Uk approach – Matching demand to inflexible generation

23

Task XIX International Meeting Wednesday 21 Oct 2009 Shanti Majithia Energy and Climate Strategy Manager Transmission, National Grid UK Is DSM the answer ?

-

Upload

iea-dsm-energy-technology-initiative -

Category

Presentations & Public Speaking

-

view

108 -

download

1

Transcript of Uk approach – Matching demand to inflexible generation

Task XIX International Meeting Wednesday 21 Oct 2009

Shanti MajithiaEnergy and Climate Strategy ManagerTransmission, National Grid UK

Is DSM the answer ?

2

overview

Introduction to National Grid

The drivers for change

The generation mix – capacity at any time

NG 2020 consultation

Developments in Electricity Generation and Demand

Reserve and Operating Margin Short term reserve, operating margin at peak demands, and operating at minimum demands

Network Operation Physical operation

Balancing Services Development

Transmission technologies & system issues

Demand Side Management and technological links

Demand side balancing opportunities

What is needed in the future of new generation technology?

Conclusions & how could it affect the future?

3

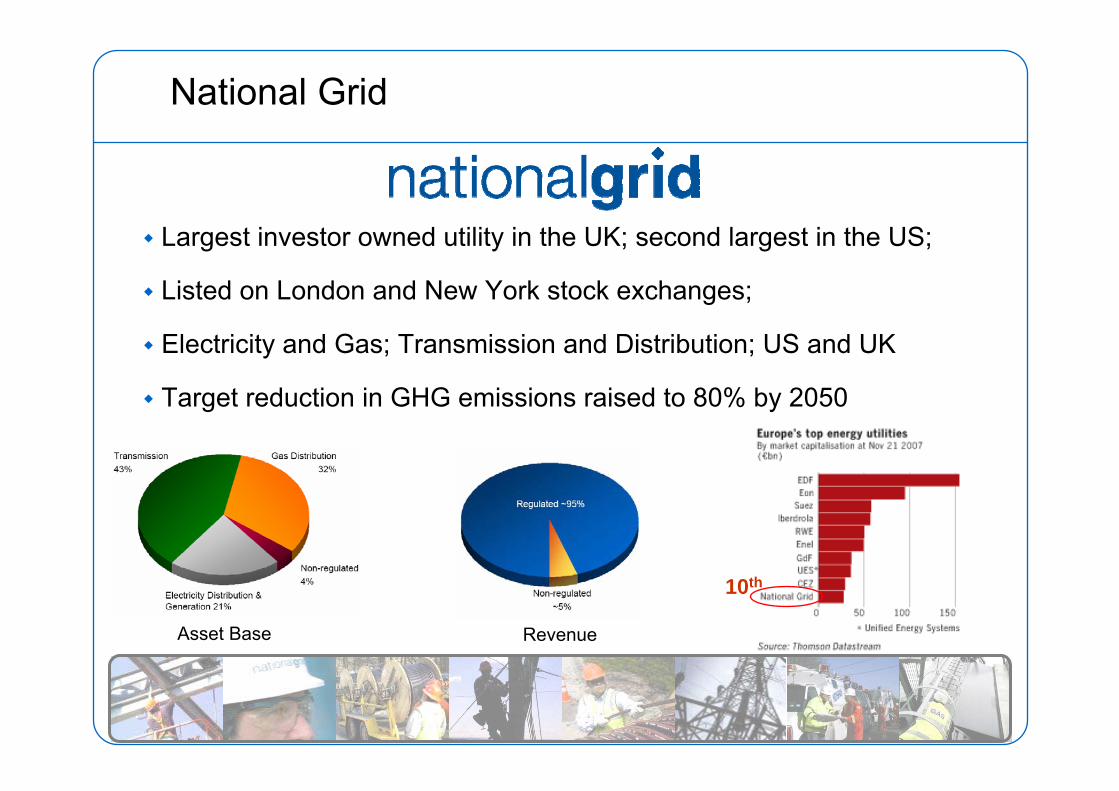

National Grid

Largest investor owned utility in the UK; second largest in the US;

Listed on London and New York stock exchanges;

Electricity and Gas; Transmission and Distribution; US and UK

Target reduction in GHG emissions raised to 80% by 2050

Asset Base Revenue

10th

4

Our Business

50:50

Transmission

UK US

Distribution

Electricity Gas

5

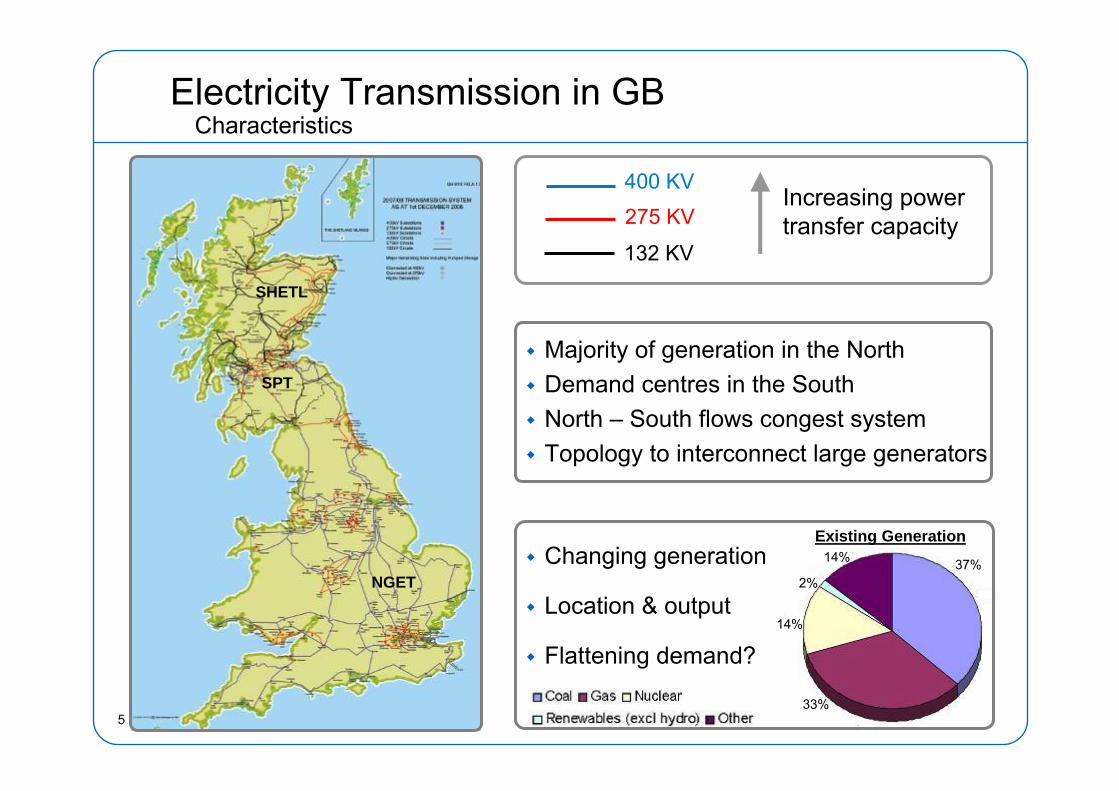

Electricity Transmission in GB

SHETL

SPT

NGET

132 KV

275 KV400 KV

Increasing power transfer capacity

Majority of generation in the NorthDemand centres in the SouthNorth – South flows congest systemTopology to interconnect large generators

Characteristics

14% 37%

14%

2%

33%

Existing GenerationChanging generation

Location & output

Flattening demand?

6

Balancing the Network

This won’t work in 2020/30 because generation is intermittent or inflexible

In 2009…

Demand is a given

Second by second balancing achieved by flexing generation

In 2020/2030…

Dynamic demandSmart metersStorageFlexing generation

Heat and Transport kicks in

29500

30500

31500

32500

33500

34500

35500

15:30 15:45 16:00 16:15 16:30 16:45 17:00 17:15 17:30 17:45 18:00 18:15 18:30 18:45 19:00 19:15 19:30Time

49.8

50

50.2

50.4

50.6

50.8

51

7

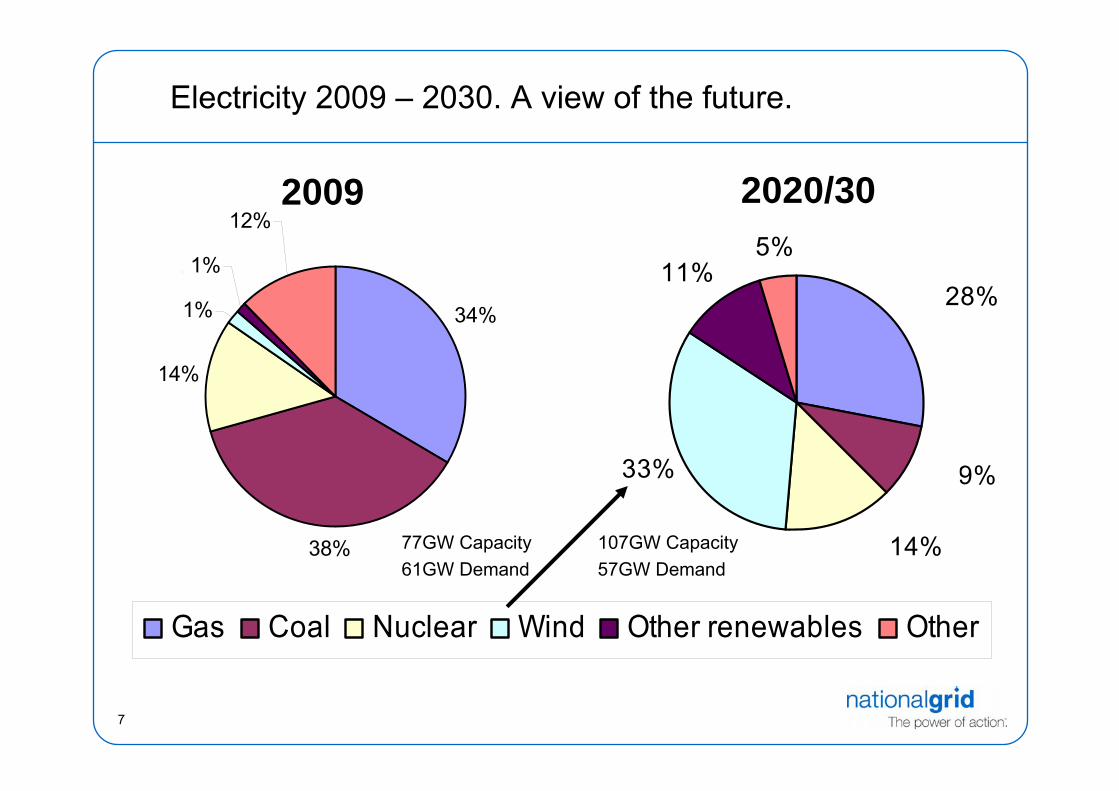

Electricity 2009 – 2030. A view of the future.

25.6, 34%

28.4, 38%

11, 14%

1.1, 1%

1.1, 1%

9.4, 12%

Gas Coal Nuclear Wind Other renewables Other

2009

77GW Capacity61GW Demand

30, 28%

10, 9%

15, 14%

35, 33%

12, 11%5, 5%

2020/30

107GW Capacity57GW Demand

34%

8

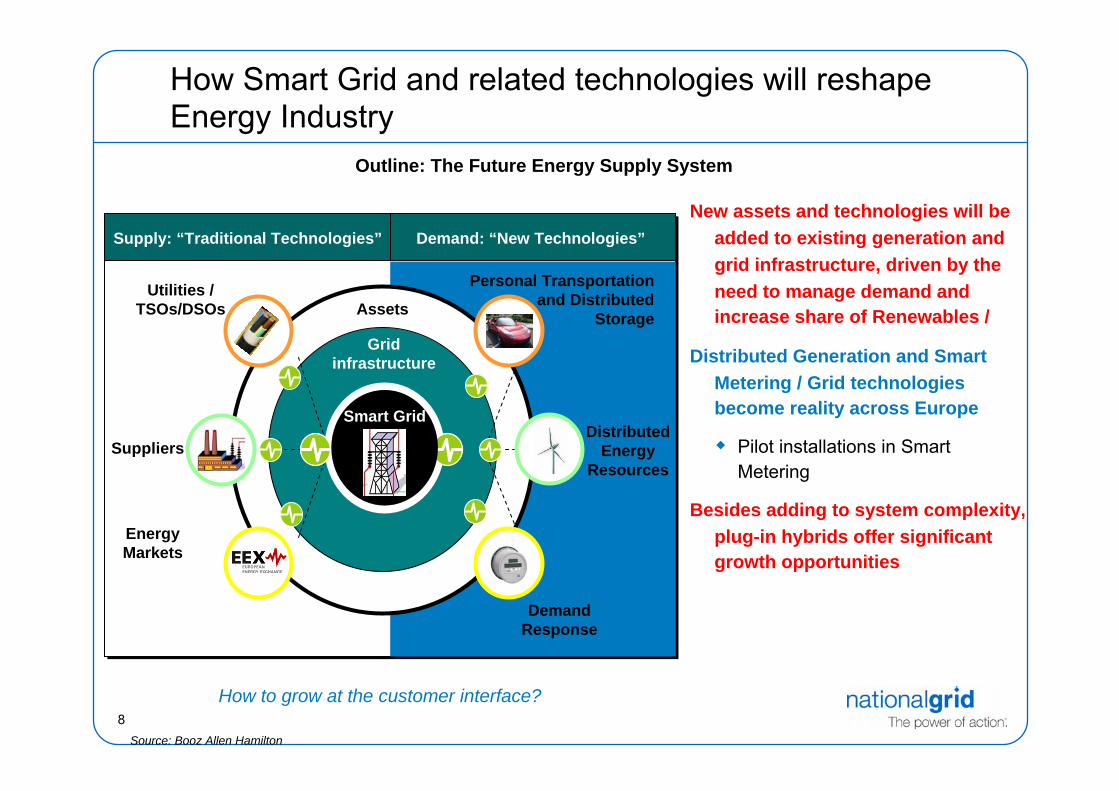

How Smart Grid and related technologies will reshape Energy Industry

How to grow at the customer interface?

Outline: The Future Energy Supply System

Source: Booz Allen Hamilton

Supply: “Traditional Technologies”Supply: “Traditional Technologies” Demand: “New Technologies”Demand: “New Technologies”

Gridinfrastructure

Assets

Personal Transportationand Distributed

Storage

DistributedEnergy

Resources

EnergyMarkets

Suppliers

Utilities /TSOs/DSOs

DemandResponse

Smart Grid

New assets and technologies will be added to existing generation and grid infrastructure, driven by the need to manage demand and increase share of Renewables /

Distributed Generation and Smart Metering / Grid technologies become reality across Europe

Pilot installations in Smart Metering

Besides adding to system complexity, plug-in hybrids offer significant growth opportunities

9

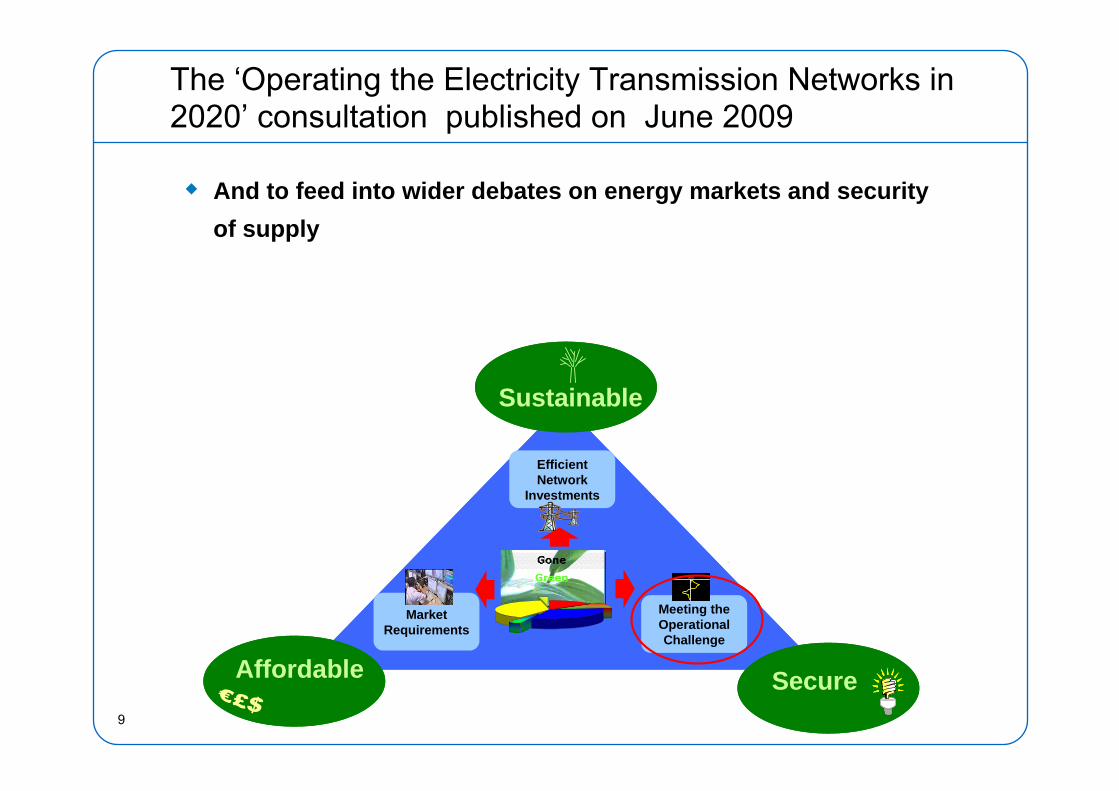

SecureAffordable

Sustainable

Efficient Network

Investments

Market Requirements

Meeting the Operational Challenge

50

50.00

SecureAffordable

Sustainable

Efficient Network

Investments

Market Requirements

Meeting the Operational Challenge

50

50.00

50.00

The ‘Operating the Electricity Transmission Networks in 2020’ consultation published on June 2009

And to feed into wider debates on energy markets and security of supply

10

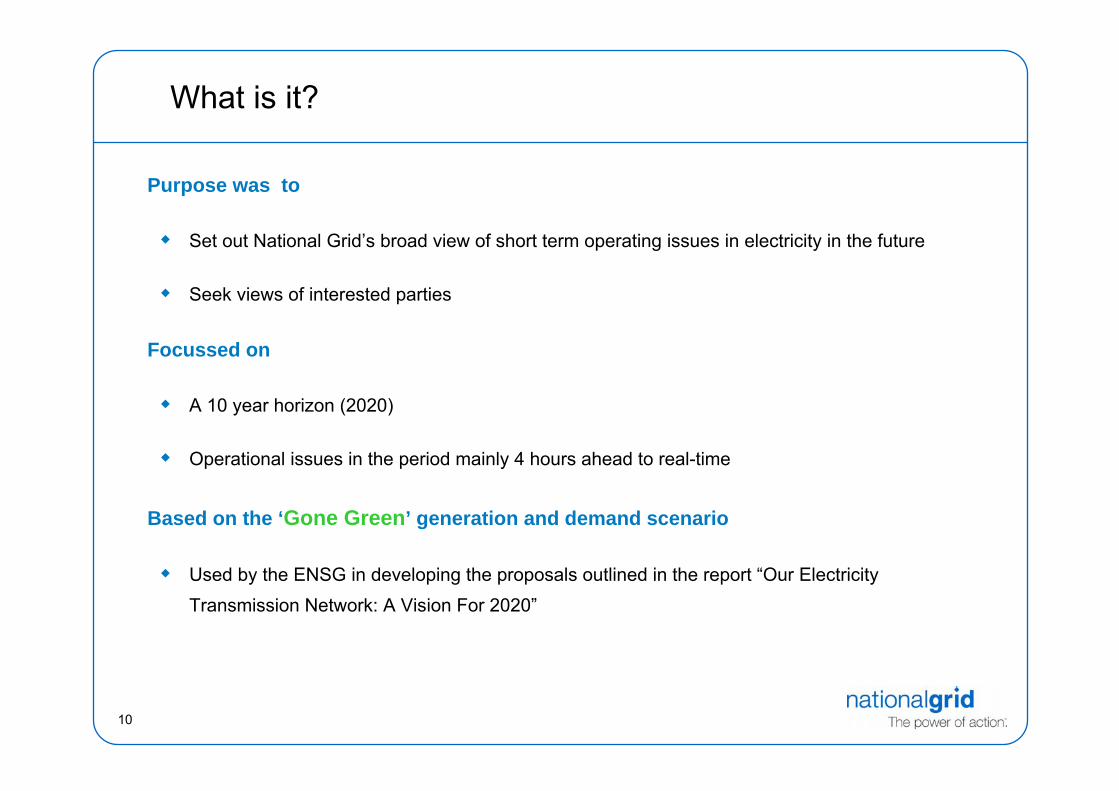

What is it?

Purpose was to

Set out National Grid’s broad view of short term operating issues in electricity in the future

Seek views of interested parties

Focussed on

A 10 year horizon (2020)

Operational issues in the period mainly 4 hours ahead to real-time

Based on the ‘Gone Green’ generation and demand scenario

Used by the ENSG in developing the proposals outlined in the report “Our Electricity Transmission Network: A Vision For 2020”

11

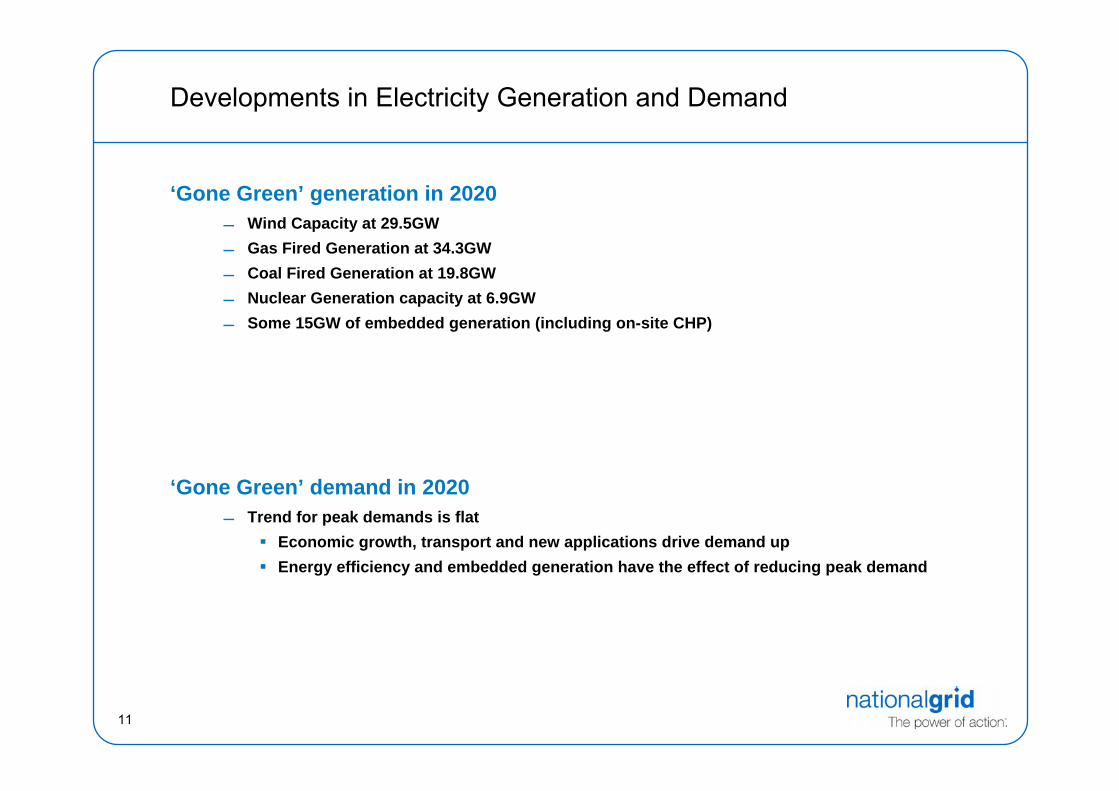

Developments in Electricity Generation and Demand

‘Gone Green’ generation in 2020 Wind Capacity at 29.5GW Gas Fired Generation at 34.3GW Coal Fired Generation at 19.8GW Nuclear Generation capacity at 6.9GW Some 15GW of embedded generation (including on-site CHP)

‘Gone Green’ demand in 2020 Trend for peak demands is flat

Economic growth, transport and new applications drive demand upEnergy efficiency and embedded generation have the effect of reducing peak demand

12

Developments in Electricity Generation and Demand

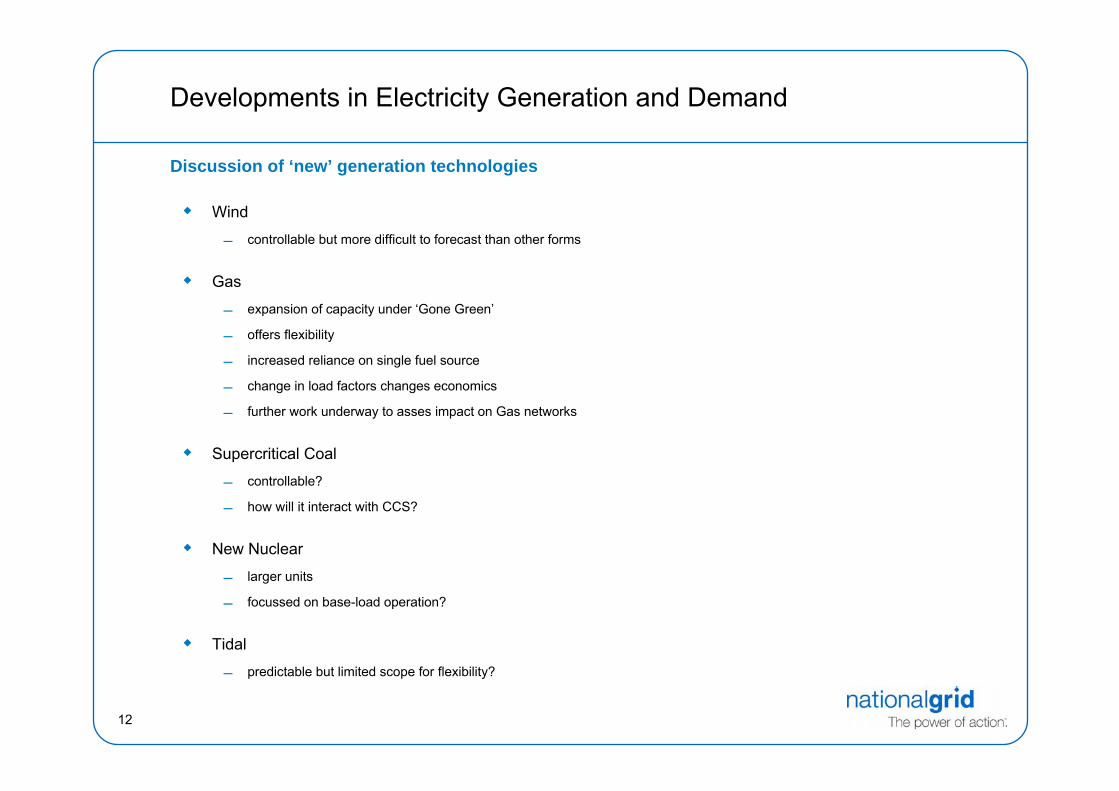

Discussion of ‘new’ generation technologies

Wind

controllable but more difficult to forecast than other forms

Gas

expansion of capacity under ‘Gone Green’

offers flexibility

increased reliance on single fuel source

change in load factors changes economics

further work underway to asses impact on Gas networks

Supercritical Coal

controllable?

how will it interact with CCS?

New Nuclear

larger units

focussed on base-load operation?

Tidal

predictable but limited scope for flexibility?

13

Developments in Electricity Generation and Demand

Discussion of ‘new’ demand side technologies

Overall trend ‘Gone Green’ trend is essentially flat for net peak demand

‘SMART’ the smart meter active demand management Smart Grid

Electric Vehicles charging period

Embedded or Distributed Generation

14

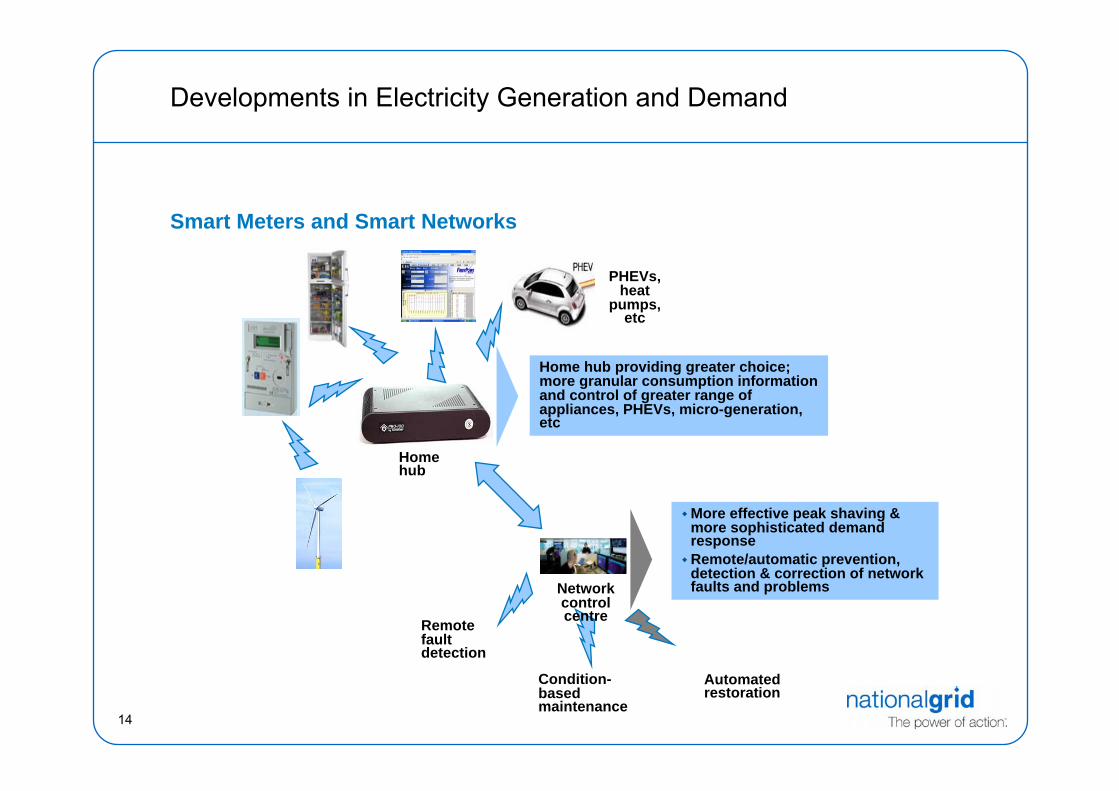

Developments in Electricity Generation and Demand

Smart Meters and Smart Networks

Home hub

Condition-based maintenance

Remote fault detection

Automated restoration

Home hub providing greater choice; more granular consumption information and control of greater range of appliances, PHEVs, micro-generation, etc

More effective peak shaving & more sophisticated demand responseRemote/automatic prevention, detection & correction of network faults and problems

PHEVs, heat

pumps, etc

Network control centre

15

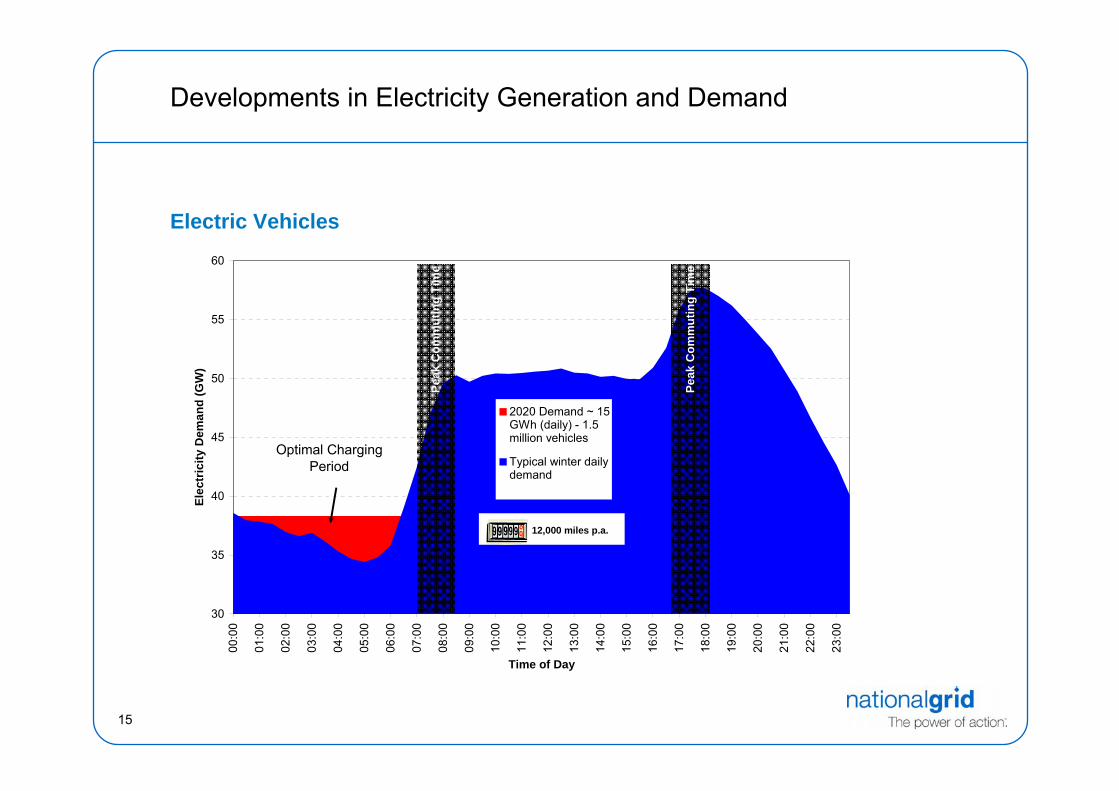

Developments in Electricity Generation and Demand

30

35

40

45

50

55

60

00:0

0

01:0

0

02:0

0

03:0

0

04:0

0

05:0

0

06:0

0

07:0

0

08:0

0

09:0

0

10:0

0

11:0

0

12:0

0

13:0

0

14:0

0

15:0

0

16:0

0

17:0

0

18:0

0

19:0

0

20:0

0

21:0

0

22:0

0

23:0

0

Time of Day

Elec

tric

ity D

eman

d (G

W)

2020 Demand ~ 15GWh (daily) - 1.5million vehicles

Typical winter dailydemand

Peak

Com

mut

ing

Tim

e

12,000 miles p.a.

Peak

Com

mut

ing

Tim

e

Optimal Charging Period

Electric Vehicles

Balancing Services Development

17

Overview of Balancing Services (1)

Frequency Response

Mandatory Frequency Response

Commercial Frequency Response: FFR, FCDM

Reserve Services

BM Start-Up, Fast Reserve, Short Term Operating Reserve

Reactive Power

Obligatory Reactive Power, Enhanced Reactive Power

System Security

Constraints Management, Maximum Generation, Black Start, Intertrips, SO to SO

Trading

18

Reserve Service

BM Start-Up

Short Term Operating Reserve

Fast Reserve

Demand Management

19

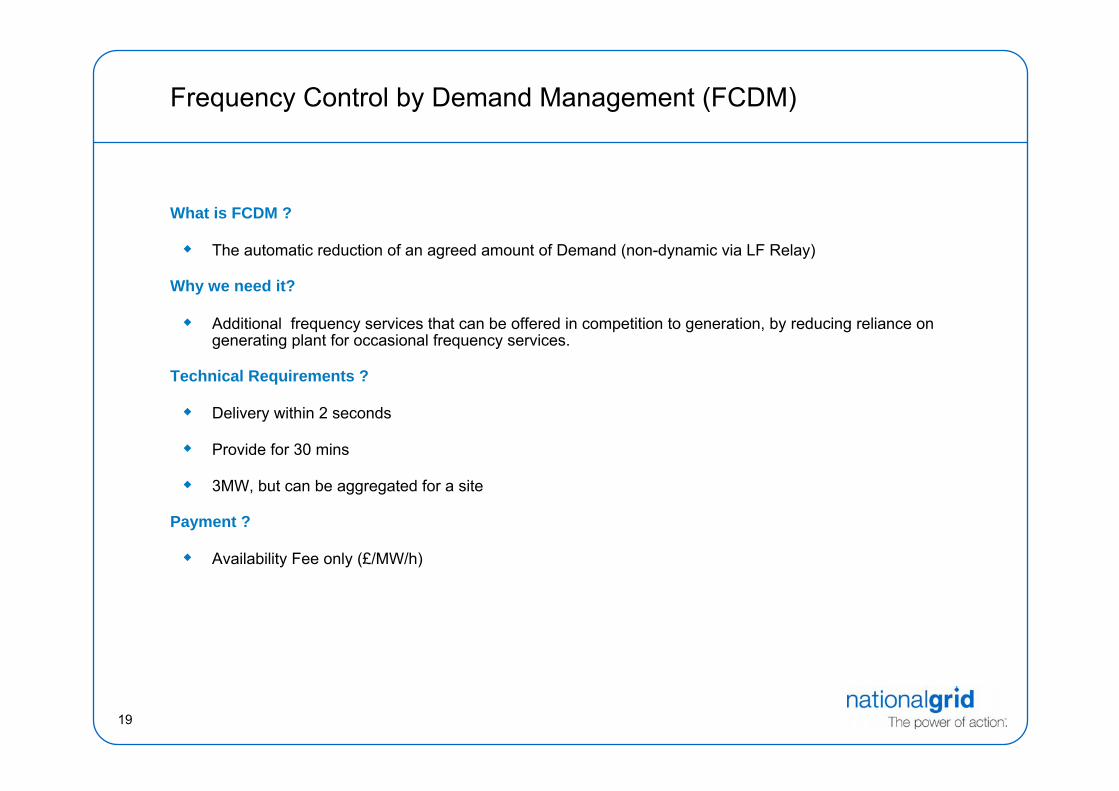

Frequency Control by Demand Management (FCDM)

What is FCDM ?

The automatic reduction of an agreed amount of Demand (non-dynamic via LF Relay)

Why we need it?

Additional frequency services that can be offered in competition to generation, by reducing reliance on generating plant for occasional frequency services.

Technical Requirements ?

Delivery within 2 seconds

Provide for 30 mins

3MW, but can be aggregated for a site

Payment ?

Availability Fee only (£/MW/h)

20

Balancing Services Development

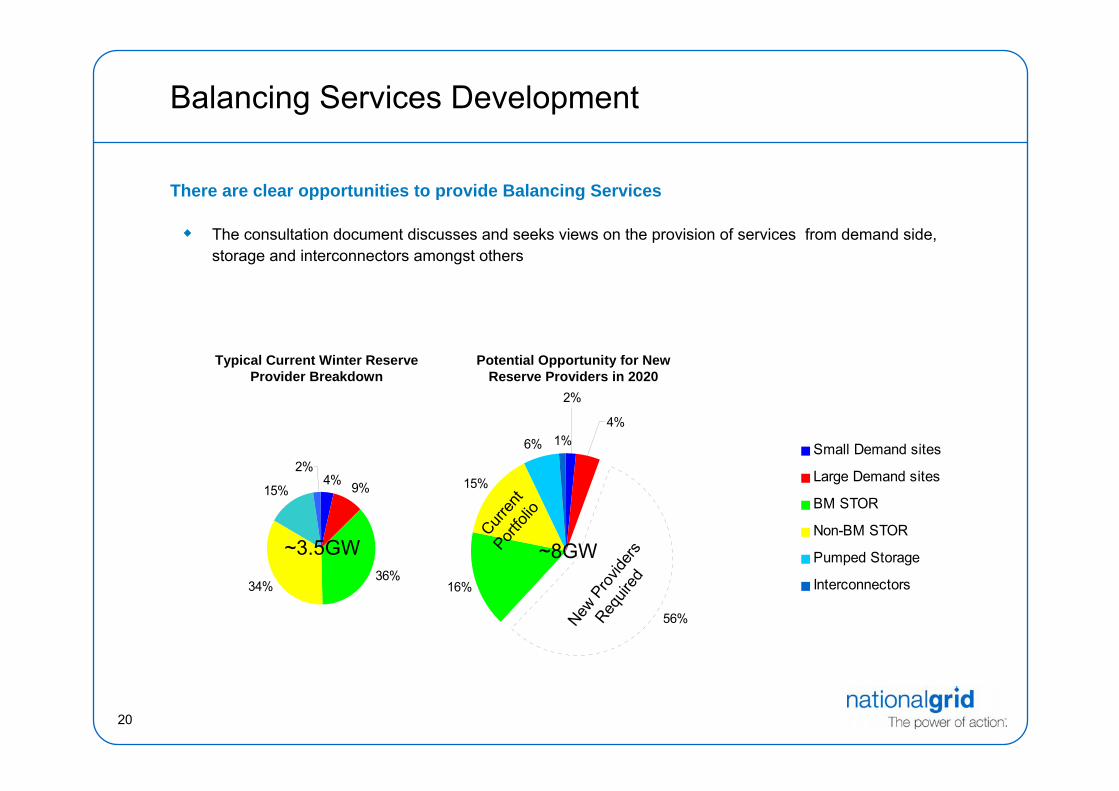

There are clear opportunities to provide Balancing Services

The consultation document discusses and seeks views on the provision of services from demand side, storage and interconnectors amongst others

Small Demand sites

Large Demand sites

BM STOR

Non-BM STOR

Pumped Storage

Interconnectors

56%

16%

15%

6% 1%

2%

4%

Small Demand sites

Typical Current Winter Reserve Provider Breakdown

Potential Opportunity for New Reserve Providers in 2020

4% 9%

36%34%

15%

2%

~3.5GW ~8GW

Curren

t Port

folio

New P

rovid

ers

Requir

ed

21

Balancing Services Development

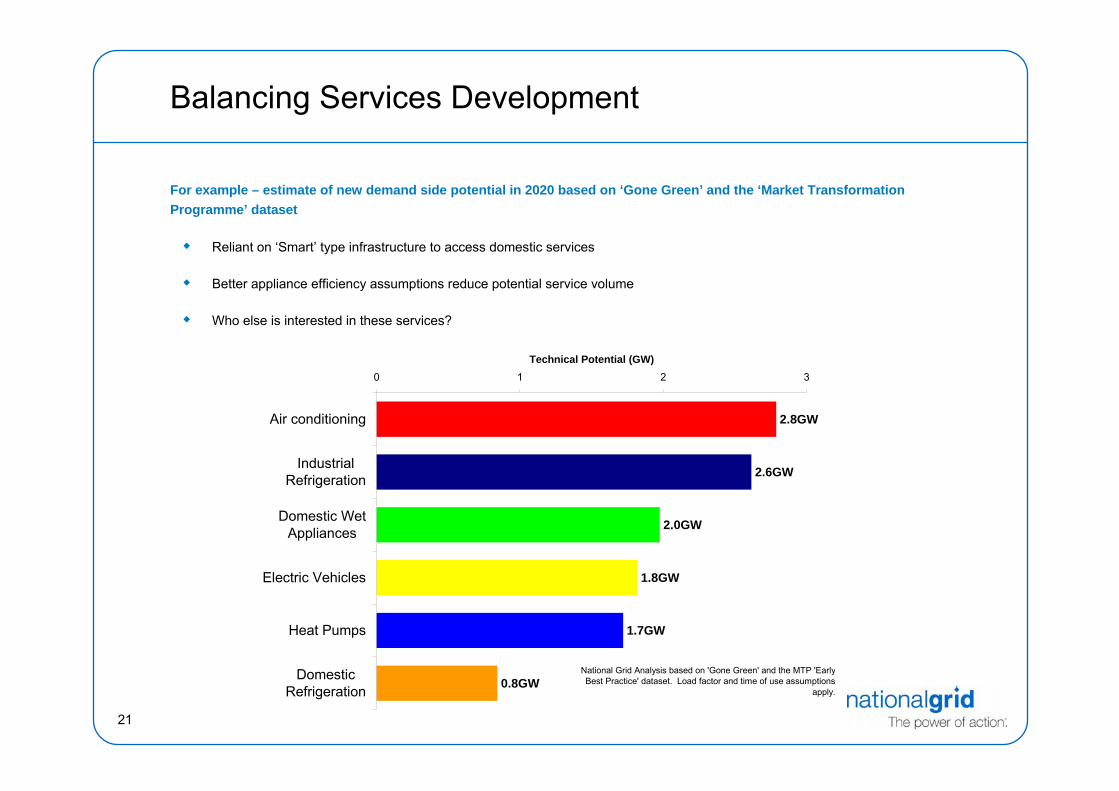

For example – estimate of new demand side potential in 2020 based on ‘Gone Green’ and the ‘Market Transformation Programme’ dataset

Reliant on ‘Smart’ type infrastructure to access domestic services

Better appliance efficiency assumptions reduce potential service volume

Who else is interested in these services?

2.8GW

0.8GW

2.0GW

2.6GW

1.7GW

1.8GW

0 1 2 3

DomesticRefrigeration

Heat Pumps

Electric Vehicles

Domestic WetAppliances

IndustrialRefrigeration

Air conditioning

Technical Potential (GW)

National Grid Analysis based on 'Gone Green' and the MTP 'EarlyBest Practice' dataset. Load factor and time of use assumptions

apply.

22

How will it work -- Demand Response

Freezers & fridges Demand side future balancing opportunities

Defer or advance cooling

Seconds and minutes

Road Transport

Charging millions of batteries or producing H2 on the forecourt when it suits the system

GWs of response from a national battery

Seconds, minutes & hours

Heat pumps

Defer or advance heating (operation of electric pumps)

Seconds, minutes and 10s of minutes

Overseas large hydro (replace their demand)

Minutes, hours, days and months

Access to 50TWH storage

23

In Summary

Massive challenge in a Era of unprecedented change

Great opportunity for technological innovation

Networks will play a key part in delivering solutions

Potential for Demand Side

– but expectations need to be realistic and should perhaps focus more on wholesale market participation;

Recognition of Investment Challenge for new generation; and

Need for strong incentive to balance the system.