UK Grocery Market Update: BFFFbfff.co.uk/wp-content/uploads/2017/06/BFFF-UK-Grocery...grocery...

44

Simon Wainwright, Head of Retail Insight June 17 UK Grocery Market Update: BFFF Insight from IGD: Retail Analysis and ShopperVista © IGD 2017

-

Upload

hoangduong -

Category

Documents

-

view

219 -

download

4

Transcript of UK Grocery Market Update: BFFFbfff.co.uk/wp-content/uploads/2017/06/BFFF-UK-Grocery...grocery...

Simon Wainwright, Head of Retail Insight June 17

UK Grocery Market Update: BFFF

Insight from IGD: Retail Analysis and ShopperVista

© IGD 2017

IGD – What we do: Delivering insights and best practice

© IGD 2017 Page 3

Contents

© IGD 2017 Page 5

Shopper Confidence & Inflation

Grocery Shifting Dynamics & Channel Implications

Future View

Challenge 1: The economy and the impact on cost of goods

© IGD 2017 Page 6

Lets remind ourselves of the size of UK Grocery…

© IGD 2017 Source: ONS December 2015 Page 7

UK Grocery retail 2016 £179bn

Non-Grocery £13bn

Grocery £166bn

Non-tobacco £146bn

Tobacco £20bn

Non-edible £32bn (ish)

Food and drink £114bn (ish)

Food and drink at foodservice

£48bn (ish)

This division is becoming

increasingly blurred

Frozen Category: £8bn £5.7bn: Retail

370000

380000

390000

400000

410000

420000

430000

440000

450000

460000

470000

480000

UK real GDP value (£millions, quarterly)

The UK economy is in growth

© IGD 2017 Source: ONS September 2016 Page 8

Brexit Impact on GDP and Inflation in 2017 & 2018 but returning to pre-Brexit forecast from 2019

Page 9

0.0

0.5

1.0

1.5

2.0

2.5

2016

2017

2018

2019

2020

2021

Ann

ual c

hang

e (%

)

Real GDP growth

Nov-16 forecast Mar-16 forecast

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2016

2017

2018

2019

2020

2021

Ann

ual c

hang

e (%

)

CPI inflation

Nov-16 forecast Mar-16 forecast

Source: Economic & Fiscal Outlook, Office for Budget Responsibility, March and November 2016

Inflation forecast to accelerate

© IGD 2017 Source: ONS data to February 2017 and CPI forecast by OBR March 2017 Page 10

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2017Q1

2017Q2

2017Q3

2017Q4

2018Q1

2018Q2

2018Q3

2018Q4

2019Q1

2019Q2

2019Q3

2019Q4

Consumer Price Inflation forecast (OBR)

2.7%

2.0% 2.4%

-4

-2

0

2

4

6

8

10

12

14

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Food & Drink catching up with CPI inflation

CPI Food & Grocery

Shoppers anticipate higher prices

© IGD 2017 Source: IGD ShopperVista, 1,000 main shoppers per month; note change in sample frame in Sep-16 Page 11

Grocery Price Expectations – Next 12 months - %

More expensive

Stay the same

Cheaper

87%

10%

3%

55%

36%

10%

81%

17%

2%

Apr’17 Apr’16 Sep’10

Page 12

0.0

0.5

1.0

1.5

2.0

2.5

2016

2017

2018

2019

2020

2021

Ann

ual c

hang

e (%

)

Real GDP growth

Nov-16 forecast Mar-16 forecast

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2016

2017

2018

2019

2020

2021

Ann

ual c

hang

e (%

)

CPI inflation

Nov-16 forecast Mar-16 forecast

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2016

2017

2018

2019

2020

2021

Ann

ual c

hang

e (%

)

Disposable h’hold income

Nov-16 forecast Mar-16 forecast

But it is disposable HH income that will be impacted

Source: Economic & Fiscal Outlook, Office for Budget Responsibility, March and November 2016

But Shoppers showing resilience in turbulent times…for now

© IGD 2017 Source: IGD ShopperVista, personal finance expectations, 1,700 UK shoppers Page 13

Personal Finance Expectations - %

Better off

Worse off

No difference

Jan’11

21%

29%

50%

20%

26%

54%

61%

29%

10%

Apr’17 Apr’16

Challenge 2: grocery share of wallet is declining

© IGD 2017 Page 14

55

56

57

58

59

60

61

62

63

64

65

2007 2008 2009 2010 2011 2012 2013 2014

Average household spending (£ per week) on selected categories at 2014 prices

Grocery spend by household has slowly declined

© IGD 2017 Source: ONS December 2015 Page 15

Food & non-alcoholic drink

0

10

20

30

40

50

60

70

80

90

2007 2008 2009 2010 2011 2012 2013 2014

Average household spending (£ per week) on selected categories at 2014 prices

Transport

Recreation & culture

Food & non-alcohol drinks

Restaurants & hotels

Grocery’s share of wallet is under pressure

© IGD 2017 Source: ONS December 2015 Page 16

Disposable income is being spent elsewhere

© IGD 2017 Source: IGD ShopperVista, October 2016 (Products/services shoppers would spend more on if they had more disposable income), 1,700 UK shoppers Page 17

Holidays 49%

Savings 48%

Home

improvement

31%

Eating out 22%

Cars 18%

Clothes 18%

Treats 17%

Food and grocery 15%

Food-to-go is growing 16 times faster than grocery

© IGD 2017 Source: IGD Research, Grocery market and Food-to-go % value growth 2015 Page 18

Food-to-go +6.5%

Grocery +0.4%

Food-to-go will continue to grow

© IGD 2017 IGD Research, Grocery Retail forecast 2016 - 2021) Page 19

£16.1bn

£21.7 bn

+35% 2016

2021

Contents

© IGD 2017 Page 20

Shopper Confidence & Inflation

Grocery Shifting Dynamics & Channel Implications

Future View

Massive lifestyle changes are underway

© IGD 2017 Page 21

Cities will expand as population increases

Living and retail space will become more of a premium

Life expectancy will continue to rise Technology will continue to impact the everyday

Massive lifestyle changes are underway

© IGD 2017 Page 22

More single person households More dual income households

People will be working longer as retirement age rises

Health consciousness will rise

Shoppers Health concerns are around Sugar. Whilst weight loss is important, Wellbeing is key.

© IGD 2017 Page 23

Manufacturers are turning to natural ingredients, reducing “nasties” through reformulation and looking to reduce pack and portion sizes

© IGD 2017 Page 24

Shopper’s truths becoming Hygiene Factors…

© IGD 2017 Page 25

Value Convenience Quality Health

Shoppers have started to re-interpret Value away from Price towards Quality and Ease

© IGD 2017 Page 26

67%

22%

11%

44%

30%

26%

Agree Neither Disagree

32%

33%

35% 42%

24%

34%

Sometimes I’m tempted to spend a bit more on better QUALITY products

Sometimes I go to the NEAREST store to me even though I know it’s a bit more

expensive

I try to save money grocery shopping but sometimes it takes too much effort so I choose

the EASIER or more expensive option

Sometimes I spend a bit more on products as they are EASIER

to cook / prepare

How loyal are Shoppers today?

© IGD 2017 Source: IGD Shoppervista, October 2016 Page 27

75% Supermarkets are largely

interchangeable

69% Less tied to a single store than previously

0

5

10

15

20

25

30

35

Tesco Sainsbury's Asda Morrisons Co-op Aldi Waitrose Lidl Iceland Other

%

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

-2.3ppts

-1.4ppts +0.4ppts

-1.6ppts

-1.3ppts +3.1ppt +1.2ppts

+2.2ppts

GB market shares

© IGD 2017 Source: Kantar Worldpanel 2010-2017 Page 28

Others

13.0 12.9

8.8

2.9 2.6 1.7

0.6 0.3

-0.8

Lidl Aldi Iceland Waitrose Morrisons Co-op Tesco Sainsbury's Asda

Implied sales growth on last year

Latest quarterly sales growth

© IGD 2017 Source: Kantar Worldpanel, 12 weeks to 26 February 2017 Page 29

27.9

16.5

15.7

10.6

6.3

5.9

5.3

4.6 2.2 5.0

Market shares

Shoppers continue to buy across a variety of formats and channels

© IGD 2017 Page 30

98% 91%

78%

60%

47% 42% 41%

0%

20%

40%

60%

80%

100%

120%

Larger formats Convenience High street discount Food discount Specialist / ethnicstores

Frozen food specialist Online

Monthly claimed usage

4.6 Average number

of channels claimed to be

used in the last month

11.8 Average number

of stores claimed to be

used in the last month

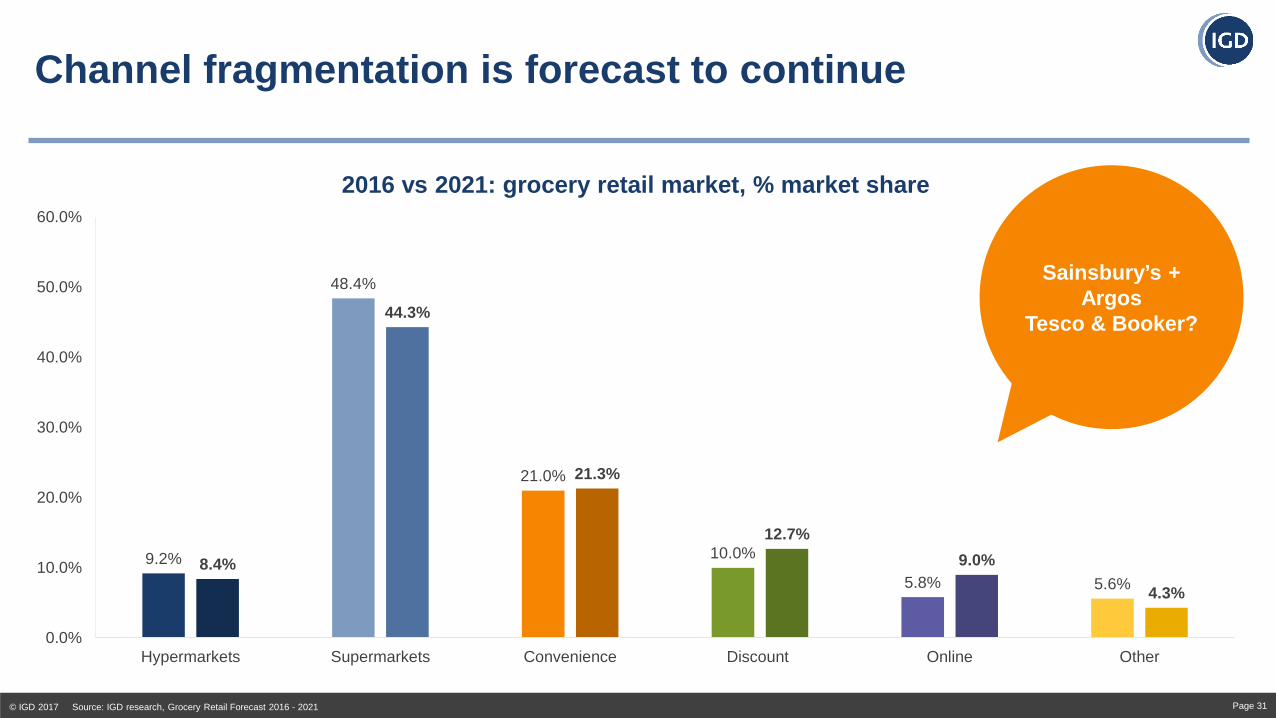

Channel fragmentation is forecast to continue

© IGD 2017 Source: IGD research, Grocery Retail Forecast 2016 - 2021 Page 31

9.2%

48.4%

21.0%

10.0%

5.8% 5.6% 8.4%

44.3%

21.3%

12.7% 9.0%

4.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Hypermarkets Supermarkets Convenience Discount Online Other

2016 vs 2021: grocery retail market, % market share

Sainsbury’s + Argos

Tesco & Booker?

Contents

© IGD 2017 Page 32

Shopper Confidence & Inflation

Grocery Shifting Dynamics & Channel Implications

Future View

Future stores focused more on healthy options

© IGD 2017 Base: 500 shoppers aged 18-25; March’17; Image source: IGD Retail Analysis Page 33

What, if anything, do you think will be different about food and grocery stores in 30 years time?

(among 18-25s)

More HEALTHY options Food will stay FRESHER for longer

MISSION based layouts

More food from around the WORLD More products made by LOCAL companies

1

3

2

Future View

© IGD 2017 Page 34

Increased shopper engagement

Omni-channel, little & often shopping

Mission focused merchandising

Space is being repurposed to expand basket sizes and reflect healthier living…

© IGD 2017 Source: IGD Retail Analysis Page 35

Morrison's, UK

Better catering to missions in-store

© IGD 2017 Page 36 Source: IGD Retail Analysis

Mission focused merchandising

Waitrose, UK

Waitrose, UK

Tesco, UK

Better catering to missions in-store

© IGD 2017 Page 37 Source: IGD Retail Analysis

Mission focused merchandising

Metro, Toronto – chilled and ambient pet food

MAD, Cooperativet, Denmark Tesco, Watford, UK

Food-to-go Accelerating

© IGD 2017 Page 38 Source: IGD Retail Analysis

• Food-to-go grew 16x faster than grocery (% value growth in 2015)

• Retailers are devoting more space to food-to-go and building ranges and merchandising solutions around breakfast, lunch, snack, leisure and drink missions

• M&S Simply Food, Little Waitrose are focusing whole store formats on food-to-go

What’s the initiative?

Asda, Eastlands

Waitrose M&S

Asda, Eastlands

Restaurant Deliveries & Meal-kit Delivery Solutions

© IGD 2017 Page 39

More & more new entrants are coming into this space including other online

specialists and meal solution providers

Gousto (UK) provides ready to prepare meal solutions. Gousto has also experimented with 30 minute deliveries in London.

Deliveroo = Rapid UK expansion

Moving into Lunch deliveries alongside Dinner

Try before you buy and self-dispense

© IGD 2017 Page 40 Source: IGD Retail Analysis

• Metro in Dusseldorf provides an in-store bar where wine shoppers can try a selection of wines before they buy

• As well as driving excitement and theatre in-store, the ability to sample wine lowers the risk of buying the wrong wine for shoppers, making Metro a destination for wine

• Self dispense is a well-established means of adding a level of shopper engagement to specific categories, often positioned as a mechanic for providing better value and choice around purchase quantities

What’s the initiative?

Olive oil – Auchan, France

Wine – Tesco, Czech Republic Metro, Dusseldorf

A great way to engage shoppers and drive penetration for brands

Increased shopper

engagement

Investment in hospitality

© IGD 2017 Page 41

Increased shopper

engagement

Fulfilling anytime, anywhere purchasing demands, simply

© IGD 2017 Page 42

Omni-Channel

Brand led initiatives launched to grow habitual loyalty and repeat purchase

© IGD 2017 Page 43

Omni-Channel

Insights & Implications

© IGD 2017 Page 44

Higher costs – but impact for all. Shoppers will trade up for Quality 1

2

3

4

Shopping more often and on the go – how can Frozen compete?

Retail’s Future: Mission Focussed, Engaging & Omni-channel

Food to Go & Home Delivery are growth areas that challenge the current Retail model – what role for Frozen?