©UFS L05068U1R(exp0606)(FL)MLIC-LD Disability Income : Helping You Build Financial Freedom.

32

©UFS L05068U1R(exp0606)(FL)MLIC-LD Disability Income : Helping You Build Financial Freedom

-

date post

19-Dec-2015 -

Category

Documents

-

view

220 -

download

1

Transcript of ©UFS L05068U1R(exp0606)(FL)MLIC-LD Disability Income : Helping You Build Financial Freedom.

©UFS

L05068U1R(exp0606)(FL)MLIC-LD

Disability Income :Helping You Build Financial Freedom

2

What We’re Going to Cover Today

• Why do your clients need DI?

• How do you benefit from selling disability insurance?

• Who makes up the individual DI market?

• What disability products does MetLife offer?

• What are the limitations of group LTD plans?

• How is the MultiLife program beneficial to you and your clients?

3

Why DI?

Why Sell Disability

Income Insurance?

4

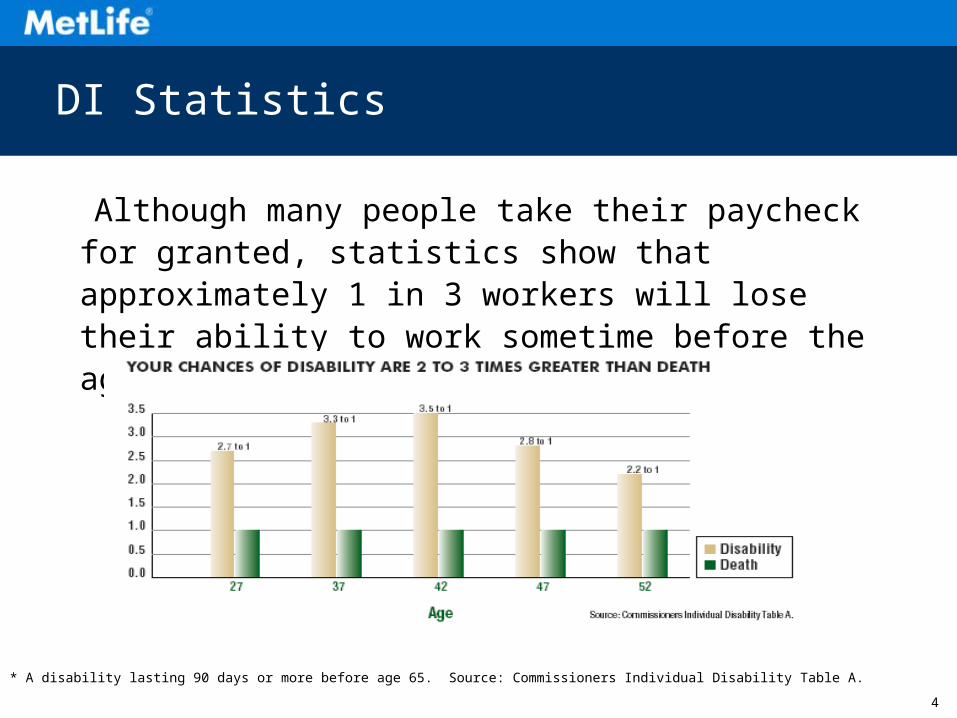

DI Statistics

Although many people take their paycheck for granted, statistics show that approximately 1 in 3 workers will lose their ability to work sometime before the age of 65*

* A disability lasting 90 days or more before age 65. Source: Commissioners Individual Disability Table A.

5

How Would Your Clients Replace Their Lost Income?

Savings

One year of disability can wipe out 10 years of savings.1

Borrow

What bank would lend them money if they were disabled and unemployed?

Social Security

To qualify, your client’s disability must be expected to last at least 12 months or end in death, in addition to other requirements.2

Other Income

Could they maintain their standard of living without placing additional strain on themselves and their family?

1 The Life Underwriter Training Council. “Fundamentals of Financial Services Course.” Volume 6, 1997 edition. 2 You also must be unable to engage in any occupation.

Other Financial Means

6

Competitive Advantages

• The ability to offer a valuable benefit to your client’s protection portfolio

• Competitive rates and a broad range of availability to most occupations

• Strong compensation potential

• Local support and expertise from a MetLife IDI Sales Representative

What’s In It For You?

7

MetLife’s Advantages

• More than 80 years in the DI industry with 130,000 DI policyholders and annual premium exceeding $131

million.1

• Customer service for all DI policyholders and claimants via toll free number, allowing direct access to a policy administrative or claim representative.

• The MetLife claim system provides prompt and on-time payment of claims including electronic funds transfer of benefit payments into a claimant’s checking or savings account.

Strength of MetLife

1 2000 LIMRA International Report

8

Disability Income

The Individual Sale

9

DI Eligibility

• Ages 18 to 59

• Earns over $18,000 annually

• Has a history of good health

• Works at least 30 hours per week

• Does not have excessive unearned income or net worth

The Individual DI Market

10

What we have to offer...

A Sample of DI Products

11

OMNI Advantage

• Non-cancelable and guaranteed renewable to age 65

• Total disability benefit

• Presumptive disability provision with elimination period

waiver

• No mental/nervous disorder limitation

• No relation to earnings provision

• No mandatory rehabilitation

OMNI Advantage* Base Contract

* Not available in CA, VT or OR

12

OMNI Essential

• Guaranteed renewable to age 65, or for five policy years if

later

• Total disability benefit

• Presumptive disability provision with elimination period waiver

• Mental/nervous disorder limitation

• No relation to earnings provision

• No mandatory rehabilitation

OMNI Essential* Base Contract

* Not available in CA, VT or OR

13

Salary Saver

• Non-cancelable, guaranteed renewable to age 65

• Total disability benefit

• Presumptive disability provision with elimination

period waiver

• Mental/nervous disorder limitation

• Benefit flexibility

Salary Saver Base Contract*

* For California Only

14

OMNI Advantage

• Residual Disability Rider (2A-6A)

• Residual With Recovery Benefit (24 or 36) months

• COLA (2A-6A)

• With Buy-Up

• Good Health Benefit (ROP) (2A-6A)

• Guaranteed Insurability (GI) (2A-6A, 18-45)

• Your Occupation Rider (5A-6A, 18-45)

• Transitional Your Occupation (4A-6A, 18-59)

• Lifetime (4A-6A, 18-45)

• Social Insurance Offset (SIO) (2A-6A)*

OMNI Advantage Optional Riders*

* Some Riders are not available for all ages.** Social Insurance Substitute in NY and NJ.

15

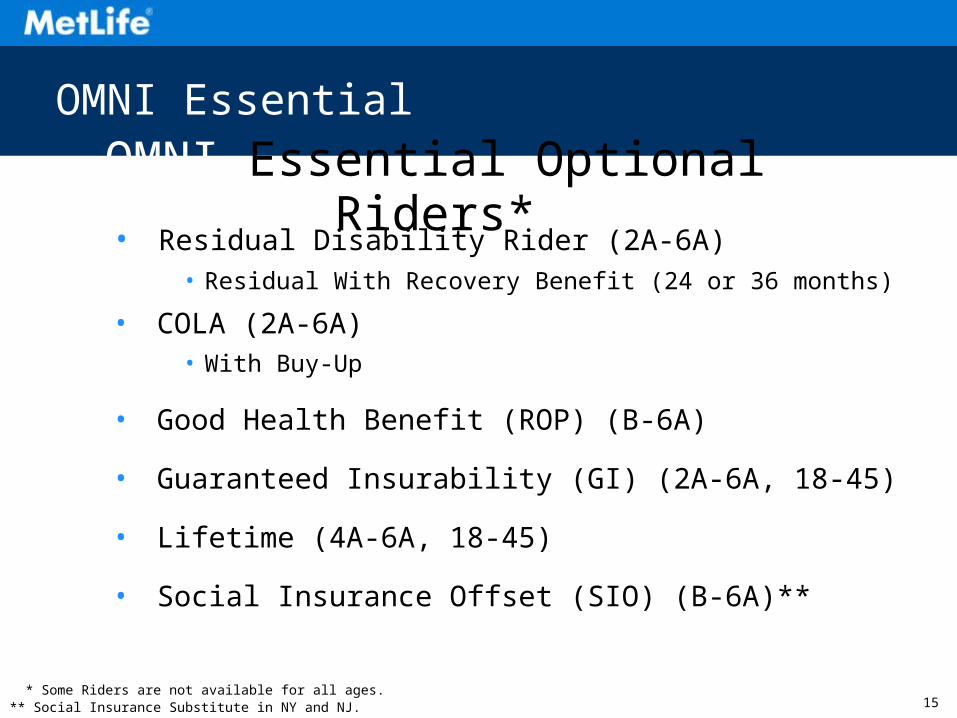

OMNI Essential

• Residual Disability Rider (2A-6A)• Residual With Recovery Benefit (24 or 36 months)

• COLA (2A-6A)• With Buy-Up

• Good Health Benefit (ROP) (B-6A)

• Guaranteed Insurability (GI) (2A-6A, 18-45)

• Lifetime (4A-6A, 18-45)

• Social Insurance Offset (SIO) (B-6A)**

OMNI Essential Optional Riders*

* Some Riders are not available for all ages.** Social Insurance Substitute in NY and NJ.

16

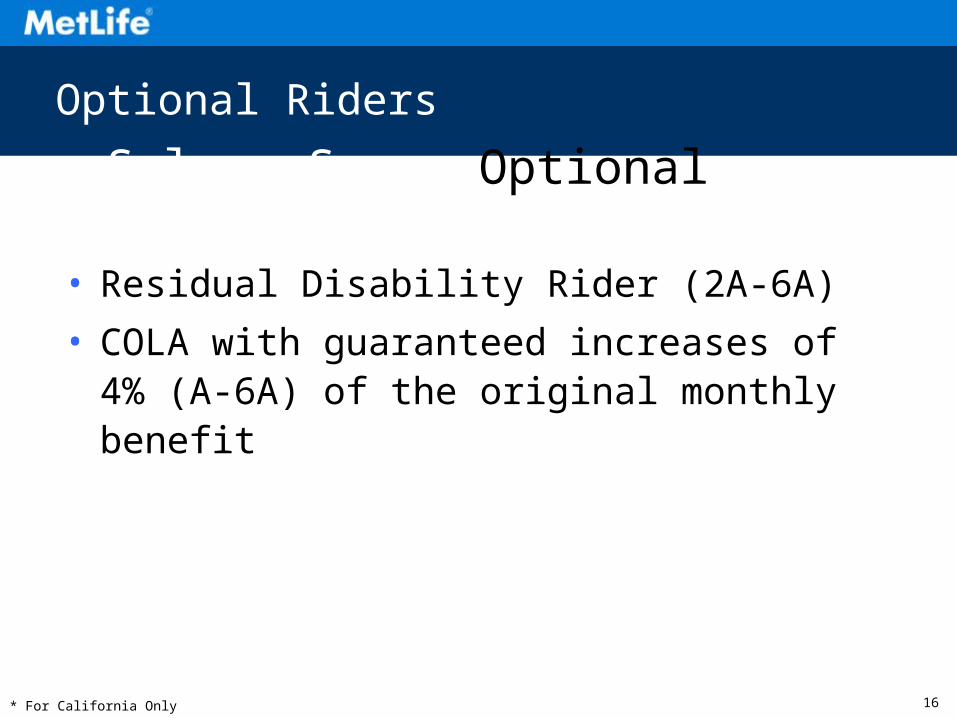

Optional Riders

Salary Saver Optional Riders*

• Residual Disability Rider (2A-6A)

• COLA with guaranteed increases of 4% (A-6A) of the original monthly benefit

* For California Only

17

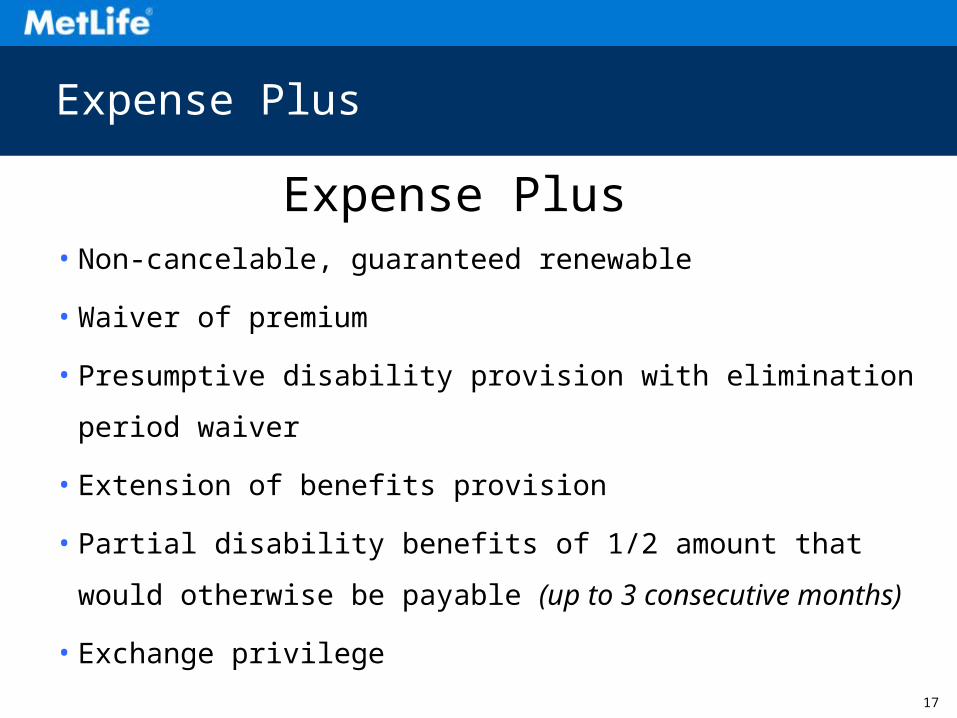

Expense Plus

• Non-cancelable, guaranteed renewable

• Waiver of premium

• Presumptive disability provision with elimination period waiver

• Extension of benefits provision

• Partial disability benefits of 1/2 amount that would otherwise

be payable (up to 3 consecutive months)

• Exchange privilege

Expense Plus

18

MultiLife

The MultiLife Sale*

*MultiLife discounts available in most states

19

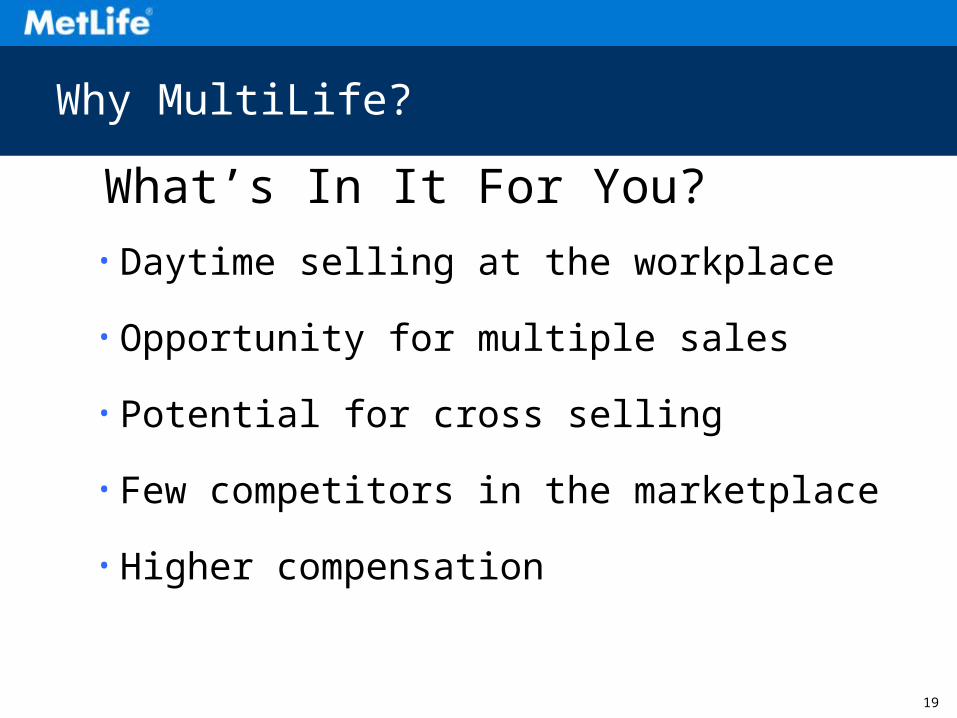

Why MultiLife?

• Daytime selling at the workplace

• Opportunity for multiple sales

• Potential for cross selling

• Few competitors in the marketplace

• Higher compensation

What’s In It For You?

20

MultiLife

• Occ classes 2A-6A

• Most White & Gray Collar Industries

• W-2 employees only

• OMNI Essential & OMNI Select policies only

• Level of discount based on case specifics

• Two MultiLife options...

MultiLife Opportunities

21

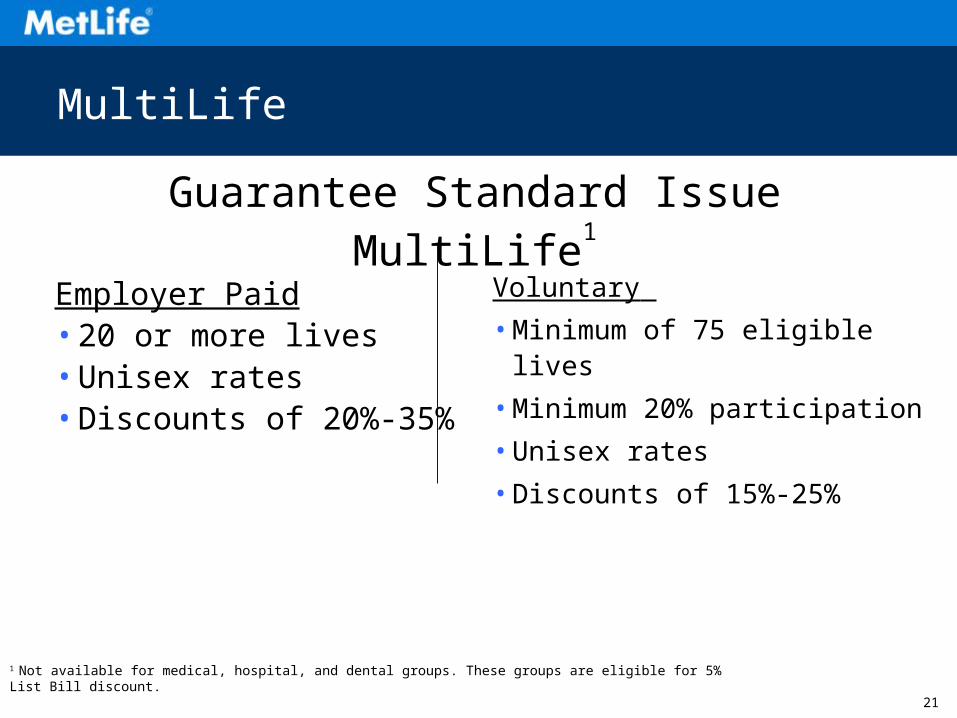

Voluntary

• Minimum of 75 eligible lives

• Minimum 20% participation

• Unisex rates

• Discounts of 15%-25%

MultiLife Opportunities

Employer Paid • 20 or more lives• Unisex rates• Discounts of 20%-35%

1 Not available for medical, hospital, and dental groups. These groups are eligible for 5% List Bill discount.

Guarantee Standard Issue MultiLife1

MultiLife

22

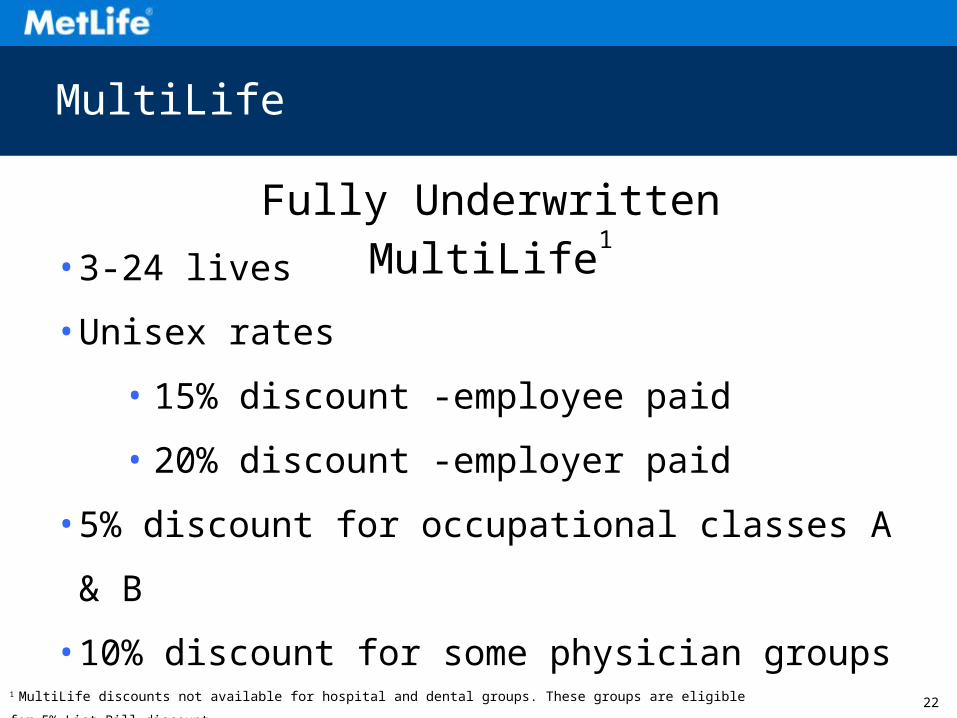

MultiLife

• 3-24 lives

• Unisex rates

• 15% discount -employee paid

• 20% discount -employer paid

• 5% discount for occupational classes A & B

• 10% discount for some physician groups

Fully Underwritten MultiLife1

1 MultiLife discounts not available for hospital and dental groups. These groups are eligible for 5% List Bill discount.

23

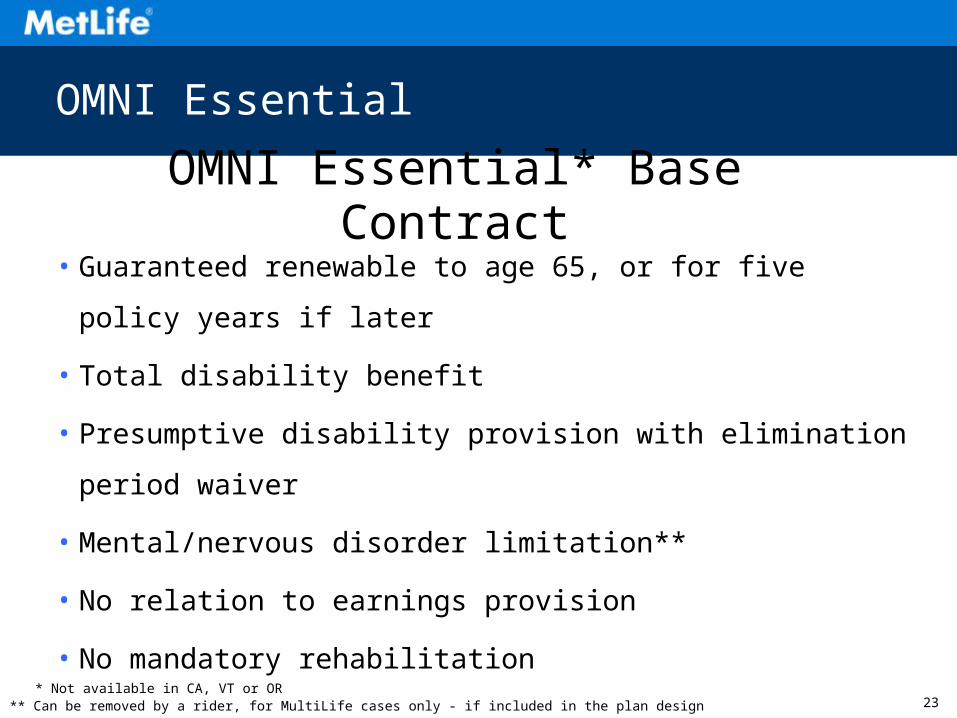

OMNI Essential

• Guaranteed renewable to age 65, or for five policy years if later

• Total disability benefit

• Presumptive disability provision with elimination period waiver

• Mental/nervous disorder limitation**

• No relation to earnings provision

• No mandatory rehabilitation

OMNI Essential* Base Contract

* Not available in CA, VT or OR** Can be removed by a rider, for MultiLife cases only - if included in the plan design

24

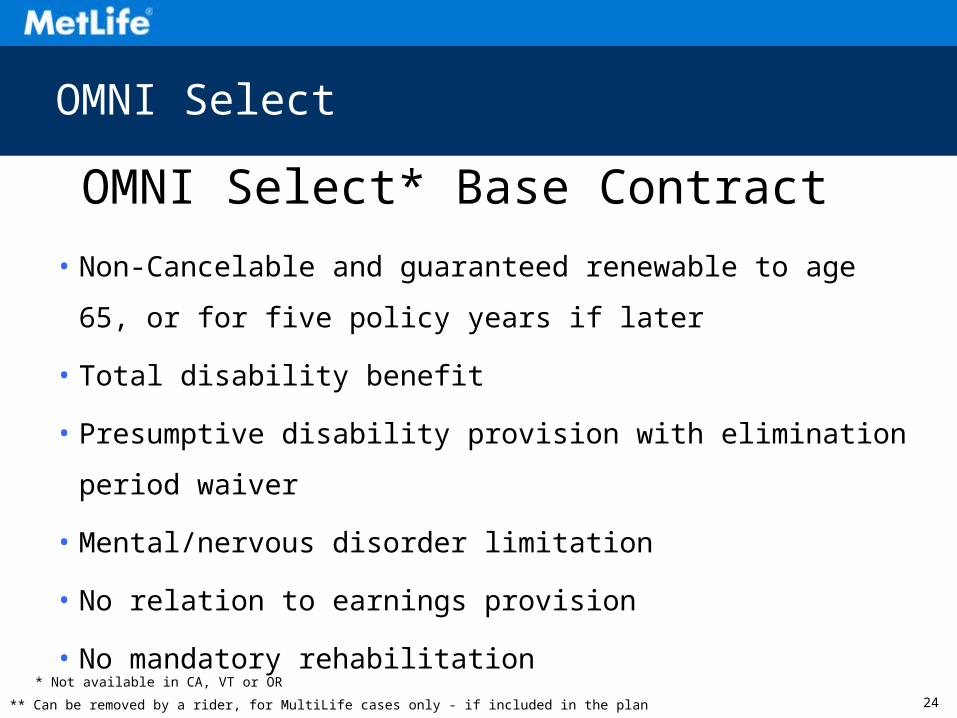

OMNI Select

• Non-Cancelable and guaranteed renewable to age 65, or for five

policy years if later

• Total disability benefit

• Presumptive disability provision with elimination period waiver

• Mental/nervous disorder limitation

• No relation to earnings provision

• No mandatory rehabilitation

OMNI Select* Base Contract

* Not available in CA, VT or OR

** Can be removed by a rider, for MultiLife cases only - if included in the plan design

25

OMNI Essential

OMNI Essential Optional Riders*Riders For GSI Cases Only

•Residual Disability Rider (2A-6A)•Residual With Recovery Benefit • (24 or 36 months)

•COLA (2A-6A)•With Buy-Up

Riders For Fully Underwritten MultiLife Cases

•Residual Disability Rider (2A-6A)•Residual With Recovery Benefit (24 • or 36 months)

•COLA (2A-6A)•With Buy-Up

•Good Health Benefit (ROP) (B-6A)•Guaranteed Insurability (GI) (2A-6A,(18-45)•Lifetime (4A-6A, 18-45)•Social Insurance Offset (SIO) (B-6A)**

* Some Riders are not available for all ages.** Social Insurance Substitute in NY and NJ.

26

OMNI Select

OMNI Select Optional Riders*Riders For GSI Cases Only

• Residual Disability Rider (2A-6A)•Residual With Recovery Benefit (24 or 36 months)

• COLA (2A-6A)•With Buy-Up

• Transitional Your Occupation (4A-6A, 18-59)

Riders For Fully Underwritten MultiLife Cases

• Residual Disability Rider (2A-6A)

•Residual With Recovery Benefit (24 or 36 months)

• COLA (2A-6A)•With Buy-Up

• Good Health Benefit (ROP) (2A-6A)• Guaranteed Insurability (GI) (2A-6A, 18-45)• Your Occupation Rider (5A-6A, 18-45)• Transitional Your Occupation (4A-6A, 18-59)• Lifetime (4A-6A, 18-45)• Social Insurance Offset (SIO) (B-6A)**

* Some Riders are not available for all ages.** Social Insurance Substitute in NY and NJ.

27

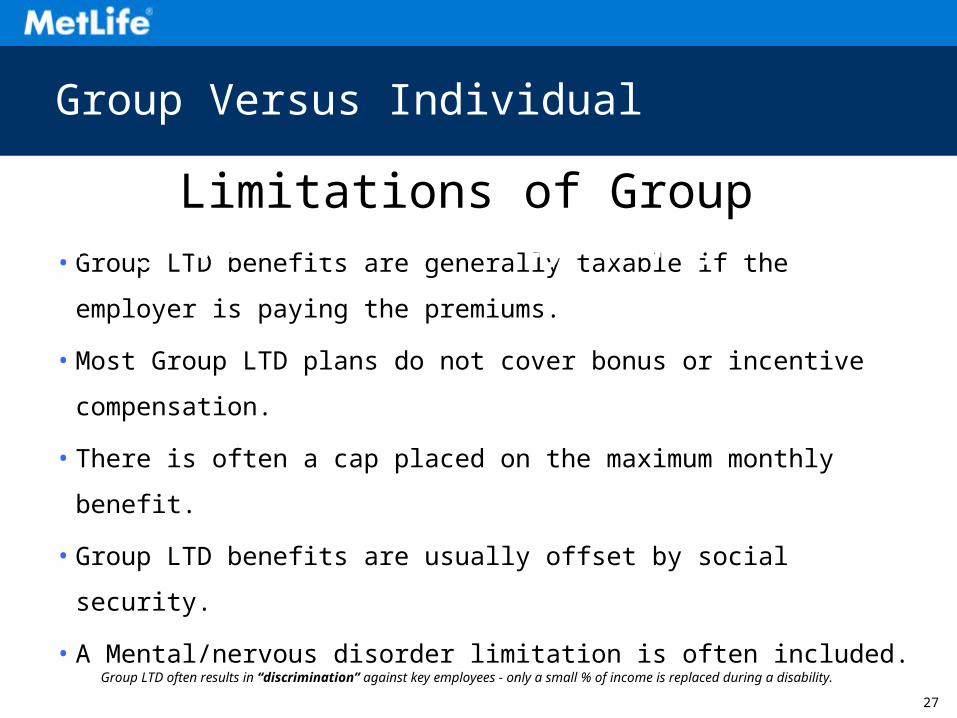

Group Versus Individual

• Group LTD benefits are generally taxable if the employer is

paying the premiums.

• Most Group LTD plans do not cover bonus or incentive

compensation.

• There is often a cap placed on the maximum monthly benefit.

• Group LTD benefits are usually offset by social security.

• A Mental/nervous disorder limitation is often included.

Limitations of Group Long-term Disability (LTD) Plans

Group LTD often results in “discrimination” against key employees - only a small % of income is replaced during a disability.

28

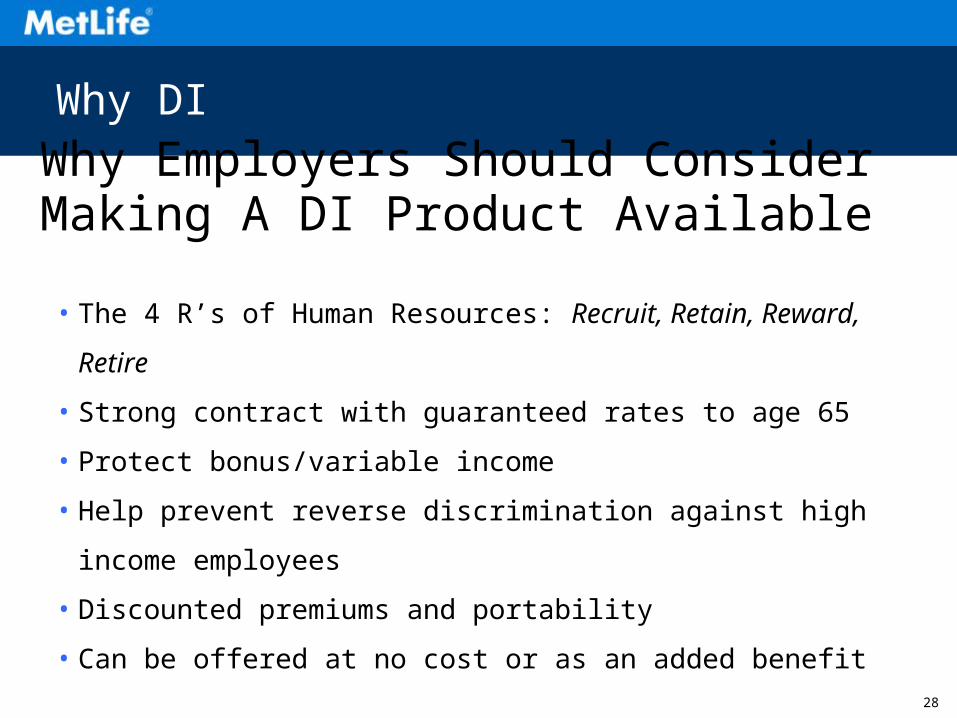

Why DI

• The 4 R’s of Human Resources: Recruit, Retain, Reward, Retire

• Strong contract with guaranteed rates to age 65

• Protect bonus/variable income

• Help prevent reverse discrimination against high income

employees

• Discounted premiums and portability

• Can be offered at no cost or as an added benefit

Why Employers Should Consider Making A DI Product Available A DI Policy Available

29

Consider This... Your Client’s Group LTD Plan Design: [60% of base salary; up to $6,000 per month]

Gross Group % ofBase Bonus Monthly LTD Individual Income

Employee Salary Income Income Benefit DI Benefit ReplacedEmployee 1 $45,000 $0 $3,750 $2,250 $0 60%Employee 2 $65,000 $10,000 $6,250 $3,250 $0 52%Employee 3 $100,000 $50,000 $12,500 $5,000 $0 40%Employee 4 $200,000 $70,000 $22,500 $6,000 $0 27%

Key employees face a lower income replacement percentage!

A MultiLife Example

MultiLife

30

The Solution… [Policy Name]This comprehensive program provides additional coverage for all eligible employees and helps reduce “discrimination” against highly compensated employees.

Gross Group % ofBase Bonus Monthly LTD Individual Income

Employee Salary Income Income Benefit DI Benefit ReplacedEmployee 1 $45,000 $0 $3,750 $2,250 $832 82%Employee 2 $65,000 $10,000 $6,250 $3,250 $1,525 76%Employee 3 $100,000 $50,000 $12,500 $5,000 $3,500 68%Employee 4 $200,000 $70,000 $22,500 $6,000 $8,700 65%

With [Policy Name], the percentage of income replaced for Employees 3 and 4 is considerably higher!

A MultiLife Example

MultiLife

31

MultiLife

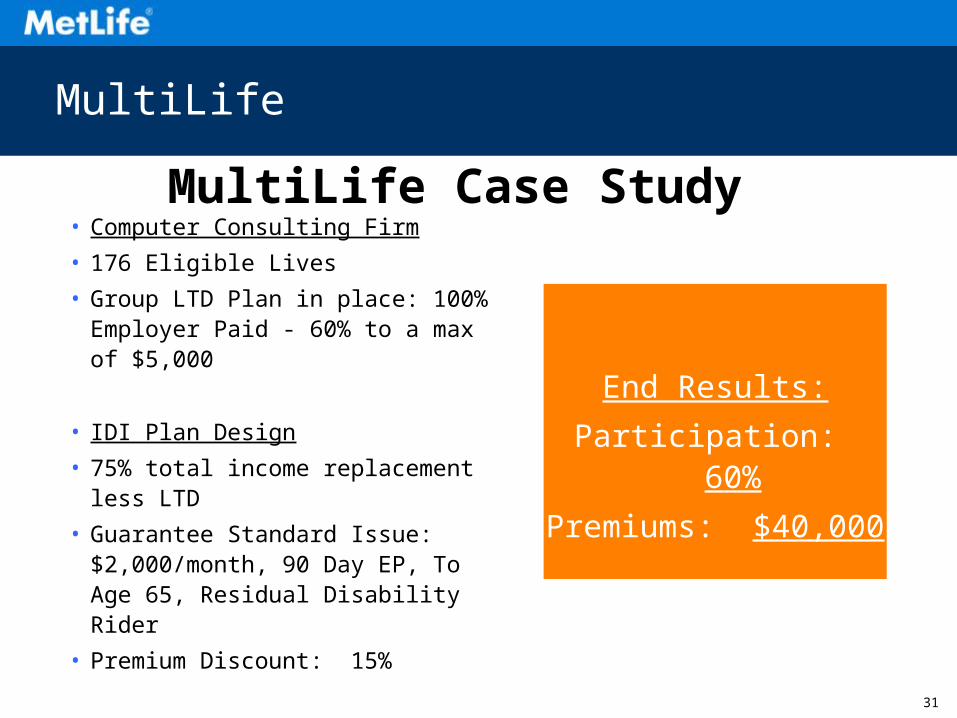

MultiLife Case Study

End Results:

Participation: 60%

Premiums: $40,000

• Computer Consulting Firm

• 176 Eligible Lives

• Group LTD Plan in place: 100% Employer Paid - 60% to a max of $5,000

• IDI Plan Design

• 75% total income replacement less LTD

• Guarantee Standard Issue: $2,000/month, 90 Day EP, To Age 65, Residual Disability Rider

• Premium Discount: 15%

32

Contact Your SBC DI Rep

• Your local SBC DI Rep can provide you with all of your DI solutions such as:

• Market Segmentation

• Client Prospecting

• Illustration Assistance

• Competition Information

How Your SBC DI Rep Can Help