TVS CREDIT SERVICES · PDF fileTVS CREDIT SERVICES LIMITED 2 Annual Report 2014-15 Bankers...

68

Transcript of TVS CREDIT SERVICES · PDF fileTVS CREDIT SERVICES LIMITED 2 Annual Report 2014-15 Bankers...

TVS CREDIT SERVICES LIMITED

1 Annual Report 2014-15

Board of Directors

Mr. Venu Srinivasan, ChairmanMr. Anupam Theraja, Whole Time DirectorMr. T.K. BalajiMr. R.RamakrishnanMr. Sudarshan VenuMr. S. SanthanakrishnanMr. P. SivaramMr. K.N. RadhakrishnanMr. V. Srinivasa RanganMs. Sasikala Varadhachari

Audit Committee

Mr. S. SanthanakrishnanMr. R. RamakrishnanMr. K.N. RadhakrishnanMr. V. Srinivasa Rangan

Nomination and Remuneration Committee

Mr. R. RamakrishnanMr. K.N. RadhakrishnanMr. V. Srinivasa Rangan

Risk Management Committee

Mr. Anupam TherajaMr. S. SanthanakrishnanMr. R. Ramakrishnan

Asset Liability CommitteeMr. Anupam TherajaMr. R. RamakrishnanMr. S. SanthanakrishnanMr. Sudarshan VenuMr. G. VenkatramanMr. V. GopalakrishnanMr. M. Kalyanaraman

Corporate Social Responsibility Committee

Mr. Venu SrinivasanMr. R. RamakrishnanMr. K.N. Radhakrishnan

Chief Executive OfficerMr. G. Venkatraman

Registered Office

“Jayalakshmi Estates”29, Haddows RoadNungambakkamChennai 600 006Phone : 91-44-28286500Fax No. : 91-44-28286570

AuditorsMr. V. Sankar Aiyar & Co.Chartered AccountantsMumbai 2-C Court Chambers,35, New Marine Lines,Mumbai- 400 020.

TVS CREDIT SERVICES LIMITED

2 Annual Report 2014-15

Bankers

State Bank of IndiaBank of BarodaState Bank of MysoreCentral Bank of IndiaUCO BankSouth Indian Bank LimitedCorporation BankIndian BankOriental Bank of CommercePunjab and Sind BankIndusind Bank LimitedCanara BankSyndicate BankIDBI Bank LimitedKarnataka Bank LimitedDCB Bank LimitedBank of IndiaUnion Bank of IndiaKarur Vysya Bank LimitedICICI Bank LimitedAxis Bank LimitedHDFC Bank Limited

Financial Institution

Housing Development Finance CorporatiionLimited

TVS CREDIT SERVICES LIMITED

3 Annual Report 2014-15

Contents Page No.

Notice 4

Director’s Report 10

Auditor’s Report 24

Balance Sheet 28

Profit and Loss Account 29

Cash Flow Statement 30

Schedules 32

Additional Notes 49

TVS CREDIT SERVICES LIMITED

4 Annual Report 2014-15

NOTICE TO THE SHAREHOLDERSNOTICE is hereby given that the seventh annualgeneral meeting of the shareholders of theCompany will be held at the Registered Office ofthe Company at No. 29, Haddows Road, Chennai600 006 on Wednesday, the 29th July 2015 at9.30 a.m. to transact the following business:

ORDINARY BUSINESS(1) To consider and if thought fit, to pass with

or without modification, the followingresolution as an ordinary resolution.

“RESOLVED THAT the audited balance sheetas at 31st March, 2015, the statement of profitand loss, notes forming part thereof, the cashflow statement for the year ended on that date,together with the directors’ report and theauditors’ report thereon as circulated to themembers and presented to the meeting beand the same are hereby approved andadopted.”

(2) To consider and if thought fit, to pass withor without modification, the followingresolution as an ordinary resolution.

“RESOLVED THAT Mr K N Radhakrishnan(holding DIN 02599393), director, who retiresby rotation and being eligible, offers himselffor re-appointment, be and is hereby re-appointed as a director of the Company.”

(3) To consider and if thought fit, to pass withor without modification, the followingresolution as an ordinary resolution.“RESOLVED THAT Mr P Sivaram (holdingDIN 00002010), director, who retires byrotation and being eligible, offers himselffor re-appointment, be and is herebyre-appointed as a director of the Company.”

(4) To consider and if thought fit to pass withor without modification the followingresolution as an ordinary resolution.“RESOLVED THAT the re-appointment ofM/s V Sankar Aiyar & Co., Chartered

Accountants, Mumbai, having FirmRegistration No. 109208W allotted by TheInstitute of Chartered Accountants of India,as statutory auditors of the Company to holdoffice for the second year in the second termof five years from the conclusion of theensuing annual general meeting, till theconclusion of the next annual generalmeeting, as recommended by the auditcommittee and approved by the board ofdirectors of the Company, in terms of Section139 of the Companies Act, 2013 read withthe Companies (Audit and Auditors) Rules,2014 on such remuneration, as may bemutually agreed upon between the board ofdirectors of the Company and the StatutoryAuditors in addition to reimbursement ofservice tax, travelling and out-of-pocketexpenses, be and is hereby ratified.”

“RESOLVED THAT the rotation of partner,namely Mr S Venkatraman, (MembershipNo. 34319) Partner, M/s. V Sankar Aiyar & Co.,Chartered Accountants, Mumbai, statutoryauditors of the Company, for auditing theaccounts of the Company for three yearscommencing from the conclusion of the ensuingannual general meeting, during the term of thetenure of their firm, as statutory auditors of theCompany, be and is hereby approved.”

SPECIAL BUSINESS(5) To consider and if thought fit to pass with

or without modification the followingresolution as an ordinary resolution.

“RESOLVED Mr Sudarshan Venu (holdingDIN 03601690), who was appointed as anadditional director and who holds office up tothe date of this annual general meeting, interms of Section 161 read with Section 149of the Companies Act, 2013, read with theCompanies (Appointment and Qualificationof Directors) Rules, 2014, be and is herebyappointed as a non-executive and nonindependent director of the Company, liableto retire by rotation.”

TVS CREDIT SERVICES LIMITED

5 Annual Report 2014-15

(6) To consider and if thought fit to pass withor without modification the followingresolution as a special resolution.

“RESOLVED THAT, subject to the provisionsof Sections 149, 150, 152, 160 and otherapplicable provisions of the Companies Act,2013 and the rules made thereunder(including any statutory modification(s)thereof for the time being in force) read withSchedule IV to the Companies Act, 2013,Mr S Santhanakrishnan (holding DIN00005069), be and is hereby appointed as anon-executive and independent director of theCompany, to hold office for the second termof three consecutive years from theconclusion of this annual general meeting andto receive remuneration by way of fees,reimbursement of expenses for participationin the meetings of the board and / orcommittees and profit related commission, ifany, in terms of applicable provisions of theCompanies Act, 2013 as determined by theboard from time to time .”

(7) To consider and if thought fit to pass withor without modification the followingresolution as an ordinary resolution.

“RESOLVED THAT, on the recommendationof the nomination and remunerationcommittee of directors and subject to theprovisions of Section 197, 198 and otherapplicable provisions, if any, of the CompaniesAct, 2013 and the rules made there-under,all non-executive directors (NEDs) of theCompany be paid, (in addition to sitting feesfor attending the meetings of the board or ofa committee thereof and travelling and stayexpenses) such sum as commission payable,at such intervals, for each such NED of theCompany, as may be decided and determinedby the board of directors of the Company, from

time to time, for each financial year, for aperiod of five years commencing from1st April 2015, within the overall limit, so asnot to exceed in aggregate 1% of the netprofits of the Company, calculated inaccordance with the provisions of section 198of the Companies Act, 2013.”

BY ORDER OF THE BOARD

Place : Chennai K SridharDate : June 23, 2015 Company Secretary

NOTES:1. A member entitled to attend and vote at the

meeting is entitled to appoint one or moreproxies to attend and vote instead of himselfand the Proxy or Proxies so appointed neednot be a member or members, as the casemay be, of the Company. The instrumentappointing the Proxy and the power ofattorney or other authority, if any, under whichit is signed or a notarially certified copy of thatpower of attorney or other authority shall beregistered office of the Company, not laterthan 48 hours before the time fixed for holdingthe meeting. A person shall not act as a Proxyfor more than 50 members and holding inaggregate not more than ten percent of thetotal voting share capital of the Company.However, a single person may act as a Proxyfor a member holding more than ten percentof the total voting share capital of theCompany provided that such person shall notact as a Proxy for any other person.

2. The explanatory statement pursuant toSection 102(1) of the Companies Act, 2013in respect of the special businesses as setout in the Notice is annexed hereto.

Encl: Proxy form

TVS CREDIT SERVICES LIMITED

6 Annual Report 2014-15

Annexure to Notice dated 23rd June 2015

EXPLANATORY STATEMENTPURSUANT TO SECTION 102 (1) OFTHE COMPANIES ACT, 2013

The following explanatory statement sets out allmaterial facts relating to the special businessmentioned in the accompanying notice dated23rd June 2015 and shall be taken as forming partof the Notice.

Item No. 5

Mr Sudarshan Venu, who was appointed asdirector on 31st January 2013, resigned from theboard effective 27th March 2015 in compliancewith the directions on age restrictions imposedby the Reserve Bank of India (RBI) through arevised regulatory framework for non-bankingfinance companies (NBFCs) issued vide DNBR(PD) CC.No.002/ 03.10.001/ 2014-15 datedNovember 10, 2014 (the Framework) CorporateGovernance and Disclosure norms.

Subsequently, the RBI vide NBFCs vide its circularNo. DNBR (PD) CC. No. 029/ 03.10.001/2014-15 dated April 10, 2015 removed such agerestrictions on appointment of directors byNBFCs.

In view of this removal of age restrictions, theboard decided to co-opt him as additional, non-executive and non-independent director of theCompany effective 23rd June 2015, especiallyafter considering his contributions to the growthof the Company and after the recommendationof Nomination and Remuneration Committee ofDirectors (NRC).

NRC also took into consideration his qualification,expertise, track record, integrity and other ‘fit andproper’ person criteria, besides other attributesto become a director of the Company, in terms ofthe relevant provisions of the Companies Act,2013 (the Act 2013) and the guidelines of RBI.

Both the NRC and the board were of the opinion,after evaluation of his expertise in the automotive

industry, besides his experience in corporategovernance issues, performance, other attributesand business practices, that his continuedassociation would be of immense benefit to theCompany and desirable to avail his services as adirector.

In terms of Section 161 read with Section 152 ofthe Act 2013, he will vacate office at this AGMand be eligible to be appointed at this AGM, asrecommended by the NRC and the board.

The Company has received from him a consentin writing to act as a Director in Form DIR-2,intimation to the effect that he is not disqualifiedto be appointed as a Director in other companiesin Form DIR-8 and a declaration and undertakingand a deed of covenant as per the guidelines ofRBI.

Accordingly, the Board recommends theresolution, as set out in item No.5, in relation toappointment of Mr Sudarshan Venu as directorfor approval by the shareholders of the Company.

A notice has been received from a member underSection 160 of the Act, 2013, along with a requisitedeposit signifying its intention to propose thecandidature of Mr Sudarshan Venu and to movethe resolution set out in Item No. 5 of this notice.

Except Mr Sudarshan Venu, being the appointeeand Mr Venu Srinivasan, chairman, being hisrelative, none of the other directors or keymanagerial personnel of the Company or theirrelatives is concerned or interested, financially orotherwise, in the resolution as set out in ItemNo. 5.

Item No. 6

As explained in item No.5 of the agenda,Mr S Santhanakrishnan, a non-executive andindependent director (NID) of the Company alsoresigned from the board effective 27th March2015, in compliance with the directions on agerestrictions imposed by the Reserve Bank of India(RBI).

TVS CREDIT SERVICES LIMITED

7 Annual Report 2014-15

In view of the subsequent removal of agerestrictions by RBI, the board also decided torecommend his appointment as NID for thesecond term of three years, especially afterconsidering his contributions to the growth of theCompany and after the recommendation ofNomination and Remuneration Committee ofDirectors (NRC).

Both the NRC and the board were of the opinion,after evaluation of his expertise in the automotiveindustry, besides his experience in corporategovernance issues, performance, other attributesand business practices, that his continuedassociation would be of immense benefit to theCompany and desirable to avail his services asan independent director of the Company.

NRC also took into consideration his qualification,expertise, track record, integrity and other ‘fit andproper’ person criteria, besides other attributesto become a director of the Company, in terms ofthe relevant provisions of the Act 2013 and theguidelines of RBI.

In the opinion of the Board, Mr S Santhana-krishnan fulfils the conditions specified in the Act,2013 and Rules made there-under to beappointed as an ID of the Company and isindependent of the Company’s Management.

The Company has received from him a consentin writing to act as Director in Form DIR-2,intimation to the effect that he is not disqualifiedto be appointed as a Director in other companiesin Form DIR-8 and a declaration in writing to theeffect that he meets the criteria of independenceas provided in sub-section 6 of Section 149 ofthe Act, 2013, besides a declaration andundertaking and a deed of covenant as per theguidelines of RBI.

In terms of the applicable provisions of the Act2013, the appointment of IDs of the Companywill be required to be approved at a generalmeeting of the shareholders.

The Company will formalize his appointment asNE-ID, if appointed by the shareholders, setting

out the terms and conditions as stipulated inSchedule IV to the Act, 2013.

Such letter of appointment will also be availablefor inspection without any fee by the members atthe Registered Office of the Company, duringnormal business hours on any working day,excluding Saturdays and shall also be uploadedon the website of the Company at Website:www.tvscredit.co.in.

A notice has been received from a member underSection 160 of the Act, 2013, along with a requisitedeposit signifying its intention to propose thecandidature of Mr S Santhanakrishnan and tomove the resolution set out in Item No. 6 of thisnotice.

Accordingly, the Board recommends the specialresolution, as set out in Item No. 6, in relation toappointment of Mr S Santhanakrishnan as anindependent director for approval by theshareholders of the Company.

None of the directors or key managerial personnelof the Company or their relatives is concerned orinterested, financially or otherwise, in theresolution as set out in Item No. 6.

Item No. 7In terms of Section 197 of the Act 2013, thedirectors, who are not in the whole-timeemployment of the Company, (Non-executivedirectors (NEDs) would be eligible to receiveremuneration, not exceeding 1% of the net profitsof the Company, in such manner, for each suchNED, as may be decided and determined by theboard of directors of the Company, from time totime, for each financial year. Presently, thedirectors do not draw any remuneration.

The board was of the opinion that NEDs wouldhave to be recognized and compensated for theirsignificant contributions toward achieving thepresent growth of the Company, besides for thetime spent by them in deliberating the operationaland other issues, their increased involvement andparticipation in meetings of various committees

TVS CREDIT SERVICES LIMITED

8 Annual Report 2014-15

and the board for advising the managing of theCompany, their increased role and functions andenhanced responsibility, consequent to theintroduction of various compliance requirementsunder the Act 2013 and RBI regulations, from timeto time, and the Company also derives substantialbenefit through their expertise and advice.

Any payment by way of remuneration to NEDswould require an approval of the shareholders ofthe Company and such approval would be validfor a period of five years as per the provisions ofthe Act 2013.

The board, therefore, decided to payremuneration by way of commission to NEDs notexceeding 1% of the net profits of the Companyin such manner, as the board may determine,from time to time, for each financial year, withinthe overall limit approved by the shareholders.

Hence, the board, in its meeting held on 23rd June2015, approved this proposal on the

recommendation of the Nomination andRemuneration Committee of directors (NRC) toseek the approval of the shareholders for paymentof remuneration for a period of five yearscommencing from 1st April 2015 to such NEDsfor each financial year and, therefore,recommends the ordinary resolution, as set outin Item No.7 of this Notice.

Except the non-executive directors, none of theexecutive directors or Key Managerial Personnelof the Company or their relatives is not concernedor interested, financially or otherwise, in theresolution set out at Item No.7 of this Notice.

By Order of the Board

Place : Chennai K SridharDate : June 23, 2015 Company Secretary

TVS CREDIT SERVICES LIMITED

9 Annual Report 2014-15

Disbursal Value Asset under Management

Net Worth Portfolio Mix

Income Growth PAT Growth

2,500 Cr

2,000 Cr

1,500 Cr

1,000 Cr

500 Cr

0 Cr

130 Cr

574 Cr

1,041 Cr

1,532 Cr

2,298 Cr

FY - 11 FY - 12 FY - 13 FY - 14 FY - 15 FY - 11 FY - 12 FY - 13 FY - 14 FY - 150 Cr

2,800 Cr

2,400 Cr

2,000 Cr

1,600 Cr

1,200 Cr

800 Cr

400 Cr 113 Cr

529 Cr

1,063 Cr

1,702 Cr

2,636 Cr

0 Cr

100 Cr

200 Cr

300 Cr

400 Cr

500 Cr

600 Cr

31 Cr117 Cr

246 Cr

400 Cr

572 Cr

FY - 11 FY - 12FY - 13 FY - 14

FY - 15 FY - 11 FY - 12 FY - 13 FY - 14 FY - 1520 Cr

30 Cr

20 Cr

10 Cr

0 Cr

10 Cr

16.48 Cr 0.25 Cr5.16 Cr

17.20 Cr

29.21 Cr

400 Cr

300 Cr

200 Cr

100 Cr

0 Cr

143 Cr 143 Cr172 Cr

262 Cr

392 Cr

FY - 11 FY - 12 FY - 13 FY - 14 FY - 15 FY - 15

Tractor20%

UsedCar

23% TW57%

TVS CREDIT SERVICES LIMITED

10 Annual Report 2014-15

The Directors have pleasure in presenting theSeventh Annual Report on the business andoperations of the Company together with theaudited accounts for the year ended March 31,2015.

1. BUSINESS AND FINANCIAL PERFORMANCEThe highlights of the financial performance of theCompany are given below :

(Rs. in Crores)

Particulars Year ended Year ended31-03-2015 31-03-2014

Revenue from Operations 572.03 399.45

Other Income 3.87 0.68

Total 575.90 400.13

Finance Costs 208.76 154.00

Business Origination,administrative & OtherExpenses 293.52 206.83

Depreciation andamortisation expenses 7.66 5.87

Bad debts written off 11.39 7.40

Provision for bad &doubtful debts 10.55 7.91

Total 531.88 382.01

Profit / (Loss) before tax 44.02 18.12

Less: Tax expense

- Current Tax 20.27 8.94

- Deferred Tax (5.47) (8.01)

Profit / (Loss) after tax 29.22 17.20

Balance brought forwardfrom previous year 6.15 (11.05)

Surplus / (Deficit) carriedto Balance sheet 35.37 6.15

The Company’s overall disbursements registereda growth of 49% at Rs. 2,298 Cr as compared toRs. 1,546 Cr in the previous year.

In line with the diversification plans of theCompany, apart from being the number one retailfinancier for TVS Motor Company Limited

REPORT OF THE DIRECTORS TO THESHAREHOLDERS

(TVSM), it also consolidated its position as thesecond largest tractor financier for Tractors andFarm Equipment Limited in the geographiesrepresented. The Company also expanded itsfootprint in used car financing by covering morelocations and channel partners. During the year,the Company financed around 3.7 lakh twowheeler customers of TVSM as against 3.0 lakhsin the previous year. The Company financed14,653 tractors during the year as against 9,685in the previous year and 17,115 used cars duringthe year as against 7,380 in the previous year.

The Company has cumulatively financed over amillion customers since its inception. During theyear under review, the assets under managementstood at Rs. 2,636 Cr as against Rs. 1,702 Crduring the previous year registering a growth of55%.

The Company continues to invest substantiallyin technology, both for sourcing and recovery,which maintained the overall productivity andcollection efficiency at higher levels. TheCompany’s portfolio quality continues to performwell with cumulative collection efficiency of morethan 98% and overdue to book at 1.22%.

Key initiatives during the financial yearDuring the year, the Company –– worked closely with OEMs to launch new

products

– expanded in North and East with additions of290 new two wheeler dealer counters

– increased rural market penetration in used carsegment to more than 100 locations

– leveraged on the existing network and theresources to provide stressed assets feebased collection services to banks andfinancial institutions

– expanded product suite by venturing into usedtractor business line

– focussed on dealer managementprogrammes across product lines to unlockchannel productivity

TVS CREDIT SERVICES LIMITED

11 Annual Report 2014-15

– drove technology initiatives through robust ITnetwork systems and point of sale solutions

– launched continuous employee recognitionand training programs

Total income during the financial year 2015increased to Rs. 575.90 Cr from Rs. 400.41 Crduring the financial year 2014, an increase of 44% over the previous year. The profit before taxfor the year has also improved and stood atRs. 44.02 Cr as against Rs. 18.12 Cr during theprevious year.

The Company continued to strengthen itsprovisioning standards beyond the requirementunder the regulations of Reserve Bank of India(RBI) by accelerating the provisioning to an earlystage of delinquency. During the year underreview, it further strengthened provisioning andtook an accelerated provisioning impact ofRs. 15.06 Cr.

2. MANAGEMENT DISCUSSION ANDANALYSIS REPORTEconomic OutlookThe year 2014 - 15 began with several challengeson the macroeconomic front, including risinginflation and dwindling industrial output. Theheadline inflation measured by WholesalePrice Index moderated to 2.33% while the retailinflation measured by Consumer Price Indexmoderated to 5.17% up to March 2015. The fallin inflation was primarily driven by low crude oilprices and downslide in food inflation. Foodprices were up 6.14% year-on-year in March2015.

The Reserve Bank of India signalled softeningof the monetary policy stance in response togradual economic improvements and decline ininflation rates. The Reserve Bank of Indiareduced the benchmark repo rate by 50 bpsduring Q4 FY 2014-15. The Central Bank alsoreduced the Statutory Liquidity Ratio (SLR) by150 bps in FY 2014-15. The Governmentmanaged to contain its fiscal deficit at 4% of theGDP as against the target of 4.1 %. The current

account deficit for 2014-15 is expected to declinebelow 1% of GDP due to subdued externaldemand and sharp corrections in the commodityprices. Overall GDP growth in the fiscal settledat around 7.4%, mostly driven by the industryand services sector.

The current economic landscape has provideda platform to implement robust fiscal & financialsector reforms to overhaul the businessenvironment which will help to unlock thecountry’s investment potential. The GDP isexpected to grow at 7.7% in FY 2015-16. Thegrowth will be on the back of strong domesticconsumption, investment and spurt in exports.The crude prices, barring geo-political shocks,are expected to remain low over the year. Withbenign oil prices and weak global demand, retailinflation is likely to soften to 5% in FY 2015-16.Despite the improved outlook, weak monsooncoupled with development challenges includingenergy shortages and infrastructure deficits maydrag the growth prospects.

Industry DevelopmentsThe two wheeler industry grew by 9% in FY2014-15. While the first half of 2014-15 witnesseda growth of 18%, the second half grew by only2%. This is mainly due to a lag effect of loweragricultural output and impact of unseasonalrains. Scooter as a category continued to gainshare in total two wheeler industry. The share ofscooters increased from 23% to 27% due tochanging consumer preferences and strongurban demand. The growth in two wheelerindustry in 2015-16 is expected to be flat at 9%as in 2014-15.

In used car, the organised retail market grew at~ 4% in FY 2014-15. The first time buyers forused cars will continue to increase from 6% inFY 2011 to 14% in FY 2016. The used car markethas benefitted from the entry of organisedplayers; increasing awareness and availability offinancing options. Indian used car market isexpected to outpace domestic new car salesgrowth in the near to medium term. Tractor sales

TVS CREDIT SERVICES LIMITED

12 Annual Report 2014-15

growth abated in FY 2014-15 after seeing arobust performance during the last year. Farmincomes have been negatively impacted bydecline in crop output and softening of cropprices. Industry is estimated to have a negativegrowth of 15% in FY 2015-16.

New Regulatory FrameworkRBI, pursuant to its review of the regulatoryframework for NBFCs, on November 2014,certain changes to the regulatory framework weremade with a view to transitioning overtime to anactivity based regulation of NBFCs, so as toharmonise and simplify regulations to facilitate asmoother compliance culture among NBFCs andstrengthen governance standards.

Accordingly, for the purpose of administeringprudential and other regulations for NBFC –deposit taking (NBFCs-D) and NBFC – non-deposit taking (NBFCs-NDs), the threshold fordefining systemic significance for NBFCs-ND hasbeen revised in the light of overall increase inthe growth of the NBFC Sector.

NBFCs-ND-SI will henceforth be those NBFCs-ND which have asset size of Rs.500 Cr andabove, as per the last audited balance sheet.Hence, all NBFCs-ND with assets of Rs.500 Crand above, irrespective of whether they haveaccessed public funds or not will have to complywith prudential regulations as applicable toNBFCs-ND-SI and will also have to comply withconduct of business regulations, if customerinterface exists. The Company, having an assetsize of more than Rs.500 Cr, would comply withall the prudential regulations applicable as perthe new regulatory framework.

These changes, which have been brought outthrough new regulatory framework, will beimplemented in a phased manner by March 31,2018. Some of the key changes are listed below:

• Classification of loan NPAs for NBFCs hasbeen made in line with banks;

• NPA recognition will change in a phasedmanner to 90 days overdue as against the

current norm of 180 days overdue for loansand 360 days for hire purchase asset;

• Increase in Tier I CAR (core CAR) willincrease in a phased manner to 10% forNBFC-D and NBFC-ND-SI;

• Stringent Corporate governance anddisclosure norms for better accountability andtransparency;

• Standard asset provisioning will standincreased from 0.25% to 0.40%

Following this new regulatory frameworkannouncement by RBI, the Central Governmentannounced certain reforms for the financialsector through budget proposals for the comingfiscal and the highlights are –

• Inclusion of NBFC-NDs, with an asset size ofRs 500 crore and above, under the ambit ofthe Securitization and Reconstruction ofFinancial Assets and Enforcement of SecurityInterest Act, 2002 (SARFAESI Act) and a newBankruptcy Code to provide a boost torecovery efforts and help rein in asset qualityproblems over the long run;

• Setting up of autonomous bank board bureaumarks the initial move towards formalising aholding company structure for public sectorbanks. This will improve governance, optimisecapital contribution by government, andprovide greater functional autonomy; and

• The new Micro Units Development RefinanceAgency (MUDRA) Bank for refinancing ofmicrofinance institutions will support microcredit.

Opportunities and Business PlansThe Indian NBFC sector is poised for growth onthe back of improved macroeconomic factors.Various fiscal and policy reforms initiated to reviveinvestment sentiments will serve to provide amuch needed impetus to the Indian financialsector. Government has initiated a number ofpolicy measures like approval of largeinfrastructure projects, increasing foreign

TVS CREDIT SERVICES LIMITED

13 Annual Report 2014-15

investment limits in insurance, railways, defenceand aerospace. These policy efforts are expectedto improve the economic activity thereby creatingopportunities in trade and financing.

In two wheeler segment the Company plans toenter new locations in micro market. TheCompany will focus on asset quality by buildingsupport structure in quality, audit and training.During the year ahead, the Company plans tomigrate from pure fund based businesses to amix of fund and fee based business by providingvarious funding options to our existing borrowersthrough tie up with banks and financialinstitutions.

The Company will focus on demand creation inthe used car and used tractor finance business.The Company plans to increase the financepenetration in smaller towns in rural space byexpanding into new locations mostly in districtheadquarters. In tractor segment the focus willbe to de-risk the new tractor segment byconsolidating the used tractor space. TheCompany plans to expand into low productiveareas to support the OEMs and leverage it forbusiness growth at existing locations.

ThreatsHowever the growth prospect might get offsetby nominal growth in crop prices, unseasonalrains, stagnating rural wages and declined rabioutput. Weakness in rural economy with highprobability of El-nino effect can result in poorspatial and seasonal distribution of rainfallaffecting kharif production. Consequently thegrowth in two wheeler industry in 2015-16 isexpected to be flat at 9% as in 2014-15. TheGovernment has to address numerouschallenges, such as infrastructure bottlenecks.It must also focus on developing policies andinitiatives which will drive economic growthbalancing the macroeconomic risks.

Infrastructure & Information TechnologyThe Company is present in 16 States and UnionTerritories with 62 area offices. The Company

carries out its credit operations from six hubs inChennai, Delhi, Pune, Indore, Jaipur and Calicut.The Company continues to invest substantiallyin technology, both for sourcing and recovery,which maintained the overall productivity andcollection efficiency at higher levels.

The Company uses web based platforms for loanprocessing and collections. The Company useshandheld devices and business applications forautomatic collection process. The Company hasdeveloped robust MIS and Dashboards atgranular levels which serve as primary decisionmaking tools.

Human ResourcesThe Company has developed a robust humanresource management framework to maximiseemployee performance. At the macro level, theCompany has undertaken many initiatives todevelop organisational leadership and culture.The Company has also launched continuousemployee recognition and training programs todevelop a talented workforce to meet day to daybusiness challenges.

The Company duly complied with all the statutorycompliances related to employment and labourlaws. As on 31st March 2015, the Company had6,323 employees on its rolls.

CAUTIONARY STATEMENTStatements in the above report describing theCompany’s objectives, projections, estimatesand expectations may be “forward lookingstatements” within the meaning of applicablesecurities laws and regulations. Actual resultscould differ materially from those expressed orimplied. Important factors that could make adifference to the Company’s operations include,among others, economic conditions affectingdemand/supply and price conditions in thedomestic markets in which the Companyoperates, changes in the governmentregulations, tax laws and other statutes andincidental factors.

TVS CREDIT SERVICES LIMITED

14 Annual Report 2014-15

3. DIVIDENDThe directors, in order to conserve the resourcesfor its future expansion, have not proposed anydividend for the year under review.

4. PUBLIC DEPOSITSThe Company has not accepted any deposit fromthe shareholders and others within the meaningof Chapter V of the Act 2013 read with theCompanies (Acceptance of Deposits) Rules,2014 during the year ended 31st March 2015.

The Company shall not raise public depositswithout prior written approval of the RBI, as perthe conditions attached to the Certificate ofRegistration issued by RBI.

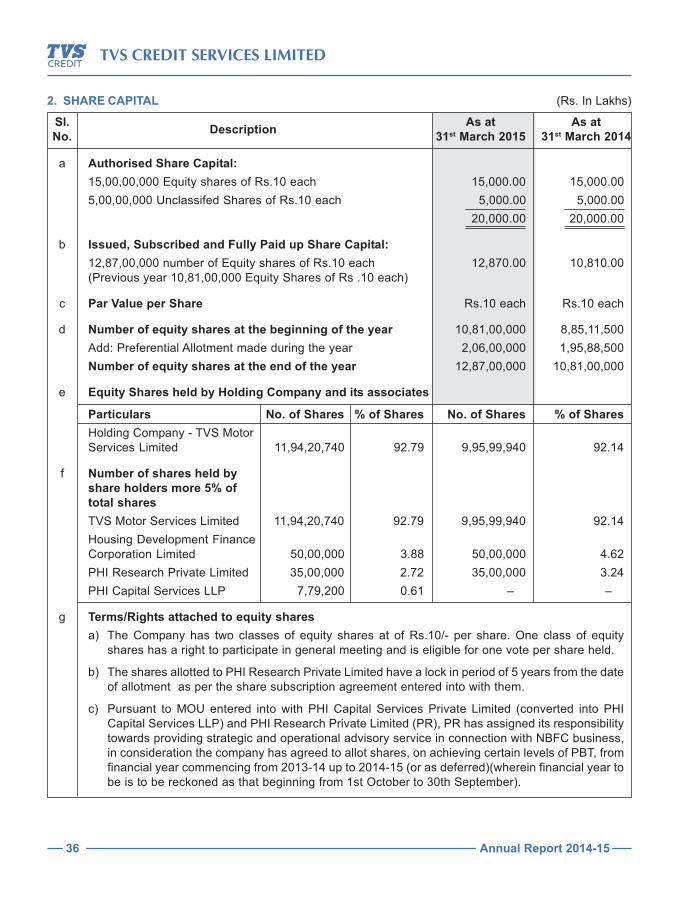

5. ISSUANCE OF EQUITY SHARESDuring the year under review, the board ofdirectors issued and allotted 1,98,20,800 equityshares of Rs.10/-each at a premium of Rs. 39/-per share aggregating to Rs.97.12 Cr to TVSMotor Services Limited, holding company andallotted 7,79,200 equity shares of Rs. 10/- eachat a premium of Rs. 39/- per share aggregatingto Rs. 3.82 Cr to PHI Capital Services LLP, interms of Sections 42 and 62 of the Act 2013 readwith the Rules made there-under, on apreferential basis.

The paid up capital of the Company accordinglystood increased from Rs. 108.10 Cr(108,100,000 equity shares of Rs.10/- each) toRs.128.70 Cr (128,700,000 equity shares ofRs.10/- each) as on 31st March 2015.

6. FUNDINGWith equity infusion of Rs. 100.94 Cr in FY2014-15, participation from banks and financialinstitutions in the form of equity and Tier 2 capital(Subordinated Debt), the Company has a strongCapital Adequacy Ratio (CAR). The CAR as on31st March 2015 stood at 16.78%.

ICRA Ltd and CRSIL Ltd have assigned ratingsfor the various facilities availed by the Company,details of the rating are given below:

The Company has been assigned A+ by CRISILand ICRA for bank loans and A1+ by CRSIL andICRA for its short term debt program.

The Company has taken various initiatives toreduce its cost of borrowings and accordinglydiversified its funding mix with borrowings fromPublic sector banks, Private sector banks,Financial Institutions and Mutual funds. Duringthe year the Company raised Rs. 625 crorethrough long term loans. No interest or principalrepayment of the term loans was due and unpaidas on March 31, 2015. The assets of theCompany which are available by way of securityare sufficient to discharge the claims of the banksas and when they become due.

The Company has securitised its AAA ratedtractor portfolio to the extent of Rs. 148 crore(principal outstanding) during the year underreview. The Company has also sold used carportfolio of Rs. 59 crore (principal outstanding)under direct assignment route. The Company hasadhered to the revised guidelines onSecuritisation and Direct assignmenttransactions issued by RBI in August 2012.

During the year the Company also raised Rs. 50crore in the form of Subordinated debt, on privateplacement basis. The Subordinated debt is ratedA+ by ICRA and has a maturity period of 5 yearsand 6 months.

With the diversification of business into used carsand tractors where the lending tenor is more than36 months, the funding programme is beingstructured in such a way that the borrowing tenormatches with the lending tenor and there is noAsset Liability mismatch. Also sufficient undrawnlimits are being maintained at any point of time.

7. DIRECTORS’ RESPONSIBILITYSTATEMENTPursuant to the requirement of Section 134(5)of the Act, 2013 with respect to Director’sResponsibility Statement, it is hereby stated that:

(a) in the preparation of the annual accounts forthe year ended 31st March 2015, the

TVS CREDIT SERVICES LIMITED

15 Annual Report 2014-15

applicable accounting standards had beenfollowed along with proper explanationrelating to material departures;

(b) the directors had selected such accountingpolicies and applied them consistently andmade judgments and estimates that werereasonable and prudent so as to give a trueand fair view of the state of affairs of theCompany at the end of the financial year andof the profit of the Company for that period;

(c) the directors had taken proper and sufficientcare for maintenance of adequate accountingrecords in accordance with the provisions ofthis Act for safeguarding the assets of theCompany and for preventing and detectingfraud and other irregularities;

(d) the directors had prepared the accounts forthe financial year ended 31st March 2015 ona going concern basis; and

(e) the directors had devised proper systems toensure compliance with the provisions of allapplicable laws and that such systems wereadequate and operating effectively.

8. DIRECTORS & KEY MANAGERIALPERSONNELAppointmentsDuring the year, M/s S Santhanakrishnan,R Ramakrishnan and V Srinivasa Rangan, wereappointed as Independent Director (IDs) for thefirst term of five consecutive years from theconclusion of the sixth Annual General Meetingand to receive remuneration by way of fees,reimbursement of expenses for participation inthe meetings of the board and / or committeesand profit related commission in terms ofapplicable provisions of the Act 2013 asdetermined by the board from time to time.

Resignations / ReappointmentsMr S Santhanakrishnan, Independent directorand Mr Sudarshan Venu, non-independentdirector resigned from the board effective27th March 2015, in compliance with the

directions by RBI through revised regulatoryframework for NBFCs issued vide DNBR (PD)CC.No.002/ 03.10.001/ 2014-15 datedNovember 10, 2014 (the Framework) CorporateGovernance and Disclosure norms. Thisframework, inter alia, mandated that independent/ non-executive directors of an NBFC should bebetween 35 to 70 years of age.However, RBI has made certain changesimmediately in the directions, based on thefeedback received from Industry representingthat such age restrictions did not exist in thepreliminary acts like Companies Act 2013 (theAct 2013) and other Securities Laws which donot impose such conditions.The board, after considering the valuablecontributions and guidance during thedeliberations of the meetings of the board givenby them and on the recommendation of thenomination and remuneration committee ofdirectors, decided to appoint Mr Sudarshan Venu,as additional, non-executive and non-independent director of the Company, in order tocontinue to avail his services for the benefit ofthe Company, especially considering hisexpertise in the automotive industry.Similarly, the board, keeping in view his vastexpertise and knowledge and in order to continueto avail his service in the interest of the Companyand on the recommendation of the nominationand remuneration committee of directors,decided to appoint Mr S Santhanakrishnan, asadditional, non-executive and non-independentdirector of the Company, in terms of Section 161read with Section 152 of the Act 2013 at the AGM.At the board meeting held on 23rd June, 2015,Mr Sudarshan Venu and Mr S Santhanakrishnanwere appointed as additional, non-executive andnon-independent directors of the Company interms of Section 161 read with Section 152 ofthe Act 2013. They will vacate office in terms ofSection 161 of the Act 2013 at the AGM and,being eligible, seek themselves for re-appointment at the ensuing 7th Annual GeneralMeeting of the Company (AGM).

TVS CREDIT SERVICES LIMITED

16 Annual Report 2014-15

The board has recommended their appointmentsas non-executive and non-independent directors,liable to retire by rotation, in accordance with thearticles of association of the Company (AoA), atthe AGM.The board also reviewed the process of duediligence undertaken by the NRC to determinethe suitability of their continuing to hold theposition as director on the board, based uponqualification, expertise, track record, integrity andother ‘fit and proper’ criteria, as per the RBIRegulations.Notices have been received from the holdingcompany viz., TVS Motor Services Limited, asper the provisions of Section 160 of the Act 2013,along with a requisite deposit amount signifyingits intention to propose the candidatures of MrSudarshan Venu and Mr S Santhanakrishnan,for appointment as directors at the ensuing AGM.

Woman directorIn terms of Section 149 of the Act 2013, theCompany is required to have a woman directoron its board.In terms of Section 149 read with Section 178 ofthe Act 2013 and based on the recommendationof the nomination and remuneration committeeof directors Ms Sasikala Varadachari wasappointed as non-executive and independentdirector of the Company, at the extra-ordinarygeneral meeting held on 30th March 2015On appointment, each ID has acknowledged theterms of appointment as set out in their letter ofappointment. The appointment letter covers, interalia, the terms of appointment, duties,remuneration and expenses, rights of access toinformation, other directorships, dealing inCompany’s shares, disclosure of Director’sinterests, insurance and indemnity. The IDs areprovided with copies of the Company’s policiesand charters of various committees of the board.

Declaration of independenceAll the existing IDs have declared that they metall the criteria of independence as provided under

Section 149(6) of the Act 2013. The detailedterms of appointment of IDs is disclosed on theCompany’s website in the following linkwww.tvscredit.co.in

Declaration and undertakingDuring the year, as per the directions of RBI on‘Non-banking financial companies – CorporateGovernance (Reserve Bank) Directions, 2015, theboard obtained necessary annual ‘declarations ofundertaking’ in the prescribed format by RBI fromthe directors.

Directors liable to retire by rotationIn terms of the AoA and the applicable provisionsof the Act 2013, M/s K N Radhakrishnan andMr P.Sivaram, non-independent directors, whoare liable to retire at the AGM and, being eligible,offer themselves for re-appointment.

The board, based on the recommendation ofNomination and Remuneration Committee(NRC), has recommended their re-appointmentas directors, liable to retire by rotation, inaccordance with the articles of association of theCompany (AoA), at the AGM.

Separate meeting of IDs:The IDs were fully kept informed of theCompany’s activities in all its spheres.

During the year under review, a separate meetingof IDs was held on 27th March, 2015 and the IDsreviewed the performance of:

(i) non-IDs viz., M/s. Venu Srinivasan,Chairman, T K Balaji, Anupam Thareja, wholetime director, P Sivaram, K N Radha-krishnan, Sudarshan Venu, directors; and

(ii) the board as a whole.

They reviewed the performance of Chairmanafter taking into account the views of Executiveand Non-Executive Directors. They alsoassessed the quality, quantity and timeliness offlow of information between the Company’sManagement and the Board that is necessary

TVS CREDIT SERVICES LIMITED

17 Annual Report 2014-15

for the Board to effectively and reasonablyperform their duties.

Number of board meetings held during theyearDuring the year under review, the board met fourtimes on 12th June 2014, 11th August 2014,3rd December 2014 and 27th March 2015 and thegap between two meetings did not exceed onehundred and twenty days.

Key Managerial Personnel (KMPs)At the board meeting held on 18th March 2014and 12th June 2014, Mr Anupam Thareja, WholeTime Director, Mr G Venkatraman, ChiefExecutive Officer, Mr V Gopalakrishnan, ChiefFinancial Officer and Mr K Sridhar CompanySecretary were designated as ‘Key ManagerialPersonnel’ of the Company in terms of Section203 of the Act 2013 read with the Companies(Appointment and Remuneration of ManagerialPersonnel) Rules, 2014.

During the year, the current term of office ofMr Anupam Thareja, as Whole Time Director ofthe Company (WTD) ceased effective 2nd May2015. The board, at its meeting held on3rd December, 2014, decided to appoint him fora further period of five years effective 3rd May2015, subject to the approval of the shareholdersof the Company, in terms of section 196/197 readwith the Companies (Appointment andRemuneration of Managerial Personnel) Rules2014 and Schedule V of the Companies Act, 2013(the Act 2013).

The said re-appointment was also recommendedby the Nomination and Remuneration Committeeof directors (NRC), after noting the justification,ascertaining the fulfilment of the ‘fit and propercriteria’ and obtaining the declaration andundertakings, on the lines of the Guidelinesprescribed as per the Revised RegulatoryFramework for Non-Banking Finance Company(NBFC) vis-à-vis other parameters, as laid downunder the ‘Nomination and Remuneration Policy’ ofthe Company, in terms of Sec 178 of the Act, 2013.

The board also decided not to recommend anyremuneration, during the period of his tenure, inview of the subsisting tripartite arrangement byway of an alliance agreement entered on 16th April2010, among the holding company, namely TVSMotor Services Limited (TVS MS) and PhiResearch Private Limited (PHI).

Accordingly, the board recommended the saidreappointment for a further period of five years,considering his vast expertise and exposure inNBFC industry for more than a decade by theapproval of the shareholders. The shareholdersalso approved the terms of appointment ofMr Anupam Thareja at the extra-ordinary generalmeeting held on 30th March 2015.

Evaluation of the board, committees anddirectorsIn terms of Section 134 of the Act 2013, the boardreviewed and evaluated its own performancefrom the perspectives of Company Performance,Strategy and Implementation, Risk Management,Corporate ethics, based on the evaluation criterialaid down by the Nomination and RemunerationCommittee.

The board discussed and assessed its owncomposition, size, mix of skills and experience,its meeting sequence, effectiveness ofdiscussion, decision making, follow up action,quality of information and the performance andreporting by the Committees viz., AuditCommittee, Nomination and RemunerationCommittee (NRC) and Corporate SocialResponsibility Committee (CSR).

The board upon evaluation concluded that it iswell balanced in terms of diversity of experienceencompassing all the activities of the Company.It is the endeavour of the Company to have adiverse board representing a range of experienceat policy-making levels in business.

The performance of individual directors includingall Independent directors assessed against arange of criteria such as contribution to thedevelopment of business strategy and

TVS CREDIT SERVICES LIMITED

18 Annual Report 2014-15

performance of the Company, understanding themajor risks affecting the Company, clear directionto the management, contribution to the boardcohesion. The performance evaluation has beendone by the entire board of directors, except theDirector concerned being evaluated. The boardnoted that all directors have understood theopportunities and risks to the Company’s strategyand are supportive of the direction articulated bythe management team towards consistentimprovement.

The board also noted that corporateresponsibility, ethics and compliance are takenseriously, and there is a good balance betweenthe core values of the Company and the interestsof stakeholders. The board satisfied with theCompany’s performance in all fronts viz.,operations, marketing, finance management,employee relations and compliance with statutory/ regulatory requirements and finally concludedthat the board operates effectively and is closelyaligned to the culture of the business.

The performance of each committee wasevaluated by the board after seeking inputs fromits members on the basis of the criteria such asmatters assessed against terms of reference,time spent by the committees in consideringmatters, quality of information received, work ofeach committee, overall effectiveness anddecision making and compliance with thecorporate governance requirements andconcluded that all the committees continued tofunction effectively, with full participation by allits members and the executive management ofthe Company.

The board reviewed each committee’s terms ofreference to ensure that the Company’s existingpractices remain appropriate. Recommendationsfrom each committee are considered andapproved by the board prior to implementation.

Nomination and Remuneration PolicyThe Nomination and Remuneration Committee(NRC) reviews the composition of the board, to

ensure that there is an appropriate mix of abilities,experience and diversity to serve the interestsof all shareholders and the Company.

During the year, in accordance with therequirements under Section 178 of the Act 2013,the Committee formulated a Nomination andRemuneration Policy to govern the terms ofnomination / appointment and remuneration of(i) directors, (ii) Key Managerial Personnel(KMPs) and (iii) Senior Management Personnel(SMPs) of the Company. The same wasapproved by the board at its meeting held on27th March 2015.

The Committee also reviews successionplanning of both SMPs and board. TheCompany’s approach in recent years is to havea greater component of performance linkedremuneration for SMPs. The process ofappointing a director / KMPs / SMPs, is that whena vacancy exists, or is expected, the NRC willidentify, ascertain the integrity, qualification withthe appropriate expertise and experience havingregard to the skills that the candidate will bringto the board / company and the balance of skillswith that of the existing members hold.

The NRC will review the profile of persons andthe most suitable person is either recommendedfor appointment by the board or is recommendedto shareholders for election. The Committee hasdiscretion to decide whether qualification,expertise and experience possessed by a personare sufficient / satisfactory for the concernedposition.

NRC will ensure that any person(s) who is / areappointed or continues in the employment of theCompany as its executive chairman, managingdirector, whole time director should comply withthe conditions as laid out under Part I of ScheduleV of the Act. NRC will ensure that anyappointment of a person as an independentDirector of the Company will be made inaccordance with the provisions of Section 149read with Schedule IV of the Act.

TVS CREDIT SERVICES LIMITED

19 Annual Report 2014-15

Criteria for performance evaluation, disclosureson the remuneration of directors, criteria ofmaking payments to non-executive directorshave been disclosed as part of CorporateGovernance report attached herewith.

9. COMMITTEES OF THE BOARDThe Board Committees play a crucial role in thegovernance structure of the Company have beenconstituted to deal with specific areas / activitiesin accordance with the requirements of theapplicable provisions of the Act 2013 / Non-Banking Financial Companies – CorporateGovernance (Reserve Bank) Directions 2015.

The Board has currently established the followingcommittees:

Audit CommitteeAs required under Section 177 of the CompaniesAct, 2013, the Company has constituted anindependent audit committee which acts as a linkbetween the statutory and the internal auditorsand the board of directors of the Company. It isauthorised to select and establish accountingpolicies, review reports of the Statutory and theInternal Auditors and meet with them to discusstheir findings, suggestions and other relatedmatters.

As on date, the Audit Committee was re-constituted with the following directorsas its members, M/s. R Ramakrishnan,K N Radhakrishnan and V Srinivasa Rangan.

The Committee meets periodically to discuss andreview such matters as required in terms ofSection 177 of the Act 2013.

Asset Liability Management CommitteeThe Company constituted an Asset LiabilityManagement Committee (ALCO), in terms ofGuidelines issued by RBI to NBFCs for effectiverisk management in its portfolios.

The Asset Liability Committee consists ofM/s. Anupam Thareja, Whole Time Director,R Ramakrishnan, Director, G Venkatraman,

Chief Executive Officer, V Gopalakrishnan, ChiefFinancial Officer and M Kalyanaraman, ChiefOperating Officer as its members.

Risk Management CommitteeThe Company being in the business of financingof two wheelers, cars and tractors has to managevarious risks. These risks include credit risk,liquidity risk, interest rate risk and operational risk.

The Company has constituted a RMC to reviewon an on-going basis the measures adopted bythe Company for the identification, measurement,monitoring and mitigation of the risks involved invarious areas of the Company’s functioning.

The Company has laid down procedures toinform board about the risk assessment andmitigation procedures, to ensure that executivemanagement controls risk through means of aproperly defined framework.

The Company has a robust asset-liabilitymanagement model to ascertain and manageinterest rate and liquidity risks.

Issues were discussed and reviewed periodicallyat meetings of RMC. This Committee meetsperiodically and oversee the risk managementactivities of the Company.

The Company continues to invest substantiallyin personnel, technology and infrastructuretowards improved process efficiencies andmitigate business risks.

Corporate Social Responsibility CommitteeDuring the year, the board of directors constituteda Corporate Social Responsibility Committee (CSRCommittee) with three directors viz., Mr VenuSrinivasan, chairman, Mr Sudarshan Venu andMr S Santhanakrishnan on 18th March 2014.

Subsequently, the CSR Committee was re-constituted in line with the provisions of Section135 of the Act 2013 with Mr Venu Srinivasan,chairman, Mr K N Radhakrishnan, director andMr R Ramakrishnan, independent director, as itsmembers of the Committee, on 27th March 2015.

TVS CREDIT SERVICES LIMITED

20 Annual Report 2014-15

CSR activities have already been textured intothe Company’s value system through SrinivasanServices Trust (SST), established by the groupcompanies in 1996 with the vision of building self-reliant rural community.

SST, the CSR arm of the Company, wasestablished in 1996. Over 19 years of service,SST has played a pivotal role in changing livesof people in many villages in rural India bycreating self-reliant communities that are modelsof sustainable development.

The Company is eligible to spend on theirongoing projects / programs, falling within theCSR activities specified under the Act 2013, asmandated by the Ministry of Corporate Affairs forcarrying out the CSR activities.

The CSR Committee formulated andrecommended a CSR policy in terms of Section135 of the Act 2013 along with a list of projects /programmes to be undertaken for CSR spendingin accordance with the Companies (CorporateSocial Responsibility Policy) Rules, 2014.

Based on the recommendations of the CSRCommittee, the board has approved the projects/ programs carried out as CSR activities by thefollowing non-profitable organizations having atrack record of more than the prescribed yearsin undertaking similar programmes / projects,constituting more than 2% of average net profits,for the immediate past three financial years,towards CSR spending for the current financialyear 2014-2015.

Accordingly, the annual report on CSR containingall the prescribed projects / programmes approvedand recommended by CSR Committee andapproved by the board and implemented for theyear under review are given by way of note attached(Annexure IV) to this Report.

10. INTERNAL CONTROL SYSTEMSThe Company’s comprehensive and effectiveinternal control system ensures smooth business

operations, meticulously recording all transactiondetails and ensuring regulatory compliance andprotecting the Company’s assets from loss ormisuse.

The Company’s internal control system isdesigned to ensure operational efficiency,protection and conservation of resources,accuracy and promptness in financial reportingand compliance with laws and regulations.

The internal control system is supported by aninternal audit process for reviewing the adequacyand efficacy of the internal controls including itssystem and processes and compliance withregulations and procedures.

Internal audit reports are discussed with themanagement and are reviewed by the auditcommittee of the board which also reviews theadequacy and effectiveness of the internalcontrols. The Company’s internal control systemis commensurate with its size, nature andoperations.

11. AUDITORSStatutory AuditorsThe Company at its sixth AGM held on 14th July2014 appointed M/s V Sankar Aiyar & Co.,Chartered Accountants, Mumbai, having FirmRegistration No. 109208W allotted by TheInstitute of Chartered Accountants of India, asstatutory auditors of the Company to hold office,for the second term of five consecutive yearsfrom the conclusion of the said AGM, subject toratification at every AGM.

The Auditors’ Report for the financial year2014-15 does not contain any qualification,reservation or adverse remark and the same isattached with the annual report.

The Company has obtained necessary certificateunder Section 141 of the Act conveying theireligibility for being statutory auditors of theCompany for the year 2015-16.

TVS CREDIT SERVICES LIMITED

21 Annual Report 2014-15

Rotation of partners of the statutory auditorsaudit firmIn terms of RBI Master Circular No.RBI/2014-15/632 No.DNBR (PD) CC No.040/03.01.011/2014-2015 dated 3rd June 2015regarding ‘Non-Banking Financial Companies –Corporate Governance (Reserve Bank)Directions, 2015, it has been made mandatoryfor any NBFC with asset size of Rs.500 Cr isrequired to rotate the partner/s of the CharteredAccountant firm conducting the audit every threeyears so that the same partner does not conductaudit of the company continuously for more thana period of three years.

However, the partner so rotated will be eligiblefor conducting the audit of NBFC after an intervalof three years. It has also been mandated thatthe NBFC is also required to incorporateappropriate terms in the letter of appointment ofthe firm of auditors and ensure its compliance.

Mr S Venkatraman, Partner in Chennai,M/s V Sankar Aiyar & Co, Chartered Accountants,Mumbai of the Company has already completedthree years of audit. Therefore,Mr S Venkatraman, their other partner in Mumbaiwill audit the accounts of the Company for thefinancial year commencing from 2015-2016,subject to their reappointment of their firms atthe annual general meeting.

Secretarial AuditorAs required under Section 204 of the Act, 2013and the Companies (Appointment andRemuneration of Managerial Personnel) Rules2014, the Company is required to appoint aSecretarial Auditor for auditing secretarial andrelated records of the Company.

Accordingly, Mr T N Sridharan, CompanySecretary in practice, Chennai has beenappointed as Secretarial Auditor for carrying outthe secretarial audit for the financial year2015-16.

As required by Section 204 of the Act, 2013, theSecretarial Audit Report for the year 2014-15,

given by Mr T N Sridharan, Company Secretaryin practice, Chennai for auditing the secretarialand related records is attached to this report. TheSecretarial Audit Report does not contain anyqualification, reservation or adverse remark.

12 CORPORATE GOVERNANCEThe Company has a strong legacy of fair,transparent and ethical governance practices.The Company’s philosophy on corporategovernance is founded on the fundamentalideologies of the group viz., Trust, Value andService.

The Company would constantly endeavour toimprove on these aspects. The Companyensures good governance through theimplementation of effective policies andprocedures, which is mandated and reviewed bythe board of the committees of the members ofthe Board.

A report on corporate governance regardingcompliance with the conditions of CorporateGovernance as stipulated under RBI guidelinesforms part of the Report and is annexed herewith.

13. ADHERENCE TO RBI NORMS ANDSTANDARDSThe Company has fulfilled the prudential normsand standards as laid down by RBI pertaining toincome recognition, provisioning ofnonperforming assets and capital adequacy. Thecapital adequacy ratio of the Company is 16.78%which is well above the prescribed minimum of15% by RBI.

As a prudent practice, the Company currentprovisioning standards are more stringent thanReserve Bank of India (RBI) prudential norms.In line with its conservative approach, theCompany continues to strengthen its provisioningnorms beyond the RBI regulation by acceleratingthe provisioning to an early stage ofdelinquencies based on the past experience andemerging trends.

TVS CREDIT SERVICES LIMITED

22 Annual Report 2014-15

The Fair Practices Code and KYC norms framedby RBI seek to promote good and fair practicesby setting minimum standards in dealing withcustomers, increase transparency so thatcustomers have a better understanding of whatthey can reasonably expect of the services beingoffered, encourage market forces throughcompetition to achieve higher operatingstandards, promote fair and cordial relationshipsbetween customers and the finance companyand foster confidence in the housing financesystem.

The Company has put in place all theCommittees prescribed by RBI and haveformulated a comprehensive CorporateGovernance Policy. The Company has instituteda mechanism to monitor and review adherenceto the Fair Practices Code, KYC norms, andInvestment & Credit policies as approved by theBoard of Directors.

14. POLICY ON VIGIL MECHANISMThe Board at its meeting held on 27th March 2015,adopted a Policy on Vigil Mechanism inaccordance with the provisions of CompaniesAct, 2013, which provides a formal mechanismfor all directors, employees and otherstakeholders of the Company, to report to themanagement their genuine concerns orgrievances about unethical behaviour, actual orsuspected fraud and any violation of theCompany’s Code of Business Conduct or Ethicspolicy.

The policy also provides a direct access to theChairperson of the Audit Committee to makeprotective disclosures to the management aboutgrievances or violation of the Company’s Codeof Business Conduct and Ethics. The policy isdisclosed on the Company’s website in thefollowing link www.tvscredit.co.in.

15. DISCLOSURES(i) Information on conservation of energy,

technology absorption, foreign exchange etc

The Company, being a non-banking financecompany, does not have any manufacturingactivity and hence the reporting on“Conservation of Energy and TechnologyAbsorption” does not arise..

Foreign currency expenditure in FY 2014-15is Nil (previous year Rs. 1.13 lakhs). TheCompany did not have any foreign exchangeearnings.

(ii) Annual ReturnExtract of Annual Return in the prescribedform is given as Annexure I to this report.

(iii) Employees’ remunerationDetails of employees receiving theremuneration in excess of the limitsprescribed under Section 197 of the Act 2013read with Rule 5(2) of the Companies(Appointment and Remuneration ofManagerial Personnel) Rules, 2014 areannexed as a statement and given inAnnexure II.

(iv) Details of related party transactionsDetails of material related party transactionsunder Section 188 of the Act 2013 are givenin Annexure III to this report in the prescribedform.

(v) Details of loans / guarantees / investmentsmadeFurnishing the details of investments underSection 186 of the Act 2013 for the financialyear 2014-2015 does not arise, since theCompany has not made any investmentduring the year under review.

In terms of Rule 11(2) of the Companies(Meetings of Board and its Powers) Rules,2014 NBFC Companies are excluded fromthe applicability of Section 186 of the Act2013, where the loans, guarantees andsecurities are provided in the ordinary courseof its business.

TVS CREDIT SERVICES LIMITED

23 Annual Report 2014-15

On loans granted to the employees, theCompany has charged interest as per itsremuneration policy, in compliance withSection 186 of the Act 2013.

(vi) Other laws

During the year under review, there were nocases filed pursuant to the provisions ofSexual Harassment of Women at Workplace(Prevention, Prohibition and Redressal) Act,2013.

16. ACKNOWLEDGEMENTThe directors gratefully acknowledge thecontinued support and co-operation receivedfrom the holding company, namely TVS Motor

For and on behalf of the Board of Directors

Place : Chennai Venu SrinivasanDate: June 23, 2015 Chairman

Services Limited and other investors. Thedirectors thank the bankers, investing institution,customers and dealers of TVS Motor CompanyLimited and TAFE Limited for their valuablesupport and assistance.

The directors wish to place on record theirappreciation of the very good work done by allthe employees of the Company during the yearunder review.

TVS CREDIT SERVICES LIMITED

24 Annual Report 2014-15

INDEPENDENT AUDITOR’S REPORT FOR THE YEAR ENDED 31ST MARCH 2015TO THE MEMBERS OF TVS CREDIT SERVICES LIMITED

Report on the Standalone Financial Statements as at 31st March 2015.1. We have audited the accompanying financial statements of TVS Credit Services Limited

(‘the Company’), which comprises the Balance Sheet as at 31 March 2015, the Statement of Profitand Loss and the Cash Flow Statement for the year then ended, and a summary of significantaccounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements2. The Company’s Board of Directors is responsible for the matters stated in Section 134(5) of the

Companies Act, 2013 (“the Act”) with respect to the preparation of these Standalone financialstatements that give a true and fair view of the financial position, financial performance and cashflows of the Company in accordance with the accounting principles generally accepted in India,including the Accounting Standards specified under Section 133 of the Act, read with Rule 7 of theCompanies (Accounts) Rules, 2014.

3. This responsibility also includes maintenance of adequate accounting records in accordance withthe provisions of the Act for safeguarding the assets of the Company and for preventing anddetecting frauds and other irregularities; selection and application of appropriate accounting policies;making judgments and estimates that are reasonable and prudent; and design, implementationand maintenance of adequate internal financial controls, that were operating effectively for ensuringthe accuracy and completeness of the accounting records, relevant to the preparation andpresentation of the financial statements that give a true and fair view and are free from materialmisstatement, whether due to fraud or error.

Auditors’ Responsibility4. Our responsibility is to express an opinion on these Standalone financial statements based on our

audit. We have taken into account the provisions of the Act, the accounting and auditing standardsand matters which are required to be included in the audit report under the provisions of the Actand the Rules made thereunder. We conducted our audit in accordance with the Standards onAuditing specified under Section 143(10) of the Act. Those Standards require that we comply withethical requirements and plan and perform the audit to obtain reasonable assurance about whetherthe financial statements are free from material misstatement.

5. An audit involves performing procedures to obtain audit evidence about the amounts and disclosuresin the financial statements. The procedures selected depend on the auditor’s judgment, includingthe assessment of the risks of material misstatement of the financial statements, whether due tofraud or error. In making those risk assessments, the auditor considers internal financial controlrelevant to the Company’s preparation of the financial statements that give a true and fair view inorder to design audit procedures that are appropriate in the circumstances, but not for the purposeof expressing an opinion on whether the Company has an adequate internal financial controlssystem over financial reporting and the operating effectiveness of such controls. An audit alsoincludes evaluating the appropriateness of accounting policies used and the reasonableness ofthe accounting estimates made by the Company’s Directors, as well as evaluating the overallpresentation of the financial statements.

TVS CREDIT SERVICES LIMITED

25 Annual Report 2014-15

6. We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinion on the Standalone financial statements.

Opinion7. In our opinion and to the best of our information and according to the explanations given to us, the

financial statements give the information required by the Act in the manner so required and give atrue and fair view in conformity with the accounting principles generally accepted in India, of thestate of affairs of the Company as at 31st March 2015, and its profit and its cash flows for the yearended on that date.

Report on Other Legal and Regulatory Requirements8. As required by the Companies (Auditor’s Report) Order, 2015 (‘the Order’),issued by the Central

Government of India in terms of sub-section (11) of section 143 of the Act, we give in the Annexurea statement on the matters specified in paragraphs 3 and 4 of the said Order.

9. As required by section 143(3) of the Act, we report that:(a) we have sought and obtained all the information and explanations which to the best of our

knowledge and belief were necessary for the purpose of our audit;(b) in our opinion proper books of account as required by law have been kept by the Company so

far as appears from our examination of those books;(c) the Balance Sheet, the Statement of Profit and Loss and the Cash Flow Statement dealt with

by this report are in agreement with the books of account;(d) in our opinion, the aforesaid Standalone financial statements, comply with the Accounting

Standards specified under Section 133 of the Act, read with Rule 7 of the Companies (Accounts)Rules, 2014;

(e) on the basis of written representations received from the directors as on 31 March 2015, andtaken on record by the Board of Directors, none of the directors are disqualified as on 31March 2015, from being appointed as a director in terms of section 164 (2) of the Act;

(f) With respect to other matters to be included in the Auditor’s Report in accordance with Rule 11of the Companies (Audit and Auditors) Rules, 2014, in our opinion and to the best of ourinformation and according to explanations give to us:i. The company has disclosed the impact of pending litigation on its financial position in its

financial statement – Refer Note No.22.3 to the financial statement.ii. The Company did not have any long term contracts including derivative contracts for which

there where any material foreseeable losses – Refer Note No.32 to the financial statement.iii. there were no amounts which were required to be transferred to the Investor Education

and Protection Fund by the Company

For V. Sankar Aiyar & Co.,Chartered AccountantsICAI Reg. No. 109208W

S. VenkatramanPlace: Chennai PartnerDate: June 23, 2015 M. No. 34319

TVS CREDIT SERVICES LIMITED

26 Annual Report 2014-15

ANNEXURE TO INDEPENDENT AUDITORS’ REPORT

1. a. The Company has maintained proper records showing full particulars including quantitativedetails and situation of Fixed Assets.

b. We are informed by the Management that the Fixed Assets have been physically verified bythem during the year and no material discrepancies were noticed

2. As the Company is a Non-Banking Finance Company it does not hold any inventories. Hencereporting under para 3(b) of the Order does not arise.

3. The company has neither taken or nor granted any loan to/ from companies, firms and otherparties covered in the Register maintained under Section 189 of the Companies Act, 2013. Henceclauses (a), (b), of Para 3 (iii) of the Order are not applicable.

4. In our opinion and according to the information and explanations given to us, there are adequateinternal control systems commensurate with the size of the Company and the nature of its businessfor the purchase of fixed assets and for the sale of services. The activities of the Company do notinvolve purchase or inventory and sale of goods. During the course of our audit, we have notobserved any continuing failure to correct major weaknesses in the internal control system.

5. According to the information and explanations given to us, the Company has not accepted anydeposits from the public. Therefore, the provisions of clause (v) of the para 3 of the Order are notapplicable to the Company.

6. The Central Government has not prescribed maintenance of cost records under section 148(1)of the Companies Act, 2013.

7. a. According to the information and explanations given to us, the Company is regular in depositingwith appropriate authorities undisputed statutory dues of Provident Fund, Employees’ StateInsurance, Income tax, Service Tax and Cess. There is no liability in respect of duty ofCustoms, duty of Excise, Wealth Tax, Sales tax. There are no arrears of Provident Fund,Employees’ State Insurance, Income tax, Service Tax and Cess outstanding as at 31st March2015 for a period of more than six months from the date it becomes payable.

b. According to the information and explanations given to us, there are no dues of Income Tax,Wealth Tax, Service Tax, duty of Customs, duty of Excise, which have not been deposited onaccount of any dispute.

c. Based on the information and explanations obtained, the company has no liability orrequirement to transfer any amount to Investor Education & Protection Fund in accordancewith the relevant provisions of the Companies Act, 1956/2013 and the Rules thereunder.

8. The Company has no accumulated losses at the end of the year and has not incurred cash lossesduring the financial year covered by our audit or in the immediately preceding financial year.

9. The company has not defaulted in repayment of dues to the Bank from whom loan was borrowed.

(Referred to in our report of even date)

TVS CREDIT SERVICES LIMITED

27 Annual Report 2014-15

For V. Sankar Aiyar & Co.,Chartered AccountantsICAI Reg. No. 109208W

S. VenkatramanPlace: Chennai PartnerDate: June 23, 2015 M. No. 34319

10. The Company has not given any guarantees for loans taken by others from banks and financialinstitutions during the year. Hence, the requirement to report under para 3(x) does not arise.

11. In our opinion, the term loans taken during the year have, prima facie, been applied for thepurpose for which they were obtained.

12. During the course of our examination of the books and records of the Company carried out inaccordance with the generally accepted auditing practices in India and according to the informationand explanations given to us, no material fraud on the Company or by the Company has beennoticed or reported during the year except for 31 cases of frauds on the Company amounting toRs. 32.03 lakhs (Refer Additional Note no. 20.d to the financial statements) detected and arebeing dealt with by the management.

TVS CREDIT SERVICES LIMITED

28 Annual Report 2014-15

BALANCE SHEET AS AT MARCH 31, 2015 (Rs. In Lakhs)

As at As atParticulars Note 31st March 31st March

No. 2015 2014

As per our report of even date For and on behalf of the BoardFor V. SANKAR AIYAR & CO.Chartered AccountantsICAI Regn No. 109208WS. VENKATARAMAN VENU SRINIVASAN ANUPAM THAREJAPartner Chairman Wholetime DirectorMembership No. 34319Chennai K. SRIDHAR G. VENKATRAMAN V. GOPALAKRISHNANJune 23, 2015 Company Secretary Chief Executive Officer Chief Financial Officer

EQUITY AND LIABILITIESShareholders’ FundsShare Capital 2 12,870.00 10,810.00Reserves and Surplus 3 26,355.94 15,400.50

39,225.94 26,210.50Non-Current LiabilitiesLong Term Borrowings 4 72,063.63 57,719.22Other Long Term Liabilities 5 8,534.38 6,863.64Long Term Provisions 6 2,116.42 1,489.32

82,714.43 66,072.18Current LiabilitiesShort Term Borrowings 4 117,933.29 92,565.05Trade payables 8 1,548.43 2,034.00Other Current Liabilities 9 59,744.92 34,188.10Short-term Provisions 6 3,972.11 3,245.83

183,198.75 132,032.98Total 305,139.12 224,315.66

ASSETSNon-current AssetsFixed Assets(i) Tangible assets 10 3,660.28 3,301.02(ii) Intangible assets 10 111.60 189.89

3,771.88 3,490.91Long term loans and advances 11 1,631.43 889.32Other Non Current Asset (Vide Additional Note No. 22.5) 12 22,017.00 22,017.00Receivable from Financing Activities 13 112,973.63 68,075.14

136,622.06 90,981.46Deferred Tax Asset (net) - (Vide Additional Note No. 22.6) 1,382.49 835.29Current AssetsTrade receivables 14 171.83 172.61Cash and cash equivalents 15 15,420.68 17,994.55Short-term loans and advances 11 2,576.70 1,207.06Receivable from Financing Activities 13 144,992.89 109,633.78Other current assets 16 200.59 –

163,362.69 129,008.00Total 305,139.12 224,315.66Significant Accounting Policies forming part offinancial statements 1 00Additional Notes forming part of financial statements 22

TVS CREDIT SERVICES LIMITED

29 Annual Report 2014-15

STATEMENT OF PROFIT & LOSS FOR THE YEAR ENDED MARCH 31, 2015 (Rs. In Lakhs)

For the year For the yearParticulars Note ended 31st March ended 31st March

No. 2015 2014

INCOMERevenue from operations 17 57,203.09 39,945.20Other Income 18 387.26 68.17Total 57,590.35 40,013.37

EXPENSESFinance costs 19 20,875.86 15,399.65Business origination and Recovery Cost 7,866.94 4,944.51Employee benefits expense 20 14,461.72 11,153.75Depreciation and amortization expense 10 766.33 586.99Other expenses 21 7,023.80 4,584.47Bad debts Written Off 1,139.38 739.63Provision for bad and doubtful debts 7 1,054.74 792.38Total 53,188.77 38,201.38Profit before tax 4,401.58 1,811.99

Tax expense:Current Tax 2,027.33 706.77MAT Credit Entitlement – 136.69MAT Credit adjusted – 50.27Deferred Tax Liability/(Asset) (547.20) (801.38)Profit after tax for the year 2,921.45 1,719.64