Unit 6 Renting vs. Owning

73

UNIT 6 RENTING VS. OWNING ORCUTT ACADEMY HIGH SCHOOL ACCOUNTING & FINANCE

-

Upload

jenny-hubbard -

Category

Economy & Finance

-

view

42 -

download

3

Transcript of Unit 6 Renting vs. Owning

UNIT 6

RENTING VS.

OWNING

ORCUTT ACADEMY HIGH SCHOOL

ACCOUNTING & FINANCE

THE FIRST

STEPS TO

HOME

OWNERSHIP

UNIT 6, LESSON 1

Renting vs. Owning

Are You Ready to Buy?

How Much Can You Borrow?

The Down Payment & Closing Costs

PREVIEW

RENTING VS. OWNING

ADVANTAGES OF

RENTING

• Possibly lower cost

• If you can save 10% or more of your earnings, you are on your way to meeting your financial goals.

• No maintenance costs

• Flexibility

• Financial freedom: spend without obligation

• Psychological freedom: move more easily

• Liquidity

• Wealth not tied up in home

COSTS OF RENTING

• Monthly rent is subject to inflation

• Consider your costs in the long-term

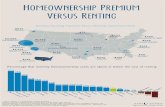

Cost of owning versus renting over 30 years

Year Ownership cost per

month

Rental cost per month

1 $920 $800

5 $980 $940

10 $1,080 $1,140

20 $1,360 $1,690

30 $1,800 $2,500

Comparing the costs of owning a home that costs $160,000

to renting that same home for $800/month.

COSTS OF RENTING

• Owning becomes less expensive in the long run

• As a homeowner, you build equity

ARE YOU READY TO BUY

ASSESSING YOUR

TIMELINE

Wait to buy a home until you plan on being there for at least 3 years (preferably five or more)

PROPERTY MUST

APPRECIATE 15%

TO COVER EXPENSES

BEFORE BUYING, ASK

YOURSELF…

Are you saving enough money monthly to reach your

retirement goals?

BEFORE BUYING, ASK

YOURSELF…

How much do you spend (and want to continue spending) on

fun things such as travel and entertainment?

BEFORE BUYING, ASK

YOURSELF…

How willing are you to budget your expenses in order to meet

your monthly mortgage payments and other housing

expenses?

BEFORE BUYING, ASK

YOURSELF…

How much of your children’s expected college educational

expenses do you want to be able to pay for?

HOW MUCH CAN YOU BORROW

THE EFFECT OF DEBT

Existing debt will lower the amount you are eligible to borrow.

Monthly Debt Payments + Housing Expenses < 38%

of monthly gross income

CALCULATING HOW

MUCH LENDERS WILL

ALLOW YOU TO BORROW

General Rule: You can borrow up to three times

(or two and a half times) your annual income when buying a home.

BUT… HOW MUCH YOU

CAN BORROW DEPENDS

ON INTEREST RATES

Set by the secondary market

EXPENSES

• Mortgage costs

• Inspection expenses

• Moving costs

• Commissions

• Title insurance

WHAT’S THE APPROXIMATE

MAXIMUM YOU CAN BORROW?

When mortgage rates are Multiply your gross income

by this figure

4% 4.6

5% 4.2

6% 3.8

7% 3.5

8% 3.2

9% 2.9

10% 2.7

11% 2.5

MULTIPLIER

The number you multiply by your gross income to determine

how much money you can borrow for a home mortgage;

determined by interest rates.

OR

The number you multiply by your mortgage expressed in

thousands of dollars (divided by 1000) to determine your

monthly mortgage payment

As rates fall, the monthly mortgage payment drops

Lower interest rates make buying real estate more affordable

CALCULATE

What is the maximum amount you can borrow?

1. Annual income $45,870

a) Interest rate 5%

b) Interest rate 11%

2. Annual income $68,900

a) Interest rate 4%

b) Interest rate 8%

3. Annual income $159,650

a) Interest rate 9%

b) Interest rate 6%

DOWN PAYMENT & CLOSING COSTS

THE DOWN PAYMENT

If you put down 20% of the purchase price of the home

• Most favorable terms, including interest rate and closing

costs

• Don’t have to pay mortgage insurance

For a $100,000 home, the down payment would be $20,000

• (100,000)(.2) = $20,000

PMI: PRIVATE

MORTGAGE INSURANCE

• If you put less than 20% down

• Protects lenders if you default on your loan

• Several hundred $ per year

• Varies depending on the percent of the purchase price you

put down

• The higher the down payment, the lower the PMI

• Visit http://www.goodmortgage.com/Calculators/PMI.html

PURCHASE PRICE

Purchase Price = Mortgage Loan + Down Payment

CLOSING COSTS

• In addition to a down payment, you must have cash saved

for closing costs

• Includes escrow fees, inspection fees, title insurance, and

other miscellaneous fees

• On average from 2-3 percent of the price of the home

• Could be anywhere from 1-8% of the price of the home

• Your lender will give you a “Good Faith Estimate”

HELP WITH CLOSING

COSTS

• You can request

• Your seller pay part of the closing costs

• Your lender add part of the closing costs to your mortgage

loan

• Interest rate will go up about .25%

1. How can you determine if you are ready to buy a home?

2. How do lenders decide how much money you can borrow to

purchase a home?

3. What factors should you consider when determining how

much money to save to buy a home?

ESSENTIAL QUESTIONS

WHAT ARE YOU LEARNING? WHY ARE YOU LEARNING IT? HOW WILL YOU USE IT?

TOTAL

HOUSING

COST UNIT 6, LESSON 2

Calculating Mortgage Payment

Taxes: The Cost and the Benefit

Insurance & Maintenance

Calculating Total Housing Cost

PREVIEW

TOTAL HOUSING

COST

1. Mortgage Payment

2. Taxes

• The Cost and the Benefit

3. Insurance

4. Maintenance

CALCULATING MORTGAGE PAYMENT

CALCULATE MORTGAGE

USING MULTIPLIER

Interest Rate 15-year mortgage

Multipliers

30-year mortgage

4% 7.4 4.77

4.5% 7.65 5.07

5% 7.91 5.37

5.5% 8.17 5.68

6% 8.44 6.00

6.5% 8.71 6.32

7% 8.99 6.65

8% 9.56 7.34

9% 10.14 8.05

10% 10.75 8.78

Multiply the multiplier by your mortgage expressed in thousands of dollars (divided by 1000)

EXAMPLE

Skye is taking out a $100,000 30-year mortgage at 6.5%. What

will be her monthly mortgage payment?

The multiplier is 6.32, so

Monthly mortgage payment = 6.32 x 100,000/1,000

= 6.32 x 100

= $632

CALCULATE MORTGAGE

USING FORMULA

M = P [ i(1 + i)n ] / [ (1 + i)n - 1]

M = The monthly payment

P = The principal, or the amount of money being borrowed

i = The interest for each compounding period, or the interest

per month for a standard mortgage

n = The number of compounding periods, or the number of

months for a standard mortgage

TAXES: THE COST AND THE BENEFIT

TAXES: THE COST

• Homeowners pay property tax, which helps support local

governments.

• Based on the assessed value of your home

• Land + Improvements

• May be higher or lower than the purchase price of the

home

TAX RATES

• Set by the county

• Usually about 1-2%

• Average property tax rates by state

• Ex: Santa Barbara County

CALCULATING

TAX COSTS

The value of a home in Greenwood County is $285,000.

Property taxes in Greenwood are 1.25%. What is the monthly

property tax bill for the home?

Annual property tax bill: (285,000)(.0125) = $3562.50

Monthly property tax bill: (3562.50)/12 = $296.88

TAXES: THE BENEFIT

• You can deduct

• Interest paid to buy, build, or improve your home

• Interest paid on a home equity loan

• Property taxes

• You can deduct a second home

• Learn more about Tax Deductions on Mortgage Interest

CALCULATING THE TAX

BENEFIT OF OWNING

TAX BENEFIT =

(Mortgage Payment + Property Taxes) (Tax Bracket)

EXAMPLE

Tyler’s gross annual income is $83,000. His mortgage payment is $1,200/month and he pays $260/month in property taxes. What is his tax benefit from owning.

(1200+260)(.25) = $365

Tax Brackets 2012 (Estimated) Single (Est) Married Filing Jointly (Est) Head of Household

10% Bracket $0 – $8,700 $0 – $17,400 $0 – $12,400

15% Bracket $8,700 – $35,350 $17,400 – $70,700 $12,400 – $47,350

25% Bracket $35,350 – $85,650 $70,700 – $142,700 $47,350 – $122,300

28% Bracket $85,650 – $178,650 $142,700 – $217,450 $122,300 – $198,050

33% Bracket $178,650 – $388,350 $217,450 – $388,350 $198,050 – $388,350

35% Bracket $388,350+ $388,350+ $388,350+

HOMEOWNER’S INSURANCE

HOMEOWNER’S

INSURANCE

• On average, between $45 and $75/month

• Varies depending on

• Home’s value

• Location

• Homeowner’s demographics

• Type and amount of insurance

LEARN MORE…

Tips on homeowner’s insurance

MAINTENANCE

MAINTENANCE

About 1% of the home’s value on average

Example:

A home with a value of $475,000

Annual maintenance = (475,000)(.01) = $4,750

Monthly maintenance = 4,750/12 = $395.83

MAINTENANCE

CHECKLIST

National Healthy Homes Training Center Checklist

TOTAL HOUSING COST

TOTAL

HOUSING COST

PUTTING THE PIECES TOGETHER!

Total Housing Cost =

(Mortgage Payment + Property Tax + Insurance + Maintenance) – (Tax Benefit)

EXAMPLE 1

Taylor is an actor living in Los Angeles, California where the property tax is 1.25%. Her gross annual income is $71,500 and the value of her property is $367,000. Her monthly mortgage payment is $1,200 and she pays $40/month for insurance. Estimate her total housing costs.

Total Housing Cost =

(Mortgage Payment + Property Taxes + Insurance + Maintenance) – (Tax Benefit)

Mortgage Payment = $1,200

Property Taxes = (367,000)(.0125)/12 = $382.29

Insurance = $40

Maintenance = (367,000)(.01)/12 = $305.83

Tax Benefit = (Mortgage Payment + Property Taxes)(Tax Bracket)

(1200 + 382.29)(.25) = 395. 57

Total Cost = 1200 + 382.29 + 40 + 305.83 - 395.57 = $1532.55

1. To calculate the mortgage payment, what three pieces of

information do you need to know?

2. How do taxes affect the overall total cost?

3. What components make up the total monthly housing

cost?

ESSENTIAL QUESTIONS

WHAT ARE YOU LEARNING? WHY ARE YOU LEARNING IT? HOW WILL YOU USE IT?

FINANCING

YOUR HOME

UNIT 6, LESSON 3

Adjustable vs. Fixed-Rate

30-year vs. 15-year

Finding a Lender

Points & Interest Rates

PREVIEW

ADJUSTABLE-RATE VS. FIXED-RATE

30-YEAR VS 15-YEAR

FIXED-RATE MORTGAGES

Interest rates never change

Monthly mortgage payment does not change

No uncertainty

BUT… if interest rates fall (and you can’t refinance), you are

stuck with your higher-cost mortgage

ADJUSTABLE RATE

MORTGAGES

• Interest rate varies over time

• Can change yearly, or even monthly

• Most often, every 6 or 12 months

• Monthly mortgage payment fluctuates

• Advantage: Potential interest savings

• Lower rates for the first few years

• After that, your rate depends on overall trends

CHOOSING BETWEEN

FIXED AND ADJUSTABLE

• Consider your ability to take on financial risk

• Reliability of income

• Job security

• Emergency savings

• Future expenses

• Stress level

• If you can’t afford the highest allowed payment on an

adjustable-rate mortgage, don’t take it.

15-YEAR VS. 30-YEAR

15-year 30-year

Pay off faster, Build equity faster Takes longer to pay off

Higher payments Lower payments

Lower interest rate (about ½

percent)

Higher interest rate

If you don’t plan on investing, it is

better to pay off your mortgage

faster

Alternative investing opportunities

CHOOSING BETWEEN

FIXED AND ADJUSTABLE

• Consider how long you plan to keep the mortgage

• Adjustable rate mortgages have lower interest rates for the

first few years.

• Wise if you plan on keeping your mortgage less than 5-7

FINDING A LENDER

SHOPPING FOR A

LENDER ON YOUR OWN

• Large banks usually don’t offer the best rates

• Check out smaller lending institutions

• Using a local bank can sometimes be a plus. Their staff

generally understand the specifics of local properties

• Find mortgage companies in cities across the country

HIRING A MORTGAGE

BROKER

• Brokers

• Submit the home buyer's application to one or more

lenders

• Work with the chosen lender until the loan closes

• Can often find a lender who will make loans that a bank

refuses

• May be necessary for problem credit

MORTGAGE BROKERS

Get paid a percentage of the loan amount

• typically 0.5-1%

Ask your mortgage broker what his cut is

The broker should shop among lenders to get you a good deal

Help you fill out documents lenders demand before giving you a

loan

BEWARE

• Some brokers place their business with the same lenders

all the time, those usually don’t offer the best rates

• You can shop on your own, so you can compare with what

your broker tells you

• Thoroughly check a broker’s references before you do

business with them

• Make sure you ask who the lender is—most brokers refuse

to reveal this info until you pay a certain amount to cover

the appraisal and credit report

POINTS AND INTEREST RATES

POINTS

• The initial fee charged by the lender, with each point being

equal to 1% of the amount of the loan.

THE SEESAW EFFECT

• As points go up, the interest rate goes down. As points

go down, the interest rate goes up.

• It is important to consider both the points and the interest

rate when comparing two mortgage loans.

COMPARING

MORTGAGES

EXAMPLE: Compare the two loans. Identify when the loans will have the same cost and which loan will have a lower cost after the identified time period.

Loan #1: 3% interest rate, 2 points

Loan #2: 4% interest rate, 1 point

𝑫𝒊𝒇𝒇𝒆𝒓𝒆𝒏𝒄𝒆 𝒊𝒏 𝒑𝒐𝒊𝒏𝒕𝒔

𝑫𝒊𝒇𝒇𝒆𝒓𝒆𝒏𝒄𝒆 𝒊𝒏 𝒓𝒂𝒕𝒆𝒔 =

𝟐−𝟏

𝟒−𝟑 =

𝟏

𝟏 = 𝟏

This formula tells you when the loans will have the same cost. After the given time period, the loan with the lower interest rate will have a lower cost, so…

After one year, Loan #1 will have a lower cost.

GETTING THE BEST RATE

1. Why is it financially wise to make a down payment of at least

20 percent of the purchase price of the property?

2. Why would you choose a fixed-rate loan? An adjustable rate

loan?

3. Why should you consider both the interest rate and the

points of a loan when shopping for a loan?

ESSENTIAL QUESTIONS

WHAT ARE YOU LEARNING? WHY ARE YOU LEARNING IT? HOW WILL YOU USE IT?