UNITED STATES SECURITIES AND EXCHANGE … · Berkshire Hathaway Energy Company and its subsidiaries...

191

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [X] Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the quarterly period ended September 30, 2017 or [ ] Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from ______ to _______ Commission File Number Exact name of registrant as specified in its charter; State or other jurisdiction of incorporation or organization IRS Employer Identification No. 001-14881 BERKSHIRE HATHAWAY ENERGY COMPANY 94-2213782 (An Iowa Corporation) 666 Grand Avenue, Suite 500 Des Moines, Iowa 50309-2580 515-242-4300 001-05152 PACIFICORP 93-0246090 (An Oregon Corporation) 825 N.E. Multnomah Street Portland, Oregon 97232 888-221-7070 333-90553 MIDAMERICAN FUNDING, LLC 47-0819200 (An Iowa Limited Liability Company) 666 Grand Avenue, Suite 500 Des Moines, Iowa 50309-2580 515-242-4300 333-15387 MIDAMERICAN ENERGY COMPANY 42-1425214 (An Iowa Corporation) 666 Grand Avenue, Suite 500 Des Moines, Iowa 50309-2580 515-242-4300 000-52378 NEVADA POWER COMPANY 88-0420104 (A Nevada Corporation) 6226 West Sahara Avenue Las Vegas, Nevada 89146 702-402-5000 000-00508 SIERRA PACIFIC POWER COMPANY 88-0044418 (A Nevada Corporation) 6100 Neil Road Reno, Nevada 89511 775-834-4011 N/A (Former name or former address, if changed from last report)

-

Upload

duongkhanh -

Category

Documents

-

view

217 -

download

2

Transcript of UNITED STATES SECURITIES AND EXCHANGE … · Berkshire Hathaway Energy Company and its subsidiaries...

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q[X] Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended September 30, 2017 or

[ ] Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934For the transition period from ______ to _______

Commission File Number

Exact name of registrant as specified in its charter; State or other jurisdiction of incorporation or organization

IRS EmployerIdentification No.

001-14881 BERKSHIRE HATHAWAY ENERGY COMPANY 94-2213782(An Iowa Corporation)

666 Grand Avenue, Suite 500Des Moines, Iowa 50309-2580

515-242-4300

001-05152 PACIFICORP 93-0246090(An Oregon Corporation)

825 N.E. Multnomah StreetPortland, Oregon 97232

888-221-7070

333-90553 MIDAMERICAN FUNDING, LLC 47-0819200(An Iowa Limited Liability Company)

666 Grand Avenue, Suite 500Des Moines, Iowa 50309-2580

515-242-4300

333-15387 MIDAMERICAN ENERGY COMPANY 42-1425214(An Iowa Corporation)

666 Grand Avenue, Suite 500Des Moines, Iowa 50309-2580

515-242-4300

000-52378 NEVADA POWER COMPANY 88-0420104(A Nevada Corporation)

6226 West Sahara AvenueLas Vegas, Nevada 89146

702-402-5000

000-00508 SIERRA PACIFIC POWER COMPANY 88-0044418(A Nevada Corporation)

6100 Neil RoadReno, Nevada 89511

775-834-4011

N/A(Former name or former address, if changed from last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the SecuritiesExchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file suchreports), and (2) has been subject to such filing requirements for the past 90 days.

Registrant Yes NoBERKSHIRE HATHAWAY ENERGY COMPANY XPACIFICORP XMIDAMERICAN FUNDING, LLC XMIDAMERICAN ENERGY COMPANY XNEVADA POWER COMPANY XSIERRA PACIFIC POWER COMPANY X

Indicate by check mark whether the registrants have submitted electronically and posted on their corporate Web sites, if any, everyInteractive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) duringthe preceding 12 months (or for such shorter period that the registrants were required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smallerreporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smallerreporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Registrant

LargeAccelerated

FilerAccelerated

filer

Non-accelerated

Filer

SmallerReportingCompany

EmergingGrowth

CompanyBERKSHIRE HATHAWAY ENERGY COMPANY XPACIFICORP XMIDAMERICAN FUNDING, LLC XMIDAMERICAN ENERGY COMPANY XNEVADA POWER COMPANY XSIERRA PACIFIC POWER COMPANY X

If an emerging growth company, indicate by check mark if the registrants have elected not to use the extended transition periodfor complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrants are a shell company (as defined in Rule 12b-2 of the Exchange Act).Yes o No x

All shares of outstanding common stock of Berkshire Hathaway Energy Company are privately held by a limited group of investors.As of October 31, 2017, 77,174,325 shares of common stock, no par value, were outstanding.

All shares of outstanding common stock of PacifiCorp are indirectly owned by Berkshire Hathaway Energy Company. As ofOctober 31, 2017, 357,060,915 shares of common stock, no par value, were outstanding.

All of the member's equity of MidAmerican Funding, LLC is held by its parent company, Berkshire Hathaway Energy Company,as of October 31, 2017.

All shares of outstanding common stock of MidAmerican Energy Company are owned by its parent company, MHC Inc., whichis a direct, wholly owned subsidiary of MidAmerican Funding, LLC. As of October 31, 2017, 70,980,203 shares of common stock,no par value, were outstanding.

All shares of outstanding common stock of Nevada Power Company are owned by its parent company, NV Energy, Inc., whichis an indirect, wholly owned subsidiary of Berkshire Hathaway Energy Company. As of October 31, 2017, 1,000 shares ofcommon stock, $1.00 stated value, were outstanding.

All shares of outstanding common stock of Sierra Pacific Power Company are owned by its parent company, NV Energy, Inc.As of October 31, 2017, 1,000 shares of common stock, $3.75 par value, were outstanding.

This combined Form 10-Q is separately filed by Berkshire Hathaway Energy Company, PacifiCorp, MidAmerican Funding, LLC,MidAmerican Energy Company, Nevada Power Company and Sierra Pacific Power Company. Information contained hereinrelating to any individual company is filed by such company on its own behalf. Each company makes no representation as toinformation relating to the other companies.

TABLE OF CONTENTS

PART I

Item 1. Financial Statements 1Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations 2Item 3. Quantitative and Qualitative Disclosures About Market Risk 151Item 4. Controls and Procedures 151

PART II

Item 1. Legal Proceedings 152Item 1A. Risk Factors 152Item 2. Unregistered Sales of Equity Securities and Use of Proceeds 152Item 3. Defaults Upon Senior Securities 152Item 4. Mine Safety Disclosures 152Item 5. Other Information 152Item 6. Exhibits 152Signatures 153Exhibit Index 154

i

Definition of Abbreviations and Industry Terms

When used in Forward-Looking Statements, Part I - Items 2 through 3, and Part II - Items 1 through 6, the following terms havethe definitions indicated.

Berkshire Hathaway Energy Company and Related EntitiesBHE Berkshire Hathaway Energy CompanyBerkshire Hathaway Energy or

the CompanyBerkshire Hathaway Energy Company and its subsidiaries

PacifiCorp PacifiCorp and its subsidiariesMidAmerican Funding MidAmerican Funding, LLC and its subsidiariesMidAmerican Energy MidAmerican Energy CompanyNV Energy NV Energy, Inc. and its subsidiariesNevada Power Nevada Power Company and its subsidiariesSierra Pacific Sierra Pacific Power Company and its subsidiariesNevada Utilities Nevada Power Company and Sierra Pacific Power CompanyRegistrants Berkshire Hathaway Energy Company, PacifiCorp, MidAmerican Funding,

MidAmerican Energy, Nevada Power and Sierra PacificSubsidiary Registrants PacifiCorp, MidAmerican Funding, MidAmerican Energy, Nevada Power and Sierra

PacificNorthern Powergrid Northern Powergrid Holdings CompanyNorthern Natural Gas Northern Natural Gas CompanyKern River Kern River Gas Transmission CompanyAltaLink BHE Canada Holdings CorporationALP AltaLink, L.P.BHE U.S. Transmission BHE U.S. Transmission, LLCHomeServices HomeServices of America, Inc. and its subsidiariesBHE Pipeline Group or

Pipeline CompaniesConsists of Northern Natural Gas and Kern River

BHE Transmission Consists of AltaLink and BHE U.S. TransmissionBHE Renewables Consists of BHE Renewables, LLC and CalEnergy PhilippinesUtilities PacifiCorp, MidAmerican Energy Company, Nevada Power Company and Sierra Pacific

Power CompanyBerkshire Hathaway Berkshire Hathaway Inc.

Certain Industry TermsAESO Alberta Electric System OperatorAFUDC Allowance for Funds Used During ConstructionAUC Alberta Utilities CommissionCPUC California Public Utilities CommissionDth DecathermsEPA United States Environmental Protection AgencyFERC Federal Energy Regulatory CommissionGHG Greenhouse GasesGWh Gigawatt HoursGTA General Tariff ApplicationIPUC Idaho Public Utilities CommissionIUB Iowa Utilities BoardkV KilovoltMW Megawatts

ii

MWh Megawatt HoursOPUC Oregon Public Utility CommissionPUCN Public Utilities Commission of NevadaREC Renewable Energy CreditRPS Renewable Portfolio StandardsSEC United States Securities and Exchange CommissionSIP State Implementation PlanUPSC Utah Public Service CommissionWPSC Wyoming Public Service CommissionWUTC Washington Utilities and Transportation Commission

iii

Forward-Looking Statements

This report contains statements that do not directly or exclusively relate to historical facts. These statements are "forward-lookingstatements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the SecuritiesExchange Act of 1934, as amended. Forward-looking statements can typically be identified by the use of forward-looking words,such as "will," "may," "could," "project," "believe," "anticipate," "expect," "estimate," "continue," "intend," "potential," "plan,""forecast" and similar terms. These statements are based upon the relevant Registrant's current intentions, assumptions, expectationsand beliefs and are subject to risks, uncertainties and other important factors. Many of these factors are outside the control of eachRegistrant and could cause actual results to differ materially from those expressed or implied by such forward-looking statements.These factors include, among others:

• general economic, political and business conditions, as well as changes in, and compliance with, laws and regulations,including income tax reform, initiatives regarding deregulation and restructuring of the utility industry, and reliabilityand safety standards, affecting the respective Registrant's operations or related industries;

• changes in, and compliance with, environmental laws, regulations, decisions and policies that could, among other items,increase operating and capital costs, reduce facility output, accelerate facility retirements or delay facility constructionor acquisition;

• the outcome of regulatory rate reviews and other proceedings conducted by regulatory agencies or other governmentaland legal bodies and the respective Registrant's ability to recover costs through rates in a timely manner;

• changes in economic, industry, competition or weather conditions, as well as demographic trends, new technologies andvarious conservation, energy efficiency and private generation measures and programs, that could affect customer growthand usage, electricity and natural gas supply or the respective Registrant's ability to obtain long-term contracts withcustomers and suppliers;

• performance, availability and ongoing operation of the respective Registrant's facilities, including facilities not operatedby the Registrants, due to the impacts of market conditions, outages and repairs, transmission constraints, weather,including wind, solar and hydroelectric conditions, and operating conditions;

• the effects of catastrophic and other unforeseen events, which may be caused by factors beyond the control of eachrespective Registrant or by a breakdown or failure of the Registrants' operating assets, including storms, floods, fires,earthquakes, explosions, landslides, mining accidents, litigation, wars, terrorism, embargoes, and cyber security attacks,data security breaches, disruptions, or other malicious acts;

• a high degree of variance between actual and forecasted load or generation that could impact a Registrant's hedgingstrategy and the cost of balancing its generation resources with its retail load obligations;

• changes in prices, availability and demand for wholesale electricity, coal, natural gas, other fuel sources and fueltransportation that could have a significant impact on generating capacity and energy costs;

• the financial condition and creditworthiness of the respective Registrant's significant customers and suppliers;

• changes in business strategy or development plans;

• availability, terms and deployment of capital, including reductions in demand for investment-grade commercial paper,debt securities and other sources of debt financing and volatility in interest rates;

• changes in the respective Registrant's credit ratings;

• risks relating to nuclear generation, including unique operational, closure and decommissioning risks;

• hydroelectric conditions and the cost, feasibility and eventual outcome of hydroelectric relicensing proceedings;

• the impact of certain contracts used to mitigate or manage volume, price and interest rate risk, including increased collateralrequirements, and changes in commodity prices, interest rates and other conditions that affect the fair value of certaincontracts;

• the impact of inflation on costs and the ability of the respective Registrants to recover such costs in regulated rates;

• fluctuations in foreign currency exchange rates, primarily the British pound and the Canadian dollar;

• increases in employee healthcare costs;

• the impact of investment performance and changes in interest rates, legislation, healthcare cost trends, mortality andmorbidity on pension and other postretirement benefits expense and funding requirements;

• changes in the residential real estate brokerage and mortgage industries and regulations that could affect brokerage andmortgage transactions;

• unanticipated construction delays, changes in costs, receipt of required permits and authorizations, ability to fund capitalprojects and other factors that could affect future facilities and infrastructure additions;

• the availability and price of natural gas in applicable geographic regions and demand for natural gas supply;

• the impact of new accounting guidance or changes in current accounting estimates and assumptions on the consolidatedfinancial results of the respective Registrants;

• the ability to successfully integrate future acquired operations into a Registrant's business; and

• other business or investment considerations that may be disclosed from time to time in the Registrants' filings with theSEC or in other publicly disseminated written documents.

Further details of the potential risks and uncertainties affecting the Registrants are described in the Registrants' filings with theSEC, including Part II, Item 1A and other discussions contained in this Form 10-Q. Each Registrant undertakes no obligation topublicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Theforegoing factors should not be construed as exclusive.

iv

Item 1. Financial Statements

Berkshire Hathaway Energy Company and its subsidiariesReport of Independent Registered Public Accounting Firm 4Consolidated Balance Sheets 5Consolidated Statements of Operations 7Consolidated Statements of Comprehensive Income 8Consolidated Statements of Changes in Equity 9Consolidated Statements of Cash Flows 10Notes to Consolidated Financial Statements 11

PacifiCorp and its subsidiariesReport of Independent Registered Public Accounting Firm 54Consolidated Balance Sheets 55Consolidated Statements of Operations 57Consolidated Statements of Changes in Shareholders' Equity 58Consolidated Statements of Cash Flows 59Notes to Consolidated Financial Statements 60

MidAmerican Energy CompanyReport of Independent Registered Public Accounting Firm 76Balance Sheets 77Statements of Operations 79Statements of Changes in Equity 80Statements of Cash Flows 81Notes to Financial Statements 82

MidAmerican Funding, LLC and its subsidiariesReport of Independent Registered Public Accounting Firm 91Consolidated Balance Sheets 92Consolidated Statements of Operations 94Consolidated Statements of Changes in Equity 95Consolidated Statements of Cash Flows 96Notes to Consolidated Financial Statements 97

Nevada Power Company and its subsidiariesReport of Independent Registered Public Accounting Firm 111Consolidated Balance Sheets 112Consolidated Statements of Operations 113Consolidated Statements of Changes in Shareholder's Equity 114Consolidated Statements of Cash Flows 115Notes to Consolidated Financial Statements 116

Sierra Pacific Power Company and its subsidiariesReport of Independent Registered Public Accounting Firm 132Consolidated Balance Sheets 133Consolidated Statements of Operations 134Consolidated Statements of Changes in Shareholder's Equity 135Consolidated Statements of Cash Flows 136Notes to Consolidated Financial Statements 137

1

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations

Berkshire Hathaway Energy Company and its subsidiaries 30PacifiCorp and its subsidiaries 68MidAmerican Funding, LLC and its subsidiaries and MidAmerican Energy Company 100Nevada Power Company and its subsidiaries 125Sierra Pacific Power Company and its subsidiaries 145

2

Berkshire Hathaway Energy Company and its subsidiaries Consolidated Financial Section

3

4

PART IItem 1. Financial Statements

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders ofBerkshire Hathaway Energy Company Des Moines, Iowa

We have reviewed the accompanying consolidated balance sheet of Berkshire Hathaway Energy Company and subsidiaries (the"Company") as of September 30, 2017, and the related consolidated statements of operations and comprehensive income for thethree-month and nine-month periods ended September 30, 2017 and 2016, and of changes in equity and cash flows for the nine-month periods ended September 30, 2017 and 2016. These interim financial statements are the responsibility of the Company'smanagement.

We conducted our reviews in accordance with the standards of the Public Company Accounting Oversight Board (United States).A review of interim financial information consists principally of applying analytical procedures and making inquiries of personsresponsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with thestandards of the Public Company Accounting Oversight Board (United States), the objective of which is the expression of anopinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our reviews, we are not aware of any material modifications that should be made to such consolidated interim financialstatements for them to be in conformity with accounting principles generally accepted in the United States of America.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States),the consolidated balance sheet of Berkshire Hathaway Energy Company and subsidiaries as of December 31, 2016, and the relatedconsolidated statements of operations, comprehensive income, changes in equity, and cash flows for the year then ended (notpresented herein); and in our report dated February 24, 2017, we expressed an unqualified opinion on those consolidated financialstatements. In our opinion, the information set forth in the accompanying consolidated balance sheet as of December 31, 2016 isfairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

/s/ Deloitte & Touche LLP

Des Moines, IowaNovember 3, 2017

BERKSHIRE HATHAWAY ENERGY COMPANY AND SUBSIDIARIESCONSOLIDATED BALANCE SHEETS (Unaudited)

(Amounts in millions)

As ofSeptember 30, December 31,

2017 2016ASSETS

Current assets:Cash and cash equivalents $ 1,142 $ 721Trade receivables, net 1,994 1,751Inventories 887 925Mortgage loans held for sale 534 359Other current assets 1,095 917

Total current assets 5,652 4,673

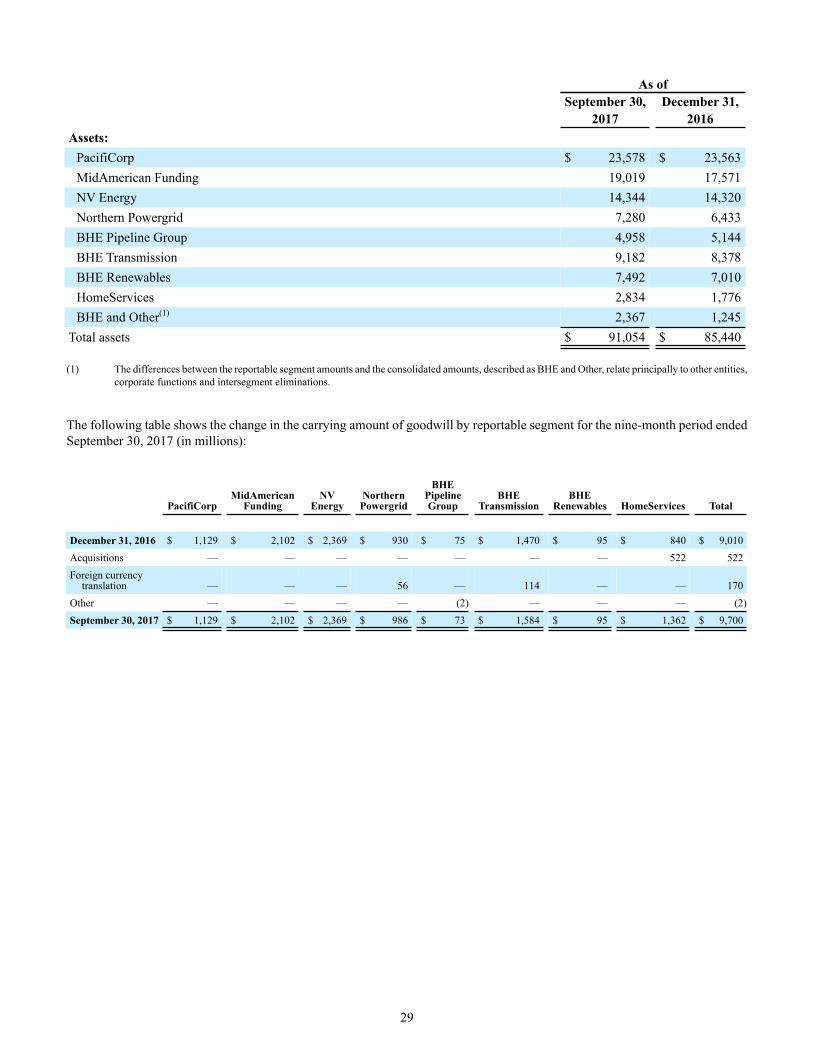

Property, plant and equipment, net 64,979 62,509Goodwill 9,700 9,010Regulatory assets 4,582 4,307Investments and restricted cash and investments 4,987 3,945Other assets 1,154 996

Total assets $ 91,054 $ 85,440

The accompanying notes are an integral part of these consolidated financial statements.

5

BERKSHIRE HATHAWAY ENERGY COMPANY AND SUBSIDIARIESCONSOLIDATED BALANCE SHEETS (Unaudited) (continued)

(Amounts in millions)

As ofSeptember 30, December 31,

2017 2016LIABILITIES AND EQUITY

Current liabilities:Accounts payable $ 1,303 $ 1,317Accrued interest 523 454Accrued property, income and other taxes 780 389Accrued employee expenses 392 261Short-term debt 2,493 1,869Current portion of long-term debt 3,070 1,006Other current liabilities 1,034 1,017

Total current liabilities 9,595 6,313

Regulatory liabilities 3,086 2,933BHE senior debt 6,771 7,418BHE junior subordinated debentures 100 944Subsidiary debt 26,183 26,748Deferred income taxes 14,832 13,879Other long-term liabilities 2,883 2,742

Total liabilities 63,450 60,977

Commitments and contingencies (Note 11)

Equity:BHE shareholders' equity:

Common stock - 115 shares authorized, no par value, 77 shares issued and outstanding — —Additional paid-in capital 6,362 6,390Retained earnings 21,534 19,448Accumulated other comprehensive loss, net (423) (1,511)

Total BHE shareholders' equity 27,473 24,327Noncontrolling interests 131 136

Total equity 27,604 24,463

Total liabilities and equity $ 91,054 $ 85,440

The accompanying notes are an integral part of these consolidated financial statements.

6

BERKSHIRE HATHAWAY ENERGY COMPANY AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(Amounts in millions)

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

2017 2016 2017 2016Operating revenue:

Energy $ 4,322 $ 4,272 $ 11,501 $ 11,102Real estate 961 820 2,502 2,152

Total operating revenue 5,283 5,092 14,003 13,254

Operating costs and expenses:Energy:

Cost of sales 1,212 1,187 3,380 3,252Operating expense 930 948 2,763 2,739Depreciation and amortization 635 639 1,905 1,898

Real estate 882 733 2,311 1,973Total operating costs and expenses 3,659 3,507 10,359 9,862

Operating income 1,624 1,585 3,644 3,392

Other income (expense):Interest expense (464) (460) (1,379) (1,401)Capitalized interest 14 14 34 128Allowance for equity funds 24 17 59 147Interest and dividend income 32 39 85 93Other, net 2 15 24 26

Total other income (expense) (392) (375) (1,177) (1,007)

Income before income tax expense and equity income 1,232 1,210 2,467 2,385Income tax expense 184 199 319 394Equity income 30 36 80 96

Net income 1,078 1,047 2,228 2,087Net income attributable to noncontrolling interests 10 11 30 25

Net income attributable to BHE shareholders $ 1,068 $ 1,036 $ 2,198 $ 2,062

The accompanying notes are an integral part of these consolidated financial statements.

7

BERKSHIRE HATHAWAY ENERGY COMPANY AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (Unaudited)

(Amounts in millions)

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

2017 2016 2017 2016

Net income $ 1,078 $ 1,047 $ 2,228 $ 2,087

Other comprehensive income, net of tax:Unrecognized amounts on retirement benefits, net of tax of $1, $7,

$(3), and $26 15 18 16 80Foreign currency translation adjustment 227 (134) 535 (339)Unrealized gains on available-for-sale securities, net of tax of

$284, $53, $355 and $89 423 80 542 151Unrealized gains (losses) on cash flow hedges, net of tax of $1,

$(3), $(3) and $(1) 1 (3) (5) (2)Total other comprehensive income, net of tax 666 (39) 1,088 (110)

Comprehensive income 1,744 1,008 3,316 1,977Comprehensive income attributable to noncontrolling interests 10 11 30 25

Comprehensive income attributable to BHE shareholders $ 1,734 $ 997 $ 3,286 $ 1,952

The accompanying notes are an integral part of these consolidated financial statements.

8

BERKSHIRE HATHAWAY ENERGY COMPANY AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CHANGES IN EQUITY (Unaudited)

(Amounts in millions)

BHE Shareholders' EquityAccumulated

Additional OtherCommon Paid-in Retained Comprehensive Noncontrolling Total

Shares Stock Capital Earnings Loss, Net Interests Equity

Balance, December 31, 2015 77 $ — $ 6,403 $ 16,906 $ (908) $ 134 $ 22,535

Net income — — — 2,062 — 14 2,076

Other comprehensive loss — — — — (110) — (110)

Distributions — — — — — (14) (14)

Other equity transactions — — 1 — — 8 9

Balance, September 30, 2016 77 $ — $ 6,404 $ 18,968 $ (1,018) $ 142 $ 24,496

Balance, December 31, 2016 77 $ — $ 6,390 $ 19,448 $ (1,511) $ 136 $ 24,463

Net income — — — 2,198 — 14 2,212

Other comprehensive income — — — — 1,088 — 1,088

Distributions — — — — — (16) (16)

Common stock purchases — — (1) (18) — — (19)

Common stock exchange — — (6) (94) — — (100)

Other equity transactions — — (21) — — (3) (24)

Balance, September 30, 2017 77 $ — $ 6,362 $ 21,534 $ (423) $ 131 $ 27,604

The accompanying notes are an integral part of these consolidated financial statements.

9

BERKSHIRE HATHAWAY ENERGY COMPANY AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(Amounts in millions)

Nine-Month PeriodsEnded September 30,

2017 2016Cash flows from operating activities:

Net income $ 2,228 $ 2,087Adjustments to reconcile net income to net cash flows from operating activities:

Depreciation and amortization 1,943 1,922Allowance for equity funds (59) (147)Equity income, net of distributions (14) (62)Changes in regulatory assets and liabilities 17 41Deferred income taxes and amortization of investment tax credits 573 546Other, net 13 (60)Changes in other operating assets and liabilities, net of effects from acquisitions:

Trade receivables and other assets (98) (348)Derivative collateral, net (16) 22Pension and other postretirement benefit plans (29) (73)Accrued property, income and other taxes 390 713Accounts payable and other liabilities 170 183

Net cash flows from operating activities 5,118 4,824

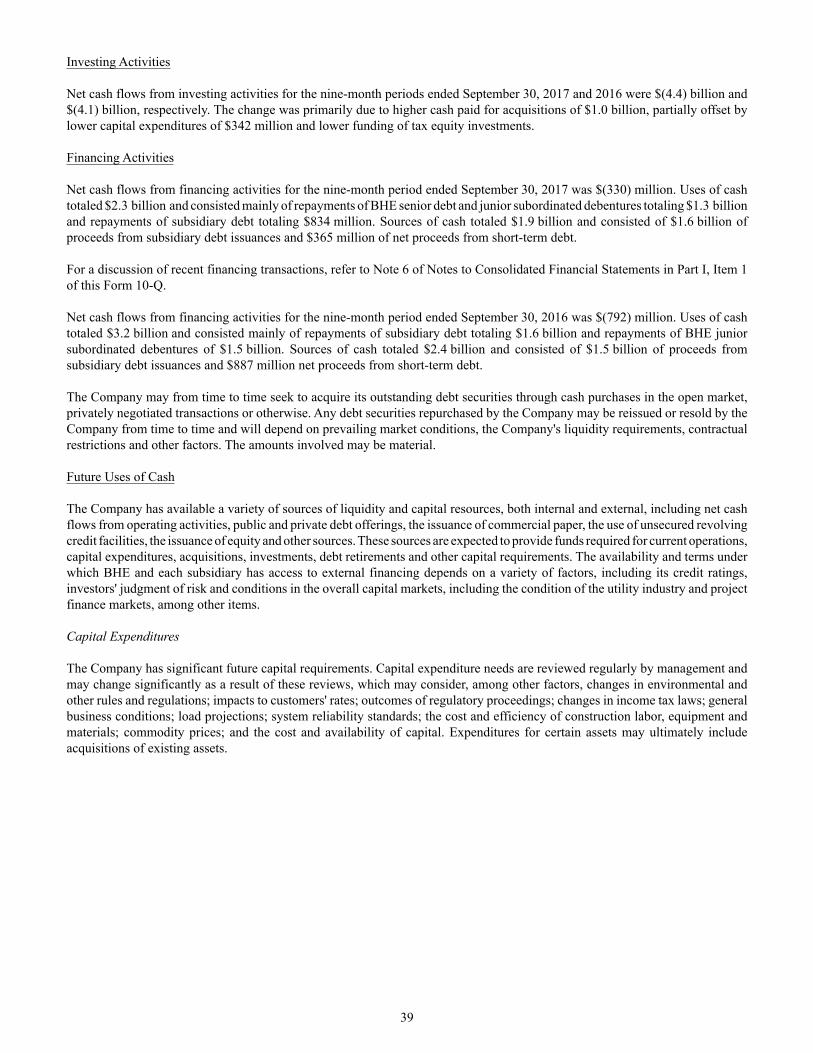

Cash flows from investing activities:Capital expenditures (3,179) (3,521)Acquisitions, net of cash acquired (1,102) (66)Increase in restricted cash and investments (45) (48)Purchases of available-for-sale securities (167) (98)Proceeds from sales of available-for-sale securities 186 125Equity method investments (54) (462)Other, net (12) (47)

Net cash flows from investing activities (4,373) (4,117)

Cash flows from financing activities:Repayments of BHE senior debt and junior subordinated debentures (1,344) (1,500)Common stock purchases (19) —Proceeds from subsidiary debt 1,562 1,484Repayments of subsidiary debt (834) (1,613)Net proceeds from short-term debt 365 887Other, net (60) (50)

Net cash flows from financing activities (330) (792)

Effect of exchange rate changes 6 (5)

Net change in cash and cash equivalents 421 (90)Cash and cash equivalents at beginning of period 721 1,108Cash and cash equivalents at end of period $ 1,142 $ 1,018

The accompanying notes are an integral part of these consolidated financial statements.

10

BERKSHIRE HATHAWAY ENERGY COMPANY AND SUBSIDIARIESNOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

11

(1) General

Berkshire Hathaway Energy Company ("BHE") is a holding company that owns a highly diversified portfolio of locally-managedbusinesses principally engaged in the energy industry (collectively with its subsidiaries, the "Company") and is a consolidatedsubsidiary of Berkshire Hathaway Inc. ("Berkshire Hathaway").

The Company is organized as eight business segments: PacifiCorp, MidAmerican Funding, LLC ("MidAmerican Funding") (whichprimarily consists of MidAmerican Energy Company ("MidAmerican Energy")), NV Energy, Inc. ("NV Energy") (which primarilyconsists of Nevada Power Company ("Nevada Power") and Sierra Pacific Power Company ("Sierra Pacific")), Northern PowergridHoldings Company ("Northern Powergrid") (which primarily consists of Northern Powergrid (Northeast) Limited and NorthernPowergrid (Yorkshire) plc), BHE Pipeline Group (which consists of Northern Natural Gas Company ("Northern Natural Gas")and Kern River Gas Transmission Company ("Kern River")), BHE Transmission (which consists of BHE Canada HoldingsCorporation ("AltaLink") (which primarily consists of AltaLink, L.P. ("ALP")) and BHE U.S. Transmission, LLC), BHERenewables (which primarily consists of BHE Renewables, LLC and CalEnergy Philippines) and HomeServices of America, Inc.(collectively with its subsidiaries, "HomeServices"). The Company, through these locally managed and operated businesses, ownsfour utility companies in the United States serving customers in 11 states, two electricity distribution companies in Great Britain,two interstate natural gas pipeline companies in the United States, an electric transmission business in Canada, interests in electrictransmission businesses in the United States, a renewable energy business primarily selling power generated from solar, wind,geothermal and hydroelectric sources under long-term contracts, the second largest residential real estate brokerage firm in theUnited States and one of the largest residential real estate brokerage franchise networks in the United States.

The unaudited Consolidated Financial Statements have been prepared in accordance with accounting principles generally acceptedin the United States of America ("GAAP") for interim financial information and the United States Securities and ExchangeCommission's rules and regulations for Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of thedisclosures required by GAAP for annual financial statements. Management believes the unaudited Consolidated FinancialStatements contain all adjustments (consisting only of normal recurring adjustments) considered necessary for the fair presentationof the unaudited Consolidated Financial Statements as of September 30, 2017 and for the three- and nine-month periods endedSeptember 30, 2017 and 2016. The results of operations for the three- and nine-month periods ended September 30, 2017 are notnecessarily indicative of the results to be expected for the full year.

The preparation of the unaudited Consolidated Financial Statements in conformity with GAAP requires management to makeestimates and assumptions that affect the reported amounts of assets and liabilities at the date of the unaudited ConsolidatedFinancial Statements and the reported amounts of revenue and expenses during the period. Actual results may differ from theestimates used in preparing the unaudited Consolidated Financial Statements. Note 2 of Notes to Consolidated Financial Statementsincluded in the Company's Annual Report on Form 10-K for the year ended December 31, 2016 describes the most significantaccounting policies used in the preparation of the unaudited Consolidated Financial Statements. There have been no significantchanges in the Company's assumptions regarding significant accounting estimates and policies during the nine-month period endedSeptember 30, 2017.

(2) New Accounting Pronouncements

In August 2017, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") No. 2017-12,which amends FASB Accounting Standards Codification ("ASC") Topic 815, "Derivatives and Hedging." The amendments in thisguidance update the hedge accounting model to enable entities to better portray the economics of their risk management activitiesin the financial statements, expands an entity’s ability to hedge non-financial and financial risk components and reduces complexityin fair value hedges of interest rate risk. In addition, it eliminates the requirement to separately measure and report hedgeineffectiveness and generally requires the entire change in fair value of a hedging instrument to be presented in the same incomestatement line as the hedged item and also eases certain documentation and assessment requirements. This guidance is effectivefor interim and annual reporting periods beginning after December 15, 2018, with early adoption permitted, and is required to beadopted using a modified retrospective approach by means of a cumulative-effect adjustment to retained earnings as of the beginningof the fiscal year of adoption. The Company is currently evaluating the impact of adopting this guidance on its ConsolidatedFinancial Statements and disclosures included within Notes to Consolidated Financial Statements.

In March 2017, the FASB issued ASU No. 2017-07, which amends FASB ASC Topic 715, "Compensation - Retirement Benefits."The amendments in this guidance require that an employer disaggregate the service cost component from the other componentsof net benefit cost and report the service cost component in the same line item as other compensation costs arising from servicesrendered by the pertinent employees during the period. The other components of net benefit cost are required to be presented inthe statement of operations separately from the service cost component and outside the subtotal of operating income. Additionally,the guidance only allows the service cost component to be eligible for capitalization when applicable. This guidance is effectivefor interim and annual reporting periods beginning after December 15, 2017, with early adoption permitted. This guidance mustbe adopted retrospectively for the presentation of the service cost component and the other components of net benefit cost in thestatement of operations and prospectively for the capitalization of the service cost component in the balance sheet. The Companyplans to adopt this guidance effective January 1, 2018. The Company does not believe this will have a material impact on itsConsolidated Financial Statements and disclosures included within Notes to Consolidated Financial Statements.

In November 2016, the FASB issued ASU No. 2016-18, which amends FASB ASC Subtopic 230-10, "Statement of Cash Flows- Overall." The amendments in this guidance require that a statement of cash flows explain the change during the period in thetotal of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. Amounts generallydescribed as restricted cash and restricted cash equivalents should be included with cash and cash equivalents when reconcilingthe beginning-of-period and end-of-period total amounts shown on the statement of cash flows. This guidance is effective forinterim and annual reporting periods beginning after December 15, 2017, with early adoption permitted, and is required to beadopted retrospectively. The Company plans to adopt this guidance effective January 1, 2018 and does not believe the adoptionof this guidance will have a material impact on its Consolidated Financial Statements and disclosures included within Notes toConsolidated Financial Statements.

In August 2016, the FASB issued ASU No. 2016-15, which amends FASB ASC Topic 230, "Statement of Cash Flows." Theamendments in this guidance address the classification of eight specific cash flow issues within the statement of cash flows withthe objective of reducing the existing diversity in practice. This guidance is effective for interim and annual reporting periodsbeginning after December 15, 2017, with early adoption permitted, and is required to be adopted retrospectively. The Companyplans to adopt this guidance effective January 1, 2018 and does not believe the adoption of this guidance will have a materialimpact on its Consolidated Financial Statements.

In February 2016, the FASB issued ASU No. 2016-02, which creates FASB ASC Topic 842, "Leases" and supersedes Topic 840"Leases." This guidance increases transparency and comparability among entities by recording lease assets and lease liabilitieson the balance sheet and disclosing key information about leasing arrangements. A lessee should recognize in the balance sheet aliability to make lease payments (the lease liability) and a right-of-use asset representing its right to use the underlying asset forthe lease term. The recognition, measurement, and presentation of expenses and cash flows arising from a lease by a lessee havenot significantly changed from previous guidance. This guidance is effective for interim and annual reporting periods beginningafter December 15, 2018, with early adoption permitted, and is required to be adopted using a modified retrospective approach.The Company plans to adopt this guidance effective January 1, 2019 and is currently evaluating the impact on its ConsolidatedFinancial Statements and disclosures included within Notes to Consolidated Financial Statements.

In January 2016, the FASB issued ASU No. 2016-01, which amends FASB ASC Subtopic 825-10, "Financial Instruments - Overall."The amendments in this guidance address certain aspects of recognition, measurement, presentation and disclosure of financialinstruments including a requirement that all investments in equity securities that do not qualify for equity method accounting orresult in consolidation of the investee be measured at fair value with changes in fair value recognized in net income. This guidanceis effective for interim and annual reporting periods beginning after December 15, 2017, with early adoption not permitted, andis required to be adopted prospectively by means of a cumulative-effect adjustment to the balance sheet as of the beginning of thefiscal year of adoption. The Company is currently evaluating the impact of adopting this guidance on its Consolidated FinancialStatements and disclosures included within Notes to Consolidated Financial Statements. The material impacts currently identifiedinclude recording the unrealized gains and losses on available-for-sale securities in the Consolidated Statements of Operations asopposed to other comprehensive income ("OCI"). For the nine-month periods ended September 30, 2017 and 2016, these amounts,net of tax, were 542 million and 151 million, respectively.

12

In May 2014, the FASB issued ASU No. 2014-09, which creates FASB ASC Topic 606, "Revenue from Contracts with Customers"and supersedes ASC Topic 605, "Revenue Recognition." The guidance replaces industry-specific guidance and establishes a singlefive-step model to identify and recognize revenue. The core principle of the guidance is that an entity should recognize revenueupon transfer of control of promised goods or services to customers in an amount that reflects the consideration to which an entityexpects to be entitled in exchange for those goods or services. Additionally, the guidance requires the entity to disclose furtherquantitative and qualitative information regarding the nature and amount of revenues arising from contracts with customers, aswell as other information about the significant judgments and estimates used in recognizing revenues from contracts with customers.In August 2015, the FASB issued ASU No. 2015-14, which defers the effective date of ASU No. 2014-09 one year to interim andannual reporting periods beginning after December 15, 2017. During 2016 and 2017, the FASB issued several ASUs that clarifythe implementation guidance for ASU No. 2014-09 but do not change the core principle of the guidance. This guidance may beadopted retrospectively or under a modified retrospective method where the cumulative effect is recognized at the date of initialapplication. The Company plans to adopt this guidance effective January 1, 2018 under the modified retrospective method and iscurrently evaluating the impact on its Consolidated Financial Statements and disclosures included within Notes to ConsolidatedFinancial Statements. The Company currently does not expect the timing and amount of revenue currently recognized to bematerially different after adoption of the new guidance as a majority of revenue is recognized when the Company has the right toinvoice as it corresponds directly with the value to the customer of the Company’s performance to date. The Company's currentplan is to quantitatively disaggregate revenue in the required financial statement footnote by regulated energy, nonregulated energyand real estate, with further disaggregation of regulated energy by jurisdiction and real estate by line of business.

13

(3) Business Acquisitions

The Company completed various acquisitions totaling $1.1 billion, net of cash acquired, for the nine-month period endedSeptember 30, 2017. The purchase price for each acquisition was allocated to the assets acquired and liabilities assumed, whichprimarily related to residential real estate brokerage businesses, development and construction costs for the 110-megawatt Alamo6 solar project and the 50-megawatt Pearl solar project, and the remaining 25% interest in the Silverhawk natural gas-fueledgeneration facility at Nevada Power. As a result of the various acquisitions, the Company acquired assets of $1.1 billion, assumedliabilities of $476 million and recognized goodwill of $522 million.

(4) Property, Plant and Equipment, Net

Property, plant and equipment, net consists of the following (in millions):

As ofDepreciable September 30, December 31,

Life 2017 2016Regulated assets:

Utility generation, transmission and distribution systems 5-80 years $ 73,138 $ 71,536Interstate natural gas pipeline assets 3-80 years 6,991 6,942

80,129 78,478Accumulated depreciation and amortization (24,525) (23,603)

Regulated assets, net 55,604 54,875

Nonregulated assets:Independent power plants 5-30 years 5,911 5,594Other assets 3-30 years 1,265 1,002

7,176 6,596Accumulated depreciation and amortization (1,304) (1,060)

Nonregulated assets, net 5,872 5,536

Net operating assets 61,476 60,411Construction work-in-progress 3,503 2,098

Property, plant and equipment, net $ 64,979 $ 62,509

Construction work-in-progress includes $3.1 billion as of September 30, 2017 and $1.8 billion as of December 31, 2016, relatedto the construction of regulated assets.

During the fourth quarter of 2016, MidAmerican Energy revised its electric and gas depreciation rates based on the results of anew depreciation study, the most significant impact of which was longer estimated useful lives for certain wind-powered generatingfacilities. The effect of this change was to reduce depreciation and amortization expense by $34 million annually, or $9 millionand $26 million for the three- and nine-month periods ended September 30, 2017, based on depreciable plant balances at the timeof the change.

14

(5) Investments and Restricted Cash and Investments

Investments and restricted cash and investments consists of the following (in millions):

As ofSeptember 30, December 31,

2017 2016Investments:

BYD Company Limited common stock $ 2,087 $ 1,185Rabbi trusts 431 403Other 132 106

Total investments 2,650 1,694

Equity method investments:BHE Renewables tax equity investments 804 741Electric Transmission Texas, LLC 693 672Bridger Coal Company 140 165Other 158 142

Total equity method investments 1,795 1,720

Restricted cash and investments:Quad Cities Station nuclear decommissioning trust funds 498 460Other 317 282

Total restricted cash and investments 815 742

Total investments and restricted cash and investments $ 5,260 $ 4,156

Reflected as:Other current assets $ 273 $ 211Noncurrent assets 4,987 3,945

Total investments and restricted cash and investments $ 5,260 $ 4,156

Investments

BHE's investment in BYD Company Limited common stock is accounted for as an available-for-sale security with changes in fairvalue recognized in accumulated other comprehensive income (loss) ("AOCI"). The fair value of BHE's investment in BYDCompany Limited common stock reflects a pre-tax unrealized gain of $1,855 million and $953 million as of September 30, 2017and December 31, 2016, respectively.

(6) Recent Financing Transactions

Long-Term Debt

In the first nine months of 2017, BHE repaid at par value a total of $944 million, plus accrued interest, of its junior subordinateddebentures due December 2044.

In September 2017, HomeServices entered into a $250 million unsecured amortizing term loan due September 2022. The amortizingterm loan has an underlying variable interest rate based on the London Interbank Offered Rate ("LIBOR") plus a spread that variesbased on HomeServices' total net leverage ratio as of the last day of each quarter. The net proceeds were used to fund the repaymentor reimbursement of amounts provided by BHE for the costs related to acquisitions.

In July 2017, Northern Powergrid Metering Limited entered into a £200 million secured amortizing corporate facility with a statedmaturity of June 2026. The amortizing facility has a variable interest rate based on the LIBOR plus a spread that varies based onan agreed-upon schedule. In July 2017, Northern Powergrid Metering Limited received proceeds of £120 million under the facilityto repay amounts provided by Yorkshire Electricity Group plc which provides internal funds for the continuing smart meterdeployment program of Northern Powergrid Metering Limited. Northern Powergrid Metering Limited has entered into interestrate swaps that fix the underlying interest rate on 85% of the outstanding debt.

In July 2017, Cordova Funding Corporation redeemed the remaining $89 million of its 8.48% to 9.07% Series A Senior SecuredBonds due December 2019, CE Generation, LLC redeemed the remaining $51 million of its 7.416% Senior Secured Bonds dueDecember 2018, and Salton Sea Funding Corporation redeemed the remaining $20 million of its 7.475% Senior Secured SeriesF Bonds due November 2018, each at redemption prices determined in accordance with the terms of the respective indentures.

In June 2017, BHE issued $100 million of its 5.0% junior subordinated debentures due June 2057 in exchange for 181,819 sharesof BHE no par value common stock held by a minority shareholder. The junior subordinated debentures are redeemable at BHE'soption at any time from and after June 15, 2037, at par plus accrued and unpaid interest.

In May 2017, Alamo 6, LLC issued $232 million of its 4.17% Senior Secured Notes due March 2042. The principal of the notesamortizes beginning March 2018 with a final maturity in March 2042. The net proceeds were used to fund the repayment orreimbursement of amounts provided by BHE for the costs related to the development, construction and financing of a 110-megawattsolar project in Texas.

In April 2017, Kern River redeemed the remaining $175 million of its 4.893% Senior Notes due April 2018 at a redemption pricedetermined in accordance with the terms of the indenture.

In February 2017, MidAmerican Energy issued $375 million of its 3.10% First Mortgage Bonds due May 2027 and $475 millionof its 3.95% First Mortgage Bonds due August 2047. An amount equal to the net proceeds was used to finance capital expenditures,disbursed during the period from February 2, 2016 to February 1, 2017, with respect to investments in MidAmerican Energy's551-megawatt Wind X and 2,000-megawatt Wind XI projects, which were previously financed with MidAmerican Energy's generalfunds.

In February 2017, MidAmerican Energy redeemed in full through optional redemption its $250 million of 5.95% Senior Notesdue July 2017.

Credit Facilities

In September 2017, HomeServices terminated its $350 million unsecured credit facility expiring July 2018 and entered into a $600million unsecured credit facility expiring September 2022. The credit facility, which is for general corporate purposes and providesfor the issuance of letters of credit, has a variable interest rate based on the LIBOR or a base rate, at HomeServices' option, plusa spread that varies based on HomeServices' total net leverage ratio as of the last day of each quarter.

In June 2017, BHE extended, with lender consent, the maturity date to June 2020 for its $2.0 billion unsecured credit facility andPacifiCorp extended, with lender consent, the maturity date to June 2020 for its $400 million unsecured credit facility, each byexercising the first of two available one-year extensions.

15

In June 2017, PacifiCorp terminated its $600 million unsecured credit facility expiring March 2018 and entered into a $600 millionunsecured credit facility expiring June 2020 with two one-year extension options subject to lender consent. The credit facility,which supports PacifiCorp's commercial paper program and certain series of its tax-exempt bond obligations and provides for theissuance of letters of credit, has a variable interest rate based on the Eurodollar rate or a base rate, at PacifiCorp's option, plus aspread that varies based on PacifiCorp's credit ratings for its senior unsecured long-term debt securities. The credit facility requiresPacifiCorp's ratio of consolidated debt, including current maturities, to total capitalization not exceed 0.65 to 1.0 as of the last dayof each quarter.

In June 2017, MidAmerican Energy terminated its $600 million unsecured credit facility expiring March 2018 and entered into a$900 million unsecured credit facility expiring June 2020 with two one-year extension options subject to lender consent. The creditfacility, which supports MidAmerican Energy's commercial paper program and its variable-rate tax-exempt bond obligations andprovides for the issuance of letters of credit, has a variable interest rate based on the Eurodollar rate or a base rate, at MidAmericanEnergy's option, plus a spread that varies based on MidAmerican Energy's credit ratings for senior unsecured long-term debtsecurities. The credit facility requires MidAmerican Energy's ratio of consolidated debt, including current maturities, to totalcapitalization not exceed 0.65 to 1.0 as of the last day of each quarter.

In June 2017, Nevada Power amended its $400 million secured credit facility, extending the maturity date to June 2020 with twoone-year extension options subject to lender consent. The amended credit facility, which is for general corporate purposes andprovides for the issuance of letters of credit, has a variable interest rate based on the Eurodollar rate or a base rate, at NevadaPower's option, plus a spread that varies based on Nevada Power's credit ratings for its senior secured long-term debt securities.The amended credit facility requires Nevada Power's ratio of consolidated debt, including current maturities, to totalcapitalization not to exceed 0.65 to 1.0 as of the last day of each quarter.

In June 2017, Sierra Pacific amended its $250 million secured credit facility, extending the maturity date to June 2020 with twoone-year extension options subject to lender consent. The amended credit facility, which is for general corporate purposes andprovides for the issuance of letters of credit, has a variable interest rate based on the Eurodollar rate or a base rate, at Sierra Pacific'soption, plus a spread that varies based on Sierra Pacific's credit ratings for its senior secured long-term debt securities. The amendedcredit facility requires Sierra Pacific's ratio of consolidated debt, including current maturities, to total capitalization not exceed0.65 to 1.0 as of the last day of each quarter.

In May 2017, BHE entered into a $1.0 billion unsecured credit facility expiring May 2018. The credit facility, which is for generalcorporate purposes and also supports BHE's commercial paper program and provides for the issuance of letters of credit, has avariable interest rate based on the Eurodollar rate or a base rate, at BHE's option, plus a spread that varies based on BHE's creditratings for its senior unsecured long-term debt securities. The credit facility requires BHE's ratio of consolidated debt, includingcurrent maturities, to total capitalization not exceed 0.70 to 1.0 as of the last day of each quarter.

16

(7) Income Taxes

A reconciliation of the federal statutory income tax rate to the effective income tax rate applicable to income before income taxexpense is as follows:

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

2017 2016 2017 2016

Federal statutory income tax rate 35% 35% 35% 35%Income tax credits (19) (16) (18) (15)State income tax, net of federal income tax benefit — — (1) —Income tax effect of foreign income (3) (3) (4) (4)Equity income 1 1 1 1Other, net 1 (1) — —

Effective income tax rate 15% 16% 13% 17%

Income tax credits relate primarily to production tax credits from wind-powered generating facilities owned by MidAmericanEnergy, PacifiCorp and BHE Renewables. Federal renewable electricity production tax credits are earned as energy from qualifyingwind-powered generating facilities is produced and sold and are based on a per-kilowatt hour rate pursuant to the applicable federalincome tax law. Wind-powered generating facilities are eligible for the credits for 10 years from the date the qualifying generatingfacilities are placed in-service.

Berkshire Hathaway includes the Company in its United States federal income tax return. The Company's provision for incometaxes has been computed on a stand-alone basis, and substantially all of its currently payable or receivable federal income taxesare remitted to or received from Berkshire Hathaway. For the nine-month periods ended September 30, 2017 and 2016, the Companyreceived net cash payments for federal income taxes from Berkshire Hathaway totaling $659 million and $860 million, respectively.

17

(8) Employee Benefit Plans

Domestic Operations

Net periodic benefit cost (credit) for the domestic pension and other postretirement benefit plans included the following components(in millions):

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

2017 2016 2017 2016Pension:

Service cost $ 6 $ 7 $ 18 $ 22Interest cost 29 31 87 94Expected return on plan assets (40) (39) (120) (120)Net amortization 7 12 22 36

Net periodic benefit cost $ 2 $ 11 $ 7 $ 32

Other postretirement:Service cost $ 3 $ 2 $ 7 $ 7Interest cost 7 7 21 23Expected return on plan assets (9) (10) (30) (31)Net amortization (3) (2) (10) (9)

Net periodic benefit credit $ (2) $ (3) $ (12) $ (10)

Employer contributions to the domestic pension and other postretirement benefit plans are expected to be $15 million and $5million, respectively, during 2017. As of September 30, 2017, $9 million and $5 million of contributions had been made to thedomestic pension and other postretirement benefit plans, respectively.

Foreign Operations

Net periodic benefit cost for the United Kingdom pension plan included the following components (in millions):

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

2017 2016 2017 2016

Service cost $ 6 $ 5 $ 19 $ 16Interest cost 15 17 44 55Expected return on plan assets (25) (27) (74) (85)Settlement 18 — 18 —Net amortization 17 11 50 34

Net periodic benefit cost $ 31 $ 6 $ 57 $ 20

Employer contributions to the United Kingdom pension plan are expected to be £45 million during 2017. As of September 30,2017, £34 million, or $43 million, of contributions had been made to the United Kingdom pension plan.

18

(9) Risk Management and Hedging Activities

The Company is exposed to the impact of market fluctuations in commodity prices, interest rates and foreign currency exchangerates. The Company is principally exposed to electricity, natural gas, coal and fuel oil commodity price risk primarily throughBHE's ownership of PacifiCorp, MidAmerican Energy, Nevada Power and Sierra Pacific (the "Utilities") as they have an obligationto serve retail customer load in their regulated service territories. The Company also provides nonregulated retail electricity andnatural gas services in competitive markets. The Utilities' load and generating facilities represent substantial underlying commoditypositions. Exposures to commodity prices consist mainly of variations in the price of fuel required to generate electricity, wholesaleelectricity that is purchased and sold, and natural gas supply for retail customers. Commodity prices are subject to wide priceswings as supply and demand are impacted by, among many other unpredictable items, weather, market liquidity, generatingfacility availability, customer usage, storage, and transmission and transportation constraints. Interest rate risk exists on variable-rate debt, future debt issuances and mortgage commitments. Additionally, the Company is exposed to foreign currency exchangerate risk from its business operations and investments in Great Britain and Canada. The Company does not engage in a materialamount of proprietary trading activities.

Each of the Company's business platforms has established a risk management process that is designed to identify, assess, manage,monitor and report each of the various types of risk involved in its business. To mitigate a portion of its commodity price risk,the Company uses commodity derivative contracts, which may include forwards, futures, options, swaps and other agreements,to effectively secure future supply or sell future production generally at fixed prices. The Company manages its interest rate riskby limiting its exposure to variable interest rates primarily through the issuance of fixed-rate long-term debt and by monitoringmarket changes in interest rates. Additionally, the Company may from time to time enter into interest rate derivative contracts,such as interest rate swaps or locks, forward sale commitments, or mortgage interest rate lock commitments, to mitigate theCompany's exposure to interest rate risk. The Company does not hedge all of its commodity price, interest rate and foreigncurrency exchange rate risks, thereby exposing the unhedged portion to changes in market prices.

There have been no significant changes in the Company's accounting policies related to derivatives. Refer to Note 10 for additionalinformation on derivative contracts.

The following table, which reflects master netting arrangements and excludes contracts that have been designated as normal underthe normal purchases or normal sales exception afforded by GAAP, summarizes the fair value of the Company's derivative contracts,on a gross basis, and reconciles those amounts to the amounts presented on a net basis on the Consolidated Balance Sheets(in millions):

Other Other OtherCurrent Other Current Long-termAssets Assets Liabilities Liabilities Total

As of September 30, 2017Not designated as hedging contracts:

Commodity assets(1) $ 16 $ 93 $ 7 $ 3 $ 119Commodity liabilities(1) (1) — (60) (135) (196)Interest rate assets 22 — — — 22Interest rate liabilities — — (3) (7) (10)

Total 37 93 (56) (139) (65)

Designated as hedging contracts:Commodity assets — — 2 6 8Commodity liabilities — — (11) (17) (28)Interest rate assets — 6 — — 6Interest rate liabilities — — (1) — (1)

Total — 6 (10) (11) (15)

Total derivatives 37 99 (66) (150) (80)Cash collateral receivable — — 21 64 85

Total derivatives - net basis $ 37 $ 99 $ (45) $ (86) $ 5

Other Other OtherCurrent Other Current Long-termAssets Assets Liabilities Liabilities Total

As of December 31, 2016Not designated as hedging contracts:

Commodity assets(1) $ 42 $ 86 $ 5 $ 2 $ 135Commodity liabilities(1) (10) — (46) (150) (206)Interest rate assets 15 — — — 15Interest rate liabilities — — (4) (6) (10)

Total 47 86 (45) (154) (66)

Designated as hedging contracts:Commodity assets 1 — 2 3 6Commodity liabilities — — (14) (8) (22)Interest rate assets — 8 — — 8Interest rate liabilities — — (3) — (3)

Total 1 8 (15) (5) (11)

Total derivatives 48 94 (60) (159) (77)Cash collateral receivable — — 13 61 74

Total derivatives - net basis $ 48 $ 94 $ (47) $ (98) $ (3) (1) The Company's commodity derivatives not designated as hedging contracts are generally included in regulated rates, and as of September 30, 2017

and December 31, 2016, a net regulatory asset of $162 million and $148 million, respectively, was recorded related to the net derivative liability of$77 million and $71 million, respectively. The difference between the net regulatory asset and the net derivative liability relates primarily to a powerpurchase agreement derivative at BHE Renewables.

19

Not Designated as Hedging Contracts

The following table reconciles the beginning and ending balances of the Company's net regulatory assets and summarizes the pre-tax gains and losses on commodity derivative contracts recognized in net regulatory assets, as well as amounts reclassified toearnings (in millions):

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

2017 2016 2017 2016

Beginning balance $ 162 $ 185 $ 148 $ 250Changes in fair value recognized in net regulatory assets 10 18 43 5Net (losses) gains reclassified to operating revenue (5) (3) 9 (6)Net losses reclassified to cost of sales (5) (5) (38) (54)Ending balance $ 162 $ 195 $ 162 $ 195

Designated as Hedging Contracts

The Company uses commodity derivative contracts accounted for as cash flow hedges to hedge electricity and natural gascommodity prices for delivery to nonregulated customers, spring operational sales, natural gas storage and other transactions.Certain commodity derivative contracts have settled and the fair value at the date of settlement remains in AOCI and is recognizedin earnings when the forecasted transactions impact earnings. The following table reconciles the beginning and ending balancesof the Company's accumulated other comprehensive (income) loss (pre-tax) and summarizes pre-tax gains and losses on commodityderivative contracts designated and qualifying as cash flow hedges recognized in OCI, as well as amounts reclassified to earnings(in millions):

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

2017 2016 2017 2016

Beginning balance $ 21 $ 26 $ 16 $ 46Changes in fair value recognized in OCI 5 15 28 35Net gains reclassified to operating revenue — 1 — 1Net losses reclassified to cost of sales (7) (7) (25) (47)Ending balance $ 19 $ 35 $ 19 $ 35 Realized gains and losses on hedges and hedge ineffectiveness are recognized in income as operating revenue, cost of sales,operating expense or interest expense depending upon the nature of the item being hedged. For the three- and nine-month periodsended September 30, 2017 and 2016, hedge ineffectiveness was insignificant. As of September 30, 2017, the Company had cashflow hedges with expiration dates extending through June 2026 and $10 million of pre-tax unrealized losses are forecasted to bereclassified from AOCI into earnings over the next twelve months as contracts settle.

20

Derivative Contract Volumes

The following table summarizes the net notional amounts of outstanding derivative contracts with fixed price terms that comprisethe mark-to-market values as of (in millions):

Unit of September 30, December 31,Measure 2017 2016

Electricity purchases Megawatt hours 9 5Natural gas purchases Decatherms 339 271Fuel purchases Gallons 2 11Interest rate swaps US$ 694 714Interest rate swaps £ 102 —Mortgage sale commitments, net US$ (442) (309)

Credit Risk

The Utilities are exposed to counterparty credit risk associated with wholesale energy supply and marketing activities with otherutilities, energy marketing companies, financial institutions and other market participants. Credit risk may be concentrated to theextent the Utilities' counterparties have similar economic, industry or other characteristics and due to direct or indirect relationshipsamong the counterparties. Before entering into a transaction, the Utilities analyze the financial condition of each significantwholesale counterparty, establish limits on the amount of unsecured credit to be extended to each counterparty and evaluate theappropriateness of unsecured credit limits on an ongoing basis. To further mitigate wholesale counterparty credit risk, the Utilitiesenter into netting and collateral arrangements that may include margining and cross-product netting agreements and obtain third-party guarantees, letters of credit and cash deposits. If required, the Utilities exercise rights under these arrangements, includingcalling on the counterparty's credit support arrangement.

Collateral and Contingent Features

In accordance with industry practice, certain wholesale derivative contracts contain credit support provisions that in part basecertain collateral requirements on credit ratings for senior unsecured debt as reported by one or more of the three recognized creditrating agencies. These derivative contracts may either specifically provide bilateral rights to demand cash or other security if creditexposures on a net basis exceed specified rating-dependent threshold levels ("credit-risk-related contingent features") or providethe right for counterparties to demand "adequate assurance," or in some cases terminate the contract, in the event of a materialadverse change in creditworthiness. These rights can vary by contract and by counterparty. As of September 30, 2017, the applicablecredit ratings from the three recognized credit rating agencies were investment grade.

The aggregate fair value of the Company's derivative contracts in liability positions with specific credit-risk-related contingentfeatures totaled $190 million and $190 million as of September 30, 2017 and December 31, 2016, respectively, for which theCompany had posted collateral of $73 million and $69 million, respectively, in the form of cash deposits. If all credit-risk-relatedcontingent features for derivative contracts in liability positions had been triggered as of September 30, 2017 and December 31,2016, the Company would have been required to post $105 million and $110 million, respectively, of additional collateral. TheCompany's collateral requirements could fluctuate considerably due to market price volatility, changes in credit ratings, changesin legislation or regulation, or other factors.

21

(10) Fair Value Measurements

The carrying value of the Company's cash, certain cash equivalents, receivables, payables, accrued liabilities and short-termborrowings approximates fair value because of the short-term maturity of these instruments. The Company has various financialassets and liabilities that are measured at fair value on the Consolidated Financial Statements using inputs from the three levelsof the fair value hierarchy. A financial asset or liability classification within the hierarchy is determined based on the lowest levelinput that is significant to the fair value measurement. The three levels are as follows:

• Level 1 — Inputs are unadjusted quoted prices in active markets for identical assets or liabilities that the Company hasthe ability to access at the measurement date.

• Level 2 — Inputs include quoted prices for similar assets or liabilities in active markets, quoted prices for identical orsimilar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the assetor liability and inputs that are derived principally from or corroborated by observable market data by correlation or othermeans (market corroborated inputs).

• Level 3 — Unobservable inputs reflect the Company's judgments about the assumptions market participants would usein pricing the asset or liability since limited market data exists. The Company develops these inputs based on the bestinformation available, including its own data.

The following table presents the Company's financial assets and liabilities recognized on the Consolidated Balance Sheets andmeasured at fair value on a recurring basis (in millions):

Input Levels for Fair Value MeasurementsLevel 1 Level 2 Level 3 Other(1) Total

As of September 30, 2017Assets:Commodity derivatives $ 1 $ 24 $ 102 $ (19) $ 108Interest rate derivatives — 14 14 — 28Mortgage loans held for sale — 534 — — 534Money market mutual funds(2) 855 — — — 855Debt securities:

United States government obligations 168 — — — 168International government obligations — 5 — — 5Corporate obligations — 37 — — 37Municipal obligations — 2 — — 2Agency, asset and mortgage-backed obligations — 1 — — 1

Equity securities:United States companies 270 — — — 270International companies 2,094 — — — 2,094Investment funds 182 — — — 182

$ 3,570 $ 617 $ 116 $ (19) $ 4,284Liabilities:

Commodity derivatives $ (1) $ (207) $ (16) $ 104 $ (120)Interest rate derivatives — (10) (1) — (11)

$ (1) $ (217) $ (17) $ 104 $ (131)

22

As of December 31, 2016Assets:Commodity derivatives $ 5 $ 49 $ 87 $ (22) $ 119Interest rate derivatives — 16 7 — 23Mortgage loans held for sale — 359 — — 359Money market mutual funds(2) 586 — — — 586Debt securities:

United States government obligations 161 — — — 161International government obligations — 3 — — 3Corporate obligations — 36 — — 36Municipal obligations — 2 — — 2Agency, asset and mortgage-backed obligations — 2 — — 2

Equity securities:United States companies 250 — — — 250International companies 1,190 — — — 1,190Investment funds 147 — — — 147

$ 2,339 $ 467 $ 94 $ (22) $ 2,878Liabilities:

Commodity derivatives $ (2) $ (199) $ (27) $ 96 $ (132)Interest rate derivatives (1) (11) (1) — (13)

$ (3) $ (210) $ (28) $ 96 $ (145)

(1) Represents netting under master netting arrangements and a net cash collateral receivable of $85 million and $74 million as of September 30, 2017 andDecember 31, 2016, respectively.

(2) Amounts are included in cash and cash equivalents; other current assets; and noncurrent investments and restricted cash and investments on theConsolidated Balance Sheets. The fair value of these money market mutual funds approximates cost.

Derivative contracts are recorded on the Consolidated Balance Sheets as either assets or liabilities and are stated at estimated fairvalue unless they are designated as normal purchases or normal sales and qualify for the exception afforded by GAAP. Whenavailable, the fair value of derivative contracts is estimated using unadjusted quoted prices for identical contracts in the market inwhich the Company transacts. When quoted prices for identical contracts are not available, the Company uses forward price curves.Forward price curves represent the Company's estimates of the prices at which a buyer or seller could contract today for deliveryor settlement at future dates. The Company bases its forward price curves upon market price quotations, when available, or internallydeveloped and commercial models, with internal and external fundamental data inputs. Market price quotations are obtained fromindependent brokers, exchanges, direct communication with market participants and actual transactions executed by the Company.Market price quotations are generally readily obtainable for the applicable term of the Company's outstanding derivative contracts;therefore, the Company's forward price curves reflect observable market quotes. Market price quotations for certain electricityand natural gas trading hubs are not as readily obtainable due to the length of the contract. Given that limited market data existsfor these contracts, as well as for those contracts that are not actively traded, the Company uses forward price curves derived frominternal models based on perceived pricing relationships to major trading hubs that are based on unobservable inputs. The estimatedfair value of these derivative contracts is a function of underlying forward commodity prices, interest rates, currency rates, relatedvolatility, counterparty creditworthiness and duration of contracts. Refer to Note 9 for further discussion regarding the Company'srisk management and hedging activities.

The Company's mortgage loans held for sale are valued based on independent quoted market prices, where available, or the pricesof other mortgage whole loans with similar characteristics. As necessary, these prices are adjusted for typical securitization activities,including servicing value, portfolio composition, market conditions and liquidity.

The Company's investments in money market mutual funds and debt and equity securities are stated at fair value and are primarilyaccounted for as available-for-sale securities. When available, a readily observable quoted market price or net asset value of anidentical security in an active market is used to record the fair value. In the absence of a quoted market price or net asset value ofan identical security, the fair value is determined using pricing models or net asset values based on observable market inputs andquoted market prices of securities with similar characteristics.

23

The following table reconciles the beginning and ending balances of the Company's assets and liabilities measured at fair valueon a recurring basis using significant Level 3 inputs (in millions):

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

Interest Auction Interest AuctionCommodity Rate Rate Commodity Rate RateDerivatives Derivatives Securities Derivatives Derivatives Securities

2017:Beginning balance $ 81 $ 8 $ — $ 60 $ 6 $ —Changes included in earnings 7 34 — 19 100 —Changes in fair value recognized in

OCI (1) — — (3) — —Changes in fair value recognized in

net regulatory assets (3) — — (5) — —Purchases — 8 — 1 6 —Settlements 2 (37) — 14 (99) —Ending balance $ 86 $ 13 $ — $ 86 $ 13 $ —

Three-Month Periods Nine-Month PeriodsEnded September 30, Ended September 30,

Interest Auction Interest AuctionCommodity Rate Rate Commodity Rate RateDerivatives Derivatives Securities Derivatives Derivatives Securities

2016:Beginning balance $ 44 $ 14 $ 18 $ 47 $ 4 $ 44Changes included in earnings 9 49 — 8 103 —Changes in fair value recognized in

OCI (2) — — (2) — 6Changes in fair value recognized in

net regulatory assets (1) — — (12) — —Purchases 1 — — 1 — —Redemptions — — — — — (32)Settlements 5 (52) — 14 (96) —Ending balance $ 56 $ 11 $ 18 $ 56 $ 11 $ 18

The Company's long-term debt is carried at cost on the Consolidated Balance Sheets. The fair value of the Company's long-termdebt is a Level 2 fair value measurement and has been estimated based upon quoted market prices, where available, or at the presentvalue of future cash flows discounted at rates consistent with comparable maturities with similar credit risks. The carrying valueof the Company's variable-rate long-term debt approximates fair value because of the frequent repricing of these instruments atmarket rates. The following table presents the carrying value and estimated fair value of the Company's long-term debt (in millions):

As of September 30, 2017 As of December 31, 2016Carrying Fair Carrying Fair

Value Value Value Value

Long-term debt $ 36,124 $ 41,197 $ 36,116 $ 40,718

24

(11) Commitments and Contingencies

Fuel, Capacity and Transmission Contract Commitments

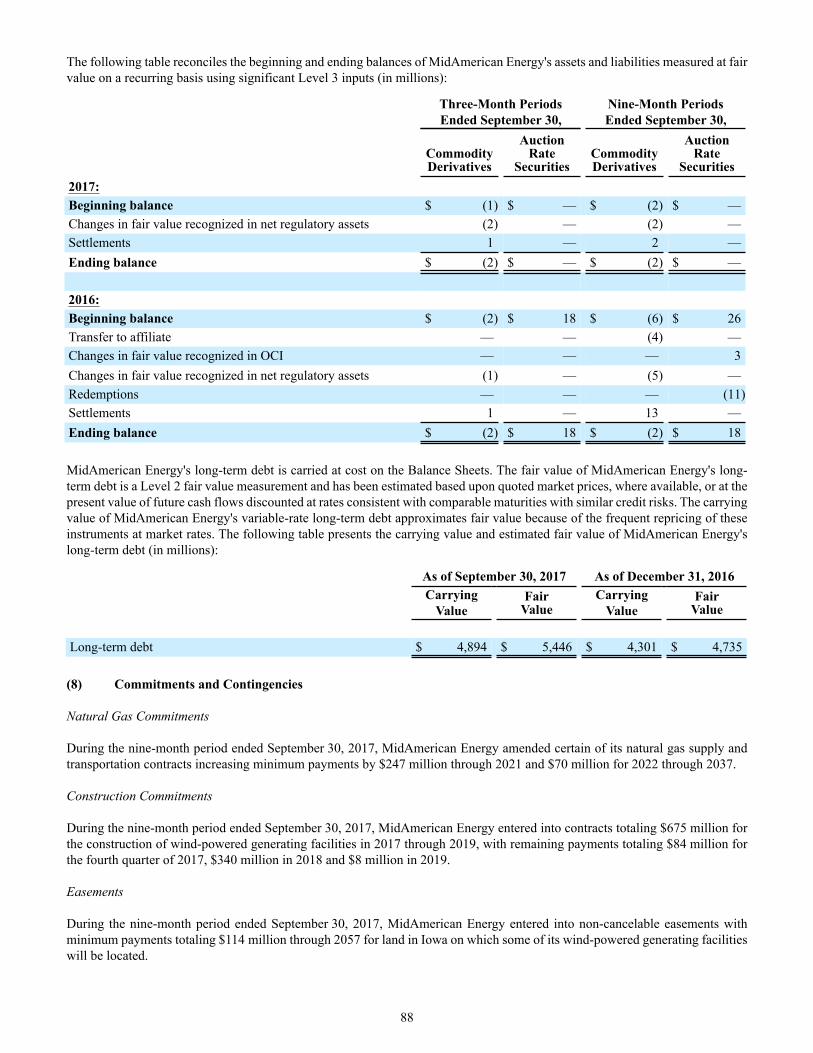

During the nine-month period ended September 30, 2017, MidAmerican Energy amended certain of its natural gas supply andtransportation contracts increasing minimum payments by $247 million through 2021 and $70 million for 2022 through 2037.

Construction Commitments

During the nine-month period ended September 30, 2017, MidAmerican Energy entered into contracts totaling $675 million forthe construction of wind-powered generating facilities in 2017 through 2019, with remaining payments totaling $84 million forthe fourth quarter of 2017, $340 million in 2018 and $8 million in 2019.

Operating Leases and Easements

During the nine-month period ended September 30, 2017, MidAmerican Energy entered into non-cancelable easements withminimum payments totaling $114 million through 2057 for land in Iowa on which some of its wind-powered generating facilitieswill be located.

Legal Matters

The Company is party to a variety of legal actions arising out of the normal course of business. Plaintiffs occasionally seek punitiveor exemplary damages. The Company does not believe that such normal and routine litigation will have a material impact on itsconsolidated financial results. The Company is also involved in other kinds of legal actions, some of which assert or may assertclaims or seek to impose fines, penalties and other costs in substantial amounts and are described below.

Environmental Laws and Regulations

The Company is subject to federal, state, local and foreign laws and regulations regarding air and water quality, renewable portfoliostandards, emissions performance standards, climate change, coal combustion byproduct disposal, hazardous and solid wastedisposal, protected species and other environmental matters that have the potential to impact the Company's current and futureoperations. The Company believes it is in material compliance with all applicable laws and regulations.

Hydroelectric Relicensing