Ukraine - PKF International · Ukraine PKF Worldwide Tax Guide 2015/16 1

22

2015 / 16

Transcript of Ukraine - PKF International · Ukraine PKF Worldwide Tax Guide 2015/16 1

2015/16

Ukraine

PKF Worldwide Tax Guide 2015/16 1

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed? Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. As you will appreciate, the production of the WWTG is a huge team effort and we would like to thank all tax experts within PKF member firms who gave up their time to contribute the vital information on their country's taxes that forms the heart of this publication. The PKF Worldwide Tax Guide 2015/16 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world's most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 1 January 2015, while also noting imminent changes where necessary. On a country-by-country basis, each summary such as this one, addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country's personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments. While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice. Services provided by member firms include: Assurance & Advisory;

Financial Planning / Wealth Management;

Corporate Finance;

Management Consultancy;

IT Consultancy;

Insolvency - Corporate and Personal;

Taxation;

Forensic Accounting; and,

Hotel Consultancy. In addition to the printed version of the WWTG, individual country taxation guides such as this are available in PDF format which can be downloaded from the PKF website at www.pkf.com

Ukraine

PKF Worldwide Tax Guide 2015/16 2

IMPORTANT DISCLAIMER This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication. This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication. The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication. Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances. PKF International is a family of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms. PKF INTERNATIONAL LIMITED JUNE 2015 © PKF INTERNATIONAL LIMITED All RIGHTS RESERVED USE APPROVED WITH ATTRIBUTION

Ukraine

PKF Worldwide Tax Guide 2015/16 3

STRUCTURE OF COUNTRY DESCRIPTIONS A. TAXES PAYABLE

COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX VALUE ADDED TAX (VAT) FRINGE BENEFITS TAX (FBT) SOCIAL SECURITY CONTRIBUTIONS LOCAL TAXES OTHER TAXES LAND TAX DUTIES FOR THE INITIAL REGISTRATION OF VEHICLES PROPERTY TAX SPECIAL PENSION FUND CHARGES STAMP DUTY EXCISE TAX CHARGE ON ENVIRONMENTAL POLLUTION CHARGE FOR SUBSOIL USAGE

B. DETERMINATION OF TAXABLE INCOME

DEPRECIATION STOCK / INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST EXPENSES LOSSES FOREIGN SOURCED INCOME INCENTIVES

C. FOREIGN TAX RELIEF D. CORPORATE GROUPS E. RELATED PARTY TRANSACTIONS F. WITHHOLDING TAX G. EXCHANGE CONTROLS H. PERSONAL TAX

MILITARY DUTY I. TREATY AND NON-TREATY WITHHOLDING TAX RATE ON DIVIDENDS

Ukraine

PKF Worldwide Tax Guide 2015/16 4

MEMBER FIRM For further advice or information please contact: City Name Contact Information Kyiv Sviatoslav Biloblovskiy +38 044 501 25 31 [email protected] BASIC FACTS Full name: Ukraine Capital: Kiev Main language: Ukrainian Population: 44.29 million (2014 estimate) Major religion: Christianity Monetary unit: Ukrainian Hryvnia (UAH) Internet domain: .ua, .укр Int. dialling code: +380 KEY TAX POINTS • Starting from 2015, the Tax Code determines taxable profits as net profits before tax as per

accounting records, either Ukrainian statutory or International Financial Reporting Standards (IFRS), and adjusted for ‘tax differences’.

• Companies generally pay corporate profit tax at a flat rate of 18%. Reduced rates of 0% or 3%

apply to qualified insurance activities. • Value Added Tax is currently levied at a rate of 20% of the taxable value of domestic supplies,

imported goods and auxiliary services. The rate on exported goods and auxiliary services is 0%. The VAT rate on supply of medicines and medical devices on the list approved by the Cabinet of Ministers of Ukraine is 7%.

• Ukrainian tax residents are subject to Personal Income Tax (PIT) on their worldwide income,

whereas non-residents are only subject to taxation on the Ukrainian sourced portion of their income. The tax rate varies from 5 to 30% of the tax base. It depends on the type and amount of income. The most common applicable rate for PIT is 20%.

• In 2015 all types of incomes, which are object for PIT, are also object for military duty. The rate

of this duty is 1.5% of the taxable income. • When paying wages (or similar payment) the source of payment is obligate to accrue and

transfers to budget unified social contribution tax (USC). The rate varies from 8.41% to 49.7% (depends on risk category, the most common applicable rate is near 37 %) of the accrued income in the form of wage (or similar payment). This part is paid at the expense of the source of payment (employer). The additional rate, which varies from 2.6% to 3.6%, is paid at the expense of the recipient's income.

• Legal entities and individuals (incl. non-residents) are the payers of property tax. The tax rate is

based on the size of the property and set in percentage (not exceeding 2%) to the minimum

Ukraine

PKF Worldwide Tax Guide 2015/16 5

statutory wage determined at 1 January of the reporting year. • Ukrainian government already announced its intention to propose amendments to tax code in

the first quarter of 2015. A. TAXES PAYABLE COMPANY TAX The tax that companies pay is known as corporate profit tax (CPT). Currently, this tax is calculated at a flat rate of 18%. A special reduced rate of 5% is set for the companies, which are related to software industry. For insurance activity, there is an additional tax, which is 3% on amount of insurance contracts from the tax object. This tax is the difference that reduces the profit before tax of the insurer. The rate of this tax for the contracts with term life insurance, a voluntary health insurance and insurance contracts within the non-state pension is 0%. Special rates apply to certain types of businesses. Starting from 01.01.2015 all entities with net taxable income more than UAH 20,000,000 (for the period ended 31.12.2014 – 10 000 000 UAH) must pay CPT in advance. The taxable base is calculated as 1/12 of the last fiscal year's CPT and must be paid in equal parts monthly. The exception of this rule is set for the entities with negative financial result in the prior year. There are some new restrictions provided for transaction between related parties as a new edition of p. 39 of Tax Code came into force on 01.01.2015. The transaction between related parties with amount exceeding UAH 1 million (VAT not included) or 3% of taxable income is recognized as "controlled". At the same time the total taxable income of the entity and / or its related parties should exceed 20 000 000 UAH. The taxable base for such transaction should be comparable to the taxable bases of similar transactions held by non-related parties. CAPITAL GAINS TAX There is no separate capital gains tax. Capital gains are treated as ordinary income. BRANCH PROFITS TAX There is no special profits tax on branches of foreign companies in Ukraine. VALUE ADDED TAX (VAT) VAT is levied on the sale of most merchandise and services and on imported goods. According to the Tax Code, the taxable base for VAT is defined as the contractual value of the goods or services supplied. There is a special method of calculating the taxable base for controlled operations as it is set in p.39 of Tax Code. The base for the operations which are recognized as controlled should be not less than the base which is calculated for the same operations between non-related parties (known as the arm-length principle (ALP)).

Ukraine

PKF Worldwide Tax Guide 2015/16 6

VAT is currently levied at a rate of 20% of the taxable value of domestic supplies, imported goods and auxiliary services. The VAT rate on exported goods and auxiliary services is 0%. The rate on supply of medicines and medical devices on the list approved by the Cabinet of Ministers of Ukraine is 7%. Ukrainian VAT legislation for the taxation of services applies the concept of "place of supply”. In general, services rendered within the Customs territory of Ukraine are taxed at the general VAT rate, regardless of whether they are rendered to residents or non-residents. However, there are certain exceptions to this rule. According to the Tax Code, certain transactions are exempt from VAT and are not subject to VAT. If entities meet certain criteria, they may be subject to mandatory registration as VAT payers. One such criterion is the volume of taxable supplies of goods/services during the previous 12-month period, with the taxable threshold set at UAH 1 000 000. However, if an entity's volume of taxable supplies in this period was less than UAH 1 000 000, then it can opt to register voluntarily. The above mentioned requirement to register for Ukrainian VAT purposes applies to both resident and non-resident entities. If an entity imports goods to Ukraine in taxable quantities, it is obliged to pay VAT during the Customs clearance process without the need to register as a VAT payer. In addition to taxable entities, VAT law defines the concept of a tax agent (individual responsible for accruing and withholding VAT) and states that, when non-residents provide services that qualify as taxable supplies in Ukraine, VAT should be accrued and remitted to the budget by the Ukrainian customer. For VAT accounting purposes, the so-called "first event" rule is normally used. According to this rule, output and input VAT on domestic sales are assessed in the reporting period in which goods/services are supplied or payment is received. In general, the tax period for VAT purposes is a calendar month. Entities liable to pay VAT must therefore submit tax returns and remit VAT on a monthly basis. According to the effective tax legislation, agricultural producers may apply a special tax regime according to which the VAT liabilities collected by agricultural companies are not payable to the budget but may be used for special business purposes. Starting on 01.01.2015 a brand new system of electronic administration is provided. It includes Electronic registration of tax invoices and automatic control of it by tax authority. Starting from 01.07.2015, VAT-payers are obliged to use special bank accounts for operations with VAT. These accounts are opened automatically in the State Treasury of Ukraine. FRINGE BENEFITS TAX (FBT) Both residents and non-residents are taxed on fringe benefits (treated as payment in kind). The value of the benefits is taxed as the employment income by grossing up for Personal Income Tax (PIT). SOCIAL SECURITY CONTRIBUTIONS Employers are liable to pay Unified Social Security Contributions relating to salaries and benefits paid to their employees.

Ukraine

PKF Worldwide Tax Guide 2015/16 7

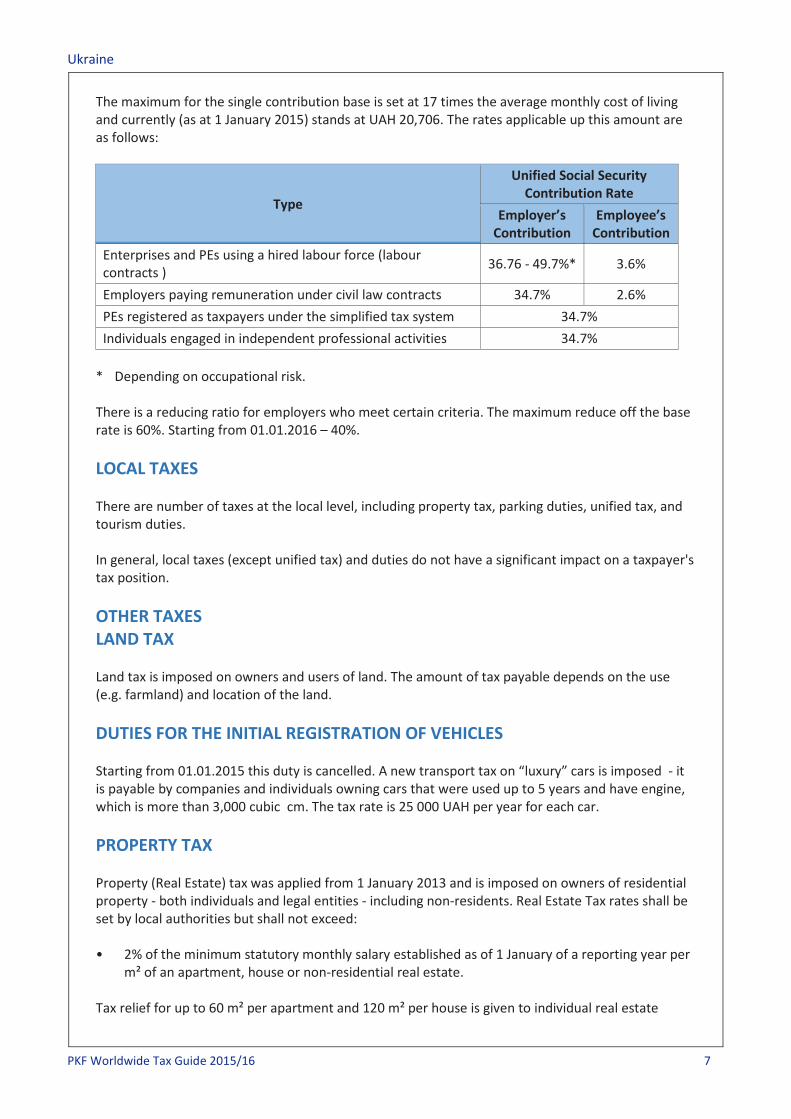

The maximum for the single contribution base is set at 17 times the average monthly cost of living and currently (as at 1 January 2015) stands at UAH 20,706. The rates applicable up this amount are as follows:

Type

Unified Social Security Contribution Rate

Employer’s Contribution

Employee’s Contribution

Enterprises and PEs using a hired labour force (labour contracts ) 36.76 - 49.7%* 3.6%

Employers paying remuneration under civil law contracts 34.7% 2.6% PEs registered as taxpayers under the simplified tax system 34.7% Individuals engaged in independent professional activities 34.7%

* Depending on occupational risk. There is a reducing ratio for employers who meet certain criteria. The maximum reduce off the base rate is 60%. Starting from 01.01.2016 – 40%. LOCAL TAXES There are number of taxes at the local level, including property tax, parking duties, unified tax, and tourism duties. In general, local taxes (except unified tax) and duties do not have a significant impact on a taxpayer's tax position. OTHER TAXES LAND TAX Land tax is imposed on owners and users of land. The amount of tax payable depends on the use (e.g. farmland) and location of the land. DUTIES FOR THE INITIAL REGISTRATION OF VEHICLES Starting from 01.01.2015 this duty is cancelled. A new transport tax on “luxury” cars is imposed - it is payable by companies and individuals owning cars that were used up to 5 years and have engine, which is more than 3,000 cubic cm. The tax rate is 25 000 UAH per year for each car. PROPERTY TAX Property (Real Estate) tax was applied from 1 January 2013 and is imposed on owners of residential property - both individuals and legal entities - including non-residents. Real Estate Tax rates shall be set by local authorities but shall not exceed: • 2% of the minimum statutory monthly salary established as of 1 January of a reporting year per

m² of an apartment, house or non-residential real estate. Tax relief for up to 60 m² per apartment and 120 m² per house is given to individual real estate

Ukraine

PKF Worldwide Tax Guide 2015/16 8

taxpayers if property is used for private purpose only. Starting from 2015, property tax was extended to cover commercial real estate owned by legal entities and individuals. There are statutory exemptions from tax (e.g., production facilities and warehouses of industrial enterprises, buildings and constructions used in agricultural production). The amounts of property tax on commercial real estate paid by the legal entity can be credited/set-off against the corporate profit tax (CPT). SPECIAL PENSION FUND CHARGES The following special charges are payable to the State Pension Fund: • 3% - 5% charge depending on the transfer value of the car (charged only at initial registration); • 1% charge on the acquisition of real estate payable by individuals and legal entities that

purchase real estate; • 7.5% charge on mobile communication services; • 2% charge on purchases of foreign currency (only for cash operations). There are also a number of other business activities that require contributions to be made to the Special Pension Fund. STAMP DUTY Stamp Duty is imposed on certain transactions, including notarisation of contracts and the filing of documents with the courts. In most cases, the amounts involved are nominal, although there are exceptions. Operations carried out at commodity exchanges and sales of real property incurs a stamp duty of 1% EXCISE TAX Excise Tax is payable on cars, alcoholic beverages, tobacco products, beer and petrol and diesel fuel, whether imported or produced domestically. Rates of excise duty are specific. CHARGE ON ENVIRONMENTAL POLLUTION Environmental pollution charges are imposed on any legal entity that discharges contaminants into the environment (air or water) or disposes of waste. The actual rate depends on the type and toxicity of each contaminant. CHARGE FOR SUBSOIL USAGE This charge is not used starting from 01.01.2015. RENTAL PAYMENTS (OIL AND GAS INDUSTRY) The rate of rent payments for oil and gas production is set for oil and condensate based on the

Ukraine

PKF Worldwide Tax Guide 2015/16 9

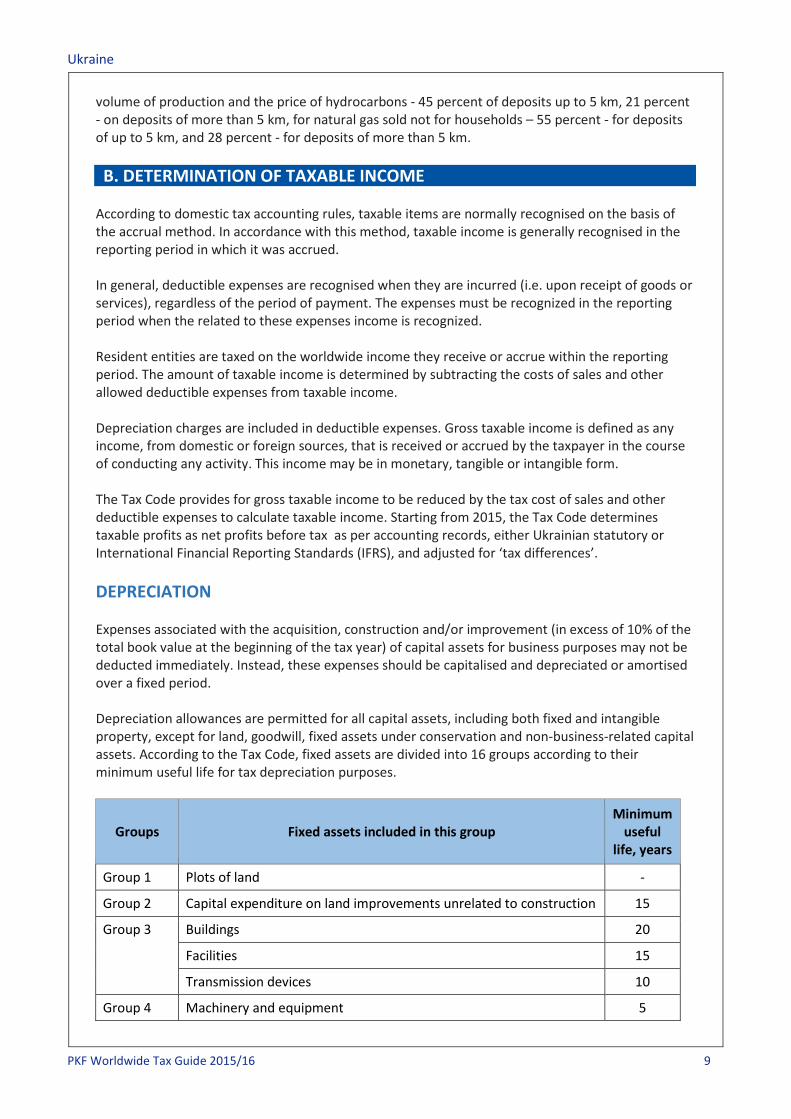

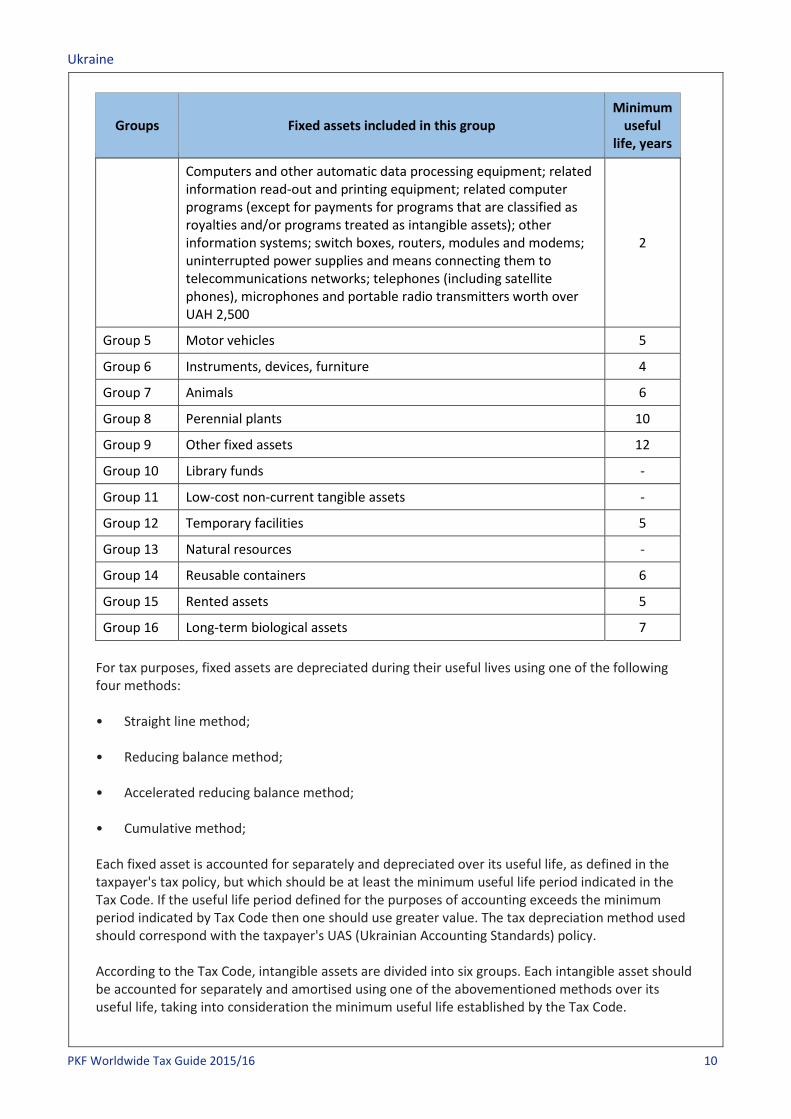

volume of production and the price of hydrocarbons - 45 percent of deposits up to 5 km, 21 percent - on deposits of more than 5 km, for natural gas sold not for households – 55 percent - for deposits of up to 5 km, and 28 percent - for deposits of more than 5 km. B. DETERMINATION OF TAXABLE INCOME According to domestic tax accounting rules, taxable items are normally recognised on the basis of the accrual method. In accordance with this method, taxable income is generally recognised in the reporting period in which it was accrued. In general, deductible expenses are recognised when they are incurred (i.e. upon receipt of goods or services), regardless of the period of payment. The expenses must be recognized in the reporting period when the related to these expenses income is recognized. Resident entities are taxed on the worldwide income they receive or accrue within the reporting period. The amount of taxable income is determined by subtracting the costs of sales and other allowed deductible expenses from taxable income. Depreciation charges are included in deductible expenses. Gross taxable income is defined as any income, from domestic or foreign sources, that is received or accrued by the taxpayer in the course of conducting any activity. This income may be in monetary, tangible or intangible form. The Tax Code provides for gross taxable income to be reduced by the tax cost of sales and other deductible expenses to calculate taxable income. Starting from 2015, the Tax Code determines taxable profits as net profits before tax as per accounting records, either Ukrainian statutory or International Financial Reporting Standards (IFRS), and adjusted for ‘tax differences’. DEPRECIATION Expenses associated with the acquisition, construction and/or improvement (in excess of 10% of the total book value at the beginning of the tax year) of capital assets for business purposes may not be deducted immediately. Instead, these expenses should be capitalised and depreciated or amortised over a fixed period. Depreciation allowances are permitted for all capital assets, including both fixed and intangible property, except for land, goodwill, fixed assets under conservation and non-business-related capital assets. According to the Tax Code, fixed assets are divided into 16 groups according to their minimum useful life for tax depreciation purposes.

Groups Fixed assets included in this group Minimum

useful life, years

Group 1 Plots of land -

Group 2 Capital expenditure on land improvements unrelated to construction 15

Group 3 Buildings 20

Facilities 15

Transmission devices 10

Group 4 Machinery and equipment 5

Ukraine

PKF Worldwide Tax Guide 2015/16 10

Groups Fixed assets included in this group Minimum

useful life, years

Computers and other automatic data processing equipment; related information read-out and printing equipment; related computer programs (except for payments for programs that are classified as royalties and/or programs treated as intangible assets); other information systems; switch boxes, routers, modules and modems; uninterrupted power supplies and means connecting them to telecommunications networks; telephones (including satellite phones), microphones and portable radio transmitters worth over UAH 2,500

2

Group 5 Motor vehicles 5

Group 6 Instruments, devices, furniture 4

Group 7 Animals 6

Group 8 Perennial plants 10

Group 9 Other fixed assets 12

Group 10 Library funds -

Group 11 Low-cost non-current tangible assets -

Group 12 Temporary facilities 5

Group 13 Natural resources -

Group 14 Reusable containers 6

Group 15 Rented assets 5

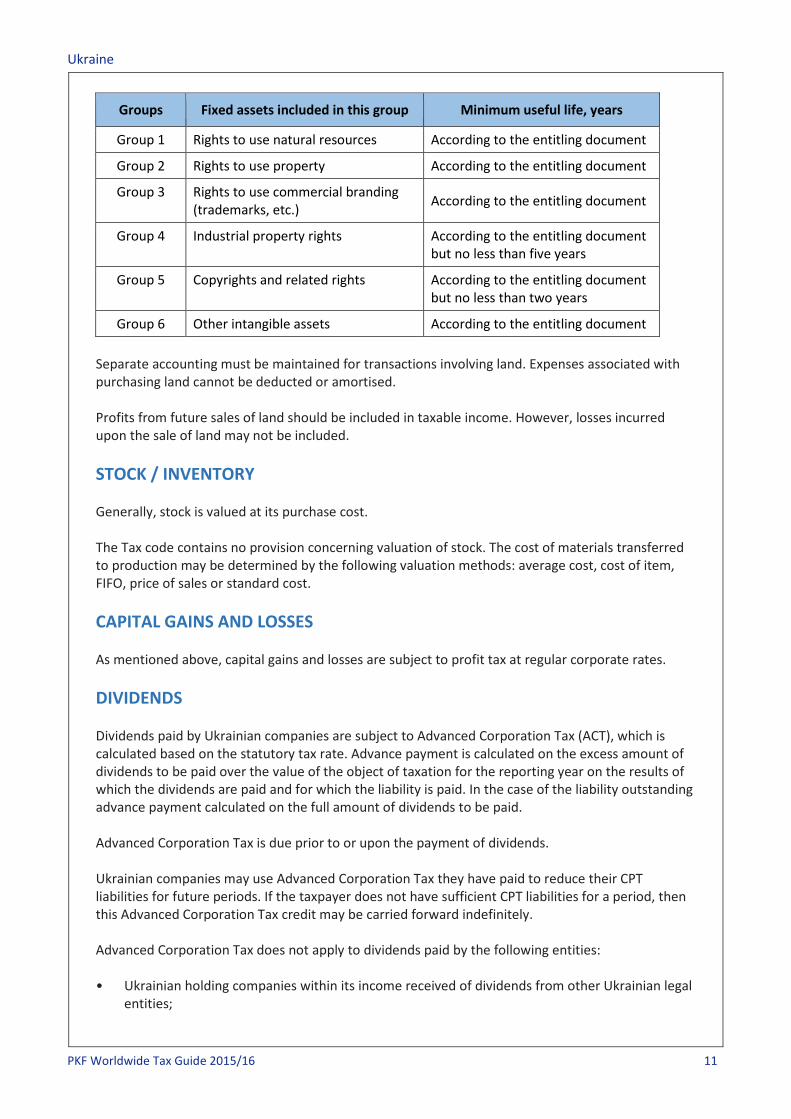

Group 16 Long-term biological assets 7 For tax purposes, fixed assets are depreciated during their useful lives using one of the following four methods: • Straight line method; • Reducing balance method; • Accelerated reducing balance method; • Cumulative method; Each fixed asset is accounted for separately and depreciated over its useful life, as defined in the taxpayer's tax policy, but which should be at least the minimum useful life period indicated in the Tax Code. If the useful life period defined for the purposes of accounting exceeds the minimum period indicated by Tax Code then one should use greater value. The tax depreciation method used should correspond with the taxpayer's UAS (Ukrainian Accounting Standards) policy. According to the Tax Code, intangible assets are divided into six groups. Each intangible asset should be accounted for separately and amortised using one of the abovementioned methods over its useful life, taking into consideration the minimum useful life established by the Tax Code.

Ukraine

PKF Worldwide Tax Guide 2015/16 11

Groups Fixed assets included in this group Minimum useful life, years

Group 1 Rights to use natural resources According to the entitling document

Group 2 Rights to use property According to the entitling document

Group 3 Rights to use commercial branding (trademarks, etc.) According to the entitling document

Group 4 Industrial property rights According to the entitling document but no less than five years

Group 5 Copyrights and related rights According to the entitling document but no less than two years

Group 6 Other intangible assets According to the entitling document Separate accounting must be maintained for transactions involving land. Expenses associated with purchasing land cannot be deducted or amortised. Profits from future sales of land should be included in taxable income. However, losses incurred upon the sale of land may not be included. STOCK / INVENTORY Generally, stock is valued at its purchase cost. The Tax code contains no provision concerning valuation of stock. The cost of materials transferred to production may be determined by the following valuation methods: average cost, cost of item, FIFO, price of sales or standard cost. CAPITAL GAINS AND LOSSES As mentioned above, capital gains and losses are subject to profit tax at regular corporate rates. DIVIDENDS Dividends paid by Ukrainian companies are subject to Advanced Corporation Tax (ACT), which is calculated based on the statutory tax rate. Advance payment is calculated on the excess amount of dividends to be paid over the value of the object of taxation for the reporting year on the results of which the dividends are paid and for which the liability is paid. In the case of the liability outstanding advance payment calculated on the full amount of dividends to be paid. Advanced Corporation Tax is due prior to or upon the payment of dividends. Ukrainian companies may use Advanced Corporation Tax they have paid to reduce their CPT liabilities for future periods. If the taxpayer does not have sufficient CPT liabilities for a period, then this Advanced Corporation Tax credit may be carried forward indefinitely. Advanced Corporation Tax does not apply to dividends paid by the following entities: • Ukrainian holding companies within its income received of dividends from other Ukrainian legal

entities;

Ukraine

PKF Worldwide Tax Guide 2015/16 12

• Investment funds; • Tax payer, whose income exempt from tax under the provisions of this Code in the amount of

income exempted from tax in the period for which the dividends are paid; The dividends paid to individuals are not subject to ACT Interest deductions. INTEREST EXPENSES Any interest expenses incurred by a taxpayer in the course of carrying out business activities are generally deductible. However, interest deductibility limitations do apply to resident taxpayers in the following circumstances: • For the taxpayer, whose amount of debt arising from transactions with related parties - non-

residents exceeds the amount of equity in over 3, 5 times (for financial institutions and companies engaged exclusively in leasing activity, more than 10 times), the financial result before tax increases by the excess of accrued interest for loans, borrowings and other debt over 50 percent of the financial result before tax, finance costs and the amount of depreciation according to the financial statements of the reporting tax period in which the accrual of interest. The exceeding amount can be used for tax purposes (as deduction) in future periods, considered the written above.

LOSSES Taxpayers' tax losses may be carried forward and should be reported in CPT returns for subsequent periods as a separate deductible expense although there are specific limitations for utilising such losses in future tax periods. Tax losses that have accumulated up to 31 December 2011 must be spread evenly over the four period 2012 - 2015 so that only 25% of that loss may be utilised in each year. A special method applies for accounting for losses relating to securities. FOREIGN SOURCED INCOME Foreign sourced income and gains are subject to profit tax at the regular rate except dividends. INCENTIVES • Small enterprises that meet certain criteria will be entitled to a 0% CPT rate from 1 April 2011

until 1 January 2016.

This is where annual income is less than or equal to UAH 3,000,000 and the average salary paid by the company is not less than two times the minimum wage. There are some restrictions depending on type of business activity.

• Small businesses may choose to adopt the Simplified tax system which is designed to reduce the tax and administrative burden on legal entities and private individuals. Taxpayers eligible to use this system, rates of tax and permitted types of business activities are described in the table below:

Ukraine

PKF Worldwide Tax Guide 2015/16 13

Group

Maximum annual

income, UAH

Maximum number of employees

Types of permitted activities*

Rate, %

1 (individuals) 300,000 None

Trading only with private individuals (retail sales and/or rendering of services)

10 Min statutory salary level

2 (individuals) 1,500,000 Max 10

persons

Trading only with private individuals or other simplified taxpayers (production of goods and/or rendering of services except for certain types of operations)

20 Min statutory salary level

3 (individuals

and legal entities)

20,000,000 Not limited Any*

2 % of income (VAT payer)

4 % of income (non-VAT payer)

4 (agricultural producers)

Not limited Not limited

Share of agricultural commodity production in the previous tax (reporting) year equals or exceeds 75 percent**

Depends on the type of land

* The following business activities are prohibited for the simplified tax system:

• Gambling establishments; • Exchange of foreign currencies; • Production, export, import and sale of excisable goods; • Extraction, production and realisation of precious metals and precious gems; • Extraction and realisation of mineral resources; • Financial services except insurance; • Management of enterprises; • Postal and connection services; • Sales of works of art, antiques; and, • Touring events businesses.

Ukraine

PKF Worldwide Tax Guide 2015/16 14

Legal entities and individuals using the Simplified Tax System are exempt from the following taxes:

• Corporate Profits Tax; • Personal Income Tax (on income of individual entrepreneurs only); • Value-Added Tax (except for those opting to be VAT payers); • Property tax • Rent for special use of water (4-th group)

** Impossible to choose the simplified tax system for entities that carry out activities for the

production of excisable goods other than wine grape Individual entrepreneurs who pay the Simplified tax shall pay the Single Social Contribution accrued on their income, but not less than the minimum statutory level of payment (minimum monthly wage multiplied by the effective rate of the charge: 1,218 x 34.7% = UAH 422,65 from 1 January 2015). C. FOREIGN TAX RELIEF A tax credit for foreign taxes paid on foreign-sourced profits or revenues is available subject to a limit of the maximum amount of Ukrainian tax due on the same profits or revenues. Any excess foreign tax credits may not be transferred to future or previous periods. Individuals are allowed to claim a credit for foreign taxes paid on income received abroad, provided there is a double tax treaty between Ukraine and the relevant foreign state. The amount of foreign tax credit is limited to the amount of Ukrainian tax that would arise from the same income in Ukraine (i.e. maximum 15% -17 %). To claim a tax credit, the taxpayer must obtain an official confirmation of the amounts of income subject to tax abroad and the tax paid thereon, issued/verified by the relevant foreign tax authority. D. CORPORATE GROUPS Starting from 1.1.2015 a taxpayer may not apply to pay consolidated CPT. The new edition of Tax Code does not contain such option. The payment should be made on general conditions. E. RELATED PARTY TRANSACTIONS Transfer pricing rules require some transactions to be recognised for tax purposes at fair market values (known as the arm-length principle (ALP)). The tax authorities have power to raise assessments if transactions between the taxpayer and associated companies are not based on fair market values. The Tax code prescribes to prepare a report on transfer pricing on a yearly basis for entities who conducted controlled operations. F. WITHHOLDING TAX Domestic withholding tax rates are set out in the table below (although more favourable treaty rates may apply). In order to benefit from any applicable treaty relief, a non-resident should provide the

Ukraine

PKF Worldwide Tax Guide 2015/16 15

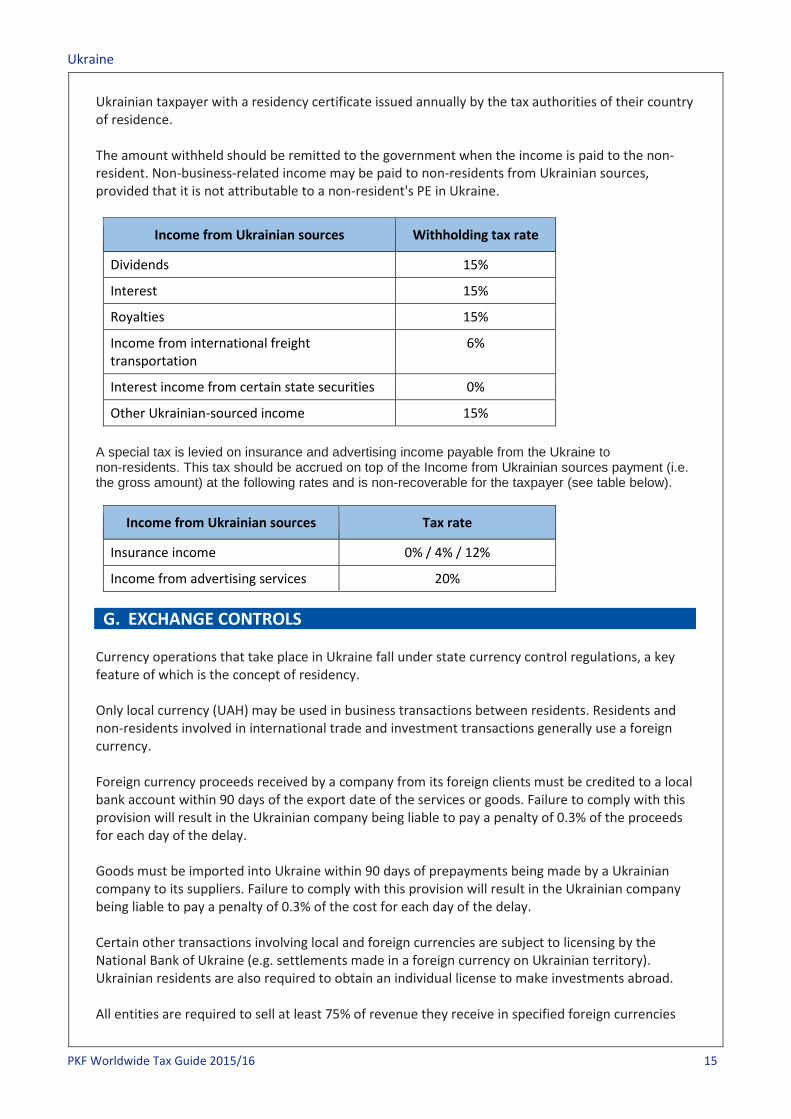

Ukrainian taxpayer with a residency certificate issued annually by the tax authorities of their country of residence. The amount withheld should be remitted to the government when the income is paid to the non-resident. Non-business-related income may be paid to non-residents from Ukrainian sources, provided that it is not attributable to a non-resident's PE in Ukraine.

Income from Ukrainian sources Withholding tax rate

Dividends 15%

Interest 15%

Royalties 15%

Income from international freight transportation

6%

Interest income from certain state securities 0%

Other Ukrainian-sourced income 15% A special tax is levied on insurance and advertising income payable from the Ukraine to non-residents. This tax should be accrued on top of the Income from Ukrainian sources payment (i.e. the gross amount) at the following rates and is non-recoverable for the taxpayer (see table below).

Income from Ukrainian sources Tax rate

Insurance income 0% / 4% / 12%

Income from advertising services 20% G. EXCHANGE CONTROLS Currency operations that take place in Ukraine fall under state currency control regulations, a key feature of which is the concept of residency. Only local currency (UAH) may be used in business transactions between residents. Residents and non-residents involved in international trade and investment transactions generally use a foreign currency. Foreign currency proceeds received by a company from its foreign clients must be credited to a local bank account within 90 days of the export date of the services or goods. Failure to comply with this provision will result in the Ukrainian company being liable to pay a penalty of 0.3% of the proceeds for each day of the delay. Goods must be imported into Ukraine within 90 days of prepayments being made by a Ukrainian company to its suppliers. Failure to comply with this provision will result in the Ukrainian company being liable to pay a penalty of 0.3% of the cost for each day of the delay. Certain other transactions involving local and foreign currencies are subject to licensing by the National Bank of Ukraine (e.g. settlements made in a foreign currency on Ukrainian territory). Ukrainian residents are also required to obtain an individual license to make investments abroad. All entities are required to sell at least 75% of revenue they receive in specified foreign currencies

Ukraine

PKF Worldwide Tax Guide 2015/16 16

(US Dollars, Euros, British Pounds, Swiss Francs and Russian roubles) and precious metals. H. PERSONAL TAX The Personal Income Tax (PIT) base for Ukrainian and foreign nationals depends on their tax residency status. Ukrainian tax residents are subject to PIT on their worldwide income, whereas non-residents are only subject to taxation on the Ukrainian-sourced portion of their income. The Tax Code also provides for a self-recognition procedure, according to which an individual can voluntarily elect to be a Ukrainian tax resident. Domestic laws provide tax residency rules and these provisions may be overruled by the respective provisions of relevant double tax treaties. The following PIT rates are generally applied: • 15% - on the worldwide income of tax residents and the Ukrainian-sourced income of non-

residents up to the monthly threshold of 10 x the minimum wage (UAH 12,180 for beginning of 2015) and 20% above this amount.

• 30% - on income from winnings and prizes. • 0% - on inheritance from immediate family members, income from the first sale of qualifying

residential property and plots of land not exceeding the limit for free land transfers (provided that the property has been in ownership for more than three years)

• 5% - for tax residents on: income from the sale of commercial property; income from the

second and any further sale of residential property within one reporting year; income from the sale of movable property by its owner, other than the first sale of a vehicle; income from the sale of plots of land over of the maximum area for free land transfers; on dividends issued by a resident issuer (except accrued dividends on shares and / or investment certificates) ; and on inheritance paid to non-relatives. The 15% and 17% tax rates apply to these forms of income received by non-residents.

• 20 % - for passive income, including accrued dividends on shares and / or investment

certificates The Tax Code also provides a list of items that must be included in an individual's taxable income. These include, among other things, gifts, insurance contributions and premiums, rental income and fringe benefits. Contributions to unqualified pension plans made on behalf of a taxpayer by another person/an employer will also be included into an individual's taxable income. Income received from the sale of real estate is not taxable if the property is sold only once during a calendar year, regardless of the size of property. Revenue earned from the sale of a house, apartment, part of an apartment, room or cottage (including the plot of land, on which it is located) is: • Not subject to tax if sold only once during a calendar year, and if the property has been owned

for more than three years; or, • Subject to 5% tax, which is levied on the amount received for a second sale of the property

within a reporting year.

Ukraine

PKF Worldwide Tax Guide 2015/16 17

Foreign individuals, who are considered Ukrainian tax residents, are taxed in the same manner and according to the same rules as Ukrainian citizens. MILITARY DUTY In 2015, all types of income, which are subject for PIT, are also subject to Military Duty. The rate of this duty is 1.5% of the taxable income. I. TREATY AND NON-TREATY WITHHOLDING TAX RATE ON DIVIDENDS

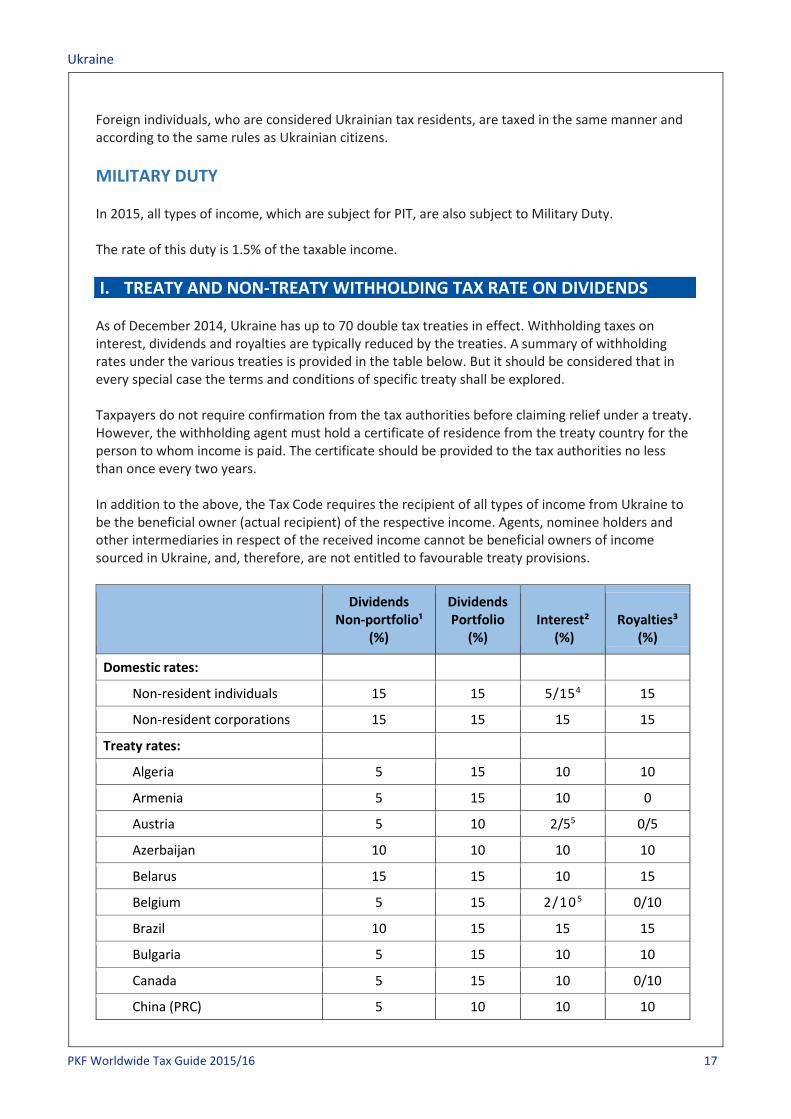

As of December 2014, Ukraine has up to 70 double tax treaties in effect. Withholding taxes on interest, dividends and royalties are typically reduced by the treaties. A summary of withholding rates under the various treaties is provided in the table below. But it should be considered that in every special case the terms and conditions of specific treaty shall be explored. Taxpayers do not require confirmation from the tax authorities before claiming relief under a treaty. However, the withholding agent must hold a certificate of residence from the treaty country for the person to whom income is paid. The certificate should be provided to the tax authorities no less than once every two years. In addition to the above, the Tax Code requires the recipient of all types of income from Ukraine to be the beneficial owner (actual recipient) of the respective income. Agents, nominee holders and other intermediaries in respect of the received income cannot be beneficial owners of income sourced in Ukraine, and, therefore, are not entitled to favourable treaty provisions.

Dividends Non-portfolio¹

(%)

Dividends Portfolio

(%) Interest²

(%) Royalties³

(%)

Domestic rates:

Non-resident individuals 15 15 5/154 15

Non-resident corporations 15 15 15 15

Treaty rates:

Algeria 5 15 10 10

Armenia 5 15 10 0

Austria 5 10 2/55 0/5

Azerbaijan 10 10 10 10

Belarus 15 15 10 15

Belgium 5 15 2/10 5 0/10

Brazil 10 15 15 15

Bulgaria 5 15 10 10

Canada 5 15 10 0/10

China (PRC) 5 10 10 10

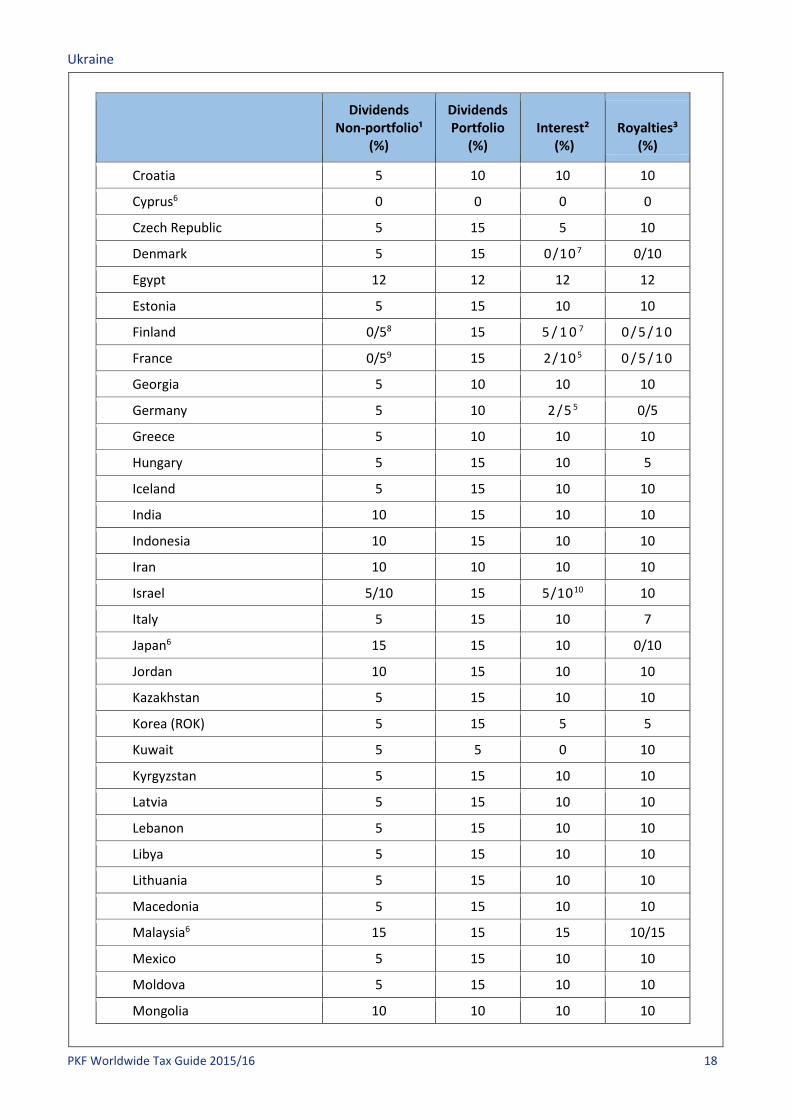

Ukraine

PKF Worldwide Tax Guide 2015/16 18

Dividends Non-portfolio¹

(%)

Dividends Portfolio

(%) Interest²

(%) Royalties³

(%)

Croatia 5 10 10 10

Cyprus6 0 0 0 0

Czech Republic 5 15 5 10

Denmark 5 15 0/107 0/10

Egypt 12 12 12 12

Estonia 5 15 10 10

Finland 0/58 15 5 / 1 0 7 0 / 5 / 1 0

France 0/59 15 2/10 5 0 / 5 / 1 0

Georgia 5 10 10 10

Germany 5 10 2/5 5 0/5

Greece 5 10 10 10

Hungary 5 15 10 5

Iceland 5 15 10 10

India 10 15 10 10

Indonesia 10 15 10 10

Iran 10 10 10 10

Israel 5/10 15 5/1010 10

Italy 5 15 10 7

Japan6 15 15 10 0/10

Jordan 10 15 10 10

Kazakhstan 5 15 10 10

Korea (ROK) 5 15 5 5

Kuwait 5 5 0 10

Kyrgyzstan 5 15 10 10

Latvia 5 15 10 10

Lebanon 5 15 10 10

Libya 5 15 10 10

Lithuania 5 15 10 10

Macedonia 5 15 10 10

Malaysia6 15 15 15 10/15

Mexico 5 15 10 10

Moldova 5 15 10 10

Mongolia 10 10 10 10

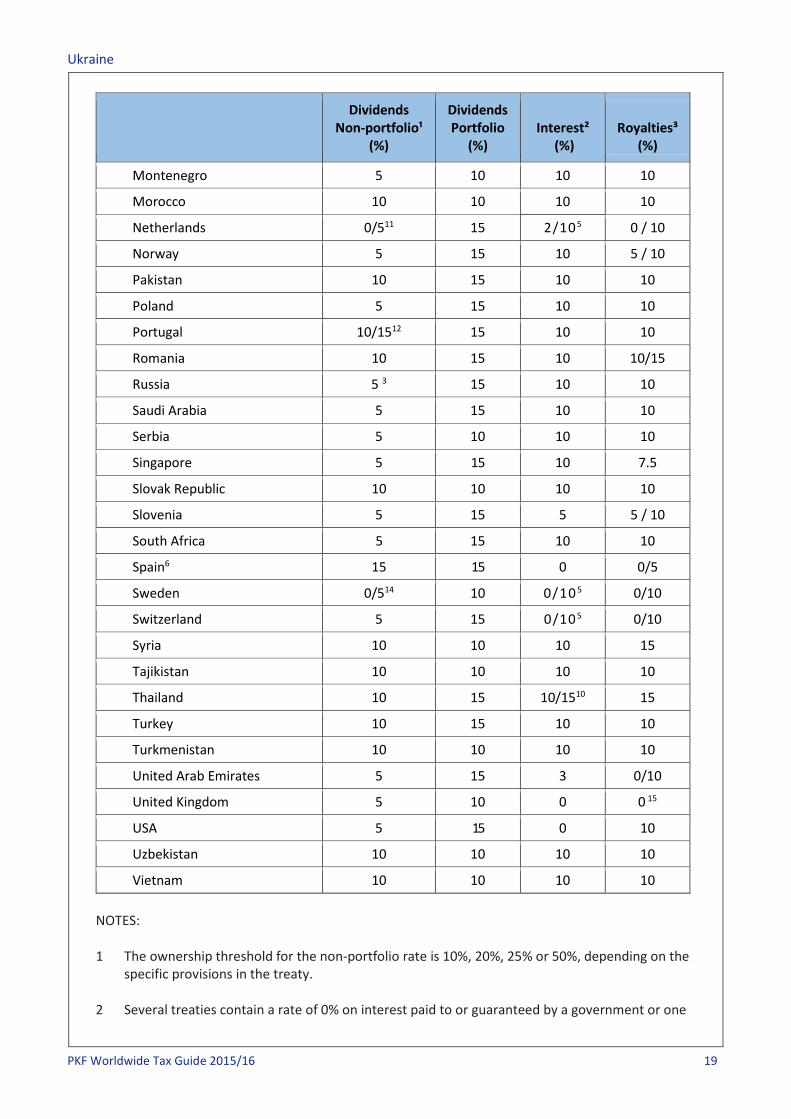

Ukraine

PKF Worldwide Tax Guide 2015/16 19

Dividends Non-portfolio¹

(%)

Dividends Portfolio

(%) Interest²

(%) Royalties³

(%)

Montenegro 5 10 10 10

Morocco 10 10 10 10

Netherlands 0/511 15 2/105 0 / 10

Norway 5 15 10 5 / 10

Pakistan 10 15 10 10

Poland 5 15 10 10

Portugal 10/1512 15 10 10

Romania 10 15 10 10/15

Russia 5 3 15 10 10

Saudi Arabia 5 15 10 10

Serbia 5 10 10 10

Singapore 5 15 10 7.5

Slovak Republic 10 10 10 10

Slovenia 5 15 5 5 / 10

South Africa 5 15 10 10

Spain6 15 15 0 0/5

Sweden 0/514 10 0/10 5 0/10

Switzerland 5 15 0/105 0/10

Syria 10 10 10 15

Tajikistan 10 10 10 10

Thailand 10 15 10/1510 15

Turkey 10 15 10 10

Turkmenistan 10 10 10 10

United Arab Emirates 5 15 3 0/10

United Kingdom 5 10 0 0 15

USA 5 15 0 10

Uzbekistan 10 10 10 10

Vietnam 10 10 10 10 NOTES: 1 The ownership threshold for the non-portfolio rate is 10%, 20%, 25% or 50%, depending on the

specific provisions in the treaty. 2 Several treaties contain a rate of 0% on interest paid to or guaranteed by a government or one

Ukraine

PKF Worldwide Tax Guide 2015/16 20

of its agencies. 3 If more than one rate is shown, this means that the rate will depend on the type of royalties

paid. 4 The lower rate applies to interest on current or deposit bank accounts, certificates of deposit,

contributions to a credit union, and participatory and fixed-yield mortgage certificates. 5 The lower rate applies to interest paid on certain credit sales, and on loans granted by a

financial institution. 6 The treaties with Cyprus, Japan, Malaysia and Spain were entered into by the USSR before it

dissolved. Ukraine will continue to honour these treaties, unless they are superseded. 7 The lower rate applies to interest paid in connection with the sale on credit of any industrial,

commercial or scientific equipment, unless the indebtedness is between associated enterprises. 8 The 0% rate applies if the investor holds at least 50% of the capital of the company paying the

dividends and the capital invested is at least USD 1,000,000; the payer of dividend should not operate in the field of gambling, show business or intermediation business, or auctions.

9 The 0% rate will apply if a French company or companies hold directly or indirectly at least 50%

of the capital of the Ukrainian company, and the aggregate investments exceeds 5 million French francs.

10 The lower rate applies to interest paid on any loan granted by a bank. 11 The 0% rate applies if the investor holds directly at least 50% of the capital of the company the

dividends, and the capital invested is at least USD 300,000. 12 The 10% rate applies if the company receiving the dividend has, for an uninterrupted period of

two years before the dividend is paid, owned at least 25% of the capital stock of the company paying the dividends.

13 The 5% rate applies if the capital invested is at least USD 50,000. 14 The 0% rate applies if the Swedish company holds directly at least 25% of the voting power of

the company paying the dividends, and at least 50% of the Swedish company is held by Swedish residents.

15 The 0% rate applies only if the royalties are taxable in the United Kingdom.