U.S. Solar Market Insight: Q4 2016 · 2018-2020 Booms: New York and Maryland ... pilot programs ......

24

U.S. Solar Market Insight: Q4 2016 State and Future of U.S. Solar Markets Austin Perea Solar Analyst [email protected] 12/14/2016

Transcript of U.S. Solar Market Insight: Q4 2016 · 2018-2020 Booms: New York and Maryland ... pilot programs ......

U.S. Solar Market Insight: Q4 2016

State and Future of U.S. Solar Markets

Austin Perea

Solar Analyst

12/14/2016

1Perea - US Solar Market Insight: Q4 2016

Contents

1. National Overview and Key Market Drivers #

2. Residential PV #

3. Non-Residential PV #

4. Utility PV #

Perea - US Solar Market Insight: Q4 2016

National Overview & Key Market Drivers1.

3Perea - US Solar Market Insight: Q4 2016

Q3 2016 – The Largest Quarter for Solar PV

479

795

546

822690

1,314

747

941 964

2,110

1,3641,287

1,395

2,205

1,3461,436 1,425

3,295

2,0032,079

4,143

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Inst

alla

tio

ns

(MW

dc)

Residential Non-Residential Utility

Q3 2016: 4,143 MWdc installed

Q1-Q3 2016: 8,225 MWdc installed

Utility PV: 3,174 MWdc

• ~75% of total PV capacity installed in Q3 2016;

~65% of total PV installed in 2016 to-date

• Contracted utility PV pipeline currently totals

19.9 GWdc

Non-Residential PV: 311 MWdc

• Up 15% from Q2 2016

• Up 37% over Q3 2015

Residential PV: 593 MWdc

• Down 10% over Q2 2016

• Up 2% over Q3 2015

Perea - US Solar Market Insight: Q4 2016

Market Segment Breakdown: Residential PV

2016: The Year of Major Market Slowdown?

2.

5Perea - US Solar Market Insight: Q4 2016

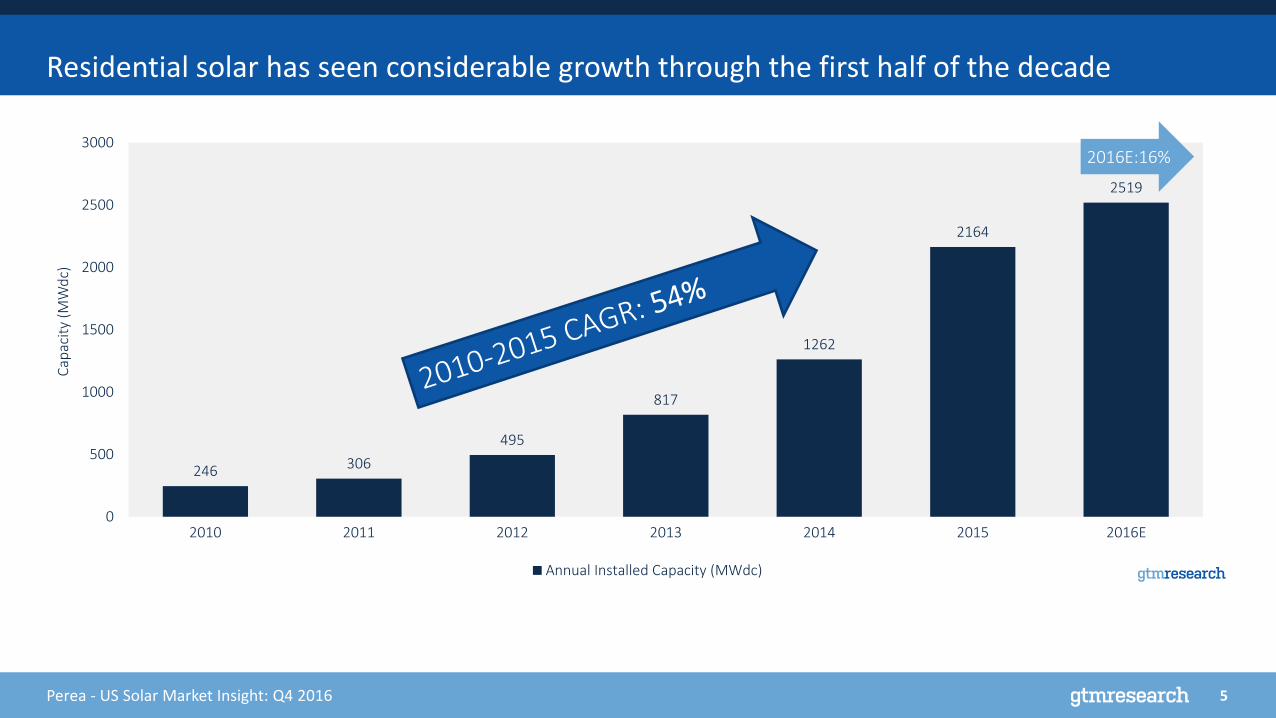

Residential solar has seen considerable growth through the first half of the decade

246 306

495

817

1262

2164

2519

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013 2014 2015 2016E

Cap

acit

y (M

Wd

c)

Annual Installed Capacity (MWdc)

2016E:16%

6Perea - US Solar Market Insight: Q4 2016

Residential PV continues to be a geographically consolidated market

California’s lowest share of residential market since 2012

76%

-7%

346%

36%59%

69%

283%

5%

211%

-15%-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016

Year

-ove

r-Ye

ar %

Gro

wth

Top 5 Residential State Markets Q1 2015-Q3 2016

California New York New JerseyMaryland Massachusetts

42%

9%7%

6%

6%

30%

Q3 2016 State Market Shares

California

New York

New Jersey

Maryland

Massachusetts

All Other States

7Perea - US Solar Market Insight: Q4 2016

Major market growth increasingly inhibited by customer fatigue

and market saturation

• Protracted lead generation timelines

• Higher customer acquisition costs

• Declining lead conversation ratios

Longer sales cycles leading to slower growth among California and other key

markets

Additionally, NEM reform and rate design continues to present

near- and long-term risk to DG economics

Emerging market most risk most pronounced

• Nevada: Rollback to NEM has cratered promising top ten market in 2016

• Utah: Utility has proposed new discriminatory solar rate class

• Arizona: Peak demand charge has potential to slash savings in 2017

• California: Transition to NEM 2.0 complicates sales process for installers

Customer fatigue and ongoing NEM & rate design battles remain hurdles for residential PV

National Level Trends for Residential Solar

Source: GTM Research/SEIA, Q3 2016 U.S. Solar Market Insight

California Residential Growth % vs. Customer Penetration

89%97%

153%

68%

52%

28%

76%

62%67%

56%

23% 19%

2%

3%

4%

7%

8%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Share o

f Ro

ofto

p P

V A

dd

ressable M

arket with

Solar

Installed

Year

-ove

r-Ye

ar %

Gro

wth

CA: Growth (%) CA: Customer Penetration (%)

8Perea - US Solar Market Insight: Q4 2016

Emerging markets will partially offset major market decline

72%

28%

2015Top Five Market Share

Rest of Market 62%

38%

2021ETop Five Market Share

Rest of Market

No state-level net metering policy – state growth primarily supported by utility-level rebates

◦ With utilities offering robust incentives the state has recently become top ten market

◦ Austin Energy VOST continues to attract national installers

20% aggregate NEM cap, retail-rate NEM but looming tax credit expiration and NEM uncertainty pose risk

◦ In-state tax credit has fueled growth in H1 2016 with 12,000 applications in 2016 vs. 3,000 in 2015

◦ 20+ MW installed in Q3 and could see significant demand pull-in from customers trying to qualify for the tax credit and

grandfathered retail-rate NEM

9Perea - US Solar Market Insight: Q4 2016

Near Term: Growth to continue, though at slower rates than expected

• Despite NEM policy certainty across most major state markets, deceleration is expected

to continue

• That said, major markets will continue to account for a large share of reduced growth

with occasional demand pull-in and emerging market growth also contributing

Long Term: Demand diversification to accelerate via Federal ITC Extension

• Policy certainty in major state markets will provide strong baseline growth for residential

PV though rate of growth will be slower than in previous years

• Demand diffusion will continue, as secondary state markets are already surpassing

growth rates of major states and are poised to assume a larger share of the market

• Growth will depend on the extent to which installers can adapt to evolving customer

acquisition landscape and tap in to new customer demographics

U.S. Residential Solar Market Outlook

Source: GTM Research/SEIA, Q4 2016 U.S. Solar Market Insight

Annual Residential PV Installation Forecast: 2010-2021E Near Term (2017) and Long Term (2018-2021) Market Outlook

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E

Res

iden

tial

PV

Inst

alla

tio

ns

(MW

dc)

Perea - US Solar Market Insight: Q4 2016

Market Segment Breakdown: Non-Residential PV

The Little Sector That Could

3.

11Perea - US Solar Market Insight: Q4 2016

2016 installations poised to benefit from:

Community solar pipeline realization

• Upside stems from nearly 300 MW of community

solar projects in development

California demand pull-in

• Solar-friendly rate design

• Customer continue to leverage NEM-Agg

Non-residential PV expected to experience

reboot

Traditional C&I still struggling

• Rate design still matters

• Declining incentive environment

• Lack of credit-worthy offtakers

• NEM cap and structure uncertainty

Non-Residential PV Overview – Where’s the upside?

0

200

400

600

800

1000

1200

1400

1600

2010 2011 2012 2013 2014 2015 2016E

Cap

acit

y (M

Wd

c)

Non-Residential 2010-2016E

12Perea - US Solar Market Insight: Q4 2016

• 2016 Outlook: Pent up demand unrealized due to…

◦ 12+ month regulatory and legislative debates over

– Interconnection cost upgrades

– NEM capacity limits

– Successor bill credit methodologies in lieu of full retail rate

• 3rd party led: Boom and bust cycles to yield flat demand ranging

between 300 – 400 MW per year beginning in 2017

◦ 2017-2018 Booms: Massachusetts and Minnesota

◦ 2018-2020 Booms: New York and Maryland

• Utility led: Majority of announced programs are 1 MW+, signaling

market’s beginning to mature beyond smaller scale, single project

pilot programs

Realizing the promise of community solar

0

100

200

300

400

500

600

An

nu

al In

stal

lati

on

s (M

Wd

c)

Utility Led Total CS Installations (MWdc)Source: GTM Research

13Perea - US Solar Market Insight: Q4 2016

California accounted for 52% of the non-residential market in

Q3 – it’s highest share of the commercial market ever

Solar-friendly tariffs such as SCE’s Option R and PG&E’s A-6 are

made up by higher portion of volumetric charges, which solar is

directly able to offset

• SCE’s Option R Tariff: 150 MW remaining in program

• PG&E’s A-6: CPUC delayed closure for medium-size customers

until March 31, 2017

No system size limitations under NEM 2.0 to fuel 1+

MW development

• NEM-A customers to benefit from higher system sizes

California’s solar-friendly rate design and NEM 2.0 transition fueling commercial market

Average Commercial Solar Export Rates in CA: Default

Tariff vs. Option R in SCE and PG&ECalifornia’s largest non-residential quarter ever?

0%

10%

20%

30%

40%

-

5

10

15

20

25

30

35

Q1-2014 Q3-2014 Q1-2015 Q3-2015 Q1-2016 Q3-2016

% N

on

-Resid

ential M

arket

Cap

acit

y (M

Wd

c) NEM-Agg Capacity

NEM-Agg Installed Capacity

NEM-Agg % Non-Residential Market Share

14Perea - US Solar Market Insight: Q4 2016

Near Term: Demand Fueled by Large Scale (1 MW+) Development

2017-2018: A gradual rebound is expected via:

• Pent-up third-party community solar demand in MA, MN, and CO and nearly 100 MWdc

of utility-led community solar

• Strong CA demand via solar-friendly rates and 1 MW+ development as NEM 2.0

transition begins

• NEM cap relief in MA, though SREC successor program rollout delay risks pushing out

greenfield origination opportunities

Long Term: Saved By the Federal ITC Extension (Especially Small Commercial)

• Long term growth will increasingly stem from the sub 1 MW non-residential PV market,

as third party financing solutions expand into the small and medium sized commercial

customer bases.

• As the effects of revised virtual NEM rules are felt in the Northeast, customer sited

development and increasingly solar + storage will play a larger role in long term growth.

◦ The exception to that trend is community solar, which remains a long term incentive-

funded growth opportunity for offsite commercial development.

U.S. Non-Residential Solar Market Outlook

Source: GTM Research/SEIA, Q3 2016 U.S. Solar Market Insight

Annual Non-Residential PV Installation Forecast: 2010-2021E Near Term (2017-2018) and Long Term (2018-2021) Market Outlook

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E

No

n-R

esid

enti

al P

V In

stal

lati

on

s (M

Wd

c)

Perea - US Solar Market Insight: Q4 2016

Market Segment Breakdown: Utility PV

Non-RPS procurement becomes largest driver of utility PV demand

4.

16Perea - US Solar Market Insight: Q4 2016

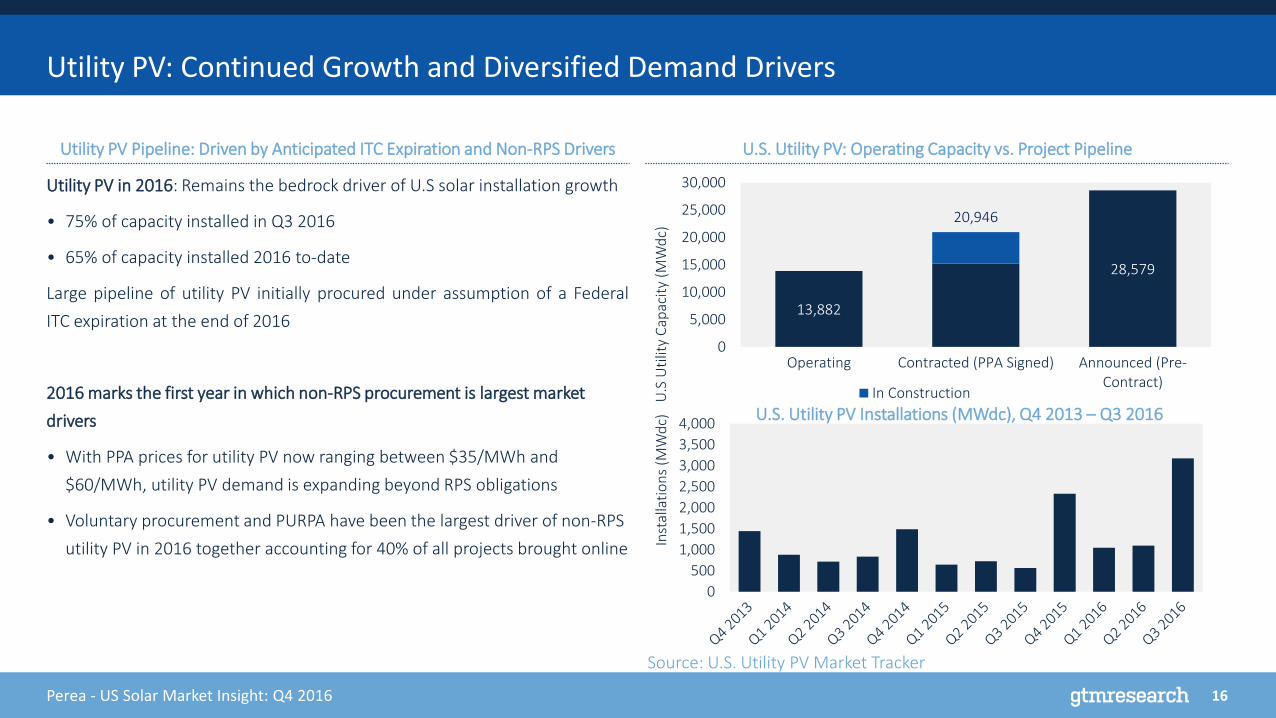

13,882

28,579

20,946

0

5,000

10,000

15,000

20,000

25,000

30,000

Operating Contracted (PPA Signed) Announced (Pre-Contract)

U.S

Uti

lity

Cap

acit

y (M

Wd

c)

In Construction

Utility PV in 2016: Remains the bedrock driver of U.S solar installation growth

• 75% of capacity installed in Q3 2016

• 65% of capacity installed 2016 to-date

Large pipeline of utility PV initially procured under assumption of a Federal

ITC expiration at the end of 2016

2016 marks the first year in which non-RPS procurement is largest market

drivers

• With PPA prices for utility PV now ranging between $35/MWh and

$60/MWh, utility PV demand is expanding beyond RPS obligations

• Voluntary procurement and PURPA have been the largest driver of non-RPS

utility PV in 2016 together accounting for 40% of all projects brought online

Utility PV: Continued Growth and Diversified Demand Drivers

Utility PV Pipeline: Driven by Anticipated ITC Expiration and Non-RPS Drivers

Source: U.S. Utility PV Market Tracker

U.S. Utility PV: Operating Capacity vs. Project Pipeline

U.S. Utility PV Installations (MWdc), Q4 2013 – Q3 2016

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Inst

alla

tio

ns

(MW

dc)

17Perea - US Solar Market Insight: Q4 2016

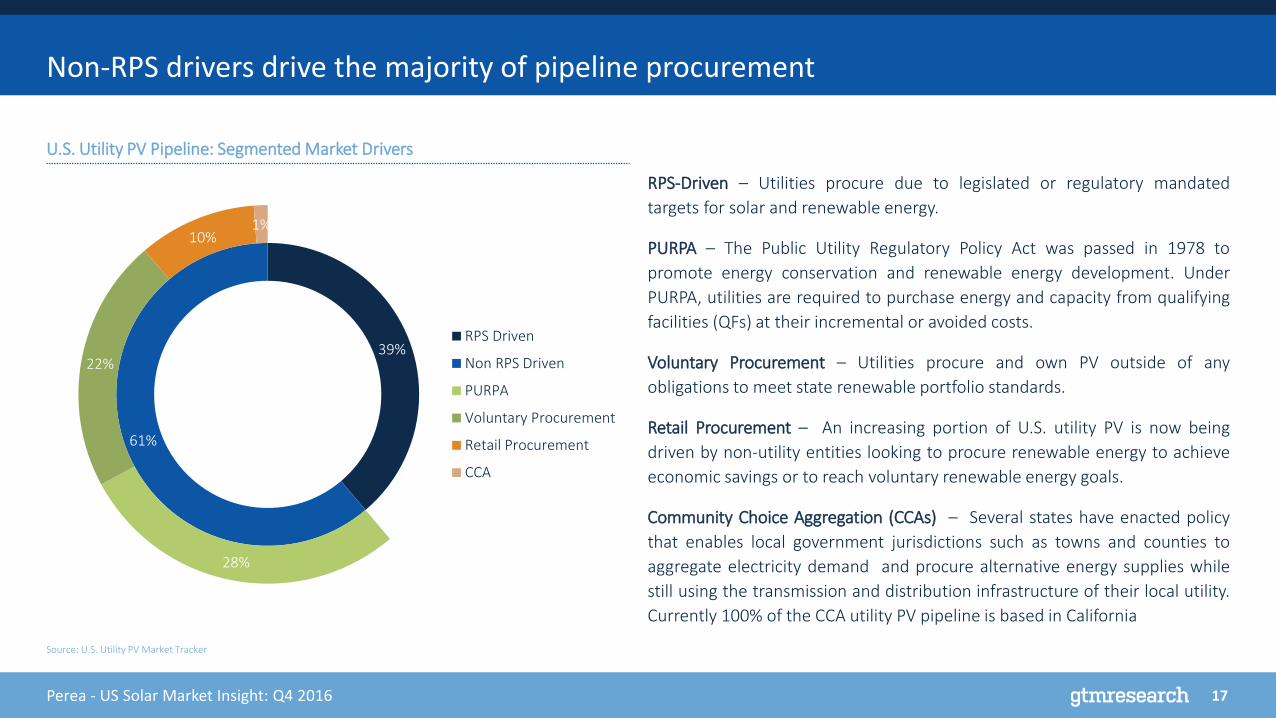

Non-RPS drivers drive the majority of pipeline procurement

RPS-Driven – Utilities procure due to legislated or regulatory mandated

targets for solar and renewable energy.

PURPA – The Public Utility Regulatory Policy Act was passed in 1978 to

promote energy conservation and renewable energy development. Under

PURPA, utilities are required to purchase energy and capacity from qualifying

facilities (QFs) at their incremental or avoided costs.

Voluntary Procurement – Utilities procure and own PV outside of any

obligations to meet state renewable portfolio standards.

Retail Procurement – An increasing portion of U.S. utility PV is now being

driven by non-utility entities looking to procure renewable energy to achieve

economic savings or to reach voluntary renewable energy goals.

Community Choice Aggregation (CCAs) – Several states have enacted policy

that enables local government jurisdictions such as towns and counties to

aggregate electricity demand and procure alternative energy supplies while

still using the transmission and distribution infrastructure of their local utility.

Currently 100% of the CCA utility PV pipeline is based in California

Source: U.S. Utility PV Market Tracker

U.S. Utility PV Pipeline: Segmented Market Drivers

39%

61%

39%

28%

22%

10%1%

RPS Driven

Non RPS Driven

PURPA

Voluntary Procurement

Retail Procurement

CCA

18Perea - US Solar Market Insight: Q4 2016

• While renewable portfolio standards

will continue to drive a significant

volume of new utility PV capacity,

non-RPS drivers will spur the majority

of new solar development for the

next several years

• In 2017, PURPA driven projects in NC,

OR, and other states will represent

the single largest driver of new

capacity additions

• Pacific Gas & Electric and Southern

California Edison account for the

biggest decline in demand for RPS

driven utility PV. In 2015 and 2016,

the two utilities accounted for 52% of

all RPS driven demand in the US and

are not facing net shorts in RPS

demand until 2021 or later

RPS Steps Down as the Primary Driver of Utility PV

Source: U.S. Utility PV Market Tracker

Percent Share of Annual Installed Capacity by Primary Utility PV Driver

83% 85%

56%49%

39%

8% 5%

14%23%

21%

9%10%

23% 17%28%

5%10% 9%

1% 1% 1% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016 In Development

% C

apac

ity

of

Uti

lity

PV

Pri

mar

y D

rive

rs

RPS Voluntary Procurement PURPA Retail Procurement CCA

19Perea - US Solar Market Insight: Q4 2016

States With >50 MW Contracted, Non RPS Utility PV Pipeline as of Nov 2016

MT

WY

ID

WA

OR

NV

UTCA

AZ

ND

SD

NE

CO

NM

TX

OK

KS

AR

LA

MO

IA

MN

WI

IL IN

KY

TN

MS AL GA

FL

SC

NC

VAWV

OH

MI

NY

PA

MD

DE

NJ

CTRI

MA

ME

VT

NH

Non RPS Drivers

Voluntary

Procurement

PURPA

Wholesale

Retail

Procurement

CCAs

MD

20Perea - US Solar Market Insight: Q4 2016

• The top 5 states (NC, TX, OR, SC, UT)

represent 58% of non-RPS utility scale

solar in development.

• PURPA: Duke Energy is seeking approval

from the NC-Utility Commission to make

developers competitively bid to develop

PURPA projects and limit PURPA growth.

• Voluntary Procurement: 92% is

concentrated in the southeast, primarily in

states with no RPS.

• Retail Procurement: With direct access

legislation in place, CA represents 36% of

retail procurement. NV represents another

20%. Retail procurement has grown rapidly

in VA and several developers have

announced they are looking for corporate

offtakers in VA or PJM territory.

Top States for All non-RPS Projects

Source: U.S. Utility PV Market Tracker

Top State Markets for Utility PV Projects Outside of RPS Obligations in Development

0

500

1000

1500

2000

2500

NC TX OR SC UT CA GA VA FL NV MT AZ IN MS MD AllOther

U.S

. Uti

lity

PV

Cap

acit

y (M

Wd

c)

Voluntary Procurement PURPA Wholesale Retail Procurement CCA

21Perea - US Solar Market Insight: Q4 2016

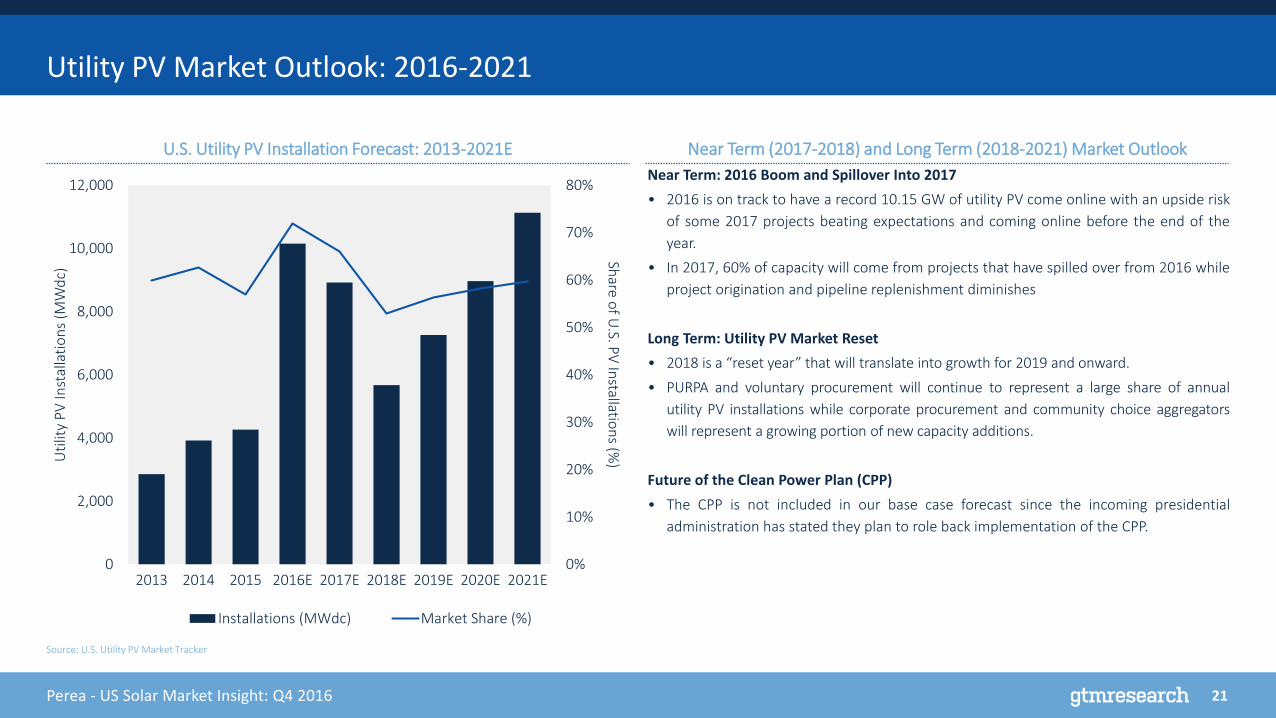

Near Term: 2016 Boom and Spillover Into 2017

• 2016 is on track to have a record 10.15 GW of utility PV come online with an upside risk

of some 2017 projects beating expectations and coming online before the end of the

year.

• In 2017, 60% of capacity will come from projects that have spilled over from 2016 while

project origination and pipeline replenishment diminishes

Long Term: Utility PV Market Reset

• 2018 is a “reset year” that will translate into growth for 2019 and onward.

• PURPA and voluntary procurement will continue to represent a large share of annual

utility PV installations while corporate procurement and community choice aggregators

will represent a growing portion of new capacity additions.

Future of the Clean Power Plan (CPP)

• The CPP is not included in our base case forecast since the incoming presidential

administration has stated they plan to role back implementation of the CPP.

Utility PV Market Outlook: 2016-2021

Source: U.S. Utility PV Market Tracker

U.S. Utility PV Installation Forecast: 2013-2021E

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

2,000

4,000

6,000

8,000

10,000

12,000

2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E

Share o

f U.S. P

V In

stallation

s (%)U

tilit

y P

V In

stal

lati

on

s (M

Wd

c)

Installations (MWdc) Market Share (%)

Near Term (2017-2018) and Long Term (2018-2021) Market Outlook

Perea - US Solar Market Insight: Q4 2016

Five Things to Keep in Mind in 20175.

23Perea - US Solar Market Insight: Q4 2016

California accounted for 42% of the residential market in Q3 – it’s lowest share since 2012

5 Things to Keep in Mind for 2017

Changes to net metering will continue to be a threat to DG economics in emerging and major states alike

The cost competitiveness of utility PV will continue to drive growth through the remainder of 2016 and

2017 as non-RPS drivers become a larger share of the pipeline

Emerging state markets are seeing unprecedented growth, but we remain cautiously optimistic due to

the susceptibility of incentive markets to boom-and-bust cycles

The future is bright for community solar with 2016 seeing the first signs of project completion - looking

forward we expect a growing portion of non-residential to be driven by community solar

1

2

3

4

5