Unit 3 – Investments, Credit and Debt. State Standard(s) Addressed: CTE P.F #16) Explain how...

55

it 3 – Investments, Credit and Debt it 3 – Investments, Credit and Debt

-

Upload

marilyn-walton -

Category

Documents

-

view

214 -

download

0

Transcript of Unit 3 – Investments, Credit and Debt. State Standard(s) Addressed: CTE P.F #16) Explain how...

Unit 3 – Investments, Credit and DebtUnit 3 – Investments, Credit and Debt

State Standard(s) Addressed:CTE P.F #16) Explain how savings and investing contribute to financial well-being, building wealth, and helping to meet financial goals. Compare and contrast investment strategies such as stocks, mutual funds, and commodities. Include time value of money and stock calculations. Design a diversified savings and investment plan. TN CCSS Mathematics F-IF

Goal(s) Objective(s):1.Describe various investment types and analyze diversity in investments. 2.Design an investment and savings plan showing mathematical calculations and research citations as needed. 3.Track the investment plan for a period of 4 weeks.

Standards & Objectives

Write Your

Essential Question!

Unit #3

It Takes It Takes Money to Money to

Make MoneyMake Money

VocabularyVocabulary• Saving – is what people usually do to

meet short-term goals. It provides safe and easy access to your money at all times.

• Investing – means you’re setting your money aside for longer-term goals. There is no guarantee that your money will grow, however the opportunity of making money is higher than with savings alone.

Notes

VocabularyVocabulary Diversification – the process of spreading

ones assets among several types of investments to lessen risk.

Volatility – the potential for rapid or unexpected change.

Portfolio - all the securities held by an investor.

Securities – a tradable financial asset of any kind.

Notes

VocabularyVocabulary Stocks – shares of a company that are bought at a

purchase price and traded daily on a business market such as the NASDAQ, New York Stock Exchange, and American Stock Exchange.

Mutual Fund – an investment alternative in which investors pool their money to buy stocks, bonds and other securities based on suggestions by investment managers.

Commodities – a marketable item produced to satisfy wants or needs, may be a good or a service.

Notes

Savings and InvestmentsSavings and Investments

UniqueUniqueSavingsSavingsFeaturesFeatures

UniqueUniqueInvestmentInvestment

FeaturesFeatures

CommonCommonFeaturesFeatures

What are some features common to both What are some features common to both investments and savings?investments and savings?

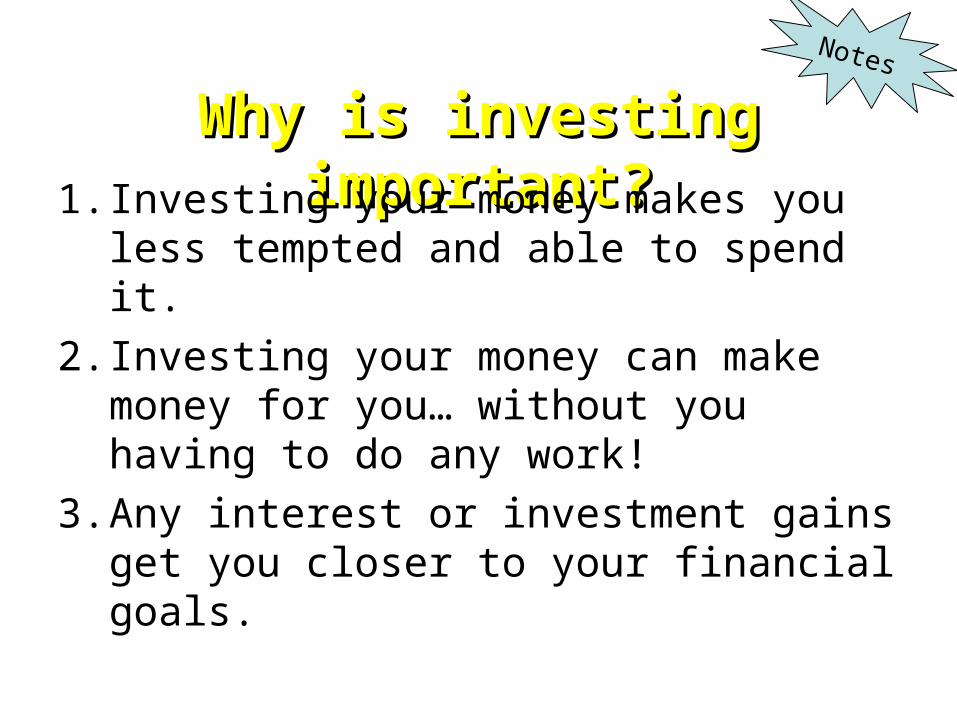

Why is investing important?Why is investing important?1. Investing your money makes you less

tempted and able to spend it.

2. Investing your money can make money for you… without you having to do any work!

3. Any interest or investment gains get you closer to your financial goals.

Notes

FinancialFinancialPlanningPlanningPyramidPyramid

PennyStock

Commo- dities

CollectiblesSpeculative Stock / Bonds /Mutual Funds

RealEstate

Blue-ChipCommonStock

GrowthMutual Funds

High-GradeConvertible

Bonds

High-GradePreferred

Stock

BalancedMutual Funds

High-GradeCorporate Bondsor Mutual Funds

High-GradeMunicipal Bondsor Mutual Funds

Money MarketAccounts

or Mutual Funds

Certificatesof Deposit

U.S. SavingsBonds

Insured Savings / Checking Accounts

TreasuryIssues

Highest RiskHighest RiskHighest EarningsHighest Earnings

Lower Lower RiskRisk

Lower Lower EarningsEarnings

3-J

Notes

VocabularyVocabulary

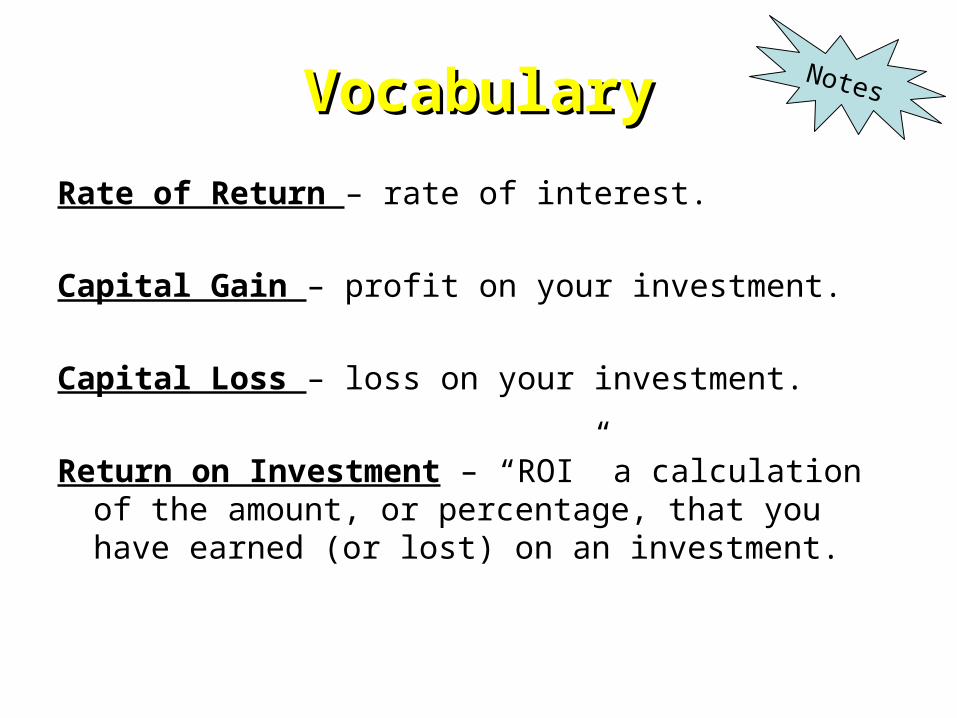

Rate of Return – rate of interest.

Capital Gain – profit on your investment.

Capital Loss – loss on your investment.

Return on Investment – “ROI” a calculation of the amount, or percentage, that you have earned (or lost) on an investment.

Notes

Return on InvestmentReturn on InvestmentNotes

R = Return, or $ received after the investment. I = Original Money Invested.

Example 1Example 1 Notes

Example 2Example 2

2. Jenny checked her savings account balance and it showed $312.00. She opened the account with $300. What is her return on investment.

Notes

Example 3Example 3

3. Sheila purchased facebook stock for $500. After one year her stock sold for $460. What is her ROI?

Notes

StocksStocks• Having stock in a company means that you

own part of that company. A company usually begins issuing shares of stock to raise money that is usually reinvested in the company.

• These are high risk investments. • Stocks are exchanged on several markets:

NASDAQ, DOW, S&P are the most common. • Liquid assets, overtime with short turn around.

Notes

Mutual FundsMutual Funds

• Takes money from many investors and uses it to make growth or income investments based on a stated investment objective.

• Some focus on income, some on growth.

• Offer flexibility and affordability by investing in several options at once.

• Professionally managed

Notes

AssignmentAssignment1. Write five questions to ask a financial

advisor tomorrow about savings and investing.

2. Begin to research stock options using yahoofinance.com

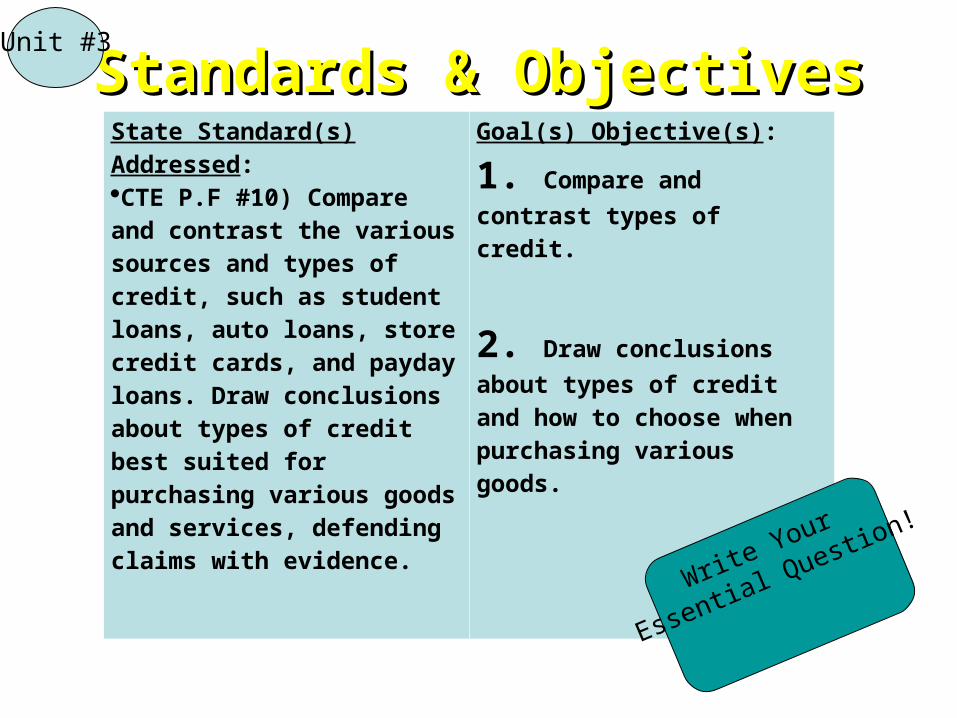

Standards & ObjectivesStandards & ObjectivesState Standard(s) Addressed:CTE P.F #10) Compare and contrast the various sources and types of credit, such as student loans, auto loans, store credit cards, and payday loans. Draw conclusions about types of credit best suited for purchasing various goods and services, defending claims with evidence.

Goal(s) Objective(s):

1. Compare and contrast

types of credit.

2. Draw conclusions about

types of credit and how to choose when purchasing various goods.

Write Your

Essential Question!

Unit #3

Credit FactsCredit FactsNearly Nearly 33%33% of teens owe money to either a of teens owe money to either a

person or company, with an average debt person or company, with an average debt of of $230$230..

About About 26%26% of teens ages 16-18 already of teens ages 16-18 already have more than $1,000 in debt.have more than $1,000 in debt.

30%30% of teens say they understand how of teens say they understand how credit card interest and fees work.credit card interest and fees work.

36%36% of teens say they know how to of teens say they know how to establish good credit.establish good credit.

VocabularyVocabularyCredit –Credit – is the concept of taking out a loan to buy is the concept of taking out a loan to buy

something now that you pay for over a period of something now that you pay for over a period of time with interest. time with interest.

Debt – Debt – the amount you owe on your credit the amount you owe on your credit accounts.accounts.

Loan Term Loan Term – the length of time you have to pay – the length of time you have to pay off the loan. Longer the term, lower the payment off the loan. Longer the term, lower the payment but higher the interest… but higher the interest…

Grace Period Grace Period – the length of time you have before – the length of time you have before you start accumulating interest. you start accumulating interest.

NOTES

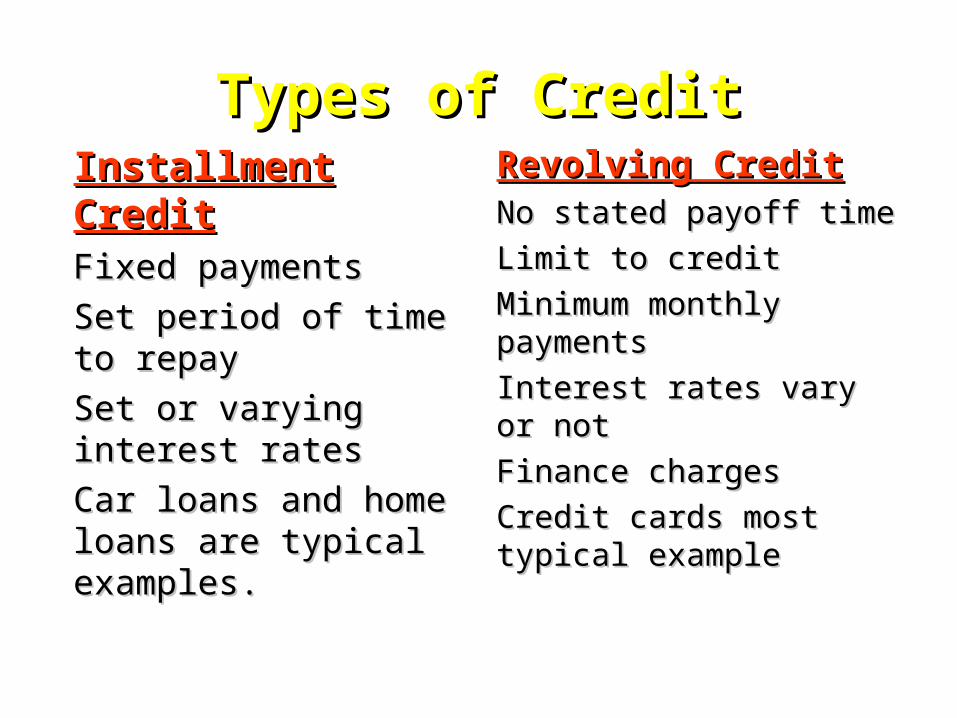

Types of CreditTypes of CreditInstallment CreditInstallment CreditFixed paymentsFixed payments

Set period of time to Set period of time to repayrepay

Set or varying interest Set or varying interest ratesrates

Car loans and home Car loans and home loans are typical loans are typical examples.examples.

Revolving CreditRevolving CreditNo stated payoff timeNo stated payoff time

Limit to creditLimit to credit

Minimum monthly Minimum monthly paymentspayments

Interest rates vary or notInterest rates vary or not

Finance chargesFinance charges

Credit cards most Credit cards most typical exampletypical example

Sources of CreditSources of CreditBanksBanks

Credit UnionsCredit Unions

Department StoresDepartment Stores

Automobile DealersAutomobile Dealers

Pay Day or Title LoansPay Day or Title Loans

Oil Companies (for gas stations)Oil Companies (for gas stations)

Federal Government (for student loans)Federal Government (for student loans)

Others?Others?

Common Types of CreditCommon Types of CreditType of Credit Institution Features

Credit Card Banks, Credit Unions, Stores, Gas Stations, Airlines

Used most places, no payoff deadline, monthly minimum payments vary, highest interest rate

Installment Loan Banks, Credit Unions, Auto dealers, other financial institutions

Large purchases, varied loan terms, set monthly payments, lower interest than credit card usually.

Student Loan Banks, Credit Unions, Federal government

Use for college expenses, some delayed payments, long loan term 10+yrs, lower interest than installment loan

Mortgage Banks, Credit Unions Loan to purchase a home, 15-30yrs, Set monthly payments, lower interest than installment

Cost of CreditCost of Credit

Annual Percentage Rate (APR) Annual Percentage Rate (APR) – a – a percentage of interest charged against the percentage of interest charged against the loan amount. loan amount.

Annual Fee Annual Fee – yearly charge for the privilege – yearly charge for the privilege of using credit. of using credit.

Finance Charge Finance Charge – represents the actual – represents the actual dollar cost of using credit to maintain a dollar cost of using credit to maintain a balance. (Monthly Interest)balance. (Monthly Interest)

NOTES

Continued…Continued…

Origination Fee Origination Fee – charge to set up a loan.– charge to set up a loan.

Over-the-limit Fee Over-the-limit Fee – fee for spending more – fee for spending more than your limit. than your limit.

Late Fee Late Fee – fee for paying your bill late. – fee for paying your bill late.

Universal Default Universal Default – a clause in credit – a clause in credit agreements that they can raise your APR agreements that they can raise your APR to a very high rate for things such as one to a very high rate for things such as one late payment, or over the limit. late payment, or over the limit.

NOTES

WHEN YOU BUY “STUFF”WHEN YOU BUY “STUFF”

In fact, you bought $500 worth of “STUFF” with your credit card.In fact, you bought $500 worth of “STUFF” with your credit card.

You bought “STUFF” with your credit card.You bought “STUFF” with your credit card.

Your APR is 18%.Your APR is 18%.

You plan to pay $10 a month to pay it off.You plan to pay $10 a month to pay it off.

You will pay $431 in interestYou will pay $431 in interest

Final cost of your purchases = $931.40Final cost of your purchases = $931.40

And it will take SEVEN YEARS and NINE MONTHSAnd it will take SEVEN YEARS and NINE MONTHS

How Long Will It Take???How Long Will It Take???

APR = 18%APR = 18%

Payment: 4% of current balancePayment: 4% of current balance

You owe $3,000.You owe $3,000.

Finance Charge $1715.69Finance Charge $1715.69

Total cost of original Total cost of original $3,000 loan = $4715.69$3,000 loan = $4715.69

After you’ve made the last payment, will what you purchased still be around???

And it will And it will take take

nearly nearly 11 YEARS 11 YEARS to pay off!to pay off!

The Cost of Using CreditThe Cost of Using Credit

APR = 24%APR = 24%

Payment: 4% of current balancePayment: 4% of current balance

$700 for a Game System$700 for a Game System

Finance Charge $550.04Finance Charge $550.04

Your CD player REALLY Your CD player REALLY cost $1,250.04cost $1,250.04

After you’ve made the last payment, will your game system still be around???

And it will And it will take overtake over7 years 7 years

to pay off!to pay off!

AssignmentAssignment

Create a chart, similar to the one you saw in Create a chart, similar to the one you saw in the notes about the different types of the notes about the different types of loans, their uses, and the common fees or loans, their uses, and the common fees or terms. terms.

Write a three sentence summary at the Write a three sentence summary at the bottom summarizing the concept of credit bottom summarizing the concept of credit and loan options.and loan options.

Standards & ObjectivesStandards & ObjectivesState Standard(s) Addressed:CTE P.F #12) Citing evidence found in credit applications, compare and contrast various types of credit and calculate the real cost of borrowing. Explain factors that can affect the approval process and identify typical information and procedures used in the application process. Analyze factors associated with purchasing an automobile including (a-f).TN CCSS Math N-QTN CCSS Reading 2, 3, 4, 9 Writing 9

Goal(s) Objective(s):1.Compare credit applications and terms. 2.Calculate the cost of debt and monthly payments.3.Explain factors that affect credit approval.

Write Your

Essential Question!

Unit #3

Applying For CreditApplying For Credit• Social Security NumberSocial Security Number

• Driver’s LicenseDriver’s License

• Date of BirthDate of Birth

• Address and PhoneAddress and Phone

• Employer InformationEmployer Information

• Income InformationIncome Information

• Total current bills and debtsTotal current bills and debts

NOTES

What Lenders want to know…What Lenders want to know…

Credit you haveCredit you have

Loan amounts you’ve receivedLoan amounts you’ve received

Current balances and limitsCurrent balances and limits

Payment historyPayment history

Debt to Income RatioDebt to Income Ratio

Debt to Income RatioDebt to Income Ratio

• May also be used to calculate Debt to May also be used to calculate Debt to Asset RatioAsset Ratio

• Used to determine if you are able to take Used to determine if you are able to take on new credit lines, or debt. on new credit lines, or debt.

• May be written as a percent 50%May be written as a percent 50%

• Debt divided by IncomeDebt divided by Income

NOTES

Example 1Example 1

Sarah has a total gross income of $58,500 Sarah has a total gross income of $58,500 per year. Her estimated monthly payment per year. Her estimated monthly payment on all debt and credit lines is $1,200. What on all debt and credit lines is $1,200. What is her annual debt to income ratio? is her annual debt to income ratio?

NOTES

Buying a Car!Buying a Car!

Down Payment – Down Payment – the total amount paid by the total amount paid by the buyer prior to financing the loan. the buyer prior to financing the loan.

Loan Amount – Loan Amount – the total amount financed the total amount financed after all taxes, fees, and services are after all taxes, fees, and services are added.added.

Monthly Payment – Monthly Payment – the total payment the total payment amount, fixed per month include all amount, fixed per month include all interest on the loan. interest on the loan.

NOTES

DepreciationDepreciation• Automobile values depreciate or reduce Automobile values depreciate or reduce

over time in most cases. over time in most cases.

• These are usually exponential in nature These are usually exponential in nature and reduce quickly at the beginning, the and reduce quickly at the beginning, the slower over time. slower over time.

• It is important to include depreciated It is important to include depreciated value when analyzing loan options and value when analyzing loan options and car choices. car choices.

NOTES

Calculating Car FinancesCalculating Car Finances

1.1. Using the “Deals On Wheels” Worksheet Using the “Deals On Wheels” Worksheet Calculate the amount to be financed for Calculate the amount to be financed for two types of cars. two types of cars.

2.2. Use bankrate.com and their monthly car Use bankrate.com and their monthly car payment calculator to determine the payment calculator to determine the monthly payment, total finance charge, monthly payment, total finance charge, and total final cost of a 10K vehicle at and total final cost of a 10K vehicle at varying APRs. varying APRs.

AssignmentAssignment• Follow the direction to complete page Follow the direction to complete page

three and four of the “Deals on Wheels” three and four of the “Deals on Wheels” packet.packet.• Research Two Vehicles: Take NotesResearch Two Vehicles: Take Notes• Calculate all related charges and expenses.Calculate all related charges and expenses.• Estimate what you could afford using Estimate what you could afford using

budgeting knowledge. budgeting knowledge. • Write 2 paragraphs about what vehicle you Write 2 paragraphs about what vehicle you

can afford to buy, at what price and why. can afford to buy, at what price and why.

Standards & ObjectivesStandards & ObjectivesState Standard(s) Addressed:CTE P.F #11) Describe the relationship between consumers and credit reports, credit scores using research and textual evidence. Analyze a sample credit report and interpret factors that may affect credit score. Explain how credit score may impact borrowing opportunities and cost of credit. Summarize how to maintain a good credit score.

Goal(s) Objective(s):1.Describe the relationship between consumers and credit reports, credit scores using research and textual evidence.2.Analyze a sample credit report and interpret factors that may affect credit score. 3.Explain how credit score may impact borrowing opportunities and cost of credit. 4.Summarize how to maintain a good credit score.

Unit #3

The 4C’s of CreditThe 4C’s of CreditCollateral – Collateral – an asset of value that lenders can take from an asset of value that lenders can take from

you if you don't repay your loan. This is a ‘secured’ loan. you if you don't repay your loan. This is a ‘secured’ loan.

Capital – Capital – lenders take comfort in knowing you have lenders take comfort in knowing you have personal items of value. EX: investments and equity in a personal items of value. EX: investments and equity in a home. home.

Capacity – Capacity – the lender’s primary concern is if you are able to the lender’s primary concern is if you are able to repay your loan. Employment history and income are key. repay your loan. Employment history and income are key.

Character – Character – does your credit record show you can pay your does your credit record show you can pay your debts. Good history of bill pay is important. debts. Good history of bill pay is important.

NOTES

Credit History Credit History is a record of your behavior is a record of your behavior related to borrowing and repaying loans.related to borrowing and repaying loans.

Credit Report Credit Report is a detailed record of your is a detailed record of your personal credit and financial transactions.personal credit and financial transactions.

Credit Score Credit Score is a rating used by credit is a rating used by credit reporting companies to help lenders decide reporting companies to help lenders decide whether and/or how much credit can be whether and/or how much credit can be extended to a borrower.extended to a borrower.

The Language of CreditThe Language of CreditNOTES

Good Tips & Bad TricksGood Tips & Bad Tricks

Pay your bills on timePay your bills on time

Set up an emergency Set up an emergency fundfund

Be choosy about loans Be choosy about loans and credit accountsand credit accounts

Maintain very low Maintain very low balances with frequent balances with frequent paymentspayments

Late Payments Late Payments

Bouncing ChecksBouncing Checks

Lots of different credit Lots of different credit lines and loanslines and loans

High Balances on your High Balances on your credit accountscredit accounts

Changing lenders Changing lenders frequentlyfrequently

NOTES

Your Free ReportYour Free ReportYou are entitled to see your credit report, and You are entitled to see your credit report, and

are allowed one free copy a year. are allowed one free copy a year.

You may need to write a letter to all credit You may need to write a letter to all credit agencies to correct errors. agencies to correct errors.

Credit reporting agencies must delete Credit reporting agencies must delete unfavorable information after seven years unfavorable information after seven years and bankruptcy after ten years. and bankruptcy after ten years.

TransUnion, Experian, and Equifax are the TransUnion, Experian, and Equifax are the three top credit reporting bureausthree top credit reporting bureaus

NOTES

AssignmentAssignment

1.1. Read the credit article posted on Mrs. Read the credit article posted on Mrs. Abel’s website under “file manager”Abel’s website under “file manager”

2.2. Complete the credit score worksheetComplete the credit score worksheet

Standards and ObjectivesStandards and ObjectivesState Standard(s) Addressed:CTE P.F #13) Identify strategies for good use of credit and effective debt management. Recognize debt problems and long-term consequences of debt and bankruptcy. Formulate a plan to eliminate debt and determine the impact debt may have on the personal budget.

Goal(s) Objective(s):1.Identify strategies for good use of credit and effective debt management.2. Recognize debt problems and long-term consequences of debt and bankruptcy. 3.Formulate a plan to eliminate debt and determine the impact debt may have on the personal budget.

Unit #3

Your Piece of the Credit PieYour Piece of the Credit Pie• Get at least one utility bill in your name, Get at least one utility bill in your name,

even if you are renting with roomies!even if you are renting with roomies!

• Get your first credit card from your own Get your first credit card from your own bank, because you have account history bank, because you have account history there. there.

• Next, you can look into small car loans.Next, you can look into small car loans.

NOTES

Deciding on your LoanDeciding on your Loan

1.1. Identify your credit goal. Identify your credit goal.

2.2. Gather information about lenders and Gather information about lenders and your options before applying.your options before applying.

3.3. Examine all alternatives, and get Examine all alternatives, and get clarification on options if needed. clarification on options if needed.

4.4. Analyze outcomes, and possible pitfalls. Analyze outcomes, and possible pitfalls.

5.5. Make a decision and apply. Make a decision and apply.

6.6. Evaluate the results of your application. Evaluate the results of your application.

NOTES

70%70%Living ExpensesLiving Expenses

10%10%Pay Pay Off Off

DebtDebt

20%20%Save or InvestSave or Invest

70/20/10 Rule of Thumb70/20/10 Rule of ThumbNOTES

•Spend 70% of income on living expenses.

•Save or Invest 20% for financial goals.

•Spend 10% on debt payments.

How to Avoid PitfallsHow to Avoid Pitfalls

1.1. Always read the fine print.Always read the fine print.

2.2. Avoid Higher interest rates. Avoid Higher interest rates.

3.3. Be picky on what you apply for. Be picky on what you apply for.

4.4. Pay the max you can every month.Pay the max you can every month.

5.5. Pay a bill at least a week before it is due.Pay a bill at least a week before it is due.

6.6. Arrange for automatic payments.Arrange for automatic payments.

7.7. Get into a savings mode, remember Get into a savings mode, remember P.Y.FP.Y.F

NOTES

Keeping Good RecordsKeeping Good Records

• Terms of Agreement: Keep or Download!Terms of Agreement: Keep or Download!

• Receipts: Prove your charges.Receipts: Prove your charges.

• Monthly Statements: keep 1 yr at a time.Monthly Statements: keep 1 yr at a time.

• Credit Card Information: keep a list of Credit Card Information: keep a list of your numbers and the customer service your numbers and the customer service contact in case of lost or stolen cards. contact in case of lost or stolen cards.

NOTES

Reducing DebtReducing Debt• Put away the plastic. Live on cash when Put away the plastic. Live on cash when

possible.possible.• Make personal commitments to pay all Make personal commitments to pay all

debts as soon as possible. They are YOUR debts as soon as possible. They are YOUR debts. debts.

• Be honest with yourself, how much do you Be honest with yourself, how much do you really owe! really owe!

• Create a repayment plan you can stick Create a repayment plan you can stick with. Pay higher interest accounts first!with. Pay higher interest accounts first!

NOTES

BankruptcyBankruptcyBankruptcy: is a legal process to get out of Bankruptcy: is a legal process to get out of

debt when you can no longer make your debt when you can no longer make your required payments. required payments. Chapter 7 – effectively allows you to erase most Chapter 7 – effectively allows you to erase most

of your debt. To qualify, you must be of your debt. To qualify, you must be unemployed or have very low income. unemployed or have very low income. Financial counseling is required. Financial counseling is required.

Chapter 13 – allows you to repay many of your Chapter 13 – allows you to repay many of your debts over a period of time, max five years. A debts over a period of time, max five years. A court usually oversees the repayment. court usually oversees the repayment.

NOTES

BankruptcyBankruptcy

• Not all debts are erased. Child support for Not all debts are erased. Child support for example and student loans stay. example and student loans stay.

• Stays on your credit for ten years. Loan Stays on your credit for ten years. Loan are almost impossible. are almost impossible.

• It is a costly process to you and your It is a costly process to you and your lenders. lenders.

NOTES

Fair Debt Collection Practices Fair Debt Collection Practices Act (FDCPA)Act (FDCPA)

Debt collector may not: Debt collector may not: Use abusive language.Use abusive language.

Call before 8am or after 9pm, or excessively. Call before 8am or after 9pm, or excessively.

Threaten to notify your employer or friends. Threaten to notify your employer or friends.

Attempt to collect more than you owe.Attempt to collect more than you owe.

Send you misleading letters that appear to be Send you misleading letters that appear to be from the government or the courts. from the government or the courts.

NOTES

AssignmentAssignment

You and a partner will work together to You and a partner will work together to create a power point presentation showing create a power point presentation showing how interest can work both for us how interest can work both for us (investments) and against us (debt). (investments) and against us (debt).

You will present this tomorrow. Follow the You will present this tomorrow. Follow the project rubric. project rubric.