TVS Motor Company -...

15

COMPANY August 5, 2016 TVS Motor Company Modest fundamentals; Luxurious valuations Source: Capitaline SELL Nifty: 8,683; Sensex: 28,078 COMPANY OUTLOOK Table: Financial snapshot (Rsmn) Year Revenue EBITDA EBITDA (%) Adj. PAT EPS (Rs) P/E EV/EBITDA (x) RoE (%) RoCE (%) FY15 100,423 6,066 6.0 3,478 7.3 39.5 23.6 22.7 18.9 FY16 112,439 7,507 6.7 4,321 9.1 31.8 18.6 24.1 20.1 FY17E 126,905 9,130 7.2 4,884 10.3 26.2 14.2 23.2 21.3 FY18E 144,379 11,212 7.8 6,175 13.0 20.7 11.3 24.8 24.6 Source: Company; IDBI Capital Research*This marks the transfer of coverage from Ashish Poddar to Pranoy Kurian Summary Q1FY17 Results: Revenues grew 12% YoY to Rs28.8bn (vol. growth of 12.5%, with domestic growth of 18% and exports falling by 13%. Motorcycles and scooters rose 11% and 19%, respectively, while mopeds increased by 18%. Turmoil in key export markets continued impacting demand, with 3W exports down 46%). As a result, realizations were subpar, falling 0.5% YoY and 6% QoQ as the lower share of exports and 3W hurt ASP’s. Margins rose 24bps YoY to 7%, but this was partly due to certain raw material costs being classified under depreciation under IND-AS. PAT rose 21% to Rs1bn. Near Term Outlook: TVS should continue reporting strong domestic volume growth over FY16-18E on the back of aggressive pricing, robust demand for scooters & mopeds and near term favourable tailwinds such as GST/7PC/normal monsoons. The TVS Victor, 200cc Apache and a new moped model are now available nationwide and are likely to maintain domestic sales momentum for F17. Volumes from the TVS-BMW tie-up are likely to contribute to topline in H2FY17. We estimate revenue growth of 13% over FY16-18E, primarily driven by volumes (10% est.), with realizations likely to remain muted due to export pressure. Management’s aim to raise margins to ~10% seems unrealistic however, and we expect margins to stay capped at the 8% mark given the price sensitivity of TVS’ moped/scooter segments and rising gross margins. Thus, we estimate EPS growth of 20% over FY16-18E. Valuation: TVS remains a stable company with decent fundamentals – presence in high growth segments, RoEs of ~25% despite OPM margins of just ~7%, a well-established brand and improving cash flow. However, TVS is likely to continue facing heightened competition in the slowing 2W segment. At CMP, TVS trades at a premium valuation of 15x on an EV/EBIT basis and 21x on an FY18 P/E basis, expensive when compared to better placed peers such as MSIL (22x) and at a substantial premium to BJAUT/HMCL. We assign the stock a 12X multiple on FY18E/EV/EBIT (16x standalone FY18 P/E) and add Rs34/a share for investments/JVs. We value the stock at Rs244 and recommend a SELL. Outlook and View 2W long term growth holds lower potential than PV’s: India’s 2W penetration has increased enormously over the past decade (~13% now vs. ~8% in 2010). However, while comparing penetration rates of 2W and PV’s in India vs other economies, we believe that the growth potential for 2Ws remains substantially below PVs (~2.5% penetration). Given the large existing base, the scope for doubling or even tripling 2W penetration rates within a decade remains far more of a challenge than it is for PV penetration rates (from ~3% to ~5% or ~8%). While scooterization will boost TVS’ short term revenue growth, industry growth is likely to moderate on the back of potential uptrending and saturation among the female workforce. Thus, for the overall 2W industry, we expect a lower growth trajectory ~7-8%+ volume growth over the next decade as compared to PVs (~10-12%+). The Ever Elusive Margin Expansion:One of the oft-cited investment rationales for TVS has been the possibility of a structural improvement in margins. Given the low base of current margins (7%), a shift towards 10% would yield a sharp rise in profitability (a 100bps margin increase boosts EPS by ~20-25%). However, TVS’ long term track record doesn’t offer much comfort, as margins have stubbornly stuck to 6-7% over the past decade. Key challenges to margin expansion include 1) High Ad/promotion spend relative to peers 2) Core segments of TVS’ revenue (mopeds, scooters) are inherently price sensitive and lower margin 3) Recent margin expansion was driven by declining commodity costs rather than structural changes, and this trend is reversing 4) Exports (higher margin) are seeing deep declines in volumes on macro-economic issues and 5) Rising competitive intensity in the scooter segment is likely to leave TVS little room for price increases. CMP Rs303 Target Price Rs244 Potential Upside/Downside (19)% Sector Automobiles Bloomberg / Reuters TVSL IN/TVSM.BO Shares o/s (mn) 475 Market cap. (Rsmn) 143,949 Market cap. (US$ mn) 2,147 3-m daily average vol. 161,240 Key Stock Data 52-week high/low Rs341/201 -1m -3m -12m Absolute (%) (1) 3 29 Rel to Sensex (%) (4) (9) 30 Price Performance Promoters 57.4 FIIs/NRIs/OCBs/GDR 15.5 MFs/Banks/FIs 14.5 Non Promoter Corporate 1.5 Public & Others 11.1 Shareholding Pattern (%) Relative to Sensex 70 80 90 100 110 120 130 140 150 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 TVSL Sensex

Transcript of TVS Motor Company -...

COMPANY

REPORT

August 5, 2016

TVS Motor Company Modest fundamentals; Luxurious valuations

Source: Capitaline

SELL Nifty: 8,683; Sensex: 28,078

COMPANY

OUTLOOK

Table: Financial snapshot (Rsmn)

Year Revenue EBITDA EBITDA (%) Adj. PAT EPS (Rs) P/E

(x)

EV/EBITDA (x) RoE (%) RoCE (%)

FY15 100,423 6,066 6.0 3,478 7.3 39.5 23.6 22.7 18.9

FY16 112,439 7,507 6.7 4,321 9.1 31.8 18.6 24.1 20.1

FY17E 126,905 9,130 7.2 4,884 10.3 26.2 14.2 23.2 21.3

FY18E 144,379 11,212 7.8 6,175 13.0 20.7 11.3 24.8 24.6 Source: Company; IDBI Capital Research*This marks the transfer of coverage from Ashish Poddar to Pranoy Kurian

Summary

Q1FY17 Results: Revenues grew 12% YoY to Rs28.8bn (vol. growth of 12.5%, with domestic growth of 18% and exports falling by 13%. Motorcycles and scooters rose 11% and 19%, respectively, while mopeds increased by 18%. Turmoil in key export markets continued impacting demand, with 3W exports down 46%). As a result, realizations were subpar, falling 0.5% YoY and 6% QoQ as the lower share of exports and 3W hurt ASP’s. Margins rose 24bps YoY to 7%, but this was partly due to certain raw material costs being classified under depreciation under IND-AS. PAT rose 21% to Rs1bn.

Near Term Outlook: TVS should continue reporting strong domestic volume growth over FY16-18E on the back of aggressive pricing, robust demand for scooters & mopeds and near term favourable tailwinds such as GST/7PC/normal monsoons. The TVS Victor, 200cc Apache and a new moped model are now available nationwide and are likely to maintain domestic sales momentum for F17. Volumes from the TVS-BMW tie-up are likely to contribute to topline in H2FY17. We estimate revenue growth of 13% over FY16-18E, primarily driven by volumes (10% est.), with realizations likely to remain muted due to export pressure. Management’s aim to raise margins to ~10% seems unrealistic however, and we expect margins to stay capped at the 8% mark given the price sensitivity of TVS’ moped/scooter segments and rising gross margins. Thus, we estimate EPS growth of 20% over FY16-18E.

Valuation: TVS remains a stable company with decent fundamentals – presence in high growth segments, RoEs of ~25% despite OPM margins of just ~7%, a well-established brand and improving cash flow. However, TVS is likely to continue facing heightened competition in the slowing 2W segment. At CMP, TVS trades at a premium valuation of 15x on an EV/EBIT basis and 21x on an FY18 P/E basis, expensive when compared to better placed peers such as MSIL (22x) and at a substantial premium to BJAUT/HMCL. We assign the stock a 12X multiple on FY18E/EV/EBIT (16x standalone FY18 P/E) and add Rs34/a share for investments/JVs. We value the stock at Rs244 and recommend a SELL.

Outlook and View 2W long term growth holds lower potential than PV’s: India’s 2W penetration has increased

enormously over the past decade (~13% now vs. ~8% in 2010). However, while comparing penetration rates of 2W and PV’s in India vs other economies, we believe that the growth potential for 2Ws remains substantially below PVs (~2.5% penetration). Given the large existing base, the scope for doubling or even tripling 2W penetration rates within a decade remains far more of a challenge than it is for PV penetration rates (from ~3% to ~5% or ~8%). While scooterization will boost TVS’ short term revenue growth, industry growth is likely to moderate on the back of potential uptrending and saturation among the female workforce. Thus, for the overall 2W industry, we expect a lower growth trajectory ~7-8%+ volume growth over the next decade as compared to PVs (~10-12%+).

The Ever Elusive Margin Expansion:One of the oft-cited investment rationales for TVS has been the possibility of a structural improvement in margins. Given the low base of current margins (7%), a shift towards 10% would yield a sharp rise in profitability (a 100bps margin increase boosts EPS by ~20-25%). However, TVS’ long term track record doesn’t offer much comfort, as margins have stubbornly stuck to 6-7% over the past decade. Key challenges to margin expansion include 1) High Ad/promotion spend relative to peers 2) Core segments of TVS’ revenue (mopeds, scooters) are inherently price sensitive and lower margin 3) Recent margin expansion was driven by declining commodity costs rather than structural changes, and this trend is reversing 4) Exports (higher margin) are seeing deep declines in volumes on macro-economic issues and 5) Rising competitive intensity in the scooter segment is likely to leave TVS little room for price increases.

CMP Rs303

Target Price Rs244

Potential Upside/Downside (19)%

Sector Automobiles

Bloomberg / Reuters TVSL IN/TVSM.BO

Shares o/s (mn) 475

Market cap. (Rsmn) 143,949

Market cap. (US$ mn) 2,147

3-m daily average vol. 161,240

Key Stock Data

52-week high/low Rs341/201

-1m -3m -12m

Absolute (%) (1) 3 29

Rel to Sensex (%) (4) (9) 30

Price Performance

Promoters 57.4

FIIs/NRIs/OCBs/GDR 15.5

MFs/Banks/FIs 14.5

Non Promoter Corporate 1.5

Public & Others 11.1

Shareholding Pattern (%)

Relative to Sensex

708090

100110120130140150

May

-15

Jun

-15

Jul-

15

Au

g-15

Sep

-15

Oct

-15

No

v-15

Dec

-15

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-16

May

-16

Jun

-16

Jul-

16

TVSL Sensex

2

Company Outlook – TVS Motor Company

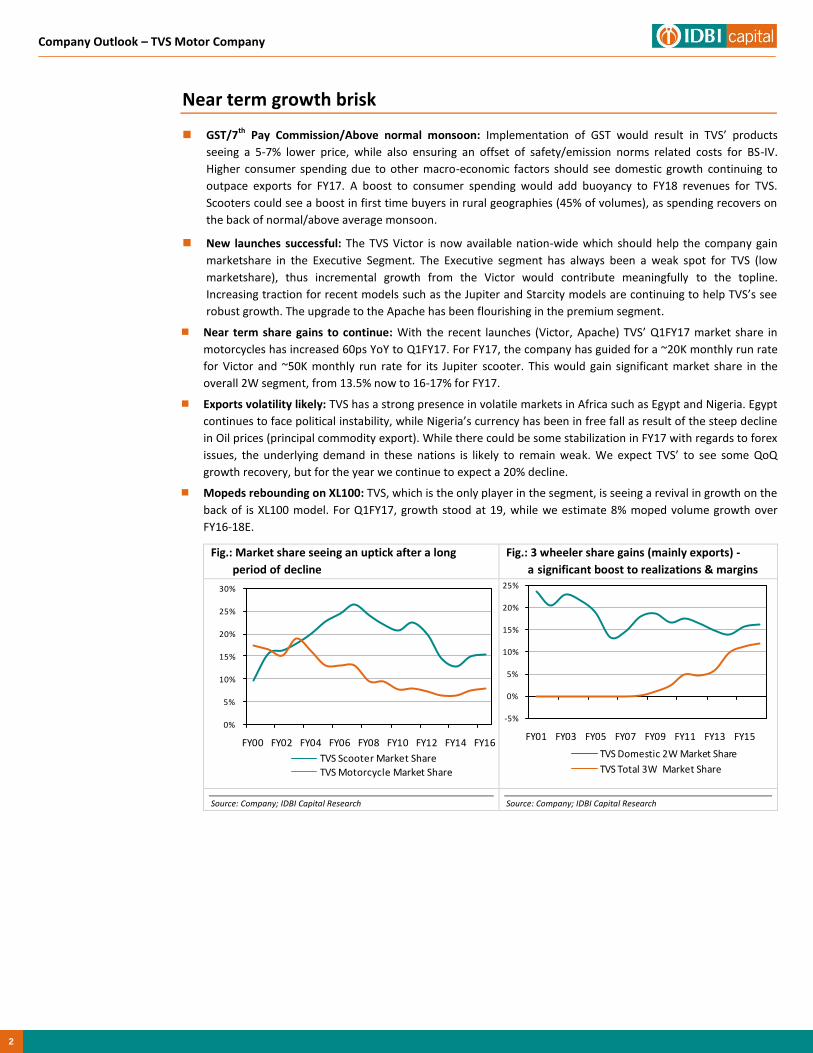

Near term growth brisk

GST/7th Pay Commission/Above normal monsoon: Implementation of GST would result in TVS’ products

seeing a 5-7% lower price, while also ensuring an offset of safety/emission norms related costs for BS-IV.

Higher consumer spending due to other macro-economic factors should see domestic growth continuing to

outpace exports for FY17. A boost to consumer spending would add buoyancy to FY18 revenues for TVS.

Scooters could see a boost in first time buyers in rural geographies (45% of volumes), as spending recovers on

the back of normal/above average monsoon.

New launches successful: The TVS Victor is now available nation-wide which should help the company gain

marketshare in the Executive Segment. The Executive segment has always been a weak spot for TVS (low

marketshare), thus incremental growth from the Victor would contribute meaningfully to the topline.

Increasing traction for recent models such as the Jupiter and Starcity models are continuing to help TVS’s see

robust growth. The upgrade to the Apache has been flourishing in the premium segment.

Near term share gains to continue: With the recent launches (Victor, Apache) TVS’ Q1FY17 market share in

motorcycles has increased 60ps YoY to Q1FY17. For FY17, the company has guided for a ~20K monthly run rate

for Victor and ~50K monthly run rate for its Jupiter scooter. This would gain significant market share in the

overall 2W segment, from 13.5% now to 16-17% for FY17.

Exports volatility likely: TVS has a strong presence in volatile markets in Africa such as Egypt and Nigeria. Egypt

continues to face political instability, while Nigeria’s currency has been in free fall as result of the steep decline

in Oil prices (principal commodity export). While there could be some stabilization in FY17 with regards to forex

issues, the underlying demand in these nations is likely to remain weak. We expect TVS’ to see some QoQ

growth recovery, but for the year we continue to expect a 20% decline.

Mopeds rebounding on XL100: TVS, which is the only player in the segment, is seeing a revival in growth on the

back of is XL100 model. For Q1FY17, growth stood at 19, while we estimate 8% moped volume growth over

FY16-18E.

Fig.: Market share seeing an uptick after a long

Fig.:period of:decline

Fig.: 3 wheeler share gains (mainly exports) -

Fig.:a:significant boost to realizations & margins

Source: Company; IDBI Capital Research Source: Company; IDBI Capital Research

0%

5%

10%

15%

20%

25%

30%

FY00 FY02 FY04 FY06 FY08 FY10 FY12 FY14 FY16

TVS Scooter Market Share

TVS Motorcycle Market Share

-5%

0%

5%

10%

15%

20%

25%

FY01 FY03 FY05 FY07 FY09 FY11 FY13 FY15

TVS Domestic 2W Market Share

TVS Total 3W Market Share

Company Outlook – TVS Motor Company

3

Fig.: TVS Product mix: Scooterization benefiting TVS Fig.: Quarterly growth- Domestic growth

Fig.:powering up, offsetting weakness in exports

Source: SIAM; IDBI Capital Research Source: Company; IDBI Capital Research

Longer term growth picture less rosy

2W segment long term growth profile uncertain: India’s 2W penetration has increased enormously over the

past decade (13% now vs 8% in 2010). However, while comparing penetration rates of India vs other emerging

nations, there remain doubts as to the long term growth potential of the 2W industry.

Well Penetrated given income level: Unlike the PV industry where ownership is extremely low, 2W’s (especially

motorcycles) are reasonably well penetrated given India’s GDP per capita.

Future of 3W uncertain: Other segments such as 3W could see lower than expected growth if 1) The

transportation industry continues up-trending towards PVs and 2) Higher share of goods are transported by

larger CV’s as fleets consolidate.

8+%+ Volume growth unlikely: Thus, for overall 2W/3W industry, we believe 8%+ volume growth over the next

decade would remain a challenge, giving the industry a lower long term growth trajectory than PVs or premium

motorcycles (350cc +).

Figure: Indian 2W industry has room for growth, but

Figure:gap between peers not extraordinary

Figure: PV’s highly underpenetrated, still at the

Figure:bottom of emerging market ladder

Source: World Bank, SIAM; IDBI Capital Research Source: World Bank, SIAM; IDBI Capital Research

0%

20%

40%

60%

80%

100%

Dec/12 Jun/13 Dec/13 Jun/14 Dec/14 Jun/15 Dec/15 Jun/16

Motorcycle Scooter Moped 3-Wh

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

Mar/13Sep/13Mar/14Sep/14Mar/15Sep/15Mar/16

EBITD

A M

argins

Domestic (% YoY, RHS)

Exports (% YoY, RHS)

China

Brazil

IndonesiaIndiaVietnam

Japan

-2000

3000

8000

13000

18000

23000

28000

33000

38000

43000

48000

-20 80 180 280 380

GD

P P

er

Cap

ita

in 2

01

0 $

pri

ces

2W Vehicles/Thousand People

China

Brazil

India

Russia

South Korea

Japan

Indonesia

-3000

2000

7000

12000

17000

22000

27000

32000

37000

42000

47000

0 50 100 150 200 250 300 350 400 450 500 550 600

GD

P P

er

Cap

ita

in 2

01

0 $

pri

ces

PV Vehicles/Thousand People

4

Company Outlook – TVS Motor Company

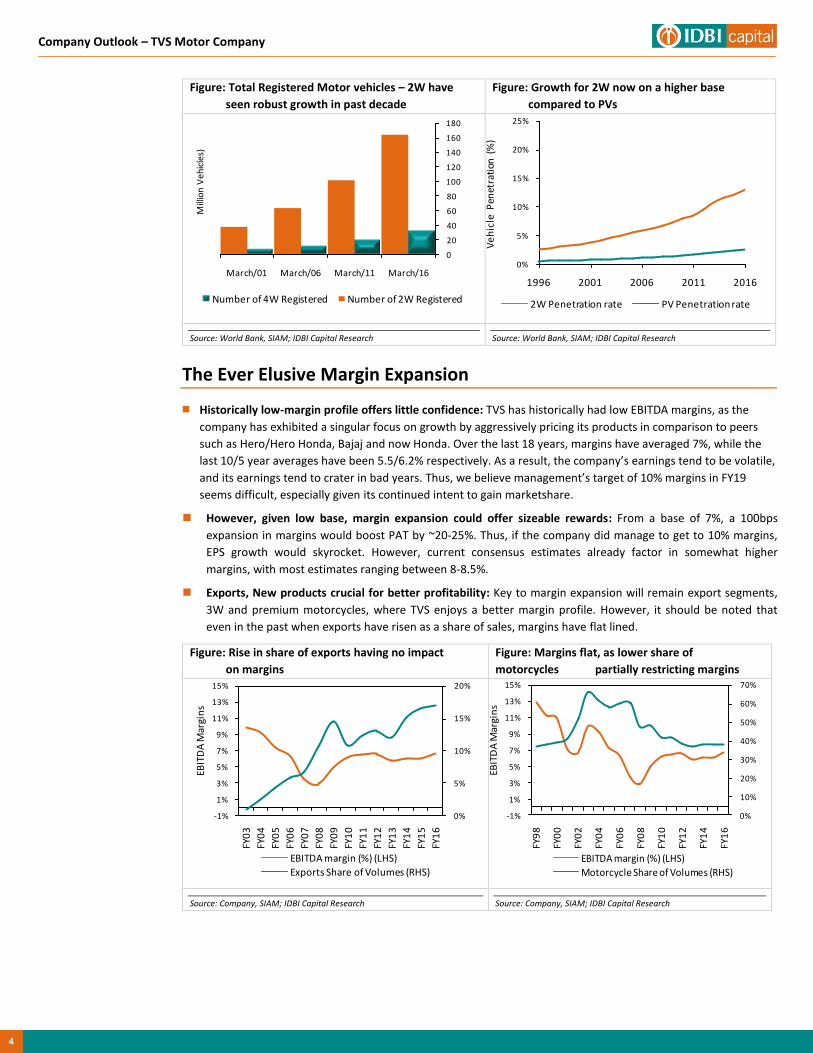

Figure: Total Registered Motor vehicles – 2W have

Figure:seen robust growth in past decade

Figure: Growth for 2W now on a higher base

Figure:compared to PVs

Source: World Bank, SIAM; IDBI Capital Research Source: World Bank, SIAM; IDBI Capital Research

The Ever Elusive Margin Expansion

Historically low-margin profile offers little confidence: TVS has historically had low EBITDA margins, as the

company has exhibited a singular focus on growth by aggressively pricing its products in comparison to peers

such as Hero/Hero Honda, Bajaj and now Honda. Over the last 18 years, margins have averaged 7%, while the

last 10/5 year averages have been 5.5/6.2% respectively. As a result, the company’s earnings tend to be volatile,

and its earnings tend to crater in bad years. Thus, we believe management’s target of 10% margins in FY19

seems difficult, especially given its continued intent to gain marketshare.

However, given low base, margin expansion could offer sizeable rewards: From a base of 7%, a 100bps

expansion in margins would boost PAT by ~20-25%. Thus, if the company did manage to get to 10% margins,

EPS growth would skyrocket. However, current consensus estimates already factor in somewhat higher

margins, with most estimates ranging between 8-8.5%.

Exports, New products crucial for better profitability: Key to margin expansion will remain export segments,

3W and premium motorcycles, where TVS enjoys a better margin profile. However, it should be noted that

even in the past when exports have risen as a share of sales, margins have flat lined.

Figure: Rise in share of exports having no impact

Figure:on margins

Figure: Margins flat, as lower share of

motorcyclesFigure:partially restricting margins

Source: Company, SIAM; IDBI Capital Research Source: Company, SIAM; IDBI Capital Research

0

20

40

60

80

100

120

140

160

180

March/16March/11March/06March/01

Mill

ion

Veh

icle

s)

Number of 4W Registered Number of 2W Registered

0%

5%

10%

15%

20%

25%

1996 2001 2006 2011 2016

Ve

hic

le P

enet

rati

on (

%)

2W Penetration rate PV Penetration rate

0%

5%

10%

15%

20%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

EBIT

DA

Mar

gin

s

EBITDA margin (%) (LHS)

Exports Share of Volumes (RHS)

0%

10%

20%

30%

40%

50%

60%

70%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

FY9

8

FY0

0

FY0

2

FY0

4

FY0

6

FY0

8

FY1

0

FY1

2

FY1

4

FY1

6

EBIT

DA

Mar

gin

s

EBITDA margin (%) (LHS)

Motorcycle Share of Volumes (RHS)

Company Outlook – TVS Motor Company

5

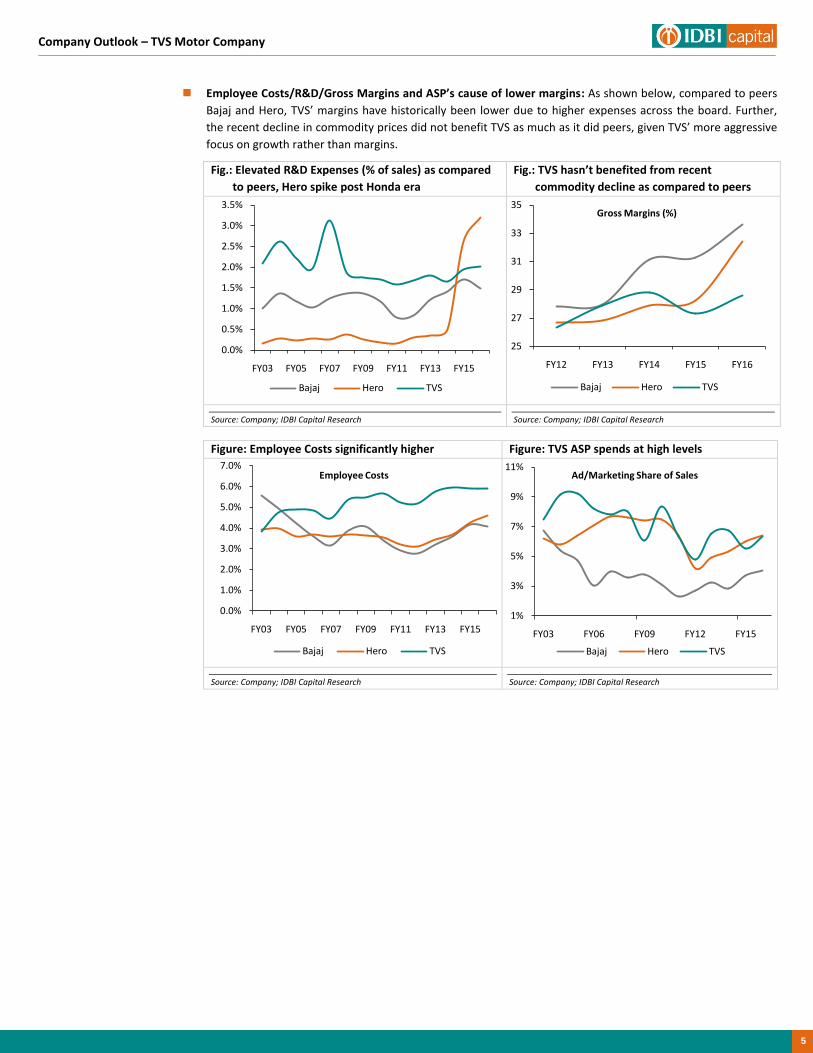

Employee Costs/R&D/Gross Margins and ASP’s cause of lower margins: As shown below, compared to peers

Bajaj and Hero, TVS’ margins have historically been lower due to higher expenses across the board. Further,

the recent decline in commodity prices did not benefit TVS as much as it did peers, given TVS’ more aggressive

focus on growth rather than margins.

Fig.: Elevated R&D Expenses (% of sales) as compared

Fig.:to peers, Hero spike post Honda era

Fig.: TVS hasn’t benefited from recent

Figucommodity decline as compared to peers

Source: Company; IDBI Capital Research Source: Company; IDBI Capital Research

Figure: Employee Costs significantly higher Figure: TVS ASP spends at high levels

Source: Company; IDBI Capital Research Source: Company; IDBI Capital Research

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

FY03 FY05 FY07 FY09 FY11 FY13 FY15

Bajaj Hero TVS

25

27

29

31

33

35

FY12 FY13 FY14 FY15 FY16

Gross Margins (%)

Bajaj Hero TVS

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

FY03 FY05 FY07 FY09 FY11 FY13 FY15

Employee Costs

Bajaj Hero TVS

1%

3%

5%

7%

9%

11%

FY03 FY06 FY09 FY12 FY15

Ad/Marketing Share of Sales

Bajaj Hero TVS

6

Company Outlook – TVS Motor Company

Other Challenges

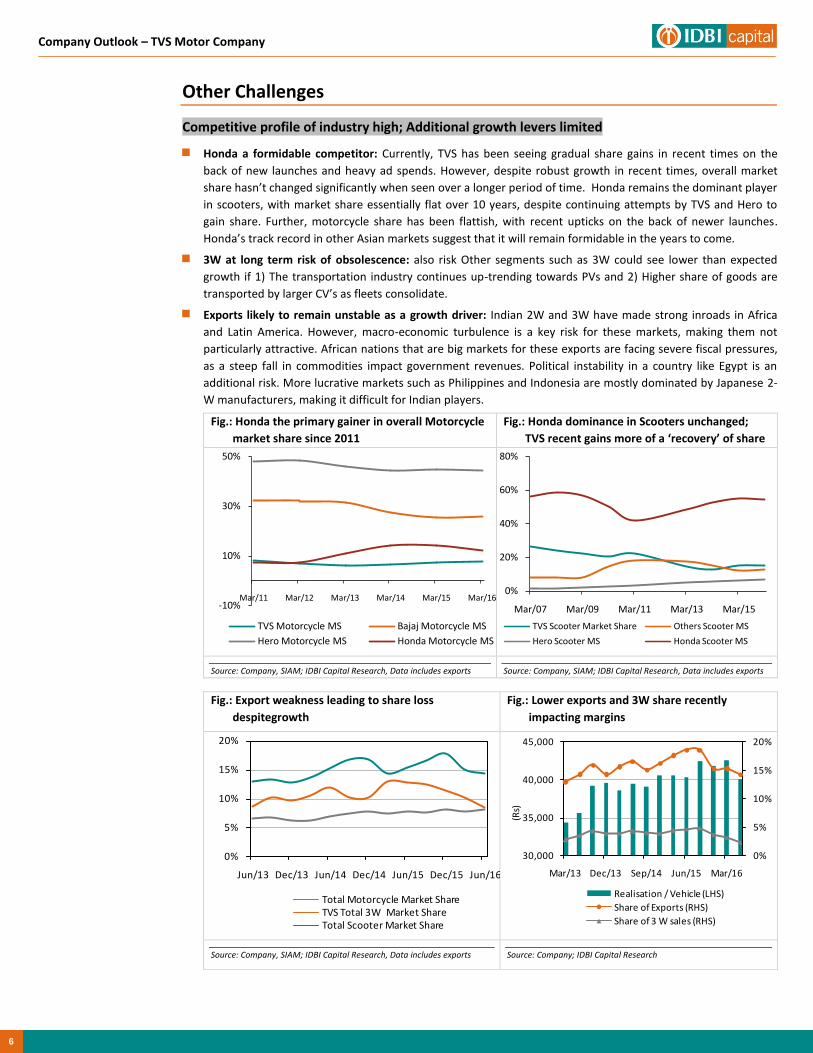

Competitive profile of industry high; Additional growth levers limited

Honda a formidable competitor: Currently, TVS has been seeing gradual share gains in recent times on the

back of new launches and heavy ad spends. However, despite robust growth in recent times, overall market

share hasn’t changed significantly when seen over a longer period of time. Honda remains the dominant player

in scooters, with market share essentially flat over 10 years, despite continuing attempts by TVS and Hero to

gain share. Further, motorcycle share has been flattish, with recent upticks on the back of newer launches.

Honda’s track record in other Asian markets suggest that it will remain formidable in the years to come.

3W at long term risk of obsolescence: also risk Other segments such as 3W could see lower than expected

growth if 1) The transportation industry continues up-trending towards PVs and 2) Higher share of goods are

transported by larger CV’s as fleets consolidate.

Exports likely to remain unstable as a growth driver: Indian 2W and 3W have made strong inroads in Africa

and Latin America. However, macro-economic turbulence is a key risk for these markets, making them not

particularly attractive. African nations that are big markets for these exports are facing severe fiscal pressures,

as a steep fall in commodities impact government revenues. Political instability in a country like Egypt is an

additional risk. More lucrative markets such as Philippines and Indonesia are mostly dominated by Japanese 2-

W manufacturers, making it difficult for Indian players.

Fig.: Honda the primary gainer in overall Motorcycle

Fig.:market share since 2011

Fig.: Honda dominance in Scooters unchanged;

Fig.:TVS recent gains more of a ‘recovery’ of share

Source: Company, SIAM; IDBI Capital Research, Data includes exports Source: Company, SIAM; IDBI Capital Research, Data includes exports

Fig.: Export weakness leading to share loss

Fig.:despitegrowth

Fig.: Lower exports and 3W share recently

Fig.:impacting margins

Source: Company, SIAM; IDBI Capital Research, Data includes exports Source: Company; IDBI Capital Research

-10%

10%

30%

50%

Mar/11 Mar/12 Mar/13 Mar/14 Mar/15 Mar/16

TVS Motorcycle MS Bajaj Motorcycle MS

Hero Motorcycle MS Honda Motorcycle MS

0%

20%

40%

60%

80%

Mar/07 Mar/09 Mar/11 Mar/13 Mar/15

TVS Scooter Market Share Others Scooter MS

Hero Scooter MS Honda Scooter MS

0%

5%

10%

15%

20%

Jun/13 Dec/13 Jun/14 Dec/14 Jun/15 Dec/15 Jun/16

Total Motorcycle Market ShareTVS Total 3W Market ShareTotal Scooter Market Share

0%

5%

10%

15%

20%

30,000

35,000

40,000

45,000

Mar/13 Dec/13 Sep/14 Jun/15 Mar/16

(Rs)

Realisation / Vehicle (LHS)

Share of Exports (RHS)

Share of 3 W sales (RHS)

Company Outlook – TVS Motor Company

7

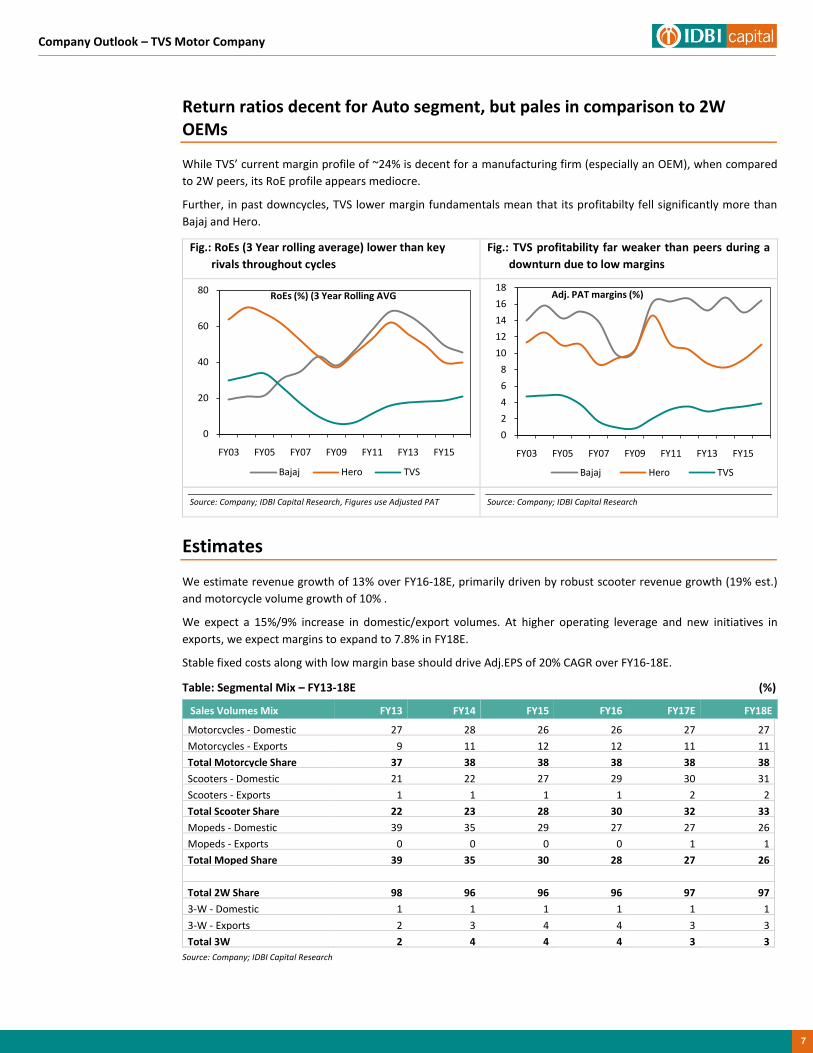

Return ratios decent for Auto segment, but pales in comparison to 2W OEMs

While TVS’ current margin profile of ~24% is decent for a manufacturing firm (especially an OEM), when compared

to 2W peers, its RoE profile appears mediocre.

Further, in past downcycles, TVS lower margin fundamentals mean that its profitabilty fell significantly more than

Bajaj and Hero.

Fig.: RoEs (3 Year rolling average) lower than key

Fig.:rivals throughout cycles

Fig.: TVS profitability far weaker than peers during a

Fig.:downturn due to low margins

Source: Company; IDBI Capital Research, Figures use Adjusted PAT Source: Company; IDBI Capital Research

Estimates

We estimate revenue growth of 13% over FY16-18E, primarily driven by robust scooter revenue growth (19% est.)

and motorcycle volume growth of 10% .

We expect a 15%/9% increase in domestic/export volumes. At higher operating leverage and new initiatives in

exports, we expect margins to expand to 7.8% in FY18E.

Stable fixed costs along with low margin base should drive Adj.EPS of 20% CAGR over FY16-18E.

Table: Segmental Mix – FY13-18E (%)

Sales Volumes Mix FY13 FY14 FY15 FY16 FY17E FY18E

Motorcycles - Domestic 27 28 26 26 27 27

Motorcycles - Exports 9 11 12 12 11 11

Total Motorcycle Share 37 38 38 38 38 38

Scooters - Domestic 21 22 27 29 30 31

Scooters - Exports 1 1 1 1 2 2

Total Scooter Share 22 23 28 30 32 33

Mopeds - Domestic 39 35 29 27 27 26

Mopeds - Exports 0 0 0 0 1 1

Total Moped Share 39 35 30 28 27 26

Total 2W Share 98 96 96 96 97 97

3-W - Domestic 1 1 1 1 1 1

3-W - Exports 2 3 4 4 3 3

Total 3W 2 4 4 4 3 3

Source: Company; IDBI Capital Research

0

20

40

60

80

FY03 FY05 FY07 FY09 FY11 FY13 FY15

RoEs (%) (3 Year Rolling AVG

Bajaj Hero TVS

0

2

4

6

8

10

12

14

16

18

FY03 FY05 FY07 FY09 FY11 FY13 FY15

Adj. PAT margins (%)

Bajaj Hero TVS

8

Company Outlook – TVS Motor Company

Fig.: We expect margins of 8+% by FY18 (Ex-BMW)

Fre:to be unlikely

Fig.: FY16-18E Volume Growth estimated at

Figur10.5%, realizations held back at 2.6% due to mix

Source: Company; IDBI Capital Research Source: Company; IDBI Capital Research

BMW Motorrad Tie-up holds potential

TVS alliance with BMW (BMW Motorrad)would provide incremental growth: Asper management, this tie-up

would will release its first product (expected to be the ~300cc BMW G 310 R) in H2FY17. All products would be

manufactured by TVS in Tamil Nadu, making TVS a contract manufacturer. Certain prodcuts could also be

launched under a TVS brand name (plans not yet finalized, but an “Akula 310” is likely to be launched first).

Technology benefits a postive:Over the long term, this would be a positve for TVS as it would gain technical

experience in higher-end motorcycles. products, particularly premium ones. While sales volumes are likely to

be small initially, the higher price tags (rumoured to be in the region of EUR 4,000-4,500) would amount to a

significant pie of revenue. The TVS launched products would also boost its brand image and product

perception.

Near Term ramp up a key monitorable:However, it remains to be seen whether the venture will be profitable

(EUR 20 Mn already invested for TVS), and at what margins TVS can operate on, given that its status in the

venture is akin to a contract manufacturer

Estimates: Given uncertainty as to timeline of ramp up and order flows, we conservatively estimate the JV

would be able to generate ~40,000 volumes (7K domestically, 33K via exports) in FY18E, based on broad

guidance and BMW’s market share in the segment. We conservatively estaimte Rs1.2bn in FY18E turnover

(Rs0.3mn blended realizations). Assuming a 4% PAT margin (JV is expected to have higher margins than stand

standalone basis), we estimate Rs1/Share in earnings from this JV. Given its potential for ramp up, we assign

Rs20/share in value for the venture.

70 79 100 112 127 144

5.8 6.0 6.06.7

7.27.8

-

20

40

60

80

100

120

140

160

0

2

4

6

8

10

FY13 FY14 FY15 FY16 FY17E FY18E

(%)

Net Sales (LHS) EBITDA Margin (RHS)

20.3 20.8 25.2 26.8 29.7 32.7

34 38

40 42 43 44

0

5

10

15

20

25

30

35

0

10

20

30

40

50

FY13 FY14 FY15 FY16 FY17E FY18E

Volumes (Mn Units) Realizations (RHS) (INR '000)

Company Outlook – TVS Motor Company

9

Valuation

Overall, TVS possesses decent fundamentals within the auto segment – RoEs of 24-26%, good growth potential on

the back of rising scooterization and the possibility of strong growth via the BMW alliance. However, there exist

certain key risks that could impact the stock. Continued weakness in the high realization exports market could

lower margins and reduce longer term growth visibility.

The 2W market (especially motorcycles) is also unlikely to grow at rates seen in the previous decade, given the

much higher penetration rate and the possibility of uptrending on the parts of consumers. TVS’ razor thin margins,

that have historically been at the ~6-7% mark, increase the volatility of earnings and uncertainty. Given market

expectations of significant margin expansion (FY18 consensus margins is at 8.3%), there remains little room for

error.

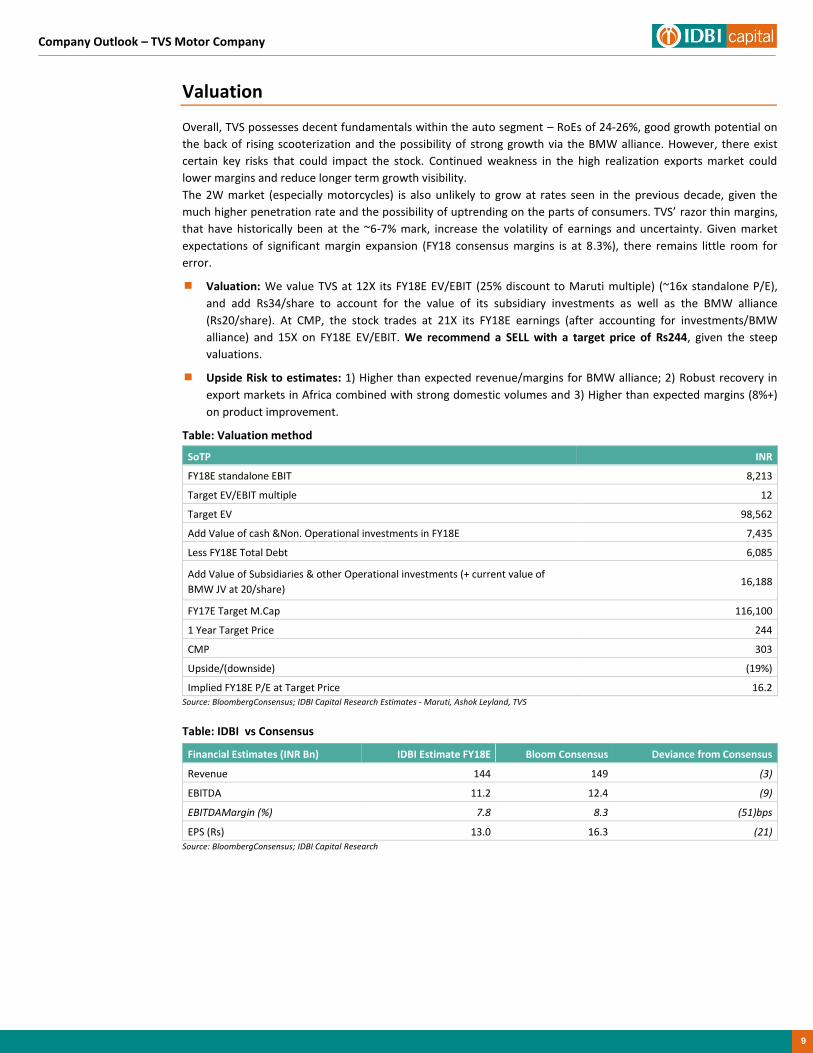

Valuation: We value TVS at 12X its FY18E EV/EBIT (25% discount to Maruti multiple) (~16x standalone P/E),

and add Rs34/share to account for the value of its subsidiary investments as well as the BMW alliance

(Rs20/share). At CMP, the stock trades at 21X its FY18E earnings (after accounting for investments/BMW

alliance) and 15X on FY18E EV/EBIT. We recommend a SELL with a target price of Rs244, given the steep

valuations.

Upside Risk to estimates: 1) Higher than expected revenue/margins for BMW alliance; 2) Robust recovery in

export markets in Africa combined with strong domestic volumes and 3) Higher than expected margins (8%+)

on product improvement.

Table: Valuation method

SoTP INR

FY18E standalone EBIT 8,213

Target EV/EBIT multiple 12

Target EV 98,562

Add Value of cash &Non. Operational investments in FY18E 7,435

Less FY18E Total Debt 6,085

Add Value of Subsidiaries & other Operational investments (+ current value of

BMW JV at 20/share) 16,188

FY17E Target M.Cap 116,100

1 Year Target Price 244

CMP 303

Upside/(downside) (19%)

Implied FY18E P/E at Target Price 16.2 Source: BloombergConsensus; IDBI Capital Research Estimates - Maruti, Ashok Leyland, TVS

Table: IDBI vs Consensus

Financial Estimates (INR Bn) IDBI Estimate FY18E Bloom Consensus Deviance from Consensus

Revenue 144 149 (3)

EBITDA 11.2 12.4 (9)

EBITDAMargin (%) 7.8 8.3 (51)bps

EPS (Rs) 13.0 16.3 (21) Source: BloombergConsensus; IDBI Capital Research

10

Company Outlook – TVS Motor Company

Relative Valuation

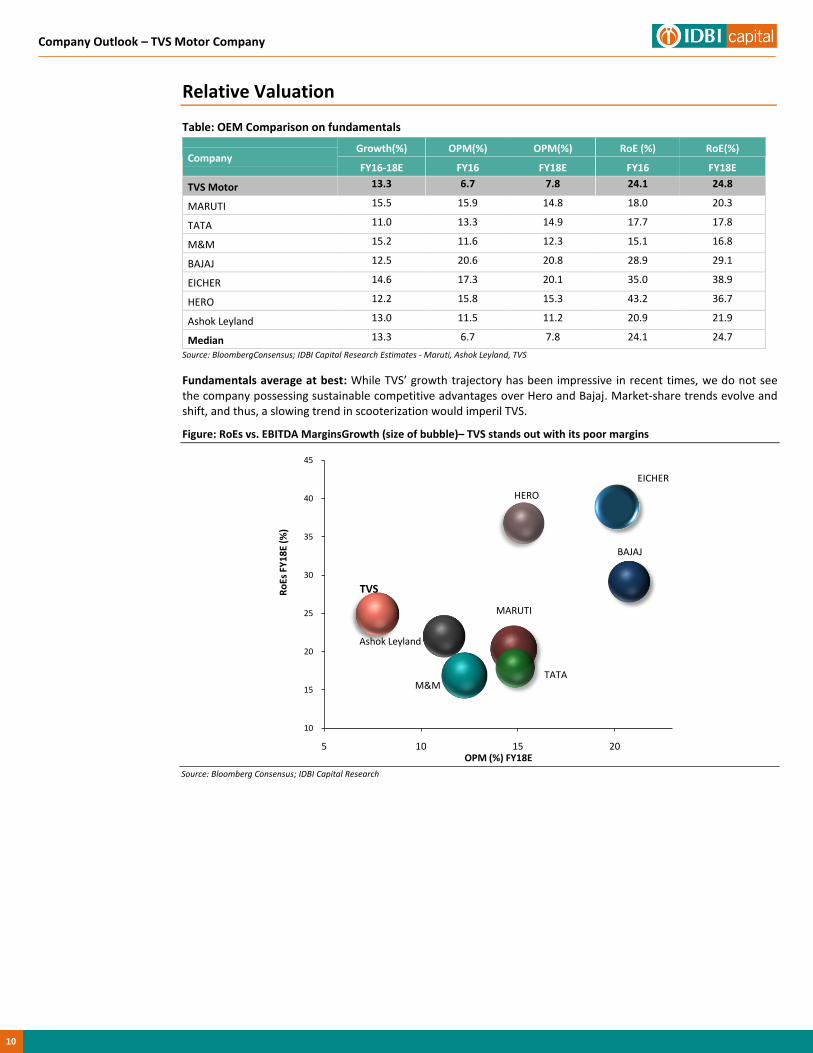

Table: OEM Comparison on fundamentals

Company Growth(%) OPM(%) OPM(%) RoE (%) RoE(%)

FY16-18E FY16 FY18E FY16 FY18E

TVS Motor 13.3 6.7 7.8 24.1 24.8

MARUTI 15.5 15.9 14.8 18.0 20.3

TATA 11.0 13.3 14.9 17.7 17.8

M&M 15.2 11.6 12.3 15.1 16.8

BAJAJ 12.5 20.6 20.8 28.9 29.1

EICHER 14.6 17.3 20.1 35.0 38.9

HERO 12.2 15.8 15.3 43.2 36.7

Ashok Leyland 13.0 11.5 11.2 20.9 21.9

Median 13.3 6.7 7.8 24.1 24.7

Source: BloombergConsensus; IDBI Capital Research Estimates - Maruti, Ashok Leyland, TVS

Fundamentals average at best: While TVS’ growth trajectory has been impressive in recent times, we do not see the company possessing sustainable competitive advantages over Hero and Bajaj. Market-share trends evolve and shift, and thus, a slowing trend in scooterization would imperil TVS.

Figure: RoEs vs. EBITDA MarginsGrowth (size of bubble)– TVS stands out with its poor margins

Source: Bloomberg Consensus; IDBI Capital Research

MARUTI

TATA

BAJAJ

EICHER

HERO

Ashok Leyland

TVS

M&M

10

15

20

25

30

35

40

45

5 10 15 20

Ro

Es F

Y1

8E

(%)

OPM (%) FY18E

Company Outlook – TVS Motor Company

11

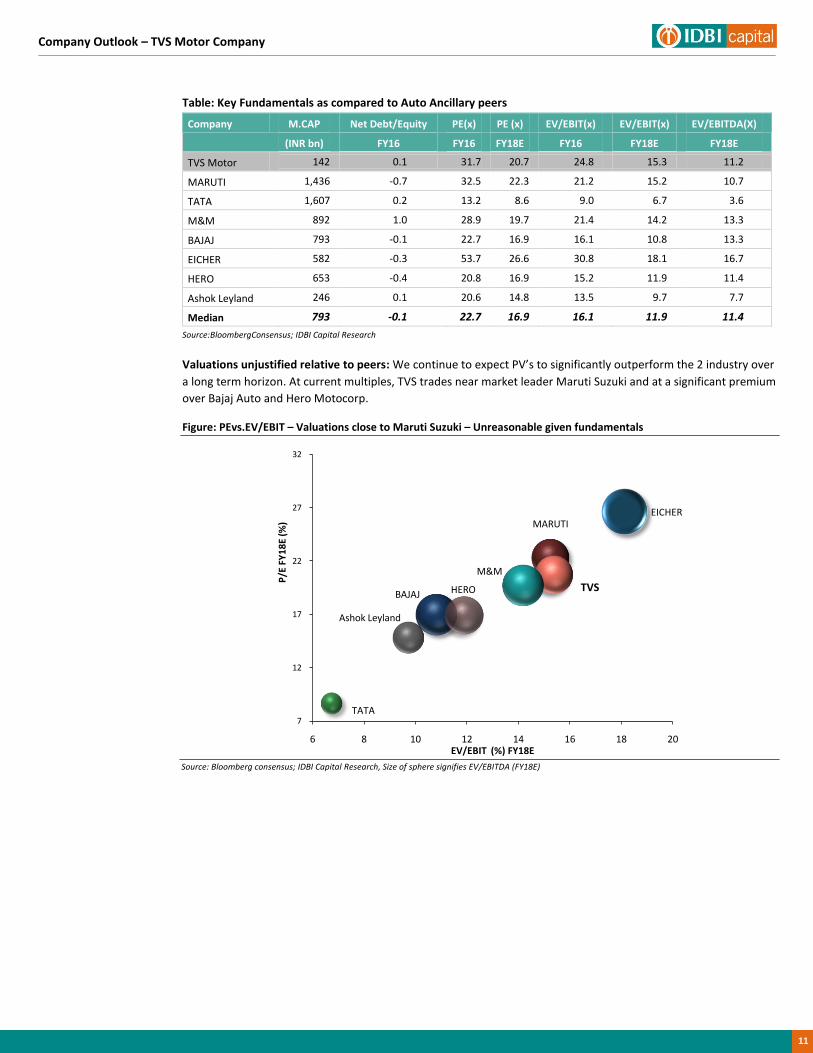

Table: Key Fundamentals as compared to Auto Ancillary peers

Company M.CAP Net Debt/Equity PE(x) PE (x) EV/EBIT(x) EV/EBIT(x) EV/EBITDA(X)

(INR bn) FY16 FY16 FY18E FY16 FY18E FY18E

TVS Motor 142 0.1 31.7 20.7 24.8 15.3 11.2

MARUTI 1,436 -0.7 32.5 22.3 21.2 15.2 10.7

TATA 1,607 0.2 13.2 8.6 9.0 6.7 3.6

M&M 892 1.0 28.9 19.7 21.4 14.2 13.3

BAJAJ 793 -0.1 22.7 16.9 16.1 10.8 13.3

EICHER 582 -0.3 53.7 26.6 30.8 18.1 16.7

HERO 653 -0.4 20.8 16.9 15.2 11.9 11.4

Ashok Leyland 246 0.1 20.6 14.8 13.5 9.7 7.7

Median 793 -0.1 22.7 16.9 16.1 11.9 11.4

Source:BloombergConsensus; IDBI Capital Research

Valuations unjustified relative to peers: We continue to expect PV’s to significantly outperform the 2 industry over

a long term horizon. At current multiples, TVS trades near market leader Maruti Suzuki and at a significant premium

over Bajaj Auto and Hero Motocorp.

Figure: PEvs.EV/EBIT – Valuations close to Maruti Suzuki – Unreasonable given fundamentals

Source: Bloomberg consensus; IDBI Capital Research, Size of sphere signifies EV/EBITDA (FY18E)

MARUTI

TATA

BAJAJ

EICHER

HERO

Ashok Leyland

TVS

M&M

7

12

17

22

27

32

6 8 10 12 14 16 18 20

P/E

FY

18

E (%

)

EV/EBIT (%) FY18E

12

Company Outlook – TVS Motor Company

Q1FY17 – Export volatility dents expectations

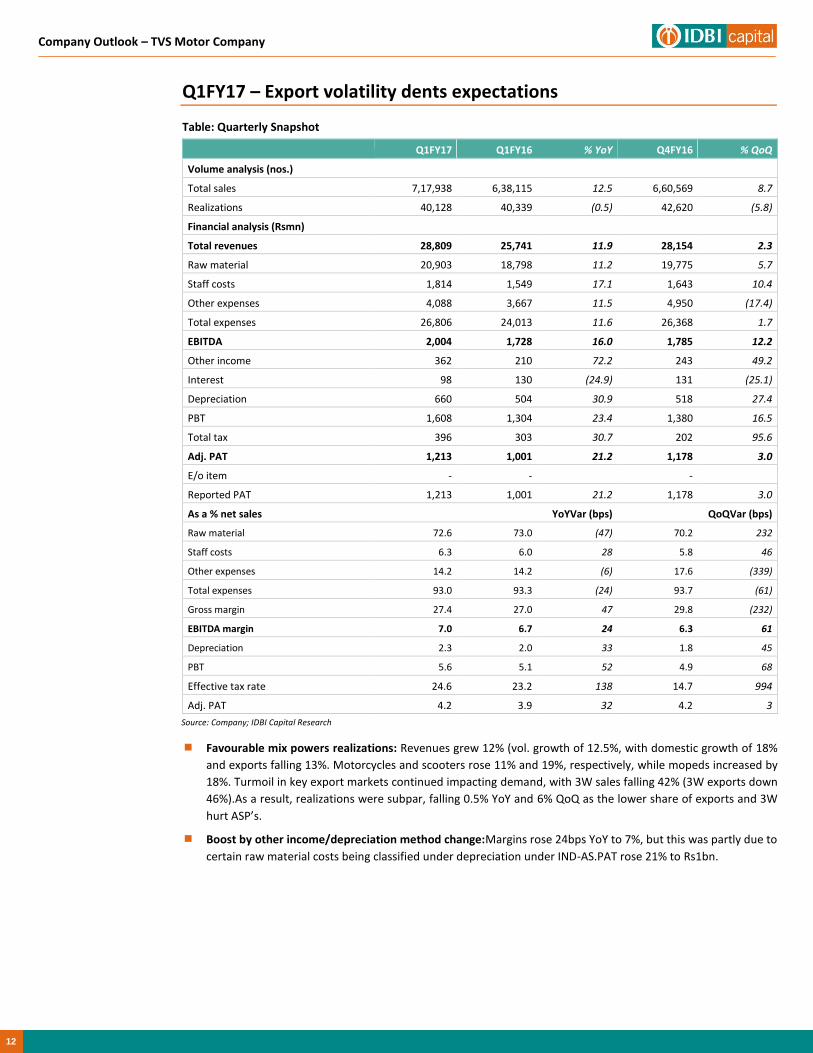

Table: Quarterly Snapshot

Q1FY17 Q1FY16 % YoY Q4FY16 % QoQ

Volume analysis (nos.)

Total sales 7,17,938 6,38,115 12.5 6,60,569 8.7

Realizations 40,128 40,339 (0.5) 42,620 (5.8)

Financial analysis (Rsmn)

Total revenues 28,809 25,741 11.9 28,154 2.3

Raw material 20,903 18,798 11.2 19,775 5.7

Staff costs 1,814 1,549 17.1 1,643 10.4

Other expenses 4,088 3,667 11.5 4,950 (17.4)

Total expenses 26,806 24,013 11.6 26,368 1.7

EBITDA 2,004 1,728 16.0 1,785 12.2

Other income 362 210 72.2 243 49.2

Interest 98 130 (24.9) 131 (25.1)

Depreciation 660 504 30.9 518 27.4

PBT 1,608 1,304 23.4 1,380 16.5

Total tax 396 303 30.7 202 95.6

Adj. PAT 1,213 1,001 21.2 1,178 3.0

E/o item - -

-

Reported PAT 1,213 1,001 21.2 1,178 3.0

As a % net sales

YoYVar (bps)

QoQVar (bps)

Raw material 72.6 73.0 (47) 70.2 232

Staff costs 6.3 6.0 28 5.8 46

Other expenses 14.2 14.2 (6) 17.6 (339)

Total expenses 93.0 93.3 (24) 93.7 (61)

Gross margin 27.4 27.0 47 29.8 (232)

EBITDA margin 7.0 6.7 24 6.3 61

Depreciation 2.3 2.0 33 1.8 45

PBT 5.6 5.1 52 4.9 68

Effective tax rate 24.6 23.2 138 14.7 994

Adj. PAT 4.2 3.9 32 4.2 3

Source: Company; IDBI Capital Research

Favourable mix powers realizations: Revenues grew 12% (vol. growth of 12.5%, with domestic growth of 18%

and exports falling 13%. Motorcycles and scooters rose 11% and 19%, respectively, while mopeds increased by

18%. Turmoil in key export markets continued impacting demand, with 3W sales falling 42% (3W exports down

46%).As a result, realizations were subpar, falling 0.5% YoY and 6% QoQ as the lower share of exports and 3W

hurt ASP’s.

Boost by other income/depreciation method change:Margins rose 24bps YoY to 7%, but this was partly due to

certain raw material costs being classified under depreciation under IND-AS.PAT rose 21% to Rs1bn.

Company Outlook – TVS Motor Company

13

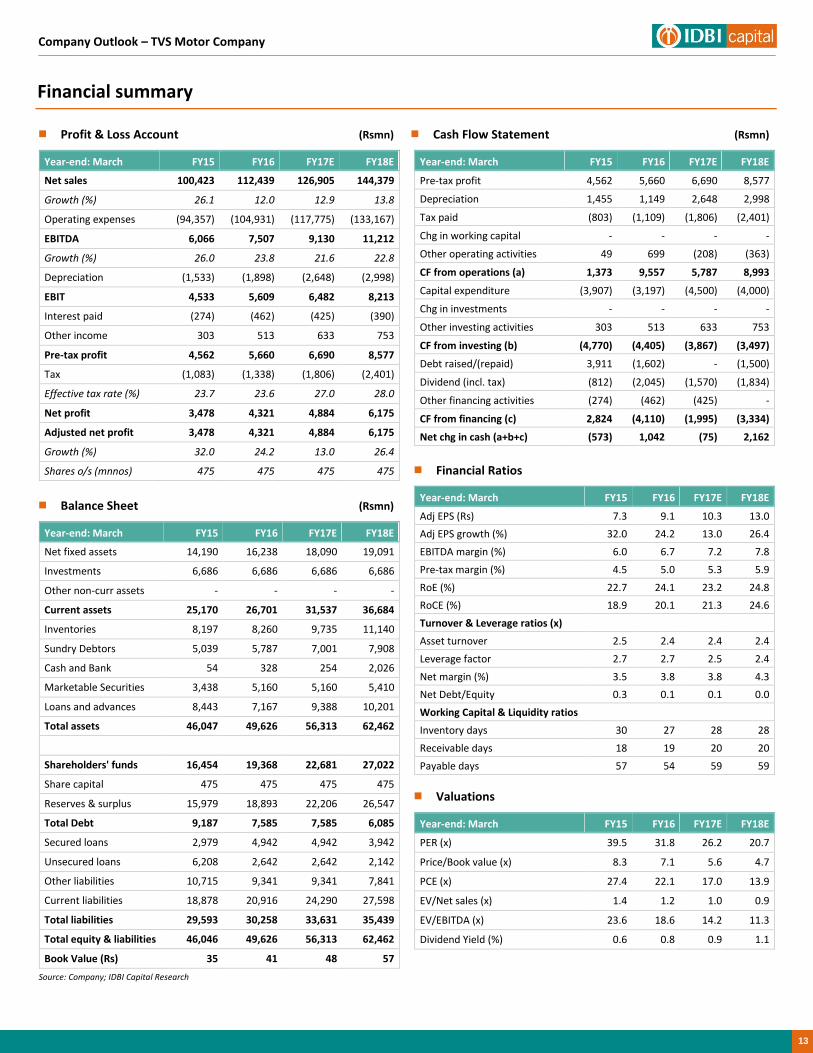

Financial summary

Profit & Loss Account (Rsmn)

Year-end: March FY15 FY16 FY17E FY18E

Net sales 100,423 112,439 126,905 144,379

Growth (%) 26.1 12.0 12.9 13.8

Operating expenses (94,357) (104,931) (117,775) (133,167)

EBITDA 6,066 7,507 9,130 11,212

Growth (%) 26.0 23.8 21.6 22.8

Depreciation (1,533) (1,898) (2,648) (2,998)

EBIT 4,533 5,609 6,482 8,213

Interest paid (274) (462) (425) (390)

Other income 303 513 633 753

Pre-tax profit 4,562 5,660 6,690 8,577

Tax (1,083) (1,338) (1,806) (2,401)

Effective tax rate (%) 23.7 23.6 27.0 28.0

Net profit 3,478 4,321 4,884 6,175

Adjusted net profit 3,478 4,321 4,884 6,175

Growth (%) 32.0 24.2 13.0 26.4

Shares o/s (mnnos) 475 475 475 475

Balance Sheet (Rsmn)

Year-end: March FY15 FY16 FY17E FY18E

Net fixed assets 14,190 16,238 18,090 19,091

Investments 6,686 6,686 6,686 6,686

Other non-curr assets - - - -

Current assets 25,170 26,701 31,537 36,684

Inventories 8,197 8,260 9,735 11,140

Sundry Debtors 5,039 5,787 7,001 7,908

Cash and Bank 54 328 254 2,026

Marketable Securities 3,438 5,160 5,160 5,410

Loans and advances 8,443 7,167 9,388 10,201

Total assets 46,047 49,626 56,313 62,462

Shareholders' funds 16,454 19,368 22,681 27,022

Share capital 475 475 475 475

Reserves & surplus 15,979 18,893 22,206 26,547

Total Debt 9,187 7,585 7,585 6,085

Secured loans 2,979 4,942 4,942 3,942

Unsecured loans 6,208 2,642 2,642 2,142

Other liabilities 10,715 9,341 9,341 7,841

Current liabilities 18,878 20,916 24,290 27,598

Total liabilities 29,593 30,258 33,631 35,439

Total equity & liabilities 46,046 49,626 56,313 62,462

Book Value (Rs) 35 41 48 57

Source: Company; IDBI Capital Research

Cash Flow Statement (Rsmn)

Year-end: March FY15 FY16 FY17E FY18E

Pre-tax profit 4,562 5,660 6,690 8,577

Depreciation 1,455 1,149 2,648 2,998

Tax paid (803) (1,109) (1,806) (2,401)

Chg in working capital - - - -

Other operating activities 49 699 (208) (363)

CF from operations (a) 1,373 9,557 5,787 8,993

Capital expenditure (3,907) (3,197) (4,500) (4,000)

Chg in investments - - - -

Other investing activities 303 513 633 753

CF from investing (b) (4,770) (4,405) (3,867) (3,497)

Debt raised/(repaid) 3,911 (1,602) - (1,500)

Dividend (incl. tax) (812) (2,045) (1,570) (1,834)

Other financing activities (274) (462) (425) -

CF from financing (c) 2,824 (4,110) (1,995) (3,334)

Net chg in cash (a+b+c) (573) 1,042 (75) 2,162

Financial Ratios

Year-end: March FY15 FY16 FY17E FY18E

Adj EPS (Rs) 7.3 9.1 10.3 13.0

Adj EPS growth (%) 32.0 24.2 13.0 26.4

EBITDA margin (%) 6.0 6.7 7.2 7.8

Pre-tax margin (%) 4.5 5.0 5.3 5.9

RoE (%) 22.7 24.1 23.2 24.8

RoCE (%) 18.9 20.1 21.3 24.6

Turnover & Leverage ratios (x)

Asset turnover 2.5 2.4 2.4 2.4

Leverage factor 2.7 2.7 2.5 2.4

Net margin (%) 3.5 3.8 3.8 4.3

Net Debt/Equity 0.3 0.1 0.1 0.0

Working Capital & Liquidity ratios

Inventory days 30 27 28 28

Receivable days 18 19 20 20

Payable days 57 54 59 59

Valuations

Year-end: March FY15 FY16 FY17E FY18E

PER (x) 39.5 31.8 26.2 20.7

Price/Book value (x) 8.3 7.1 5.6 4.7

PCE (x) 27.4 22.1 17.0 13.9

EV/Net sales (x) 1.4 1.2 1.0 0.9

EV/EBITDA (x) 23.6 18.6 14.2 11.3

Dividend Yield (%) 0.6 0.8 0.9 1.1

14

Company Outlook – TVS Motor Company

Notes

Dealing (91-22) 6637 1150 [email protected]

Key to Ratings

Stocks:

BUY: Absolute return of 15% and above; ACCUMULATE: 5% to 15%; HOLD: Upto ±5%; REDUCE: -5% to -15%; SELL: -15% and below.

IDBI Capital Markets&Securities Ltd. (Formerly known as “IDBI Capital Market Services Ltd.”) Equity Research Desk

3rd Floor, Mafatlal Centre, Nariman Point, Mumbai – 400 021. Phones: (91-22) 4322 1212; Fax: (91-22) 2285 0785; Email: [email protected]

SEBI Registration: BSE & NSE (Cash & FO) – INZ000007237, NSDL – IN-DP-NSDL-12-96, Research – INH000002459, CIN – U65990MH1993GOI075578

Compliance Officer: Christina D’souza; Email: [email protected]; Telephone: (91-22) 4322 1212 Disclaimer This document has been prepared by IDBI Capital Markets & Securities Ltd. (IDBI Capital) and is meant for the recipient only for use as intended and not for circulation. This document should not

be reproduced or copied or made available to others. No person associated with IDBI Capital is obligated to call or initiate contact with you for the purposes of elaborating or following up on the

information contained in this document.

Recipients may not receive this report at the same time as other recipients. IDBI Capital will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is from the public domain or sources believed to be reliable. While reasonable care has been taken to ensure that information given is at the time believed to be

fair and correct and opinions based thereupon are reasonable, due to the very nature of research it cannot be warranted or represented that it is accurate or complete a nd it should not be relied

upon as such. In so far as this report includes current or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.

Opinions expressed are current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable basis, the information discussed in this material, IDBI Capital,

its directors, employees are under no obligation to update or keep the information current. Further there may be regulatory, compliance, or other reasons that prevent us from doing so.

Prospective investors and others are cautioned that any forward-looking statements are not predictions and may be subject to change without notice.

IDBI Capital, its directors and employees and any person connected with it, will not in any way be responsible for the contents of this report or for any losses, costs, expenses, charges, including

notional losses/lost opportunities incurred by a recipient as a result of acting or non acting on any information/material contained in the report.

This is not an offer to sell or a solicitation to buy any securities or an attempt to influence the opinion or behaviour of investors or recipients or provide any investment/tax advice.

This report is for information only and has not been prepared based on specific investment objectives. The securities discussed in this report may not be suitable for all investors. Investors must

make their own investment decision based on their own investment objectives, goals and financial position and based on their own analysis.

Trading in stocks, stock derivatives, and other securities is inherently risky and the recipient agrees to assume complete and full responsibility for the outcomes of all trading decisions that the

recipient makes, including but not limited to loss of capital.

Opinions, projections and estimates in this report solely constitute the current judgment of the author of this report as of the date of this report and do not in any way reflect the views of IDBI

Capital, its directors, officers, or employees.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such

distribution, publication, availability or use would be contrary to law, regulation or which would subject IDBI Capital and affiliates to any registration or licensing requirement within such

jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are

required to inform themselves of and to observe such restriction.

IDBI Capital, its directors or employees or affiliates, may from time to time, have positions in, or options on, and buy and sell securities referred to herein. IDBI Capital or its affiliates, during the

normal course of business, from time to time, may solicit from or perform investment banking or other services for any company mentioned in this document or their connected persons or be

engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or

their affiliate companies or act as advisor or lender / borrower to such company(ies)/affiliate companies or have other potential conflict of interest.

This report may provide hyperlinks to other websites. Except to the extent to which the report refers to the website of IDBI Capital, IDBI Capital states that it has not reviewed the linked site and

takes no responsibility for the content contained in such other websites. Accessing such websites shall be at recipient's own risk.

E-mail is not a secure method of communication. IDBI Capital Markets & Securities Ltd. cannot accept responsibility for the accuracy or completeness of any e-mail message or any attachment(s).

This transmission could contain viruses, be corrupted, destroyed, incomplete, intercepted, lost or arrive late. IDBI Capital, its directors or employees or affiliates accept no liability for any damage

caused, directly or indirectly, by this email.

Company Outlook – TVS Motor Company

15

Disclosures

I, Pranoy Kurian, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is

or will be directly or indirectly related to the specific recommendations or views expressed in this report.

IDBI Capital Markets & Securities Ltd. (“IDBI Capital”) and its associates (IDBI Capital is a wholly owned subsidiary of IDBI Bank Ltd. IDBI Asset Management Ltd., IDBI MF Trustee Company Ltd. and

IDBI Intech Ltd.) are a full-service, banking, integrated investment banking, investment management, brokerage and financing group. We along with our affiliates are leading underwriter of

securities and participants in virtually all securities trading markets in India. We and our affiliates have investment banking and other business relationships with a significant percentage of the

companies covered by our Research Department. Investors should assume that IDBI Capital and/or its affiliates are seeking or will seek investment banking or other business from the company or

companies that are the subject of this material. IDBI Capital generally prohibits its analysts, persons reporting to analysts, and their dependant family members having a financial conflict of

interest in the securities or derivatives of any companies that the analysts cover. Additionally, IDBI Capital Markets & Securities Ltd. generally prohibits its analysts and persons reporting to

analysts from serving as an officer, director, or advisory board member of any companies that the analysts cover. Our salespeople, t raders, and other professionals may provide oral or written

market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make

investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things,

may give rise to real or potential conflicts of interest. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is

provided herein.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. We are not soliciting

any action based on this material. It is for the general information of clients of IDBI Capital. It does not constitute a personal recommendation or take into account the particular investment

objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this material, clients should consider whether it is suitable for their particular

circumstances and, if necessary, seek professional advice. The price and value of the investments referred to in this materia l and the income from them may go down as well as up, and investors

may realize losses on any investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur.

We and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance of this material, may from time to time have “long” or “short” positions in, act as

principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein. For the purpose of calculating whether IDBI Capital Markets & Securities Ltd. and its affiliates

holds beneficially owns or controls, including the right to vote for directors, 1% of more of the equity shares of the subjec t issuer of a research report, the holdings does not include accounts

managed by IDBI Asset Management Company/ IDBI Mutual Fund.

IDBI Capital Markets & Securities Ltd. established in 1993, is a wholly owned subsidiary of IDBI Bank Limited. IDBI Capital Markets & Securities Ltd. is one of India’s leading brokerage and

distribution house.

IDBI Capital Markets & Securities Ltd. is a corporate trading and clearing member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE), and a dealer of the OTC

Exchange of India (OTCEI) and is also a SEBI registered Merchant Banker and Portfolio Manager. Our businesses include stock broking, services rendered in connection with distribution of primary

market issues and financial products like merchant banking, depository services and Portfolio Management.

IDBI Capital Markets & Securities Ltd. is also a depository participant with National Securities Depository Limited (NSDL) and is also a Mutual Fund Advisor registered with Association of Mutual

Funds in India (AMFI)

We hereby declare that our activities were neither suspended nor we have materially defaulted with any stock exchange authority with whom we are registered in last five years. However SEBI,

Exchanges and Depositories have conducted the routine inspection and based on their observations have issued advise letters or levied minor penalty on IDBI Capital for certain operational

deviations. We have not been debarred from doing business by any Stock Exchange / SEBI or any other authorities; nor has our certificate of registration been cancelled by SEBI at any point of

time.

We offer our research services to primarily institutional investors and their employees, directors , fund managers, advisors who are registered with us.

The Research Analyst has not served as an officer, director or employee of Subject Company.

We or our associates may have received compensation from the subject company in the past 12 months. We or our associates may have managed or co-managed public offering of securities for

the subject company in the past 12 months. We or our associates may have received compensation for investment banking or merchant banking or brokerage services from the subject company

in the past 12 months. We or our associates may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the

subject company in the past 12 months. We or our associates may have received any compensation or other benefits from the Subject Company or third party in connection with the research

report.

Research Analyst or his/her relative’s may have financial interest in the subject company. IDBI Capital Markets & Securities Ltd. or its associates may have financial interest in the subject company.

Research Analyst or his/her relatives does not have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of

publication of Research Report.IDBI Capital Markets & Securities Ltd. or its associates may have actual/beneficial ownership of 1% or more securities of the subject company at the end of the

month immediately preceding the date of publication of Research Report. The Subject Company may have been a client during twelve months preceding the date of distribution of the research

report.

Price history of the daily closing price of the securities covered in this note is available at nseindia.com and economictimes.indiatimes.com/markets/stocks/stock-quotes.