Turnover Effects on Stock Price Performance in the High ...

24

Turnover Effects on Stock Price Performance in the High Fashion Industry: Chief Executive Officer versus Creative Director Author: Ugur Yuksel Student number: 10559086 Thesis supervisor: Jan Lemmen Finish date: July 2016 University of Amsterdam Faculty of Economics and Business BSc ECB – Bachelor of Science in Economics & Business Specialisation in Economics & Finance

Transcript of Turnover Effects on Stock Price Performance in the High ...

Turnover Effects on Stock Price Performance in the High Fashion Industry: Chief Executive Officer versus Creative Director

Author: Ugur Yuksel Student number: 10559086 Thesis supervisor: Jan Lemmen Finish date: July 2016

University of Amsterdam

Faculty of Economics and Business BSc ECB – Bachelor of Science in Economics & Business Specialisation in Economics & Finance

ii

ABSTRACT

This research sheds light on a particular turnover: the Creative Director. These Creative Directors are able to double firm value in a few years using the right creative strategy. The main purpose is to see if shareholders react to Creative Director turnovers as well as CEO turnovers. An event study is conducted on turnover announcements of Creative Directors and CEOs in the high fashion industry. MacKinlay’s (1997) event study methodology is used. The research resulted in significant effects on stock prices for both Creative Director turnovers as CEO turnovers, concluding that shareholders also react to Creative Director turnovers and therefore imply that they realise how important Creative Directors can be for a high fashion house.

KEYWORDS

turnovers, event study, finance, stocks, creative director, chief executive officer, CEO, fashion industry

JEL CLASSIFICATION

G14

Information and Market Efficiency/Event Studies

Statement of Orginality

This document is written by Student Ugur Yuksel who declares to take full responsibility for the contents

of this document.

I declare that the text and the work presented in this document is original and that no sources other than those mentioned in the text and its references have been used in creating it.

The Faculty of Economics and Business is responsible solely for the supervision of completion of the work, not for the contents.

iii

TABLE OF CONTENTS ABSTRACT ii TABLE OF CONTENTS iii LIST OF TABLES AND FIGURES iv 1. INTRODUCTION 1 2. LITERATURE REVIEW 2 3. METHODOLOGY 6 4. DATA 10 5. RESULTS 11 5.1 Creative Director Estimation - Window Regressions 12 5.2 Chief Executive Officer Estimation - Window Regressions 12

5.3 Significance Tests of the Turnover Effect 13

5.3.1 Event window [-5, +5] 14

5.3.2 Event window [-1, +1] 15

5.4 Overall Abnormal Return 15 5.4.1 Creative Director 16 5.4.2 Chief Executive Officer 17 6. CONCLUSIONS 18 REFERENCES 19

iv

LIST OF TABLES AND FIGURES

Figure 1 Estimation Window and Event Window 9

Figure 2 Plot of the overall average Abnormal Returns of CD turnovers 16

Figure 3 Plot of the overall average Abnormal Returns of CEO turnovers 17

Table 1 Turnovers and Fashion Houses 11

Table 2 Estimation Window Regression Results - CD 12

Table 3 Estimation Window Regression Results - CEO 13

Table 4 Actual Returns, Normal Returns and Abnormal Returns of CD Turnovers surrounding the announcement 13

Table 5 Actual Returns, Normal Returns and Abnormal Returns of CEO Turnovers surrounding the announcement 14

Table 6 Turnover Effect on Stock Prices - Significance Test Results

Event window [-5, +5] 14

Table 7 Turnover Effect on Stock Prices - Significance Test Results

Event window [-1, +1] 15

Table 8 Average overall Abnormal Returns 15

Table 9 Significance test on interval [-1, +1] of overall Abnormal Returns for CDs 16

Table 10 Significance test on interval [-3, +2] of overall Abnormal Returns for CEOs 17

1

1. INTRODUCTION

According to the Joint Economic Committee of the US Congress the global fashion industry was

worth $1.2 trillion dollars in 2015. In 2016, the website businessoffashion.com (BoF) was nominated

for a Webby Award which is called ‘The Internet’s highest honor’ by the New York Times. In an article

in Women’s Wear Daily (WWD) in 2009 Miles Socha argues that despite deep recession fashion firms

are performing well; Chanel’s couture business had an 10% increase in sales in 2008. Yet there has

been done little financial academic research about this trillion dollar industry with growing

popularity.

This research sheds light on top management turnover effects on stock prices of high fashion

houses in the fashion industry. For the term high fashion house the following definition is used in this

research: a fashion house that presents a couture collection at least once a year during fashion week

in Paris, Milan, London or New York using a runway show.

There has been done a lot of research in the past regarding management turnover effects on

stock prices outside the fashion industry. Warner, Watts and Wruck published a work in 1988 in

which one of their outcomes was that stock prices showed small, but statistically significant,

abnormal movement after a turnover announcement. This result supports the Efficient Market

Hypothesis (Fama, 1970) which claims that in efficient markets, stock prices reflect all available

information and therefore prices adjust to new information in the market. And there is more support

for the Efficient Market Hypothesis regarding top management turnover. When Angela Ahrendts,

former Chief Executive Officer (CEO) of Burberry, announced in 2013 that she was resigning her post,

share prices decreased with nearly 8% (Yahoo! Finance).

Boeker defined top management, in a research he did in 1997 about managerial

characteristics, as individuals directly reporting to a firm’s CEO. Warner, Watts and Wruck (1988)

define top management as CEOs, chairmen and presidents. But in fashion, there is another key

position which is at least as important as the CEO: the Creative Director (CD). The fashion industry is

extremely competitive which puts pressure on the ability of offering consumers the most actual

trends (Christopher et al., 2004). And that is where the CD pops his head out. The role of the CD at a

fashion house includes creative processes as managing clothing designs and setting up branding, but

also contributing to marketing and strategy. Having an highly creative and innovative CD is therefore

the only way to survive in the industry.

These CDs can make or break a brand and therefore are able to decrease or increase the

market value of a fashion house. For example, after Hedi Slimane started as CD of Yves Saint Laurent

in 2012, annual sales revenue more than doubled from €353 million in 2011 to €707 million in 2014.

But this holds not only for Slimane. After expanding the number of sales points and increasing sales

2

revenues of high fashion house Balenciaga, Nicolas Ghesquière resigned to accept the title of CD at

Louis Vuitton. After his appointment Ghesquière boosted sales growth resulting in fourth-quarter

sales which were above expectation.

With this said, it should be fair to assume that financial markets, beside CEO turnovers, also

react to CD turnovers. But is this really the case? This study examined the effect of CD turnovers on

stock prices and also compared it to the effect of CEO turnovers in the high fashion industry. This is

done by looking at the effects of six turnovers of CDs and six turnovers of CEOs between 2010 and

2016. The primarily purpose of this event study is to get an insight in whether or not the financial

markets react to CD turnovers in the fashion industry, while we know from previous research that

markets do react significantly to CEO or other top management turnovers.

2. LITERATURE REVIEW

The scientific research done about top management turnover mostly covers CEO and other top

management posts, but no CDs. Therefore, the literature reviewed does not cover CD turnovers.

The earlier mentioned Warner, Watts and Wruck (1988) researched the relation between

stock prices and top management turnovers. They used mean squared market model prediction

errors to measure abnormal stock return. No significant evidence was found regarding abnormal

stock returns before or at announcement. However, a variance shift test resulted in a small

significant reaction of stock prices at announcement, but this is called economically unimpressive by

the authors. For the post announcement period, evidence was found of a decrease in stock price

with a mean prediction error of -1.75% for day 5 through day 30 after announcement. The authors

mention that the 5-day lag is surprising given the fact that they found a reaction at announcement

earlier. In my opinion, this is a logical result assuming the existence of a small group of stockholders

who are experienced and therefore can make a quick decision about selling or holding their shares

immediately at announcement. On the other side, there is a bigger group of stockholders who need

time to do their research and act after an average of 5 days after announcement. The difference in

size of the two groups would also explain the fact that the reaction at announcement was smaller

than the price drop after the 5-day-period. However, there is no evidence that supports this theory

and therefore further research is required.

Denis and Denis (1995) found a significant relation between stock prices and top

management changes. They divided top management changes in forced resignations and normal

retirements. Their research resulted in evidence of negative pre-turnover abnormal stock returns for

firms with forced turnovers. Forced turnovers are mostly preceded by shareholder wealth losses in

3

contradiction to normal retirement turnovers. According to their research, forced turnovers have

higher positive effects on stock prices than non-forced turnovers. These findings are consistent with

the research done by Warner et al. and like them, Denis and Denis also note the fact these effects on

stock prices are economically small.

The findings of Denis and Denis are consistent with Huson, Malatesta, and Parrino (2004).

They found evidence on forced turnovers having a significantly positive effect on stock prices and in

periods preceding a forced turnover, the firms have poor financial performance as well. These results

imply that share prices go up after a firm announces that their top management will change, when

top management did not perform well in the preceding period, suggesting that investor expectations

are positive because they think better times are coming. But shareholders can be misguided by a

firms management turnover. Boeker (1992) claims that some of the top management turnovers that

take place are scapegoating, meaning that firms tend to dismiss CEOs or top management after a

period of poor performance because they need to show the public and shareholders that a head has

rolled, while he or she was not directly responsible for the poor performance. This implies that a not

only CEOs, but also CDs can be forced to resign after a poor preceding period, while he or she was

not responsible for the underperformance.

A research done by Egholm and Nordström (2011) resulted in a significant positive effect on

stock prices after a voluntary CEO turnover, and a negative effect on stock prices when a CEO

resigned after a poor performing period, which is assumed as a non-voluntary resign. This is in

contradiction in what is discussed in the earlier named researches. A small bias in the research of

Egholm and Nordström is the fact that they executed their research regarding Nordic markets

whereas the earlier discussed researches focused on the United States mainly. This can be due to

differences in firm- and market culture per country. Further, they conclude that company size does

not have a significant effect, where the distinction between an internal or external successor does.

An internal successor influences stock prices negatively on the announcement day. The authors claim

that this finding can be explained by the fact that external appointments are thought to bring new

strategies, knowledge and competencies to the firm. Besides these variables, they also added the

variable gender to their research, but they found no evidence that this influenced stock prices. The

latter can be explained, according to the authors, by the fact that Nordic countries are highly gender

equal.

One of the results that came out a research done by Bonnier and Bruner (1989) is that the

power of the position being filled in the top management group, has a large significant effect on

stock prices when turning over. This seems logical given that a CEO turnover has more impact on the

firm than a turnover of a manager who reports to the CEO. Interesting for my research is that

according to the research of Bonnier and Bruner, there can be concluded if a CD position in the high

4

fashion industry is seen as a powerful post by the shareholders. It would be surprising if shareholders

do not see a CD as a powerful position, given the fact that they are extremely important for a fashion

house (remember the earlier discussed CDs as Hedi Slimane). Presuccession performance has a

significant negative effect on stock prices (Friedman and Sigh, 1989) but given the fact that I only

look at resignations in my research, this succession related effect can be ignored. When a CD resigns,

there is almost never a successor immediately; this can take months.

Furtado and Rozeff (1987) conclude in their research Management Changes and Stock

Returns that capital markets ‘’pay attention and respond to news concerning management

appointments and dismissals’’. They find that a turnover in one of the top four posts of a firm has a

positive relation with wealth increases for shareholders. The effects are small, but significant. Again,

little economically impressive. Another result of their research is that external successions of the top

four posts are greeted in a more negative manner than internal successions. This contradicts the

findings of Egholm and Nördstrom mentioned earlier. But as earlier mentioned, this difference can

be explained by the fact that Egholm and Nördstrom looked at Nordic markets, where Furtado and

Rozeff focused on the United States. This again implies that financial market can react differently on

turnovers per country.

But what about the age of the turning over individual? In 1995 a study was published about

the relation between age and voluntary turnover by Healy, Lehman and McDaniel. They researched

this relation using a meta-analysis of a sample of 42625 individual turnovers between 1959 and 1993.

Healy et al. find a small relationship between age and turnover. A covariance of -0.08 to be precisely.

The sign of the covariance seems pretty logical, because it indicates an inverse relation between the

two variables; the older an individual gets, the more chance he or she resign voluntarily. Their results

contrasted the work of Rhodes (1983), who found a larger correlation.

Coughlan and Schmidt (1984) looked into the effect of compensation and turnover on stock

price performance. They name an agent problem which is very interesting. Simply said, they claim

that managers have incentives to act in short-term shareholder’s interest instead of long-term

benefits for the firm itself. To prevent this, firms have custom made compensation methods for their

executives. Coughlan and Schmidt researched the effect of compensation change on stock prices.

The results of this part of their research is not that interesting for my research. Another effect they

investigated is the effect of CEO turnover on stock prices, what is exactly what I did. They split the

CEO sample in two groups: older and younger than 64. For the sample younger than 64, a logit

regression shows that there is a significant inverse relation between a CEO turnover and abnormal

stock price performance. This result is not surprising. But for the turnovers of CEOs who are 64 and

older, the logit regression shows an insignificant but positive relation between stock price

performance and turnovers. Notable is the fact that the different sample groups have contradicting

5

results, although one is not significant. An explanation which sounds logical is the one that stock

prices react inversely to a young-CEO turnover because shareholders assume these CEOs did not

change because of old age and therefore the turnover is probably because of poor performance. So

according to this research, executives younger than 64, which CDs mostly are, have the odds against

them in this perspective.

Steven Kaplan (1994) also researched top executive turnover effects on stock prices, but did

this for the United States and Japan to compare both countries with each other. A little bias arises

from his research method because Kaplan compares CEOs from the United States with Japanese

Presidents. We can agree that these two top executives play a different role in the daily management

of a firm. His findings for Japan are a bit strange. President turnover in Japan is not significantly

related to any of the performance measures Kaplan worked with, which are stock return, sales

growth and change in pretax income. He explains this by claiming that it is standard for Japanese top

executives to resign their posts at regular intervals without regard to firm performance. However,

when taking non-standard top executive turnovers, Kaplan finds a significant inverse relationship

between the turnovers and all the performance measures, except for sales growth. What is

interesting for my research is the fact that, just like most of the earlier mentioned researchers,

Kaplan finds an inverse relation between stock prices and top management turnover. For United

States CEO turnover, he finds inverse relationship with all the performance measures. These

performance measures all are statistically significant with stock prices adding the most power. This

indicates that stock prices are a very good statistically measure of firm performance, which supports

my method of using stock prices in this research.

A recent study, published in 2015, done by Jenter and Kanaan about CEO turnovers on stock

prices sheds a light on another aspect of the turnover. They focus on the reasons a CEO is forced to

resign, or simply said fired. In their abstract they claim that they found evidence on the fact that

CEOs are often fired after bad firm performance caused by factors beyond their control. For example,

they documented that low industry stock returns increase the probability of a board firing a CEO. This

supports the earlier mentioned scapegoating in which firms just need to let a head roll in bad

performance periods to let the public and shareholders know they are taking measures. Jenter and

Kanaan mention also that boards try to filter these factors beyond a CEO’s control when measuring

the quality of a CEO, but that these filters are too weak to remove the overall effects. That suggests

that boards probably know most of the time that their decision of firing a CEO is based on an

exogenous shock beyond CEO control. The fact that boards know this and still fire CEOs in these

cases again supports the scapegoating-theory. Also, the fact that CEO turnover is affected by

industry performance makes it almost mandatory to control for market- or industry-performance

when researching stock prices, which I did.

6

The earlier mentioned Egholm and Nordström (2011) found no evidence on stock price reactions

regarding the gender of the turning over individual in Nordic countries. Weisberg and Kirschenbaum

(1993) also studied gender in turnovers. They start their research with explaining that there are

different work values and a different work environment for men and women. For example, as we all

know are woman most of the time influenced by factors as the availability of childcare. Brief and

Nord (1990) claimed that because of these factors, women experience more conflict of priorities

between work and for example family. In contradiction to Egholm and Nordström, Weisberg and

Kirschenbaum found evidence on a significant effect of gender on turnovers. They also found that

women have significantly shorter lengths of service in firms and a lower wage level. Like mentioned

earlier, the contradiction that arises can be due to the fact that Nordic countries are very gender

equal. Weisberg and Kirschenbaum (1993) used a sample of 506 textile workers in Israel, which is in

cultural view a very different country than the Nordic countries. With respect to my research about

the fashion industry, I am not worried about the gender-effect. It is logical to assume that the fashion

industry is one of the most open minded industries in the world, both in gender as in sexual

orientation. Fashion is globally seen as a more woman-thing and the fact that a lot of CDs are

homosexual supports my way of thinking about the fashion industry’s very equal character. In fact, I

strongly believe this industry has a more equal and open-minded character than the Nordic

countries, in which gender did not play a role, but further research is required to validate this

assumption.

3. METHODOLOGY

This research follows the event study methodology that MacKinlay published in 1997 in his work

Event Studies in Economics and Finance. In his paper, MacKinlay describes an event study as follows:

Using financial market data, an event study measures

the impact of a specific event on the value of a firm.

Event studies are besides this, also used for another purpose: testing the efficient market hypothesis.

By researching the effect of information on financial markets, one can conclude how efficient

markets process new information, and therefore how efficient the market is.

In my research, the event is a turnover announcement of a CD or CEO of a high fashion

house. As mentioned earlier, for the term high fashion house the following definition is used: a

fashion house that presents a couture collection at least once a year during fashion week in Paris,

7

Milan, London or New York using a runway show. Instead of taking the official resignation dates, this

research looks at the moment of announcement, because financial markets start reacting to

information when the information is publicly available (Fama, 1970). Mention the words start

reacting in the latter sentence. As we have seen in the research done by Warner, Watts and Wruck

(1988), a large group of shareholders reacted to an event after five days. An explanation for this was

that shareholders start to do their research, simply said make up their mind, about a turnover and

react to the announcement later. This is important for the event window, but more about the event

window later.

MacKinlay’s method uses abnormal returns to measure the impact of an event. Assuming

normality in stock prices, the abnormal return of for firm i and time period t is given by:

𝐴𝑅𝑖𝑡 = 𝑅𝑖𝑡 − 𝐸(𝑅𝑖𝑡|𝑋𝑡)

With:

𝐴𝑅𝑖𝑡 = 𝑎𝑏𝑛𝑜𝑟𝑚𝑎𝑙 𝑟𝑒𝑡𝑢𝑟𝑛

𝑅𝑖𝑡 = 𝑎𝑐𝑡𝑢𝑎𝑙 𝑟𝑒𝑡𝑢𝑟𝑛

𝐸(𝑅𝑖𝑡|𝑋𝑡) = 𝑛𝑜𝑟𝑚𝑎𝑙 𝑟𝑒𝑡𝑢𝑟𝑛

Normal returns are defined by the expected return when the event would not have taken place.

MacKinlay distinguishes between two models; the constant mean return model and the market

model. Because the market model is not based on only statistics but also considers investor behavior,

the market model is used in this research. Also, the market model controls for market abnormalities,

which is almost mandatory to include when researching stock prices which are sensitive for market-

and industry shocks. Remember the conclusion of Jenter and Kanaan (2015) in the chapter Literature

Review.

The market model computes the normal returns (𝐸(𝑅𝑖𝑡|𝑋𝑡)) using an equation based on the

commonly known CAPM method. Central in this method is the use of betas to determine the returns

of a stock. Beta measures the correlation with the market return. For example, a beta of 1.3 implies

that the stock price of the firm increases with 1.3 times the increase in the market. These betas are

determined using a regression with the following equation:

𝑅𝑖𝑡 = 𝐸(𝑅𝑖𝑡|𝑋𝑡) = 𝛼𝑖 + 𝛽𝑖 𝑅𝑚𝑎𝑟𝑘𝑒𝑡 + 𝜀𝑖

𝐸(𝜀𝑖𝑡 = 0) 𝑣𝑎𝑟(𝜀𝑖𝑡) = 𝜎𝜀2

𝑖

8

MacKinlay claims is his paper that the market model is an improved model of the constant mean

return model, because it removes the amount of return that is related to the market and therefore

the variance is reduced. In contrast, he also notes that there is proof of deviations from CAPM which

raises questions about the validity of it. However, a more elaborate model like the 3-factor model

could have been used, but the market model is still a very suitable method for an event study like

this one.

There is some discussion about the validity of stock return as a performance measure. The

earlier mentioned study of Kaplan (1994) used different performance measures to determine the

effect of CEO turnover on stock prices. Like said, all of the performance measures were statistically

significant, which results in a high power. Out of the performance measures, stock prices were

adding the most power to his research. This implies not only that stock prices are the best measure

out of the measures he used, but also that stock prices are a good overall measure of firm

performance. Also, McWilliams and Siegel (1997) argue that stock prices are a good measure

because it reflects the true value of firms according to investors and shareholders, with relevant

information processed in the price.

There can be a lot said about the measuring periods before, during and after the event. The

whole period is split up in two windows. The estimation window is the period before the event, and

in this case the event is the announcement. This period is defined from T0 to T1 in Figure 1 below. The

purpose of this window is to measure the correlation of the stock with the market, also known as the

earlier mentioned beta. This period needs to be long enough to estimate a solid beta, but also short

enough to avoid periods of static stock prices. Therefore, MacKinlay advices a 120-day estimation

window (Egholm and Nordström, 2011). Also, the estimation should not overlap with the event

window. To get significant betas, different estimation windows have been used for different

companies. These estimation windows differ between 50-days and 200-days.

After the estimation window comes the event window. This is the period in which the event

is taking place. In the case of a turnover announcement this window should be one day. However,

MacKinley argues that choosing an event window longer than one day minimizes the error that the

announcement came out on a Saturday, Sunday or a Friday late afternoon. He also recommends to

include a few days before the announcement date to minimize the error when people inside the firm

have information about a turnover before announcement. In this research there has been chosen to

test two event windows on the following intervals:

[-5, +5] and [-1, +1]

with [T1, T2]

9

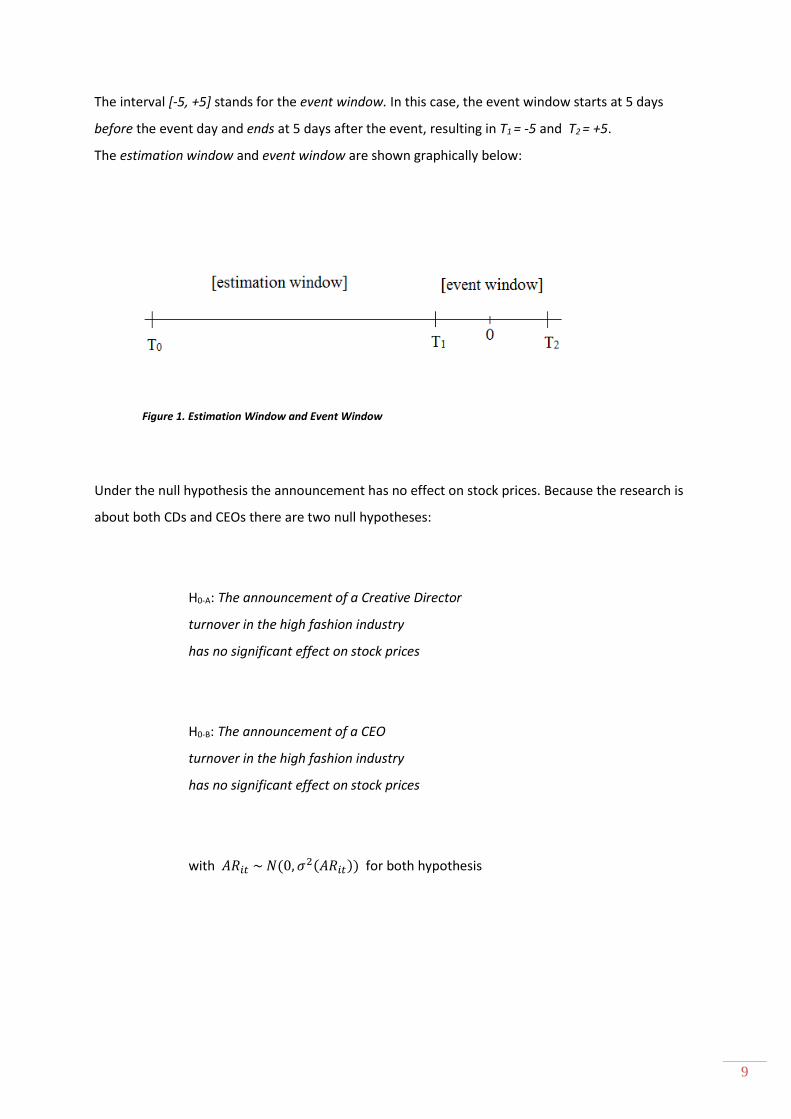

The interval [-5, +5] stands for the event window. In this case, the event window starts at 5 days

before the event day and ends at 5 days after the event, resulting in T1 = -5 and T2 = +5.

The estimation window and event window are shown graphically below:

Figure 1. Estimation Window and Event Window

Under the null hypothesis the announcement has no effect on stock prices. Because the research is

about both CDs and CEOs there are two null hypotheses:

H0-A: The announcement of a Creative Director

turnover in the high fashion industry

has no significant effect on stock prices

H0-B: The announcement of a CEO

turnover in the high fashion industry

has no significant effect on stock prices

with 𝐴𝑅𝑖𝑡 ~ 𝑁(0, 𝜎2(𝐴𝑅𝑖𝑡)) for both hypothesis

10

After the abnormal returns are computed, the significance needs to be tested. This is done using

average cumulative abnormal returns (CAR) of the event window [T1, T2] and the MacKinlay (1997)

test statistic:

𝜃 =CAR(T1, T2)

𝑣𝑎𝑟 (CAR(T1, T2))

12

~𝑁(0,1)

Boehmer, Musumeci and Poulsen (1991) state in their work about event study methodology that

parametric significance tests, like the one explained above, are often conducted in combination with

non-parametric test to double check significance of a certain event. The non-parametric test they

write about is the sign test, in which the proportion of positive abnormal returns in the event

window are tested on the hypothesis that this number is equal to 0.5. However, the writers also

mention that there is a problem with this approach mentioning that Fama (1970) found evidence on

the fact that returns are skewed to the right, implying a proportion of 0.5 is useless. Also, the sign

test is heavily criticised after a research conducted by Brown and Warner (1980). In their research,

they looked into measuring security performance in various ways. One of their claims is that the sign

test suffer from at least the same problems as parametric t-test. Besides that, they find that non-

parametric tests reject the null hypothesis not often enough when testing for positive returns. Their

overall conclusion about event study methodology is that they found no evidence that there is a

better method than using a simple, one-factor market model. With respect to testing significance,

their advice is to use a parametric t-test. These are the main reasons my research is conducted using

MacKinlay’s market model and his proposed parametric significance test, without adding a non-

parametric test like the sign test to it.

4. DATA

The CD en CEO turnovers are found on websites of BoF, WWD, VogueUK , The Wall Street Journal

and Forbes. The exact announcement dates are found by looking at the date of the article of a certain

turnover and searching for signs like yesterday or for example last Friday for both CDs and CEOs. The

used websites are renowned fashion watchers with high reliability of the published articles. The Wall

Street Journal and Forbes are renowned sources for business publications, making it reliable as well.

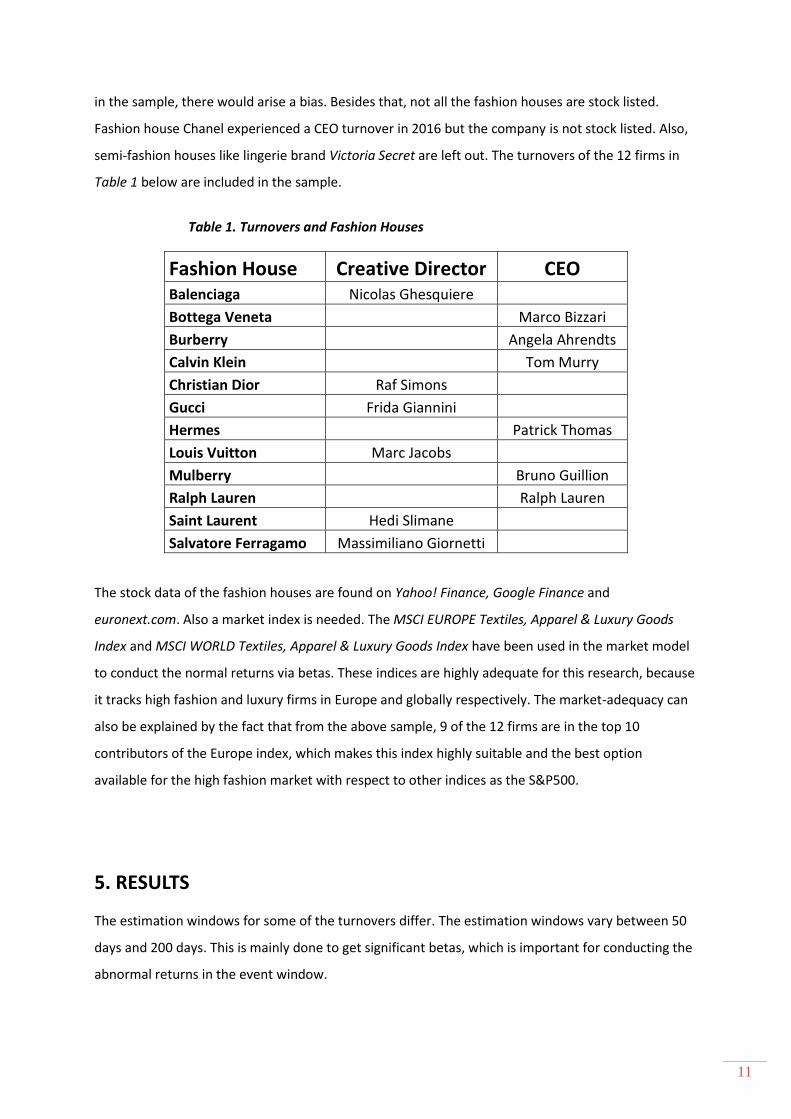

To exclude biases as much as possible and in order to obtain a balanced sample, some of the

found turnovers are left out. For example, if a CEO resigns to start working for another fashion house

11

in the sample, there would arise a bias. Besides that, not all the fashion houses are stock listed.

Fashion house Chanel experienced a CEO turnover in 2016 but the company is not stock listed. Also,

semi-fashion houses like lingerie brand Victoria Secret are left out. The turnovers of the 12 firms in

Table 1 below are included in the sample.

Table 1. Turnovers and Fashion Houses

The stock data of the fashion houses are found on Yahoo! Finance, Google Finance and

euronext.com. Also a market index is needed. The MSCI EUROPE Textiles, Apparel & Luxury Goods

Index and MSCI WORLD Textiles, Apparel & Luxury Goods Index have been used in the market model

to conduct the normal returns via betas. These indices are highly adequate for this research, because

it tracks high fashion and luxury firms in Europe and globally respectively. The market-adequacy can

also be explained by the fact that from the above sample, 9 of the 12 firms are in the top 10

contributors of the Europe index, which makes this index highly suitable and the best option

available for the high fashion market with respect to other indices as the S&P500.

5. RESULTS

The estimation windows for some of the turnovers differ. The estimation windows vary between 50

days and 200 days. This is mainly done to get significant betas, which is important for conducting the

abnormal returns in the event window.

Fashion House Creative Director CEO Balenciaga Nicolas Ghesquiere

Bottega Veneta Marco Bizzari

Burberry Angela Ahrendts

Calvin Klein Tom Murry

Christian Dior Raf Simons

Gucci Frida Giannini

Hermes Patrick Thomas

Louis Vuitton Marc Jacobs

Mulberry Bruno Guillion

Ralph Lauren Ralph Lauren

Saint Laurent Hedi Slimane

Salvatore Ferragamo Massimiliano Giornetti

12

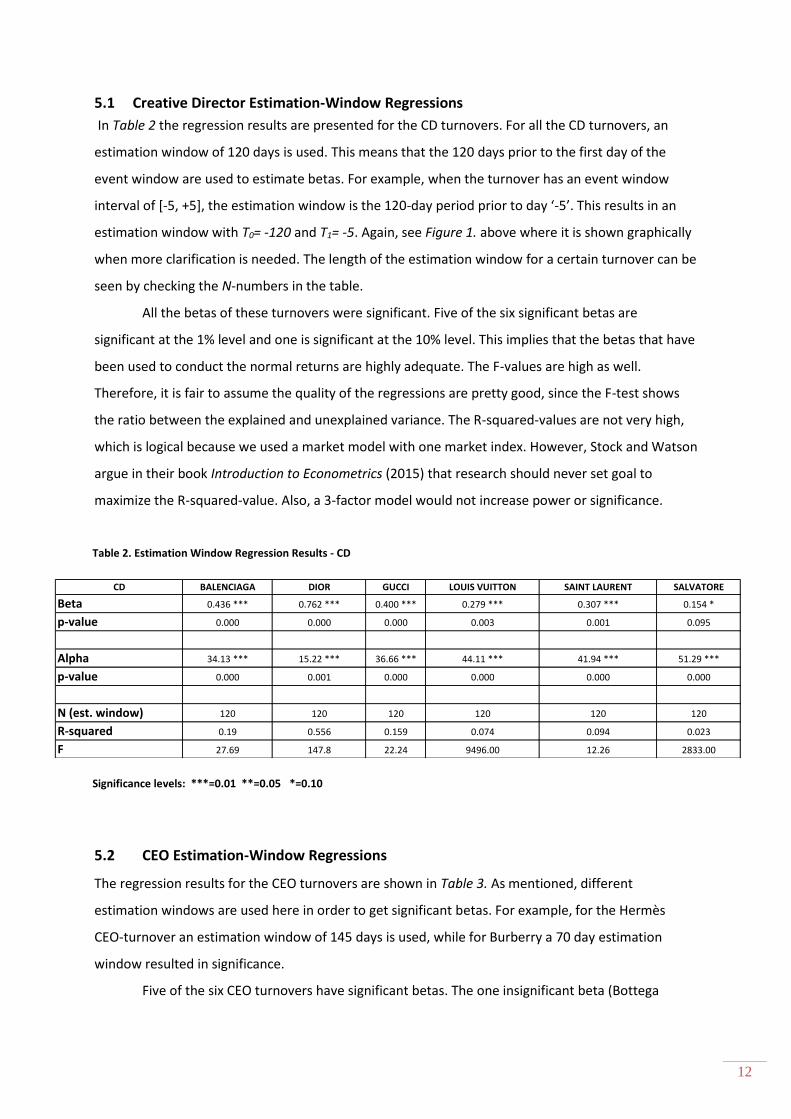

5.1 Creative Director Estimation-Window Regressions

In Table 2 the regression results are presented for the CD turnovers. For all the CD turnovers, an

estimation window of 120 days is used. This means that the 120 days prior to the first day of the

event window are used to estimate betas. For example, when the turnover has an event window

interval of [-5, +5], the estimation window is the 120-day period prior to day ‘-5’. This results in an

estimation window with T0= -120 and T1= -5. Again, see Figure 1. above where it is shown graphically

when more clarification is needed. The length of the estimation window for a certain turnover can be

seen by checking the N-numbers in the table.

All the betas of these turnovers were significant. Five of the six significant betas are

significant at the 1% level and one is significant at the 10% level. This implies that the betas that have

been used to conduct the normal returns are highly adequate. The F-values are high as well.

Therefore, it is fair to assume the quality of the regressions are pretty good, since the F-test shows

the ratio between the explained and unexplained variance. The R-squared-values are not very high,

which is logical because we used a market model with one market index. However, Stock and Watson

argue in their book Introduction to Econometrics (2015) that research should never set goal to

maximize the R-squared-value. Also, a 3-factor model would not increase power or significance.

5.2 CEO Estimation-Window Regressions

The regression results for the CEO turnovers are shown in Table 3. As mentioned, different

estimation windows are used here in order to get significant betas. For example, for the Hermès

CEO-turnover an estimation window of 145 days is used, while for Burberry a 70 day estimation

window resulted in significance.

Five of the six CEO turnovers have significant betas. The one insignificant beta (Bottega

Table 2. Estimation Window Regression Results - CD

Significance levels: ***=0.01 **=0.05 *=0.10

CD BALENCIAGA DIOR GUCCI LOUIS VUITTON SAINT LAURENT SALVATORE

Beta 0.436 *** 0.762 *** 0.400 *** 0.279 *** 0.307 *** 0.154 *

p-value 0.000 0.000 0.000 0.003 0.001 0.095

Alpha 34.13 *** 15.22 *** 36.66 *** 44.11 *** 41.94 *** 51.29 ***

p-value 0.000 0.001 0.000 0.000 0.000 0.000

N (est. window) 120 120 120 120 120 120

R-squared 0.19 0.556 0.159 0.074 0.094 0.023

F 27.69 147.8 22.24 9496.00 12.26 2833.00

13

Veneta) has the estimation window that resulted in the highest significance. Three of the five

significant betas are significant at an 1% level and the other two are significant at a 10% level. Like

the F-values of the CD regressions, the F-values of the CEO regressions are high as well. The R-

squared-values are low, but a high R-squared-value should never be a goal and a 3-factor model

would not increase power or significance, like earlier said.

5.3 Significance Tests of the Turnover Effect

Using these regression results, the normal returns are computed. The normal returns are then

deducted from the actual returns, resulting in an abnormal return (AR). These can be found in Table

4 and Table 5.

Table 3. Estimation Window Regression Results - CEO

CEO BURBERRY CALVIN KLEIN HERMES RALPH LAUREN BOTTEGA MULBERRY

Beta 0.217 * 0.352 *** 0.473 *** 0.368 * 0.0495 0.510 ***

p-value 0.076 0.000 0.000 0.084 0.162 0.000

Alpha 26.98 *** 47.61 *** 23.15 *** (-63.02) 72.77 *** (-176.5) ***

p-value 0.000 0.000 0.004 0.41 0.000 0.001

N (est. window) 70 145 145 50 200 140

R-squared 0.046 0.123 0.242 0.061 0.01 0.153

F 3254.00 20.09 45.71 3115.00 1.97 24.84

Significance levels: ***=0.01 **=0.05 *=0.10

CD

Actual Return Normal Return AR Actual Return Normal Return AR Actual Return Normal Return AR

5 0.00888 -0.00089 0.00977 0.00306 0.00213 0.00093 0.00516 -0.00811 0.01327

4 0.01053 0.01750 -0.00698 0.00223 0.00308 -0.00086 0.01575 -0.00163 0.01738

3 0.02478 -0.00111 0.02589 0.00168 -0.00519 0.00686 -0.00684 0.00575 -0.01259

2 0.00765 -0.00313 0.01078 -0.00776 -0.00359 -0.00416 0.01053 -0.00097 0.01151

1 0.02013 -0.00652 0.02666 0.02763 0.02126 0.00637 -0.02409 -0.00027 -0.02383

0 0.00454 0.00586 -0.00133 0.03174 0.02258 0.00916 -0.02015 -0.00196 -0.01818

-1 0.00207 0.00226 -0.00019 0.00830 0.00300 0.00530 -0.00812 -0.00217 -0.00595

-2 0.00582 -0.00490 0.01072 -0.00736 -0.00606 -0.00129 -0.00218 0.00397 -0.00616

-3 0.00166 0.00237 -0.00071 0.00206 0.00075 0.00132 -0.02044 0.00172 -0.02216

-4 0.00503 0.01021 -0.00518 -0.01078 -0.01232 0.00153 -0.00997 0.00055 -0.01052

-5 -0.00790 -0.00567 -0.00223 -0.00058 -0.00188 0.00130 0.00853 -0.00005 0.00859

CD

Actual Return Normal Return AR Actual Return Normal Return AR Actual Return Normal Return AR

5 -0.00485 -0.00307 -0.00178 0.00532 0.00173 0.00359 -0.00409 0.00045 -0.00454

4 -0.00586 -0.00190 -0.00395 -0.01990 -0.00388 -0.01602 -0.01870 -0.00187 -0.01683

3 -0.01056 -0.00208 -0.00848 0.01055 0.00191 0.00863 -0.00223 -0.00279 0.00056

2 0.00652 0.00041 0.00611 -0.02506 -0.00562 -0.01944 0.02228 0.00411 0.01817

1 0.00691 0.00135 0.00555 0.01203 0.00089 0.01114 0.02704 0.00166 0.02538

0 -0.02229 -0.00349 -0.01880 -0.02132 -0.00372 -0.01760 -0.02592 -0.00297 -0.02295

-1 0.01683 0.00315 0.01368 -0.02574 -0.00557 -0.02017 -0.00135 0.00184 -0.00319

-2 -0.00308 -0.00122 -0.00187 0.03365 0.00819 0.02546 -0.03377 -0.00116 -0.03261

-3 -0.00714 -0.00008 -0.00706 0.01530 0.00332 0.01198 0.00710 -0.00165 0.00875

-4 -0.00203 -0.00210 0.00007 -0.02753 -0.00593 -0.02160 0.03048 0.00094 0.02954

-5 -0.00741 -0.00024 -0.00716 -0.00158 0.00367 -0.00525 0.00548 -0.00248 0.00796

LOUIS VUITTON SAINT LAURENT SALVATORE

BALENCIAGA DIOR GUCCI

Table 4. Actual Returns, Normal Returns and Abnormal Returns of CD Turnovers surrounding the announcement

14

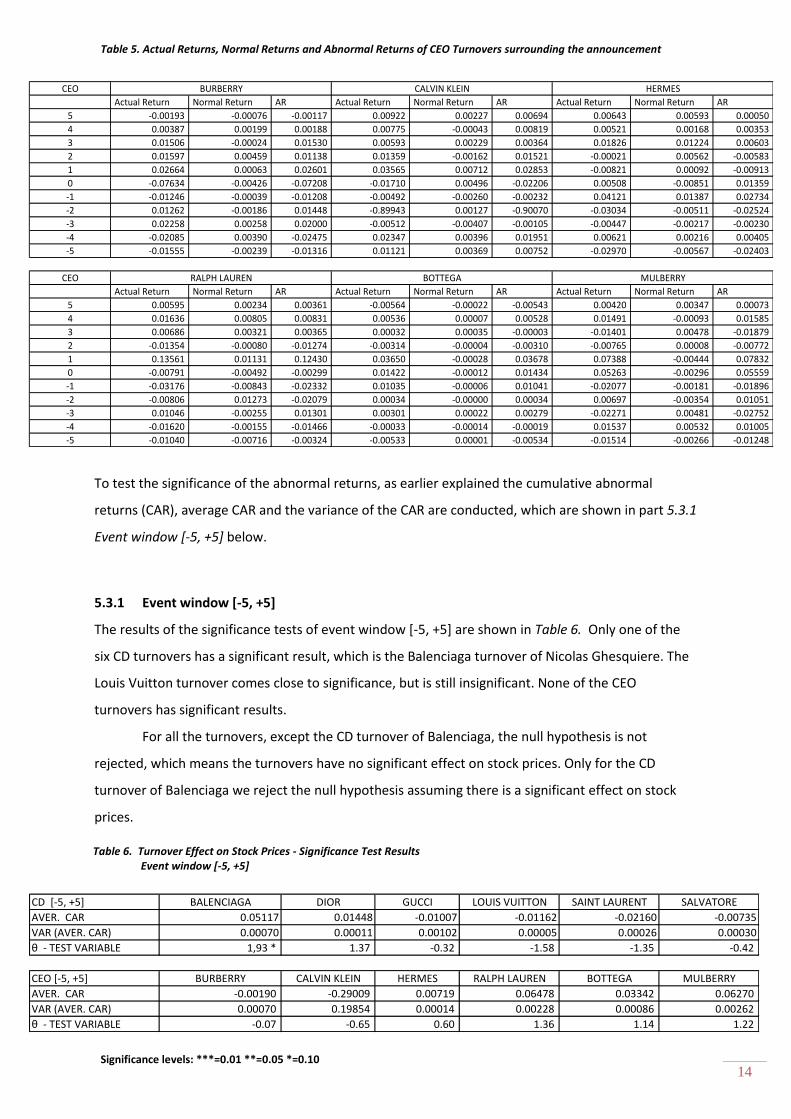

Table 5. Actual Returns, Normal Returns and Abnormal Returns of CEO Turnovers surrounding the announcement

To test the significance of the abnormal returns, as earlier explained the cumulative abnormal

returns (CAR), average CAR and the variance of the CAR are conducted, which are shown in part 5.3.1

Event window [-5, +5] below.

5.3.1 Event window [-5, +5]

The results of the significance tests of event window [-5, +5] are shown in Table 6. Only one of the

six CD turnovers has a significant result, which is the Balenciaga turnover of Nicolas Ghesquiere. The

Louis Vuitton turnover comes close to significance, but is still insignificant. None of the CEO

turnovers has significant results.

For all the turnovers, except the CD turnover of Balenciaga, the null hypothesis is not

rejected, which means the turnovers have no significant effect on stock prices. Only for the CD

turnover of Balenciaga we reject the null hypothesis assuming there is a significant effect on stock

prices.

Significance levels: ***=0.01 **=0.05 *=0.10

Table 6. Turnover Effect on Stock Prices - Significance Test Results Event window [-5, +5]

CEO

Actual Return Normal Return AR Actual Return Normal Return AR Actual Return Normal Return AR

5 -0.00193 -0.00076 -0.00117 0.00922 0.00227 0.00694 0.00643 0.00593 0.00050

4 0.00387 0.00199 0.00188 0.00775 -0.00043 0.00819 0.00521 0.00168 0.00353

3 0.01506 -0.00024 0.01530 0.00593 0.00229 0.00364 0.01826 0.01224 0.00603

2 0.01597 0.00459 0.01138 0.01359 -0.00162 0.01521 -0.00021 0.00562 -0.00583

1 0.02664 0.00063 0.02601 0.03565 0.00712 0.02853 -0.00821 0.00092 -0.00913

0 -0.07634 -0.00426 -0.07208 -0.01710 0.00496 -0.02206 0.00508 -0.00851 0.01359

-1 -0.01246 -0.00039 -0.01208 -0.00492 -0.00260 -0.00232 0.04121 0.01387 0.02734

-2 0.01262 -0.00186 0.01448 -0.89943 0.00127 -0.90070 -0.03034 -0.00511 -0.02524

-3 0.02258 0.00258 0.02000 -0.00512 -0.00407 -0.00105 -0.00447 -0.00217 -0.00230

-4 -0.02085 0.00390 -0.02475 0.02347 0.00396 0.01951 0.00621 0.00216 0.00405

-5 -0.01555 -0.00239 -0.01316 0.01121 0.00369 0.00752 -0.02970 -0.00567 -0.02403

CEO

Actual Return Normal Return AR Actual Return Normal Return AR Actual Return Normal Return AR

5 0.00595 0.00234 0.00361 -0.00564 -0.00022 -0.00543 0.00420 0.00347 0.00073

4 0.01636 0.00805 0.00831 0.00536 0.00007 0.00528 0.01491 -0.00093 0.01585

3 0.00686 0.00321 0.00365 0.00032 0.00035 -0.00003 -0.01401 0.00478 -0.01879

2 -0.01354 -0.00080 -0.01274 -0.00314 -0.00004 -0.00310 -0.00765 0.00008 -0.00772

1 0.13561 0.01131 0.12430 0.03650 -0.00028 0.03678 0.07388 -0.00444 0.07832

0 -0.00791 -0.00492 -0.00299 0.01422 -0.00012 0.01434 0.05263 -0.00296 0.05559

-1 -0.03176 -0.00843 -0.02332 0.01035 -0.00006 0.01041 -0.02077 -0.00181 -0.01896

-2 -0.00806 0.01273 -0.02079 0.00034 -0.00000 0.00034 0.00697 -0.00354 0.01051

-3 0.01046 -0.00255 0.01301 0.00301 0.00022 0.00279 -0.02271 0.00481 -0.02752

-4 -0.01620 -0.00155 -0.01466 -0.00033 -0.00014 -0.00019 0.01537 0.00532 0.01005

-5 -0.01040 -0.00716 -0.00324 -0.00533 0.00001 -0.00534 -0.01514 -0.00266 -0.01248

HERMESCALVIN KLEINBURBERRY

RALPH LAUREN BOTTEGA MULBERRY

CD [-5, +5] BALENCIAGA DIOR GUCCI LOUIS VUITTON SAINT LAURENT SALVATORE

AVER. CAR 0.05117 0.01448 -0.01007 -0.01162 -0.02160 -0.00735

VAR (AVER. CAR) 0.00070 0.00011 0.00102 0.00005 0.00026 0.00030

θ - TEST VARIABLE 1,93 * 1.37 -0.32 -1.58 -1.35 -0.42

CEO [-5, +5] BURBERRY CALVIN KLEIN HERMES RALPH LAUREN BOTTEGA MULBERRY

AVER. CAR -0.00190 -0.29009 0.00719 0.06478 0.03342 0.06270

VAR (AVER. CAR) 0.00070 0.19854 0.00014 0.00228 0.00086 0.00262

θ - TEST VARIABLE -0.07 -0.65 0.60 1.36 1.14 1.22

15

5.3.2 Event window [-1, +1]

In Table 7 the results of event window [-1, +1] are summarized. It seems that narrowing down the

event window helped improving the significance of the turnover effects. The significance of this

event window is higher, resulting in significance for three of the six CD turnovers and also three of

the six CEO turnovers.

For the CDs, two of the three turnovers are significant at the 1% level and the other one at

10%. The other three insignificant ones are far from significant. The three significant CEO turnovers

all are significant at 1% level.

The null hypothesis is not rejected for the CD turnovers of Louis Vuitton, Saint Laurent and

Salvatore Ferragamo and the CEO turnovers of Burberry, Calvin Klein and Hermes. This means the

turnovers have no significant effect on stock prices. For the CD turnovers of Balenciaga, Dior and

Gucci and the CEO turnovers of Ralph Lauren, Bottega Veneta and Mulberry the null hypothesis is

rejected implying there is a significant effect of the turnover on stock prices.

5.4 Overall Abnormal Return

The tests conducted above measure the turnover effects for the fashion houses individually. Besides

that, the turnovers are also tested all together for CDs and CEOs. The arithmetic average of every

event window day is taken to measure the average daily AR. These are summarized in Table 8 below.

Table 7. Turnover Effect on Stock Prices - Significance Test Results Event window [-1, +1]

Significance levels: ***=0.01 **=0.05 *=0.10

CD [-1, +1] BALENCIAGA DIOR GUCCI LOUIS VUITTON SAINT LAURENT SALVATORE

AVER. CAR 0.02571 0.01424 -0.03793 -0.00242 -0.00732 0.00902

VAR (AVER. CAR) 0.00000 0.00005 0.00016 0.00009 0.00036 0.00020

θ - TEST VARIABLE 31,17 *** 1,94 * (-3,02) *** -0.25 -0.39 0.63

CEO [-1, +1] BURBERRY CALVIN KLEIN HERMES RALPH LAUREN BOTTEGA MULBERRY

AVER. CAR -0.02607 0.01305 0.00904 0.11453 0.04981 0.10906

VAR (AVER. CAR) 0.00207 0.00018 0.00043 0.00021 0.00015 0.00080

θ - TEST VARIABLE -0.57 0.97 0.43 7,95 *** 4,01 *** 3,86 ***

CD Average AR CEO Average AR

5 0.00354 5 0.00087

4 -0.00454 4 0.00717

3 0.00348 3 0.00163

2 0.00383 2 -0.00047

1 0.00854 1 0.04747

0 -0.01162 0 -0.00227

-1 -0.00175 -1 -0.00315

-2 -0.00096 -2 -0.15357

-3 -0.00131 -3 0.00082

-4 -0.00103 -4 -0.00100

-5 0.00053 -5 -0.00845

Table 8. Average overall Abnormal Returns

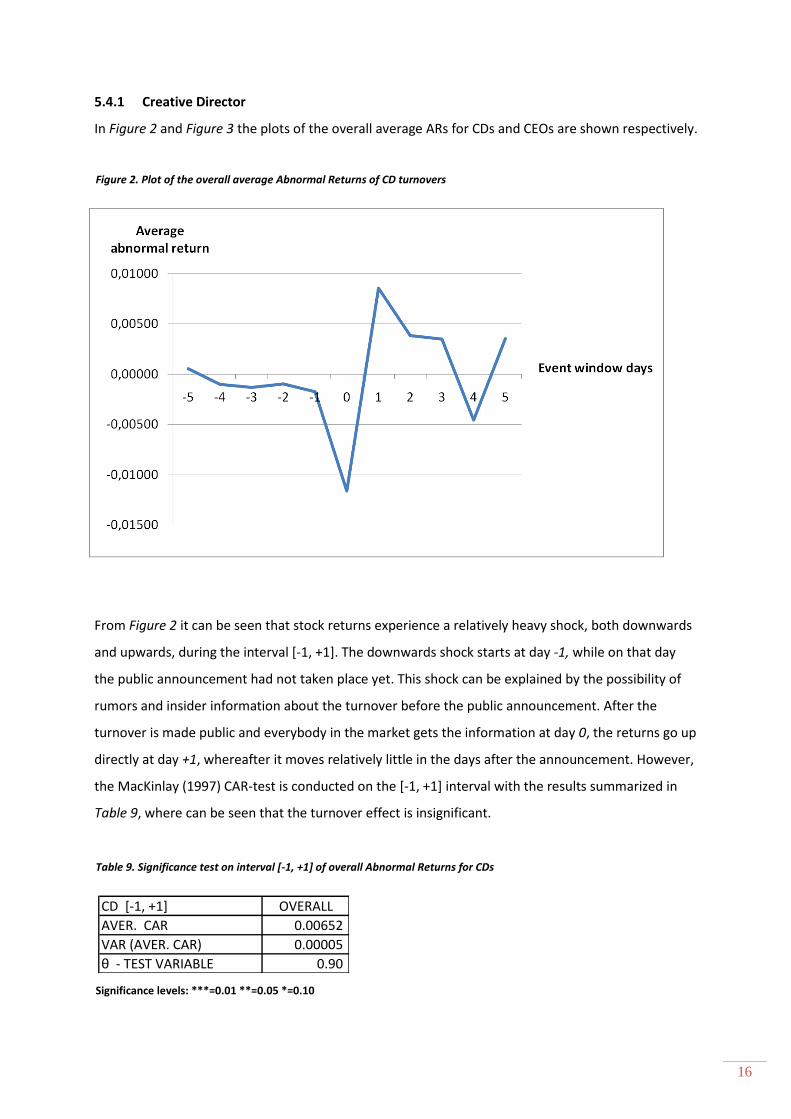

16

5.4.1 Creative Director

In Figure 2 and Figure 3 the plots of the overall average ARs for CDs and CEOs are shown respectively.

From Figure 2 it can be seen that stock returns experience a relatively heavy shock, both downwards

and upwards, during the interval [-1, +1]. The downwards shock starts at day -1, while on that day

the public announcement had not taken place yet. This shock can be explained by the possibility of

rumors and insider information about the turnover before the public announcement. After the

turnover is made public and everybody in the market gets the information at day 0, the returns go up

directly at day +1, whereafter it moves relatively little in the days after the announcement. However,

the MacKinlay (1997) CAR-test is conducted on the [-1, +1] interval with the results summarized in

Table 9, where can be seen that the turnover effect is insignificant.

Figure 2. Plot of the overall average Abnormal Returns of CD turnovers

CD [-1, +1] OVERALL

AVER. CAR 0.00652

VAR (AVER. CAR) 0.00005

θ - TEST VARIABLE 0.90

Table 9. Significance test on interval [-1, +1] of overall Abnormal Returns for CDs

Significance levels: ***=0.01 **=0.05 *=0.10

17

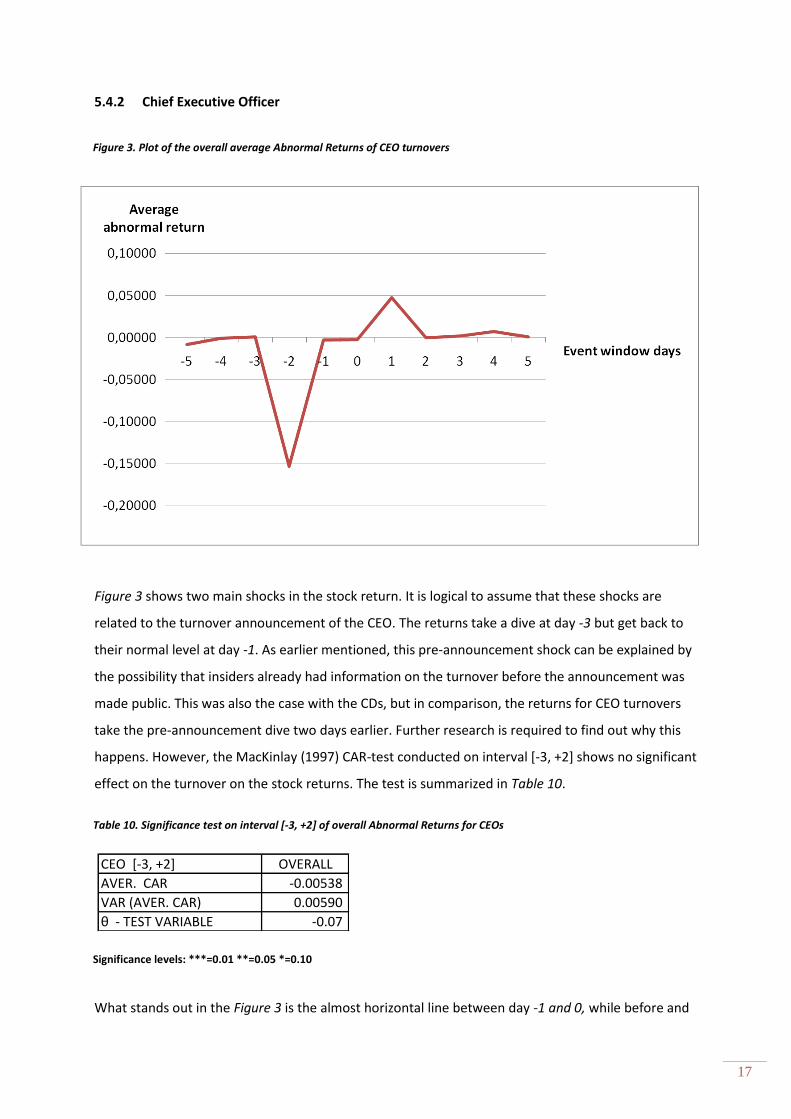

5.4.2 Chief Executive Officer

Figure 3 shows two main shocks in the stock return. It is logical to assume that these shocks are

related to the turnover announcement of the CEO. The returns take a dive at day -3 but get back to

their normal level at day -1. As earlier mentioned, this pre-announcement shock can be explained by

the possibility that insiders already had information on the turnover before the announcement was

made public. This was also the case with the CDs, but in comparison, the returns for CEO turnovers

take the pre-announcement dive two days earlier. Further research is required to find out why this

happens. However, the MacKinlay (1997) CAR-test conducted on interval [-3, +2] shows no significant

effect on the turnover on the stock returns. The test is summarized in Table 10.

What stands out in the Figure 3 is the almost horizontal line between day -1 and 0, while before and

Figure 3. Plot of the overall average Abnormal Returns of CEO turnovers

Table 10. Significance test on interval [-3, +2] of overall Abnormal Returns for CEOs

CEO [-3, +2] OVERALL

AVER. CAR -0.00538

VAR (AVER. CAR) 0.00590

θ - TEST VARIABLE -0.07

Significance levels: ***=0.01 **=0.05 *=0.10

18

after that period the returns are relatively bouncing. This can be explained by an inside trade

prohibition at the day before the public announcement. That would also explain why the stock

returns took a dive and got back on their normal level before the information was made public. The

prohibition could have pressured shareholders who knew there was going to be a turnover

announcement to react quick, because day -2 would be the last day to trade the stocks before the

announcement was made public.

6. CONCLUSION

Using the [-5, +5] event window, the conclusion would be that turnovers in the high fashion industry

normally do not influence stock prices. Only one CD turnover had a significant effect and no CEO

turnover. This is in contradiction with the previous researches of Chapter 2 Literature Review. Most

of the reviewed literature showed a significant effect of turnovers on stock prices. It is logical to

assume that the event window was not right, when only one of the twelve turnovers turns out to be

significant.

In contrast, the [-1, +1] event window showed interesting results. The half of the CD

turnovers had significant effects on stock prices and also the half of the CEO turnovers had significant

effects. These results are way more logical than the results of the other event window, implying that

a narrow event window results in more significant outcomes.

The overall tests on the CD and CEO turnovers show no significant effect on the stock price.

However, as can be seen in Figure 2 and Figure 3, the stocks experience several shocks surrounding

the announcement day. Therefore, it may be logical to assume that both CD and CEO turnovers have

effects on stock prices. However, the effect are economically unimpressive, like some of the earlier

mentioned researches concluded. A limitation of this conducted method is the fact that the sample

was small. That is probably the reason the results were insignificant. Only six CD turnovers and six

CEO turnovers are tested. Larger samples could result in significant outcomes.

Further research is required to conclude which of the two event windows is best at

determining the effect of turnovers on stock prices. But assuming the [-1, +1] event window is good

enough and the (insignificant) shocks shown in the plots are legit, the conclusion of this research is

that shareholders react to CD turnovers as well as CEO turnovers. The reaction to CEO turnovers is no

surprise regarding previous research. But the reaction to CD turnovers is interesting. This implies

that shareholders in the high fashion industry do their homework and know that Creative Directors

like Frida Giannini (Gucci) and Raf Simons (Dior) are able to increase the value of a fashion house and

therefore react on these kind of turnovers. Shareholders apparently realise how important CDs are

for a high fashion house.

19

REFERENCES

Beatty, R., & Zajac, E. (1987). CEO Change and Firm Performance in Large Corporations: Succession Effects and Manager Effects. Strategic Management Journal, 8(4), 305-317. Boehmer, E., Musumeci, J., & Poulsen, A. B. (1991). Event-study Methodology under Conditions of Event-induced Variance. Journal of Financial Economics, 30(2), 253-272. Boeker, W. (1992). Power and Managerial Dismissal: Scapegoating at the Top. Administrative Science Quarterly, 37(3), 400-421. Boeker, W. (1997). Strategic Change: The Influence of Managerial Characteristics and Organizational Growth. The Academy of Management Journal, 40(1), 152-170. Bonnier, K., & Bruner, R. F. (1989). An Analysis of Stock Price Reaction to Management Change in Distressed Firms. Journal of Accounting and Economics, 11(1), 95-106.

Brief, A. P., & Nord, W. R. (1990). Meanings of Occupational Work: A Collection of Essays. Lexington, MA: Lexington Books, pp. 203-232.

Brown, S. J., & Warner, J. B. (1980). Measuring Security Price Performance. Journal of Financial Economics, 8(3), 205-258.

Brun, A., Caniato, F., Caridi, M., Castelli, C., Miragliotta, G., Ronchi, S., Sianesi , A., & Spina, G. (2008). Logistics and Supply Chain Management in Luxury Fashion Retail: Empirical investigation of Italian Firms. International Journal of Production Economics, 114(2), 554-570. Christopher, M., Lowson, R., & Peck, H. (2004). Creating Agile Supply Chains in the Fashion Industry. International Journal of Retail & Distribution Management, 32(8), 367-376. Cillo, P., De Luca, L. M., & Troilo, G. (2010). Market Information Approaches, Product Innovativeness, and Firm Performance: An Empirical Study in the Fashion Industry. Research Policy, 39(9), 1242-1252. Clayton, M. C., Hartzell, J. C., & Rosenberg, J. (2005). The Impact of CEO Turnover on Equity Volatility. The Journal of Business, 78(5), 1779-1808. Coughlan, A. T., & Schmidt, R. M. (1985). Executive Compensation, Management Turnover, and Firm Performance. Journal of Accounting and Economics, 7(1-3), 43-66.

Denis, D., & Denis, D. (1995). Performance Changes Following Top Management Dismissals. The Journal of Finance, 50(4), 1029-1057. Egholm, A. C., & Nordström, J. (2011). Stock Price Reactions to CEO Turnover.

Fama, E.F. (1991). Efficient Capital Markets: II. The Journal of Finance, 46(5), 1575–1617.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383–417.

Fama, E. F., Fisher, L., Jensen, M. C., & Roll, R. (1969). The Adjustment of Stock Prices to New Information. International Economic Review, 10(1), 1-21.

20

Furtado, E. P., & Rozeff, M. S. (1987). The Wealth Effects of Company Initiated Management Changes. Journal of Financial Economics, 18(1), 147-160. Friedman, S. D., & Singh, H. (1989). CEO Succession and Stockholder Reaction: The Influence of Organizational Context and Event Content. The Academy of Management Journal, 32(4), 718–744.

Healy, M. C., Lehman, M., & Mcdaniel, M. A. (1995). Age And Voluntary Turnover: A Quantitative Review. Personnel Psychology, 48(2), 335-345. Huson, M. R., Malatesta, P. H., & Parrino, R. (2004). Managerial Succession and Firm Performance. Journal of Financial Economics, 74(2), 237-275. Jenter, D., & Kanaan, F. (2015). CEO Turnover and Relative Performance Evaluation. The Journal of Finance, 70(5), 2155-2184. Kaplan, S. (1994). Top Executive Rewards and Firm Performance: A Comparison of Japan and the United States. Journal of Political Economy, 102(3), 510-546. Macchion, L., Moretto, A., Caniato, F., Caridi, M., Danese, P., & Vinelli, A. (2015). Production and Supply Network Strategies within the Fashion Industry. International Journal of Production Economics, 163(1), 173-188. MacKinlay, A. C. (1997). Event Studies in Economics and Finance. Journal of Economic Literature, 35(1), 13–39. Mcwilliams, A., & Siegel, D. (1997). Event Studies in Management Research: Theoretical and Empirical Issues. Academy of Management Journal, 40(3), 626-657. Murphy, K. J., & Zimmerman, J. L. (1993). Financial Performance Surrounding CEO Turnover. Journal of Accounting and Economics, 16(1-3), 273-315. Rhodes, S. R. (1983). Age-related Differences in Work Attitudes and Behavior: A Review and Conceptual Analysis. Psychological Bulletin, 93(2), 328-367. Setiawan, D. (2011). An Analysis of Market Reaction to CEO Turnover Announcement: The Case In Indonesia. International Business & Economics Research Journal, 7(2), 119-128. Socha, M. (2009). Despite Deep Recession, Fashion Firms Still See A Big Role For Couture. WWD: Women's Wear Daily, 198(3), 1-2. Stock, J. H., & Watson, M. W. (2015). Introduction to econometrics. Boston: Pearson/Addison Wesley. Turker, D., & Altuntas, C. (2014). Sustainable Supply Chain Management in the Fast Fashion Industry: An Analysis of Corporate Reports. European Management Journal, 32(5), 837-849.

Warner, J. B., Watts, R. L., & Wruck, K. H. (1988). Stock prices and top management changes. Journal of Financial Economics, 20(1-2), 461-492. Weisberg, J., Kirschenbaum, A. (1993). Gender and Turnover: A Re-examination of the Impact of Sex on Intent and Actual Job Changes. Human Relations, 46(8), 987-1006.