UPDATES ON GST - MRAI Features of GST GST Overview Taxable Event ... VAT/CST, Entry Tax, CVD/SAD...

21

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential. UPDATES ON GST METAL RECYCLING INDUSTRY N.MATHIVANAN

Transcript of UPDATES ON GST - MRAI Features of GST GST Overview Taxable Event ... VAT/CST, Entry Tax, CVD/SAD...

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

UPDATES ON GST

METAL RECYCLING INDUSTRY

N.MATHIVANAN

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

GST UPDATE GST Development

Salient Features of GST

GST Overview

Taxable Event – Supply / Nature of Supply and

Place of Supply

Registration

GST Rates

Valuation

Input Tax Credit and its Matching

Return

Compliance Calendar

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

GST Development - When will GST come?

GST Constitutional

Amendment Act, 2016 - 8th

September 2016

(Power to collect taxes under

existing provisions till 16.9.2017)

Formed GST Council

(First Meeting on

22.09.2016)

Passage of CGST and IGST Laws by Centre and SGST

Law by States

(Expected by March 2017)

Rollout of GST

(Expected Date 1.7.2017)

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

GST – Salient Features

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

GST- Overview

Taxes subsumed under GST: Excise duty, VAT, CST, Service tax, CVD, SAD, Entry tax, etc.

Taxes not subsumed: Clean energy cess & stowing excise duty on coal, Electricity Duty, etc.

GST is IT Systems driven

Input tax credit – key pillar under GST

6

Taxable Event – Supply

Concept of composite supply and mixed supply

Supply for consideration

All forms of supply

Made or agreed to be made

For a consideration

By a Person In the course or furtherance of

Business

Sale/ Transfer /Barter / Exchange /License / Rental / Lease / Disposal

Phrase “To another person” not incorporated

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

Supply without a consideration Sc

hed

ule

I

Permanent transfer/ disposal of business assets where input tax has been availed

Supply between related persons or distinct persons specified in section 10, when made in the course or furtherance of business

1. By principal to agent where agent undertakes to supply such goods

2. By agent to principal where agent undertakes to receive goods on behalf of principal

Importation of services by taxable person from related person or any of his establishments outside India, in the course or furtherance of business

New Business Transactions taxable under GST without consideration

E.g. – Use of office facility by another group entity

Copyright (c) 2015. Lakshmikumaran & Sridharan / Confidential.

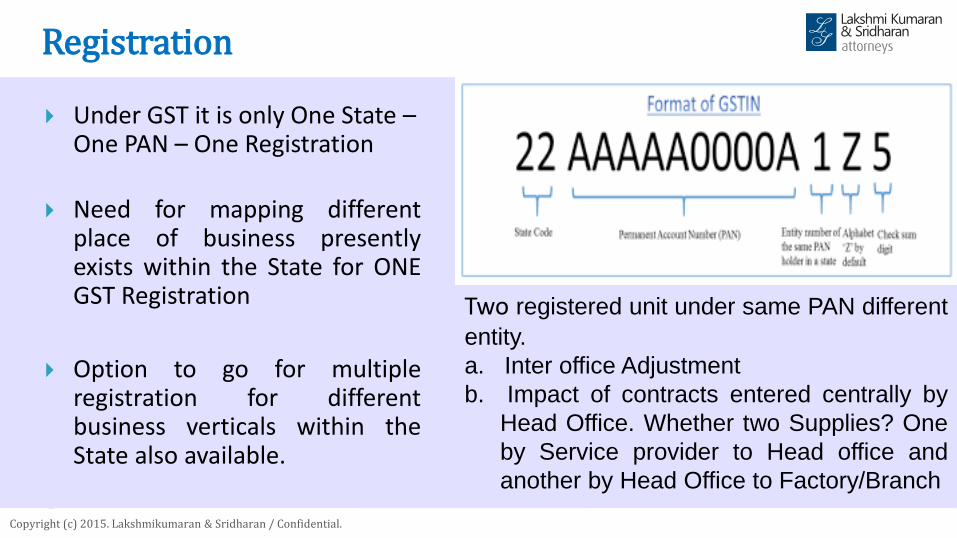

Registration

Under GST it is only One State – One PAN – One Registration

Need for mapping different place of business presently exists within the State for ONE GST Registration

Option to go for multiple registration for different business verticals within the State also available.

Two registered unit under same PAN different

entity.

a. Inter office Adjustment

b. Impact of contracts entered centrally by

Head Office. Whether two Supplies? One

by Service provider to Head office and

another by Head Office to Factory/Branch

9

Supply under GST

GST Supply

Intra State Supply

Goods and/or Services

SGST

CGST

Inter State Supply

Goods and/or Services

IGST

Import

Goods

Basic Custom Duty

IGST

Services

IGST

Export

Goods and/or Services

Physical Export

1. Pay IGST and Refund to be

claimed by Exporter

2. Sale without IGST

Supply to SEZ

Goods and/or Services

Zero Rated

Pay IGST and Refund to be claimed by SEZ

Non GST Supply

E.g. Diesel

Supply

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

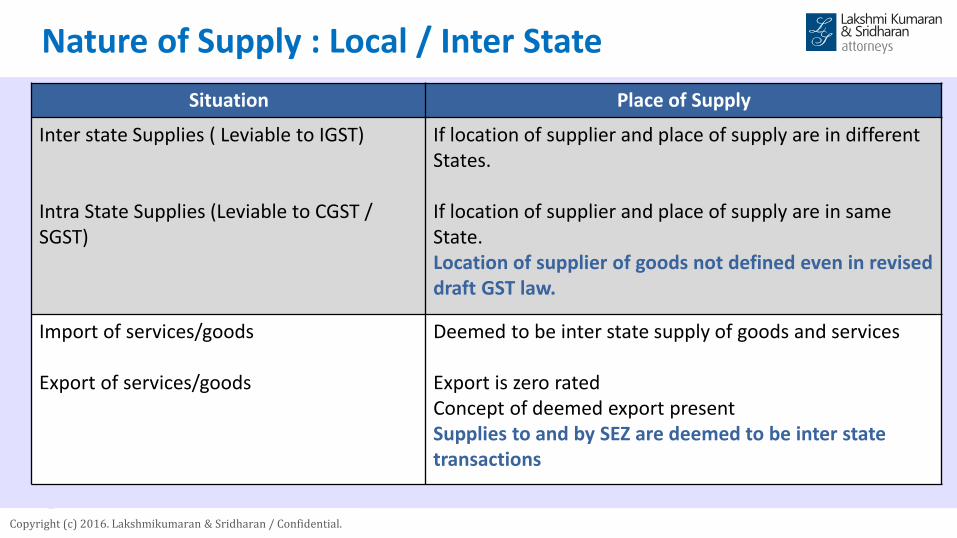

Situation Place of Supply

Inter state Supplies ( Leviable to IGST) Intra State Supplies (Leviable to CGST / SGST)

If location of supplier and place of supply are in different States. If location of supplier and place of supply are in same State. Location of supplier of goods not defined even in revised draft GST law.

Import of services/goods Export of services/goods

Deemed to be inter state supply of goods and services Export is zero rated Concept of deemed export present Supplies to and by SEZ are deemed to be inter state transactions

Nature of Supply : Local / Inter State

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

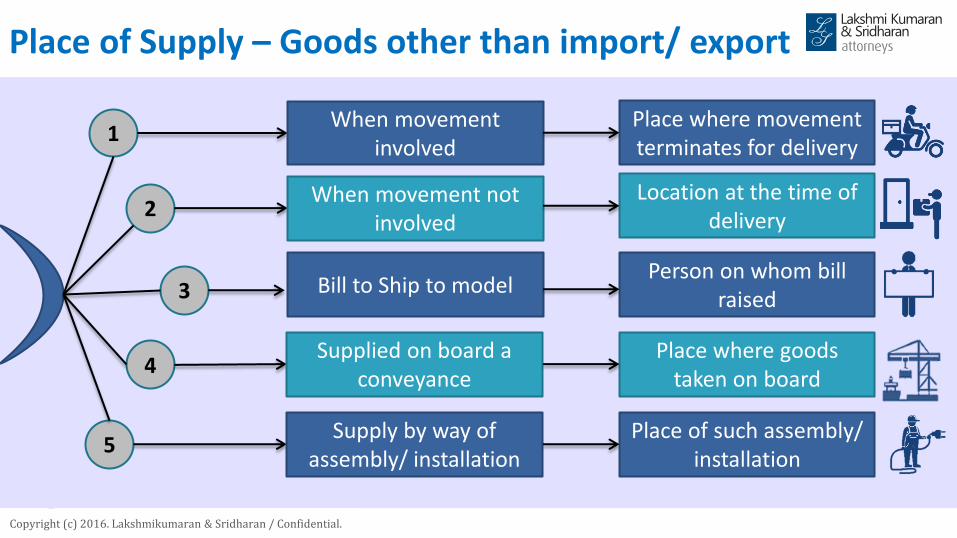

Place of Supply – Goods other than import/ export

1

2

3

4

5

When movement involved

Place where movement terminates for delivery

When movement not involved

Location at the time of delivery

Supplied on board a conveyance

Place where goods taken on board

Bill to Ship to model Person on whom bill

raised

Supply by way of assembly/ installation

Place of such assembly/ installation

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

Place of Supply – Goods imported/ exported

The place of supply of goods imported into India shall be the location of the importer

The place of supply of goods exported from India shall be location outside India

Import India Export

Copyright (c) 2015. Lakshmikumaran & Sridharan / Confidential.

GST RATES

Exact list of taxes/cesses getting subsumed will be made available by GST Council/Legislation.

Can Petroleum products purchased against Form C even in GST regime ?

Further, rate of GST shall be mapped HSN wise.

Excise, Service Tax, VAT/CST, Entry Tax,

CVD/SAD will be subsumed.

ED,VAT /CST continuing on 5

petroleum products namely Petrol, diesel,

natural gas, ATF & Crude oil.

Four rate prescribed :

5% , 12%, 18% and 28%. Cess may be levied on high end/

luxury products.

Proposal for three tier rate structure for

services

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

Value of taxable supply Transaction Value

Freight and insurance upto delivery of goods

Different value based on payment terms – Inherent interest component

Discount post removal

Valuation in case of transfer from one unit to another unit? Comparable value or cost of production

Valuation in case of transfer to depot Comparable value or cost of production or depot value?

Credit accumulation at depot in case of comparable value

Valuation

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

Input Tax Credit

Input Tax Credit IGST/CGST/SGST charged on any supply of goods and/or services to taxpayer and includes any amount paid under reverse charge but excludes any such amount paid under composition levy

• Goods/Service • used or intended to be

used • by a supplier • in the course or

furtherance of business

Inputs/ Input Services

• Means goods, • the value of which is

capitalized in the books of accounts of the person claiming the credit and

• which are used or intended to be used in the course or furtherance of business

Capital Goods

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

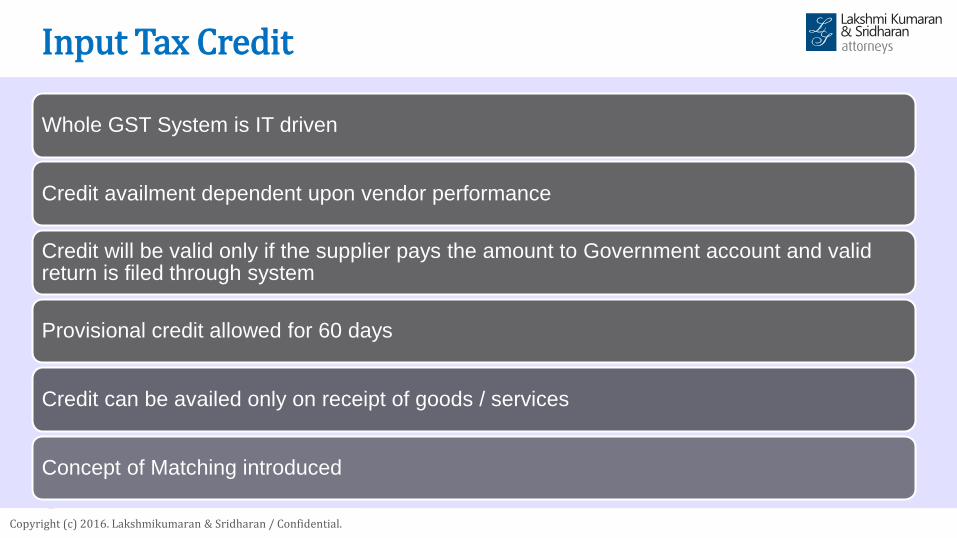

Input Tax Credit

Whole GST System is IT driven

Credit availment dependent upon vendor performance

Credit will be valid only if the supplier pays the amount to Government account and valid return is filed through system

Provisional credit allowed for 60 days

Credit can be availed only on receipt of goods / services

Concept of Matching introduced

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

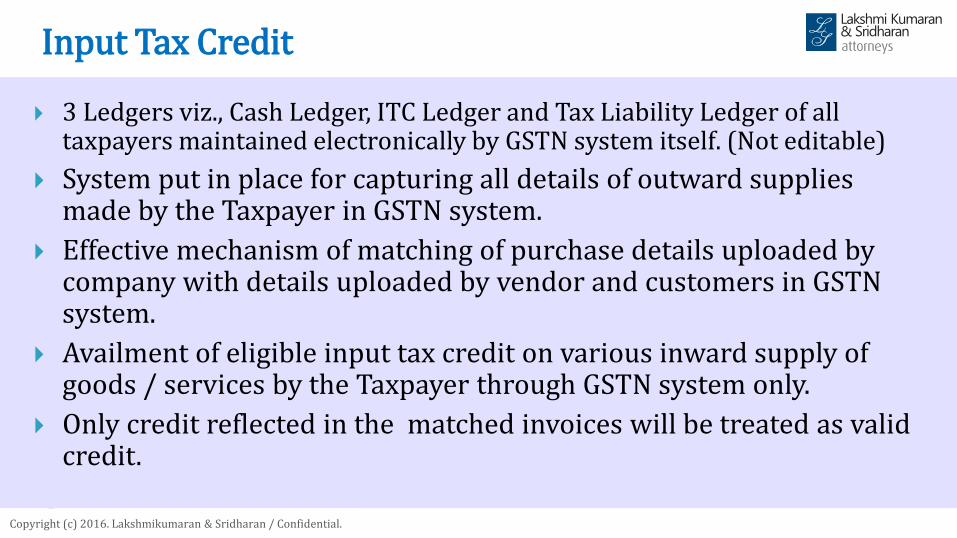

Input Tax Credit

3 Ledgers viz., Cash Ledger, ITC Ledger and Tax Liability Ledger of all taxpayers maintained electronically by GSTN system itself. (Not editable)

System put in place for capturing all details of outward supplies made by the Taxpayer in GSTN system.

Effective mechanism of matching of purchase details uploaded by company with details uploaded by vendor and customers in GSTN system.

Availment of eligible input tax credit on various inward supply of goods / services by the Taxpayer through GSTN system only.

Only credit reflected in the matched invoices will be treated as valid credit.

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

Basic Features of Returns

Invoice based Return

Concept of Auto population

Designed for system based matching

Settlement through data received in returns

No revised returns – changes through amendments to original details

Maintenance of ledgers – Cash, ITC and liability

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

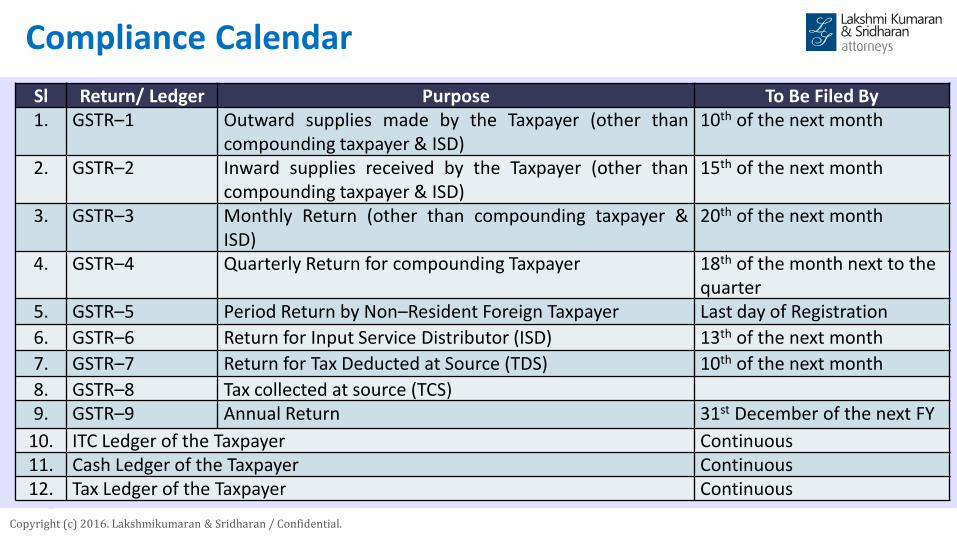

Compliance Calendar

Sl Return/ Ledger Purpose To Be Filed By 1. GSTR–1 Outward supplies made by the Taxpayer (other than

compounding taxpayer & ISD) 10th of the next month

2. GSTR–2 Inward supplies received by the Taxpayer (other than compounding taxpayer & ISD)

15th of the next month

3. GSTR–3 Monthly Return (other than compounding taxpayer & ISD)

20th of the next month

4. GSTR–4 Quarterly Return for compounding Taxpayer 18th of the month next to the quarter

5. GSTR–5 Period Return by Non–Resident Foreign Taxpayer Last day of Registration

6. GSTR–6 Return for Input Service Distributor (ISD) 13th of the next month

7. GSTR–7 Return for Tax Deducted at Source (TDS) 10th of the next month

8. GSTR–8 Tax collected at source (TCS) 9. GSTR–9 Annual Return 31st December of the next FY

10. ITC Ledger of the Taxpayer Continuous 11. Cash Ledger of the Taxpayer Continuous 12. Tax Ledger of the Taxpayer Continuous

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

GST Preparedness

GST Understanding and Awareness

Business transactions and its treatment in GST Regime

GST Efficient Business Model

Strategy for smooth transition

Smooth GST implementation

GST Compatibility - IT & Accounting System

Copyright (c) 2016. Lakshmikumaran & Sridharan / Confidential.

L&S

Offices

NEW DELHI [email protected] MUMBAI [email protected] BENGALURU [email protected] CHENNAI [email protected] HYDERABAD [email protected]

GURGAON [email protected] CHANDIGARH [email protected] PUNE [email protected] KOLKATA [email protected] AHMEDABAD [email protected]

Committed to International Standards in Quality and Information Security

If you wish to subscribe to GST updates, please send an e-mail to [email protected]

GENEVA [email protected]

LONDON [email protected]

INTERNATIONAL

INDIA

www.lakshmisri.com

Thank You

![[Economy 4 Newbie] VAT & GST (basic stuff) « Mrunal](https://static.fdocuments.net/doc/165x107/544ce789b1af9fc6498b497a/economy-4-newbie-vat-gst-basic-stuff-mrunal.jpg)