Trends in LNG Markets. Global Liquefaction Capacity Forecast.

21

Trends in LNG Markets

-

Upload

bruno-wilkins -

Category

Documents

-

view

233 -

download

3

Transcript of Trends in LNG Markets. Global Liquefaction Capacity Forecast.

Trends in LNG Markets

Global Liquefaction Capacity Forecast .

Global Liquefaction Capacity Forecast (Based on Operator's Announced Dates)

0

100

200

300

400

500

600

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Pacific

Middle East

Atlantic - Mediterranean

Higher Gas Prices in Asia

Historical and Forecasted Gas prices: Henry Hub (US) vs. Asia

0

5

10

15

20

25

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

Japan Korea Taiwan Henry Hub

• In the US, gas is a traded commodity with robust growth on the supply side, while is Asia LNG prices are defined by long – term contracts linked to the price of oil• The price differential between the US and Japan, currently - $2.00 /MMBtu, is forecasted to grow to ~ $6.00 - $8.00 /MMBtu by 2020

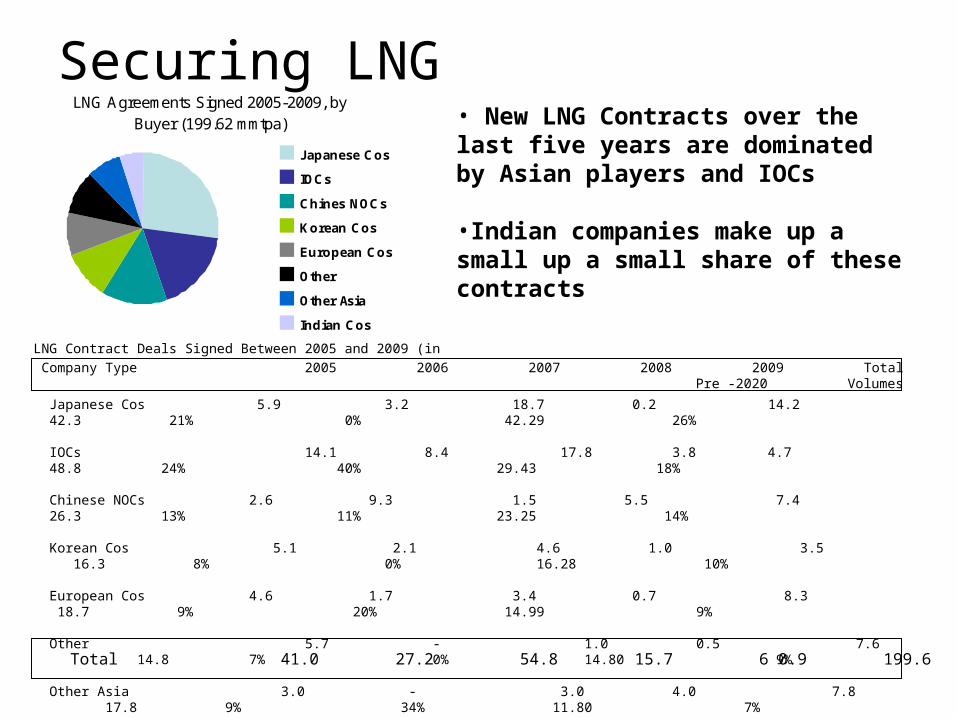

Securing LNGLNG Agreements Signed 2005-2009, by

Buyer (199.62 mmtpa)

Japanese Cos

IOCs

Chines NOCs

Korean Cos

European Cos

Other

Other Asia

Indian Cos

• New LNG Contracts over the last five years are dominated by Asian players and IOCs

•Indian companies make up a small up a small share of these contracts

LNG Contract Deals Signed Between 2005 and 2009 (in mmtpa)

Company Type 2005 2006 2007 2008 2009 Total Total% %Unlikely Pre-2020 Pre -2020 Volumes % Pre - 2020

Japanese Cos 5.9 3.2 18.7 0.2 14.2 42.3 21% 0% 42.29 26%

IOCs 14.1 8.4 17.8 3.8 4.7 48.8 24% 40% 29.43 18%

Chinese NOCs 2.6 9.3 1.5 5.5 7.4 26.3 13% 11% 23.25 14%

Korean Cos 5.1 2.1 4.6 1.0 3.5 16.3 8% 0% 16.28 10%

European Cos 4.6 1.7 3.4 0.7 8.3 18.7 9% 20% 14.99 9% Other 5.7 - 1.0 0.5 7.6 14.8 7% 0% 14.80 9%

Other Asia 3.0 - 3.0 4.0 7.8 17.8 9% 34% 11.80 7%

Indian Cos - 2.5 4.8 - 7.5 14.8 7% 41% 8.75 5%

Total 41.0 27.2 54.8 15.7 6 0.9 199.6 100% 19% 161.60 100%

Contracting LNG from Liquefaction Project

Global Liquefaction Capacity Forecast

0

100

200

300

400

500

600

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Announced Start

Pacific

Middle East

Atlantic - Mediterranean

Prosposed Liquefaction Projects for by Country (410mmtpa)

Australia

Iran

Nigeria

Russia

PNG

Venezuela

US

Egypt

Indonesia

Libya

Brazil

Canada

Angola

Eq. guinea

Erunei

UAE

Iraq

Cameroon

Timor

• Future supply growth is heavily weighted to the Pacific Basin

• Atlantic Basin Projects in particular are hampered by geopolitical risks and growing domestic demand

Australia Source for Majors

Proposed Liquefaction Projects for Majors by Location

0102030405060708090

100

BG CVX ENI RDS Total

Angola

Australia

Brazil

Brunei

Egypt

Indonesia

Iran

Iraq

Libya

Nigeria

PNG

Russia

UAE

Venezuela

Is Floating Liquefaction Potential Game Changer?• Floating liquefaction holds great potential for LNG producers:

- The new technology will allow for the development of smaller, more stranded gas reserves previously too distant from markets to monetize

- Once proven, new developments could be online faster than traditional liquefaction projects, as NIMBY and permitting concerns are avoided, and the actual liquefaction “plant” may already exist (and is mobile)

• Australia will likely be the proving ground for the world’s first floating liquefaction project. About a dozen such projects have been proposed; half of these are in Australia. The country provides an ideal place to test the new technology because:

- Producers face minimal to no political, environmental or regulatory risk in offshore Australia

- Sufficient feedstock exists and is not threatened by domestic demand needs

- Other proposed locations for floating plants include Brazil, Canada, Egypt, Indonesia, Iran, Iraq and Nigeria, most of which face greater risks for testing and proving this new technology

- Shell has two other proposed floating liquefaction projects in Australia waters, as well as a proposed project in Iraq and in Egypt

PRESENTATION ON“Global Overview of the LNG Business and

Key Trends”

LNG – A BRIEF STUDY

LNG Characteristics LNG Cycle Natural Gas: Production & Reserve Demand: Natural Gas LNG Scenario

THE LNG CYCLE

Upstream:• Gas Reservoir

Development• Gas Production Facilities

… Treatment and Liquefaction

• LNG Storage, Loading Terminal and Jetty

• LNG Tankers

Down stream:• LNG Unloading Terminal

and Jetty• Storage• Compression• Pipeline and Downstream

Consumer Development

LNG projects comprise several distinct distinct elements, each of which is necessary to implement a successful project:

LNG UPSTREAM – BLOCK DIAGRAM

Train - 1

SlugCatcher

GasSweetening

DehydrationMercuryRemoval

DehydrationMercuryRemoval

LNGStorage,Loading

Sulfur Recovery

LPGCondensateFractionation

SulfurStorage, Loading

Train - 2

Train - 3

Feed GasFromOffshore LNG

Liquids

Sulfur

CO2+H2S

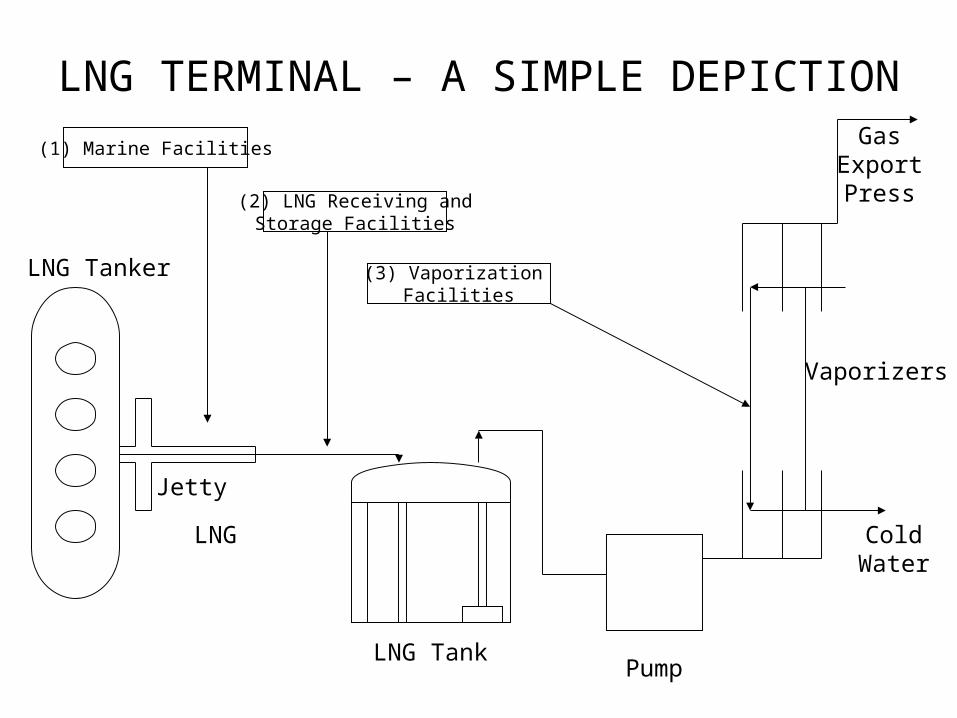

LNG TERMINAL – A SIMPLE DEPICTION

(1) Marine Facilities

(2) LNG Receiving andStorage Facilities

(3) Vaporization Facilities

LNG Tanker

Jetty

LNG

LNG TankPump

ColdWater

Vaporizers

GasExportPress

LNG DOWNSTREAM – BLOCK DIAGRAM

JETTY

UnloadingArms

Vapor ReturnArm

Return GasBlowers

Flare / Vent BOGcompressors

Storage Tanks

Recon denser

Vaporizer

HP Send- OutPump Re-gasification

System

ToPipelineLNG jetty, berth, unloading

LNG Storage tanksLNG re-gasification systemLNG Pumping System• In-tank and• External LNG PumpsVapor handling systemSupporting facilities

LNG CHARACTERISTICS Methane in Natural Gas does not liquefy under pressure. To make

LNG, Natural Gas must be liquefied through refrigeration. Becomes liquid at – 160 C at atmospheric pressure. Volume reduces by 620 times when liquefied. Spilled LNG will crack a steel plate like boiling water hitting frozen

glass.

LNG Composition (Typical Mol %)N --- 0 – 1.0%

Methane --- 85.1 – 96.7% (Lean)Ethane --- 1.9 – 8.6% (Rich)Propane --- 0.68 – 4.1%i – Butane, n – Butane --- Traces – 3.0%Mol. Wt. --- 16.8 – 20.0 (Rich)Gross Heating Value --- 10.450 Kcal / NMSpecific Gravity --- 0.44 – 0.50

LNG – GREEN AND SAFE

LNG is …• Odorless,• Non – toxic (harmful components removed)• And non – corrosive.

Less dense than water – evaporates if spilled in ocean or water bodies

LNG vapors are lighter than air – less chance of ignition if emitted.

LNG is not under pressure for shipping and storage.

LNG does not explode.

Natural gas burns more efficiently and cleaner than any other fuel.

Estimate of Natural Gas Reserves (TCM)

1997 2006 2009North Americe 8.3 8.0 8.0South / Central America

6.2 7.6 7.7

Europe & Eurasia 6.1 59.4 59.4Middle East 49.5 73.0 73.2Africa 10.6 14.5 14.6Asia Pacific 10.7 13.8 17.5Total 146.3 176.3 180.4

Estimate of Share of Gas Reserves

5%

41%

8%4%8%

34%

North America

S & Cent. America

Europe & Eurasia

Middle East

Africa

Asia Pacific

Country TCM %Share

Russian 43.30 23.44

Iran 29.61 16.03

Qatar 25.46 13.78

Turkmenistan 7.94 4.30

Saudi Arabia 7.57 4.10

America 15.80 8.55

United Arab Emirates

6.43 3.48

Nigeria 5.22 2.83

Egypt 2.02 1.09

Libya 1.50 0.81

Algeria 4.50 2.44

Indonesia 3.18 1.72

Malaysia 3.0 1.62

Iraq 3.17 1.72

Norway 2.91 1.58

Australia 2.51 1.36

Other 20.62 11.16

Total 184.74

• Major gas reserves awayfrom mature markets• Close to developing markets• Russia & Iran hold 40% of Gas reserve.• LNG exporting countries Hold 50% of reserves.

Estimate of Natural Gas Production (BCM / Year)

1997 2006 2009North America 735 754 785South / Central America

83 147 160

Europe & Eurasia

898 1076 1085

Middle East 175 339 400Africa 99 181 195Asia Pacific 245 373 400Total 2235 2870 3025

Prognosticated Natural Gas Demand

0

20

40

60

80

100

NATURAL GAS - NEXT 15 YEARS

N. America 26.931.834.4

W, europe 14.816.418.2

Asia 3.94.44.9

EE / FSU 23.527.330.9

Dev. Countries 21.225.229.8

200120102015

LNG Producing Countries EXISTING UNDER POSSIBLE TOTAL

CONSTRUCTION PROPOSED

ALGERIA 19.9 4.5 4.0 – 5.0 28.4 – 29.4

ANGOLA 0.0 5.2 0.0 5.2

AUSTRALIA 15.2 24.2 33.8 – 43.3 73.2 – 82.7

BRUNEI 7.2 0.0 0.0 7.2

EGYPT 12.3 3.6 5.1 21.0

EQUATEORIAL GUIENA 3.72 0.0 4.4 8.12

INDONESIA 26.2 7.6 2.0 35.8

IRAN 0.0 0.0 46.4 46.4

LIBYA 0.7 0.0 0.0 0.7

MALAYSIA 23.3 1.3 0.0 24.6

NIGERIA 22.2 8.40 22.0 52.6

NORWAY 4.18 0.0 0.0 4.18

OMAN 10.9 0.0 0.0 10.9

PAPUA NEW GUIENA 0.0 6.3 9 15.3

PERU 0.0 4.45 0.0 4.45

QATAR 30.4 46.8 0.0 7.2

RUSSIA 9.6 0.0 20 29.6

TRINDAD 15.3 0.0 5.2 20.5

UAE 5.6 0.0 0.0 5.6

USA 1.5 0.0 0.0 1.5

VENEZUYELA LNG 0.0 0.0 4.7 4.7

YEMEN 0.0 6.7 0.0 6.7

TOTAL 208.2 119.1 156.6 – 167.1 483.9 – 494.4

LNG CONSUMERS2005 2010 2015

Belgium 2.1 6.3 6.1

China 0.0 7.7 12.5

France 10.1 18.4 18.2

India 4.8 12.5 20.0

Italy 1.9 8.8 10.2

Japan 60.9 69.0 74.6

Mexico East 0.0 1.9 1.9

Mexico West 0.0 4.6 6.3

Singapore 0.0 0.0 1.1

South Korea 23.5 32.5 41.5

Spain 17.6 28.9 30.6

Taiwan 7.5 9.2 12.0

UK 0.4 14.0 21.6

US East 12.5 23.2 53.4

Others 5.9 13.4 30.5

Total 147.0 250.4 340.6