Upside Down: The $400 Billion Federal Asset Budget Corporation for Enterprise Development September...

18

Upside Down: The $400 Upside Down: The $400 Billion Federal Asset Billion Federal Asset Budget Budget Corporation for Enterprise Development Corporation for Enterprise Development September 23, 2010 September 23, 2010 Eugene Steuerle Eugene Steuerle Richard B. Fisher Institute Fellow Richard B. Fisher Institute Fellow The Urban Institute The Urban Institute To receive Gene’s regular column, “The Government We Deserve,” send an To receive Gene’s regular column, “The Government We Deserve,” send an email to: email to: [email protected] [email protected]

-

Upload

jonah-berry -

Category

Documents

-

view

214 -

download

0

Transcript of Upside Down: The $400 Billion Federal Asset Budget Corporation for Enterprise Development September...

Upside Down: The $400 Billion Upside Down: The $400 Billion Federal Asset BudgetFederal Asset Budget

Corporation for Enterprise DevelopmentCorporation for Enterprise DevelopmentSeptember 23, 2010September 23, 2010

Eugene SteuerleEugene SteuerleRichard B. Fisher Institute FellowRichard B. Fisher Institute Fellow

The Urban InstituteThe Urban Institute

To receive Gene’s regular column, “The Government We Deserve,” send an email to:To receive Gene’s regular column, “The Government We Deserve,” send an email to:[email protected]@urban.org

Two Long-term Goals of Mine (1) To relate asset development policies to principles such as

progressivity & efficiency

(2) To channel asset research to where the saving takes place and where the subsidies are made

Four parts to this presentation:A profile of saving over the lifespanSaving by socio-economic classPrivate versus public savingHow we subsidize saving

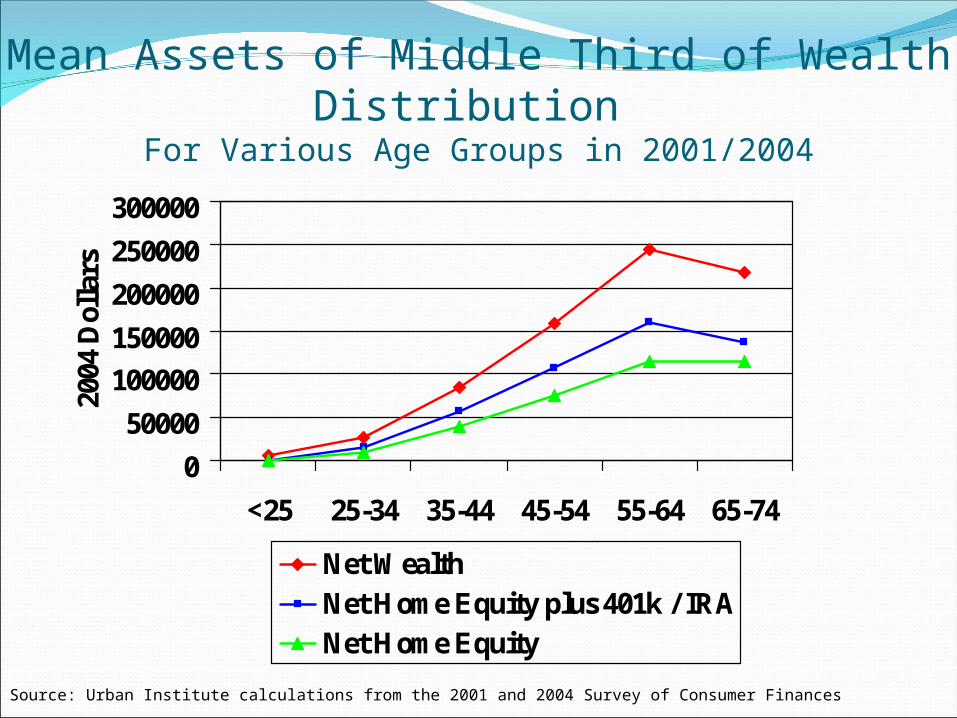

Profile of SavingHomes and pensions matter mostFor middle class, pension saving starts early

In fact, much saving can come from simply hanging onto pension assets until retirement

For many, asset spend-down also starts with more than two decades of life expectancy remaining

Mortgage debt pay-down a traditional (but continuing?) major source of saving

CDs and checking accounts often learning tools—not major sources of asset accumulation

Mean Assets of Middle Third of Wealth Distribution For Various Age Groups in 2001/2004

0

50000

100000

150000

200000

250000

300000

<25 25-34 35-44 45-54 55-64 65-74

2004

Dol

lars

Net WealthNet Home Equity plus 401k / IRANet Home Equity

Source: Urban Institute calculations from the 2001 and 2004 Survey of Consumer Finances

Source: Urban Institute calculations from the 1992, 1995, 2001 and 2004 Survey of Consumer Finances and DYNASIM3.

Figure 3a. Annual Wealth Accrual Per Adult between Early 1990's and Early 2000's for Typical Households by Education (2004 Dollars)

$11,800

$22,400

$1,600$3,900

$5,700$4,700

$6,900

$12,100

$31,300

25-34 in 1992/1995 to 35-44 in 2001/2004

35-44 in 1992/1995to 45-54 in 2001/2004

45-54 in 1992/1995to 55-64 in 2001/2005

Age

Less Than High School

High School

College

Annual Wealth Accrual Per Adult between Early 90s and Early 00s for Typical Households,

by Education (2004 Dollars)

Within Cohort Change in Household Wealth over Nine Year Period

0

20000

40000

60000

80000

100000

120000

140000

25-34 35-44 45-54 55-64

Age in 1992/1995

2004

dol

lars

Net Housing 401Ks and IRAs All Other WealthSource: Urban Institute calculations from the 1992, 1995, 2001, and 2004 Survey of Consumer Finances

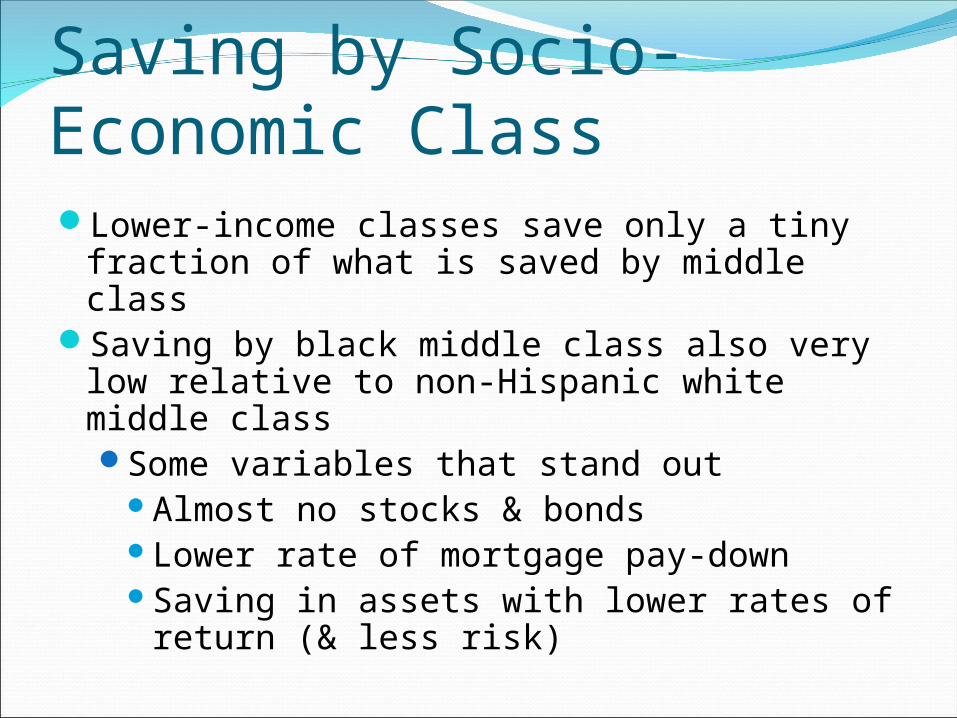

Saving by Socio-Economic ClassLower-income classes save only a tiny fraction of what is

saved by middle classSaving by black middle class also very low relative to non-

Hispanic white middle classSome variables that stand out

Almost no stocks & bondsLower rate of mortgage pay-down Saving in assets with lower rates of return (& less

risk)

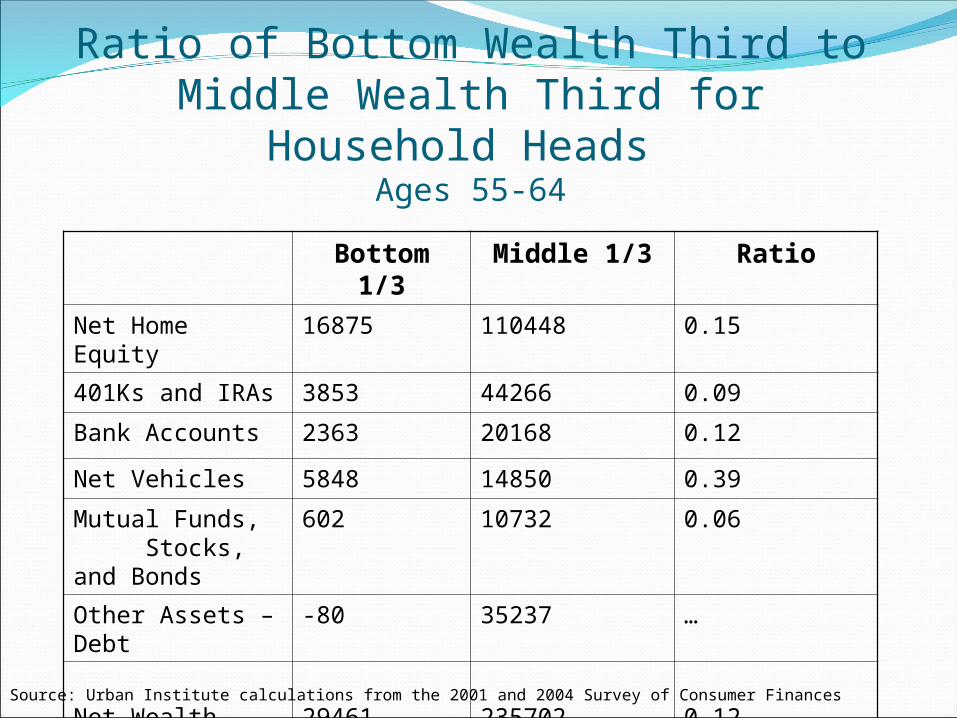

Ratio of Bottom Wealth Third to Middle Wealth Third for Household Heads

Ages 55-64

Bottom 1/3 Middle 1/3 Ratio

Net Home Equity 16875 110448 0.15

401Ks and IRAs 3853 44266 0.09

Bank Accounts 2363 20168 0.12

Net Vehicles 5848 14850 0.39

Mutual Funds, Stocks, and Bonds

602 10732 0.06

Other Assets –Debt -80 35237 …

Net Wealth 29461 235702 0.12

Source: Urban Institute calculations from the 2001 and 2004 Survey of Consumer Finances

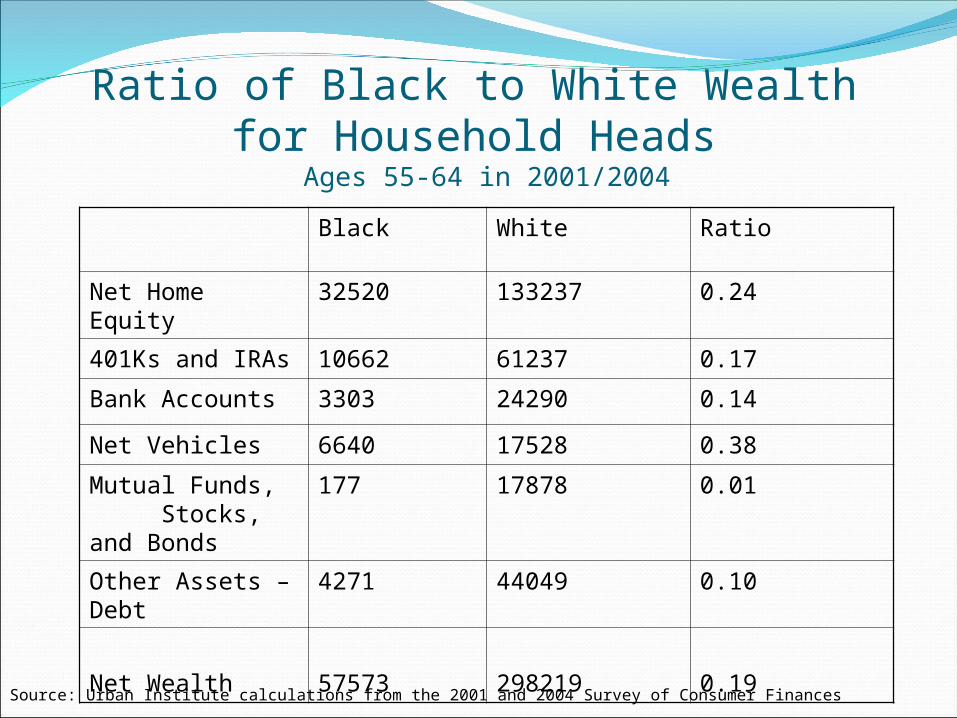

Ratio of Black to White Wealth for Household Heads

Ages 55-64 in 2001/2004

Black White Ratio

Net Home Equity 32520 133237 0.24

401Ks and IRAs 10662 61237 0.17

Bank Accounts 3303 24290 0.14

Net Vehicles 6640 17528 0.38

Mutual Funds, Stocks, and Bonds

177 17878 0.01

Other Assets –Debt 4271 44049 0.10

Net Wealth 57573 298219 0.19

Source: Urban Institute calculations from the 2001 and 2004 Survey of Consumer Finances

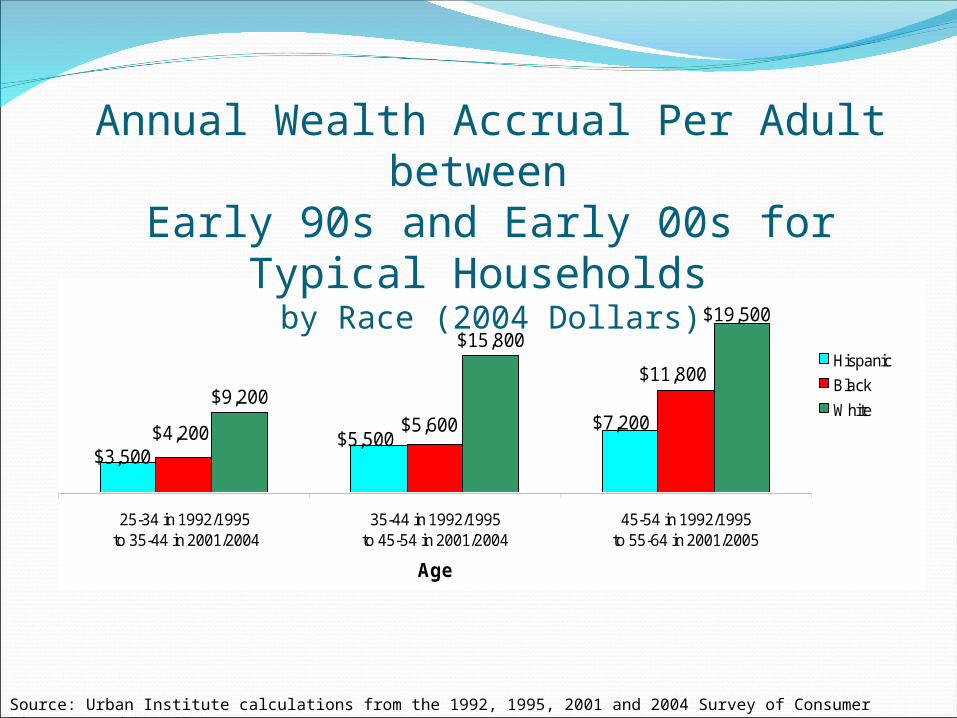

$9,200

$15,800

$3,500

$7,200$5,500$4,200

$11,800

$5,600

$19,500

25-34 in 1992/1995 to 35-44 in 2001/2004

35-44 in 1992/1995to 45-54 in 2001/2004

45-54 in 1992/1995to 55-64 in 2001/2005

Age

Hispanic

Black

White

Annual Wealth Accrual Per Adult between Early 90s and Early 00s for Typical Households

by Race (2004 Dollars)

Source: Urban Institute calculations from the 1992, 1995, 2001 and 2004 Survey of Consumer Finances and DYNASIM3.

Private versus Public SavingSocial Security and Medicare “wealth” dominates all

private wealth for close to 2/3rds of population

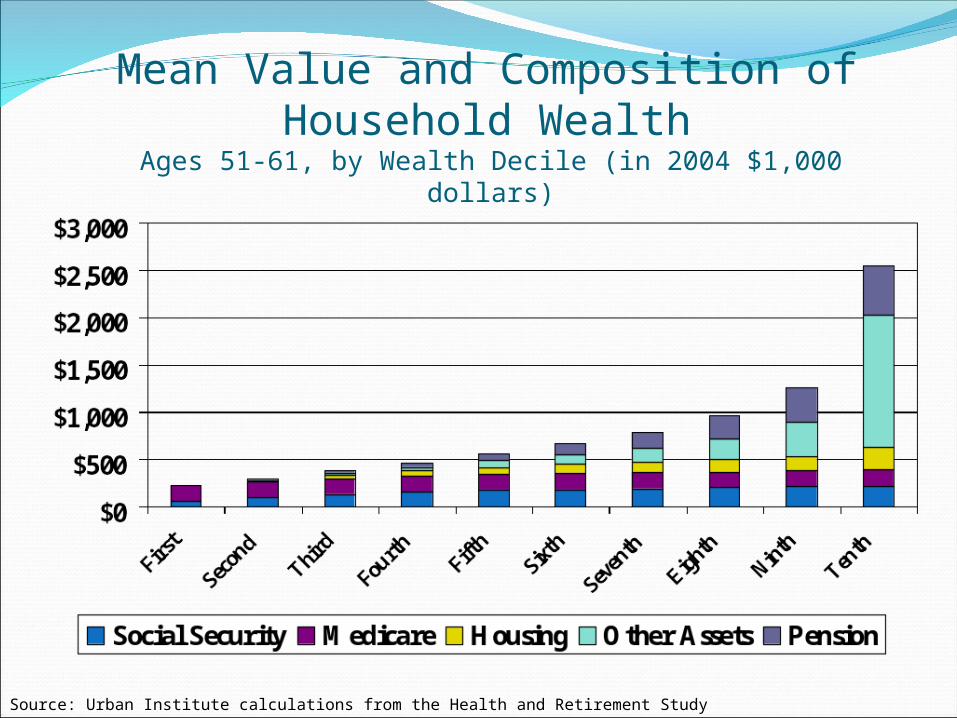

Mean Value and Composition of Household WealthAges 51-61, by Wealth Decile (in 2004 $1,000 dollars)

Source: Urban Institute calculations from the Health and Retirement Study

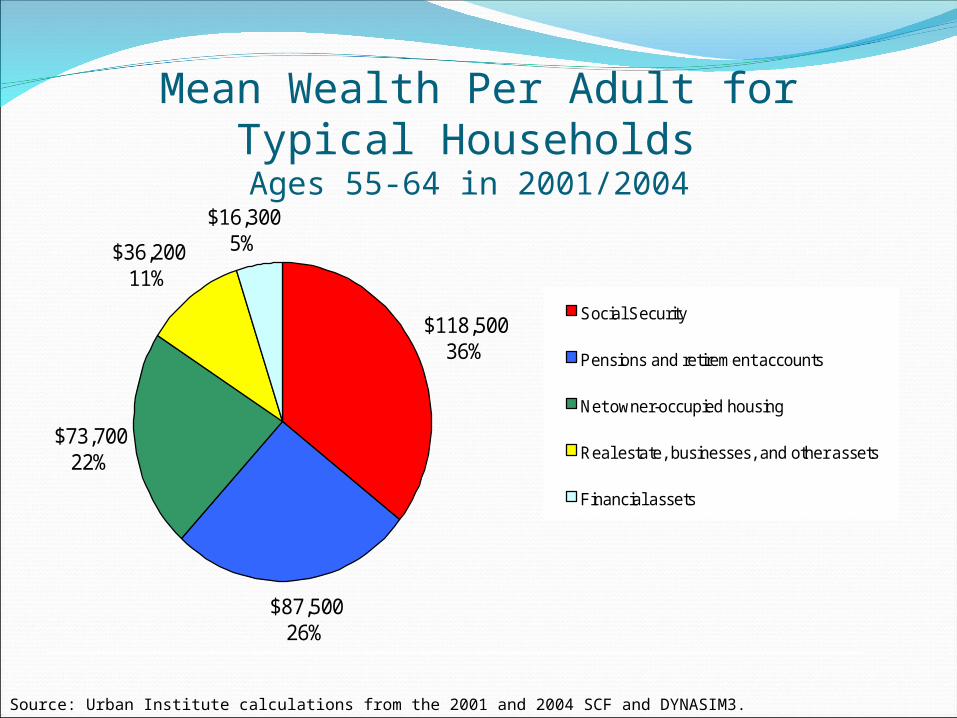

$118,50036%

$87,50026%

$73,70022%

$36,20011%

$16,3005%

Social Security

Pensions and retirement accounts

Net owner-occupied housing

Real estate, businesses, and other assets

Financial assets

Figure 1. Mean Wealth Per Adult for Typical Households Ages 55-64 in 2001/2004

Source: Urban Institute calculations from the 2001 and 2004 SCF and DYNASIM3.Notes: Typical households are in the middle quintile of the wealth distribution. Financial assets include bank accounts, CDs, stocks, bonds, and mutual funds. Other assets are net of non-housing debt. Social Security and defined-benefit pension wealth are the expected present value of future benefits. Future Social Security benefits are based on lifetime earnings records that were statistically matched to adults in the SCF from DYNASIM3. Future DB pension benefits are based on what adults expect to receive or are already receiving. The analysis combines the 2001 and 2004 surveys and expresses all amounts in 2004 dollars.

Total Wealth = $332,300

Source: Urban Institute calculations from the 2001 and 2004 SCF and DYNASIM3.

Mean Wealth Per Adult for Typical Households Ages 55-64 in 2001/2004

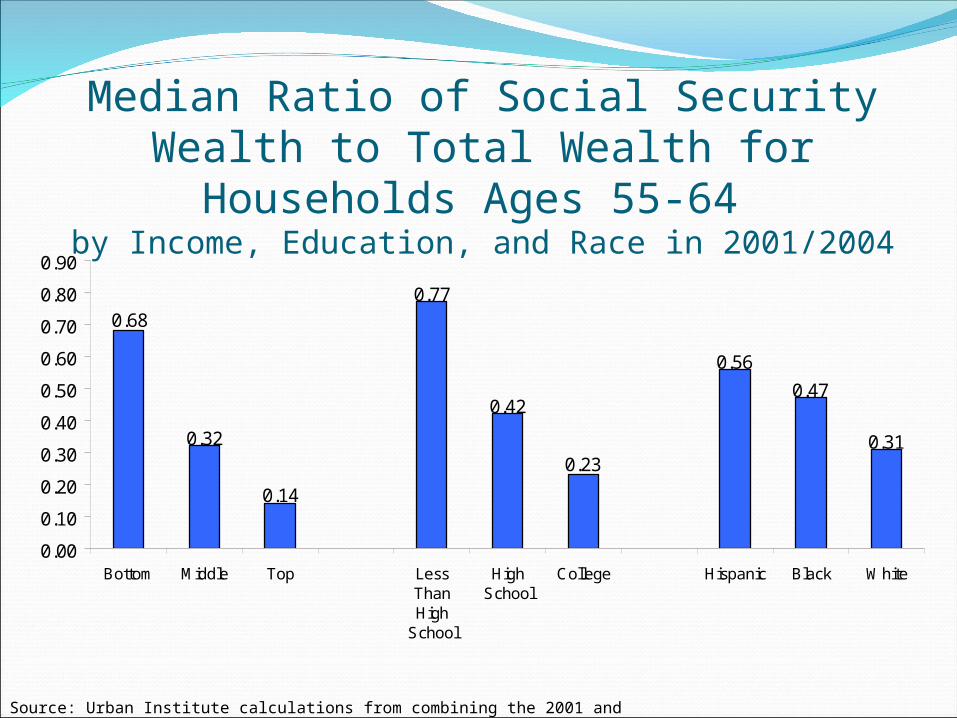

0.31

0.47

0.56

0.23

0.42

0.77

0.14

0.32

0.68

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Bottom Middle Top LessThanHigh

School

HighSchool

College Hispanic Black White

Figure 5. Median Ratio of Social Security Wealth to Total Wealth for Households Ages 55-64 by Income, Education, and Race in 2001/2004

Source: Urban Institute calculations from combining the 2001 and 2004 SCFand DYNASIM3.

Notes: Wealth includes the expected present value of future Social Security and pension benefits, retirement accounts, net owner-occupied housing, real estate, businesses, and financial assets.

Income Quintile

Source: Urban Institute calculations from combining the 2001 and 2004 SCF and DYNASIM3.

Median Ratio of Social Security Wealth to Total Wealth for Households Ages 55-64 by Income, Education, and Race in 2001/2004

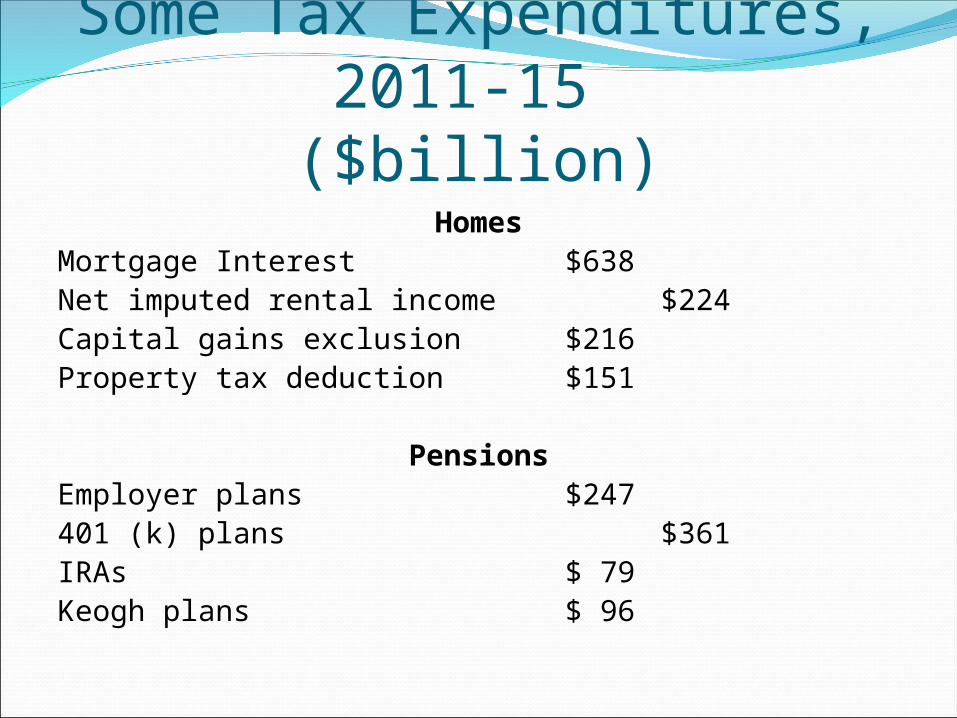

How We Subsidize Saving

Tax subsidies accrue to higher income classes since:They face higher tax ratesThey do most of the saving

Some Tax Expenditures, 2011-15 ($billion)

HomesMortgage Interest $638 Net imputed rental income $224Capital gains exclusion $216Property tax deduction $151

PensionsEmployer plans $247401 (k) plans $361IRAs $ 79Keogh plans $ 96

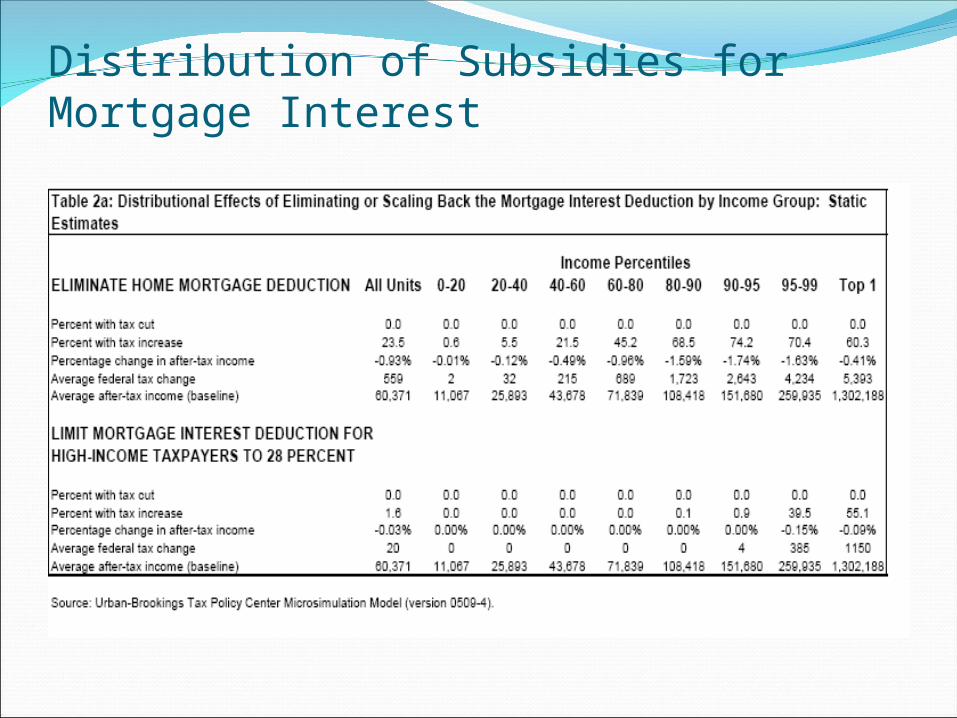

Distribution of Subsidies for Mortgage Interest

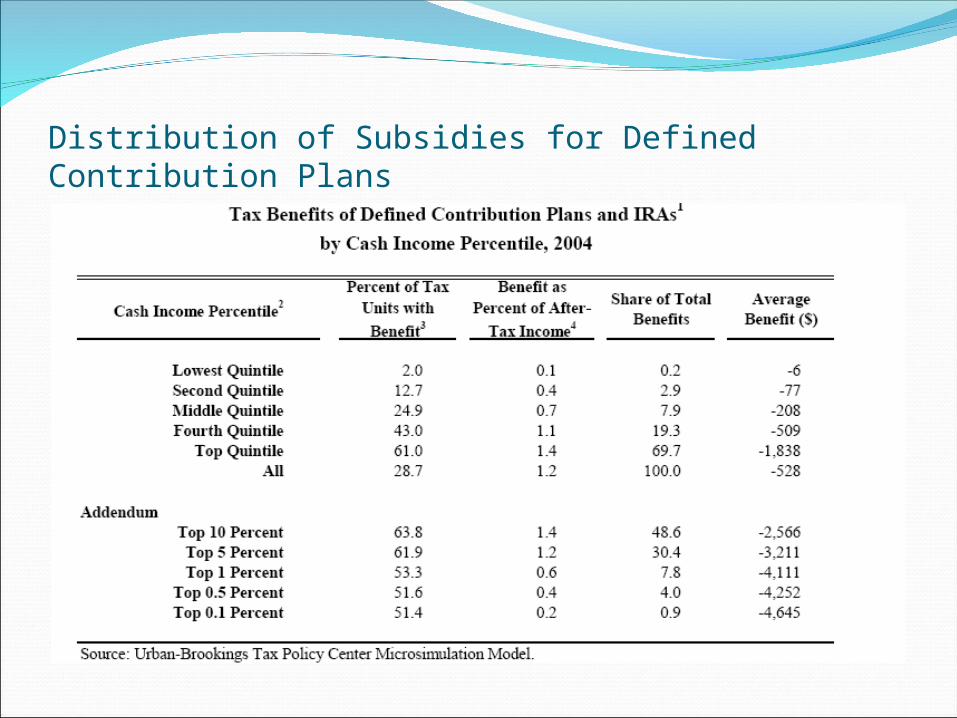

Distribution of Subsidies for Defined Contribution Plans