U.S. Energy Policy: The Burdens of the Past and Moving Forward John P. Banks Nonresident Fellow...

26

U.S. Energy Policy: The Burdens of the Past and Moving Forward John P. Banks Nonresident Fellow Brookings Institution September 25, 2012 BROOKINGS MOUNTAIN WEST - UNLV

-

Upload

scarlett-norton -

Category

Documents

-

view

216 -

download

0

Transcript of U.S. Energy Policy: The Burdens of the Past and Moving Forward John P. Banks Nonresident Fellow...

U.S. Energy Policy: The Burdens of the Past and Moving Forward

John P. BanksNonresident Fellow

Brookings Institution

September 25, 2012

BROOKINGS MOUNTAIN WEST - UNLV

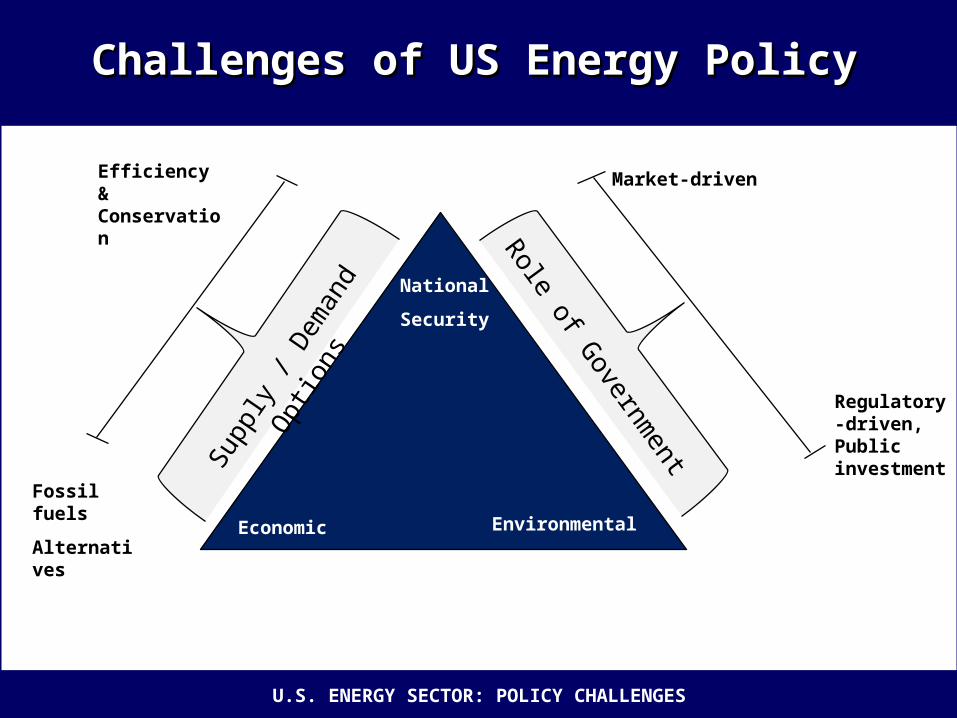

U.S. ENERGY SECTOR: POLICY CHALLENGES

Challenges of US Energy PolicyChallenges of US Energy Policy

National

Security

Environmental Economic

Role of G

overnment

Market-driven

Regulatory-driven, Public investment

Supp

ly /

Dem

and

Opt

ions

Fossil fuels

Alternatives

Efficiency & Conservation

U.S. ENERGY SECTOR: POLICY CHALLENGES

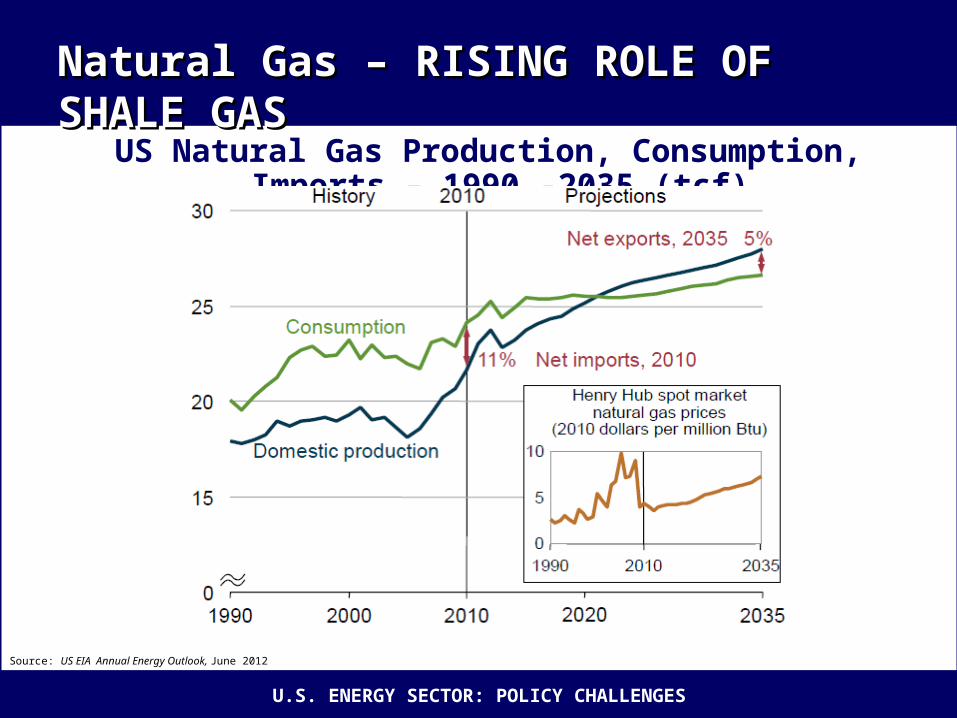

Natural Gas – RISING ROLE OF SHALE GASNatural Gas – RISING ROLE OF SHALE GAS

US Natural Gas Production, Consumption, Imports – 1990 -2035 (tcf)

Source: US EIA Annual Energy Outlook, June 2012

U.S. ENERGY SECTOR: POLICY CHALLENGES

Enormous Shale Gas Resource (USG estimates)Enormous Shale Gas Resource (USG estimates)

Most estimates of total range from 1,800 to 2,500 tcf

US current consumption: total of @ 23 Tcf (or 62 bcf/d)

This has been revised by EIA to 482 tcf

Marcellus from 410 tcf to 141 tcf

U.S. ENERGY SECTOR: POLICY CHALLENGES

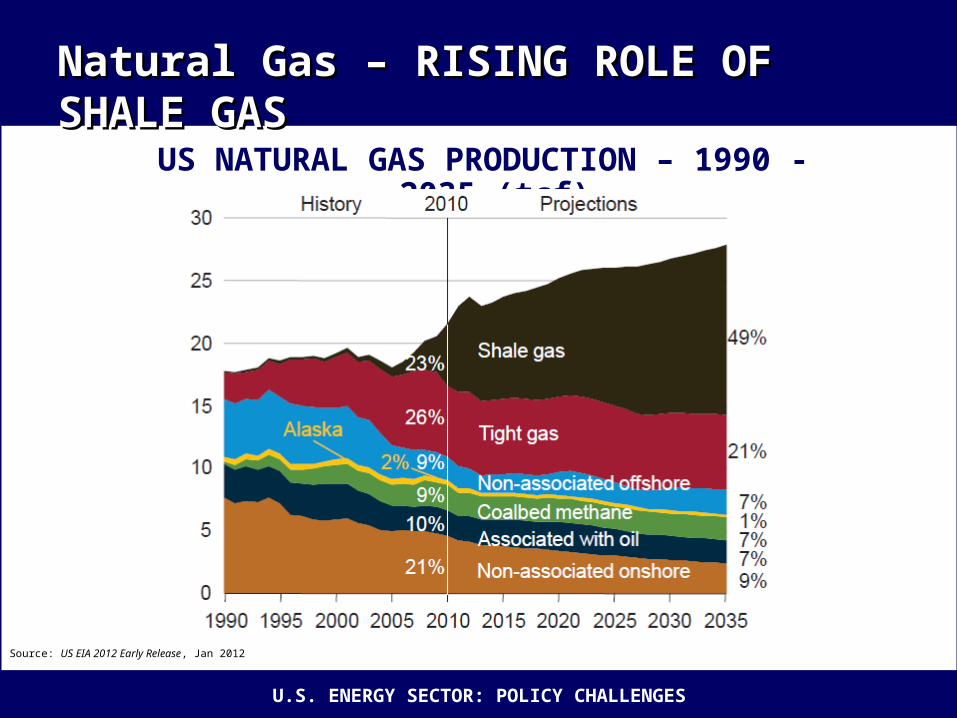

Natural Gas – RISING ROLE OF SHALE GASNatural Gas – RISING ROLE OF SHALE GAS

US NATURAL GAS PRODUCTION – 1990 -2035 (tcf)

Source: US EIA 2012 Early Release, Jan 2012

U.S. ENERGY SECTOR: POLICY CHALLENGES

OIL: US Production Up - Imports DownOIL: US Production Up - Imports Down

Source: US EIA

U.S. ENERGY SECTOR: POLICY CHALLENGES

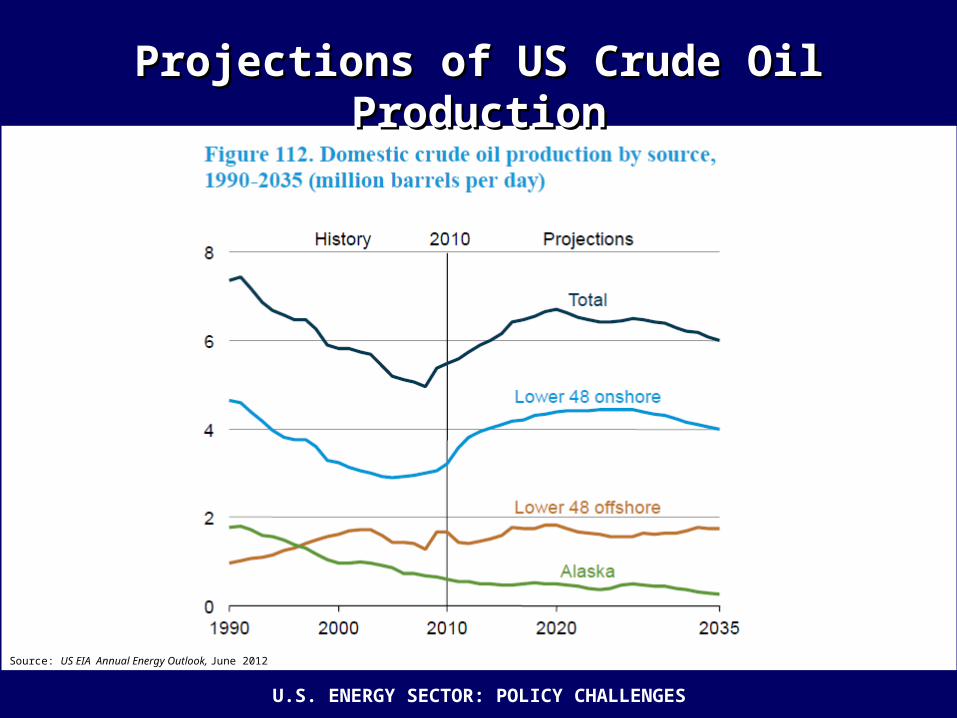

Projections of US Crude Oil ProductionProjections of US Crude Oil Production

Source: US EIA Annual Energy Outlook, June 2012

U.S. ENERGY SECTOR: POLICY CHALLENGES

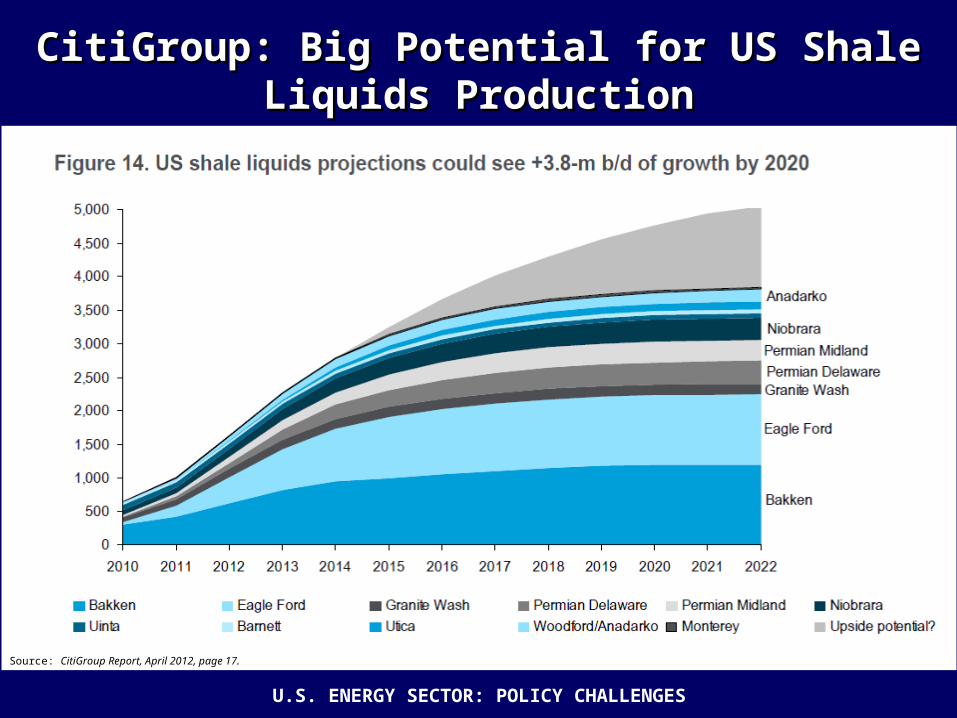

CitiGroup: Big Potential for US Shale Liquids ProductionCitiGroup: Big Potential for US Shale Liquids Production

Source: CitiGroup Report, April 2012, page 17.

U.S. ENERGY SECTOR: POLICY CHALLENGES

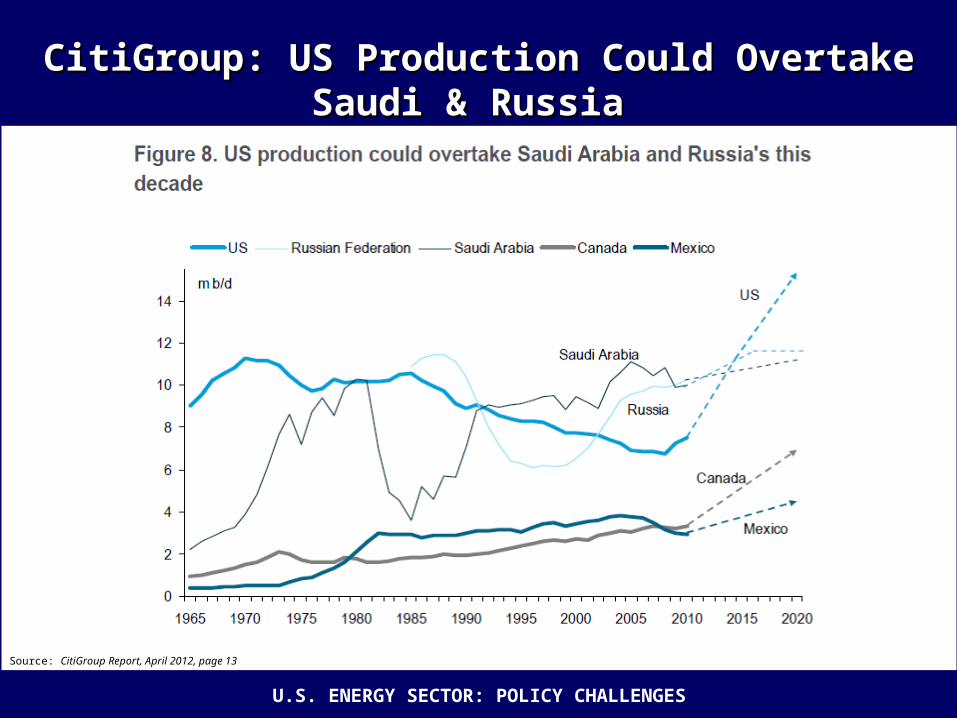

CitiGroup: US Production Could Overtake Saudi & Russia CitiGroup: US Production Could Overtake Saudi & Russia

Source: CitiGroup Report, April 2012, page 13

U.S. ENERGY SECTOR: POLICY CHALLENGES

PEW: US Leads Global Clean Energy Technology MarketPEW: US Leads Global Clean Energy Technology Market

Source: Pew Charitable Trust, Who’s Winning the Clean Energy Race, 2011 edition page 14

U.S. ENERGY SECTOR: POLICY CHALLENGES

US Clean Energy MarketUS Clean Energy Market

U.S. DOE, 2010 Renewable Energy Data Book (September 2011).

U.S. ENERGY SECTOR: POLICY CHALLENGES

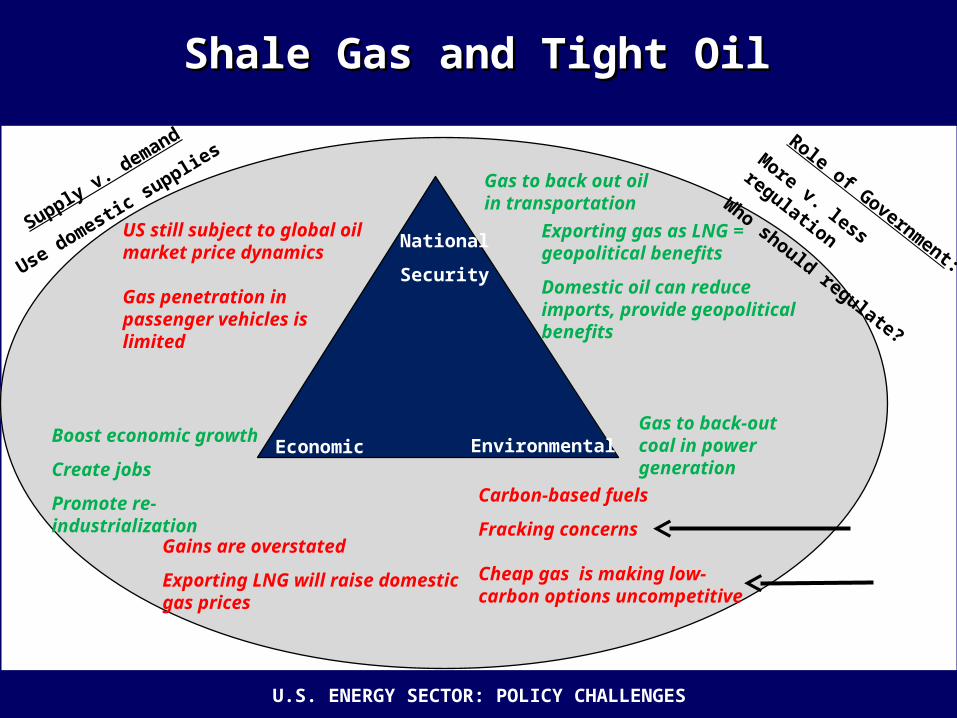

Shale Gas and Tight OilShale Gas and Tight Oil

National

Security

Environmental Economic

Gas to back out oil in transportation

Boost economic growth

Create jobs

Promote re-industrialization

Gas to back-out coal in power generation

Exporting gas as LNG = geopolitical benefits

Domestic oil can reduce imports, provide geopolitical benefits

Carbon-based fuels

Fracking concerns

Cheap gas is making low-carbon options uncompetitive

US still subject to global oil market price dynamics

Gas penetration in passenger vehicles is limited

Gains are overstated

Exporting LNG will raise domestic gas prices

Role of Government:

More v. less regulation

Who should regulate?

Supply v. demand

Use domestic supplie

s

U.S. ENERGY SECTOR: POLICY CHALLENGES

Shale Gas & Tight Oil – Environmental ConcernsShale Gas & Tight Oil – Environmental Concerns

NYC DEC Hearing - 11-30-11 (photo: J Banks)

U.S. ENERGY SECTOR: POLICY CHALLENGES

Shale Gas & Tight Oil – Environmental ConcernsShale Gas & Tight Oil – Environmental Concerns

New York City – June 5, 2012 (photo: J Banks)

U.S. ENERGY SECTOR: POLICY CHALLENGES

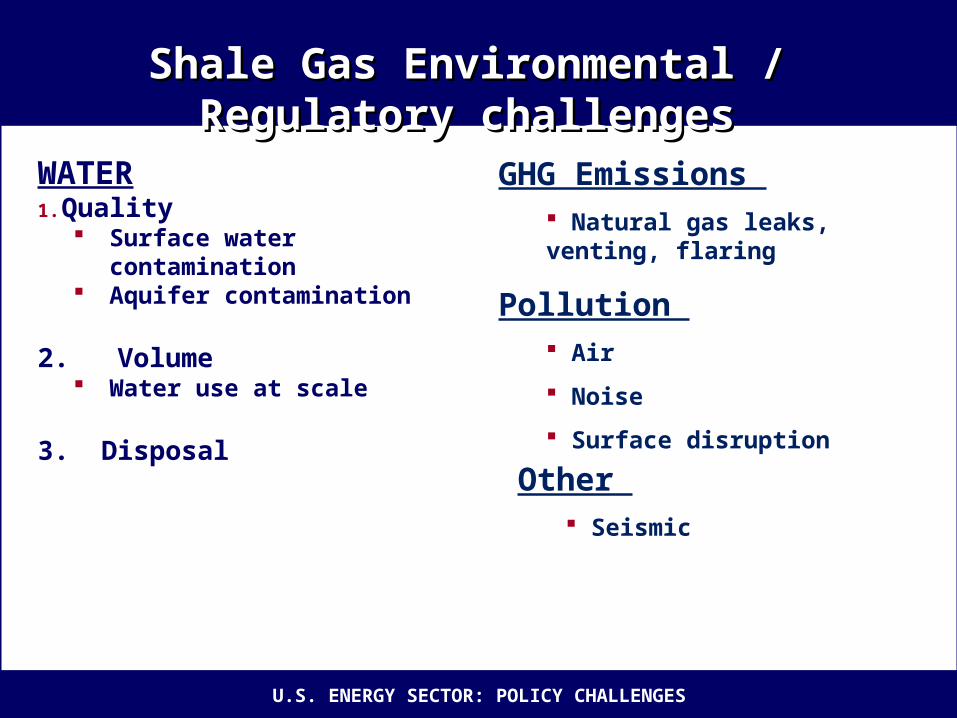

Shale Gas Environmental / Regulatory challengesShale Gas Environmental / Regulatory challenges

WATER1. Quality

Surface water contamination Aquifer contamination

2. Volume Water use at scale

3. Disposal

GHG Emissions Natural gas leaks, venting, flaring

Pollution Air

Noise

Surface disruption

Other Seismic

U.S. ENERGY SECTOR: POLICY CHALLENGES

Coal Plant Retirement Projections Coal Plant Retirement Projections

http://www.realclearenergy.org/charticles/2012/07/30/coal_retirements_2012-2016.html

U.S. ENERGY SECTOR: POLICY CHALLENGES

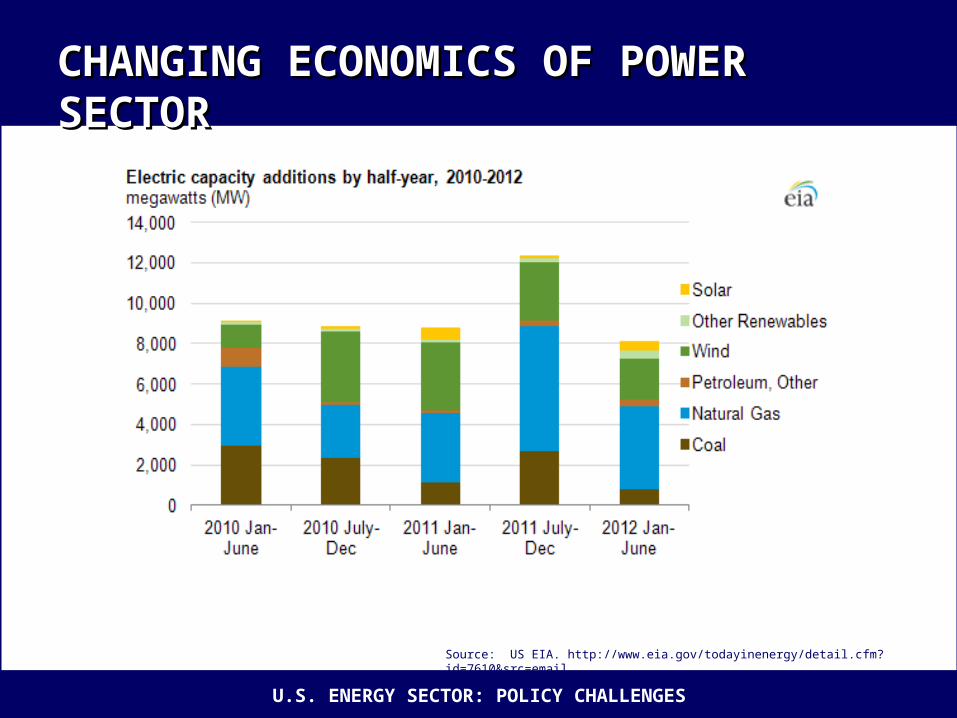

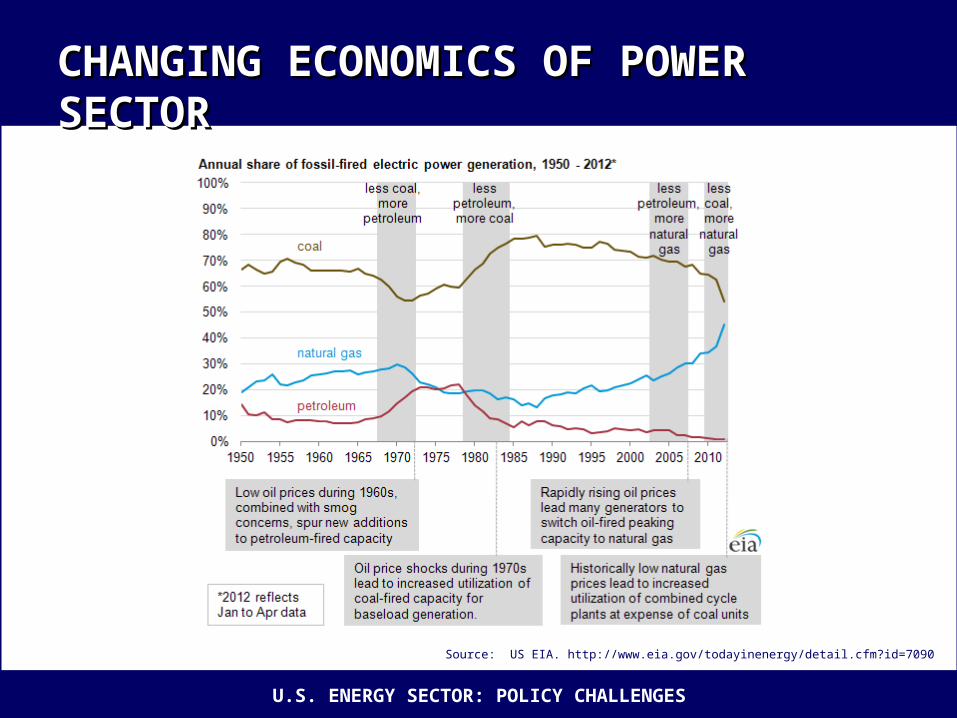

CHANGING ECONOMICS OF POWER SECTORCHANGING ECONOMICS OF POWER SECTOR

Source: US EIA. http://www.eia.gov/todayinenergy/detail.cfm?id=7610&src=email.

U.S. ENERGY SECTOR: POLICY CHALLENGES

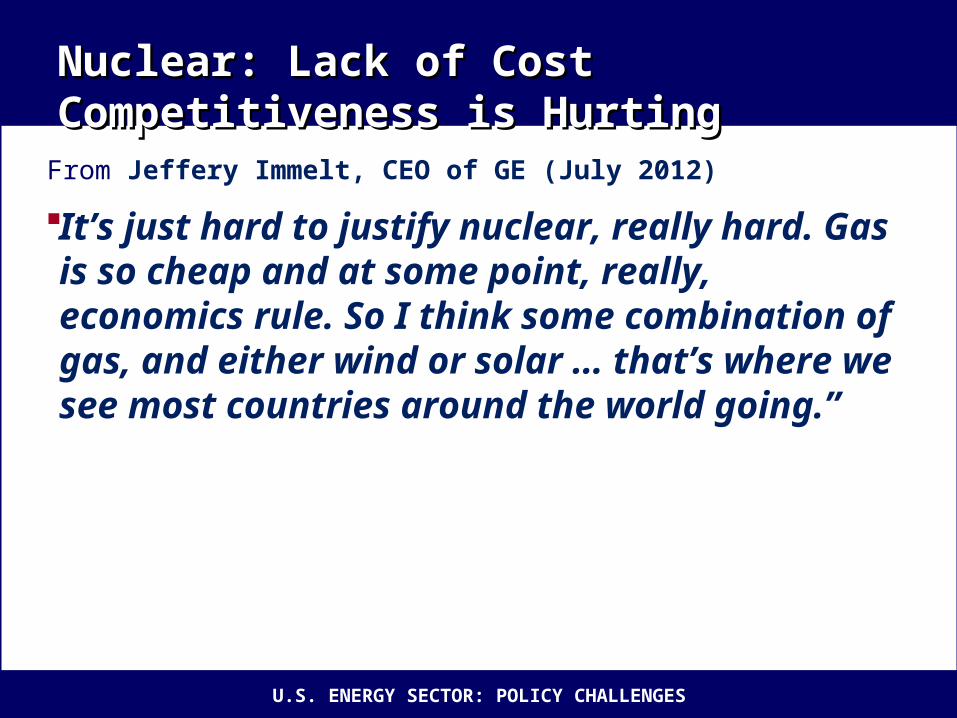

Nuclear: Lack of Cost Competitiveness is HurtingNuclear: Lack of Cost Competitiveness is Hurting

From Jeffery Immelt, CEO of GE (July 2012)

:It’s just hard to justify nuclear, really hard. Gas is so cheap and at some point, really, economics rule. So I think some combination of gas, and either wind or solar … that’s where we see most countries around the world going.”

U.S. ENERGY SECTOR: POLICY CHALLENGES

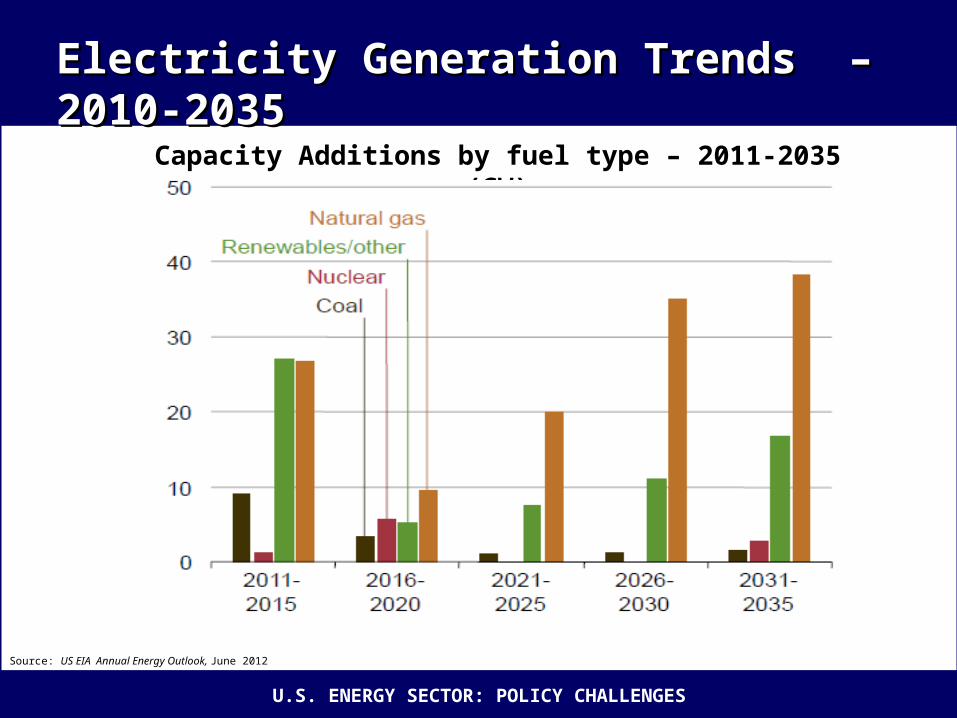

Electricity Generation Trends – 2010-2035Electricity Generation Trends – 2010-2035

Capacity Additions by fuel type – 2011-2035 (GW)

Source: US EIA Annual Energy Outlook, June 2012

U.S. ENERGY SECTOR: POLICY CHALLENGES

15

29

13

186

9

Colorado:• Shale gas• Wind

Iowa:• Wind• Ethanol

Energy & Toss-Up StatesEnergy & Toss-Up States

Ohio:• Shale Gas• Coal

Florida:• Offshore drilling

North Carolina:• Offshore drilling

Virginia:• Offshore drilling

TOTAL ELECTORAL COLLEGE VOTES SHOWN: 96

6Nevada:• Nuclear• Renewables

U.S. ENERGY SECTOR: POLICY CHALLENGES

The End

U.S. ENERGY SECTOR: POLICY CHALLENGES

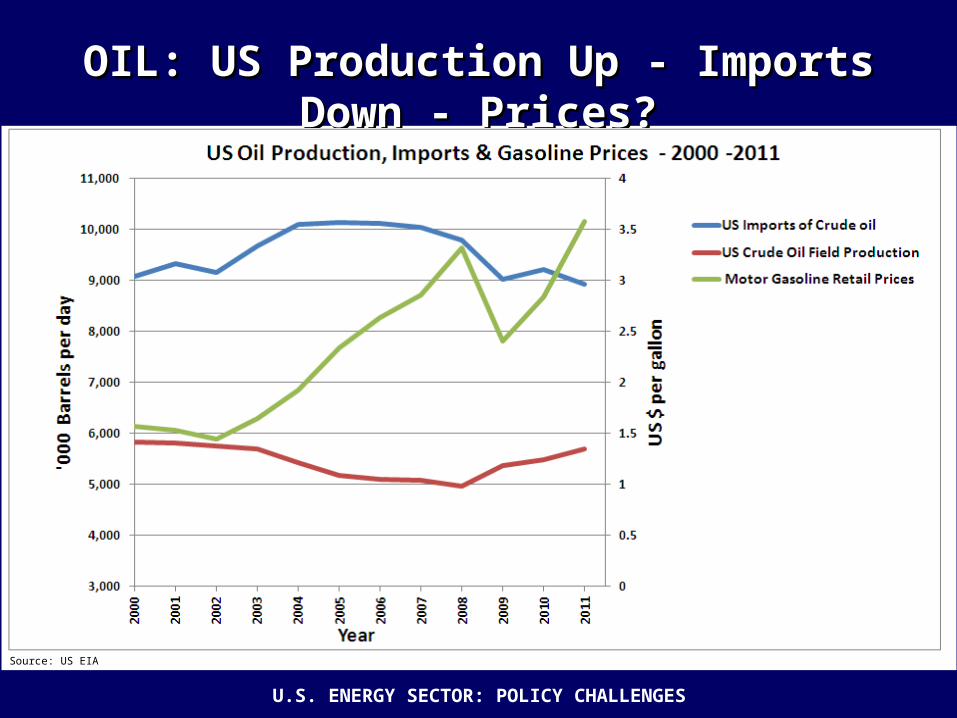

OIL: US Production Up - Imports Down - Prices?OIL: US Production Up - Imports Down - Prices?

Source: US EIA

U.S. ENERGY SECTOR: POLICY CHALLENGES

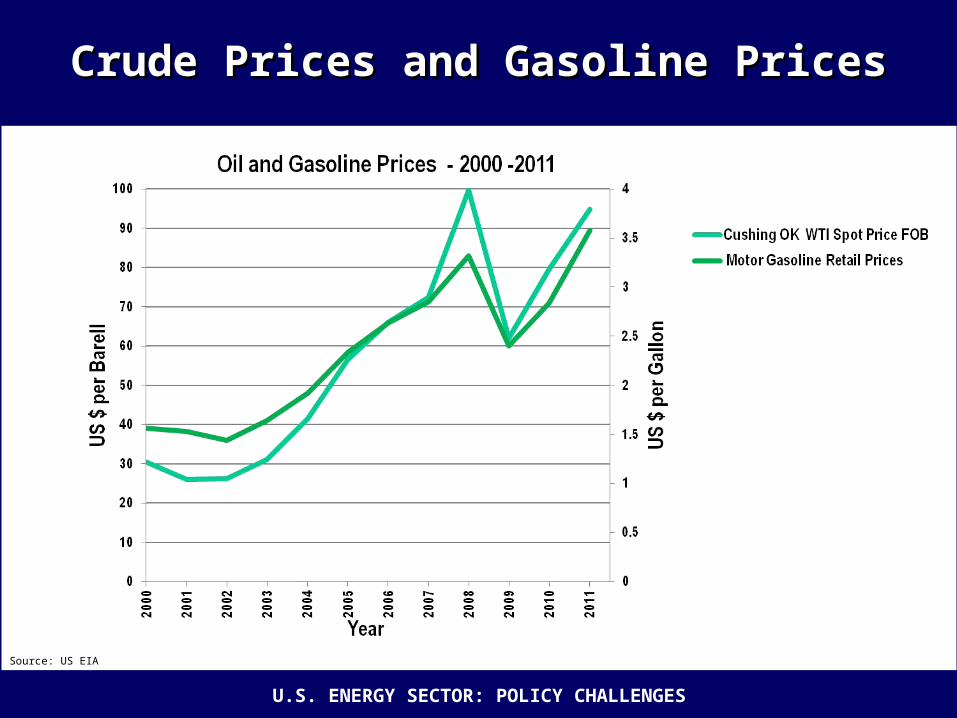

Crude Prices and Gasoline PricesCrude Prices and Gasoline Prices

Source: US EIA

U.S. ENERGY SECTOR: POLICY CHALLENGES

CHANGING ECONOMICS OF POWER SECTORCHANGING ECONOMICS OF POWER SECTOR

Source: US EIA. http://www.eia.gov/todayinenergy/detail.cfm?id=7090 .

U.S. ENERGY SECTOR: POLICY CHALLENGES

Keystone XL PipelineKeystone XL Pipeline

U.S. ENERGY SECTOR: POLICY CHALLENGES

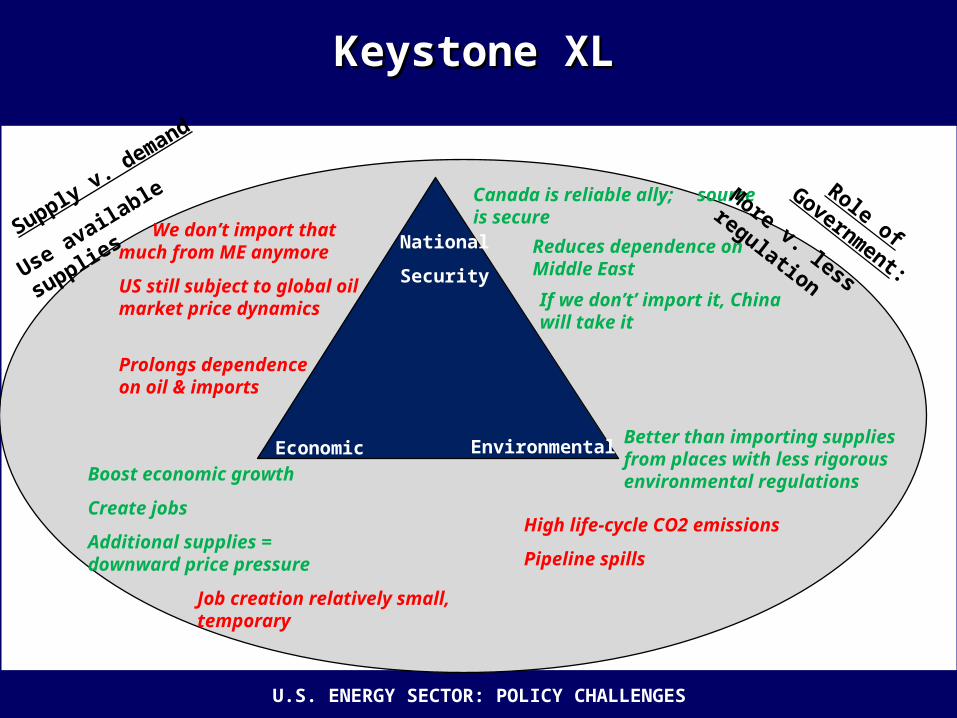

Keystone XLKeystone XL

National

Security

Environmental Economic

Canada is reliable ally; source is secure

Boost economic growth

Create jobs

Additional supplies = downward price pressure

Better than importing supplies from places with less rigorous environmental regulations

Reduces dependence on Middle East

High life-cycle CO2 emissions

Pipeline spills

We don’t import that much from ME anymore

US still subject to global oil market price dynamics

Prolongs dependence on oil & imports

Job creation relatively small, temporary

If we don’t’ import it, China will take it

Role of Government:

More v. less regulation

Supply v. demand

Use available supplie

s

![BURDENS OF PROOF AND QUALIFIED IMMUNITY€¦ · 2012] Burdens of Proof and Qualified Immunity 137 A. Burdens of Proof The first observation that must be made when discussing burdens](https://static.fdocuments.net/doc/165x107/5b408ec47f8b9a2f138d5242/burdens-of-proof-and-qualified-2012-burdens-of-proof-and-qualified-immunity.jpg)