Union Budget Analysis 2014-15

63

description

Analysis

Transcript of Union Budget Analysis 2014-15

1

Auto Components ...........................12-13

Automobiles ....................................14-15

Banking & Financial Serv .................16.17

Cement ...........................................18-19

Coal ......................................................20

Construction ...................................21-23

Consumer Durables ........................24-25

Education .............................................26

Engineering & Cap. Goods ..............27-28

Fertilizers .........................................29-30

FMCG ..............................................31-32

Gems & Jewellery ...........................33-34

Hospitals and Healthcare ................35-36

Hotels ...................................................37

IT and ITES .......................................38-39

Media ...................................................40

Mining and Minerals .......................41-42

Non-ferrous Metals .........................43-44

Oil and Gas ......................................45-46

Pipes ...............................................47-48

Ports .....................................................49

Power (incl renewables)..................50-51

Real Estate ......................................52-53

Roads and highways ........................54-55

Shipping ...............................................56

Steel ................................................57-58

Sugar ....................................................59

Textiles ............................................60-61

Warehouse/ Logistics ...........................62

TABLE OF CONTENTS Economic Survery 2013-14 .......................................................... 2-3

Railway Budget 2014-15 .............................................................. 4-5

Union Budget 2014-15 ............................................................... 6-11

Sectors

2

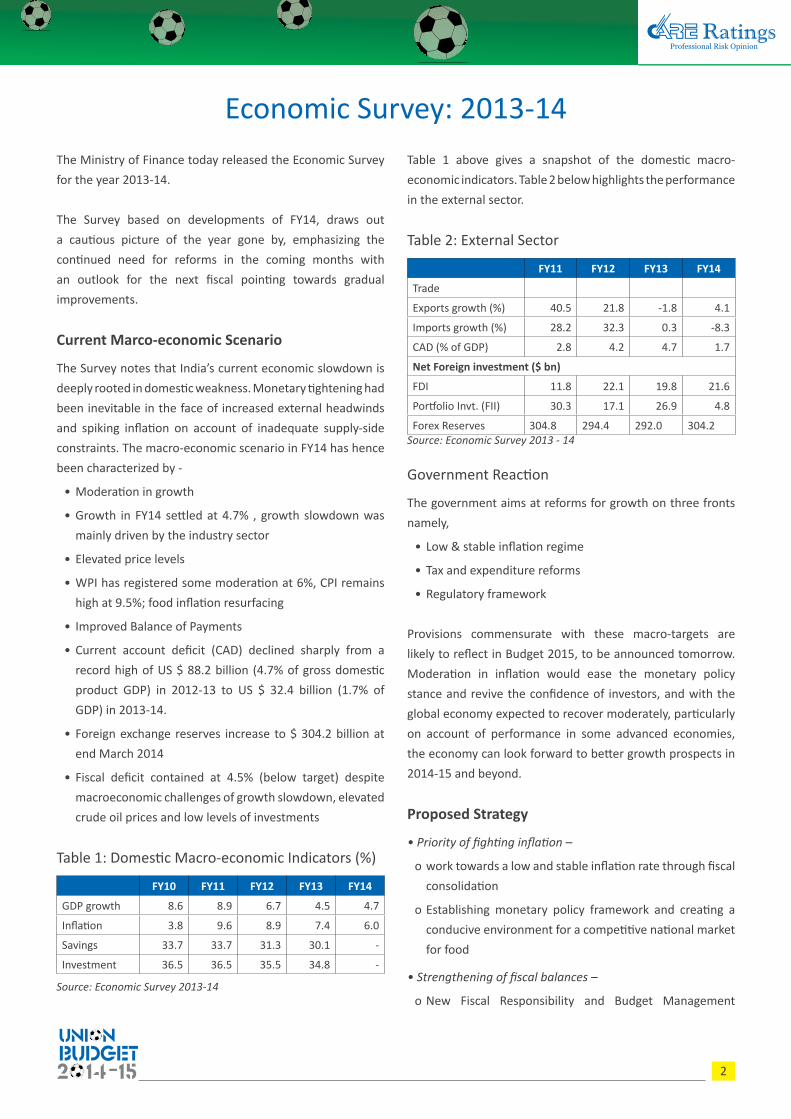

The Ministry of Finance today released the Economic Survey for the year 2013-14.

The Survey based on developments of FY14, draws out a cautious picture of the year gone by, emphasizing the continued need for reforms in the coming months with an outlook for the next fiscal pointing towards gradual improvements.

Current Marco-economic Scenario

The Survey notes that India’s current economic slowdown is deeply rooted in domestic weakness. Monetary tightening had been inevitable in the face of increased external headwinds and spiking inflation on account of inadequate supply-side constraints. The macro-economic scenario in FY14 has hence been characterized by -

• Moderation in growth

• Growth in FY14 settled at 4.7% , growth slowdown was mainly driven by the industry sector

• Elevated price levels

• WPI has registered some moderation at 6%, CPI remains high at 9.5%; food inflation resurfacing

• Improved Balance of Payments

• Current account deficit (CAD) declined sharply from a record high of US $ 88.2 billion (4.7% of gross domestic product GDP) in 2012-13 to US $ 32.4 billion (1.7% of GDP) in 2013-14.

• Foreign exchange reserves increase to $ 304.2 billion at end March 2014

• Fiscal deficit contained at 4.5% (below target) despite macroeconomic challenges of growth slowdown, elevated crude oil prices and low levels of investments

Table 1: Domestic Macro-economic Indicators (%)

FY10 FY11 FY12 FY13 FY14

GDP growth 8.6 8.9 6.7 4.5 4.7

Inflation 3.8 9.6 8.9 7.4 6.0

Savings 33.7 33.7 31.3 30.1 -

Investment 36.5 36.5 35.5 34.8 -

Source: Economic Survey 2013-14

Table 1 above gives a snapshot of the domestic macro-economic indicators. Table 2 below highlights the performance in the external sector.

Table 2: External Sector

FY11 FY12 FY13 FY14

Trade

Exports growth (%) 40.5 21.8 -1.8 4.1

Imports growth (%) 28.2 32.3 0.3 -8.3

CAD (% of GDP) 2.8 4.2 4.7 1.7

Net Foreign investment ($ bn)

FDI 11.8 22.1 19.8 21.6

Portfolio Invt. (FII) 30.3 17.1 26.9 4.8

Forex Reserves 304.8 294.4 292.0 304.2Source: Economic Survey 2013 - 14

Government Reaction

The government aims at reforms for growth on three fronts namely,

• Low & stable inflation regime

• Tax and expenditure reforms

• Regulatory framework

Provisions commensurate with these macro-targets are likely to reflect in Budget 2015, to be announced tomorrow. Moderation in inflation would ease the monetary policy stance and revive the confidence of investors, and with the global economy expected to recover moderately, particularly on account of performance in some advanced economies, the economy can look forward to better growth prospects in 2014-15 and beyond.

Proposed Strategy

• Priority of fighting inflation –

o work towards a low and stable inflation rate through fiscal consolidation

o Establishing monetary policy framework and creating a conducive environment for a competitive national market for food

• Strengthening of fiscal balances –

o New Fiscal Responsibility and Budget Management

Economic Survey: 2013-14

3

(FRBM) Act, better accounting practices and improved budgetary management

o Simple, predictable and stable tax regime - a single-rate goods and services tax (GST), a simple direct tax code (DTC), and a transformation of tax administration

o Prioritization of expenditure reforms involving three elements: shifting subsidy programmes away from price distortions to income support, a change in the focus of government spending towards provision of public goods, and a systems of accountability through a focus on outcomes

• Business Confidence –

o Increasing concern about the difficulties faced by firms

o Need to simplify processes including those relating to tax policy and administration.

• Well developed corporate market –Various policy reform measures were implemented in consultation with all market regulators and the Ministry of Corporate affairs (MCA) to improve the regulatory regime and stimulate the growth of the corporate bond market:

o Strengthening of the legal framework for regulation of corporate debt by amendments in SARFESI Act and Income Tax Act.

o Relaxation of investment guidelines for pension funds, provident funds, insurance funds, etc.

o Introduction of new products or removal of legal or regulatory constraints for nascent products such as covered bonds, municipal bonds, credit default swaps, credit enhancements, and securitization receipts.

o Amendment in definition of deposit in Companies (Acceptance of Deposits) Rules 1975.

o Development of securitized debt market by ensuring clarity in taxation policy for securitized debt.

o Rationalization of withholding tax (WHT) on FIIs for G-Secs and corporate bonds.

o Relaxation of investment norms of insurance / pension funds

o Insurance companies allowed participating in the repo market to increase liquidity. The RBI also reduced the minimum haircut requirement in corporate debt repo. Repo in corporate debt also permitted on commercial papers, certificates of deposit, and non-convertible debentures of less than one year of original maturity.

o Insurance companies and mutual funds allowed participating as market makers in credit default swap (CDS) market

o Setting up of central counter party (CCP) and creation of trade guarantee fund for trading in corporate bonds in stock exchanges.

o New trading platform and risk management system for corporate bonds including a centralized database on outstanding amount, settlement value, and traded volume to eliminate fragmentation of information

Outlook for FY15

• GDP growth likely to be in the range of 5.4% - 5.9%

o downside risks to the economy arising from a poor monsoon, the external environment and the poor investment climate

• CAD to be limited to around $ 45 billion, 2.1% of GDP

• Easing of supply-side constraints should lead to lower inflation, such that RBI has room to lower interest rates to boost investments and growth.

4

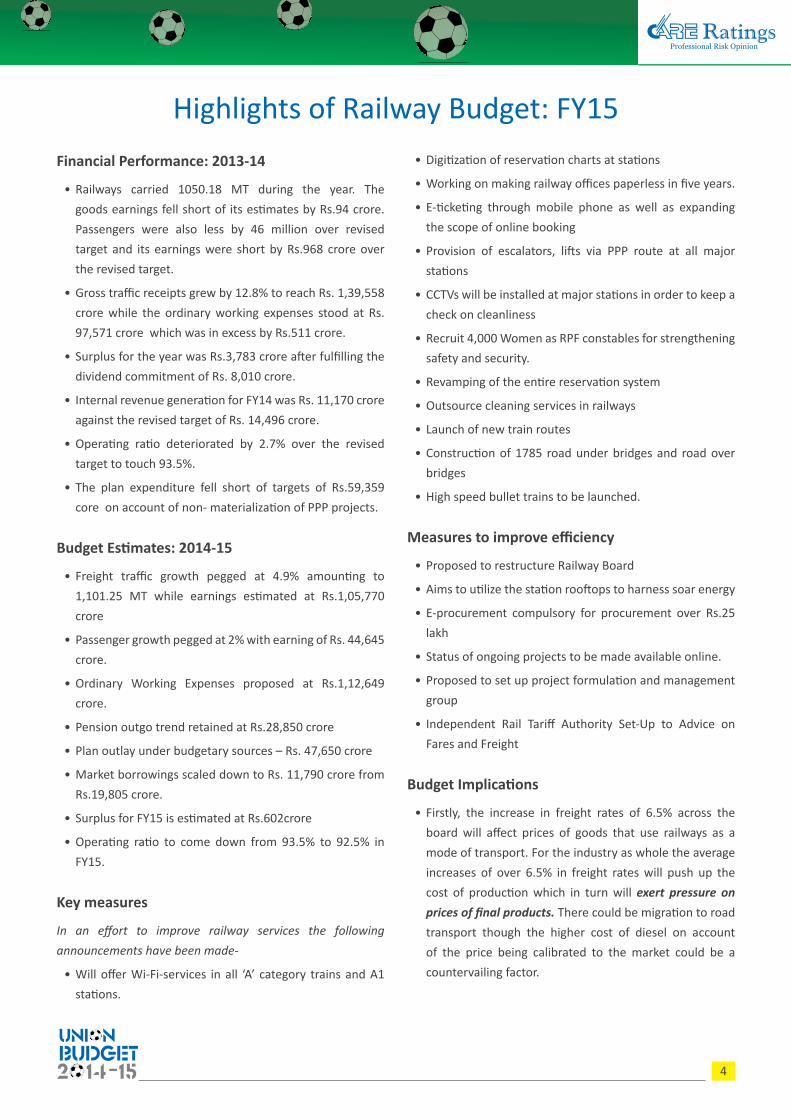

Financial Performance: 2013-14

• Railways carried 1050.18 MT during the year. The goods earnings fell short of its estimates by Rs.94 crore. Passengers were also less by 46 million over revised target and its earnings were short by Rs.968 crore over the revised target.

• Gross traffic receipts grew by 12.8% to reach Rs. 1,39,558 crore while the ordinary working expenses stood at Rs. 97,571 crore which was in excess by Rs.511 crore.

• Surplus for the year was Rs.3,783 crore after fulfilling the dividend commitment of Rs. 8,010 crore.

• Internal revenue generation for FY14 was Rs. 11,170 crore against the revised target of Rs. 14,496 crore.

• Operating ratio deteriorated by 2.7% over the revised target to touch 93.5%.

• The plan expenditure fell short of targets of Rs.59,359 core on account of non- materialization of PPP projects.

Budget Estimates: 2014-15

• Freight traffic growth pegged at 4.9% amounting to 1,101.25 MT while earnings estimated at Rs.1,05,770 crore

• Passenger growth pegged at 2% with earning of Rs. 44,645 crore.

• Ordinary Working Expenses proposed at Rs.1,12,649 crore.

• Pension outgo trend retained at Rs.28,850 crore

• Plan outlay under budgetary sources – Rs. 47,650 crore

• Market borrowings scaled down to Rs. 11,790 crore from Rs.19,805 crore.

• Surplus for FY15 is estimated at Rs.602crore

• Operating ratio to come down from 93.5% to 92.5% in FY15.

Key measures

In an effort to improve railway services the following announcements have been made-

• Will offer Wi-Fi-services in all ‘A’ category trains and A1 stations.

• Digitization of reservation charts at stations

• Working on making railway offices paperless in five years.

• E-ticketing through mobile phone as well as expanding the scope of online booking

• Provision of escalators, lifts via PPP route at all major stations

• CCTVs will be installed at major stations in order to keep a check on cleanliness

• Recruit 4,000 Women as RPF constables for strengthening safety and security.

• Revamping of the entire reservation system

• Outsource cleaning services in railways

• Launch of new train routes

• Construction of 1785 road under bridges and road over bridges

• High speed bullet trains to be launched.

Measures to improve efficiency

• Proposed to restructure Railway Board

• Aims to utilize the station rooftops to harness soar energy

• E-procurement compulsory for procurement over Rs.25 lakh

• Status of ongoing projects to be made available online.

• Proposed to set up project formulation and management group

• Independent Rail Tariff Authority Set-Up to Advice on Fares and Freight

Budget Implications

• Firstly, the increase in freight rates of 6.5% across the board will affect prices of goods that use railways as a mode of transport. For the industry as whole the average increases of over 6.5% in freight rates will push up the cost of production which in turn will exert pressure on prices of final products. There could be migration to road transport though the higher cost of diesel on account of the price being calibrated to the market could be a countervailing factor.

Highlights of Railway Budget: FY15

5

• The increase in freight rates (6.5%) and the increase in passenger fares (14.2%)together would result in additional revenue mop up of Rs 8,000 crore. This is likely to partly offset the increasing cost during the year.

• Passenger friendly measures such as e-ticketing system, e-ticketing through mobile phones, free Wi-Fi facilities in some trains, escalators and lifts at major stations, CCTVS to monitor stations, large scale computerization,platform and unreserved tickets through internet,etc.have been proposed. These initiatives will largely have a positive impact on various sectors particularly information technology (IT), telecommunication and engineering.

• Besides, expansion of railways with faster clearances of proposed projects in the pipeline will positively boost the demand for industries such as steel, aluminum cables, cement, solar equipment, electrical equipment, etc.

• The modernization of the railways through induction of technology will also help eliminate corruption and bring in more efficiency into the system.

• Share of freight traffic earnings shall increase furtheras no shift towards substitutes such as road transport is expected with hike in diesel prices already in place.

• The Budget provides significant opportunities for Public investments via PPP mode. It also seeks to bring in resources through FDI mode. Over Rs 6000 cr is to be mobilized through this route. To make it more attractive tax holidays have been proposed.

• Borrowings through IRFC would be Rs 11,790 cr, which presumably would be tax free bonds. This will be useful for households and complement any effort in the Union Budget to enhance the savings rate.

6

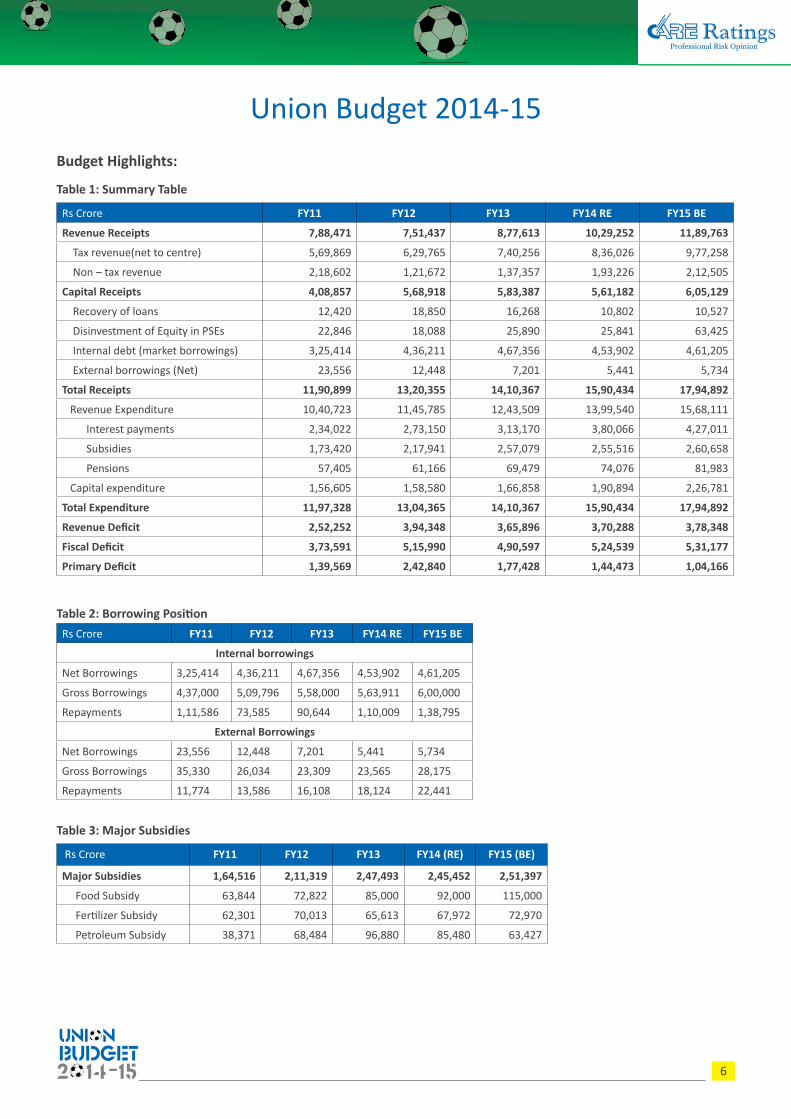

Budget Highlights:

Table 1: Summary Table

Rs Crore FY11 FY12 FY13 FY14 RE FY15 BE

Revenue Receipts 7,88,471 7,51,437 8,77,613 10,29,252 11,89,763

Tax revenue(net to centre) 5,69,869 6,29,765 7,40,256 8,36,026 9,77,258

Non – tax revenue 2,18,602 1,21,672 1,37,357 1,93,226 2,12,505

Capital Receipts 4,08,857 5,68,918 5,83,387 5,61,182 6,05,129

Recovery of loans 12,420 18,850 16,268 10,802 10,527

Disinvestment of Equity in PSEs 22,846 18,088 25,890 25,841 63,425

Internal debt (market borrowings) 3,25,414 4,36,211 4,67,356 4,53,902 4,61,205

External borrowings (Net) 23,556 12,448 7,201 5,441 5,734

Total Receipts 11,90,899 13,20,355 14,10,367 15,90,434 17,94,892

Revenue Expenditure 10,40,723 11,45,785 12,43,509 13,99,540 15,68,111

Interest payments 2,34,022 2,73,150 3,13,170 3,80,066 4,27,011

Subsidies 1,73,420 2,17,941 2,57,079 2,55,516 2,60,658

Pensions 57,405 61,166 69,479 74,076 81,983

Capital expenditure 1,56,605 1,58,580 1,66,858 1,90,894 2,26,781

Total Expenditure 11,97,328 13,04,365 14,10,367 15,90,434 17,94,892

Revenue Deficit 2,52,252 3,94,348 3,65,896 3,70,288 3,78,348

Fiscal Deficit 3,73,591 5,15,990 4,90,597 5,24,539 5,31,177

Primary Deficit 1,39,569 2,42,840 1,77,428 1,44,473 1,04,166

Table 2: Borrowing Position Rs Crore FY11 FY12 FY13 FY14 RE FY15 BE

Internal borrowings

Net Borrowings 3,25,414 4,36,211 4,67,356 4,53,902 4,61,205

Gross Borrowings 4,37,000 5,09,796 5,58,000 5,63,911 6,00,000

Repayments 1,11,586 73,585 90,644 1,10,009 1,38,795

External Borrowings

Net Borrowings 23,556 12,448 7,201 5,441 5,734

Gross Borrowings 35,330 26,034 23,309 23,565 28,175

Repayments 11,774 13,586 16,108 18,124 22,441

Table 3: Major Subsidies

Rs Crore FY11 FY12 FY13 FY14 (RE) FY15 (BE)

Major Subsidies 1,64,516 2,11,319 2,47,493 2,45,452 2,51,397

Food Subsidy 63,844 72,822 85,000 92,000 115,000

Fertilizer Subsidy 62,301 70,013 65,613 67,972 72,970

Petroleum Subsidy 38,371 68,484 96,880 85,480 63,427

Union Budget 2014-15

7

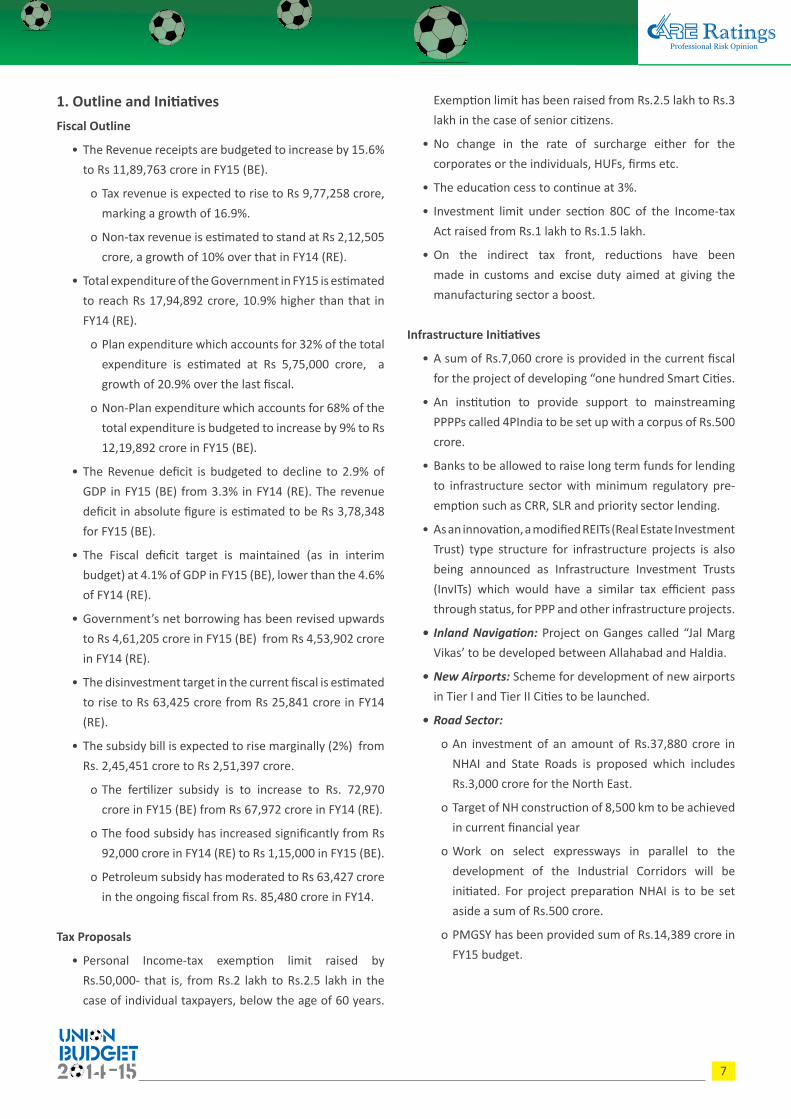

1. Outline and Initiatives Fiscal Outline

• The Revenue receipts are budgeted to increase by 15.6% to Rs 11,89,763 crore in FY15 (BE).

o Tax revenue is expected to rise to Rs 9,77,258 crore, marking a growth of 16.9%.

o Non-tax revenue is estimated to stand at Rs 2,12,505 crore, a growth of 10% over that in FY14 (RE).

• Total expenditure of the Government in FY15 is estimated to reach Rs 17,94,892 crore, 10.9% higher than that in FY14 (RE).

o Plan expenditure which accounts for 32% of the total expenditure is estimated at Rs 5,75,000 crore, a growth of 20.9% over the last fiscal.

o Non-Plan expenditure which accounts for 68% of the total expenditure is budgeted to increase by 9% to Rs 12,19,892 crore in FY15 (BE).

• The Revenue deficit is budgeted to decline to 2.9% of GDP in FY15 (BE) from 3.3% in FY14 (RE). The revenue deficit in absolute figure is estimated to be Rs 3,78,348 for FY15 (BE).

• The Fiscal deficit target is maintained (as in interim budget) at 4.1% of GDP in FY15 (BE), lower than the 4.6% of FY14 (RE).

• Government’s net borrowing has been revised upwards to Rs 4,61,205 crore in FY15 (BE) from Rs 4,53,902 crore in FY14 (RE).

• The disinvestment target in the current fiscal is estimated to rise to Rs 63,425 crore from Rs 25,841 crore in FY14 (RE).

• The subsidy bill is expected to rise marginally (2%) from Rs. 2,45,451 crore to Rs 2,51,397 crore.

o The fertilizer subsidy is to increase to Rs. 72,970 crore in FY15 (BE) from Rs 67,972 crore in FY14 (RE).

o The food subsidy has increased significantly from Rs 92,000 crore in FY14 (RE) to Rs 1,15,000 in FY15 (BE).

o Petroleum subsidy has moderated to Rs 63,427 crore in the ongoing fiscal from Rs. 85,480 crore in FY14.

Tax Proposals

• Personal Income-tax exemption limit raised by Rs.50,000- that is, from Rs.2 lakh to Rs.2.5 lakh in the case of individual taxpayers, below the age of 60 years.

Exemption limit has been raised from Rs.2.5 lakh to Rs.3 lakh in the case of senior citizens.

• No change in the rate of surcharge either for the corporates or the individuals, HUFs, firms etc.

• The education cess to continue at 3%.

• Investment limit under section 80C of the Income-tax Act raised from Rs.1 lakh to Rs.1.5 lakh.

• On the indirect tax front, reductions have been made in customs and excise duty aimed at giving the manufacturing sector a boost.

Infrastructure Initiatives

• A sum of Rs.7,060 crore is provided in the current fiscal for the project of developing “one hundred Smart Cities.

• An institution to provide support to mainstreaming PPPPs called 4PIndia to be set up with a corpus of Rs.500 crore.

• Banks to be allowed to raise long term funds for lending to infrastructure sector with minimum regulatory pre-emption such as CRR, SLR and priority sector lending.

• As an innovation, a modified REITs (Real Estate Investment Trust) type structure for infrastructure projects is also being announced as Infrastructure Investment Trusts (InvITs) which would have a similar tax efficient pass through status, for PPP and other infrastructure projects.

• Inland Navigation: Project on Ganges called “Jal Marg Vikas’ to be developed between Allahabad and Haldia.

• New Airports: Scheme for development of new airports in Tier I and Tier II Cities to be launched.

• Road Sector:

o An investment of an amount of Rs.37,880 crore in NHAI and State Roads is proposed which includes Rs.3,000 crore for the North East.

o Target of NH construction of 8,500 km to be achieved in current financial year

o Work on select expressways in parallel to the development of the Industrial Corridors will be initiated. For project preparation NHAI is to be set aside a sum of Rs.500 crore.

o PMGSY has been provided sum of Rs.14,389 crore in FY15 budget.

8

• Railways:

o A sum of Rs. 100 crore to be allocated for metro projects in Lucknow and Ahmedabad.

• Shipping:

o Rs.11,635 crore will be allocated for the development of Outer Harbour Project in Tuticorin for phase I.

o SEZs will be developed in Kandla and JNPT.

o Comprehensive policy to be announced to promote Indian ship building industry.

• Energy:

o 10 year tax holiday extended to the undertakings which begin generation, distribution and transmission of power by 31.03.2017

o An exercise to rationalize coal linkages to optimize transport of coal and reduce cost of power isbeing considered..

o Rs.400 crores provided for a scheme for solar power driven agricultural pump sets and water pumping stations.

o Rs.100 crore is allocated for a new scheme “Ultra-Modern Super Critical Coal Based Thermal Power Technology.”

o Comprehensive measures for enhancing domestic coal production are being put in place.

o The budget also proposes Rs.200 crore for power reforms along with Rs. 500 cr for rural power plan for New Delhi.

Social Initiatives

• New programme “Neeranchal” to give impetus to watershed development in the country with an initial outlay of Rs.2,142 crore.

• Allocation for National Housing Bank increased to Rs.8,000 crore to support Rural housing.

• An amount of Rs.50,548 crore is proposed under the Schedule Cast Plan and Rs. 32,387 crore under Tribal Sub Plan (TSP)- Schedule Tribe.

• For the welfare of the tribals “Van Bandhu Kalyan Yojna” launched with an initial allocation of Rs.100 crore.

• Outlay of Rs.50 crore for pilot testing a scheme on “Safety for Women on Public Road Transport”.

• Sum of Rs.150 crore on a scheme to increase the safety of women in large cities

• A sum of Rs.100 crore is provided for “Beti Bachao, Beti Padhao Yojana”, a focused scheme to generate awareness and help in improving the efficiency of delivery of welfare services meant for women.

Agriculture Initiatives

• A sustainable growth of 4% in Agriculture will be achieved in FY15

• An amount of Rs 100 crores set aside for Agri-tech Infrastructure Fund

• To mitigate the risk of Price volatility in the agriculture produce, a sum of Rs 500 crore is provided for establishing a Price Stabilization Fund

• Central Government to work closely with the State Governments to re-orient their respective APMC Acts

• A target of Rs 8 lakh crore has been set for agriculture credit during FY15

• Corpus of Rural Infrastructure Development Fund (RIDF) raised by an additional Rs 5000 crore

• Allocation of Rs 5,000 crore provided for the Warehouse Infrastructure Fund

• Long Term Rural Credit Fund” to set up for the purpose of providing refinance support to Cooperative Banks and Regional Rural Banks with an initial corpus of Rs 5,000 crore.

• Rs. 1,000 crore provided for “Pradhan Mantri Krishi Sinchayee Yojna” for assured irrigation.

• Restructuring FCI, reducing transportation and distribution losses and efficacy of PDS to be taken up on priority.

• New Urea Policy to be formulated

Industry Initiatives

• Rs. 100 crore provided for setting up a National Industrial Corridor Authority.

• Proposed to establish an Export promotion Mission to bring all stakeholders under one umbrella.

• Apprenticeship Act to be suitably amended to make it more responsive to industry and youth

• Sum of Rs 500 crore for developing a Textile mega-cluster at Varanasi and six more at Bareilly, Lucknow,

9

Surat, Kutch, Bhagalpur and Mysore

• Rs 10,000 crore provided through equity venture capital funds, quasi equity, soft loans and other risk capital specially to encourage new startups by youth to be set up in MSME sector

• Introduction of GST to be given thrust

Banking Initiatives

• Requirement to infuse Rs 2,40,000 crore as equity by 2018 in our banks to be in line with Basel-III norm

• Banks to be encouraged to extend long term loans to infrastructure sector with flexible structuring, to be permitted to raise long term funds for lending to infrastructure sector with minimum regulatory pre-emption such as CRR, SLR and Priority Sector Lending (PSL)

Financial Sector

• Introduction of uniform KYC norms and inter-usability of the KYC records across the entire financial sector.

• Introduce one single operating demat account.

• Uniform tax treatment for pension fund and mutual fund linked retirement plan.

2. Impact Analysis on various components of GDP(i) AgricultureThe government aims at a 4% growth in agriculture in this fiscal and to achieve this growth it plans to undertake various measures. The government has stated its aim for a second green revolution and has laid out measures to improve technology & investment to make the sector competitive. It has made allocation for the short & long term investment in the sector and for an agri – infrastructure fund. Higher provision of credit at Rs 8 lakh crore to agriculture marking a 20% increase over the agricultural credit last year while also being higher than the increase in overall credit disbursed by banks. This will help to improve the production and logistics for various crops. Also, the continuation of interest rate subvention is timely, as it will help provide the much needed funds to farmers and help ease their financial burden to an extent at a time when they are pressured by sub-normal monsoons. Other initiatives such as making allocations for warehousing and intent on reorienting the long overdue APMC Act would benefit both the producers and the

consumers. NREGA ProgrammeNREGA in the past has not been too successful in producing meaningful public assets. The government aims at redesigning the programme by providing employment for more productive, asset creation which has linkages to agriculture & allied activities. The allocation towards this programme has been retained at around Rs 33,000 crore.

(ii) InfrastructureTransportThe government has emphasized the need to accelerate infrastructure development. Government strategy to boost investments in infrastructure segment via PPP mode indicates an increased thrust on the sector. Budgetary allocations to the Ministry of Road Transport and highway for building National Highways and Ministry of Railways for high speed trains such as metros are expected to encourage the transportation and overall logistics segment in India. Increase in allocations to schemes such as PMGSY is expected to improve access for rural population. In addition, the proposed projects to be undertaken to develop roads, airports and railways will also aid in generating employment opportunities. Thus, improvement in overall connectivity across the states in turn shall aid particularly the manufacturing segment activities and drive the overall economic growth.

EnergyThe energy sector has been affected particularly due to shortage in coal thereby severely impacting thermal power generation. The government’s proposal to rationalize coal linkages will have a positive impact on the thermal power plants. Various incentives have been provided such as 10 year tax holiday extended to the undertakings which begin generation, distribution and transmission of power by 31.03.2017. This will further encourage new players to enter the power sector. In addition, the budget also proposes Rs.200 crore for power reforms along with Rs. 500 cr for rural power plan in order to make New Delhi a world class city. It also focuses on undertaking modern power projects. These measures are expected to have a positive impact on the power sector.

In order to boost infrastructure financing, the budget provides various financing measures. Firstly, it lays emphasis on the PPP mode to funds sources for infrastructure projects. Besides, the government has also proposed to allow banks

10

to raise long term funds for lending to infrastructure sector with minimum regulatory pre-emption such as CRR, SLR and priority sector lending. Given the increased planned outlay for infrastructure sector, the budget is expected to positive for the infrastructure segment.

(iii) Deficit The government retained the fiscal deficit target of 4.1% from the interim budget. The attainment of the targeted 4.1% of GFD (as a percentage of GDP in FY15), would be contingent on the overall growth of the economy and the consequent increases in revenue. With no major changes on the taxation and revenue front, growth in the same would have to be robust enough to help meet this target.

(iv) DisinvestmentThe government has set a disinvestment target of Rs 63,425 crore for the current fiscal, mainly driven by the current market conditions. There is a disconnection in the current economic conditions and the equity market movements. The movement in the market has been driven mainly by sentiment. With the stock market on an upturn, this could be the right time to offload equity into the market. However, the final decision taken on disinvestment would be company specific. Also it remain to be seen whether disinvestment of this magnitude would be one that involves the entire market or whether it would be done through cross holding of PSUs as has been the case in the past.

(v) Interest rate and liquidityThe long term gross market borrowing plan of the government for FY15 is in line with the envisaged plan in the interim budget at Rs 6,00,000 crore growing by 6.4% compared to last year. However since this amount is not very different from the earlier estimate in the interim budget, there is no pressure expected on the liquidity in the system. Gross borrowings in the form of external assistance are estimated to grow by 19.6% to Rs 28,175 crore from Rs 23,565 crore in FY14.

The net borrowing from the internal debt market is likely to increase slightly to Rs 4,61,205 crore in FY15 from 4,53,902 crore last year. The net borrowing under external assistance will grow by 5.4% to Rs 5,734 crore in FY15.

The implicit interest rate for FY15 appears to have fallen to 6.9% in FY15 from 7.13% in FY14 suggesting that the Government anticipates a decline in interest rate in the

ongoing fiscal. However, this is highly unlikely given the failed monsoon so far, uncertainty in oil prices. Moreover, it appears as though interest rates will continue to be inflation driven and hence are out of the budgetary context.

(vi) DebtPublic debt of the GoI is stated to rise by 11.9% in FY15 to Rs. 49,60,065 crore. Internal debt which accounts for 96% of the public debt is estimated to grow by 12.3% to Rs 47,71,602 crore and external debt will increase by a small 3.1% to Rs 1,88,463 crore. The other liabilities of the Government are estimated to rise by 11% to stand at Rs 62,22,658 crore in Fiscal ’15 from Rs 55,87,149 crore last year.

Table 3: Debt Profile (Rs Cr)

Rs crore FY13 (A) FY14 (RE) FY15 (BE)

Public Debt 39,41,855 44,33,026 49,60,065

Internal Debt 37,64,566 42,50,297 47,71,602

External Debt 1,77,289 1,82,729 1,88,463

Other liabilities 11,28,747 11,54,423 12,62,592

Total debt 50,70,601 55,87,449 62,22,658

(vi) Financial Services: ImpactCapital MarketsThe extension of the 5% withholding tax on all corporate debt issued by Indian corporates abroad would bring about the much needed uniformity in tax treatment of investors. This move could help attract foreign investors towards Indian corporate bonds thereby deepening the bond market. It would also aid corporates in tapping the bond markets to raise funds.

The Government reiterated the importance of deepening the bond market and the currency derivative markets in the country and regulators were urged to lower restrictions on the same.

Single KYC norms and demat account to apply across the entire financial system. This would help households dealing in these markets.

(vii) Inflation: Macro impactWhile the budget announcements are not likely to have any immediate impact on inflation, there are certain steps in the right direction when viewed from the long term perspective. The following conjectures can be drawn based on the announcements and estimates in the budget.

11

• The reduction in the duties of manufactured items could ease inflationary pressures in these items.

• The reduction in petroleum subsidy would result in an increase in the prices of petroleum products to be borne by consumers. Petroleum prices could be further pressed by the unrest in Iraq.

• The Government is to increase the warehousing capacity for increasing the shelf life of agriculture produce. Additional scientific warehousing infrastructure in the country will also be set up. This will preserve the earning capacity of farmers and ease the price volatility of agriculture produce.

12

Auto Components Industry Snapshot:

During the last decade strong growth scenario in automobile sales has fuelled growth in the auto component industry. Apart from rising demand from local OEMs, the industry also got boost by the entry of global automobile OEMs to seize low-cost advantage of manufacturing in India.

Growing income levels during last one decade translated into strong automobile sales which in turn resulted in high demand for OEM segment. However, last couple of years were challenging for OEM segment due to strained demand for new vehicles from domestic as well as exports market.

The replacement segment had hardly any impact of the economic slowdown on account of the huge existing vehicle population. Moreover, the relatively faster increase in the density of roads has led to greater passenger & cargo movement by roads vis-à-vis rail which too has added to replacement demand.

CARE Ratings believes auto component manufacturers have to derive new strategies like expanding product offering to cater larger end user industry base, focusing on exports markets, improving technology, etc. to negate the impact of demand slowdown. Moreover, the industry would also be benefited on the back of increasing localisation drive by global OEMs in order to cut down cost combined with rising exports. However, complete revival of auto component industry largely depends on recovery of OEM segment which forms around 62 per cent of the industry turnover.

Duty Structure

Customs Duty (%) Before After Impact Excise Duty (%) Before After Impact

Engine & engine parts, except the below-mentioned

7.5 7.5 = Engine & engine parts 12 12 =

Silencer, exhaust pipes & radiators

10 10 = Drive transmission, steering, suspension & braking parts

12 12 =

Drive transmission, steering, suspension & braking parts, except the below-mentioned

10 10 = Spark plug, distributors, ignition coils & starter motors

12 12 =

Couplings & seals 7.5 7.5 =Spark plug, distributors, ignition coils & starter motors

7.5 7.5 =

Proposal and Impact

Budget proposals Impact on the IndustryPre-budget announcement of extension of excise duty rebate till December 31, 2014, was reiterated by the Finance Minister.

Lower excise duty would translate into lower vehicle prices; consequently, induce growth in demand which would in turn lead to higher demand for auto components.

13

Impact on Companies

Company Impact Comments

Bharat Forge Ltd. +

Pre-budget extension of excise duty cut for automobile industry would boost vehicle demand which would translate into higher demand for auto ancillaries.

Bosch Ltd. +Exide Industries Ltd. +Motherson Sumi Ltd +Sona Koyo Steering Systems Ltd. +WABCO India Ltd. +

14

AutomobilesIndustry Snapshot:

The automobile industry is sensitive to economic cycles. Factors like interest rates, fuel prices, disposable income, inflation, consumer confidence etc. have strong influence on the industry demand. However, the extent of cyclicality differs across passenger vehicles (PV), commercial vehicles (CV) and two-wheeler (TW) industry. For instance, medium and heavy commercial vehicle (M&HCV) along with PV industry is highly sensitive to factors like interest rates, fuel prices and consumer spending whereas TW and light commercial vehicles (LCV) are comparatively less sensitive to the aforesaid factors.

The PV industry bore the brunt of economic slowdown during FY14 on account of high interest rates coupled with high inflation and spiralling fuel prices. The CV industry was worst hit in FY14 witnessing sharp drop in growth levels as low freight demand disallowed fleet expansion by transport operators. The TW industry witnessed a moderate growth due to low dependence on financing and support from rural demand as the rural economy thrived on account of good monsoon last fiscal.

In a year when vehicle sales were trembling across segment in automotive sector, scooters segment continued to flourish owing to the improved mileage and unisex appeal of newer breed of scooters. UVs and LCVs which were the other star performers during past couple of years failed to continue growth momentum against economic headwinds.

While the fundamentals for the sector remain intact, growth is currently constrained by the general economic slowdown. Interest rates, fuel pricing, infrastructure and agriculture spending would be decisive factors for automobile sector to emerge out of the current slump in the short term.

Duty Structure

Customs Duty (%) Before After Impact Excise Duty (%) Before After Impact

Passenger Cars Small Cars* 8 8* =Old 105 105 = Mid-size Cars@ 20 20* =New 100 100 = Large Cars# 24 24* =Two Wheelers SUV 24 24* =Old 105 105 = Buses 8 8* =New 60 (75^) 60 (75^) = Trucks 8 8* =Two Wheeler Two Wheeler 8 8* =Old 10 10 = Three Wheeler 8 8* =New 10 10 = Hybrid Vehicles 5 5* =

N o t e : *Indicates cars which have engine capacity less than 1,500cc in case of diesel and 1,200cc in case of petrol and length less than 4 meters.

@ Indicates cars which have engine capacity less than 1,500cc in case of diesel and 1,200cc in case of petrol and length more than 4 meters.

#indicates cars having engine capacity more than 1,500cc in case of diesel cars and 1,200cc in case of petrol and length exceeding 4 meters.

Definition of SUV as per central excise department is a vehicle with engine capacity greater than 1,500cc, length exceeding 4000mm and ground clearance 170 mm and above

^ Indicates motorcycle with engine capacity > 800 cc

* Excise duty rebate provided during Interim budget 2014-15 is extended in the Union Budget 2014-15 until 31st December, 2014.

15

Proposal and Impact

Budget proposals Impact on the Industry

Pre-budget announcement of extension of excise duty rebate till December 31, 2014, was reiterated by the Finance Minister.

Automobile demand has been constrained on account of higher ownership cost of vehicles on account of high fuel and financing costs coupled with lower propensity to spend owing to lower job prospects, low growth in income levels and high inflation level. However, lower excise duty would translate into lower vehicle prices, consequently, induce growth in demand.

Hike in agriculture credit from Rs.700,000 crore to Rs.800,000 crore Improved rural liquidity, thereby push demand for Tractors and TWs.

Extension of interest rate subvention scheme for crop loans Improved rural liquidity, thereby push demand for Tractors and TWs.

Impact on Companies

Company Impact Comments

Maruti Suzuki India Ltd + Pre-budget extension of excise duty cut coupled with improved rural liquidity goes in favor of Maruti as rural sales form a sizable portion of total sales of the company.

Ashok Lyeland Ltd. + Pre-budget extension of excise duty cut coupled with higher allocations towards both rural and urban infrastructure would push demand for M&HCV.

Hero Motocorp Ltd + Pre-budget extension of excise duty cut coupled with improved rural liquidity goes in favor of Hero as rural sales form a sizable portion of total sales of the company.

Bajaj Auto Ltd. + Pre-budget extension of excise duty cut would help company keep vehicle prices low which would in turn result in higher demand.

16

Banking & Financial ServicesIndustry Snapshot:

Banks The banking sector has a very high correlation with the overall economic growth in the country. During

FY14, the overall economy continued to witness moderation in growth with GDP growth at 4.7%. The manufacturing sector saw negative growth at -0.7% during the year while sectors like construction and services sector witnessed low growth. As a result, the credit growth during FY14 was also muted at around 14% supported by growth in sectors like services, agriculture and personal loans. The muted economic scenario impacted the overall performance of banks as indicated in deterioration in asset quality leading to higher provisioning costs and moderation in income impacting profitability besides moderated credit growth. The Gross NPA ratio for the banks increased from 3.31% as on March 31, 2013 to 3.91% as on March 31, 2014. Although both the profitability and asset quality of the banks was impacted, currently the Indian banks remained adequately capitalised with median Capital Adequacy Ratio (CAR) of around 11.5% (under Basel III). During FY14, interest rates continued to be at an elevated level, given the Reserve Bank of India’s (RBI) focus on controlling inflation.

During FY15, RBI is likely to keep its focus on inflation in view of uncertain monsoon, due to which the interest rates are likely to remain more or less stable during the year. CARE’s GDP growth forecast for FY15 is expected to improve gradually to 5.2% to 5.5% considering the new government’s plan to focus more on investment in the infrastructure sector, time bound action and improved co-ordination between the Central and State Governments to ensure smooth implementation of new Government policies. The improvement in overall economic growth and governmental clearances in projects would help recovery in sectors like infrastructure and manufacturing which may result in stabilisation of the asset quality of banks and propel credit growth in the range of 16% to 18% during FY15.

In addition to fund the uptick in credit growth, the banks would be required to raise substantial equity capital in the next 4-5 years to comply with the Basel III guidelines. With public sector banks having over 70% market share, the government would be required to infuse equity capital in the banks. As per CARE’s estimates, the total equity capital requirement for Indian banks till March 2019 (when Basel III would be fully implemented) is likely to be in the range of Rs.1.5-1.8 trillion assuming that the economic growth picks up (estimated average GDP at 6%) and the average credit growth is in the range of 15% to 16% over the next five years.

Housing Finance Companies Strong demand due to low penetration of housing finance especially from Tier II and III cities, increasing urbanization, tax

incentives and stable asset quality have helped the Housing Finance Companies (HFCs) witnessed a growth of around 16% - 17% in their loan portfolio during FY14. The Gross NPA ratio for HFCs was in the range of 0.75% to 0.80% as on March 31, 2014 as compared to 0.65% to 0.70% as on March 31, 2013. Most of the HFCs remained adequately capitalized. The credit growth for HFCs is projected in the range of 18% to 20% (CAGR) during FY14-FY16 mainly led by demand in Tier-II and Tier-III cities.

In the budget for FY14, the Congress led government had introduced Section 80EE in the Income Tax Act which provided additional deduction to first time home buyers in respect of interest on loan taken for residential house property for loans sanctioned during the period April 1, 2013 to March 31, 2014. The value of the house should not be more than Rs.40 lakh and the amount of loan availed should not be more than Rs.25 lakh. The scheme had helped home buyers in Tier II and Tier III cities wherein the housing ticket size are under Rs.25 lakh. However, there was no amendment/extension in the interim budget for FY15. HFCs are expecting an extension of the scheme in the budget for FY15 to help increase their business.

17

Proposal and Impact

Budget proposals Impact on the Industry

Capitalisation of banks by way of increasing public shareholding in banks. Government to maintain majority shareholding in public sector banks.

Government maintaining the majority shareholding in the public sector banks is a credit positive while greater autonomy and making banks accountable should improve the performance of banks in the medium term.The interim budget had an allocation of Rs.11,200 crore for capitalisation of public sector banks, however, large part of capitalization of the banks now would be through capital markets.

Establishment of six new Debt Recovery Tribunals Likely to help early resolution of troubled assets.Banks will be permitted to raise long term funds for lending to infrastructure sector with minimum regulatory preemption such as CRR, SLR and Priority Sector Lending (PSL).

Raising long term funds will help banks to manage their asset –liability mix better to allow them to lend to the infrastructure sector.

Additional incentive of 3% for timely payment of concessional agriculture loan given at 7% under the Interest Subvention Scheme for short term crop loans.

Additional incentive will help improve credit culture among the farmers and have positive impact on the asset quality of banks.

Sum of Rs.7,060 crore to develop ‘Smart Cities’, as satellite towns of larger cities and by modernizing the existing mid-sized cities.

This growth in urbanization will provide growth opportunities for banks and HFCs.

The increased allocation to Rs.8,000 crore for National Housing Bank (NHB) for Rural Housing Fund

The Government’s continued thrust on providing low cost affordable housing is a positive for HFCs.

Sum of Rs.4,000 crore from the priority sector lending shortfall to support affordable housing to economically weaker segments (EWS) and low income group segment (LIG)

The Government’s continued thrust on providing low cost affordable housing is a positive for HFCs and banks.

Increase the deduction limit on account of interest on loan in respect of self-occupied house property from Rs.1.5 lakh to Rs.2 lakh

Help banks and HFCs business growth.

Proposed ‘Long Term Rural Credit Fund’ in NABARD for the purpose of providing refinance support to Cooperative Banks and Regional Rural Banks with an initial corpus of Rs.5,000 crore.

Improve the long term investment in credit in the agriculture sector and provide funding to Regional Rural Banks (RRB) and Co-operative Banks.

Allocation of Rs.50,000 crore to Short Term Cooperative Rural Credit (STCRC) – Refinance Fund.

Provide lower cost fund to NABARD and in turn help increased and timely credit to farmers.

The composite cap in the Insurance sector proposed to be increased from 26% to 49%, with full Indian management and control, through the FIPB route.

Positive impact on the insurance sector as it will bring in more foreign investment in the sector which will help the growth in the sector.

Increase in capital gains arising on transfer of units of non-equity mutual funds, held for more than a year from 10% to 20%. The holding period for such units is increased from 12 months to 36 months

Likely to shift investments from debt funds to bank deposits and other instruments.

18

CementIndustry Snapshot:

The Indian cement industry witnessed a dismal demand growth in the past few years. In FY14, the consumption of cement showed a tepid growth of 3.5 per cent on a YoY basis, the lowest growth over the last one decade.

The slowdown in the real estate sector and delay in takeoff of various infrastructural projects in the period FY11-14 took a toll on the cement demand. Spiralling cost of capital, delays in execution of infrastructure as well as industrial projects on account of land acquisition & environmental clearance hurdles and the overall economic slowdown adversely affected the offtake of cement.

Though the demand for cement in the long term remains intact, the demand for cement is expected to show a gradual recovery in the short to medium term. The newly elected government is expected to focus on strengthening the infrastructure in the country. Also, focus on low-cost affordable housing and revival in overall economic growth is expected to provide some respite to the cement demand.

The cement industry has been grappling with cost pressure in the past few months due to raise in the railway freight cost and diesel prices. However, the industry has managed to pass on the higher input cost through a series of price hikes in the same period.

Duty Structure

Customs Duty (%) Before After Impact Excise Duty (%) Before After Impact

Cement Cement

OPC/PPC/PSC#- Basic- CVD- Special CVD

Nil12

4

Nil12

4

= - Retail 12*+Rs.120/t

12*+Rs.120/t

=

Clinker- Basic- CVD- Special CVD

1012

4

1012 4

= - Bulk 12# 12 =

- Clinker 12 12 =*An abatement of 30% on Retail Sale price and is on adveloram, # on adveloram, # OPC- Ordinary Portland cement, PPC- Portland pozzalana cement and PSC- Portland slag cement.

19

Proposal and Impact

Budget proposals Impact on the Industry• Key schemes announced1) Concession on requirement (Built up area and capital) for FDI for development of

smart cities.2) Enhancement of allocations for the year 2014-15 to Rs.8,000 crore for Rural

Housing via National Housing Bank (NHB).3) Allocate of Rs.4,000 crore for NHB with a view to increase the flow of cheaper

credit for affordable housing to the urban poor/EWS/LIG segment.4) Inclusion of slum development in the list of Corporate Social Responsibility (CSR)5) Porposal to award 16 new port projects worth Rs.11,635 crore in this year6) Investment in National Highways Authority of India and State Roads of an amount

of Rs.37,880 crore, including Rs.3,000 crore for the North East. 7) Setting aside Rs.14,389 crore for PMSGY

The said schemes/ measures to boost infrastructure and housing segments. This is expected to spur cement demand.

• Increase of custom duty on coalThis would result in marginal increase in cost of production of cement by about Rs.0.15 per bag.

Impact on Companies

Company Impact Comments

Ultratech Cement + Various schemes announced to have a positive impact on the demand. However, increase in custom duty on steam coal to result in marginal increase in cost of production.

ACC +Ambuja +Indian Cement +

20

CoalIndustry Snapshot:

Indian coal industry’s domestic production/off-take stood at 567/582MT in FY14 (refers to the period April 01 to March 31). Against this the demand for coal stood at 722MT in FY14 resulting in deficit of 19.3%, which was met through import. CARE expects Indian coal production to reach 690MT for the base case scenario implying a 5.5% CAGR from FY14-FY17. The growth in coal production would be contributed by Coal India Limited (CIL) (expected to reach 564MT implying 5.7% CAGR during FY14-FY17E) and 7% production CAGR from the captive mines (68.7MT in FY17E). The demand of coal is expected to grow at 5.4% for the same period translating into higher reliance on imported coal which is expected to reach to 148.8MT by FY17E.

Over the past one year, various policy measures like coal price pooling, coal banking, etc, have been proposed in order to tide over the coal deficit in the country. While there have been several policy announcements the implementation remains tardy due to lack on consensus among various stakeholders.

Duty Structure

Customs Duty (%) Before After Impact

Non-Coking Coal 2% 2.5% =Coking Coal Nil 2.5% =Non-coking & coking Coal (Counter Veiling Duty)

2% 2% = Met coke Nil 2.5% =Clean Energy Cess Rs50/tonne Rs100/tonne =

Impact on Companies

Company Impact Comments

Coal India Limited = Since, energy cess is pass-through, Coal India Limited would not be impacted.

21

ConstructionIndustry Snapshot:

Construction is integral to support India’ growing need for infrastructure and industrial development. In the last 10 years, construction as a percentage of gross domestic product (GDP) has been in the range of 7.43% to 8.10%. The industry witnessed a slowdown in the last couple of years mainly on account of slowdown in the economy, delay in project awarding and execution due to environmental clearance hurdles, aggressive bidding by players, land acquisition issues and political instability in some states.

As on March 31, 2014, the multiple of order backlog to the net sales of the major construction companies stood at around 2.9 times.

Raw material cost accounts for about 40% of the total cost of a construction company of which cement and steel are the major inputs. Rising input costs alongwith other factors like high interest on increased debt burden resulted into a declining trend in profitability margins in the last couple of years. With the revenue of the industry growing at a snail’s pace; coupled with the rising cost pressure, the PBDIT margin of the industry is expected to remain under pressure in the short term.

Duty Structure

Excise Duty (%) Before After Impact

Cement Retail 12% ad-valorem* + Rs. 120 per tonne 12% ad-valorem* + Rs. 120 per tonne =Cement Bulk 12% ad-valorem* 12% ad-valorem* =Steel 12% 12% =

*An abatement of 30% on the Retail Sale Price.

22

Proposal and Impact

Budget proposals Impact on the IndustryRoads:A huge investment of Rs.37,880 crore (including Rs.3,000 crore for North East) is proposed in NHAI and state roads along with measures to reduce maze of clearances as the government intends to construct national highways of 8,500 km during FY15. Government intends to set up National Industrial Corridor Authority; with a view to give impetus to transport connectivity which will lead to India’s growth in manufacturing and urbanization. Improving supply chain for faster transport of goods to various cities would be done by working on select expressways along with development of industrial corridor. NHAI shall be required to set aside Rs.500 crore for project preparation of the same.

The continual increased focus of the government on infrastructure development especially roads, smart cities, ports, watershed development, airway, and waterway would be beneficial for the construction sector in terms of providing increased orders.

AirportsTo improve air connectivity and make air travel an accessible option for large number of Indians, a scheme for development of new airports in tier-I and tier-II is expected to be launched through Airport Authority of India or PPPs.RailwaysThe Railway Budget for FY15 proposed construction of 1785 road under bridges and road over bridges and provision of escalators, lifts via PPP route at all major stations. It also focused on expansion of rail infrastructure with faster implementation of projects planned.The Union Budged 2014 proposes construction of urban metros including light rail systems through PPP mode to be supported by the central government through Viability Gap Funding (VGF). During FY15 government intends to set aside Rs. 100 crore for metro projects in Lucknow and Gujrat.Further, a sum of Rs. 1,000 crore is provided towards rail connectivity in border areas and an additional Rs. 1,000 crore is provided for rail connectivity in North Eastern states.

Ports To boost trade, 16 new port projects are expected to be awarded with a focus on port connectivity. Rs.11,635 crore is expected to be allocated for the development of Outer Harbour Project in Tuticorin for phase-I. SEZs are also expected to be developed in Kandla, Gujarat and JNPT, Maharashtra. Inland waterwaysDevelopment of inland waterways through construction of Jal Marg Vikas (National Waterways – I) between Allahabad and Haldia covering a distance of 1,620 Kms. It would enable commercial navigation of vessels with atleast 1,500 tonne capacity at an estimated cost of Rs. 4,200 crore.Smart cities: The PM’s vision of developing ‘100 smart cities’ as satellite towns of larger cities and modernizing the existing mid-sized cities would be done through allocation of Rs.7,060 crore Requirement of built-up area and capital conditions for FDI is reduced from 50,000 sq mtrs to 20,000 sq mtrs and from USD 10 million to USD 5 million with a 3 year post completion lock-in period. To increase impetus to watershed development in the country, a new programme called ‘Neeranchal’ has been introduced with an initial outlay of Rs.2,142 crore in FY15.

23

FinancingBanks would be encouraged to extend long term loans to infrastructure sector with flexible structure to absorb potential adverse contingencies. For the same, banks could raise long-term funds for lending to infrastructure sector with minimum regulatory preemption such as CRR, SLR and priority sector lending.Corpus towards the Pooled Municipal Debt Obligation is increased from Rs. 5,000 crore to Rs. 50,000 crore and also extended upto March 31, 2019.

Ensuring funding support from banks through relaxation of norms for lending to infrastructure sector will be an impetus to construction industry. The increased corpus towards Pooled Municipal Debt Obligation is expected to finance public transport, solid waste disposal, sewerage treatment and drinking water projects in urban areas.

Impact on Companies

Company Impact Comments

Hindustan Construction Company Limited +

Increased allocation towards various infrastructure projects is expected to result in increased order inflow to the construction companies along with improved funding avenue from banks.

NCC Limited +Gammon India Limited +IVRCL Infrastructures and Projects Limited +Sadbhav Engineering Limited +Simplex Infrastructures Limited +Patel Engineering Limited +

24

Consumer DurablesIndustry Snapshot:

The Consumer Goods industry is broadly classified into consumer appliances and consumer electronics. Consumer appliances, also popularly known as White Goods include refrigerators, sewing machines, washing machines, air conditioners, microwave ovens, fans etc. Consumer electronics, widely referred to as Brown Goods include Televisions, Mobile phones, CD and DVD players, kitchen appliances etc. These goods include various kinds of domestic appliances used on a regular basis to facilitate our day to day living.

The Indian Consumer Goods industry, one of the largest growing electronics market in the world is characterised by presence of large domestic producers (Videocon, MIRC electronics, Bajaj Electricals, Godrej, Blue Star, Voltas, TTK Prestige, etc) and strong MNCs (Multinational Companies) like Sony, Samsung, LG, Whirlpool etc. have healthy presence in most of the product categories they are present. The size of the industry is estimated at around Rs 400 billion during FY13. Global players dominate this space and have around 65% market share of the Indian Consumer Goods Industry.

The urban market forms a major chunk (i.e. 65%) of revenues of the industry. The key growth drivers are rising income levels, easy availability of consumer credit, various policy support from the government like relaxation in customs duties and excise duty, encouragement to FDI policies in the sector, awareness of brands and products, change in lifestyle, new model launches with technological improvements and ease of shopping through various online formats. Further, large domestic market with growing youth population, lower penetration levels in rural areas and lower per capita daily consumption indicates opportunities for further growth of thisindustry.

The key challenges faced by the players in the industry are volatile input prices, slowdown in GDP growth, adverse monsoon, high inflation, high interest rates, intense competition, high advertisement costs and currency depreciation.In a view to boost the consumerdemand, the Interim Union Budget for 2014-15, has slashed excise duty across the consumer durable categories. This excise duty cut is applicable till 30th June, 2014. CARE Ratings expects these challenges to remain in the short term and growth in domestic demand for the sector would be impacted to some extent. However, the long-term prospects for the industry would remain healthy on the back of growth expected from rural demand as a result of higher disposable rural income, low penetration in rural markets, improvement in GDP growth rate and various measures expected to be undertaken by GOI (Government of India) like simplification of tax structure through introduction of GST etc. CARE Ratings estimates the Consumer Goods Industry to grow by around 10% on CAGR basis during FY13-FY18.\

Duty Structure

Customs Duty (%) Before After Impact Excise Duty (%) Before After Impact

Cathode ray TVs 10 0 + Electrical manufacturing and equipments (chapter 85)*

10 10 =

LCD/LED TV panels of below 19 inches

10 0 +E-Book Reader 7.5 0 +

*The Union Budget 2014-15 has proposed to extend duty concessions beyond June 30, 2014 for a period of 6 months up to December 31, 2014

25

Proposal and Impact

Budget proposals Impact on the IndustryBasic customs duty on cathode ray TVs, LCD/LED TV panels of below 19 inches reduced from 10% to Nil The reduction in customs duty will be positive for the industry as it

will increase the demand for the products due to decrease in cost and will discourage sales in the grey market.Basic customs duty on E-Book Reader reduced from

7.5% to NilExcise duty on electrical manufacturing and equipments (chapter 85) is to be maintained at 10% for a further period of 6 months upto December 31, 2014

The extension of concession in excise duty till December 31, 2014 will provide much needed relief needed to revive the industry.

Impact on Companies

Company Impact Comments

Mirc Electronics Ltd +The proposed reduction in customs duty would positively impact the demand for LCD/LED TV panels of below 19 inches which would consequently increase the revenues.

26

EducationIndustry Snapshot:

Education sector in India is a mix of government-operated & privately operated educational institutions and allied education products & services providers. Educational sector is highly influenced by the various government schemes and policies launched primarily to improve the quality of education and the planned expenditure by government to improve the literacy level in the country. The government has been laying a lot of emphasis on increasing the reach and quality of the education system in the country and this has also provided increasing opportunities for private sector players engaged in providing education and also related allied products / services. In the past, the government had initiated several schemes including the Sarva Shiksha Abhiyan and Rashtriya Madhymik Shiksha Abhiyan to improve the quality of education and eventually the literacy level in the country.

In the interim budget presented in February 2014, the central government’s yearly allocation towards the education increased by 21% to Rs.79,451 crore for 2014-2015 as against Rs.65,867 crore allocated in the budget for 2013-2014 . Additionally there was budget allocation of Rs.2,600 crore for taking over partial interest burden on education loans outstanding as on December 31, 2013 and availed by students prior to 31/03/2009 as an extension of similar scheme extended in the previous budget. This was expected to benefit over 9 lakh student borrowers.

The budget for 2013-14 also had allocations of Rs.27,258 crore for Sarva Shiksha Abhiyan and Rs.3,983 crore for Rashtriya Madhymik Shiksha Abhiyan in addition to Rs.5,284 crore provided to various ministries for giving scholarships to students belonging to Scheduled Castes, Scheduled Tribes, Other Backward Classes and Minorities, and girl children and Rs.13,215 crore towards mid day meal scheme.

The growth in the Indian Education sector would be driven by growing personal disposable incomes, increasing government spend and also efforts of government to improve the regulatory framework for the education sector.

Proposal and Impact

Budget proposals Impact on the IndustryBudgetary allocation to SSA at Rs.28,635 crore The government reemphasized its focus on school education with

y-o-y increase in government expenditure on various schemes. This continued focus on school education with an objective of increasing gross enrollment ratio is expected to result in increase in enrollment in the higher education segment. Given its significant presence in higher education, private sector educational institutions are likely to benefit.

Budgetary allocation to RMSA at Rs.4,966 crore

School assessment programme being initiated at a cost of Rs.30 crore In the last decade, the government has spent significant amount

in increasing school education infrastructure. In a move towards assessment and improvement of quality in education, these programmes have been proposed in the current budget. This is likely to improve the quality of education in the long term.

To infuse new training tools and motivate teachers, ‘Pandit Madan Mohan Malviya New Teachers Training Programme’ being launched. Initial sum of Rs.500 crore is set aside for the same.

Impact on Companies

Company Impact CommentsEducomp Solutions + The increased budgetary allocation to the education sector opens new sources of

revenues along-with increasing demand of up-gradation of existing infrastructure. The increase in budgetary allocation to the education sector is expected to result in higher inflow of orders to the private sector players especially for companies engaged in information and communication technology segment of education.

Everonn Education +Aptech +NIIT +

27

Engineering & Capital GoodsIndustry Snapshot:

Performance of the domestic engineering & capital goods sector reflects the current state of the investment cycle in the economy and is generally considered a leading indicator for the industrial production cycle.

The demand in the sector is driven largely by private and public sector capex, mainly in the base industries like oil & gas, power, chemicals, construction & infrastructure, metals, etc. During the last two-three years, various factors like sub-5% growth in GDP, issues in land acquisition, delays in statutory and other clearances, elongated cash conversion cycle and weak growth in demand for end products has led to curtailment/deferment of capex by most of the players, dampening of the order inflows and deterioration in the financial profile of the players in the sector.

Nevertheless, with the long-term fundamentals of the economy remaining in-tact despite large external shocks and with a strong domestic-demand led economy, major players in the sector are expected to do well in the medium-term, despite the recent turbulences in the economy.

CARE expects the capex cycle to show improvement in the medium-term, with growing business confidence, expectations from a stable and decisive government and likely improvement in investment policy environment.

Duty Structure

Customs Duty (%) Before After Impact Excise Duty (%) Before After Impact

Stainless Steel (Flat Products)

5 7.5 - Stainless Steel 12 12 =Electrical Steel 5 5 = Aluminium 12 12 =Copper 5 5 =Aluminium 5 5 =

Proposal and Impact

Budget proposals Impact on the Industry

Increase in ceiling of FDI from 26% to 49% under the approval route in defence manufacturing

This will provide some incentive for foreign manufacturers to set up factories in India, given that India is one of the largest importers of defence equipments. Management control that should rest with the Indian partner could be crucial for some investors, especially in the technologically intensive industry

PSU capex of Rs.247,000 crore in FY15This is in line with the capex incurred in FY14. However, any thrust over increasing the pace of execution of projects would be crucial to percolate its effect down the value chain.

Setting up Infrastructure Investment Trusts (InvITs) with tax efficient pass through status, modeled on the Real Estate Investment Trust (REITs) structure

This could provide much needed risk capital to the infrastructure sector, which in turn could boost competitiveness of domestic manufacturers and could also contribute to the local demand growth

Feeder separation under ‘Deen Dayal Upadhyay Gram Jyoti Yojana’

Would give boost to distribution infrastructure products. However, a large number of the distribution infrastructure projects depend upon the initiatives of the respective state entities

28

New investments proposed in all types of infrastructure projects including roads, seaports, airports, gas pipelines, inland waterways, power transmission lines, etc.

This will, in turn, trigger a higher demand for construction equipments used for these projects

Additional 15,000 KMs of gas pipeline to be constructed under PPP model

Once rolled out, it would boost the demand of gas compressors and other associated capital goods.

Investment allowance on investments of Rs.25 crore and above (earlier on Rs.100 crore and above)

This would provide additional incentive to SMEs to undertake capex, but the impact is likely to be contingent upon revival for demand of end products

Extension of 10 year tax holiday to entities which commence power generation, transmission and distribution of power till March 31, 2017

This could act as a catalyst for speeding up of projects under implementation and pre-pone the demand for related capital goods

Customs Duty and Excise Duty benefits for domestic manufacture of solar power panels, wind turbine parts as well as Bio-CNG plants

This would incentivize procurement of the domestically produced plants

Impact on Companies

Company Impact Comments

ABB India Ltd. = Stable

Action Construction Equipment Ltd. + Large investment in roads network envisaged in FY15 through NHAI would improve the demand for construction equipments

Alstom India Ltd. + Extension of tax benefit to power plants to be commissioned till 31-March-2017 is likely to speed up implementation of power plants

Bharat Heavy Electricals Ltd. + Extension of tax benefits for power plants

C.R.I. Pumps Pvt. Ltd. + Likely to receive boost in demand due to its large and established presence in agricultural pumps

Emico Elecon (India) Ltd. = Stable

Elecon Engineering Company Ltd. = Stable

Engineers India Ltd. = Stable

Kalpataru Power Transmission Ltd. +Extension of tax benefit to power transmission and distribution projects to be commissioned till 31-March-2017 is likely to boost demand from customers

KEC International Ltd. +Larsen & Toubro Ltd. = Stable

Shanti Gears Ltd. = Stable

Siemens Ltd. = Stable

Sterlite Technologies Ltd. +Extension of tax benefit to power transmission and distribution projects to and thrust on broadband connectivity be commissioned till 31-March-2017 is likely to boost demand from customers

Texmaco Rail & Engineering Ltd. = Stable

Thermax Ltd. + Extension of tax benefits to power plants

TRF Ltd. = Stable

Voltamp Transformers Ltd. + Extension of tax benefit to power transmission and distribution projects

29

FertilizersIndustry Snapshot:

Domestic fertilizer consumption reduced by 4% year on year (y-o-y) in FY14 to 51 million metric tonnes (MMT) with urea consumption remaining stable at 30 MMT while the demand for non urea (decontrolled) fertilizers reduced by 10% y-o-y in FY14. The fertilizer subsidy budget of Rs.67,971 crore for FY14 fell short by around Rs.35,000 crore of subsidy payments which carried over to FY15.

The fertilizer industry is facing the challenges and uncertainties such as delays in subsidy payments, unavailability of domestic gas for urea units which were required to change their feedstock base to gas under new pricing scheme–III (NPS-III), high cost of regasified liquefied natural gas (R-LNG), likely upward revision in domestic gas price and removal of guaranteed buyback provision in new urea investment policy (NIP) for fresh urea capacity addition. Further, the production of urea above the cut-off quantity would become unviable due to subsidy linkage to international parity price (IPP) with rise in domestic gas and R-LNG price. Some of the concerns are expected to be addressed in forthcoming budget.

The demand for fertilizers under the present scenario is likely to increase marginally in FY15 with stable urea consumption and likely increase in demand of non urea fertilizers due to reduced IPP of raw material and finished fertilizers, which might be affected by delayed monsoon. The sales data of fertilizers in Q1FY15 exhibit a growth rate of 7% y-o-y mainly due to low inventory level carried over from previous year due to liquidity pressure created by delayed subsidy payment.

CARE expects the fertilizer subsidy budget for FY15 to remain around the level declared during interim budget for FY15 (Rs.68,000 crore) mainly due to Government of India’s (GoI) target to contain the fiscal deficit and reluctance to increase the price of urea and other fertilizers. However, the estimated requirements are likely to be around Rs.1,10,000 crore which includes rollover of subsidy from FY14, likely increase in subsidy due to higher gas cost and increase in fixed cost for urea.

GoI is expected to boost the domestic urea production by revival of sick units of Fertilizer Corporation of India Ltd and Hindustan Fertilizers Corporation Ltd, however, it would be capitalized over the period of 3-4 years and would require substantial capital outlay. GoI is also expected to encourage setting up of joint venture (JV) fertilizer plants abroad in countries with availability of gas at reasonable price to reduce the subsidy burden.

Duty Structure

Customs Duty (%) Before After Impact Excise Duty (%) Before After Impact

Urea 5% 5% = Urea 12% 12% =DAP 5% 5% = DAP 12% 12% =MOP 5% 5% = MOP 12% 12% =Ammonia 5% 5% = Ammonia 12% 12% =Phosphoric Acid 5% 5% = Phosphoric Acid 12% 12% =Sulphur 2.5% 2.5% = Sulphur 12% 12% =Rock Phosphate 2.5% 2.5% = Rock Phosphate 12% 12% =

30

Proposal and Impact

Budget proposals Impact on the Industry

Formulation of new urea policy

New urea policy is likely to aim at boosting domestic production of urea which is short of domestic demand. The exact contours of the policy are not yet known, however, the way the new policy deals with issues like guaranteed buy back and allocation of cost effective gas would be crucial.

Increase in subsidy for urea

Urea comprises 59% of the total fertilizer consumption in India based on volume. The increase in subsidy for urea would certainly aid all the stakeholders of urea. However, the overall subsidy budget over the past few years have fallen short of the actual figures. This is expected to continue for FY15 also.

Enhanced credit to the farm sector through agriculture credit outlay of Rs.8 lakh crore, extension of interest subvention scheme, creation of long term rural credit fund of Rs.5,000 crore, increased allocation to short term cooperative rural credit by Rs.5,000 crore and credit to landless joint farming groups

Fertilizer demand would to get a fillip on account of easier credit availability and may also influence farmers to use complex fertilizers suiting their soil needs rather than opting for the low cost urea. This may lead to improved yield especially in the scenario of delayed monsoon.

Improve access to irrigation through ‘Pradhan Mantri Krishi Sinchayee Yojana’ with an outlay of Rs.1,000 crore

The move is expected to reduce dependence on monsoon and provide assured irrigation. Assured irrigation would also entail stable demand for fertilizers.

Impact on Companies

Company Impact CommentsIndian Farmers Fertiliser Cooperative Ltd = The increase in subsidy allocation to urea would certainly reduce the gap

between budgeted and actual subsidy witnessed during past few years.

The new urea policy is expected to address the shortfall in domestic production. The exact contours of the policy are not yet known, however, the way the new policy deals with issues like guaranteed buy back provision and allocation of cost effective gas would be crucial.

The easier farm credit would influence farmers for balanced use of fertilizers.

National Fertilizers Ltd =Rasthriya Chemicals & Fertilizers Ltd =Chambal Fertilizers & Chemicals Ltd =Gujarat Narmada Valley Fertilizers & Chemicals Ltd =Gujarat State Fertilizers & Chemicals Ltd =

31

FMCGIndustry Snapshot:

Fast Moving Consumer Goods (FMCG) are also commonly known as consumer packaged goods. These goods have a swift turnover with relatively low cost as compared to other products and are consumed on a regular basis to form as a daily part and parcel of our life. FMCG is mainly classified into various segments such as household care, personal care, packaged foods and beverages, spirits and tobacco etc. Various examples of FMCG under different segments (as classified above) include a wide range of repeatedly purchased consumer products such as detergents, oral/hair/skin care products, deodorants, perfumes, feminine hygiene, paper products, packaged food products, cigarettes etc.

The Indian FMCG industry is the fourth largest sector in the economy exhibiting double digit growth rate for the past few years. The Industry is characterised by presence of large domestic producers (for e.g. Nirma, Godrej Consumer, Amul, etc) and strong MNCs (Multinational Companies) like Hindustan Unilever Limited, Procter & Gamble, Nestle etc); well established distribution network, prevailing intense competition between the organised and unorganised sector players and low operational cost. The urban market forms a major chunk (i.e. 66%) of revenues of the Indian FMCG Industry. According to Confederation of Indian Industries (CII), the size of the Indian FMCG industry was more thanUS$ 33.4 billion in CY12.

Various factors such as growing trend in urbanisation, rise in income levels driving purchase, evolving consumer lifestyle, ease of shopping through various online stores, growth in modern trade, increase in FDI inflows over the past few years, awareness of brands, low operational costs, new product launches etc. have been key growth drivers for this sector. Further, large domestic market with growing youth population, lower penetration levels in rural areas and lower per capita daily consumptionindicates opportunities for further growth of thisindustry.