Trends in light rail in Europe by Keolis Metro & Light Rail Director

30

1 Trends in Light Rail in Europe Regis Hennion Metro & Light Rail Director 25 Feb 2016

Transcript of Trends in light rail in Europe by Keolis Metro & Light Rail Director

1

Trends in Light Rail in Europe

Regis Hennion

Metro & Light Rail Director25 Feb2016

Keolis

Europe: a look back

New systems: trams and tram-trains

Extensions everywhere

On the technical side

2

Trends in Light Rail in Europe

3

Keolis: an international leader in passenger transport

FrenchCompany

15countries

60,000employees

5.6 billion

revenue

1.3 billion

railway passengers

3 billion

passengers

Keolis operates and maintainspublic transport networks

in total safety

70%

30%

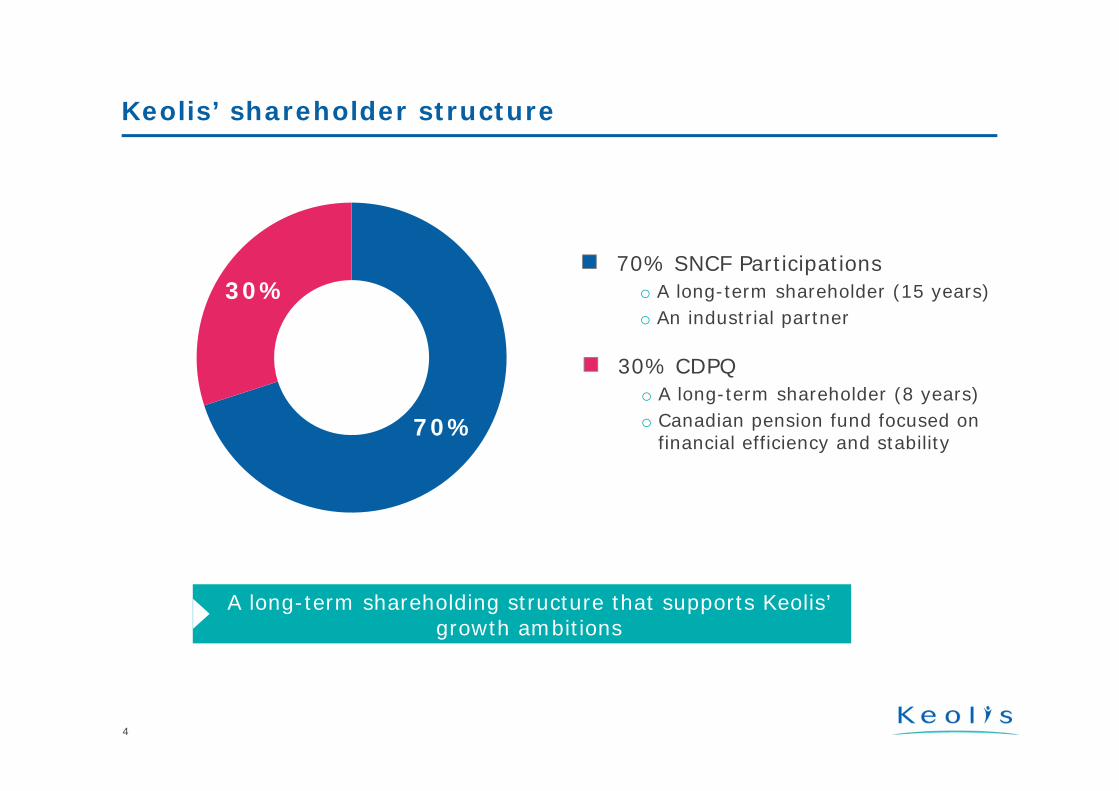

Keolis’ shareholder structure

4

A long-term shareholding structure that supports Keolis’ growth ambitions

70% SNCF Participationso A long-term shareholder (15 years)o An industrial partner

30% CDPQo A long-term shareholder (8 years)o Canadian pension fund focused on

financial efficiency and stability

5

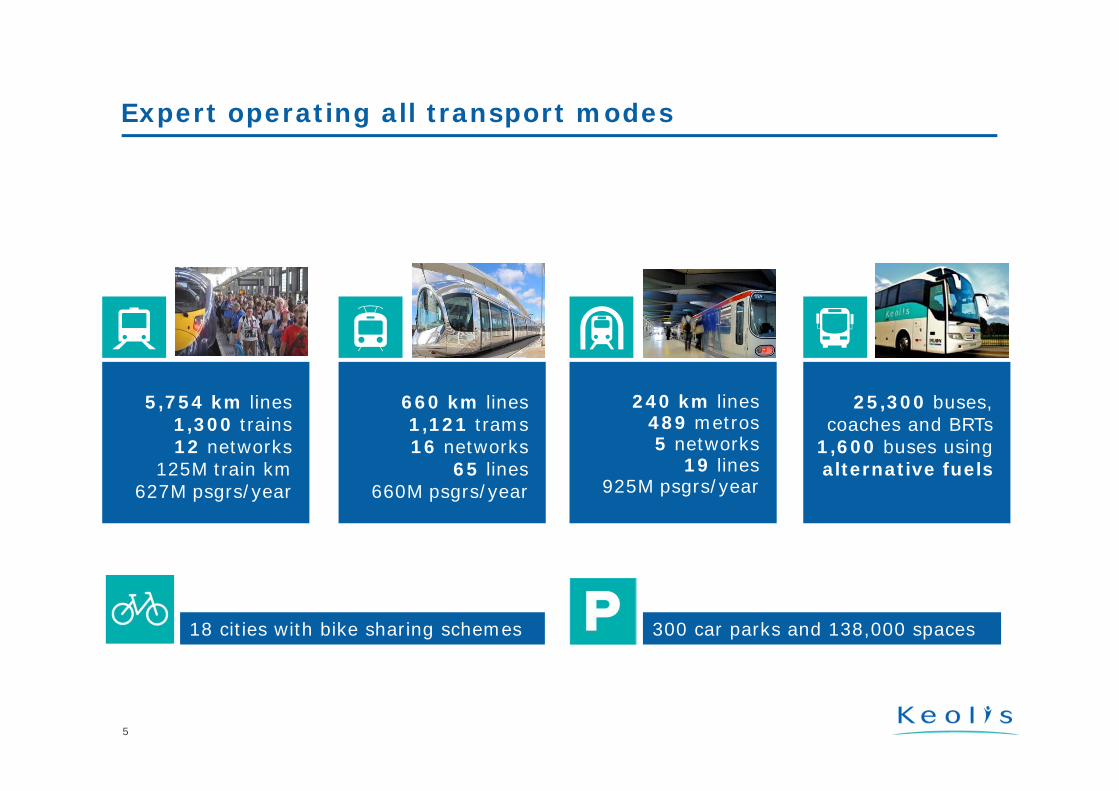

Expert operating all transport modes

5,754 km lines1,300 trains12 networks

125M train km627M psgrs/year

660 km lines1,121 trams16 networks

65 lines660M psgrs/year

25,300 buses, coaches and BRTs

1,600 buses usingalternative fuels

240 km lines489 metros5 networks

19 lines925M psgrs/year

18 cities with bike sharing schemes 300 car parks and 138,000 spaces

Keolis

Europe: a look back

New systems: trams and tram-trains

Extensions everywhere

On the technical side

6

Trends in Light Rail in Europe

7

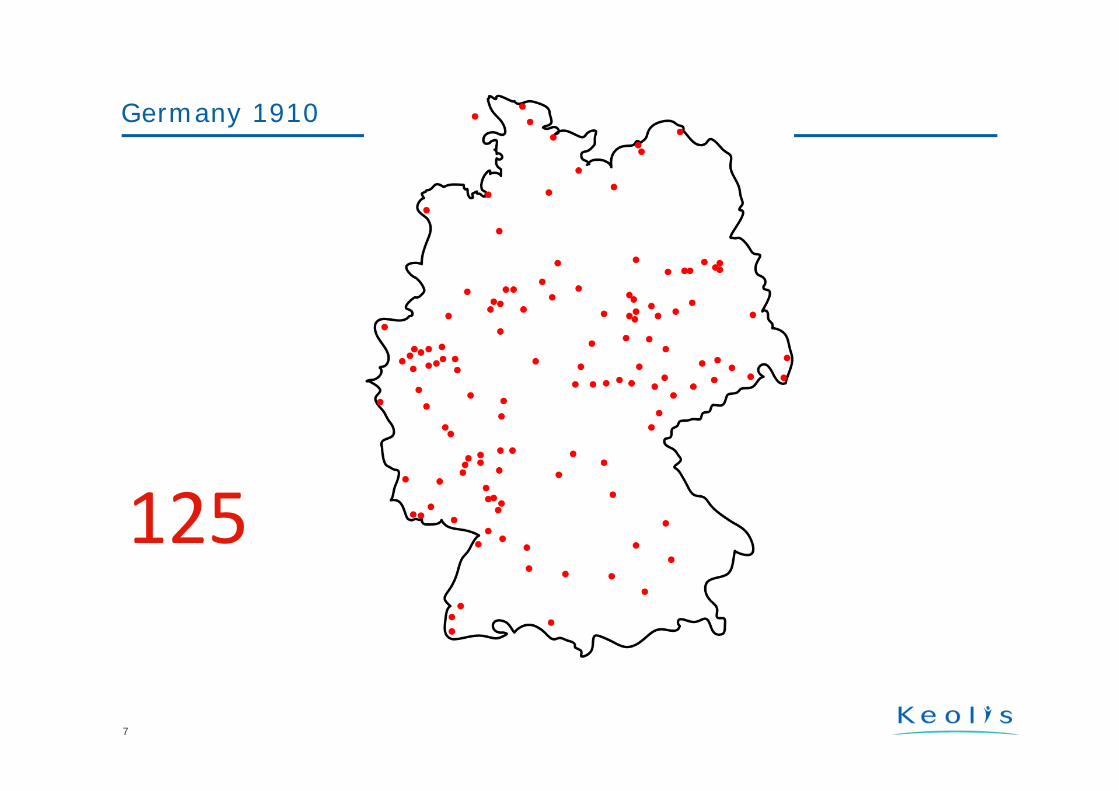

125

Germany 1910

8

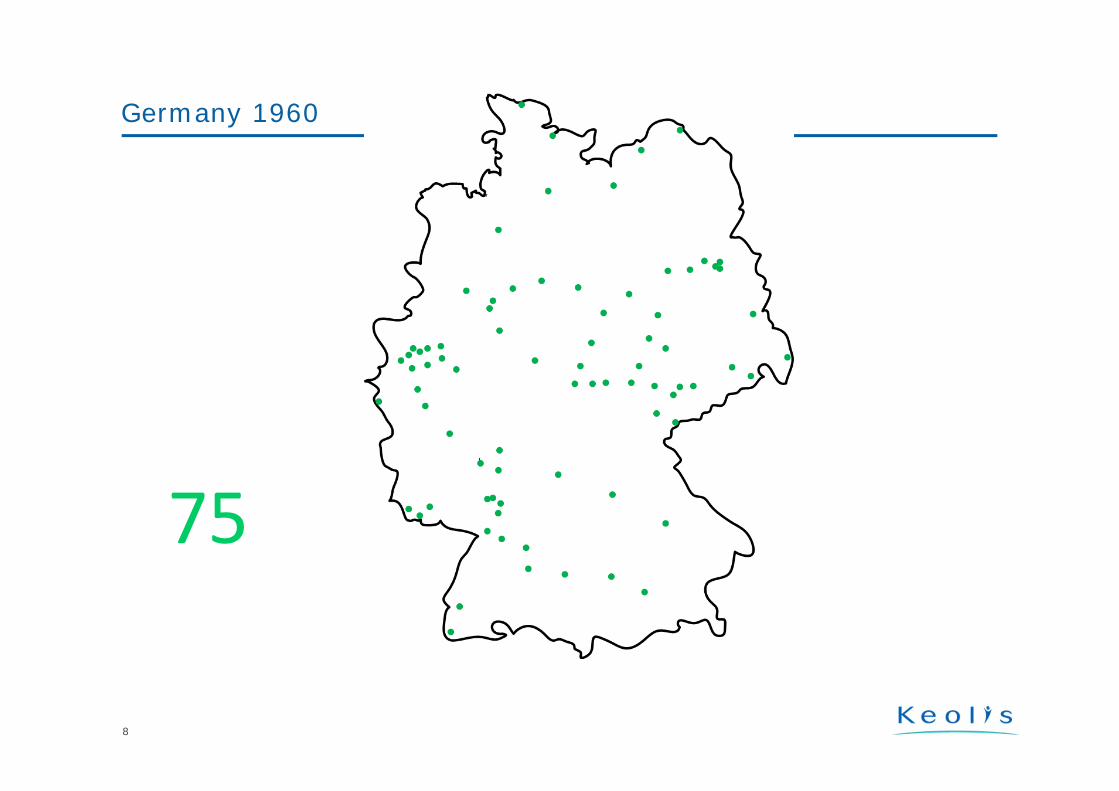

75

Germany 1960

9

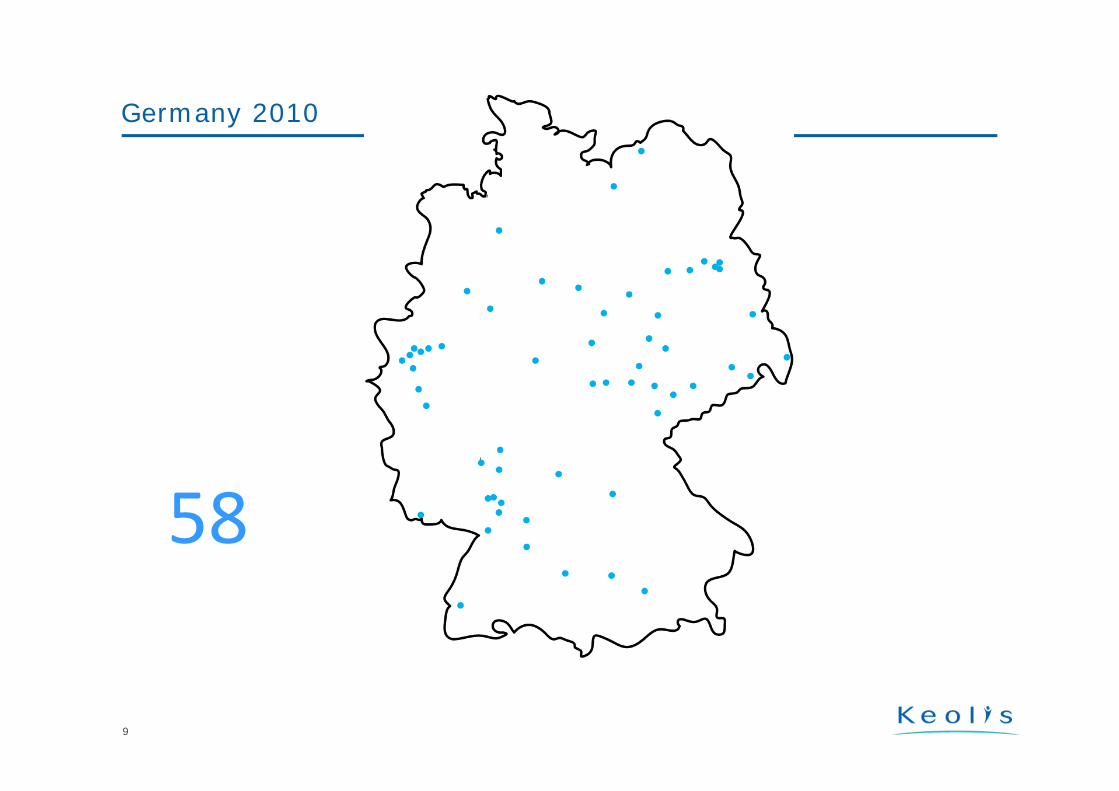

58

Germany 2010

10

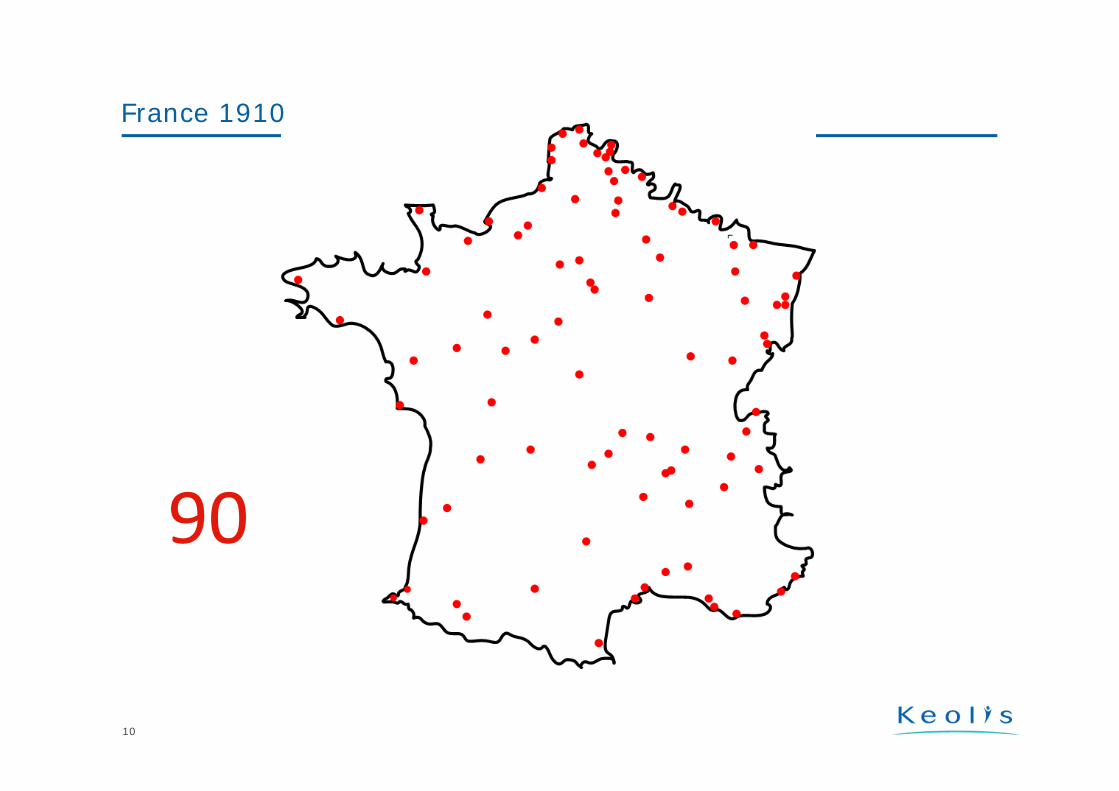

90

France 1910

11

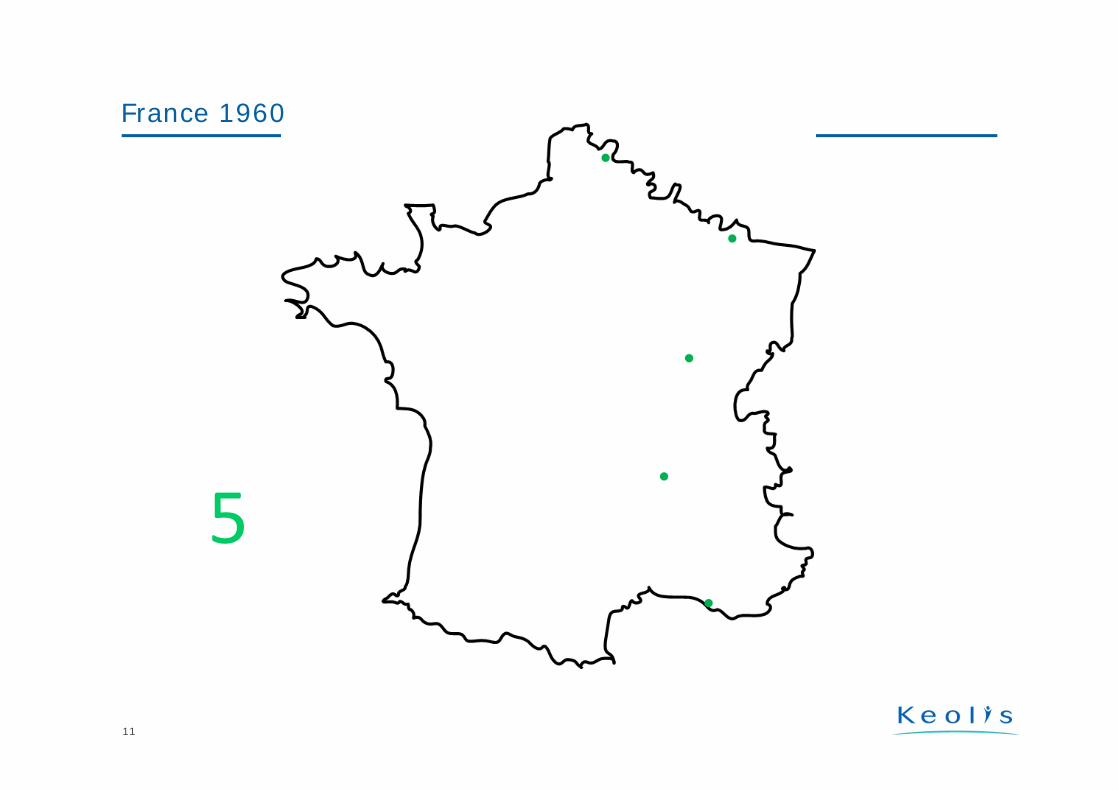

5

France 1960

12

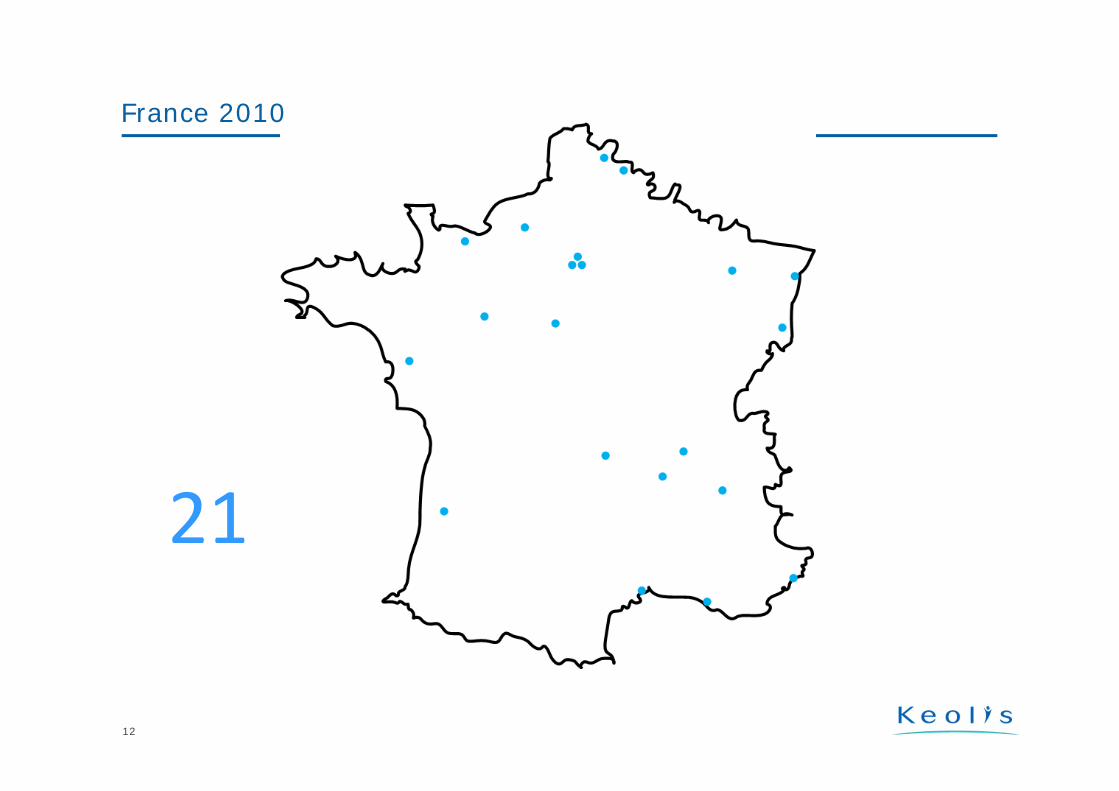

21

France 2010

Keolis

Europe: a look back

New systems: trams and tram-trains

Extensions everywhere

On the technical side

13

Trends in Light Rail in Europe

A strong demand for light rail

Some projects on hold because of economic turn down

BRT as an alternative?

But no strong appetite for PPPs

Many projects in Scandinavia

14

New systems tram and tram-train

15

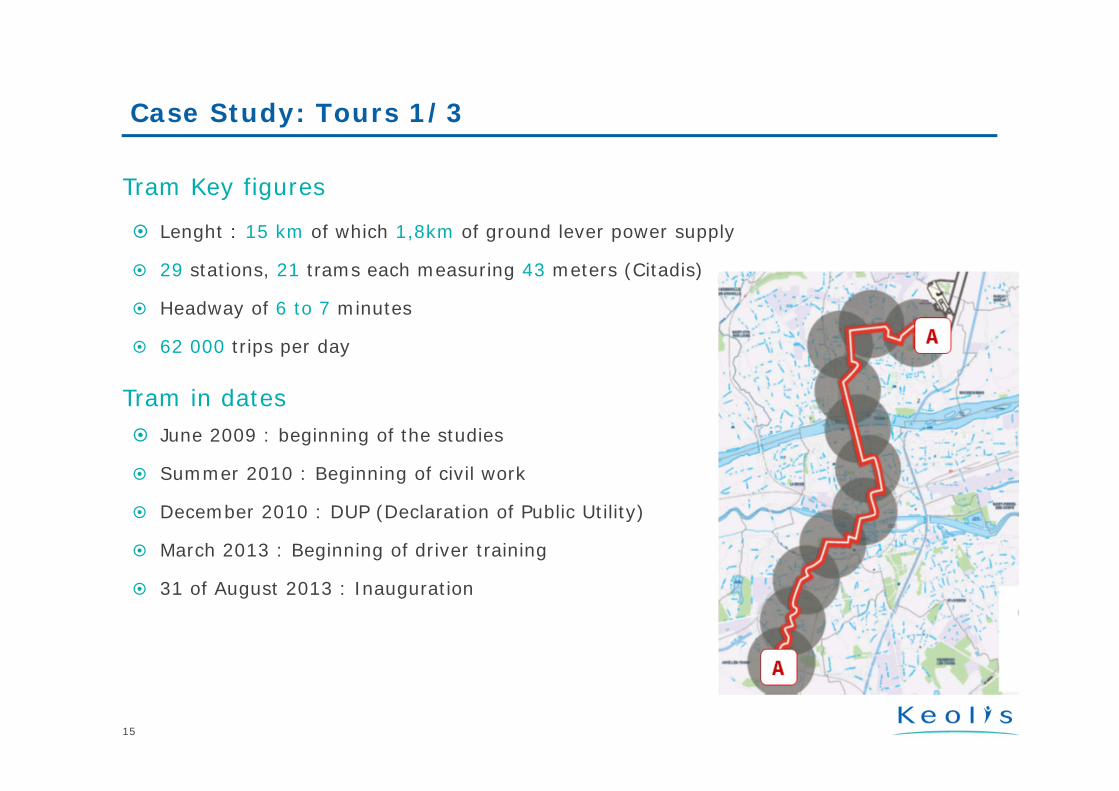

Case Study: Tours 1/3

Tram Key figures

Lenght : 15 km of which 1,8km of ground lever power supply

29 stations, 21 trams each measuring 43 meters (Citadis)

Headway of 6 to 7 minutes

62 000 trips per day

Tram in dates June 2009 : beginning of the studies

Summer 2010 : Beginning of civil work

December 2010 : DUP (Declaration of Public Utility)

March 2013 : Beginning of driver training

31 of August 2013 : Inauguration

16

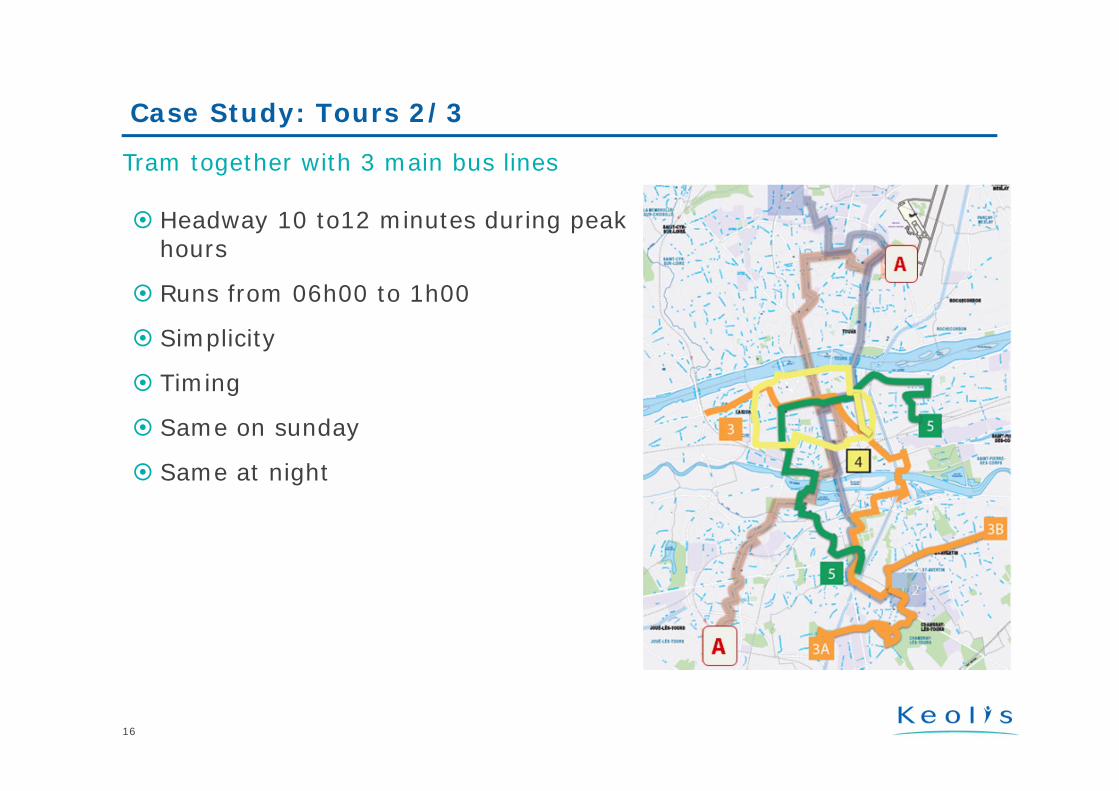

Case Study: Tours 2/3

Tram together with 3 main bus lines

Headway 10 to12 minutes during peak hours

Runs from 06h00 to 1h00

Simplicity

Timing

Same on sunday

Same at night

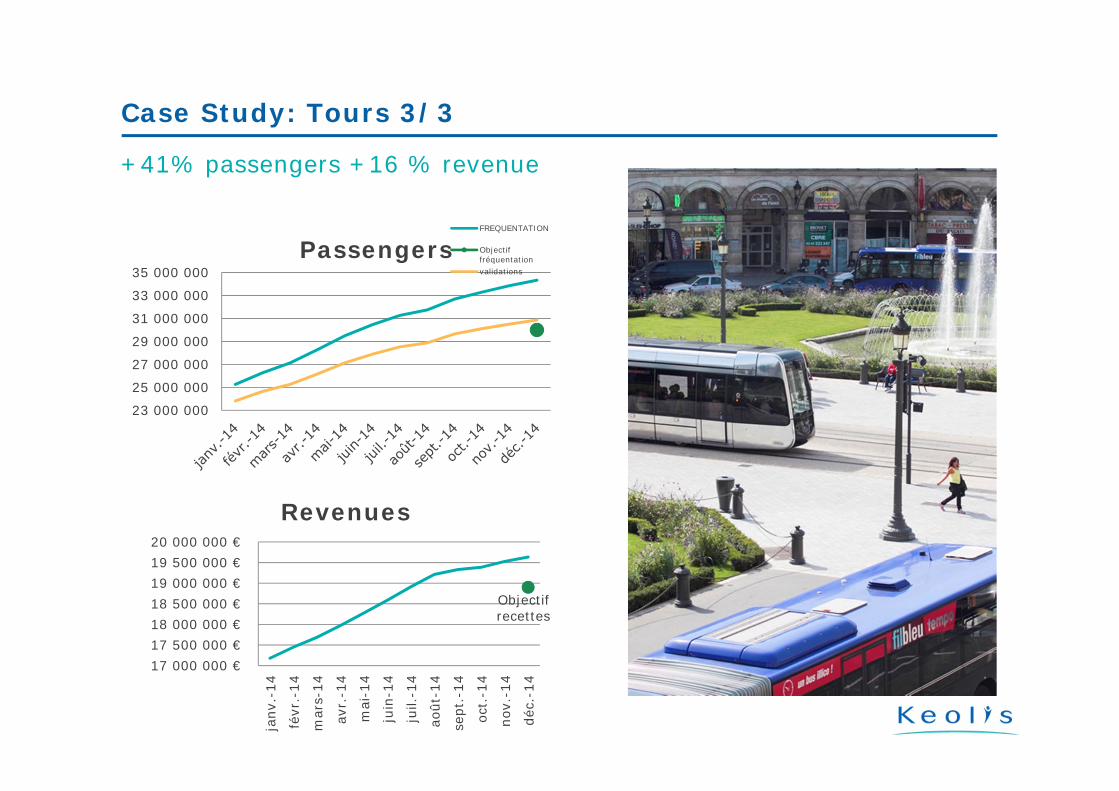

+41% passengers +16 % revenue

Case Study: Tours 3/3

23 000 000

25 000 000

27 000 000

29 000 000

31 000 000

33 000 000

35 000 000Passengers

FREQUENTATION

Objectiffréquentationvalidations

Objectif recettes

17 000 000 €17 500 000 €18 000 000 €18 500 000 €19 000 000 €19 500 000 €20 000 000 €

janv

.-14

févr

.-14

mar

s-14

avr.

-14

mai

-14

juin

-14

juil.

-14

août

-14

sept

.-14

oct.

-14

nov.

-14

déc.

-14

Revenues

18

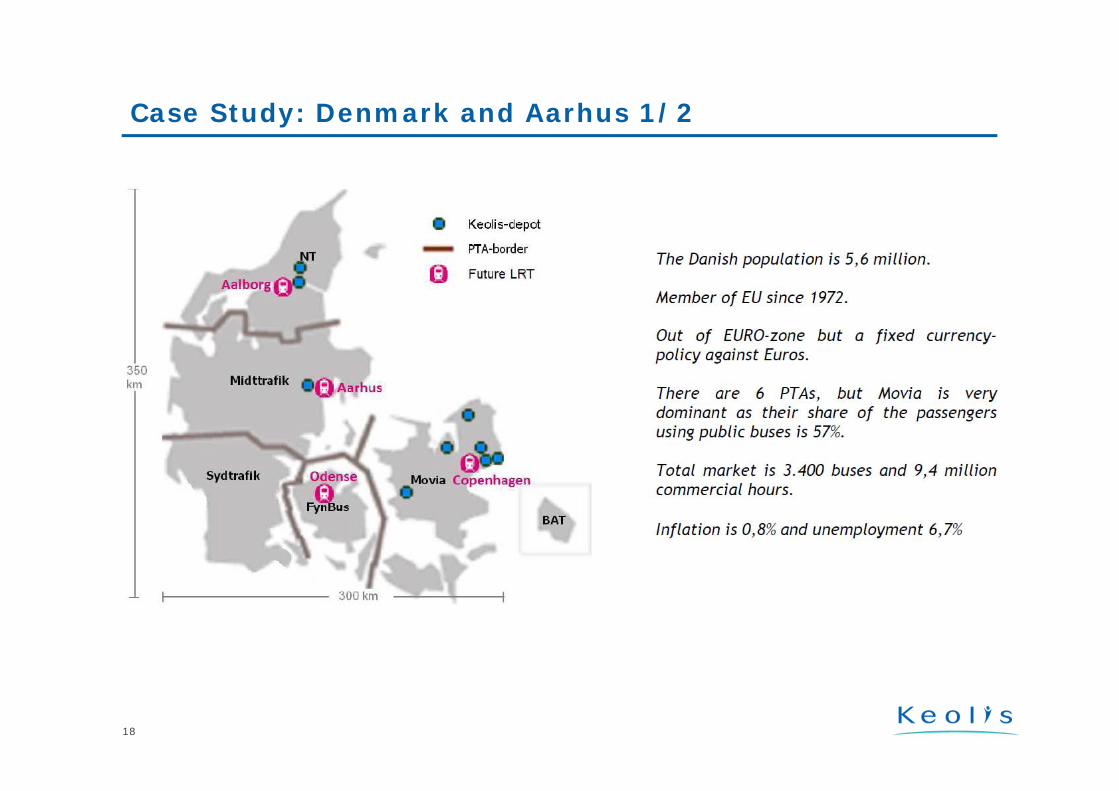

Case Study: Denmark and Aarhus 1/2

19

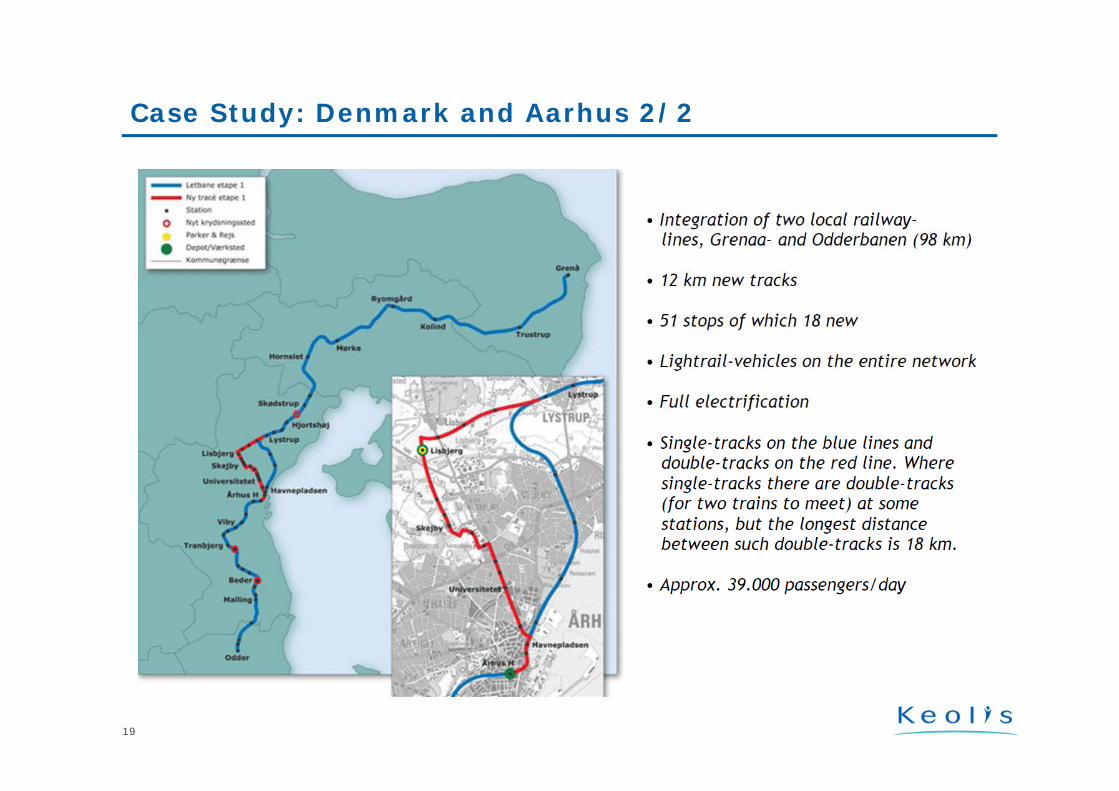

Case Study: Denmark and Aarhus 2/2

Keolis

Europe: a look back

New systems: trams and tram-trains

Extensions everywhere

On the technical side

20

Trends in Light Rail in Europe

21

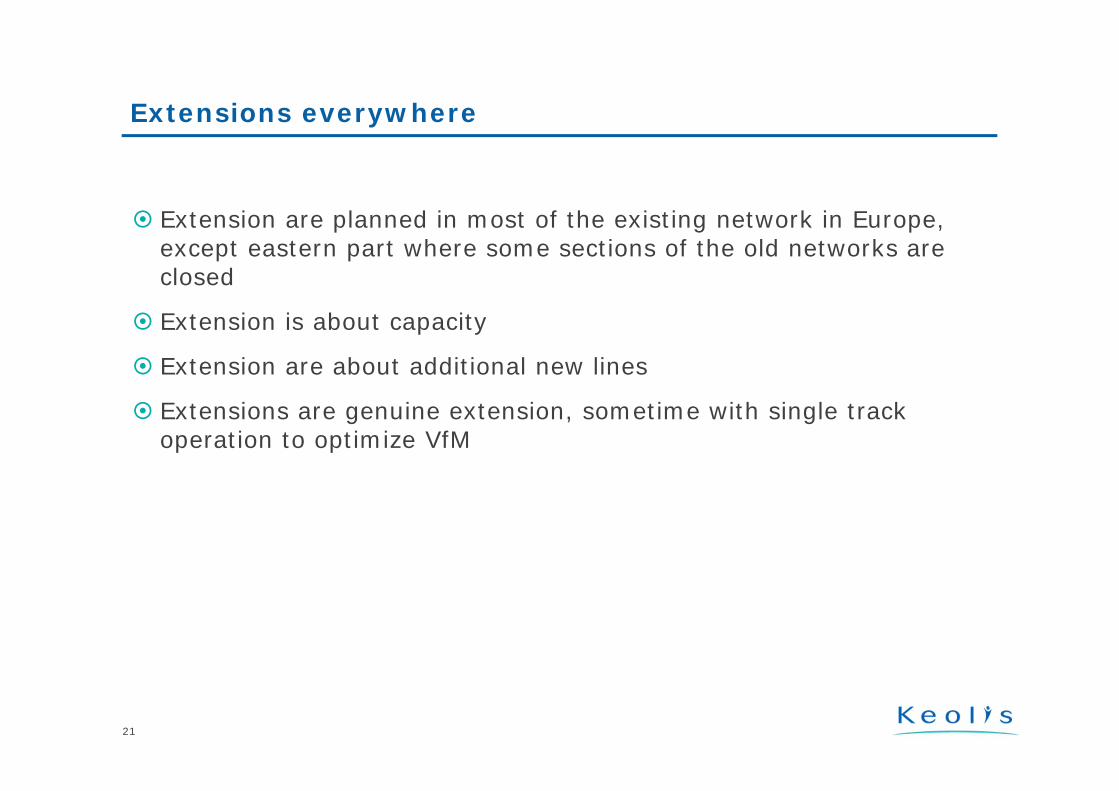

Extensions everywhere

Extension are planned in most of the existing network in Europe, except eastern part where some sections of the old networks are closed

Extension is about capacity

Extension are about additional new lines

Extensions are genuine extension, sometime with single track operation to optimize VfM

22

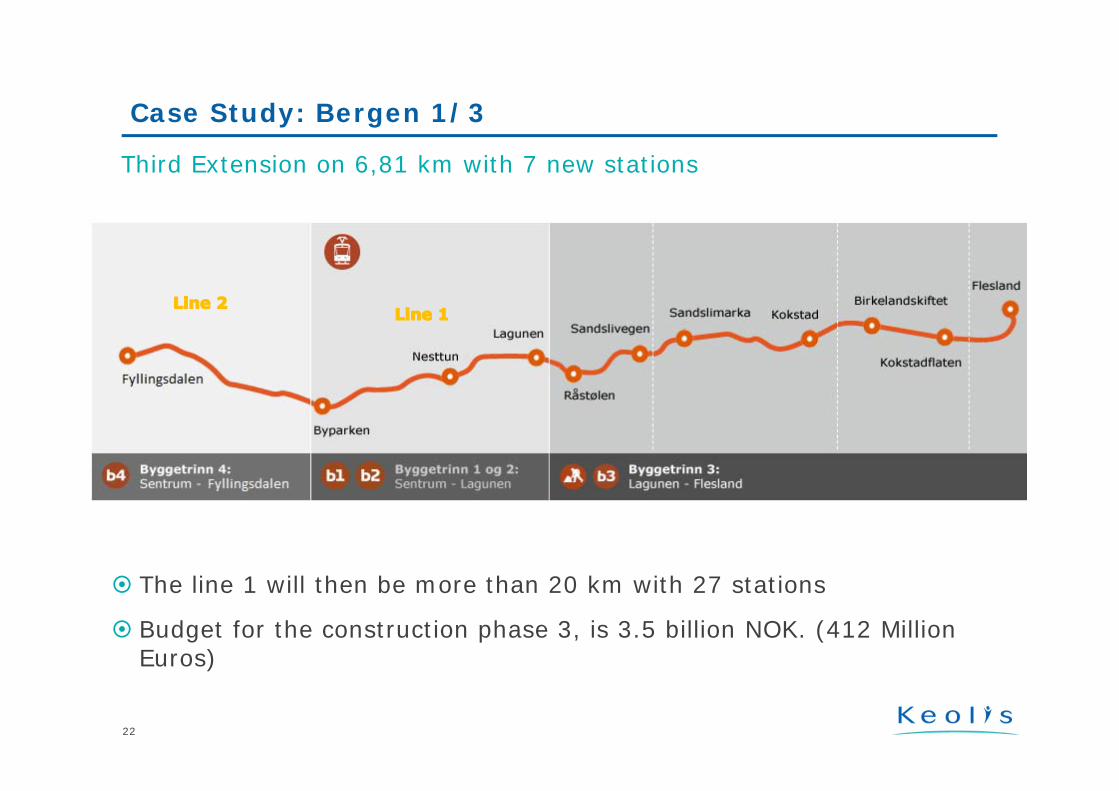

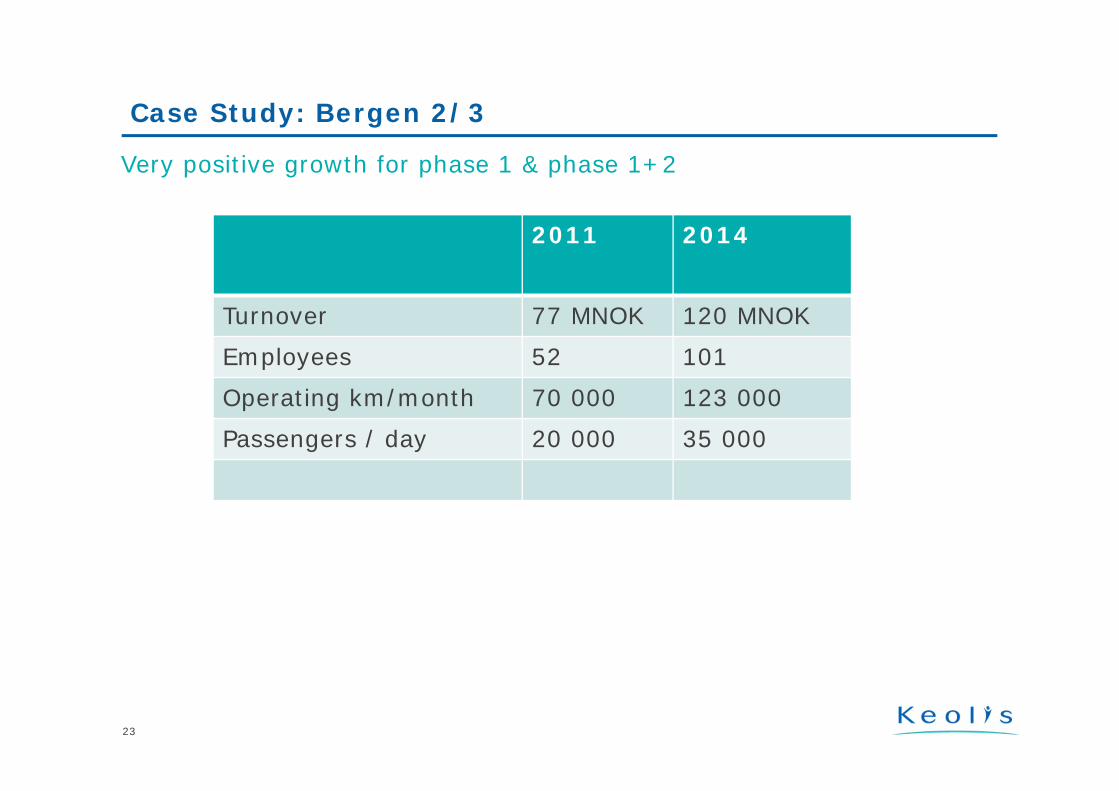

Case Study: Bergen 1/3

The line 1 will then be more than 20 km with 27 stations

Budget for the construction phase 3, is 3.5 billion NOK. (412 Million Euros)

Third Extension on 6,81 km with 7 new stations

23

Very positive growth for phase 1 & phase 1+2

Case Study: Bergen 2/3

2011 2014

Turnover 77 MNOK 120 MNOK

Employees 52 101

Operating km/month 70 000 123 000

Passengers / day 20 000 35 000

24

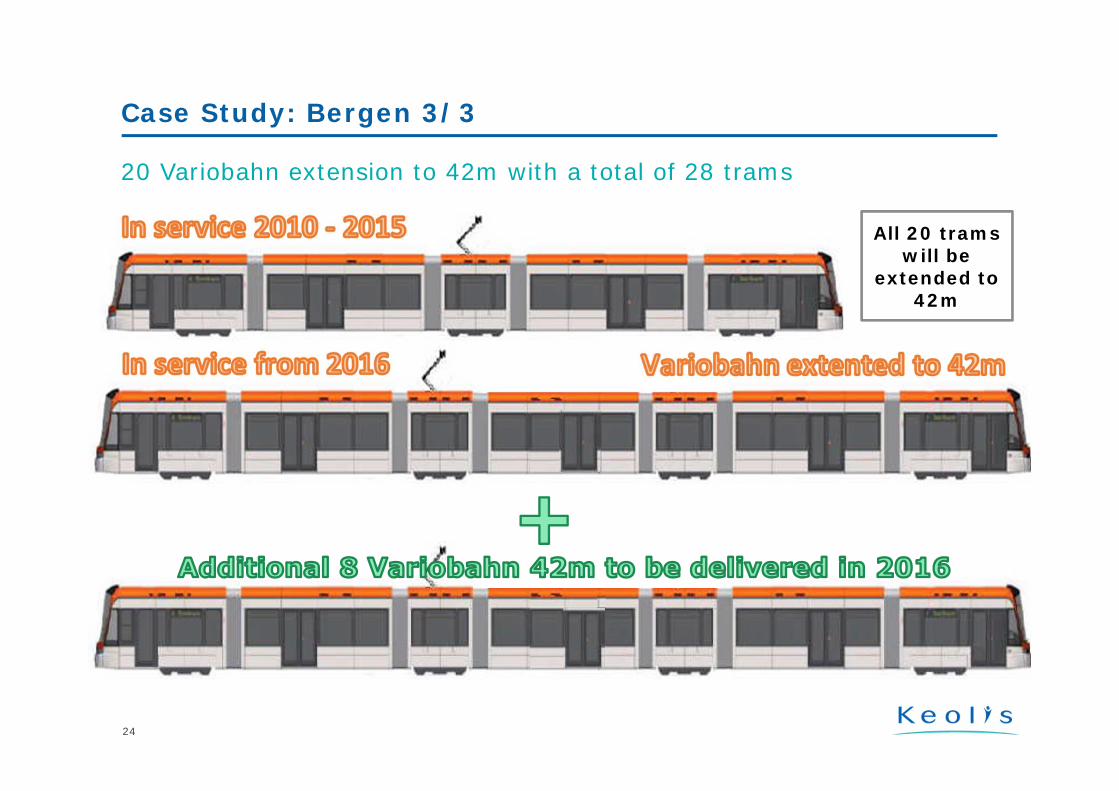

20 Variobahn extension to 42m with a total of 28 trams

Case Study: Bergen 3/3

All 20 trams will be

extended to 42m

25

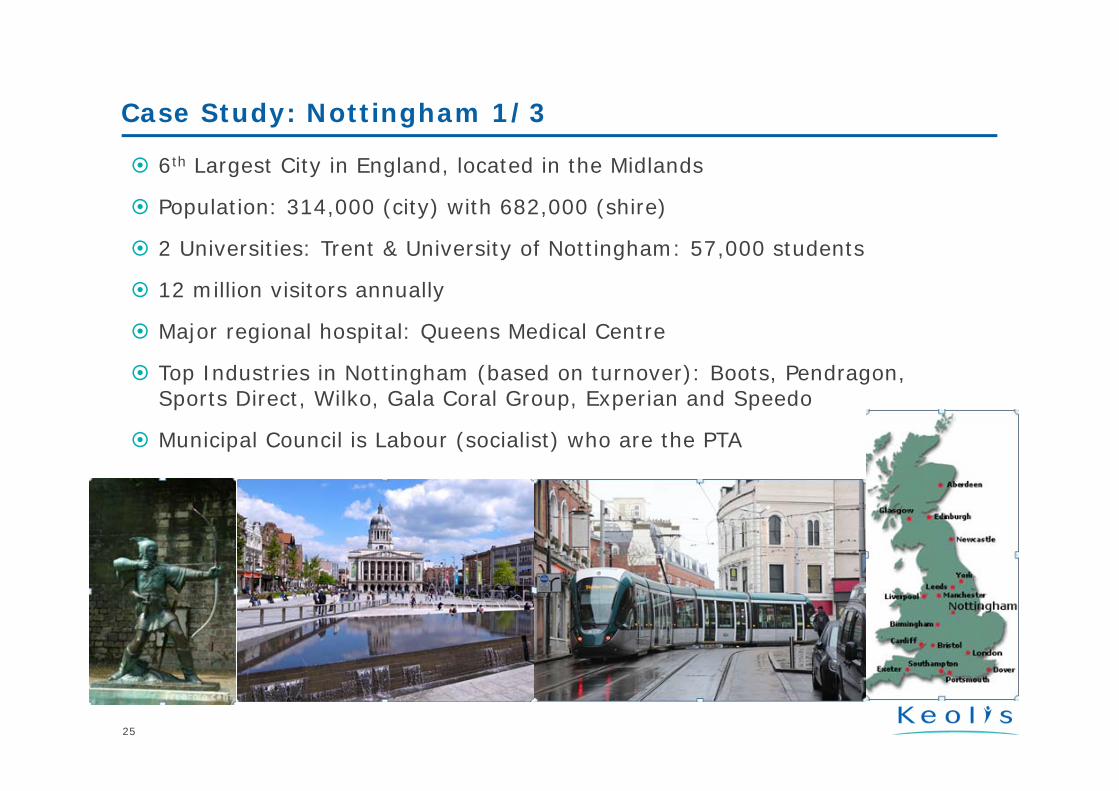

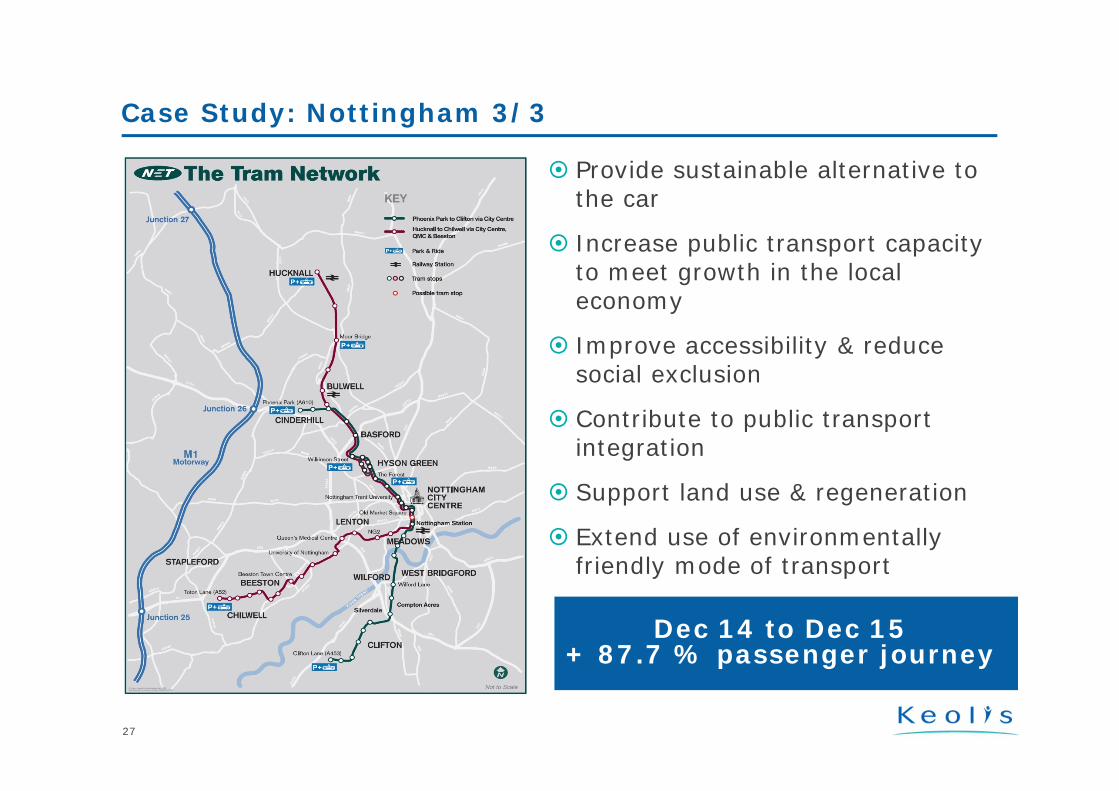

Case Study: Nottingham 1/3

6th Largest City in England, located in the Midlands

Population: 314,000 (city) with 682,000 (shire)

2 Universities: Trent & University of Nottingham: 57,000 students

12 million visitors annually

Major regional hospital: Queens Medical Centre

Top Industries in Nottingham (based on turnover): Boots, Pendragon, Sports Direct, Wilko, Gala Coral Group, Experian and Speedo

Municipal Council is Labour (socialist) who are the PTA

26

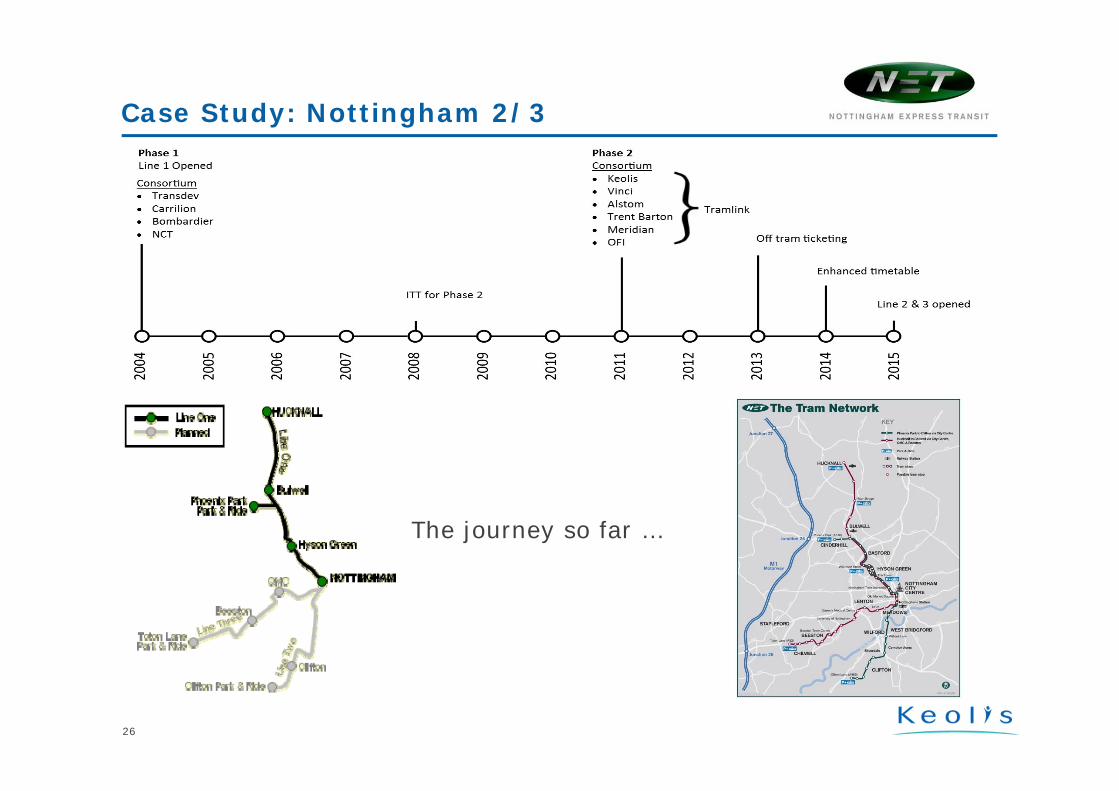

Case Study: Nottingham 2/3

The journey so far …

Provide sustainable alternative to the car

Increase public transport capacity to meet growth in the local economy

Improve accessibility & reduce social exclusion

Contribute to public transport integration

Support land use & regeneration

Extend use of environmentally friendly mode of transport

27

Case Study: Nottingham 3/3

Dec 14 to Dec 15 + 87.7 % passenger journey

Keolis

Europe: a look back

New systems: trams and tram-trains

Extensions everywhere

On the technical side

28

Trends in Light Rail in Europe

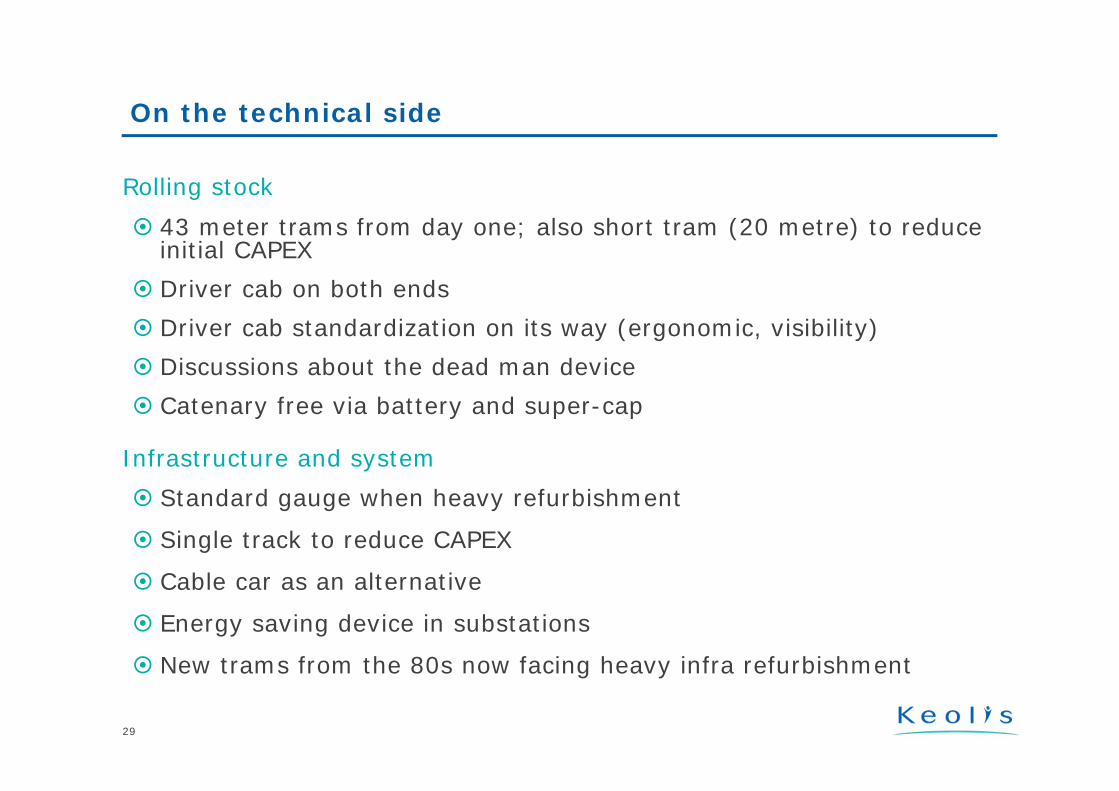

43 meter trams from day one; also short tram (20 metre) to reduce initial CAPEX

Driver cab on both ends Driver cab standardization on its way (ergonomic, visibility) Discussions about the dead man device Catenary free via battery and super-cap

29

On the technical side

Rolling stock

Standard gauge when heavy refurbishment

Single track to reduce CAPEX

Cable car as an alternative

Energy saving device in substations

New trams from the 80s now facing heavy infra refurbishment

Infrastructure and system

Thank youfor your attention

Thank you for your attention

Questions / Answers