out of India's annual iron ore production of more than 200 MT, about 50 per cent is exported.

Iron ore exports increased 17 per cent to 12.6 MT in February 2009 from 10.8 MT in the same

month a year ago, owing to a moderate revival in demand from Chinese steel producers, as per

the latest data compiled by a group of top Indian mining firms.

Earlier, according to a study, with the rise in demand for steel in China, India's iron ore exports

went up by 38 per cent to reach 13.6 MT in December 2008 against 9.8 MT in December 2007.

Around 50-60 per cent of India’s iron ore is exported to China.

____________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but we do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking & Financial Services

B. Prathap IT

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods; Real & Infra

D.Asha Kiran Kumar Auto

E. Swethalatha Oil & Gas

A.Rajesh FMCG

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,TakeoverOffers, Offer for Sale and Buy

Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,Placement of Equity / Debt with

multilateral organizations, Short Term Funds Management Debt & Equity, Working Capital Limits, Equity &

DebtSyndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and cross-border), divestitures, spin-offs,

valuation of business, corporate restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising of capital through FCCBs, GDRs,

ADRs and listing of the same on International Stock Exchanges namely AIMs, Luxembourg, Singapore Stock

Exchanges and other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com