UNION BUDGET 2016 - wirc-icai.orgX(1)S(k5rzns55tzz1eqvqpk4jweic... · marico. stocks to watch it...

84

UNION BUDGET 2016 ORGANIZED BY BFSI AND CAPITAL MARKET STUDY GROUP OF WIRC OF ICAI PRESENTATION BY : CA MANISH CHOKSHI

Transcript of UNION BUDGET 2016 - wirc-icai.orgX(1)S(k5rzns55tzz1eqvqpk4jweic... · marico. stocks to watch it...

UNION BUDGET 2016

ORGANIZED BY BFSI AND CAPITAL MARKET

STUDY GROUP OF WIRC OF ICAI

PRESENTATION BY :CA MANISH CHOKSHI

Trends in GDP Growth Rate (%)

GDP CALCULATION CHANGED WEF FROM SEPT 2014

GDP Growth Rate Country Wise

0

2

4

6

8

10

12

IIPINDEX OF INDUSTRIAL PRODUCTION

FISCAL DEFICIT

0

2

4

6

8

10

12

FISCAL DEFICT %

CURRENT ACCOUNT DEFICIT AS % TO GDP

BRENT CRUDE OIL PRICE CHART

INFLATION AT WPI – WHOLESALE PRICE INDEX FROM 7.52 IN NOV 2013 TO -0.09 IN JAN16

INFLATION - CPI IS RISING INSPITE OF FALL IN OIL PRICES. THIS DATA SUGGESTS THAT FURTHER REDUCTION IN INTEREST RATE MAY NOT TAKE PLACE IN 2016

Inflation Rate of Top 5 Countries

12

India Interest Rates

Rate of Interest of Top 5 Countries

FDI IN INDIA

INDIAN EXPORTS ARE FALLING

INDIAN IMPORTS ARE FALLING CONTINIOUSLY ON ACCOUNT OF OIL SLUMP

GOLD IMPORTS SURGES MORE THAN DOUBLE IN DEC 15 COMPARED TO DEC 14 ( in billion USD )

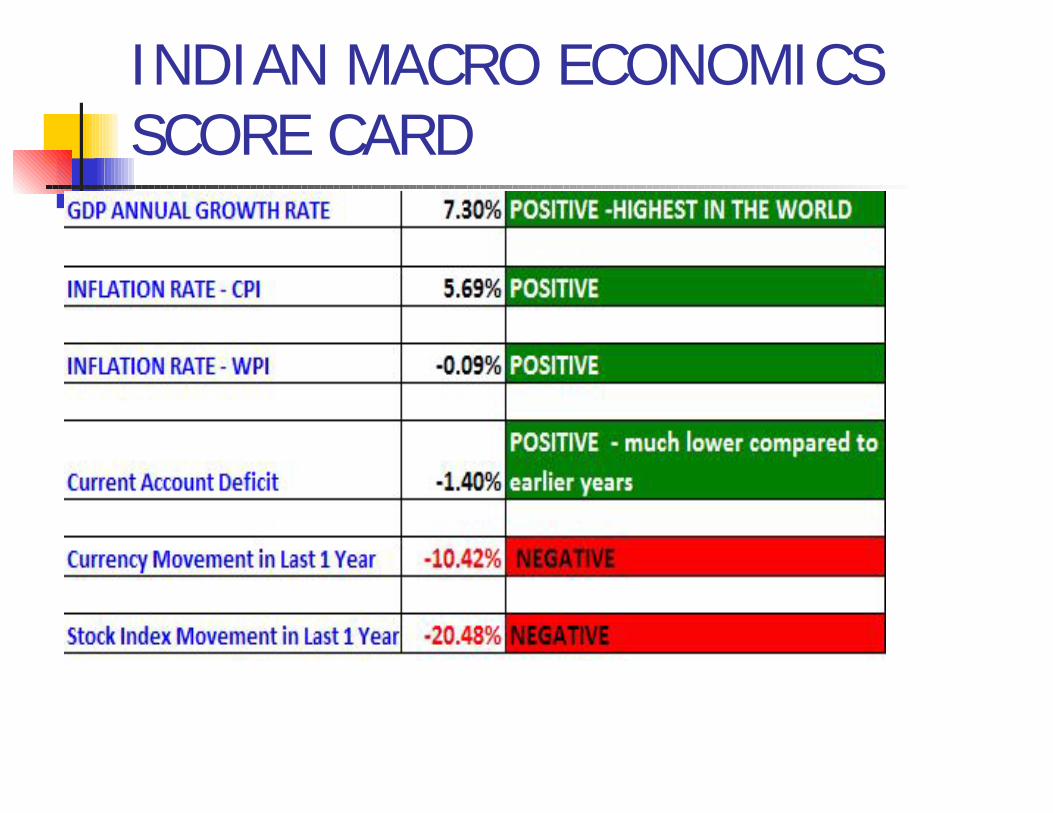

INDIAN MACRO ECONOMICS SCORE CARD

IS INDIA AN OASIS IN THE DESERT OF GLOBAL CRISIS

IS INDIA A SWEAT SPOTIN THE WHOLE WORLD

CURRENCY MOVEMENTS OF EMERGING & ASIAN ECONOMIES OF THE WORLD vis-à-vis USD

CHINA GDP GROWTH RATE IS FALLING YEAR AFTER YEAR

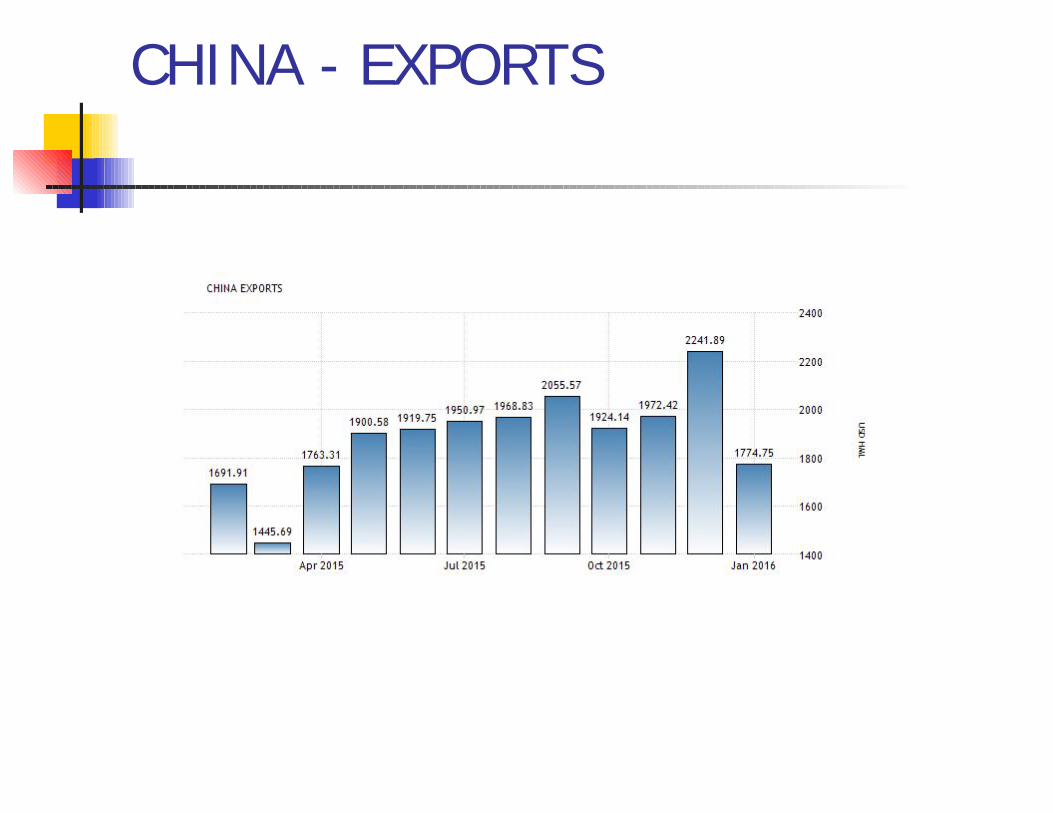

CHINA - EXPORTS

CHINA IMPORTS

CHINA EXPORTS TO INDIA

CHINA CAPITAL FLOWS

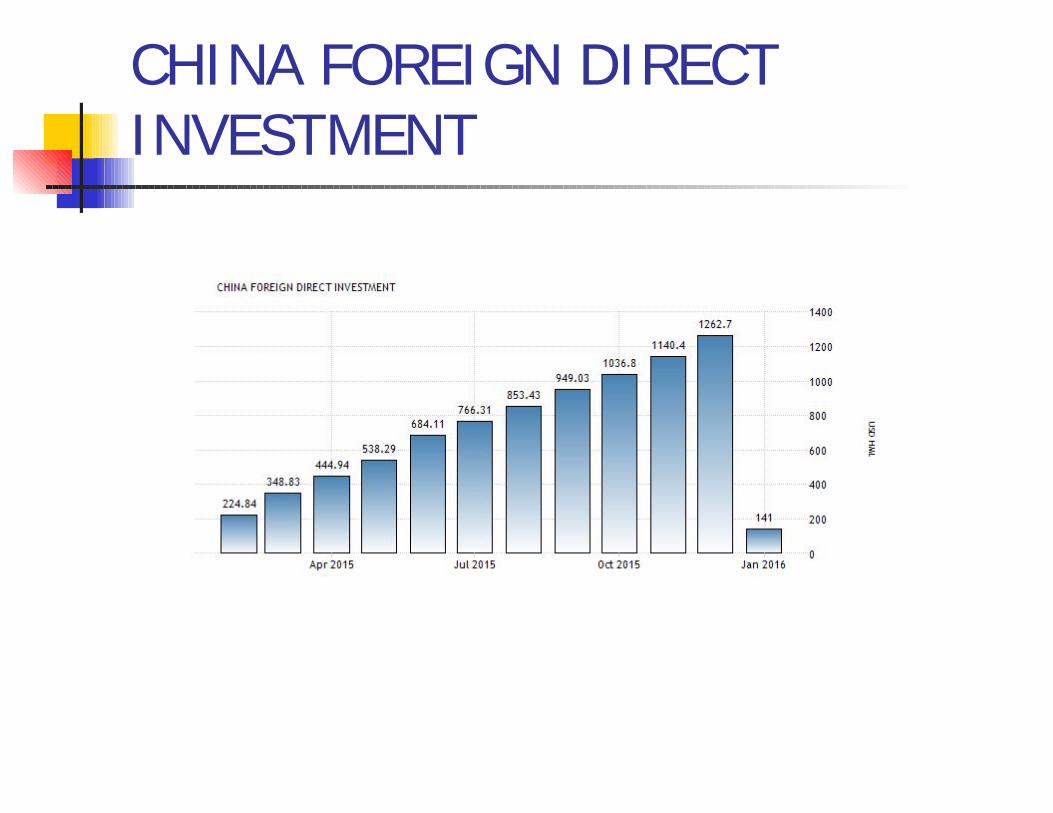

CHINA FOREIGN DIRECT INVESTMENT

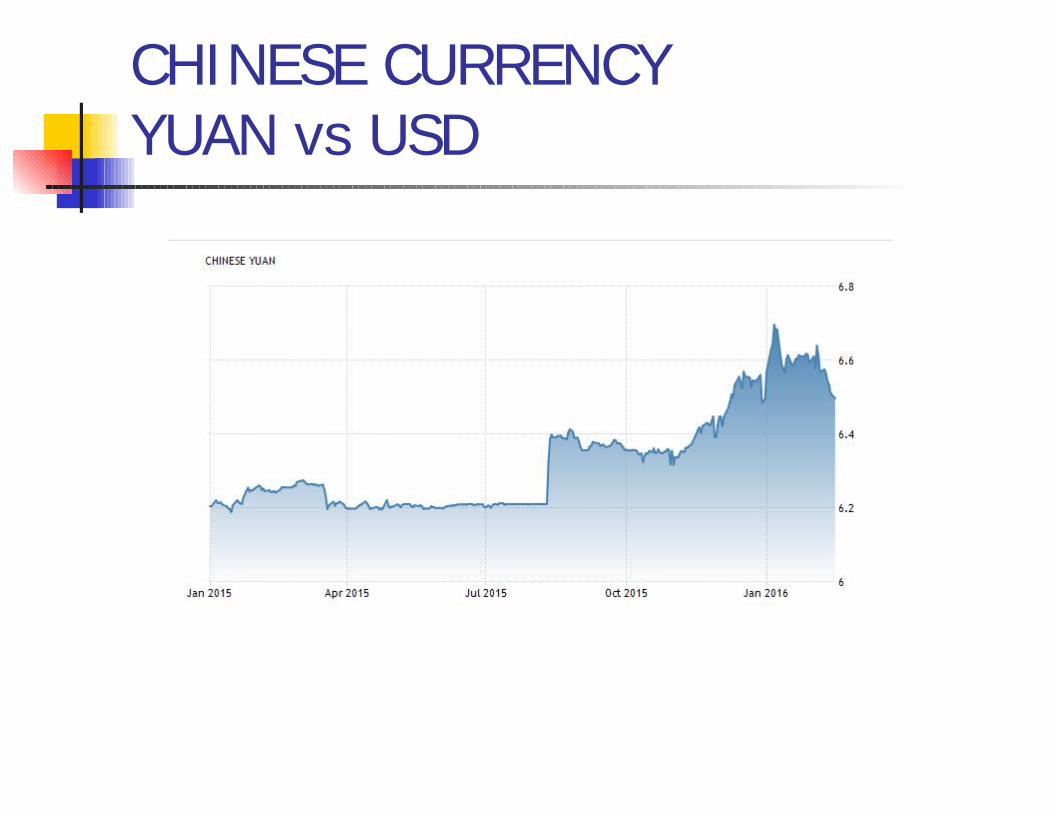

CHINESE CURRENCYYUAN vs USD

Shanghai Shenzhen CSI 300 Index- FALL FROM 5353 TO 3051 =2302 PTS FALL =43 % FALL FROM IN JUN 2015.

BUDGET 2016HIGHLIGHTS

STOCK MARKET

FII's MONTHLY EQUITY INVESTMENT IN 2015-16 IN RS. '000 CRORE

MONTHLY FII’s INVESTMENT IN DEBT MARKET IN LAST 1 YEAR

A cumulative view Q3FY16 results of 4169 Companies are not encouraging

BSE SENSEX PE RATIOON THIS BASIS THE MARKETS CANNOT BE SAID TO BE UNDERVALUED

PERFOMANCE OF BSE 30 AND BSE SECTORIAL INDICES

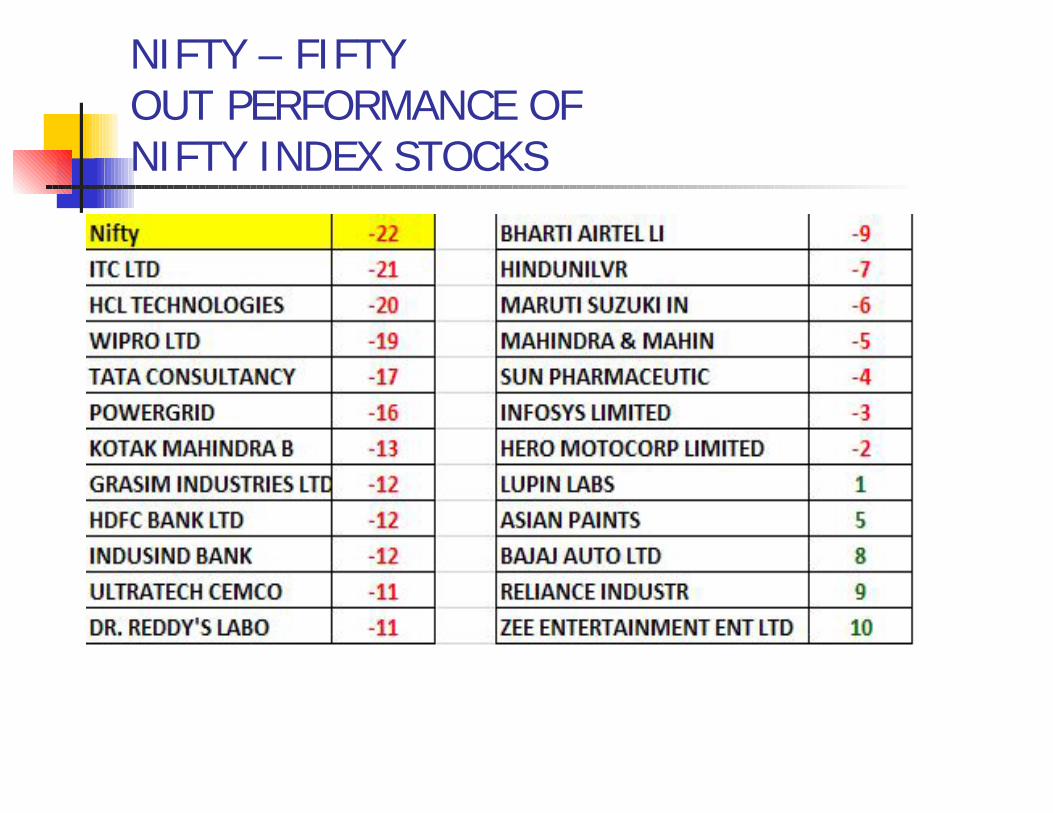

NIFTY – FIFTYOUT PERFORMANCE OFNIFTY INDEX STOCKS

NIFTY – FIFTYUNDER PERFORMANCE OFNIFTY INDEX STOCKS

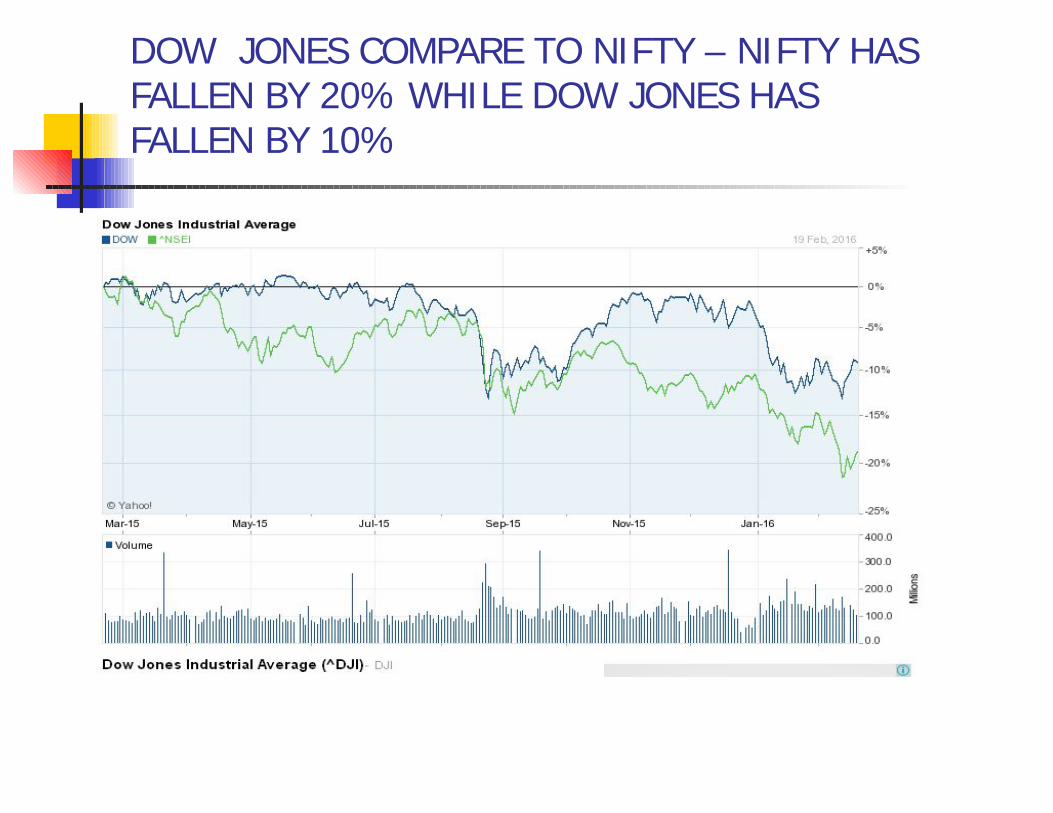

DOW JONES COMPARE TO NIFTY – NIFTY HAS FALLEN BY 20% WHILE DOW JONES HAS FALLEN BY 10%

JAPANESE NIKKEI & BSE 30 PERFORMANCE COMPARED

Shanghai Shenzhen CSI 300 Index- FALL FROM 5353 TO 3051 =2302 PTS FALL =43 % FALL FROM IN JUN 2015.

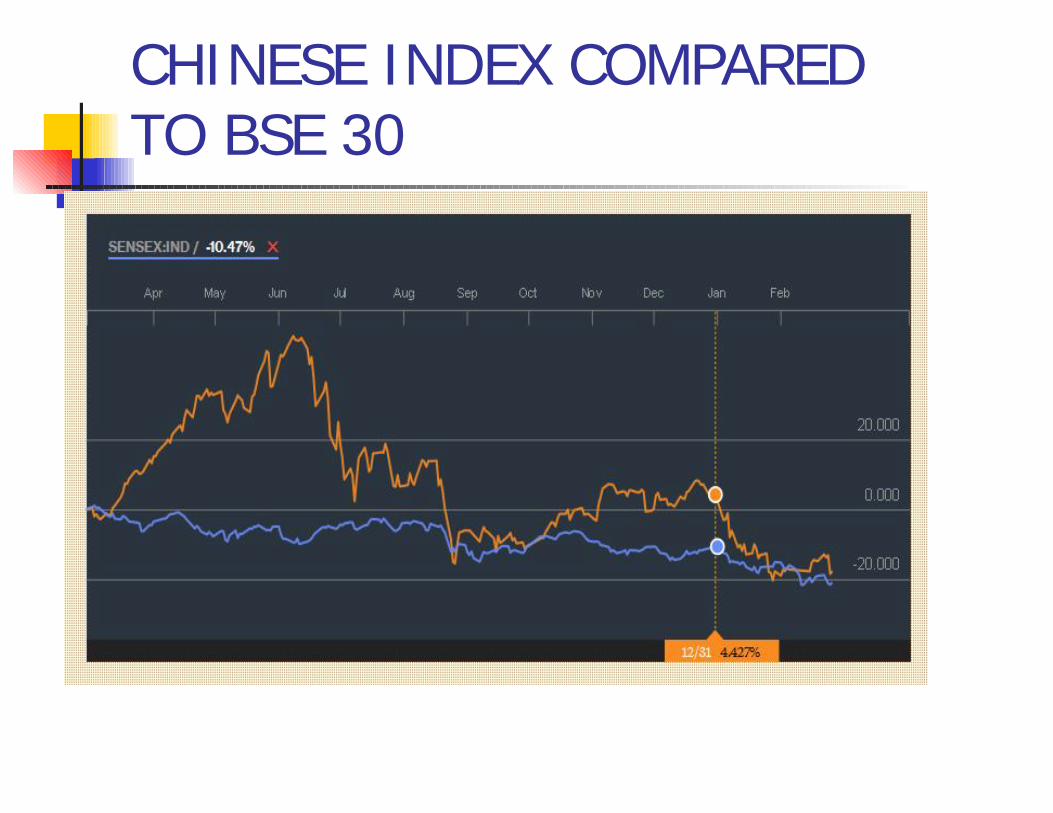

CHINESE INDEX COMPARED TO BSE 30

NIFTY INTRADAY

BSE SECTORIAL INDICES BUDGET DAY

F & O LOSERS

F & OGAINERS

NIFTY SECTORIAL INDICES

NSE CASH SCRIPS LOSERS

NSE CASH SCRIPS GAINERS

COMMODITIES & CURRENCIES

GOLD GOLD BEES

GOLD IS BULLISH

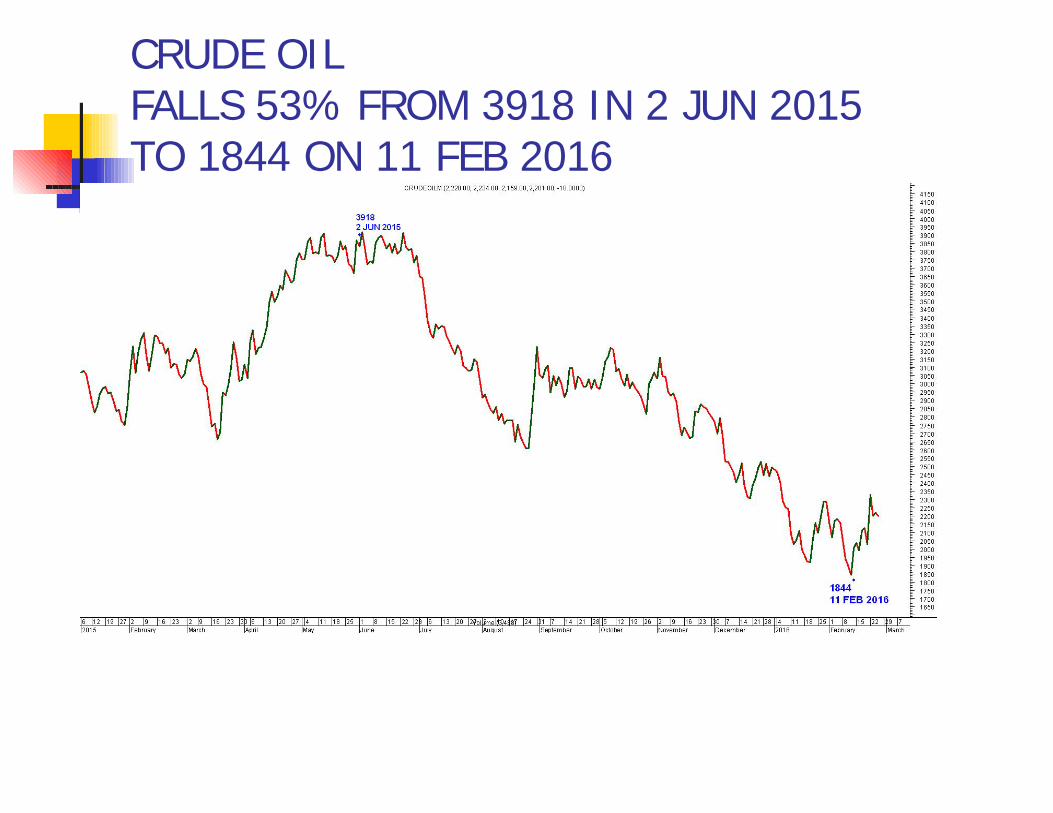

CRUDE OILFALLS 53% FROM 3918 IN 2 JUN 2015 TO 1844 ON 11 FEB 2016

EURO vs INR

GBP vs INR

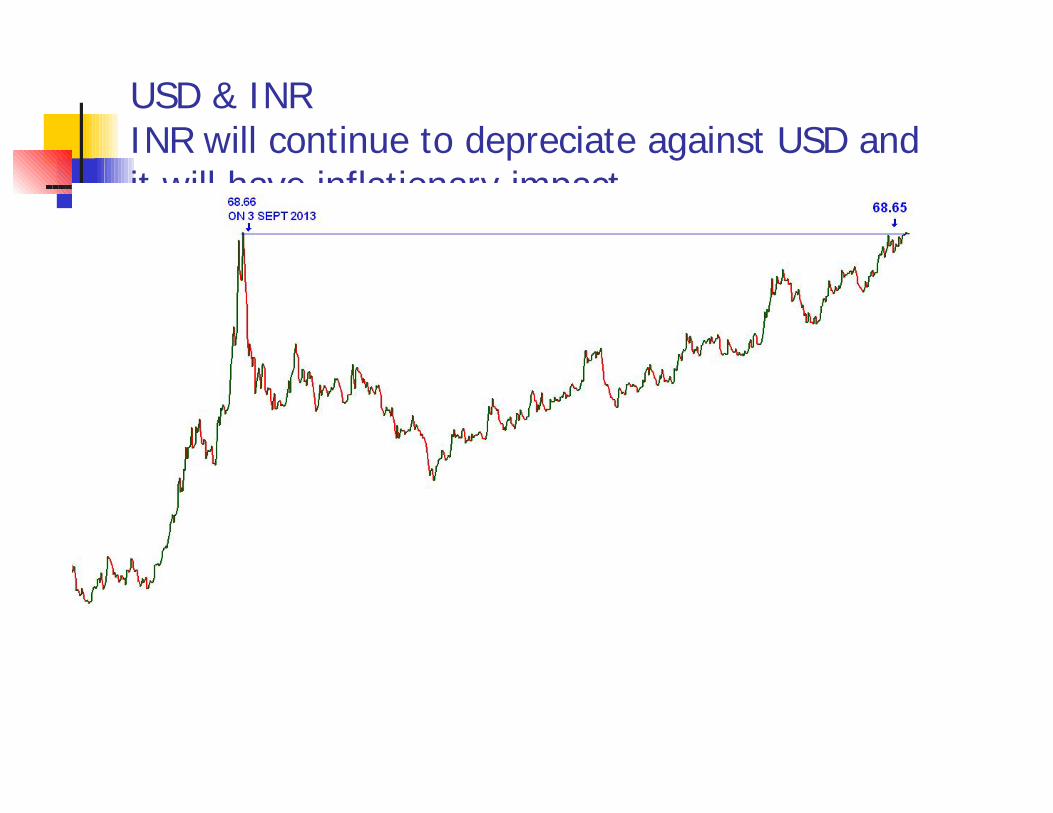

USD & INR INR will continue to depreciate against USD and it will have inflationary impact

INR will continue to depreciate against USD

Economic Survey on Currency Rupee's value must be fair, avoiding

strengthening; fair value can be achieved through monetary relaxation

India needs to prepare itself for a major currency readjustment in Asia in wake of a similar adjustment in China

Gradual depreciation in rupee can be allowed if capital inflows are weak

NIFTY INTRA DAY CHART ON BUDGET

NIFTY HAS FALLEN BY 22%

BANKING SECTORDO NOT BUY NOW

PSU Banks hit by huge losses RBI has mandated to clean up and to

provide fully for NPA’s Banks say- the provisioning will keep on

happening till next 3 quarters No clarity on the quantum of losses yet Due to uncertainty banks will continue

to underperform

SBI

TATA STEEL

RELIANCE

STOCKS TO WATCH

ASIAN PAINTS

STOCKS TO WATCHDEFENSIVE STOCKS

HIND UNILEVER MARICO

STOCKS TO WATCHIT SECTOR

INFOSYS TATA ELXI

STOCKS TO WATCHBANKING & FINANCE SECTOR

KOTAK MAHINDRA BAJAJ FINANCE CHOLAMANDALAM INV

STOCKS TO WATCHPHARMA & HEALTH SECTOR

LUPIN SUN PHARMA APOLLO HOSPITAL AJANTA PHARMA DR REDDY

STOCKS TO WATCHCEMENT

ULTRA TECH RAMCO CEMENTS

STOCKS TO WATCHAUTO

EICHER MOTORS TVS MOTOR ASHOK LEYLAND M & M

PIDILITE RAJESH EXPORTS SUPREME INDUSTRIES PIRAMAL ENTERPRISES TORRENT POWER VAKRANGEE FINOLEX INDUSTRIES

NDTV TV TODAY ZEE ENTERTAINMENT

IRB

TO SUMMARIZE

Economic Growth will remain stable around 7.5% but will not show impressive rise

Inflation will remain stable with a positive bias The Global Risk will continue to dampen exports INR will continue to depreciate against USD RBI may not cut rate more than 0.25 till

December 2016 Corporate results are not expected to show

impressive growth in the next 2 quarters

TO SUMMARIZE

The positive effect of GDP growth of 7.5% is not felt.

TO SUMMARIZE

Market will continue to fall Still this level is not the bottom and we

may see more pain Market May touch 6300 The SIP investor should continue to

invest. Economic Problems in China will put

pressure on Indian markets

TO SUMMARIZE

The Global risk still looms large Investors with fresh funds may invest

say 20 % of their total investible funds now in Nifty basket or fundamentally strong scrips and keep on adding at every 200-300 Nifty point fall.

In a day or two the Budget will be forgotten.

India will continue to remain an amazing Growth Story

82

DISCLAIMER

The stocks discussed here are for academic discussion and studies only. I do not advise to invest in any of the stocks as discussed above. Please check with your certified financial advisor before taking any decision.

84

THANKYOU VERY MUCH