UNLOCKING ECOMMERCE GROWTH: SOLVING THE ......and SaaS providers, to ISOs and PSPs, to other B2B...

6

firstdata.com/paymentfacilitators A First Data Position Paper UNLOCKING ECOMMERCE GROWTH: SOLVING THE PAYMENT FACILITATOR CHALLENGE Eliminating Payment Barriers to Drive New Revenue

Transcript of UNLOCKING ECOMMERCE GROWTH: SOLVING THE ......and SaaS providers, to ISOs and PSPs, to other B2B...

firstdata.com/paymentfacilitators

A First Data Position Paper

UNLOCKING ECOMMERCE GROWTH: SOLVING THE PAYMENT FACILITATOR CHALLENGEEliminating Payment Barriers to Drive New Revenue

firstdata.com ©2017 First Data Corporation. All rights reserved. 2

eCommerce Growth Drives Emergence of the Payment FacilitatorIn short, payment facilitators are organizations that engage merchants to provide digital payment acceptance accounts—payment cards, online payments, alternative payments, etc.—under a single acquirer agreement. This role is far from new. PayPal®, perhaps the most well-known payment facilitator, debuted its solution in 1998, and Stripe brought its product to market in 2011. However, as eCommerce continues explosive global growth—and expectations

of anytime-anywhere, seamless digital transactions become the norm—nearly every business is looking to integrate seamless digital payment acceptance into its offering. Forward-thinking businesses now see that the opportunity isn’t just to deliver digital transaction capabilities to sub-merchants—it’s to more fully control the entire sub-merchant experience and capture significant payment processing revenue by actually becoming a payment facilitator.

Executive SummaryConnectivity is now the very fabric of modern life—we learn, share, socialize, buy and virtually live online. In this hyperconnected world, eCommerce continues exponential global growth as nearly every aspect of the business world—in every vertical and in every place in the world—becomes increasingly digital. The demand from businesses and the consumers they serve for seamless, simple digital transaction experiences has created a transformative new role in the payments landscape: the payment facilitator.

The payment facilitator model enables organizations—ranging from ISOs and PSPs to software vendors and value-added resellers—to provide a complete and simplified option for onboarding sub-merchants and providing these customers with a seamless, integrated digital payment acceptance platform. Forward-thinking companies with global growth goals are increasingly acting as payment facilitators, building these kinds of frictionless eCommerce capabilities for their sub-merchants. The payment facilitator model not only helps solve the many challenges and pain points traditionally associated with connecting sub-merchants with digital payment capabilities—it enables payment facilitators to capture a burgeoning revenue stream from payment processing volume that is expected to reach $1.16 trillion globally in the next two years.1

However, though the payment facilitator role inarguably simplifies many things, businesses working to become payment facilitators and those already operating in this role also face new technological, risk and compliance challenges. They’re struggling to build and integrate the necessary technologies, burdened by regulatory requirements that grow increasingly more complicated, overwhelmed by the complexities of taking on new kinds of payment risk and finding their global scalability impeded by limited currency and payment method acceptance.

With the introduction of our Global PFAC™ solution set, First Data is bringing the full force of our unmatched experience and expertise to solving these challenges by providing a single, global partner for accelerating eCommerce. Through the powerful combination of proven payment technologies and a single global contracting and integration experience, Global PFAC provides a simplified, central platform that empowers payment facilitators to deliver an outstanding sub-merchant experience, enable unmatched global scalability and optimize revenue opportunities, while significantly reducing the technology integration, risk management and compliance burdens so organizations can focus on their core business.

1 Double Diamond Group, “Why Software Vendors Should Be Payment Facilitators,” 2016

firstdata.com ©2017 First Data Corporation. All rights reserved. 3

Thus, businesses ranging from software vendors and SaaS providers, to ISOs and PSPs, to other B2B organizations that provide services to sub-merchants, are joining the payment facilitator landscape. As of late 2016, the Double Diamond Group identified more than 11,000 B2B companies that are “ideal candidates to become [payment facilitators].”2 Many of these companies serve markets largely untapped in terms of digital payments—health, education, transportation and government/utilities, to name a few. Unlocking the potential payment volume in these markets is predicted to drive an astounding 88-percent growth in gross payments volume in the next five years.3 Put in more direct terms, analysts say companies moving into the payment facilitator role have a $4.4 billion revenue opportunity in front of them.

Why the Payment Facilitator Model is the Future of eCommerce Traditionally, enabling digital payments has been a difficult and time-consuming challenge. For example, a software vendor seeking to integrate digital payment acceptance into an application needed to work with several third parties—including a payment processor, a payment gateway and a software vendor offering the technology to actually enable digital transactions. Not only was this burdensome for the business, but it led to a disjointed experience for the end user or consumer—a patchwork solution with frustrating, unintuitive workflows. In addition, the onboarding process placed an immense burden on sub-merchants, requiring a long list of paperwork and processes that could take days or weeks.

The payment facilitator model simplifies things for all involved, removing the complex requirements of a traditional ISO. In our example, the software vendor can create a single umbrella acquiring agreement and act as a single partner—payment processor, payment gateway and technology provider—to give a seamless experience to sub-merchants. Sub-merchants, in turn, can enjoy

dramatically faster onboarding—filling out a single form on a single website—that can be completed in a few hours. The sub-merchant has the simplicity of working with a single partner for digital payment acceptance, and doesn’t have to worry about the acquirer, ISO or other contracts happening behind the scenes. Finally, this streamlined, single-source solution means a seamless digital payment experience for consumers/end users. A global consumer base has the highly convenient and personalized choice of transacting when and where they want, with the device and payment method they want, and in the currency they prefer.

2 Double Diamond Group, “Why Software Vendors Should Be Payment Facilitators,” 20163 Ibid.

A GROWING OPPORTUNITY PAYMENT FACILITATORS PROCESSED

IN PAYMENTS IN 20162018 PROJECTIONS SHOOTING UP TO

A SUCCESSFUL PAYMENT FACILITATOR SOLUTION OFFERS:

Easy, immediate sub-merchant onboarding

PAYMENT FACILITATORS FACE NUMEROUS CHALLENGES

• Inelegant Technologies• Regulatory Requirements• New Kinds of Payment Risk• Global Payment Acceptance

Simplified risk management and compliance

Global scalability and payment acceptance for sub-merchants

Access to burgeoning payment processing revenue

“Businesses across sectors now have a tremendous

opportunity to take control of a seamless digital

transaction experience for sub-merchants and

their end users, while capturing an immense new

revenue stream.”

- Peter O’Halloran,

First Data GM of eCommerce

firstdata.com ©2017 First Data Corporation. All rights reserved. 4

Payment Expertise Shouldn’t Be the Barrier to GrowthAs more businesses race to capture the payment facilitator opportunity, they’re smashing into a harsh wall of technological and regulatory challenges. Whether they’re ISO or PSPs expanding their payment processing capabilities, or ISVs moving into the payments world for the first time, they’re realizing they need new technology solutions and resources to manage additional risk and compliance requirements. Instead of focusing on their core service and their customer relationships, many find their growth limited by a lack of payments expertise—something that has nothing to do with their core business.

Companies taking on the payment facilitator role often prefer not to siphon significant resources away from their core business to address the technical, regulatory and risk-management requirements of payment facilitators. But in looking for a partner to ease this pain, they also shouldn’t be forced to give up control and compromise customer convenience and satisfaction—nor should they lose out on payment facilitator revenue.

Payment Facilitators Must Prepare for Global ScalabilityIn the rush to build a payment facilitator platform, many organizations narrow their focus on the current needs of existing sub-merchants—and the current needs of their sub-merchants’ existing customers. But an emerging reality of modern eCommerce is that every business must be prepared to quickly scale to serve a truly global customer base. For the payment facilitator, this means building a technology solution that can deliver flexible currency and payment method acceptance. This enables sub-merchants to provide digital experiences that anticipate customer needs and preferences and deliver seamless convenience to customers around the world—allowing them to transact when they want, where they want, in the currency or payment method they prefer.

Moreover, building this level of scalability and flexibility into the technological platform gives a payment facilitator invaluable agility to freely pursue global opportunities.

First Data is Solving the Payment Facilitator Challenge

As a global leader in commerce-enabling technology and solutions, First Data is uniquely positioned to solve the payment facilitator challenge—and to help these businesses capture this immense opportunity and drive global growth. We’ve been there since the birth of eCommerce and understand the market forces, complexities, challenges and opportunities shaping the future of eCommerce. Our unmatched combination of deep payments industry expertise, worldwide relationships and integrations and our complete portfolio of trusted payments technologies gives us a singular ability to attack the payment facilitator challenge from every angle. We’re building global platforms that empower seamless digital transaction experiences—providing payment facilitators with a single integration interface that enables sub-merchants to easily authorize transactions in more than 150 currencies worldwide, and settle in 17 currencies. We’re simplifying sub-merchant onboarding and helping payment facilitators manage and mitigate risk. We’re leveraging our core strengths to solve the complexities of the digital payment landscape—and freeing payment facilitators to focus on their own core strengths and services.

The Two Models of Payment FacilitationA business moving into the role of payment facilitator

can adopt a retail or wholesale model. In the retail

payment facilitation model, the payment facilitator,

known as the “master merchant”, outsources the

“back-end” elements of payment processing to a

third party. This partner provides the master merchant

account, handles payment processing, underwriting

and risk management—freeing the master merchant to

focus on its core service offering and its relationships

with sub-merchants. While the retail model provides

the simplest path to becoming a payment facilitator,

the master merchant hands over control over the

customer experience, as well as a portion of payment

processing revenue, to the third party partner.

“Payment facilitators need to be nimble, agile, and have access to proven technology to achieve global scale, especially as eCommerce has opened the door for companies to do business worldwide. Our Global PFAC solution empowers master merchants to do business wherever they want, whenever they want, while streamlining the administrative burden of enabling payments around the world.”

- Shane Fitzpatrick, First Data Global Head of eCommerce

firstdata.com ©2017 First Data Corporation. All rights reserved. 5

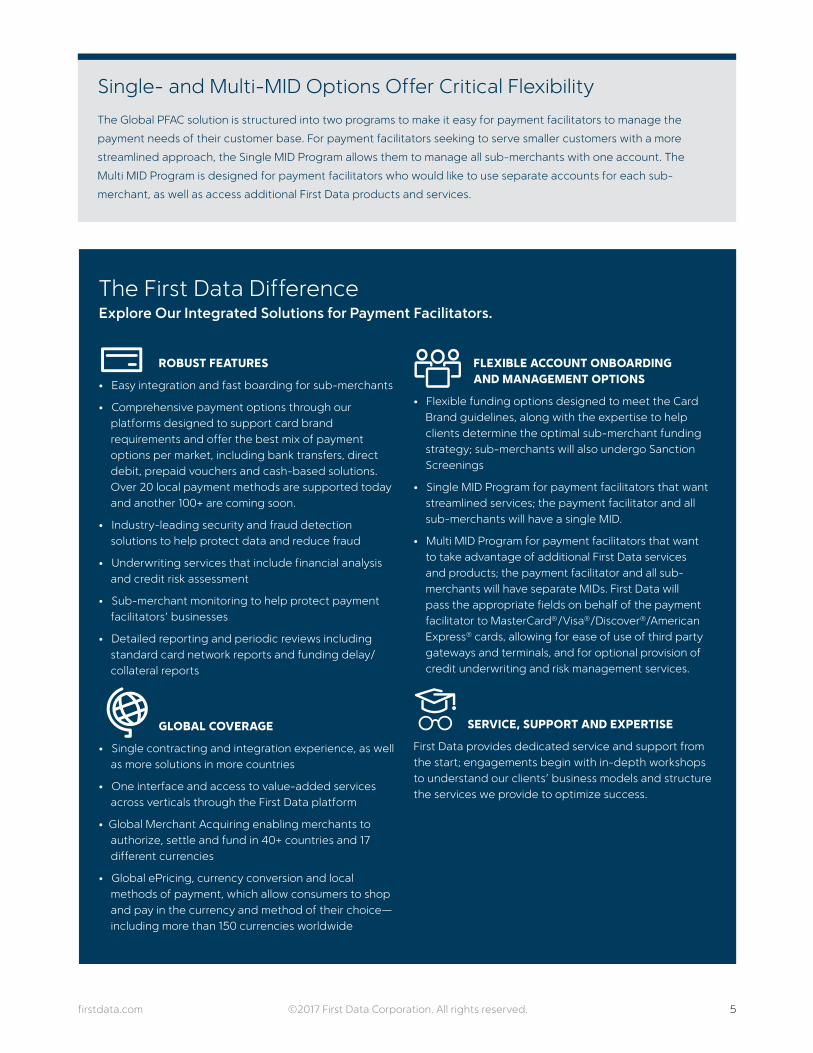

ROBUST FEATURES

• Easy integration and fast boarding for sub-merchants

• Comprehensive payment options through our platforms designed to support card brand requirements and offer the best mix of payment options per market, including bank transfers, direct debit, prepaid vouchers and cash-based solutions. Over 20 local payment methods are supported today and another 100+ are coming soon.

• Industry-leading security and fraud detection solutions to help protect data and reduce fraud

• Underwriting services that include financial analysis and credit risk assessment

• Sub-merchant monitoring to help protect payment facilitators’ businesses

• Detailed reporting and periodic reviews including standard card network reports and funding delay/ collateral reports

GLOBAL COVERAGE

• Single contracting and integration experience, as well as more solutions in more countries

• One interface and access to value-added services across verticals through the First Data platform

• Global Merchant Acquiring enabling merchants to authorize, settle and fund in 40+ countries and 17 different currencies

• Global ePricing, currency conversion and local methods of payment, which allow consumers to shop and pay in the currency and method of their choice—including more than 150 currencies worldwide

FLEXIBLE ACCOUNT ONBOARDING AND MANAGEMENT OPTIONS

• Flexible funding options designed to meet the Card Brand guidelines, along with the expertise to help clients determine the optimal sub-merchant funding strategy; sub-merchants will also undergo Sanction Screenings

• Single MID Program for payment facilitators that want streamlined services; the payment facilitator and all sub-merchants will have a single MID.

• Multi MID Program for payment facilitators that want to take advantage of additional First Data services and products; the payment facilitator and all sub-merchants will have separate MIDs. First Data will pass the appropriate fields on behalf of the payment facilitator to MasterCard®/Visa®/Discover®/American Express® cards, allowing for ease of use of third party gateways and terminals, and for optional provision of credit underwriting and risk management services.

SERVICE, SUPPORT AND EXPERTISE

First Data provides dedicated service and support from the start; engagements begin with in-depth workshops to understand our clients’ business models and structure the services we provide to optimize success.

The First Data DifferenceExplore Our Integrated Solutions for Payment Facilitators.

Single- and Multi-MID Options Offer Critical Flexibility

The Global PFAC solution is structured into two programs to make it easy for payment facilitators to manage the

payment needs of their customer base. For payment facilitators seeking to serve smaller customers with a more

streamlined approach, the Single MID Program allows them to manage all sub-merchants with one account. The

Multi MID Program is designed for payment facilitators who would like to use separate accounts for each sub-

merchant, as well as access additional First Data products and services.

LEARN HOW OUR GLOBAL PFAC SOLUTIONS CAN ACCELERATE YOUR ECOMMERCE GROWTH

firstdata.com/paymentfacilitators

©2017 First Data Corporation. All rights reserved. The First Data® name, logo and related trademarks and service marks are owned by First Data Corporation and are registered or used in the U.S. and many foreign countries. All trademarks, service marks and trade names referenced in this material are the property of their respective owners.

LEVERAGING THE

POWER OF ONE

• One partner

• One contract

• Global presence

• Range of payment methods

• Licensed and compliant

• Single settlement

• Fraud filters

• Secure, stable and scalable

• Innovative

• Flexible to meet your needs