Tupras London 08

47

Investor Meeting February 200 8

Transcript of Tupras London 08

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 1/47

Investor Meeting

February 2008

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 2/47

Tüpraş Key Messages

• High marginenvironment

GlobalRefining

Environment

• Significant upsidefrom on-going &new refineryupgrades

TüpraşUpgrades

• Expansion to newactivities• trading• retailing

NewOpportunities

• Restructuring andefficiencyimprovementpotential

Restructuring

• No SignificantLiabilities

Environmental

• Strong financialperformance and

high dividend yield

Financial

2

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 3/47

3

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 4/47

Macro Outlook

Slowdown

•David McCormick - US Treasury

•John Snow – Ex US Treasury•Joseph Stiglitz – Ex World Bank

•Martin Wolf - FT Editor

Recession

•Kenneth Rogoff – Lehman Bros•George Soros - Investor•Sergio Ermotti – Unicredit CEO•Nouriel Roubini - Economist

-2,0

0,0

2,0

4,0

6,0

2007 -1Q 2007 -2Q 2007 -3Q 2007 -4Q 2008 -1Q 2008 -2Q

(%) Quarterly Growth GlobalEUG7USAJap

0

123456789

1011

12

2002 2003 2004 2005 2006 2007 2008

(%) GDP Growth

USA China

India Global

Slowdown or Recession

Forex Trend

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 5/47

Crude Oil

RisingDemandfrom EM

LowDollarValue

Terrorism

(Nigeria,Iraq,

Angola)

War Risk /Embargo

(Iran)

OPECQuotas

ResourceNationalism

High

Prices

5

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 6/47

Margin Environment

Margin Drivers

Growing Global Demand

• Sustainable demand, driven by globaleconomic growth

Regional product shortages supportsstrong margins

• Gasoline in USA & Diesel in Europe

• Margins supported by FOB / CIFdifference

Refineries became more complex & moreinterdependent

• Shutdown in one unit impact wholerefinery

Specifications reduce flexibility

Refinery Capacity Investments

Refinery projects taking longer andcosting more

• Increases in supply capacity are laggingdemand

Credit crunch will hit projects hard

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

10,0

Changing Environment

2003-2005 1999-2002

2006 2007

6

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 7/47

Rising Refinery Costs

7

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 8/47

Global Product Consumption & Refining Capacity

40

50

60

70

80

90

100

110

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

Product ConsumptionProduct Consumption With Low GrowthActual Refining CapacityEstimated Refining Capacity

Source: OGJ, Reuters, Tüpraş

M

i l l i o n b b l / d a y

8

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 9/47

Turkish Oil Products Demand ProjectionBase Case (Million Ton)

0

5

10

15

20

25

30

35

40

45

93 95 99 '00 '06 '07 '10 '15 2020

LPG Naphtha GasolineJet Gas Oil / Diesel Fuel Oil

Asphalt Others ProductionIncld. Ataş

3.53.5

2.52.62.2 2.4

12.2 13.2

4.0 3.4

2.2 2.3

1.9 2.1

5%

-17%

8%

35.4

39.3

7%

31.1 +2,3 %30.5

2006 ∆2007T

9

0.2%

-3%

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 10/47

Turkey’s Imports

Million ton 2005 2006 2007E

Gasoline 0,7 0,8 0,6

Jet Fuel - 0,2 0,2

Gas Oil 4,4 6,0 6,7

Fuel Oil 0,9 0,4 0,6

Total Import 6,0 7,4 8,1

Import Share, %

Turkey 25.3 31.8 34.4

Excluding Tüpraş 24.1 26.1 25.6

Distributors Share 95% 82% 74%

10

Note: Excluding LPG

13%

22%

59%

6%

Gasoline 2006

Israel

Greece

Romania

Other

7%

72%

6%4% 2% 9%

Gasoil / Diesel 2006

FSU Countries

Russia

Greece

Romania

Italy

Other

>90% from the Black Sea

Source: TÜPRAŞ, GDPA & EMRA

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 11/47

Legislation - Petroleum Market Law

• Market Supervised by Energy Markets Regulatory Authority

(EMRA)Regulator

• Pricing set by the market for both refinery gate and pump price• No limit on imports• Refining companies may own distributors

Freedoms

• All market participants needs a licence from EMRA• Refiners should give priority to indigenous crude oil• National inventory requirement of 90 days worth of domestic

sales, with 20 days product stock held by both refiners anddistributors – Draft Law

• Maintain continuous production and supply of refined oil productsas required by the Turkish Armed Forces

Obligations

• The market share of each distributor in the domestic market shallbe limited to 45%Limits

11

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 12/47

Storage Capacity and Compulsory Stock Requirement

Enerji0,4%

Shell5,8%

Bölünmez0,5%

Delta4,1%

Aktaş0,7%

Aytemiz3,0%

Siyam1,6%

Tuta

2,4%

POAŞ11,2%

Altınbaş2,5%

Others2,9%

Balpet0,8%

Total4,3%

Turkuaz0,6%

BP6,3%

Petline0,4%

Opet11,3%

TÜPRAŞ41,1%

Product Storage Capacity in Turkey Storage Capacity of Tüpraş (000’ton)

Crude Oil Product Total

1,700 2,600 4,300

Current Compulsory Stock of TÜPRAŞ(20days)

920 kton

Tüpraş owns 4 times more storagecapacity than its 20 day compulsorystock requirement.

Tüpraş owns 65% of combined crude oil

& product stock capacityTüpraş+ Opet own more than half of

total product storage capacity (52.4%) inTurkey.

12

Source: EMRA

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 13/47

Developments in Turkish Petroleum Sector

2005

• EU• EURO IV

2007

• Turkey• National

MarkerProcess

2008

• Turkey• EURO IV• 1000 ppm• National

CompulsoryStock

2009

• EU• EURO V

• Turkey• EURO V

Expected

Change in Fuel Regulations & Standards: EU and Turkey

1000 ppm: From Jan 1st 2008, all gasoil sold in Turkey will have at maximum 1000 ppm sulphur content

EURO IV: 50 ppm S for gasoline & diesel, aromatics (35%) for gasoline

EURO V: 10 ppm S

10 ppm Diesel already in the market ahead of regulations

National Marker Process introduced in order to prevent illegal trade.

National Compulsory Stock may become an issue in 2008.

13

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 14/4714

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 15/47

TÜPRAŞ Assets

Baku

Ceyhan

Black Sea

Marmara

Mersin

Ankara

İstanbul

Körfez Kırıkkale5.0 mtNC: 5.32 (6.32)

Batman1,1 mtNC:1.83

Kirkuk

P e t r o -

c h e m i c a l s Körfez

100% Share

Capacity: 50 kt

Product: Carbon Black S h i p p i n g

Ditaş

79.98% Share

165 kDWT Crude Tanker

15 kDWT Product Tanker R e t a i l i n g Opet

40% Share

1,280 Retail Sites

850 kM3 Storage

Trading, Lubricants &Bunkering activities

İzmit11.0 mtNC: 7.78

İzmir 11.0 mt

NC: 7.66

Total Capacity: 28.1 Million TonsCurrent Nelson Complexity(NC): 7.08 (7.25)

15

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 16/47

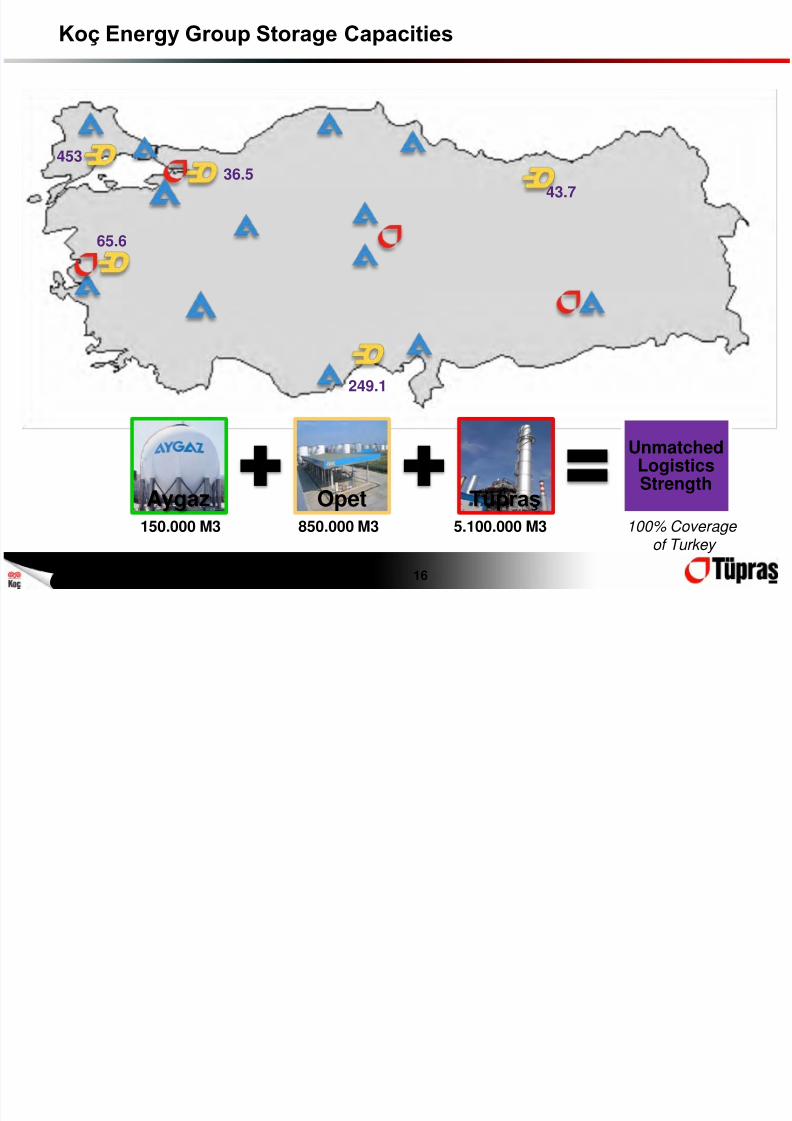

36.5

65.6

249.1

453

43.7

Koç Energy Group Storage Capacities

Aygaz Opet Tüpraş

UnmatchedLogisticsStrength

850.000 M3150.000 M3 5.100.000 M3 100% Coverage of Turkey

16

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 17/47

0,10,4

2004 2005 2006 2007

0,4

2004 2005 2006 2007 1,2 0,9 0,5 0,9

2004 2005 2006 2007

0,10,5

2004 2005 2006 2007

2,3 2,2 2,2 2,1

2004 2005 2006 2007

Russia

Kazakhstan

Iran

S. Arabia

IraqSyria

Italy

Libya

Algeria

Domestic Crude

Azerbaijan

4,8 4,6 4,50,1

2004 2005 2006 2007

5,87,1

6,7

9,1

2004 2005 2006 2007

5,87

8,9 8,9

2004 2005 2006 2007

3,5 3,5 3,5 3,3

2004 2005 2006 2007

0,1 0,1

2004 2005 2006 2007

0,4 0,3 0,2

2004 2005 2006 2007

17

Crude Suppliers of TÜPRAŞ (million ton)

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 18/47

Gross Refining Margin

Improving Margin Premium Investments in yield improvements

Operational optimisation

Bigger domestic market share Better export premiums

18

Drivers of Refining Margin: Advantageous crude supply

Strong purchasing power Flexible crude slate Refineries designed for sour crude Favorable transport costs A strong position in import infrastructure Pipeline links and reduced storage needs

for key customers High exporting ability

Gross Margin

($ / bbl)

Average

1st Q 6M 9M Year

2006

Med Complex 4,8 5,9 5,7 5,3

TÜPRAŞ 3,7 5,4 6,3 5,9Difference -1,1 -0,5 0,6 0,6

2007

Med Complex 5,7 6,5 5,6 5,3

TÜPRAŞ 5,0 7,2 7,1 7,2

Difference -0,7 0,8 1,6 1,9

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 19/47

Crude Processing and Production 12M 2007/2006

0,8 0,81,4 0,9

3,6 4,0

2,2 2,6

7,6 7,1

5,8 5,4

2,22,3

1,01,0

24,6 24,0

0,0

5,0

10,0

15,0

20,0

25,0

30,0

12M 2006 12M 2007

Production Mix (mn ton)

Others

Asphalt

Fuel Oil

Gasoil

Jet / Kero

Gasolines

Naphtha

LPG

60

70

80

90

100

110

J F M A M J J A S O N D

Tüpraş Capacity Utilisation (%)

2004 2005

2006 2007

%93,2

%88,8

%92,4

Annual

-2.5%

19

%91,1

• Crude Volume Optimisation• Maximising capacity ofconversion units

• 25.6 mn tons of crude oilwere processed anddecreased 2.5%

Production

• Processed heavierCrude Oil API 32.1 vs32.5 for 2006

• White ProductionYield 67.5% from67.1% in 2006

Crude

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 20/47

Changing Product Yields

Through investment and

optimisation, yields are becomingmore profitable

Increased Gasoline

More high priced Jet

Asphalt Maximisation 1.410 869

3.612 3.965

0

1.000

2.000

3.000

4.000

5.000

6.000

2006 2007

V o l u m e M T

Gasoline / Naphtha

Gasolines Naphtha

2.156 2.588

7.615 7.118

9.771 9.706

0

2.000

4.0006.000

8.000

10.000

12.000

2006 2007

V o l u m

e M T

Middle Distillate

Jet /Kerosene Gasoil

5.799 5.432

2.220 2.286

0

2.000

4.000

6.000

8.000

10.000

2006 2007

V o l u m

e M T

Fuel Oil / Asphalt

Fuel Oil Asphalt

20

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 21/47

Tüpraş Total Product Sales – 12 Months

kton 2006 2007 Difference

Total Sales 26,137 26,328 191

LPG 1,190 968 -222

Naphtha 1,410 869 -541

Gasolines 3,659 4,047 388

Jet Fuel/Kerosene 2,123 2,556 433Gasoil 50 PPM 2,070 2,215 145

Gasoil 7000 PPM 6,793 6,709 -84

Middle Distillates 10,986 11,480 494

Fuel Oil 5,780 5,691 -89

Asphalt 2,186 2,291 105

Lube Oil 325 308 -17

Other 601 674 73

Record

21

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 22/47

Tüpraş Domestic Product Sales

Kton 2006 2007 Difference

Domestic Sales Total 19,899 19,937 38

LPG 1.173 949 -223

Naphtha 1.010 771 -239

Gasolines 1.814 1.897 83

Jet Fuel / Kerosene 2.033 2.201 168

Gasoil 50 ppm 6.653 6.637 -16Gasoil 909 1.725 817

Middle Distillates 9.595 10.563 969

Fuel Oil 3.627 2.954 -673

Asphalt 2.179 2.292 112

Lube Oil 502 511 10Other 1.173 949 -223

White Product 14,021 14,605 584

Black Product 5,878 5,332 -546

White Product (%) 70% 73% 3%

Record 22

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 23/47

Progress in the near term strategy: Increasing Trading Activities

30% Increase in sales from

imported products

Focus trading on high marginproducts

Gasoil import contributed to marketshare increase

Low Sulphur Fuel oil was importedto produce heating oil without theneed to process more sweet

crudes.

6.192

6.509

1.370

1.853

- 2.000 4.000 6.000 8.000 10.000

2006

2007

Domestic Gasoil Sales, kton

Production Trading

Product 2006 2007 Diff. %

LPG 334 101 -70%

Diesel 1.370 1.853 35%

Fuel Oil - 264

Total 1.704 2.218 30%

23

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 24/47

Tüpraş vs The Market – 2007 /2006

-2,9

4,6 5,3

-4

-2

0

2

4

6

MarketGrowth TupraşGrowth ShareIncrease

Gasoline

7,910,6

1,60

36

9

12

MarketGrowth

TupraşGrowth

ShareIncrease

Gas Oil

6,19,2

2,00

36

9

12

MarketGrowth

TupraşGrowth

ShareIncrease

Automotive Fuels

Tüpraş increased its market sharein automotive products, growingsale faster than the market

Better sales strategy, NationalMarker & targeted discounting allhad an impact

Source: Tüpraş, PetDer Excluding Auto LPG

24

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 25/47

Total Sales By Customers – 12 M 2007

Sales By Customer Group (%)

PetrolRetailers

54,8%

LPGDist.3,5%

Petkim3,4%

Export24,3%

Others2,8%

Asphalt8,7%

Military2,4%

Sales To Petrol Retailers (%)

POAŞ35,7%

Shell19,8%

BP12,3%

OPET12,0%

Others(45)

20,2%

First 4 Distributor’s Share in Total Sales toDistributors = 79.80 %Total Sales: 26,328 kton

25

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 26/47

TÜPRAŞ Exports 12M 2007/2006

40098

1.845 2.151

1.301562

405

470

2.1522.737

135 373

6.238 6.390

0500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

5.500

6.000

6.5007.000

12M 2006 12M 2007

Export by Product (kton)

Naphtha Gasoline Gas oilHVGO Fuel Oil Other

2,0

2,8 3,0 3,4

4,6

6,2 6,4

0,3 0,6 0,7 1,01,9

3,03,4

0

2

4

6

8

01 02 03 04 05 06 07

Export By Years

Mn Ton Bn $

Italy14%

Croatia7%

Malta6%

OtherEurope

10%

Greece9%

Singapore15%

South

Africa9%

UAE4%

S. Arabia6%

Other12%

USA

8%

Export by Market

26

USA & Europe > 54%

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 27/47

27

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 28/47

Strategy: Key Parameters

Master PlanInvestment

Restructuring

OperationalExcellence

Profitability Focused

Investment

“ResidiumUpgrading”

Master Plan Investment

Euro V Specifications

Product Yield Improvements

Restructuring

HR Improvements

New Management Techniques

Trading Focus

Operational Excellence Expense Reduction & Profitability

Productivity Improvements

Profitability Focused Investment

Asphalt Maximizasion

Crude / Product Blending

Increased Tank Capacity

Railway Transportation System

Residium Upgrading Project

Fuel Oil Diesel

28

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 29/47

Progress in the near term strategy: Investments

On-Going Investment

May 31st: Izmit CCR onstream July 8th : Izmit HDS onstream

Kırıkkale HDS &CCR 2nd Q 2008

Other Investments Wagon loading facilities in Izmit are

completed

Tank investments to add 1 million M3

capacity (+20%)

8 MW Wind Turbine investment to bemade in Izmir by 2011

220 250

53

123

0

50

100

150

200

250

300

350

400

2006 2007

Million $

New and Other Inv. Master Plan

273

29

373

Including Related Interest Costs

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 30/47

Upside Potential

Products

2005 Actual Production

(2)

After Investment (Max.)

(1)

Difference

(1)-(2)Net

Margin$/ton

Maximum

EBIT

Kton % Kton % Kton Million USD

LPG 764 3.2 1,120 4.5 356 63 22.2

Naptha 1,388 5.8 419 1.7 -969

Gasoline 3,548 14.9 5,837 23.7 2,289 40 91.6

Jet Fuel 2,013 8.4 2,683 10.9 670 50 33.5

Gas Oil 7,566 31.7 7,847 31.8 281 30 235.4

Black Products 8,127 34.0 6,303 25.6 -1,824

Others 484 2.0 457 1.9

Total 23,889 100.0 24,666 100.0 803.2 382.7

Crude Processed 25,494 26,500

Note: Based on Optimal Crude Slate

30

Ü

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 31/47

TÜPRAŞ’s Major Investment Study-Residium Upgrading

W h y R e s i d i u m U p g r a d e ? • Jet-Gasoil demand growth

• Contraction in Fuel Oilmarket

• Alternative to new refineryprojects

• Matching Production todemand• Local trends are

mirrored in globalmarkets

P r o f i t a b

i l i t y • Converts low-value blackproduct to high-value

white products• Increases Tüpraş’s margin

premium over itscompetitors

• Improves long term cashflow & income

• Note: Makes no assumption about refinery margins going forward.

31

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 32/47

32

P fi bili I di 2006 200 (T P )

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 33/47

Profitability Indicators - 2006 /2007 (Tax Purpose)

2006 2007Difference

Amount (%)

Dtd.Brent Price, ($/bbl) 65.1 72.5 7,4 11,4%

Brent vs Tupras Crude Cost, ($/bbl) -4.5 -3.8 0,7 -15,6%

Processed Crude API 32,5 32,1

White Product Yield, (%) 67,1 67,5 0,4%

Med. Complex Margin,($/bbl) 5,30 5,32 0,4%

Tupras Margin,($/bbl) 5,86 7,22 23,2%

Operating Profit, (mn. $) 501 652 151 30%EBITDA, (mn. $) 722 881 159 22%

33

I S 2006/2007 (T P )

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 34/47

Income Statement :2006/2007 (Tax Purpose)

4Q2006

4Q2007 % Diff. Million USD 2006 2007 % Diff.

3.429 4.793 40 Net Sales 14.115 15.838 12

106 243 129 Gross Profit 768 1.081 41

(56) (128) 128 Operating Expenses (267) (429) 61

50 115 130 Operating Profit 501 652 30

25 49 93 Income From Others, (Net) 129 243 88

15 (2) (112) Finance Expenses (11) (15) 37

91 163 79 Profit Before Tax 619 880 42

74 131 76 Net Profit 507 708 40

34

FX Ri k (2007 T P )

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 35/47

FX Risk (2007 Tax Purpose)

Consolidated

Assets

Consolidated

Liabilities

Financial Loans:322

Short TermLoans:74

Payables: 1.909

Stock:1.798

Recievables:267

Cash:

244

+4

35

Fi i l Hi hli ht

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 36/47

Financial Highlights

356279

429

768 769711

769

881

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7 / 9 M

2 0 0 7 T a x

EBITDA ( USD Million)

New

One Off

Natural Gas

5,2 5,2 6,18,6

11,114,1 12,1

15,8

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2

0 0 7 / 9 M

2 0 0 7 T a x

Revenue ( USD Billion)

154 116 291

491 508 575725 708

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7 / 9 M

2 0 0 7 T a x

Net Income ( USD Million)

36

2007 Tax = Results for Tax Purposes

Di id d

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 37/47

Dividends

Tüpraş is a cash generatingcompany, with a good ability togenerate dividends, in addition toinvesting.

In 2006 the dividend yield wasaround %8.5

Tüpraş plans to continue to pay out100% of distributable income

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

2002 2003 2004 2005 2006

Earnings & DividendsYTL/Share

Earnings Per Share Dividend

37

R ti & C t G

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 38/47

Ratings & Corporate Governance

Fitch Rating Comparison

As of January28, 2008

FOREIGNCURRENCY LOCAL CURRENCY

Long-term Long-term National

SOVEREIGN BB (Stab) BB (Stab) -

TÜPRAŞ BB (Stab) BBB-(Stab) AAA (tur) (Stab)

Vestel BB- (Neg) BB- (Neg) -

Hürriyet BB (Stab) BB (Stab) AA (tur) (Stab)

Turkcell BB (Stab) BBB-(Stab) -

Corporate Governance Rating

62,65

88,09

88,31

77,34

79,12

0% 50% 100%

Board

Stakeholders

Transparency

Shareholders

Overall

Rating by Saha Ratings

38

Highlights

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 39/47

Highlights

• Driven by Global Economic GrowthStrong Global Oil Demand

• Increasing costs and project timelinesLagging Refinery Investments

• Sustainable economic growth• Rapid car park growth• Currently low per capita oil consumption

Growing & High PotentialDomestic Market

• 4 well located refineries• Strategically valuable & profitable affiliates

Domestic Monopoly

• Improvements in production mix and efficiencyImproving Operations

• Strengthening competitive position & profitabilityInvestments

• Post privatisation management changes• HR Restructuring

Restructuring Upsides

• Profitable opportunities for further investmentFurther Upgrade Potential

• Strong cash generation ability & improving resultsProfitability

• Strong performance under volatile environmentsSafe Haven

39

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 40/47

Thank you…

The Investor Relations section of our company website has a wealth of constantly

updated information of interest to investors.

www.tupras.com.tr

40

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 41/47

41

TÜPRAŞ Sh h ld S

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 42/47

TÜPRAŞ Shareholder Structure

Koc Holding

75%

Shell

Turkey

0.1%

Aygaz

20%

Opet

3%

Enerji Yatırımları A.Ş.

Free Float

(ForeignInvestor’s

Share: ~85%)

Shell O. Invt.B.V

1.9%

Ditaş79.98%

40.0%

51%

49%

42

The Distribution Business Opet

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 43/47

The Distribution Business, Opet

• Purchasing 40% of Opet shares for US$380million from Aygaz (Dec 2006)

Tüpraş entered the retail market

• First Step in diversifying along the value chain• Positive impact on earning going forward

Reasons for investment

Retail Business

• Turkey’s 3rd largest

• 1.300 Retail sites, 2 Brands

Storage Capacity

• Second largest in Turkey, with 5 Terminals total850.000 M3

Other Business

• Petrol Trading, Bunkering & Lubricants

2006 Revenue $4 Billion

2006 EBITDA $145 Million

Sustainable growth in sales andincome

9,6 11,5 12,7 14,4 15,3

0

5

10

15

20

2003 2004 2005 2006 2007

Opet Auto Fuels Market Share

43

Market Share in Retailing 2007/2006

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 44/47

Market Share in Retailing 2007/2006

(1000 M3 )

5.651 5.385

3.677 4.086

2.523 2.841

2.611 2.7761.173

1.2251.945

2.31217.580

18.624

2006 2007

Motor Fuels sales increased by 5.9% y-o-y in 2007

32.1

6.7

14.9

14.3

11.1

20.9

28.9

6.6

14.9

15.3

12.4

21.9

Source: PETDER

POAŞ

Shell

OPET

BP

Total

others

Share,% Share,%5.9%

44

“O ti l E ll P " ith SHELL Gl b l S l ti

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 45/47

“Operational Excellence Program" with SHELL Global Solutions

Operational Excellence Programme (OEP)

Opportunity ConfirmationPhase Implementation Phase

2006 2007 2008 2009 2010 2011 Total

Net Benefit, Mn$ 10 44 75 115 138 378

The program areas for OEP are:

Hydrocarbon Margin

Maintenance and Reliability

Energy and Loss

Operating and Maintenance cost

Health and Safety Environment

Selective De-bottlenecking

45

ISE Relative Performance 2007

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 46/47

ISE Relative Performance 2007

80

90

100

110

120

130

140

150

160

0 4 J a n

1 8 J a n

0 1 F e b

1 5 F e b

0 1 M a r

1 5 M a r

2 9 M a r

1 2 A p r

2 6 A p r

1 0 M a y

2 4 M a y

0 7 J u n

2 1 J u n

0 5 J u l

1 9 J u l

0 2 A u g

1 6 A u g

3 0 A u g

1 3 S e p

2 7 S e p

1 1 O c t

2 5 O c t

0 8 N o v

2 2 N o v

0 6 D e c

2 0 D e c

IMKB-100 Relative Tüpraş Relative

P4646

Disclaimer

8/8/2019 Tupras London 08

http://slidepdf.com/reader/full/tupras-london-08 47/47

Disclaimer

This presentation contains forward-looking statements that reflect the

Company management’s current views with respect to certain future events.Although it is believed that the expectations reflected in these statements are

reasonable, they may be affected by a variety of variables and changes in

underlying assumptions that could cause actual results to differ materially.

Neither Tüpraş nor any of its directors, managers or employees nor any other

person shall have any liability whatsoever for any loss arising from use of this

presentation.

![Untitled Document [cdn-pays.bnpparibas.com] · 2012-08-29 · 12 harewood avenue bnp paribas london branch bnp paribas london ! nw16aa united kingdom london 10 harewood avenue - -](https://static.fdocuments.net/doc/165x107/5e6c94489ff81c748422d085/untitled-document-cdn-pays-2012-08-29-12-harewood-avenue-bnp-paribas-london.jpg)