Understanding International Gross Capital Flows - UW · Understanding International Gross Capital...

24

Understanding International Gross Capital Flows 1 International Gross Capital Flows: New Uses of Balance of Payments Data and Application to Financial Crises Thorsten Janus, University of Wyoming Daniel Riera-Crichton, Bates College Abstract Most studies of international financial openness and crises link economic performance to either the net inflow of capital or the gross inflow (outflow) defined as the change in foreign (domestic) holdings of domestic (foreign) assets over a period. In this paper we decompose the net inflow into four rather than two components. We show that the four- way decomposition provides a better understanding of six recent financial crises and predicts sudden stops better than a standard two-way decomposition. We conclude that four-way decompositions can be more informative than either the net capital inflow or two-way decompositions of the net inflow. Keywords: Capital Flows, Financial Integration, External Crises, Balance of Payments Crises JEL: F21, F32, F36, G15

-

Upload

nguyenkhuong -

Category

Documents

-

view

215 -

download

0

Transcript of Understanding International Gross Capital Flows - UW · Understanding International Gross Capital...

Understanding International Gross Capital Flows

1

International Gross Capital Flows: New Uses of

Balance of Payments Data and Application to

Financial Crises

Thorsten Janus, University of Wyoming

Daniel Riera-Crichton, Bates College

Abstract

Most studies of international financial openness and crises link economic performance to

either the net inflow of capital or the gross inflow (outflow) defined as the change in

foreign (domestic) holdings of domestic (foreign) assets over a period. In this paper we

decompose the net inflow into four rather than two components. We show that the four-

way decomposition provides a better understanding of six recent financial crises and

predicts sudden stops better than a standard two-way decomposition. We conclude that

four-way decompositions can be more informative than either the net capital inflow or

two-way decompositions of the net inflow.

Keywords: Capital Flows, Financial Integration, External Crises, Balance of Payments

Crises

JEL: F21, F32, F36, G15

Understanding International Gross Capital Flows

2

1. Introduction

With a supportive institutional framework, international capital flows and financial

openness have the potential to advance economic growth, stability, and development. For

instance, they can promote investment and financial development (Baldwin and Martin

1999, Chinn and Ito 2006) or even jump-start economic development (Murphy et al

1989). When the institutional framework is weak, however, international capital flows

and financial openness can lead to bubbles and financial crises (Prasad et al. 2003).

A number of papers explore the economics of capital flows. However, most

empirical (Burnside et al. 2004, Bordo et al. 2010) as well as theoretical papers -

including business cycle and growth studies (Barro et al. 1992, Aghion et al. 2004) as

well as financial crisis models (Calvo 1998, Dooley 2000) – have focused on the net

capital inflow. A smaller empirical literature, which we discuss below, distinguishes

gross inflows and outflows of capital.1 In this paper, however, we argue that a focus on

either net flows or its component gross in- and outflows may be unnecessarily restrictive.

In order to express our departure from previous work, we note that the standard

definition of the net capital inflow (NI) is ALNI where L ( A ) is the increase

in foreign (domestic) holdings of domestic (foreign) assets in the balance of payments

1There may be several reasons to study gross capital flows. For one thing, if only net inflows mattered, then

it is unclear why gross flows are many times larger. Inflowing capital may affect a country’s output

composition, technology or institutions differently from outflowing capital (Baldwin and Martin 1999,

Abiad et al. 2008). In- and outflows may also differ according to risk, returns, and contractual lending

terms (Mody and Murshid 2005), and the liquidity and information sets of investors (Rothenberg and

Warnock forthcoming, Tille and van Wincoop 2008).

Understanding International Gross Capital Flows

3

(BoP) over the period.2 The gross inflow (outflow) is L ( A ). Although this definition

seems intuitive, a sizable share of the BoP recorded changes in assets holdings (for

various countries, years and asset categories), however, are actually negative.3 A negative

change in foreign (domestic) holdings of domestic (foreign) assets represents

disinvestment in the domestic (foreign) economy. When the standard definition of the

inflow (outflow), L ( A ) simply adds the negative and positive changes across asset

categories in the BoP –the categories are FDI, portfolio, and other capital flows - it fails

to distinguish a fall in new foreign investment from a corresponding disinvestment. Since

many countries face imperfections in financial markets, the implicit assumption that

economy-wide foreign investment and disinvestment are perfect substitutes is unlikely to

be correct. Intuitively, disinvestment is the disruption of an existing credit relationship,

and if collateral or information is relationship-specific, it may be difficult for a borrower

to find a new domestic or foreign lender despite a high social return to lending (Bernanke

1983, Caballero and Krishnamurthy 2001). Liquidity problems of industries hit by

disinvestment shocks may spread via backward and forward linkages. For instance,

Hendricks and Singhal (2005) find that supply-chain disruptions for US firms lead to

cumulative abnormal stock market returns of -40% over a three year period starting one

year before the disruption announcement.4

2 See for example Ito (1999), Caballero et al. (2004), Alfaro et al. (2005), Faucette et al. (2005), Prasad and

Wei (2005), Rothenberg and Warnock (forthcoming), and Tille and van Wincoop (2008).

3 In our dataset, about 25% of recorded asset changes and more than 10% of liability changes are negative.

4 Foreign disinvestments may also warn future investors to stay away or cause a fire-sale of assets

exacerbating initial liquidity problems. Even if some domestic agents increase foreign credit access at the

Understanding International Gross Capital Flows

4

Given the potential asymmetries between foreign investment and disinvestment,

we extract a disinvestment measure from the balance of payments using the identity

AALLNI4 , (1)

0L : positive liability changes/inflowing foreign investment

0L : absolute value of negative liability changes/outflowing foreign disinvestment

0A : positive asset changes/outflowing domestic investment

0A : absolute value of negative asset changes/inflowing domestic disinvestment.

Equation (1) identifies four sources of variation in a country’s net capital inflow.

In contrast, the two-way decompositions used in previous work only considers variations

in the “net gross” inflow )( LLL and the “net gross” outflow )( AAA .

Thus, the standard decomposition fails to measure investment separately from

disinvestment and treats the two as perfect substitutes. We show below that the four-way

decomposition provides a better explanation of six recent financial crises and predicts

sudden stops empirically better than the standard decomposition. For instance, the

standard methodology suggests that recent crises in Indonesia, Mexico, and South Korea

largely reflected declining gross capital inflows. Our more precise method shows that

these crises were mainly due to foreign disinvestment. We further show that that in South

Korea there was a sizable domestic capital outflow accompanied by domestic capital

repatriation during the crisis. We similarly identify a large amount of capital repatriation

to the US and UK during the global crisis of 2008-9.

same time others lose it, leaving aggregate foreign lending unchanged, credit-unconstrained agents may be

unwilling to lend to constrained agents (Caballero and Krishnamurthy 2001).

Understanding International Gross Capital Flows

5

We believe that the four-way decomposition of net capital inflows in equation (1)

can be important for policy makers. First, it can help distinguish the output effects of

international investments from those of disinvestments. For instance, if foreign

disinvestments [ L ] decrease output more than domestic capital outflows [ A ] during

financial crises (Janus and Riera-Crichton 2010), then the benefits of capital controls may

outweigh the costs for the former but not the latter.5 If domestic residents tend to be well-

informed, and their capital promotes output growth more than asset bubbles, then it may

be better to encourage inflows from capital repatriation [ A ] than foreign inflows [ L ].

Second, the four-way decomposition can reveal whether policies needed to retain existing

investors and attract new investors are different. Third, as noted it can help policy

markers predict financial crises. Fourth, by distinguishing four rather than two types of

capital flows, and correctly classifying disinvestments as outflows rather than negative

inflows, it can help policy-makers design and monitor effectiveness of capital controls.

The paper belongs to the literature linking international capital flows to economic

outcomes, such as growth and financial crises. While the literature has focused on net

capital flows (see Obstfeld 2009 for a survey), several recent papers link gross capital

flows to financial crises. Broner et al. (2011) show that gross capital flows are large and

volatile compared to net flows, as well as procyclical in the sense of retrenching during

crises. Rothenberg and Warnock (forthcoming) find that roughly half of the sudden stops

in their sample reflect a rise in capital outflows or “sudden flight” more than a fall in

inflows or a “true sudden stop” (Faucette et al. 2005). Using different definitions, Cowan

5 Conversely, controls on domestic outflows may be justified if they are the main driver of fluctuations in

the net capital inflow (Rothenberg and Warnock forthcoming).

Understanding International Gross Capital Flows

6

et al. (2008) find that outflow surges account for eighteen of one hundred sudden stops in

their sample, while inflow declines account for fifty-seven. Forbes and Warnock

(forthcoming) study episodes of “surge,” “stop,” “flight,” and “retrenchment” in capital

flows, defined, respectively, as sharply increasing and decreasing inflows and sharply

increasing and decreasing outflows. Our key departure from these papers is that we study

a four-way rather than two-way decomposition of net capital flows.

In the remainder of the paper, Section 2 applies the four-way decomposition (1) to

explain six recent financial crises. Section 3 applies it to sudden stop prediction and

Section 4 concludes. Most variable definitions and data sources are in the appendix.

2. Explaining Six Recent Financial Crises

In this section we study gross private international capital flows during six recent

financial crises: South Korea and Indonesia in 1997, Mexico in 1994, Argentina in 2002,

and the US and UK during the Great Recession of 2008-9.6

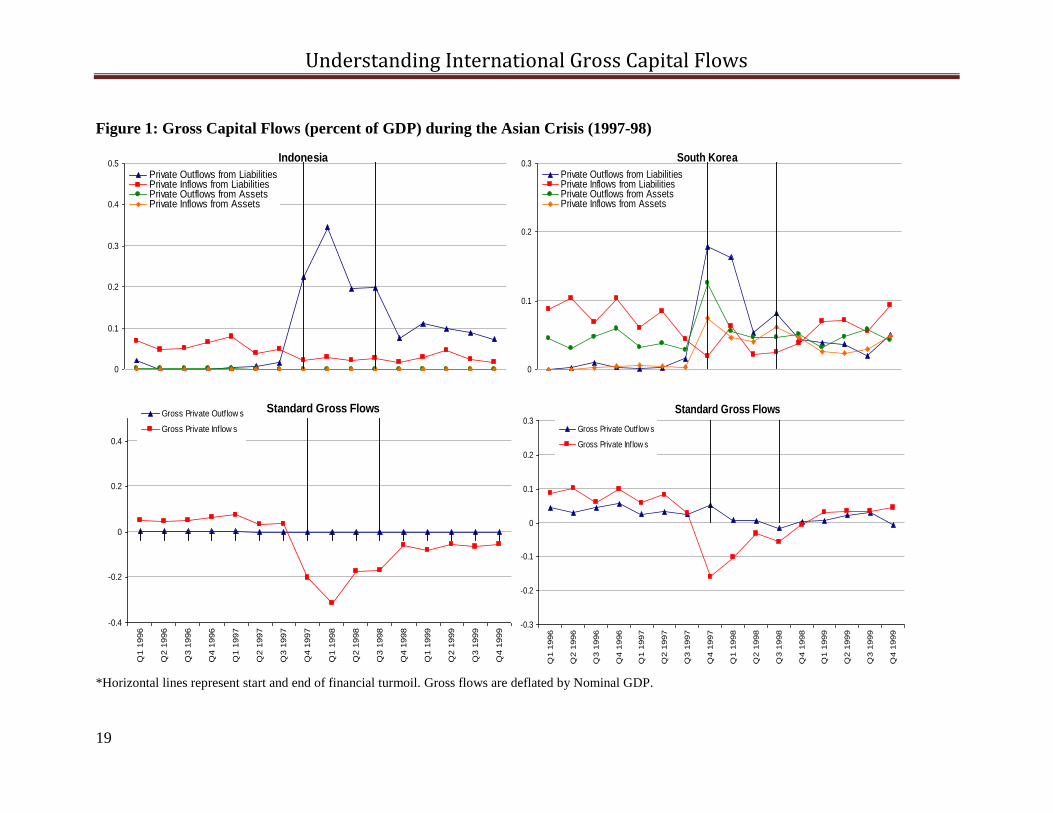

In Figure 1, the thick lines mark the balance of payments crises suffered by

Indonesia and South Korea in 1997-8, as identified in Kaminsky and Reinhart (1999).

According to the standard two-way net inflow decomposition, the proximate cause of

both South Korea’s and Indonesia’s balance of payments crisis was a sharp decline in

gross capital inflows from positive to highly negative levels. Although a negative total

inflow implies some degree of disinvestment, the size of the disinvestment is not clear. In

6 We focus on private capital flows rather than official flows because the former are more important for

most countries and may have different dynamics than official flows. The data source is described below.

Understanding International Gross Capital Flows

7

contrast, our four-way decomposition estimates the foreign disinvestment more precisely

(the sharp spike in private outflows from liabilities [ L ] in the upper panels).

Interestingly, between the second quarter of 1997 and the time the crisis hit in the fourth

quarter, there was almost no change in foreign inflows to Indonesia (private inflows from

liabilities L[ ]) and only a moderate fall in foreign inflows to South Korea. The four-way

decomposition therefore establishes, in a firmer and more precise manner than the

standard two-way decomposition, that the proximate cause of both crises was investment

reversals. Another novel finding is that we observe both a rise in South Korean capital

outflows (private outflows from assets [ A ]) and repatriation of capital by South

Koreans (private inflows from assets ][ A ). One possibility is that South Korean

investors repatriated funds from abroad to buy or support projects abandoned by foreign

investors. Thus, South Korean capital may have put a floor under asset prices.

Next, using the left half of Figure 2 we study Mexico’s balance of payments crisis

in 1994-95 (again as defined in Kaminsky and Reinhart (1999)). As for the Asian

economies, the standard decomposition suggests that Mexico’s loss of capital was

entirely due to a fall in gross inflows. However, it remains unclear how much reflected

disinvestment as opposed to declining new investment. The four-way decomposition

shows that after an early sharp decline inflows actually remained substantial and stable in

the four quarters leading up to the crisis. As with the Asian crises, therefore, Mexico’s

balance of payments crisis was associated with foreign disinvestment more than a fall in

new foreign investment.

Understanding International Gross Capital Flows

8

The right side of Figure 3 shows capital flows surrounding Argentina’s current

account reversal, banking and debt crisis in the first quarter of 2002.7 In this case, while

the two-way decomposition shows a declining capital inflow leading up to the crisis, the

four-way decomposition shows that foreign investment in Argentina (private inflows

from liabilities) actually increased in the two quarters preceding the crisis. Thus, the fall

in foreign acquisitions of Argentinean assets is more than fully explained by foreign

disinvestment. Moreover, as in South Korea, both foreign disinvestment (private outflows

from liabilities) and Argentinean capital repatriation (private inflows from assets) rose

preceding the crisis. Similarly to South Koreans, therefore, Argentineans may have

purchased domestic assets from foreigners. Finally we note that, comparing the spikes in

outflows from assets with those of outflows from liabilities, the former appear to lead the

latter. This may suggest that domestic investors left Argentina before foreign investors.

Based on data from financial markets, Frankel and Schmukler (1996) similarly find that

domestic investor flight Granger-caused foreign flight during Mexico’s 1994-95 crisis

and conclude that domestic investors may have seen the crisis coming earlier.

Understanding any information asymmetries and causal relations between foreign and

domestic investor behavior may be important to understand and predict financial crises.

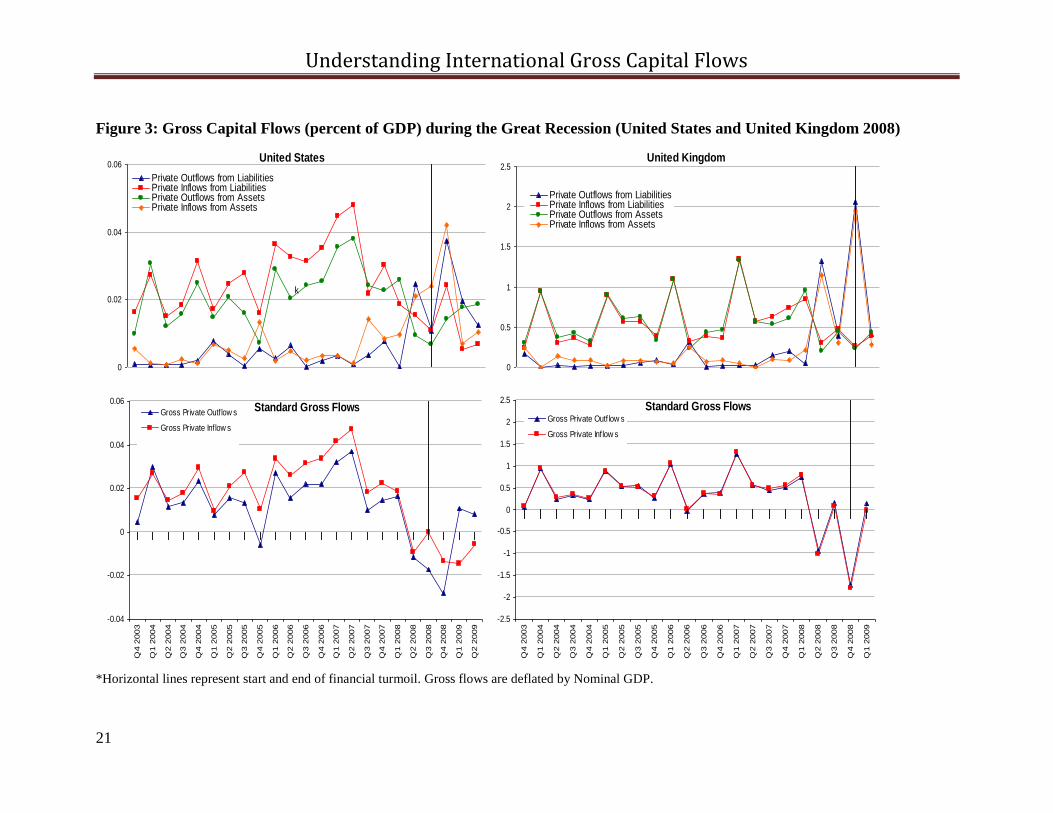

Finally, in Figure 4, we focus on the United States and United Kingdom during

the Great Recession. According to the two-way decomposition, both capital inflows to

the US and outflows fell sharply before the crisis. Once the crisis began, inflows were

7Since Argentina’s crisis and the Great Recession years we study in Figure 4 are not included in Kaminsky

and Reinhart (1999), we get the crisis quarters from Janus and Riera-Crichton (2010). Each crisis quarter

features a rise in the current account-to-GDP ratio of more than twice the country-specific standard

deviation of that ratio, as well as an annual three percentage point rise in the current account-to-GDP ratio.

Understanding International Gross Capital Flows

9

fairly stable, but there was a sizable increase in outflows. In contrast, but more consistent

with the anecdotal evidence, the four-way decomposition shows a large increase in both

foreign disinvestment from the US (outflows from liabilities) and US repatriation of

capital (inflows from assets). Thus, as foreign investors disengaged from the US, US

investors disengaged from abroad. The standard two-way decomposition fails to capture

the size of both foreign flight from the US (the standard inflows measure only goes

slightly negative) and US disinvestment from abroad. Nor does it reveal that only a small

part of the rise in US holdings of foreign assets after the crisis came from US residents

purchasing foreign assets. Rather, as shown by the four-way decomposition, it came from

falling US repatriation of capital (inflows from assets). For the UK, similarly, the two-

way decomposition underestimates both foreign investor flight and capital repatriation.

3. Predicting Sudden Stops

In this section, we study the ability of a four-way decomposition of net capital inflows to

predict financial crises in the form of sudden stops. Following Hutchison and Noy (2006)

we define a sudden stop as the simultaneous occurrence of a currency crisis and a current

account reversal. Calvo (1998) argues that the output loss from a current account reversal

may be larger when accompanied by a real depreciation and Hutchison and Noy (2006)

provide supporting evidence. For robustness, we use two measures of current account

reversals: a rise in the current account-to-GDP ratio of more than twice the country-

specific standard deviation of that ratio (ST1); and a rise of three percentage points or

more in the current account-to-GDP ratio compared to the same quarter the previous year

Understanding International Gross Capital Flows

10

(ST2).8 We define a currency crisis as a departure of two standard deviations or more in

the level of exchange market pressure (Eichengreen et al. 1996), formulated as follows

for country i and time t : 2

%

2

%

%%

Ei

it

Ri

it

it

EREMP

. In this expression, itR% is the

percent change in official reserves from last period, itE% stands for the percent change

in the real exchange rate, and 2

% Ri and 2

% Ei are the respective country-specific

variances of the percent change over the sample years.9

Due to the binary nature of the dependent variables, we estimate a logit model.

The state transition matrices presented in Table 1 uncover a sizeable persistence in the

two crisis dummies and undergoing financial turmoil one quarter may affect the

probability of turmoil the next quarter. Thus, we control for lagged crisis incidence.

The estimated crisis probability for each observation, denoted ipö , is a continuous

variable, while the dependent variable is binary. We, therefore, follow the large body of

literature on Early Warning Systems in defining a threshold C as follows: If Cpi ö ,

then, the model is said to predict a crisis, and otherwise, it does not. The threshold is

usually chosen to minimize the noise-to-signal ratio, i.e. the ratio of incorrectly to

correctly predicted crises (Berg and Patillo 1999): )(/)( CTPCFPNSR , where FP and

8 The incidence of the two types of sudden stops in the data is available on request.

9While Hutchison and Noy (2006) also use real exchange rates, Eichengreen et al. (1996) use nominal rates.

The latter also include nominal interest rate deviations in the EMP index, but most of the subsequent

literature has focused on reserve and exchange rate changes due to data limitations.

Understanding International Gross Capital Flows

11

TP denote the number of false and true positive predictions. For generality we present

the NSRs generated by the capital flow decompositions for all thresholds )1,0(C .10

Our regressions use quarterly balance of payments data from the IMF’s

International Financial Statistics (IFS). It includes 43 non-OECD economies, most of

which are emerging markets, as well as Mexico and South Korea.11

It spans 1970 to

2009, although it is limited before the mid 1980s. Table 2 shows the summary statistics.

Apart from gross capital flows, we control for the lags of output growth, the current

account, the stock of international reserves, domestic credit growth, a dummy for

hyperinflation, and relative export growth (the growth of the exports-imports ratio).12

Columns (1) and (3) in Table 3 show the results for the four-way decomposition

of capital flows. Columns (2) and (4) show the results for the two-way decomposition. A

Wald test after each of regressions (1) and (3) rejects at the 99% confidence level that the

coefficient on inflows from liabilities equals minus the coefficient on outflows from

liabilities. Thus, the coefficient on inflows using the standard decomposition seems to

reflect the average of the heterogeneous effects of a rise in new foreign investment and a

fall in foreign investment reversals.13

In Figure 4 we show our method’s relative ability

10

The working paper shows that using other measures to compare Early Warning Systems gives similar

results. Candelon et al (2010) and Granger and Machina (2006) present a broader discussion of forecasting.

11 We drop the Bahamas, Bahrain, Panama and Tonga due to their large capital flows-to-GDP ratios.

12 These controls follow the literature on Early Warning Systems (Berg and Patillo 1999, Kaminsky and

Reinhart 1999, Kumar et al. 2003, Candelon et al. 2010).

13 The qualitative results are not sensitive to omitting the lagged dependent variable or adding country fixed

effects; estimating a complementary log-log, linear or probit model; or controlling for fiscal expenditures,

economic or financial risk, terms of trade, financial development or trade openness. We are also aware that,

Understanding International Gross Capital Flows

12

to predict sudden stops as measured by the NSR . Using our first sudden stop measure, the

results in the upper panel show that the four-way decomposition of net inflows neither

helps nor hinders crisis prediction.14

In contrast, the results for the second sudden stop

measure in the lower panel strongly favor four-way decomposition: the NSR is

substantially lower than for the two-way decomposition for almost all crisis thresholds.

4. Conclusion

Most macroeconomic studies of international capital flows focus on either net inflows or

gross inflows (outflows) computed as the increase in foreign (domestic) holdings of

domestic (foreign) assets in the balance of payments. In this paper, however, we show

that decomposing net inflows into four rather than two gross flow components can help to

explain six recent financial crises and predict sudden stops empirically. On this basis we

believe that four-way decompositions can increase the ability of policy-makers to

monitor and manage international capital flows. all else constant, a change in any gross capital flow in (1) will affect the current account used to define the

sudden stop dummy. This mechanical link between gross flows and the current account cannot be driving

the results, however. First, we are already controlling for the current account. Second, gross capital flows

define the level of the current account, while sudden stops are defined using the change.

14 One reason the NSRs are similar using our first sudden stop measure may the relatively few crisis in the

data. For instance, with 20 false and 35 true positives, one falsely predicted crisis changes the NSR by (21-

20)/35=0.029 (Candelon et al. 2010). The four-way decomposition does do slightly better at predicting true

positives, however. This is consistent with outflows from liabilities being the only significant gross flow in

the first two columns in Table 3, and may be important if the value of preparing for a crisis exceeds the

value of preparing needlessly (so true positives are more valuable than false positives).

Understanding International Gross Capital Flows

13

References

Abiad, A., Oomes, N. & Ueda, K. (2008) The Quality Effect: Does Financial

Liberalization Improve the Allocation of Capital? Journal of Development Economics,

87(2), 270-82.

Aghion, P., Howitt, P. & Mayer-Foulkes, D. (2004) The Effect of Financial Development

on Convergence: Theory and Evidence. Quarterly Journal of Economics, 120(1), 173-

222.

Alfaro, L., Kalemli-Ozcan, S. & Valosovych, V. (2005) Capital Flows in a Globalized

World: The Role of Policies and Institutions. In Capital Controls and Capital Flows in

Emerging Economies: Policies, Practices and Consequences (S. Edwards, Ed.). Chicago:

University of Chicago Press.

Baldwin, R. & Martin, P. (1999) Two Waves of Globalization: Superficial Similarities,

Fundamental Differences. NBER Working Paper No. 6904.

Barro, R. J, Mankiw, G. N. & Sala-i-Martin, X. (1992) Capital Mobility in Neoclassical

Models of Growth. NBER Working Paper No. 4206.

Berg, A., & Pattillo, C. (1999) Predicting Currency Crises: The Indicators Approach and

an Alternative. Journal of International Money and Finance, 18(4), 561-586.

Bernanke, B. S. (1983) Nonmonetary Effects of the Financial Crisis in the Propagation of

the Great Depression. American Economic Review, 73(3), 257-76.

Bordo, M., Cavallo, A. & Meissner, C. M. (2010) Sudden Stops: Determinants and

Output Effects in the First Era of Globalization. Journal of Development Economics,

91(2), 227–241.

Understanding International Gross Capital Flows

14

Broner, F. A, Didier, T., Erce, A. & Schmukler, S. L. (2011) Gross Capital Flows:

Dynamics and Crises. World Bank Policy Research Working Paper No. 5768.

Burnside, C., Eichenbaum, M. & Rebelo, S. (2004) Government Guarantees and Self-

Fulfilling Speculative Attacks. Journal of Economic Theory, 119(1), 31-63.

Caballero, R. J & Krishnamurthy, A. (2001) International and Domestic Collateral

Constraints in a Model of Emerging Market Crises. Journal of Monetary Economics,

48(3), 513-48.

Caballero, R. J, Cowan, K. & Kearns, J. (2004) Fear of Sudden Stops: Lessons from

Australia and Chile. Journal of Policy Reform, 8(4), 313-54.

Calvo, G.A. (1998) Capital Flows and Capital-Market Crises: The simple Economics of

Sudden Stops. Journal of Applied Economics, 1(1), 35-54.

Candelon, B., Dumitrescu, E.-I. & Hurlin, C. (2010) How to Evaluate an Early Warning

System? Towards a Unified Statistical Framework for Assessing Financial Crises

Forecasting Methods. Working Paper, Maastricht University.

Chinn, M. & Ito, H. (2006) What Matters for Financial Development? Capital Controls,

Institutions, and Interactions. Journal of Development Economics, 61(1), 163-192.

Cowan, K., De Gregorio, J., Micco, A. & Neilson, C. (2008) Financial Diversification,

Sudden Stops, and Sudden Starts. In Current Account and External Financing (K.

Cowan, S. Edwards, R. Valdés, & N. Loayza, Eds.). Central Bank of Chile.

Dooley, M. P. (2000) A Model of Crises in Emerging Markets. Economic Journal,

110(460), 256-272.

Eichengreen, B., Rose, A. & Wyplosz, C (1996) Contagious Currency Crises. NBER

Working Paper No. 5681.

Understanding International Gross Capital Flows

15

Faucette, J., Rothenberg, C. & Warnock, F. (2005) Outflows-induced Sudden Stops.

Journal of Policy Reform, 8(2), 119-130.

Forbes, K., & Warnock, F. (forthcoming) Capital Flow Waves: Surges, Stops, Flight and

Retrenchment. Journal of International Economics.

Frankel, J. A & Schmukler, S. L. (1996) Country Fund Discounts and the Mexican Crisis

of December 1994: Did Local Residents Turn Pessimistic before International Investors?

Open Economies Review, 7(1), 511-534.

Granger, C. W. J. & Machina, M. J. (2006) Forecasting and Decision Theory. In

Handbook of Economic Forecasting, Vol. 1 (G. Elliott, C. W. J. Granger & A.

Timmermann, Eds.). Amsterdam: North-Holland.

Hendricks, K. B & Singhal, V. R. (2005) An Empirical Analysis of the Effect of Supply

Chain Disruptions on Long-Run Stock Price Performance and Equity Risk of the Firm.

Production and Operations Management, 14(1), 35-52.

Hutchison, M. M. & Noy, I. (2006) Sudden Stops and the Mexican Wave: Currency

Crises, Capital Flow Reversals and Output Loss in Emerging Markets. Journal of

Development Economics, 79(1), 225-248.

Ito, T. (1999). Capital Flows in Asia. NBER Working Paper No. 7134.

Janus, T. & Riera-Crichton, D. (2010) The Output Effects of Gross Foreign Investment

Reversals. Working Paper, Bates College.

Kaminsky, G. L. & Reinhart, C. M. (1999) The Twin Crises: The Causes of Banking and

Balance-of-Payments Problems. American Economic Review, 89(3), 473-500.

Kumar, M., Moorthy, U. & Perraudin, W. (2003) Predicting Emerging Market Currency

Crashes. Journal of Empirical Finance, 10(4), 427-454.

Understanding International Gross Capital Flows

16

Mody, A. & Murshid, A. P. (2005) Growing up With Capital Flows. Journal of

International Economics, 65(1), 249-266.

Murphy K. M, Shleifer, A. & Vishny, R. W. (1989) Industrialization and the Big Push.

Journal of Political Economy, 97(5), 1003-26.

Obstfeld, M. (2009) International Finance and Growth in Developing Countries: What

Have We Learned? IMF Staff Papers, 56(1), 63-111.

Prasad, E., Rogoff, K., Wei, S.-J. & Kose, M. A. (2003) The Effects of Financial

Globalization on Developing Countries: Some Empirical Evidence. IMF Occasional

Paper No. 220.

Prasad, E. & Wei, S.-J. (2005) The Chinese Approach to Capital Inflows: Patterns and

Possible Explanations. IMF Working Paper No. 05/79.

Rothenberg, A., & Warnock, F. (forthcoming) Sudden Flight and True Sudden Stops.

Review of International Economics.

Tille, C. & Wincoop, E. v. (2008) International Capital Flows under Dispersed

Information: Theory and Evidence. NBER Working Paper No. 14390.

Understanding International Gross Capital Flows

17

Appendix: Variables, Data Sources, Figures and Tables

Real GDP Growth: Defined as the as the quarter-on-quarter percentage change in real

$US GDP, Ln(Y(t))-lnY(t-4)). The main source is the IMF’s International Financial

Statistics (IFS) dataset, from which we also draw GDP deflators. We first transform

nominal to real GDP, then convert it to US$ using the nominal exchange rate in IFS, and

then compute the growth rate. Other sources for real GDP are OECD Source, Economist

Intelligence Unit (EIU), DataStream (DS) and the CEIC Data Company Ltd. (CEIC).

Total Gross Capital Flows: Total gross flows are calculated adding up the absolute

value of all liability increases and decreases plus total asset increases and decreases from

the capital and financial balance of each country.

Private Outflows from Liabilities (POfL): Defined as the absolute value of all

decreases in foreign liabilities from private domestic residents in the financial and capital

accounts.

Private Inflows from Liabilities (PIfL): Defined as the absolute value of all increases in

foreign liabilities from private domestic residents in the financial and capital accounts.

Private Outflows from Assets (POfA): Defined as the absolute value of all increases in

foreign assets from private domestic residents in the financial and capital accounts.

Private Inflows from Assets (PIfA): Defined as the absolute value of all decreases in

foreign assets from private domestic residents in the financial and capital accounts.

Net Inflows: Defined as the current account deficit minus the increase in international

reserves. The main source for balance of payments data is the IMF’s Balance of

Payments Statistics (BOPS). Data for Taiwan and Switzerland was obtained from CEIC.

Understanding International Gross Capital Flows

18

Domestic Credit: defined Stock of domestic credit is measured as bank lending to public

and private sectors, plus bank lending in domestic currency overseas (Line 32 in IFS).

The Main source is IFS but we also use data from EIU, DS and CEIC.

Stock of Reserves: Defined as the total stock of international reserves minus gold.

Sources are IFS, DS and EIU.

Inflation: Domestic CPI Inflation. Main sources are IFS, DS, EIU and CEIC. Hyperinflation

is inflation exceeding 100% per quarter.

Relative Export Growth: The growth rate of the ratio (export/imports) in current US

dollars with export and import data extracted from IFS, DS, EIU and CEIC.

Real Effective Exchange Rate (REER): The real effective exchange rate index

represents a nominal effective exchange rate index adjusted for relative movements in

national price or cost indicators of the home country,

iw

ii

t

i PPeeREER )]/)(/[(

Where e: Exchange rate of the subject currency against the US dollar (US dollars per

rupee in index form); ei: Exchange rates of currency i against the US dollar (US dollars

per currency i in index form); wi: Weights attached to the country/ currency i in the

index; P: Consumer Price Index (CPI) of Subject country and Pi is the Consumer price

index of country i. An Increase in REER corresponds to a Real Domestic Appreciation.

Data belongs to the IFS dataset, OECD and the Broad REER calculated by JP Morgan

and provided through Datastream.

Understanding International Gross Capital Flows

19

Figure 1: Gross Capital Flows (percent of GDP) during the Asian Crisis (1997-98)

*Horizontal lines represent start and end of financial turmoil. Gross flows are deflated by Nominal GDP.

Indonesia

0

0.1

0.2

0.3

0.4

0.5

Private Outflows from LiabilitiesPrivate Inflows from LiabilitiesPrivate Outflows from AssetsPrivate Inflows from Assets

South Korea

0

0.1

0.2

0.3

Private Outflows from LiabilitiesPrivate Inflows from LiabilitiesPrivate Outflows from AssetsPrivate Inflows from Assets

Standard Gross Flows

-0.4

-0.2

0

0.2

0.4

Q1 1

996

Q2 1

996

Q3 1

996

Q4 1

996

Q1 1

997

Q2 1

997

Q3 1

997

Q4 1

997

Q1 1

998

Q2 1

998

Q3 1

998

Q4 1

998

Q1 1

999

Q2 1

999

Q3 1

999

Q4 1

999

Gross Private Outflow s

Gross Private Inflow s

Standard Gross Flows

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

Q1 1

996

Q2 1

996

Q3 1

996

Q4 1

996

Q1 1

997

Q2 1

997

Q3 1

997

Q4 1

997

Q1 1

998

Q2 1

998

Q3 1

998

Q4 1

998

Q1 1

999

Q2 1

999

Q3 1

999

Q4 1

999

Gross Private Outflow s

Gross Private Inflow s

Understanding International Gross Capital Flows

20

Figure 2: Gross Capital Flows (percent of GDP) during financial turmoil in Latin America (Argentina 2002, Mexico 1995)

*Horizontal lines represent start and end of financial turmoil. Gross flows are deflated by Nominal GDP.

Mexico

0

0.01

0.02

0.03

0.04 Private Outflows from LiabilitiesPrivate Inflows from LiabilitiesPrivate Outflows from AssetsPrivate Inflows from Assets

Argentina

0

0.01

0.02

0.03

0.04

0.05

Private Outflows from LiabilitiesPrivate Inflows from LiabilitiesPrivate Outflows from AssetsPrivate Inflows from Assets

Standard Gross Flows

-0.04

-0.02

0

0.02

0.04

Q1 1

993

Q2 1

993

Q3 1

993

Q4 1

993

Q1 1

994

Q2 1

994

Q3 1

994

Q4 1

994

Q1 1

995

Q2 1

995

Q3 1

995

Q4 1

995

Q1 1

996

Q2 1

996

Q3 1

996

Q4 1

996

Gross Private Outflow s

Gross Private Inflow s

Standard Gross Flows

-0.04

-0.02

0

0.02

0.04

0.06

Q1 2

000

Q2 2

000

Q3 2

000

Q4 2

000

Q1 2

001

Q2 2

001

Q3 2

001

Q4 2

001

Q1 2

002

Q2 2

002

Q3 2

002

Q4 2

002

Q1 2

003

Q2 2

003

Q3 2

003

Q4 2

003

Gross Private Outflow s

Gross Private Inflow s

Understanding International Gross Capital Flows

21

Figure 3: Gross Capital Flows (percent of GDP) during the Great Recession (United States and United Kingdom 2008)

*Horizontal lines represent start and end of financial turmoil. Gross flows are deflated by Nominal GDP.

United States

0

0.02

0.04

0.06

Private Outflows from LiabilitiesPrivate Inflows from LiabilitiesPrivate Outflows from AssetsPrivate Inflows from Assets

k

United Kingdom

0

0.5

1

1.5

2

2.5

Private Outflows from LiabilitiesPrivate Inflows from LiabilitiesPrivate Outflows from AssetsPrivate Inflows from Assets

Standard Gross Flows

-0.04

-0.02

0

0.02

0.04

0.06

Q4 2

003

Q1 2

004

Q2 2

004

Q3 2

004

Q4 2

004

Q1 2

005

Q2 2

005

Q3 2

005

Q4 2

005

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Gross Private Outflow s

Gross Private Inflow s

Standard Gross Flows

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

Q4 2

003

Q1 2

004

Q2 2

004

Q3 2

004

Q4 2

004

Q1 2

005

Q2 2

005

Q3 2

005

Q4 2

005

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Gross Private Outflow s

Gross Private Inflow s

Understanding International Gross Capital Flows

22

Figure 4: Noise-to-Signal Ratios (NSR) for Logit Models of Sudden Stops (Type 1 in Upper Panel, Type 2 in Lower Panel)

23

Table 1: Transition Matrices for Sudden Stops

ST 1 0 1 Total ST 2 0 1 Total

0 4,861 57 4,918 0 4,689 100 4,789

% 98.84 1.16 100 % 97.91 2.09 100

1 51 56 107 1 91 145 236

% 47.66 52.34 100 % 38.56 61.44 100

Total 4,912 113 5,025 Total 4,780 245 5,025

97.75 2.25 100 95.12 4.88 100

Notes: ST1 is a sudden stop defined as a currency crisis along with a rise in the current account-to-GDP

ratio of more than twice the country-specific standard deviation of that ratio; ST2 is a sudden stop defined

as a currency crisis along with a quarter-to-quarter rise of three percentage points or more in the current

account-to-GDP ratio.

Table 2: Summary Statistics

Variable Obs Mean Std. Dev. Min Max

Standard Private Gross Inflows* 5429 0.099943 0.241149 -2.04754 3.033564

Standard Private Gross Outflows* 5429 0.083404 0.240495 -2.74348 3.183507

Private Outflows from Liabilities* 5429 0.038408 0.107626 0 3.144324

Private Outflows from Assets* 5429 0.121371 0.256126 0 3.376829

Private Inflows from Liabilities* 5429 0.138351 0.255195 0 3.315092

Private Inflows from Assets* 5429 0.037968 0.107798 0 3.557818

Real Output Growth in US$ 5429 -0.00273 0.228313 -3.75227 0.89835

Current Account Balance* 5429 -0.01148 0.065682 -0.64946 0.291153

Stock of Reserves* 5429 0.432199 0.53556 0.001904 4.258942

Domestic Credit Growth 5429 0.022719 0.231026 -2.71431 3.881695

Hyperinflation dummy 5429 0.01492 0.121244 0 1

Relative Export Growth 5429 3.635688 246.7352 -936.756 18079.07

Notes: *Variables are deflated by GDP. [Private] Outflows from Liabilities, Outflows from Assets, Inflows

from Liabilities and Inflows from Assets correspond to, respectively, L- , A

+, L

+ , and A

- in equation (1).

Standard Private Gross Inflows and Outflows equal, respectively, )( LL and )( AA .

24

Table 3: Sudden Stops Prediction Using Four-and Two-way Decompositions of Net

Capital Inflows into Gross Flows

ST1 ST1 ST2 ST2 FOUR-WAY TWO-WAY FOUR-WAY TWO-WAY

Crisis (t-1) 4.293 4.365 3.635 3.704

[0.421]*** [0.516]*** [0.312]*** [0.299]***

Private Outflows from Liabilities (t-1) 9.816 9.598

[4.126]** [2.425]***

Private Outflows from Assets (t-1) -3.803 2.469

[4.713] [1.985]

Private Inflows from Liabilities (t-1) -0.425 -0.009

[3.6 38] [1.923]

Private Inflows from Assets (t-1) -1.133 -7.184

[5.331] [2.392]***

Standard Private Gross Inflows (t-1) -4.946 -3.027

[3.131] [1.687]*

Standard Private Gross Outflows (t-1) -1.483 4.867

[4.221] [1.738]***

Output Growth (t-1) -0.793 -0.93 -1.046 -1.159

[0.440]* [0.480]* [0.370]*** [0.365]***

Current Account (t-1) -5.328 -6.716 -3.321 -4.677

[3.051]* [3.245]** [2.135] [2.094]**

Stock of Reserves (t-1) -1.449 -0.973 -0.236 -0.071

[0.686]** [0.635] [0.286] [0.256]

Domestic Credit Growth (t-1) 1.302 1.276 -0.336 -0.257

[0.727]* [0.725]* [0.519] [0.515]

Hyperinflation (t-1) -0.399 -0.53 -0.073 -0.133

[0.700] [0.698] [0.621] [0.623]

Relative Export Growth (t-1) -0.109 -0.151 -0.081 -0.112

[0.260] [0.262] [0.165] [0.164]

Observations 2450 2450 2450 2450

Number of countries 43 43 43 43

Pseudo R-Squared 0.3639 0.3584 0.3332 0.3192

Log Likelihood Full Model -172.241 -173.719 -333.509 -340.486

Log Likelihood Only Constant -270.757 -270.757 -500.137 -500.137

Notes: Standard errors in brackets. *,**,*** significant at 10%, 5% and 1%. All gross capital flows, the

current account and the stock of reserves are deflated by GDP. [Private] Outflows from Liabilities

Outflows from Assets, Inflows from Liabilities and Inflows from Assets correspond to, respectively, L- ,

A+, L

+ , and A

- in equation (1). ST1 is a sudden stop defined as a currency crisis along with a rise in the

current account-to-GDP ratio of more than twice the country-specific standard deviation of that ratio; ST2

is a sudden stop defined as a currency crisis along with a quarter-to-quarter rise of three percentage points

or more in the current account-to-GDP ratio.