Understanding the Business Value of Sustainability Initiatives

44

Business Value of Sustainability Initiatives May 23 rd , 2016 | Houston Francisco Cordero | Consultant | Antea Group

-

Upload

antea-group -

Category

Environment

-

view

316 -

download

1

Transcript of Understanding the Business Value of Sustainability Initiatives

Business Value of Sustainability InitiativesMay 23rd, 2016 | HoustonFrancisco Cordero | Consultant | Antea Group

Sustainability

Lets start with ‘Sustainability’…

RealityWhen the economics work, the social and environmental benefits will last

Shared Value

RomanticizedPeople, Planet, Profit…Triple Bottom Line…

ClassicMeets the needs of the present without compromising the needs of future generations

Brundtland Report 1987

What Makes Sustainability Strategic?The many ways in which sustainability impacts…

Leadership AgendaIncreasingly more companies have sustain‐ability as a top manage‐ment agenda item

Future ChallengesSustainability mega‐forces will impact every business over the next 20 years

CompetitivenessSustainability is a strategic and integral part of business

Source: McKinsey Global Survey Results, Sustainability’s Strategic Worth, 2014

Impacts On Competitiveness – How?

Advance Enabling Growth

Gain Market Share

Acquire New Revenue

Strengthen Saving Cash

Added Financial Flexibility

Greater Capital Productivity

Increased Employee Retention & Productivity

Protect Improved Risk & Reputation ManagementCost Avoidance

Can The Sustainability Strategy Help Navigate The Storm?

• Force for internal collaboration – ‘Integral’ approach?

• Find new ways to leverage the organization’s talent & current activities?

• Help create a more ‘long‐term’ mindset and establish a pace for enduring success?

• Can sustainability help to scale the company’s best ideas & practices?

• Can we get a few ‘quick wins’ and communicate the good news to the organization?

Oil price shockDeclining productionTaxesDisappointing resultsAusterity drive Personnel cutsRenegotiation w/suppliers & contractorsExtensive pension liabilityGlobal competition

Effective Sustainability Strategy Takes Into Account…

Shared Value

Leadership AgendaFuture ChallengesCompetitiveness

• Accelerate progress by removing obstacles to better, more sustainable business decision‐making

• Focus on making key elements of sustainability more tangible, helping to build a better case for investment

“37%of CEOs said a lack of clear link to business value was a critical factor deterring faster action on sustainability”

The UN Global Compact‐Accenture CEO Study on Sustainability 2013, September 2013

“It is not unreasonable for business leaders to want a positive return on their sustainability expenditures…for me, the convenient

analogy is advertising…”Sustainability a CFO Can Love, Harvard Business Review, April 2014

The Need to Determine Business Value

Shared Value

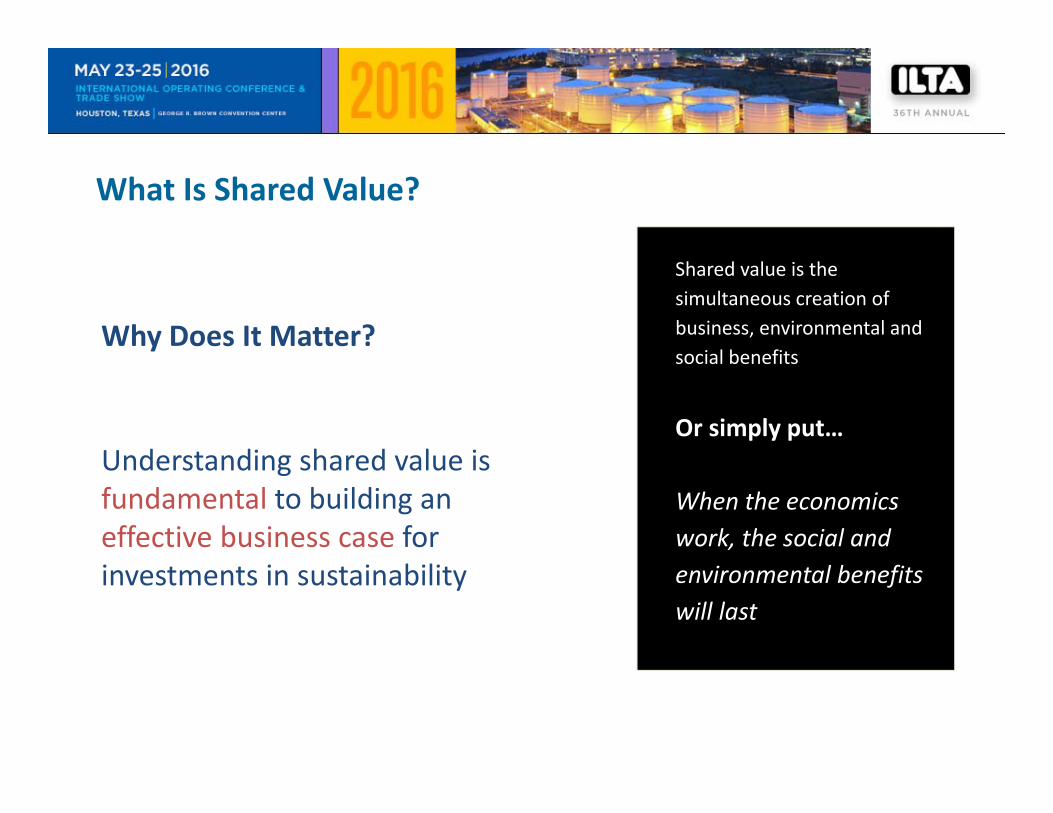

What Is Shared Value?

Why Does It Matter?

Understanding shared value is fundamental to building an effective business case for investments in sustainability

Shared value is the simultaneous creation of business, environmental and social benefits

Or simply put…

When the economics work, the social and environmental benefits will last

More On The Concept of Shared Value

Source: Insights: Ideas for Change ‐Michael Porter ‐ Creating Shared Value, https://www.youtube.com/watch?v=aUdPDVO‐toM

Measuring Shared Value

Environmental Impact

Social Impact

Business Impact

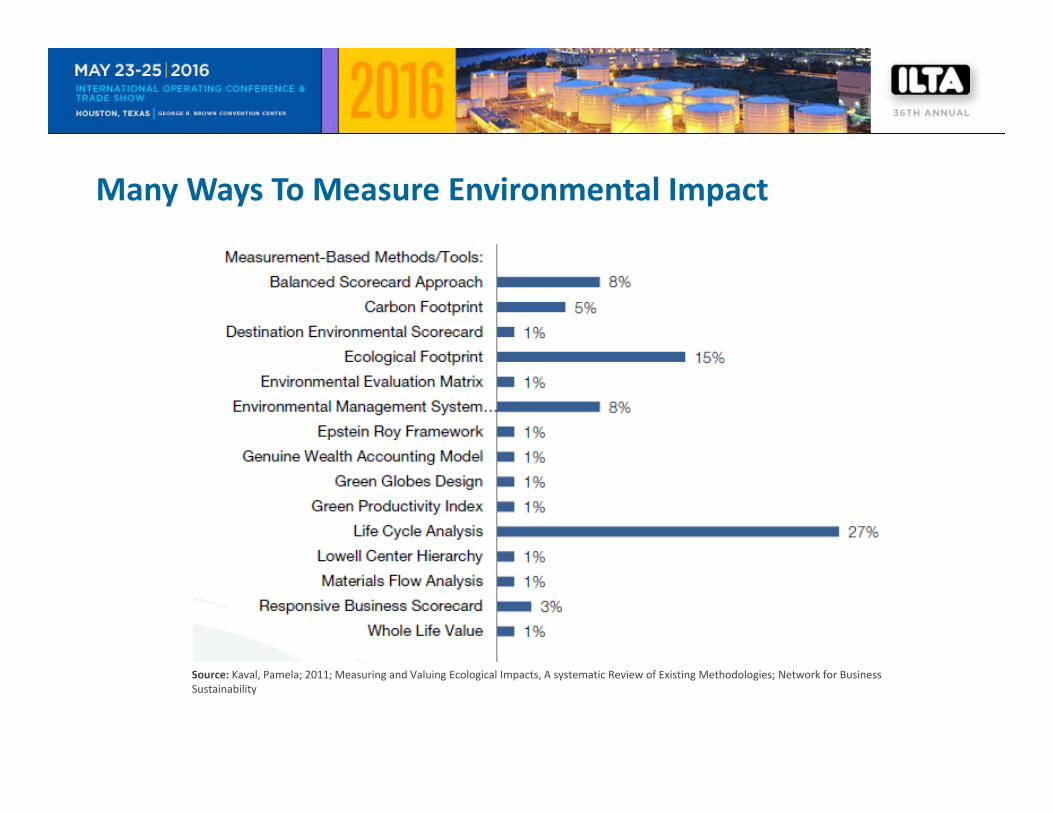

Many Ways To Measure Environmental Impact

Source: Kaval, Pamela; 2011; Measuring and Valuing Ecological Impacts, A systematic Review of Existing Methodologies; Network for BusinessSustainability

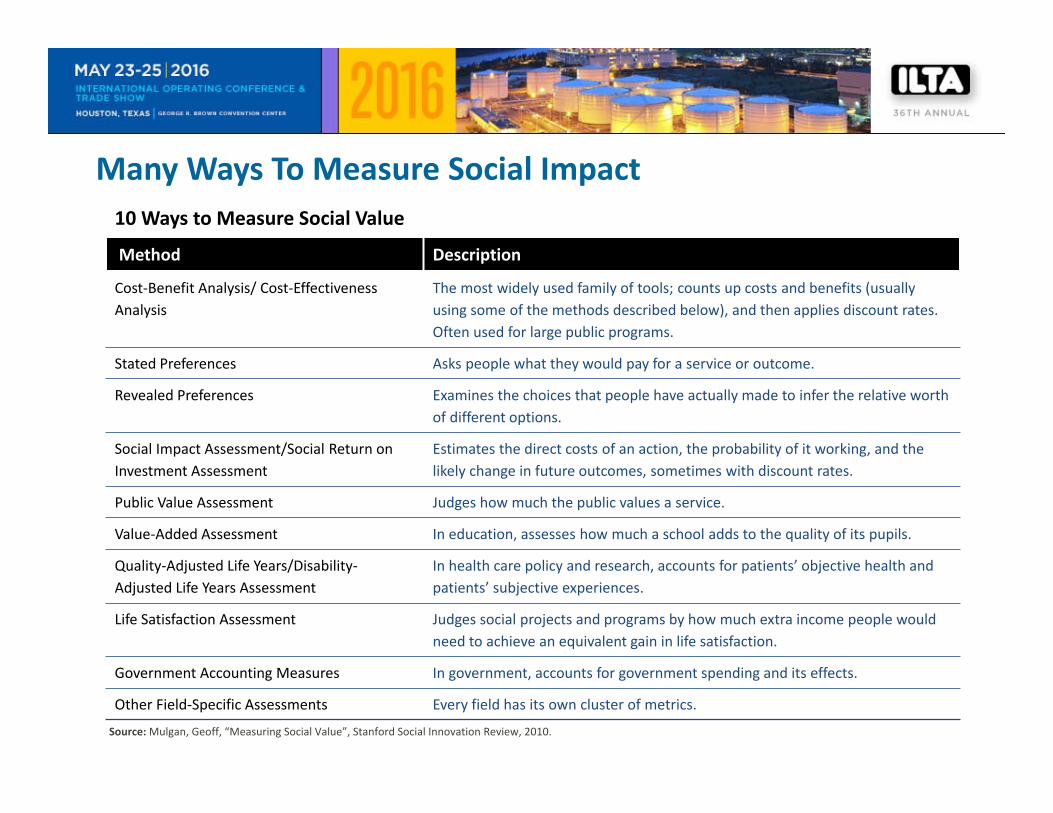

Many Ways To Measure Social Impact10 Ways to Measure Social Value

Method Description

Cost‐Benefit Analysis/ Cost‐Effectiveness Analysis

The most widely used family of tools; counts up costs and benefits (usually using some of the methods described below), and then applies discount rates. Often used for large public programs.

Stated Preferences Asks people what they would pay for a service or outcome.

Revealed Preferences Examines the choices that people have actually made to infer the relative worth of different options.

Social Impact Assessment/Social Return on Investment Assessment

Estimates the direct costs of an action, the probability of it working, and the likely change in future outcomes, sometimes with discount rates.

Public Value Assessment Judges how much the public values a service.

Value‐Added Assessment In education, assesses how much a school adds to the quality of its pupils.

Quality‐Adjusted Life Years/Disability‐Adjusted Life Years Assessment

In health care policy and research, accounts for patients’ objective health and patients’ subjective experiences.

Life Satisfaction Assessment Judges social projects and programs by how much extra income people would need to achieve an equivalent gain in life satisfaction.

Government Accounting Measures In government, accounts for government spending and its effects.

Other Field‐Specific Assessments Every field has its own cluster of metrics.

Source:Mulgan, Geoff, “Measuring Social Value”, Stanford Social Innovation Review, 2010.

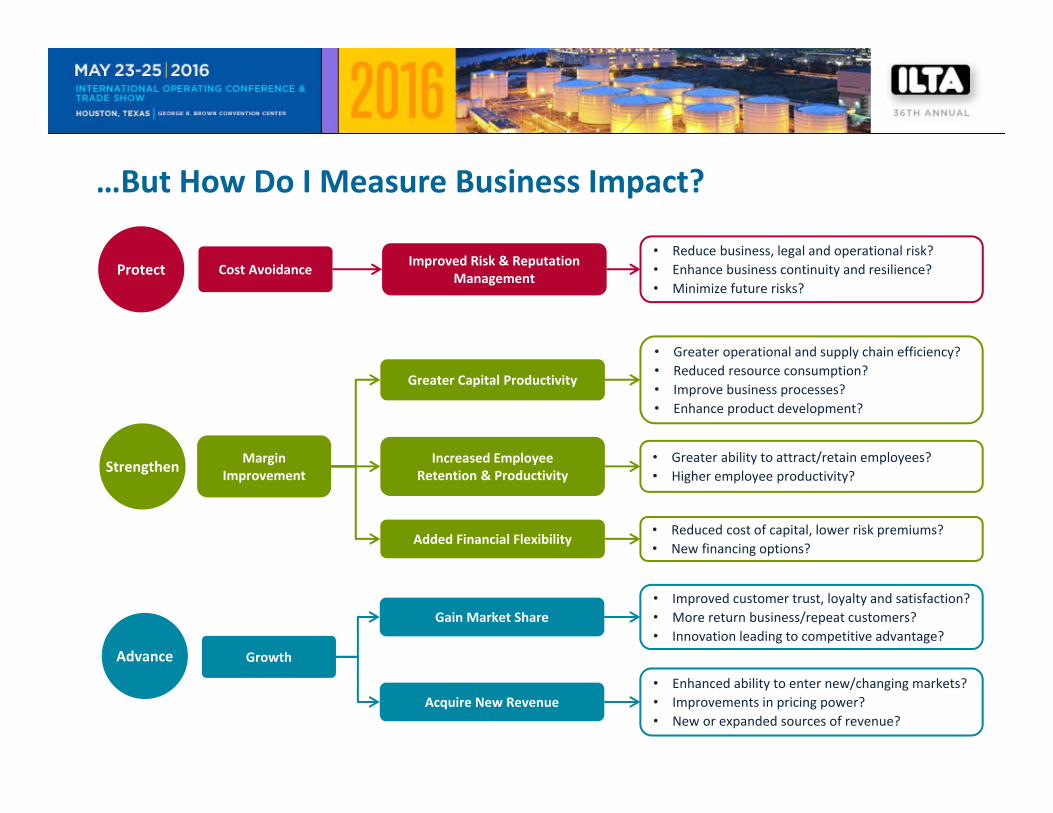

…But How Do I Measure Business Impact?

Advance Growth

Gain Market Share

Acquire New Revenue

• Improved customer trust, loyalty and satisfaction?• More return business/repeat customers? • Innovation leading to competitive advantage?

• Enhanced ability to enter new/changing markets?• Improvements in pricing power?• New or expanded sources of revenue?

Strengthen Margin Improvement

Added Financial Flexibility

Greater Capital Productivity

Increased Employee Retention & Productivity

• Greater operational and supply chain efficiency?• Reduced resource consumption? • Improve business processes?• Enhance product development?

• Greater ability to attract/retain employees? • Higher employee productivity?

• Reduced cost of capital, lower risk premiums?• New financing options?

Protect Improved Risk & Reputation Management

• Reduce business, legal and operational risk? • Enhance business continuity and resilience? • Minimize future risks?

Cost Avoidance

Discovering Shared Value Opportunities

Find opportunities to create shared value by inspecting situations through the lens of an investor

S T R ENG TH EN

Are we using resources, like water in the most efficient manner possible?

INVEST $2.4 million over 3 years

• Reducing consumption of water by 20 million gallons annually, AND

• Avoid more than $9.75 million in water‐related costs over the same time period by eliminating money otherwise spent to maintain, treat, move, heat, cool and discharge this resource

Building the Business Case

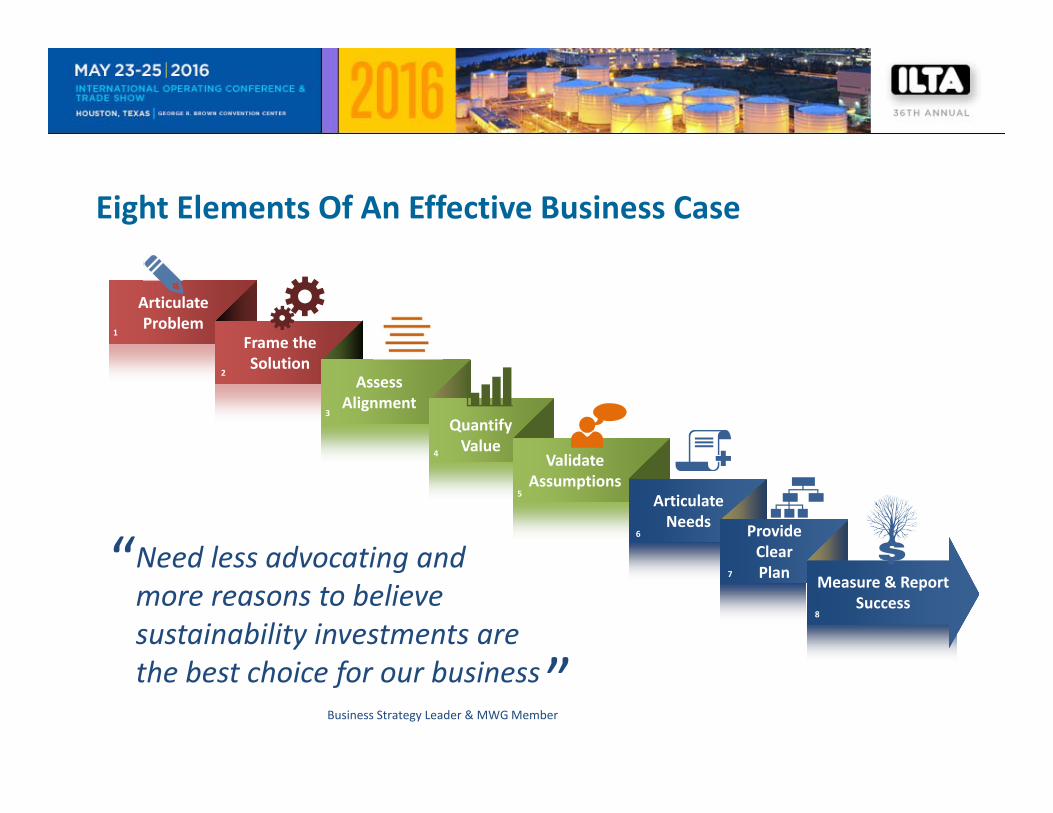

Eight Elements Of An Effective Business Case

Need less advocating and more reasons to believe sustainability investments are the best choice for our business

Business Strategy Leader & MWG Member

“

”

Articulate Problem

Frame the Solution

Assess Alignment

1

3Quantify Value

2

4

6

ValidateAssumptions

Articulate Needs Provide

Clear Plan Measure & Report

Success

5

7

8

6

2

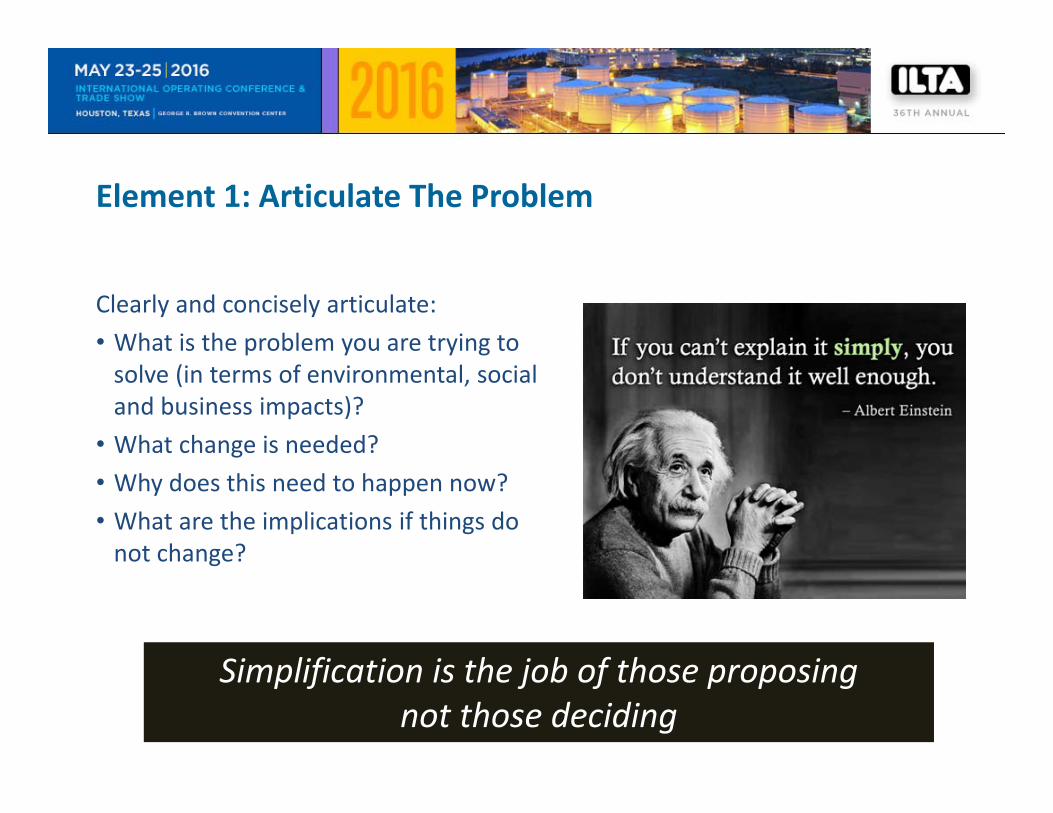

Element 1: Articulate The Problem

Clearly and concisely articulate:• What is the problem you are trying to solve (in terms of environmental, social and business impacts)?

• What change is needed?• Why does this need to happen now?• What are the implications if things do not change?

Simplification is the job of those proposing not those deciding

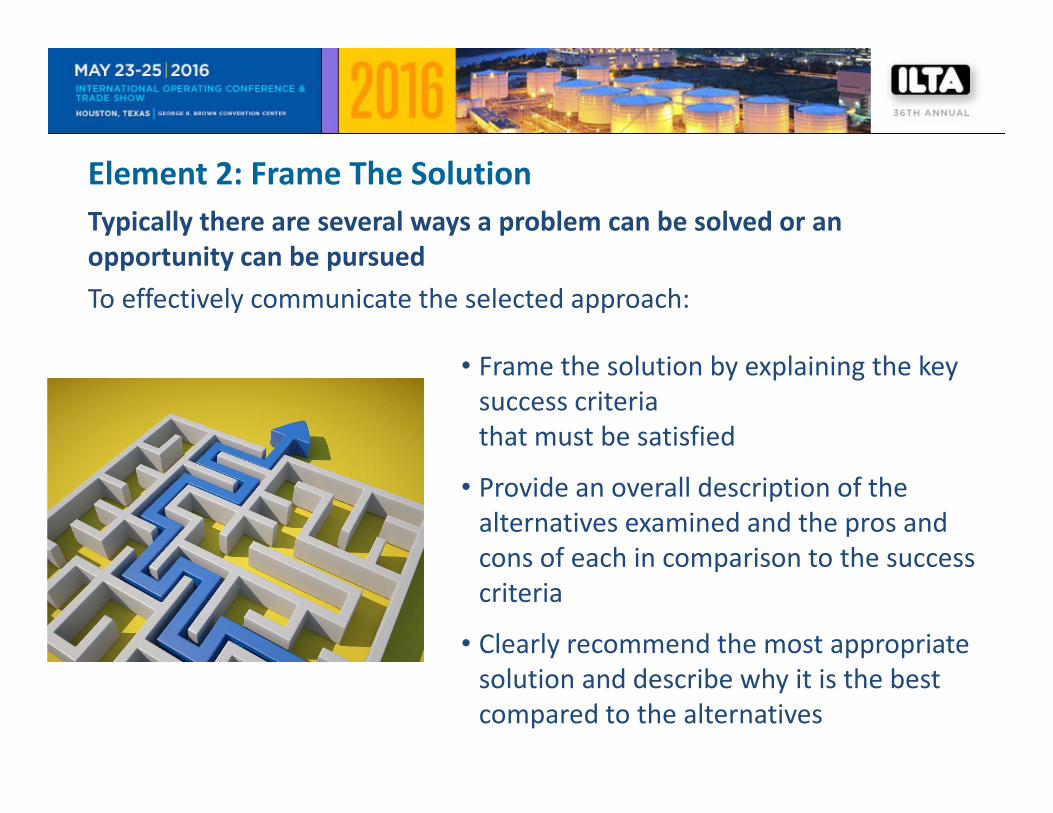

Element 2: Frame The SolutionTypically there are several ways a problem can be solved or an opportunity can be pursuedTo effectively communicate the selected approach:

• Frame the solution by explaining the key success criteria that must be satisfied

• Provide an overall description of the alternatives examined and the pros and cons of each in comparison to the success criteria

• Clearly recommend the most appropriate solution and describe why it is the best compared to the alternatives

Element 3: Value of Alignment

Understand Key Stakeholders Interests & Intent

For investors and those who’s support is otherwise needed…

• Synergistic strategies?

• Similar projects or initiatives?

• Common goals, objectives, vision or mission?

Align – With the interests of stakeholders who will decide upon and support the proposed investment

Elements 4 & 5: Quantify Value & Assumptions

PRESUMING: investment will allow

• Significant improvements in ingredient traceability to identify/mitigate presently unknown risks; and

• Effective implementation of historically successful programs (e.g., sourcing guidelines, grower training, etc. ‐ reducing negative env. and social impacts)

INVEST €3.4 million over 5 years

• Improving social and environmental conditions for growers & their lands; AND

• Significantly reducing the probability of realizing risks that may cost the company €9.9 million or more over the same period

4. Create Value ‐ Including positive return & shared value for investors, environmental and society

5. Plausible – With reasonable assumptions most can agree upon

Elements 6 & 7: Articulate Needs & Your Plan

6. Have You Made Your Needs Clear?

• Monetary Resources ‐ How much overall? Justification for amount?

• Cash Flow ‐ Initial funding and additional cash flow requirements?

• Human Resources ‐ Staff, cross‐functional support, volunteers, etc., that need to be involved? How much time?

• Major Decisions – What major decisions will be needed along the way?

7. Have You Made Your Plans Clear?

• Planned Efforts – Summarizing what steps/stages will be required for solution implementation?

• Schedule – Outlining when work will be started/finished as well as associated spending, staffing and milestones/major decision points?

• Initiative Team – Listing key roles, responsibilities and individuals that will lead and manage implementation?

Element 8: Measure & Report Success

KPIs

Solution implementation progress v. spend

Trends indicating satisfaction of key criteria originally established for the solution/investment

Management of Change

Any changes to scope, schedule, budget, etc.

Risks ‐ have any been realized or are there new concerns?

Routine Communications

Keep investors and key stakeholders informed on progress and fore‐casted outcomes

Describe how success will be measured & reported

Measuring

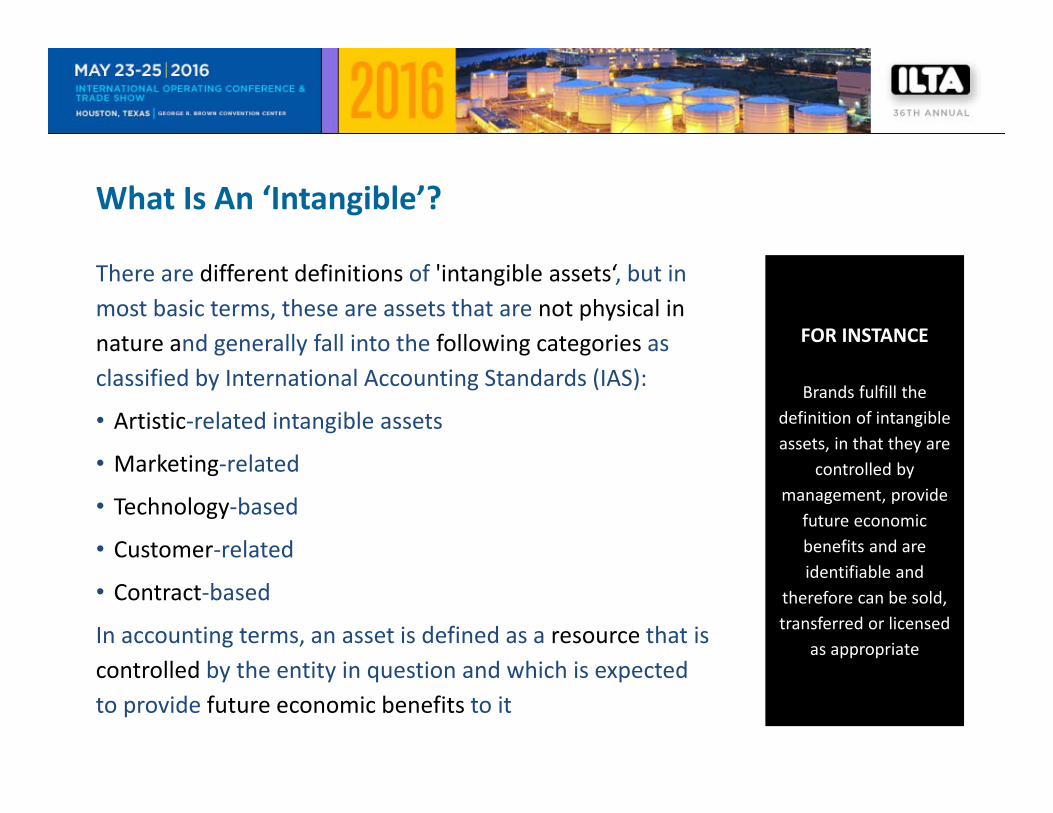

What Is An ‘Intangible’?

There are different definitions of 'intangible assets‘, but in most basic terms, these are assets that are not physical in nature and generally fall into the following categories as classified by International Accounting Standards (IAS):

• Artistic‐related intangible assets• Marketing‐related

• Technology‐based• Customer‐related

• Contract‐basedIn accounting terms, an asset is defined as a resource that is controlled by the entity in question and which is expected to provide future economic benefits to it

FOR INSTANCE

Brands fulfill the definition of intangible assets, in that they are

controlled by management, provide

future economic benefits and are identifiable and

therefore can be sold, transferred or licensed

as appropriate

Intangibles In Sustainability Parlance

“[intangibles are]…the indirect and unpriced value creators (or destroyers)… [and] include the ability to attract and retain talent; support from the community and the license to operate from society; reduced risk and enhanced resilience; customer loyalty; and all brand equity…a firm’s environmental and social performance can enhance or diminish all these assets.”

Source: Resilience in a Hotter World, A. Winston, April 2014 Harvard Business Review

Anything can be measured no matter how fuzzy the measurement is, it’s still a measurement if it tells you more than you knew before

Douglas W. Hubbard

• Are you more informed on some of these topics than others?

• Is your current state of uncertainty in itself something you can quantify?

• Is this then not a form of measurement?

• What could you do to refine you answers?

Let’s Take A Measurement Test…

# Question

Lower Bound (95% chance value is higher)

Upper Bound(95%chance value is lower)

Actual

1 What year did Hernán Cortés land in Mexico?

1519

2 What is the wingspan of a Boeing 747 jet?

59.6 m

3 How many hectares make up the entire area of the Amazon Rainforest?

62million

What Do We Mean By Measurement?

To quantify something?

To compute an exact value?

To reduce to a single number?

To choose a representative amount?

Well not exactly…

DEFINITION OFMEASUREMENT

A quantitatively expressed reduction of uncertainty based on one or more observations

…or simply put

Observations that quantitatively reduce

uncertainty

A mere reduction in uncertainty (not elimination) is enough to consider it a ‘measurement’

What To Measure?

Example: How big is the car?What does this mean – what type or model, weight, height, length, how many people it can conformably hold?

What are we really measuring when we say:

• Improving brand?

• Increasing our social license to operate?

• Improved health and well‐being?

• More engaged employees?

How: Measurement Instruments

very precise indirect, extrapolated, inferred or deductive reasoning

For many, measurement seems impossible when it is necessaryto infer or deduce the ‘unseen’

from something ‘seen’

Measurement Methods & Myths

1) It’s never been measured before…

There is a tendency to believe you are the first to measure, research will most certainly prove you wrong

2) I have little or no data on the subject…

Don’t assume only direct answers to your questions are useful, extrapolation is an amazing substitute

3) It is not precise enough… Error is inherent to all measurements, don’t be dismissive, keep the purpose in mind –uncertainty reduction, not elimination

4) I cannot afford to collect the information…

Think of your first idea as the ‘hard way’ to measure, and with a little more ingenuity you’ll identify an easier, more economical approach

Let’s start with perceived obstacles that often keep ‘intangibles intangible’

Not Convinced? The Value Of More Information

When is it worth gathering more information?

• Size of the prize?

• How certain do we need to be?

• What’s the chance and cost of being wrong?

Source: http://timoelliott.com/blog/2014/02/cartoon‐the‐value‐of‐reliable‐information.html

Example:Decomposition, Quantification, Monetization

…And Move Forward With:

Three Key Concepts Toward Making Intangibles More Tangible

DEFINITION OF MONETIZATION

The process of converting or expressing

a result in terms of money or currency

DEFINITION OFDECOMPOSITION

Breaking an uncertain variable into constituent parts to identify directly observable things that are easier to measure

DEFINITION OFQUANTIFICATION

To find, determine, express or calculate (i.e., ‘measure’) the

quantity or amount of something

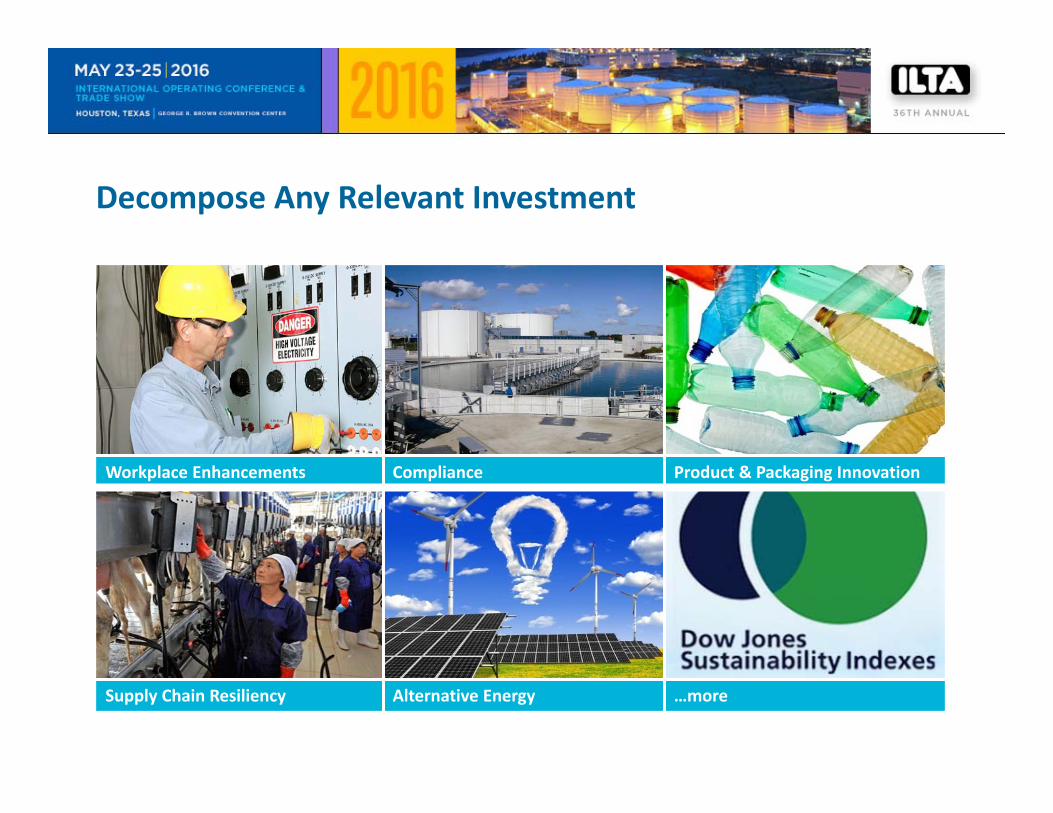

Decompose Any Relevant Investment

Workplace Enhancements Compliance Product & Packaging Innovation

Supply Chain Resiliency Alternative Energy …more

Decomposition – How Does It Work?

For our purposes, 3 to 4 levels of questioning is usually enough, but don’t hesitate to probe ‘deeper’ if needed…

Question 1

What Drives Value?Response A Question 2

In How Many Ways?Response B Response 1 Question 3

To What Degree?

Response n Response 2 Response i Can We:• Observe?• Measure?• Quantify?• Monetize?

Response n Response ii

Response n

Decomposition – Example

Question 1What Drives Value In Sustainability?

Enhancements In The Workplace

Question 2

In How Many Ways?

Gains In Resource Efficiency Engages Our TalentQuestion 3

To What Degree?

Product Innovations Improves Occupational Health & Safety IncreasesRetention Can We:

• Observe?• Measure?• Quantify?• Monetize?

Etc. Improves Working Conditions In The Supply Chain

Increases Attraction

Etc. Increases Productivity

Can we now quantify and monetize increases in employee retention, talent attraction and productivity due to our investments in sustainability?

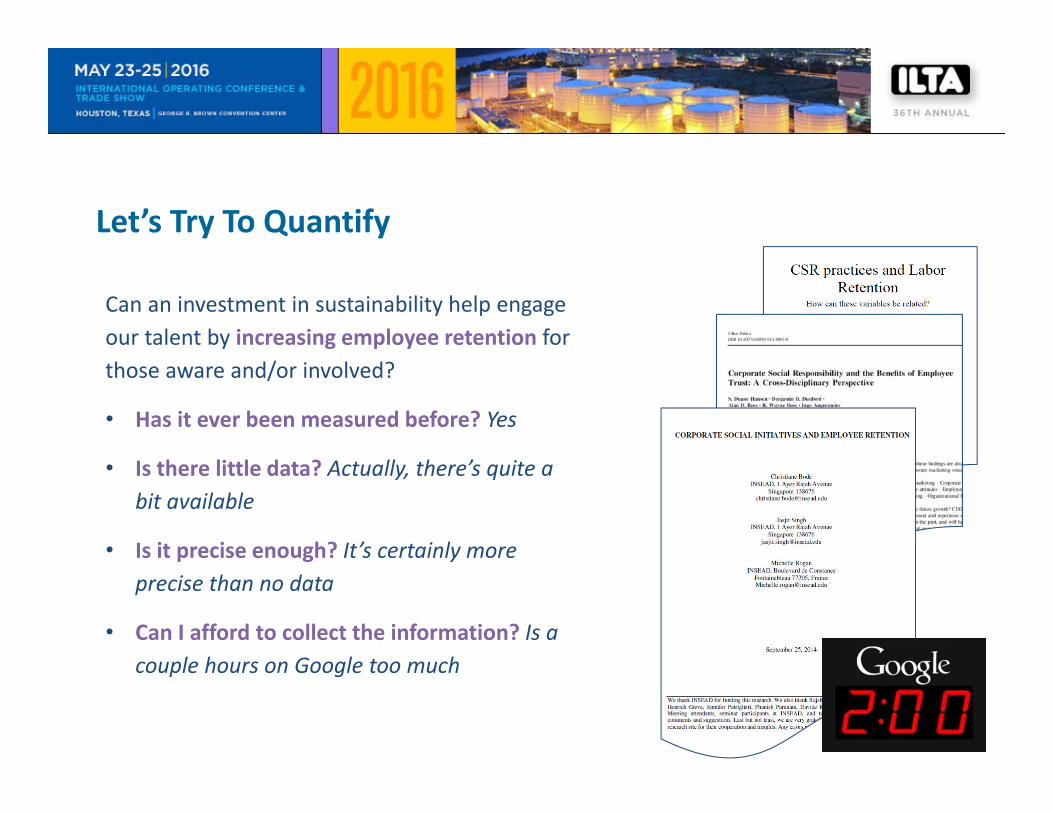

Let’s Try To Quantify

Can an investment in sustainability help engage our talent by increasing employee retention for those aware and/or involved?

• Has it ever been measured before? Yes

• Is there little data? Actually, there’s quite a bit available

• Is it precise enough? It’s certainly more precise than no data

• Can I afford to collect the information? Is a couple hours on Google too much

Past Studies Start To Answer The Question

To What Degree?One study indicated that employees who had been engaged in a sustainability initiative(s) were less likely to consider leaving the company, in this case ≈12% less likely 3 years after that experience

Source: Corporate Social Initiatives & Employee Retention, C, Bode, et. al., INSEAD,

2014Retention Effect of Participation in a Corp. Social Initiative (CSI)

≈12%difference

Now We Are Getting Somewhere…

Assuming there’s reasonably comparability and confidence in the research, we can now say investments in certain sustainability initiatives:

1. Should create value for the organization

2. Through workplace enhancements

3. By engaging our talent

4. Which results in increasing employee retention

5. By ≈12% for those aware and/or involved in such efforts

for every

100 EMPLOYEESengaged

±12 will be less likely to consider

leaving

Quantification To Monetization

Once again, some basic research should yield a way to translate the quantified impact into a monetized impact – in this case we’ll choose ≈20% as the average cost of replacing an employeeNote: Some estimate this value as high as 200%, but most use a number between 10%‐30% Source: There Are Significant Business Costs to Replacing Employees, H. Boushey, et. al.,

Center for American Progress, 2012

Putting It Altogether…Decom

positio

n POTENTIAL RETURNS FOR INVESTING IN SUSTAINABILITY

Workplace Enhancements – From Greater Engagement of Talent

Reduced Employee Turnover/Replacement & Assoc. Costs

Qua

ntificatio

n

# of different employees engaged by the sustainability initiative per year

500

Duration of initiative (years) 5

% of employees less likely to leave as they are aware and/or involved in the initiative 12%

# Of Employees Less Likely To Leave 300

Mon

etization Cost of employee turnover (% of annual salary) 20%

Average salary of engaged employees ($) $50,000

Total Value Created Over 5 Year Period Due To Reduced Employee Turnover/Replacement

$3,000,000

Example: Investment Cash Flow AnalysisPROTECT: Relevant Cost Avoidance Benefits Category Year 1 Year 2 Year 3 Year 4 Year 5 5‐Yr Proj

Benefit1 Production Losses Averted Business Continuity $95,000 $190,000 $380,000 $380,000 $380,000 $1,425,0002 Avoid Reputation Damage Reputational Mgt ‐3 Reduced/Eliminate Response costs Risk Mgt ‐4 Avoid/Minimize Collateral Damage Cost Risk Mgt ‐5 Avoid Escalating/Volatile Resource Cost Business Continuity ‐

Total Cost Avoidance Benefit: $95,000 $190,000 $380,000 $380,000 $380,000 $1,425,000

STRENGTHEN: Relevant Cash Savings Benefits Category Year 1 Year 2 Year 3 Year 4 Year 5 5‐Yr ProjBenefit

1 Less Frictional Cost Assoc w/Expansions Capital Productivity $460,000 $920,000 $920,000 $920,000 $920,000 $4,140,0002 Reduced Resource Consumption Capital Productivity ‐3 Less Pre‐Treatment Needed Capital Productivity ‐4 Reduced Future Capital Cost Financial Flexibility ‐5 Employee Engagement Benefits Emp. Productivity ‐

Total Cash Savings Benefit: $460,000 $920,000 $920,000 $920,000 $ 920,000 $4,140,000

Investment Cost Summary Category Year 1 Year 2 Year 3 Year 4 Year 5 5‐Yr Proj Cost1 Watershed Conservation Practices Inc. in Water Fund $02 Landowner Compensation Inc. in Water Fund $03 Training, Guidelines, Best Practice Sharing Inc. in Water Fund $04 Water Fund Participation (2 FTE @ 10%) Water Fund Element $40,000 $40,000 $40,000 $40,000 $40,000 $200,0005 Water Fund Contributions Conservation $1,000,000 $1,000,000 $1,000,000 $1,000,000 $1,000,000 $5,000,000

Total Cost: $1,040,000 $1,040,000 $1,040,000 $1,040,000 $1,040,000 $5,200,000

Cash Flow Forecast: $(485,000) $70,000 $260,000 $260,000 $260,000 $365,000

Hurdle Rate: Net Present Value > 0: $185,000 PASSEDHurdle Rate: Internal Rate of Return >15%: 18% PASSED

Assumptions Notes Discount Rate: 8%; Finance Rate: 8%; Reinvestment Rate: 8% Gradual ramp‐up of benefit realization as indicated

Gray shaded areas represent additional possible benefits not estimated at this time

Thank you.

Francisco Cordero+1 404 414 [email protected]

For additional information contact:

Francisco Cordero+1 404 414 [email protected]

For additional information contact: