Using Credit. Terms to know Credit Creditor Revolving Charge Account Installment Account Vehicle...

25

Using Credit

-

Upload

robert-perry -

Category

Documents

-

view

222 -

download

0

Transcript of Using Credit. Terms to know Credit Creditor Revolving Charge Account Installment Account Vehicle...

Using Credit

Terms to know

• Credit• Creditor• Revolving Charge

Account• Installment Account• Vehicle leasing• Cash loan• Collateral• Cosigner

• Home equity loan• Equity• Credit rating• Credit bureau• Credit agreement• Finance charges• Interest• Annual percentage rate

(APR)• Grace period• Bankruptcy

Understanding Credit

• Credit: allows you to buy goods and services now and pay for them later.

• Credit is based on trust between the creditor and you

Understanding Credit

• Creditor: may be a business or a person who gives you goods or services and expects you to pay later.

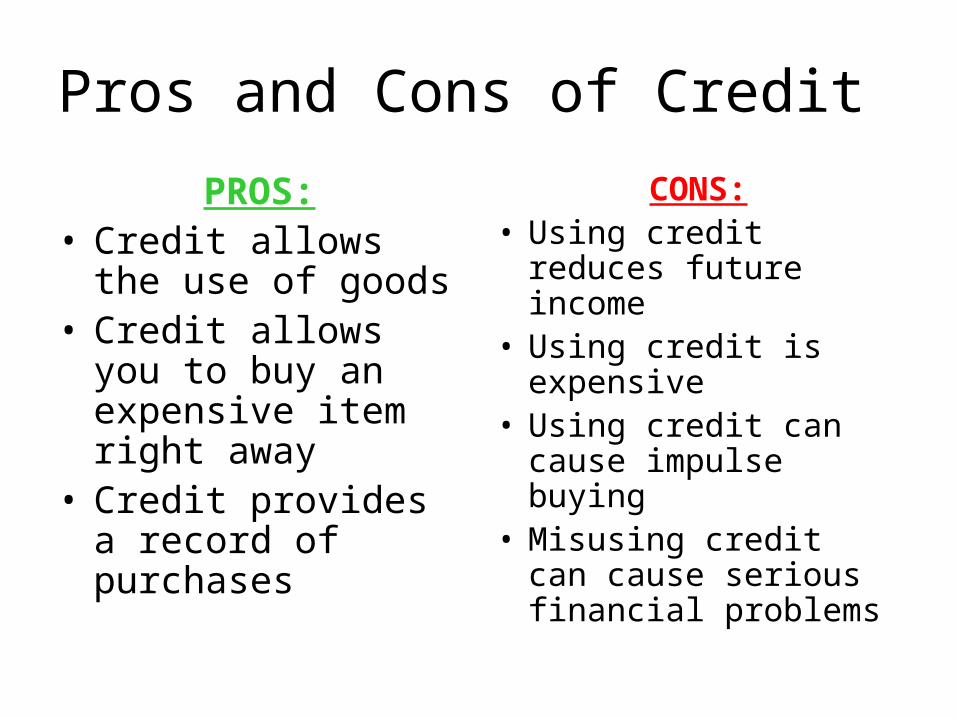

Pros and Cons of Credit

PROS:• Credit allows the use

of goods• Credit allows you to

buy an expensive item right away

• Credit provides a record of purchases

CONS:• Using credit reduces

future income• Using credit is

expensive• Using credit can

cause impulse buying• Misusing credit can

cause serious financial problems

Types of Credit

• Credit card accounts

• Charge accounts

• Installment accounts

• Vehicle leasing

• Cash loans

• Home equity loans

Credit Card

• Many department stores (Sears, Macys, etc) and companies (Amex, Chase, Capital 1) give credit cards so consumers (you) can use credit to buy their goods and services.

Credit Card

• The cost of using a credit card is often high!• Most bank card companies charge and annual fee (a fee

each year)• Interest on credit cards can be high as well

Credit Card

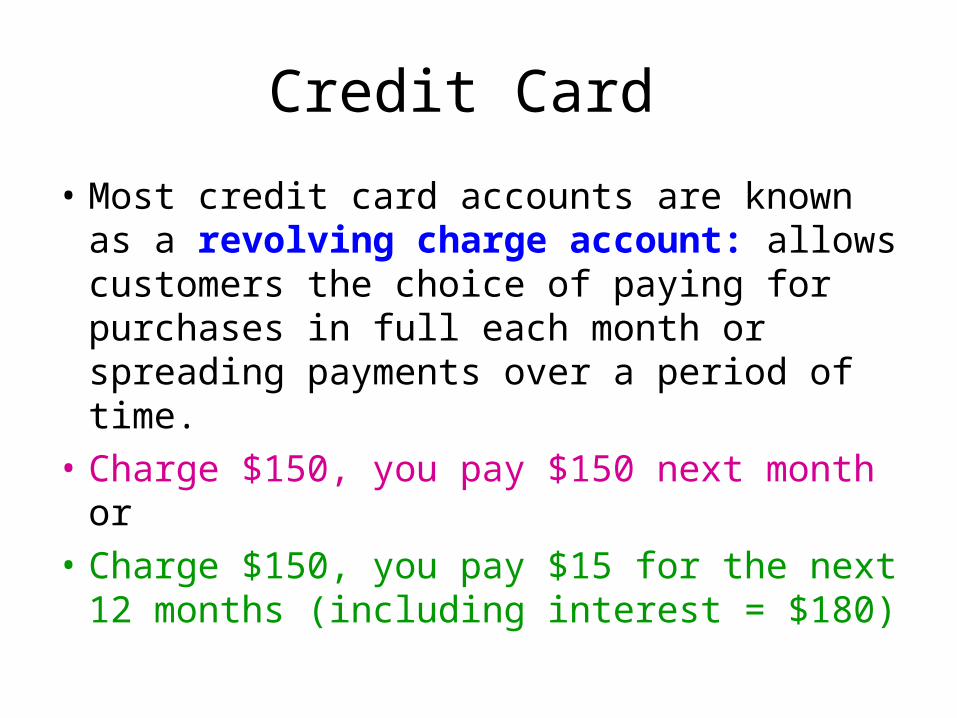

• Most credit card accounts are known as a revolving charge account: allows customers the choice of paying for purchases in full each month or spreading payments over a period of time.

• Charge $150, you pay $150 next month or

• Charge $150, you pay $15 for the next 12 months (including interest = $180)

Types of Credit

• Some businesses allow customers to charge goods and services on a charge account.

• An installment account is often used to charge expensive items like a major appliance or furniture. Usually the customer puts down a cash payment & pays the rest monthly for a set schedule.

Types of Credit

• Vehicle Leasing: a credit transaction by which a person rents a car according to certain restrictions

• Must put down a down payment

• Held to same standards as buying a car

Types of Credit

• Cash loans: If you need $$$ to buy something, you get a loan on credit & it must be repaid

• Banks, Savings & loans associations, Credit Unions, Loan companies and some life insurance companies.

Types of Credit

• To get most cash loans, a borrower is required to pledge collateral.

• Collateral: is something of value held by the creditor in case you are unable to repay the loan

Type of Credit

• Although a person may have nothing to pledge as collateral, getting a loan is still possible.

• A cosigner: is a responsible person who signs a loan agreement with the borrower

Types of Credit

• Home equity loan: type of loan that provides automatic access to a sum of money separate from the amount the homeowner borrowed to purchase the house.

• Equity: is determined by subtracting how much is owed on a house from the amt the house is worth

Types of Credit

• For example, if you house is worth $90,000 and you still owe $70,000, the amount of equity in your home is $20,000.

• With excellent credit, you may borrow this amount of money off of your home for whatever you may need

Establishing Credit

• When you first try to establish credit, you may have a hard time.

• You will have to begin by completing credit applications to establish a credit rating.

• Credit rating: the creditor’s evaluation of a person’s willingness and ability to pay debts.

Establishing Credit

• In evaluating a credit rating, creditors look for a person who is a good credit risk, that is people who will pay their bills!

Establishing Credit

• Making regular, on-time payments on credit purchases, loans, or fixed expenses such as rent, utilities

• Owning a car, home, stocks, or bonds

• Living in the same community for a period of time.

Building your credit rating

• Get a job and stay employed

• Open a checking account

• Open a savings account

• Buy an item on a layaway plan

• Apply to a gasoline company or a local store for a credit card

What’s in a credit record?

• Once you use credit, you automatically establish a credit record at a local or national credit reporting agency

• Credit Bureau: an agency that collects and keeps files of financial information on individual consumers

• Transunion, Equifax and Experian

What’s in a credit record?

• Information on your credit record (report) shows only the facts collected by the credit bureau

• You have the right to check your credit record and the right to dispute any credit misunderstandings

• Generally, negative information stays in the report for 7 years

Credit Ratings

Credit Report

Q & A

• What types of credit are available to consumers?

• Why is it important to establish credit?

• How do creditors use credit bureaus?

• How can a person maintain a good credit rating?

• What should a person do when a credit bill cannot be paid?