TSX : KXS RICHARD MONKMAN, CFO JOHN SICARD, CPO April 2015.

17

TSX : KXS RICHARD MONKMAN, CFO JOHN SICARD, CPO April 2015

-

Upload

patience-bishop -

Category

Documents

-

view

216 -

download

2

Transcript of TSX : KXS RICHARD MONKMAN, CFO JOHN SICARD, CPO April 2015.

TSX : KXS

RICHARD MONKMAN, CFO

JOHN SICARD, CPOApril 2015

2

Forward Looking StatementsForward-Looking Information

This document contains forward-looking statements within the meaning of applicable Canadian securities legislation. In some cases, these forward-looking statements can be identified by words or phrases such as “may”, “will”, “expect”, “anticipate”, “aim”, “estimate”, “intend”, “plan”, “seek”, “believe”, “potential”, “continue”, “is/are likely to” or the negative of these terms, or other similar expressions intended to identify forward-looking statements. We have based these forward-looking statements on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs.

These forward-looking statements include, among other things, statements relating to: our expectations regarding our revenue, expenses and operations; our plans for and timing of expansion of our solutions and services; our future growth plans; the acceptance by our customers and the marketplace of new technologies and solutions; our ability to attract new customers and develop and maintain existing customers; our expectations with respect to advancement in our technologies; our competitive position and our expectations regarding competition; and anticipated trends and challenges in our business and the markets in which we operate.

Forward-looking statements are based on certain assumptions and analysis made by us in light of our experience and perception of historical trends, current conditions and expected future developments and other factors we believe are appropriate, and are subject to risks and uncertainties. Although we believe that the assumptions underlying these statements are reasonable, they may prove to be incorrect. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Given these risks, uncertainties and assumptions, you should not place undue reliance on these forward-looking statements. These statements are provided to assist external stakeholders in understanding Kinaxis’ expectations as of the date of this document and may not be appropriate for other purposes.

Whether actual results, performance or achievements will conform to our expectations and predictions is subject to a number of known and unknown risks, uncertainties, assumptions and other factors, including those identified on page 3 of our Management’s Discussion and Analysis for the third quarter ended September 30, 2014, and in our other public disclosure documents, which are available under our profile on SEDAR (www.sedar.com). Although the forward-looking statements contained in this document are based upon what our management believes are reasonable assumptions, these risks, uncertainties, assumptions and other factors could cause our actual results, performance, achievements and experience to differ materially from our expectations, future results, performances or achievements expressed or implied by the forward-looking statements. The forward-looking statements made in this document relate only to events or information as of the date of this document is made and are expressly qualified in their entirety by this cautionary statement. Except as required by law, we do not assume any obligation to update or revise any forward-looking statements, whether as a result of new information, future event or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

Non-IFRS Measures

This document makes reference to certain non-IFRS measures, specifically Adjusted EBITDA. These non-IFRS measures are not recognized measures under IFRS and do not have a standardized meaning prescribed by IFRS, and are therefore unlikely to be comparable to similar measures presented by other companies. Rather, these measures are provided as additional information to complement the IFRS measures by providing further understanding of our results of operations from management’s perspective. Accordingly, they should not be considered in isolation or as a substitute for analysis of our financial information reported under IFRS. We use Adjusted EBITDA to provide investors with supplemental measures of our operating performance and thus highlight trends in our core business that may not otherwise be apparent when relying solely on IFRS financial measures. We also believe that securities analysts, investors and other interested parties frequently use non-IFRS measures in the evaluation of issuers. Our management also uses non-IFRS measures in order to facilitate operating performance comparisons from period to period, prepare annual operating budgets and assess our ability to meet our capital expenditure and working capital requirements.

Adjusted EBITDA is not a recognized, defined or standardized measure under IFRS. Our definition of Adjusted EBITDA will likely differ from that used by other companies (including our peers) and therefore comparability may be limited. Non-IFRS measures should not be considered a substitute for or in isolation from measures prepared in accordance with IFRS. Investors are encouraged to review our financial statements and disclosures in their entirety and are cautioned not to put undue reliance on non-IFRS measures and view them in conjunction with the most comparable IFRS financial measures.

For a reconciliation of Adjusted EBITDA to the most comparable IFRS financial measure please see page 7 of our Management’s Discussion and Analysis for the fourth quarter ended December 31, 2014:

• Under our profile on SEDAR (www.sedar.com)

All amounts are in United States dollars, unless otherwise indicated.

3

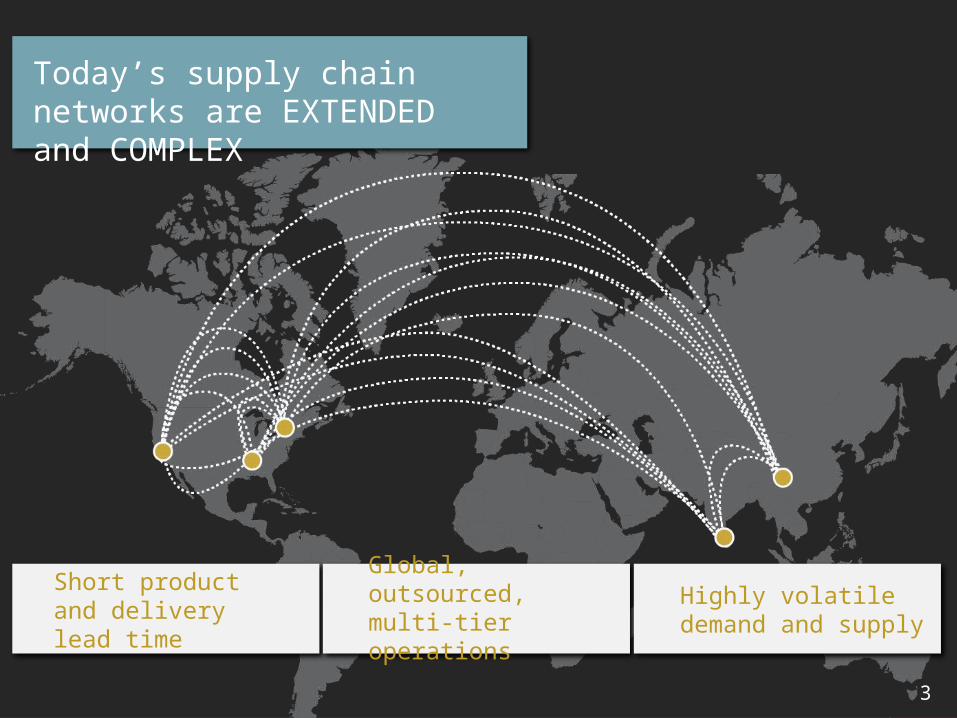

Today’s supply chain networks are EXTENDED and COMPLEX

Global, outsourced, multi-tier operations

Highly volatile demand and supply

Short product and delivery lead time

3

4

RapidResponseA single product that provides customers end-to-end visibility and planning, change simulation and response co-ordination across their supply chain networks

In today’s world, the ability to respond to change is more important than the plan

4

5

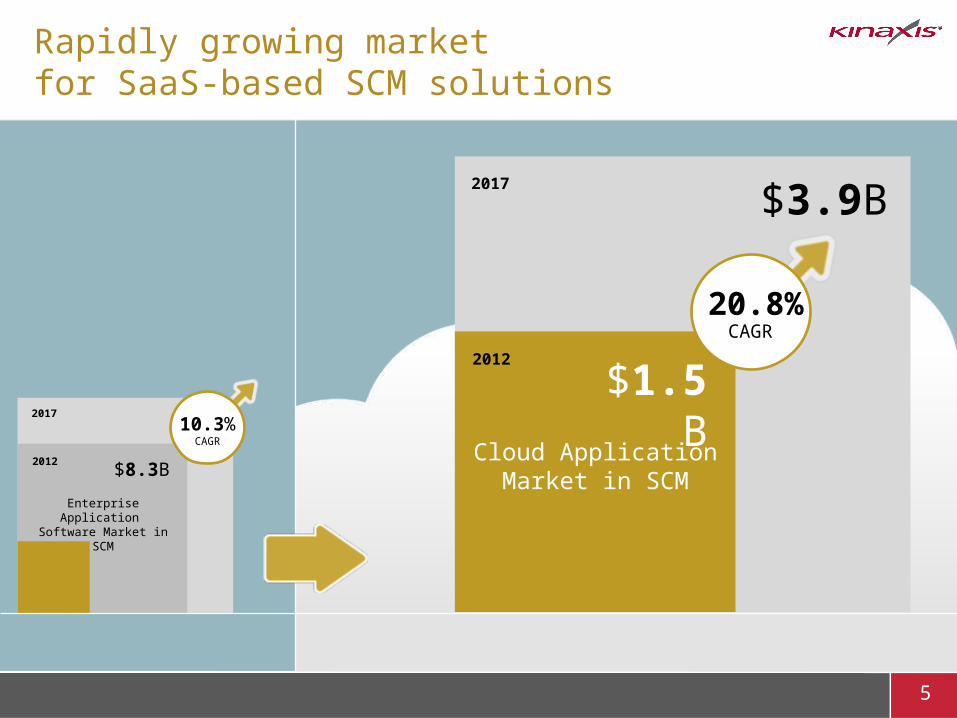

Rapidly growing market for SaaS-based SCM solutions

2012

2017

$8.3B

Enterprise Application Software Market in SCM

2012

2017

$3.9B

Cloud ApplicationMarket in SCM

$1.5B

20.8%CAGR

10.3%CAGR

6

Investment Highlights

>20% Annual Growth in the SaaS segment of $8.3B SCM Software Market1.

2.

3.

4.

5.

Recognized Visionary Product

>80% FTM of Subscription Revenue Visibility

24% Annual Subscription Revenue CAGR(1)

& Strong Multi-Year Adjusted EBITDA(2)

Strong Management Team; CEO, CFO & CPO Team Together for Nearly a Decade

(1) 4-year CAGR (2011-2014)(2) Adjusted EBITDA is a non-IFRS measure, for reconciliation of Adjusted EBITDA to profit before income taxes, please see “Management’s Discussion & Analysis”

7

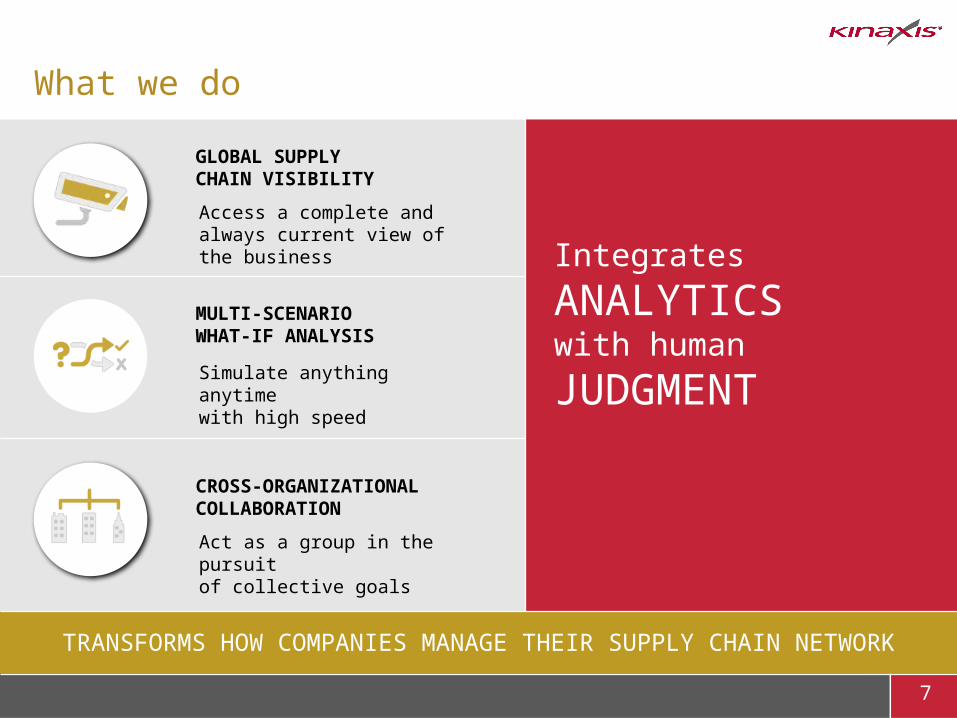

What we do

GLOBAL SUPPLYCHAIN VISIBILITY

Access a complete and always current view of the business

MULTI-SCENARIO WHAT-IF ANALYSIS

Simulate anything anytime with high speed

CROSS-ORGANIZATIONAL COLLABORATION

Act as a group in the pursuit of collective goals

Integrates

ANALYTICSwith human

JUDGMENT

TRANSFORMS HOW COMPANIES MANAGE THEIR SUPPLY CHAIN NETWORK

8

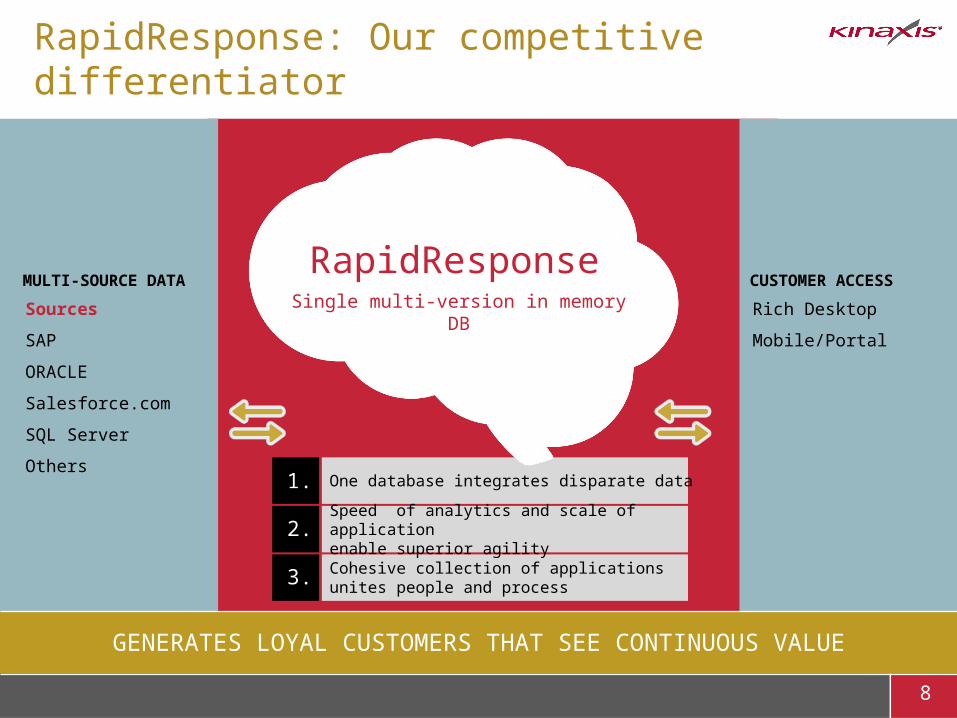

RapidResponse: Our competitive differentiator

GENERATES LOYAL CUSTOMERS THAT SEE CONTINUOUS VALUE

MULTI-SOURCE DATA CUSTOMER ACCESS

Rich Desktop

Mobile/Portal

Sources

SAP

ORACLE

Salesforce.com

SQL Server

Others1.

2.

3.

One database integrates disparate data

Speed of analytics and scale of application enable superior agility

Cohesive collection of applicationsunites people and process

RapidResponseSingle multi-version in memory DB

9

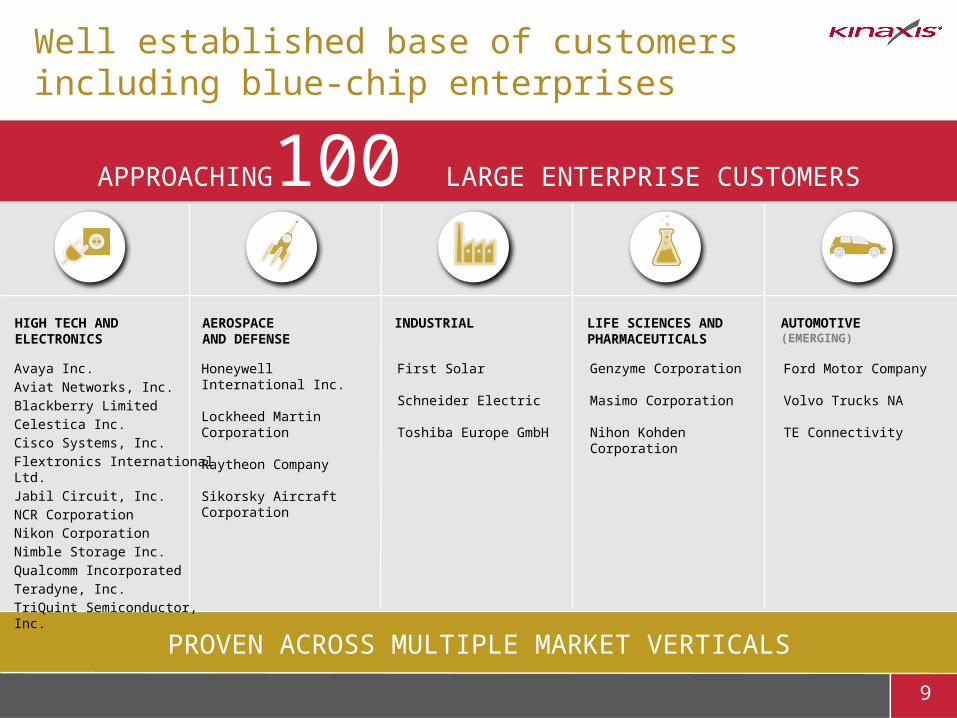

Well established base of customersincluding blue-chip enterprises

PROVEN ACROSS MULTIPLE MARKET VERTICALS

HIGH TECH AND ELECTRONICS

AEROSPACE AND DEFENSE

INDUSTRIAL LIFE SCIENCES AND PHARMACEUTICALS

Honeywell International Inc.

Lockheed Martin Corporation

Raytheon Company

Sikorsky Aircraft Corporation

First Solar

Schneider Electric

Toshiba Europe GmbH

Genzyme Corporation

Masimo Corporation

Nihon Kohden Corporation

APPROACHING100 LARGE ENTERPRISE CUSTOMERS

AUTOMOTIVE (EMERGING)

Ford Motor Company

Volvo Trucks NA

TE Connectivity

Avaya Inc.

Aviat Networks, Inc.

Blackberry Limited

Celestica Inc.

Cisco Systems, Inc.

Flextronics International Ltd.

Jabil Circuit, Inc.

NCR Corporation

Nikon Corporation

Nimble Storage Inc.

Qualcomm Incorporated

Teradyne, Inc.

TriQuint Semiconductor, Inc.

10

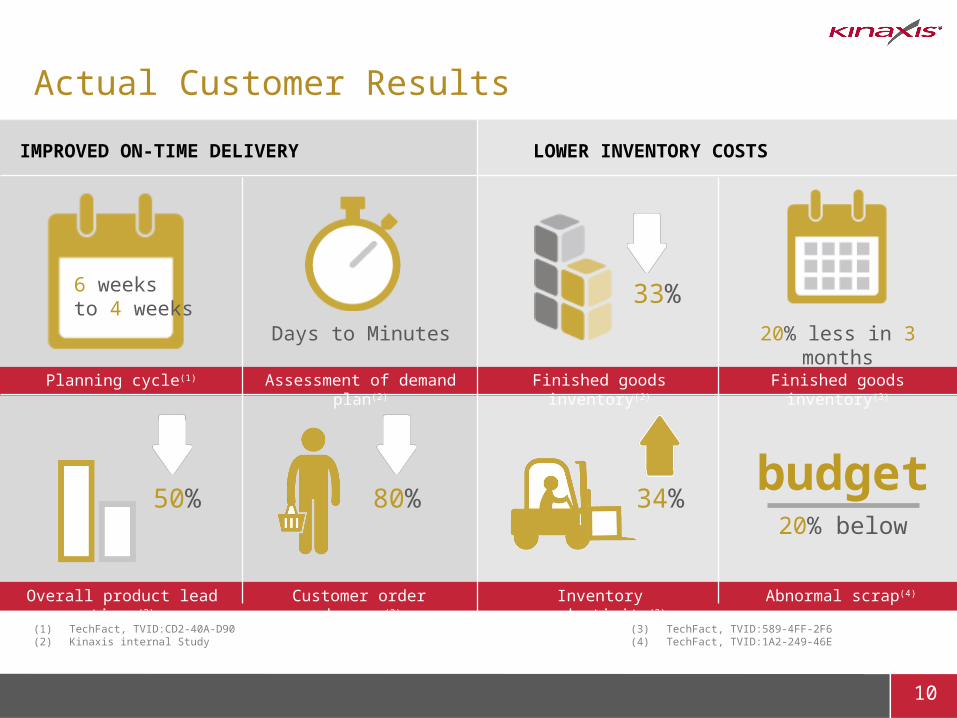

Actual Customer Results

IMPROVED ON-TIME DELIVERY LOWER INVENTORY COSTS

Overall product lead times(2)

Assessment of demand plan(2)

Customer order changes(2)

Finished goods inventory(2)

Abnormal scrap(4)

Finished goods inventory(3)

Inventory productivity(2)

6 weeks to 4 weeks

Days to Minutes

33%

20% less in 3 months

50% 80% 34%budget

20% below

(1) TechFact, TVID:CD2-40A-D90(2) Kinaxis internal Study

(3) TechFact, TVID:589-4FF-2F6(4) TechFact, TVID:1A2-249-46E

Planning cycle(1)

11

Plan Respond

12

Strong track record of revenue and adjusted EBITDA

HIGH LEVEL OF REVENUE VISIBILITY

2011 2012 2013 2011 2012 2013

Q4

2013

Q4

2014

Q42

013

Q4

2014

38.0

46.7

60.8

26.6

33.1

40.0

16.318.8

9.1

11.3

3.8

4.4

23%CAGR

24%CAGR

US Dollars (Millions)

REVENUE ADJUSTED EBITDA(1)SUBSCRIPTION REVENUE

2011

12.4

33%

2012

9.6

21%

2014

16.1

23%

(1) Adjusted EBITDA is a non-IFRS measure, for reconciliation of Adjusted EBITDA to profit before income taxes, please see “Management’s Discussion & Analysis”

12.6

9.9

13.3

10.1

27%QoQ

2014

70.1

2014

51.1

13.9

10.9

2013

15.0

25%

28%YoY

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

13

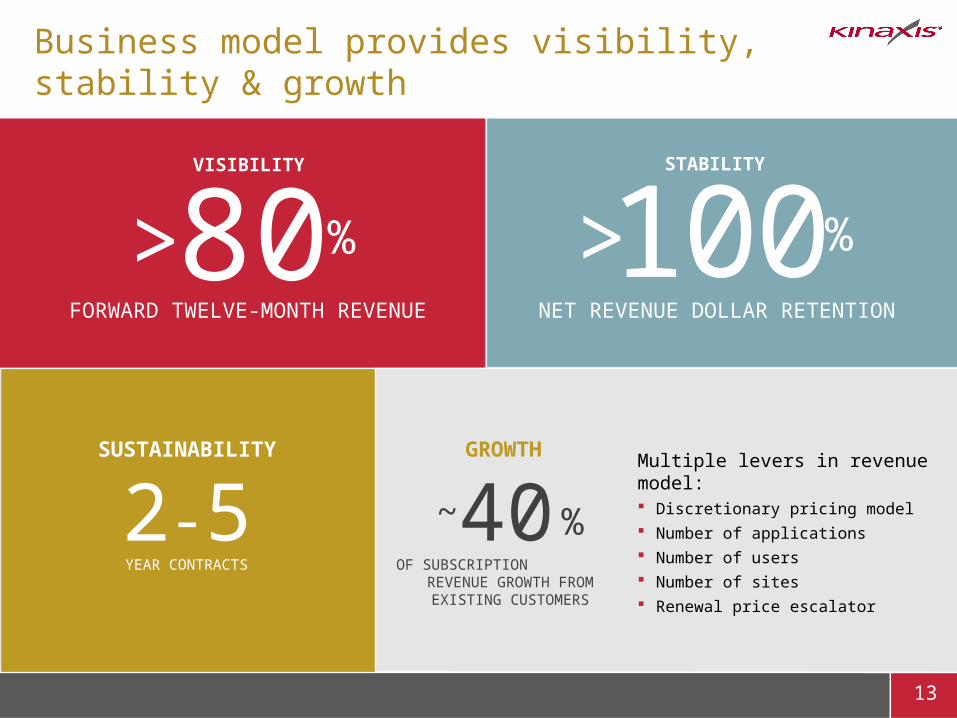

Business model provides visibility, stability & growth

NET REVENUE DOLLAR RETENTION

2-5

100> %

YEAR CONTRACTS

STABILITY

GROWTH

OF SUBSCRIPTION REVENUE GROWTH FROM

EXISTING CUSTOMERS

40 %

Multiple levers in revenue model: Discretionary pricing model Number of applications Number of users Number of sites Renewal price escalator

SUSTAINABILITY

FORWARD TWELVE-MONTH REVENUE

80> %

VISIBILITY

~

14

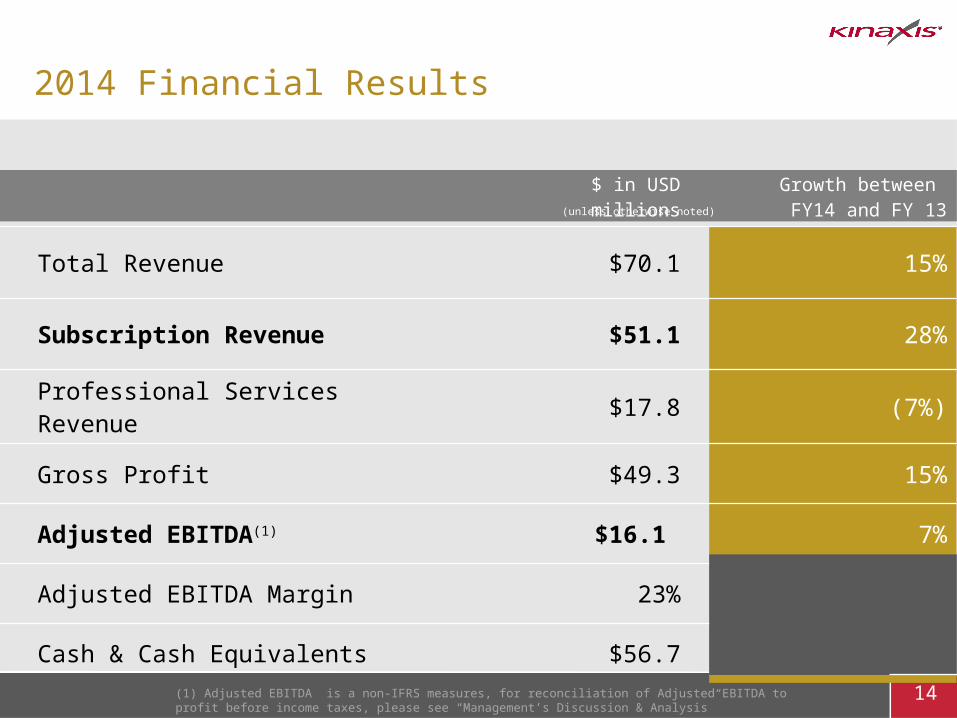

2014 Financial Results

$ in USD millionsGrowth between FY14 and FY 13

Total Revenue $70.1 15%

Subscription Revenue $51.1 28%

Professional Services Revenue $17.8 (7%)

Gross Profit $49.3 15%

Adjusted EBITDA(1) $16.1 7%

Adjusted EBITDA Margin 23%

Cash & Cash Equivalents $56.7

(unless otherwise noted)

(1) Adjusted EBITDA is a non-IFRS measures, for reconciliation of Adjusted EBITDA to profit before income taxes, please see “Management’s Discussion & Analysis”

15

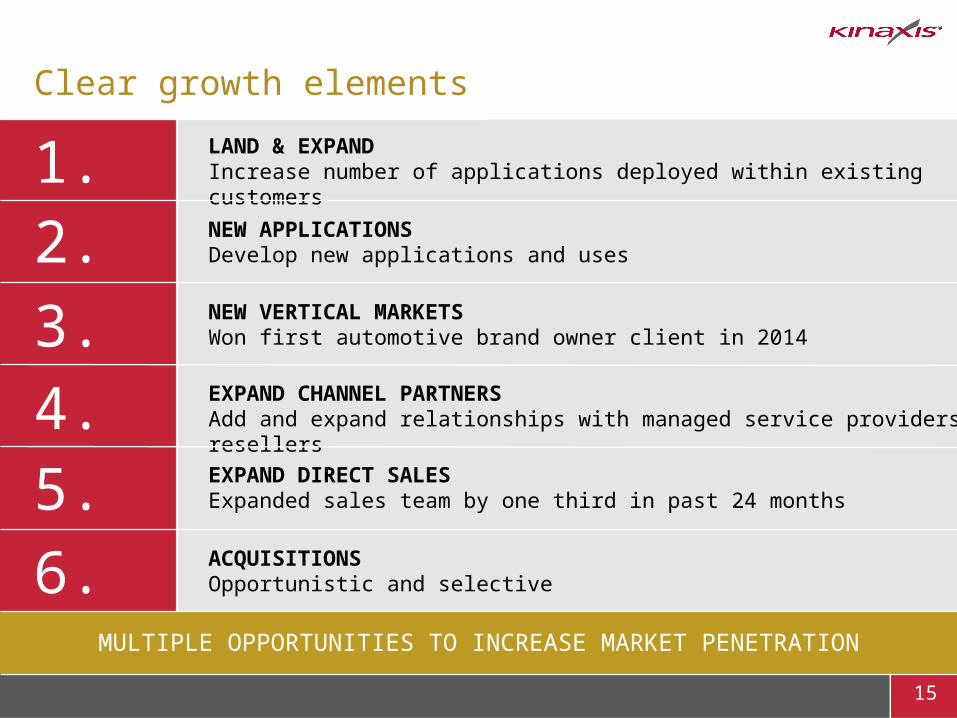

Clear growth elements

LAND & EXPANDIncrease number of applications deployed within existing customers

MULTIPLE OPPORTUNITIES TO INCREASE MARKET PENETRATION

1.2.

3.

4.5.

NEW APPLICATIONSDevelop new applications and uses

NEW VERTICAL MARKETSWon first automotive brand owner client in 2014

EXPAND CHANNEL PARTNERSAdd and expand relationships with managed service providers and resellers

EXPAND DIRECT SALESExpanded sales team by one third in past 24 months

6. ACQUISITIONSOpportunistic and selective

16

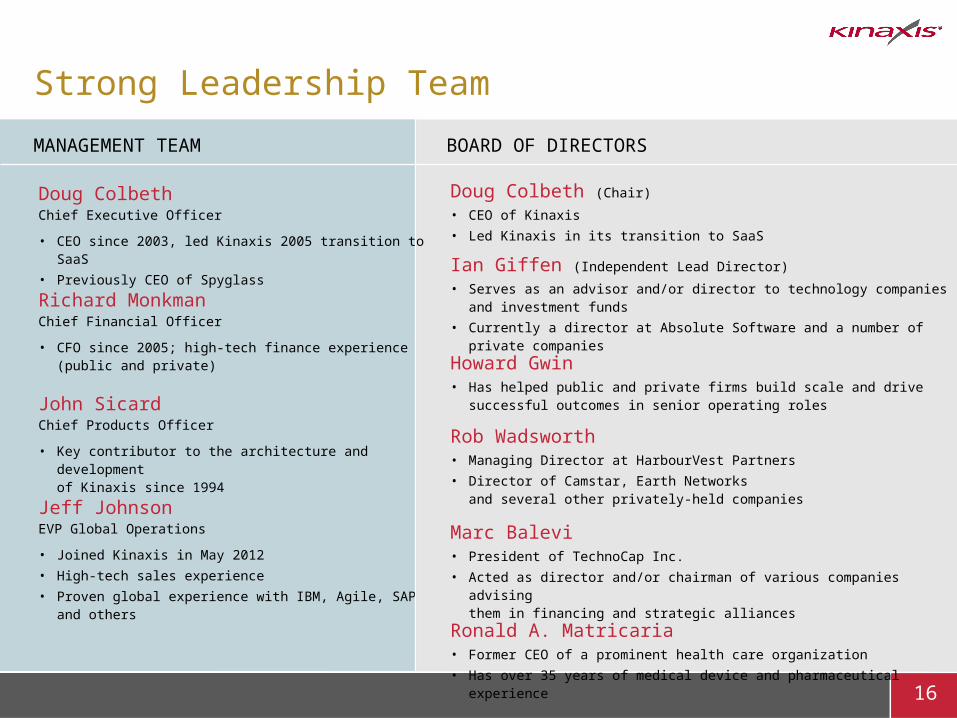

Strong Leadership Team

MANAGEMENT TEAM BOARD OF DIRECTORS

Doug Colbeth Chief Executive Officer

• CEO since 2003, led Kinaxis 2005 transition to SaaS• Previously CEO of Spyglass

Richard Monkman Chief Financial Officer

• CFO since 2005; high-tech finance experience (public and private)

John Sicard Chief Products Officer

• Key contributor to the architecture and development of Kinaxis since 1994

Jeff Johnson EVP Global Operations

• Joined Kinaxis in May 2012• High-tech sales experience• Proven global experience with IBM, Agile, SAP

and others

Doug Colbeth (Chair)• CEO of Kinaxis• Led Kinaxis in its transition to SaaS

Ian Giffen (Independent Lead Director)• Serves as an advisor and/or director to technology companies

and investment funds• Currently a director at Absolute Software and a number of private companies

Howard Gwin• Has helped public and private firms build scale and drive

successful outcomes in senior operating roles

Rob Wadsworth• Managing Director at HarbourVest Partners• Director of Camstar, Earth Networks

and several other privately-held companies

Marc Balevi• President of TechnoCap Inc.• Acted as director and/or chairman of various companies advising

them in financing and strategic alliances

Ronald A. Matricaria • Former CEO of a prominent health care organization• Has over 35 years of medical device and pharmaceutical experience

TSX : KXS

RICHARD MONKMAN, CFO

JOHN SICARD, CPOApril 2015