TRENDS IN ISLAMIC PROJECT AND … copy available at: 1753252 1 TRENDS IN ISLAMIC PROJECT AND...

33

Electronic copy available at: http://ssrn.com/abstract=1753252 1 TRENDS IN ISLAMIC PROJECT AND INFRASTRUCTURE FINANCE IN THE MIDDLE EAST: RE‐EMERGENCE OF THE MURĀBAHA Michael J.T. McMillen* “Ah! that is clearly a metaphysical speculation, and like most metaphysical speculations has very little reference at all to the actual facts of real life, as we know them.” “Even these metallic problems have their melodramatic side.” “True. In matters of grave importance, style, not sincerity is the vital thing.” Oscar Wilde, THE IMPORTANCE OF BEING EARNEST (1895, in premier) INTRODUCTION This paper focuses on a trend in Islamic financing of Middle Eastern project and infrastructure transactions that emerged during the 2007 global financial crisis. That financial crisis, and some concurrent events within the Islamic finance field, resulted in an abrupt and dramatic change in the structures used to implement these types of financings. The confident 2007‐2008 prognostications of massive project and infrastructure spending, particularly in the Middle East, proved incorrect, at least in terms of timing. 1 While some oil rich nations that invested cautiously in the last decade, such as Saudi Arabia, Abu Dhabi and Qatar, have continued their projects, most countries severely reduced project and infrastructure spending. 2 Global recession ensued. Private commercial financing ran, and continues * Michael J.T. McMillen is a member of the bar of the State of New York, United States of America. Dr. McMillen has been the chair of and senior advisor to the Islamic Finance Section, American Bar Association, Section on International Law, and is an Adjunct Professor, Islamic Finance, University of Pennsylvania Law School. Copyright © and all intellectual property rights (text, 2010; Figures, as noted in each Figure), retained by, and reserved to, Michael J.T. McMillen. An earlier version of this paper was published as Trends in Islamic Project and Infrastructure Finance in the Middle East: Re‐Emergence of the Murabaha, in INVESTING IN THE GCC MARKETS:NEW OPPORTUNITIES IN A CHANGING LANDSCAPE, Kamar Jaffer and Sohail Jaffer, eds., at 133 (2009). To enhance accessibility to readers outside the United States (and outside the legal profession), citations have not yet been conformed to the Blue Book: A Uniform System of Citation. Draft of September 8, 2011 1 See, generally, Michael J.T. McMillen, Islamic Project Finance: An Introduction to Principles and Structures, III GLOBAL INFRASTRUCTURE 1 (2009), Fulbright & Jaworski L.L.P. (entire issue) (“McMillen – Islamic Project Finance”), and the sources cited at notes 5, 7 and 11. With respect to project and infrastructure financing activity, see, e.g.: Middle East contracts awarded: June 2009, MEED, 11 June 2009, updated 17 June 2009, at http://www.meed.com/printPagel.html?pageid=2033705; Gulf Projects July 2009: Index rises 1.1 per cent, MEED, 29 July 2009, at http://www.meed.com/printPage.html?padeid=2039298; Key transport projects in the region weather the economic storm, MEED, 2 July 2009, updated 15 July 2009, at http://www.meed.com/printPage.html?pageid=2036201; Transport Outlook 2009,INFRASTRUCTURE JOURNAL, March 18, 2009, at http://www.ijonline.com/genv2/Secured/print/PrintArticle.aspx?ArticleID=54766; Debt Funding in Infrastructure 2009, INFRASTRUCTURE JOURNAL, April 1, 2009, at http://wwww.ijonline.com/genv2/Secured/print/PrintArticle.aspex?ArticleID=55129; and Islamic banks fill funding gap for regional projects, MEED, 8 April 2009, at http://www.meed.com/printPage.html.pageid=2017759. 2 See Mathew Martin, Project Finance Market Remains Muted in the Middle East, 6 MEED 11‐17 February 2011, available at http://www.meed.com/sectors/finance/banking/project‐finance‐market‐remains‐muted‐in‐the‐

Transcript of TRENDS IN ISLAMIC PROJECT AND … copy available at: 1753252 1 TRENDS IN ISLAMIC PROJECT AND...

Electronic copy available at: http://ssrn.com/abstract=1753252

1

TRENDS IN ISLAMIC PROJECT AND INFRASTRUCTURE FINANCE IN THE MIDDLE EAST: RE‐EMERGENCE OF THE MURĀBAHA

Michael J.T. McMillen*

“Ah! that is clearly a metaphysical speculation, and like most metaphysical speculations has very

little reference at all to the actual facts of real life, as we know them.”

“Even these metallic problems have their melodramatic side.”

“True. In matters of grave importance, style, not sincerity is the vital thing.”

Oscar Wilde, THE IMPORTANCE OF BEING EARNEST (1895, in premier)

INTRODUCTION

This paper focuses on a trend in Islamic financing of Middle Eastern project and infrastructure

transactions that emerged during the 2007 global financial crisis. That financial crisis, and some

concurrent events within the Islamic finance field, resulted in an abrupt and dramatic change in the

structures used to implement these types of financings. The confident 2007‐2008 prognostications of

massive project and infrastructure spending, particularly in the Middle East, proved incorrect, at least in

terms of timing.1 While some oil rich nations that invested cautiously in the last decade, such as Saudi

Arabia, Abu Dhabi and Qatar, have continued their projects, most countries severely reduced project

and infrastructure spending.2 Global recession ensued. Private commercial financing ran, and continues

* Michael J.T. McMillen is a member of the bar of the State of New York, United States of America. Dr. McMillen has been the chair of and senior advisor to the Islamic Finance Section, American Bar Association, Section on International Law, and is an Adjunct Professor, Islamic Finance, University of Pennsylvania Law School. Copyright © and all intellectual property rights (text, 2010; Figures, as noted in each Figure), retained by, and reserved to, Michael J.T. McMillen. An earlier version of this paper was published as Trends in Islamic Project and Infrastructure Finance in the Middle East: Re‐Emergence of the Murabaha, in INVESTING IN THE GCC MARKETS: NEW

OPPORTUNITIES IN A CHANGING LANDSCAPE, Kamar Jaffer and Sohail Jaffer, eds., at 133 (2009). To enhance accessibility to readers outside the United States (and outside the legal profession), citations have not yet been conformed to the Blue Book: A Uniform System of Citation. Draft of September 8, 2011 1 See, generally, Michael J.T. McMillen, Islamic Project Finance: An Introduction to Principles and Structures, III GLOBAL INFRASTRUCTURE 1 (2009), Fulbright & Jaworski L.L.P. (entire issue) (“McMillen – Islamic Project Finance”), and the sources cited at notes 5, 7 and 11. With respect to project and infrastructure financing activity, see, e.g.: Middle East contracts awarded: June 2009, MEED, 11 June 2009, updated 17 June 2009, at http://www.meed.com/printPagel.html?pageid=2033705; Gulf Projects July 2009: Index rises 1.1 per cent, MEED, 29 July 2009, at http://www.meed.com/printPage.html?padeid=2039298; Key transport projects in the region weather the economic storm, MEED, 2 July 2009, updated 15 July 2009, at http://www.meed.com/printPage.html?pageid=2036201; Transport Outlook 2009, INFRASTRUCTURE JOURNAL, March 18, 2009, at http://www.ijonline.com/genv2/Secured/print/PrintArticle.aspx?ArticleID=54766; Debt Funding in Infrastructure 2009, INFRASTRUCTURE JOURNAL, April 1, 2009, at http://wwww.ijonline.com/genv2/Secured/print/PrintArticle.aspex?ArticleID=55129; and Islamic banks fill funding gap for regional projects, MEED, 8 April 2009, at http://www.meed.com/printPage.html.pageid=2017759. 2 See Mathew Martin, Project Finance Market Remains Muted in the Middle East, 6 MEED 11‐17 February 2011, available at http://www.meed.com/sectors/finance/banking/project‐finance‐market‐remains‐muted‐in‐the‐

Electronic copy available at: http://ssrn.com/abstract=1753252

2

to run, tepid. To the extent there is discussion of project and infrastructure financing in the private

commercial realm, the discussion focuses on models that were previously reserved to real estate

financings: e.g., the mini‐perm financings involving short‐term construction loans. Sukūk markets went

abruptly dormant, in sharp contrast to the pre‐September 2008 patterns.3 Conventional capital markets

were and remain quiescent. Liquidity is severely restricted. The wide range of Sharīʿah‐compliant

financing devices used prior to September 2008 has disappeared.

What has emerged through this period, where financing is available, is increasing use of murābaha

financing structures. The murābaha has long been a staple of short‐term financings and working capital

financings and the primary device for revolving credit facilities. Its use in term financings has increased

markedly since 2007. And it seems to have become more prominent in sukūk issuances (directly and via

sukūk al‐wakāla bil istithmar). It seems only slight exaggeration to say that trends in Islamic project and

infrastructure finance have been reduced (at least for the moment) to a single trend, comprised of a

single word: murābaha.4

middle‐east/3086822.article (“Martin: Project Finance”). See, also, Mathew Martin, Project Finance in Saudi Arabia: Slow Off the Blocks, 21 MEED 21‐27 May 2010, available at http://www.meed.com/sectors/finance/project‐finance/project‐finance‐in‐saudi‐arabia‐slow‐off‐the‐blocks/3006560.article. Martin: Project Finance notes that the total amount of project financing raised in 2010 for Middle Eastern projects was US$ 33.7 billion for 13 projects, with nearly all of that amount provided by Middle Eastern banks. That compares with US$ 40 billion raised in 2008 for 29 projects and US$ 24 billion raised in 2009. For 2010, 70% of the total project financing was raised for projects in Saudi Arabia, followed by Egyptian projects at 12% of the total and Emirati projects at 9% of the total. Most of the projects financed in 2010 were oil and gas projects (54.3%), followed by industrial projects (34%) and power and water projects (11.7%). As noted in Mathew Martin, Saudi Banks Support Project Finance Sector, 6 MEED 11‐17 February 2011, available at http://www.meed.com/sectors/finance/banking/saudi‐banks‐support‐project‐finance‐sector/3086949.article, the financing pattern is clearly provision of local financing in local currencies by local banks for local projects, where bank financing is available at all; there is relatively little financing on a regional (or international) basis. Long‐term financing is relatively difficult to obtain, and conventional bonds are emerging as a primary source of funding. See, e.g., James Gavin, Bonds Bridging the Funding Gap, 6 MEED 11‐17 February 2011, available at http://www.meed.com/sectors/finance/banking/bonds‐bridging‐the‐funding‐gap/3086961.article, and James Gavin, Issuers Favour Traditional Bonds, 15 MEED 9‐15 April 2010, available at http://www.meed.com/sectors/finance/bonds/issuers‐favour‐traditional‐bonds/3005537.article. These articles also note that conventional bonds are being preferred over sukūk offerings, possibly as a result of defaults on sukūk issuances during the financial crisis. That is not to say, however, that sukūk are being avoided altogether: only that conventional bonds are taking a larger portion of the issuance pie, particularly in refinancing transactions. In addition, public‐private‐partnership structures are gaining acceptance. See, e.g., James Gavin, Private Partnerships Win Acceptance in the Middle East, 6 MEED 11‐17 February 2011, available at http://www.meed.com/sectors/finance/banking/private‐partnerships‐win‐acceptance‐in‐the‐middle‐east/3086975.article. And, of course, state spending in the region is a mainstay of various national economic platforms and financing programs. See, e.g., Mathew Martin, State Spending Averts Recession in Saudi Arabia, 13 MEED 26 March – 1 April 2010, available at http://www.meed.com/sectors/economy/government/state‐spending‐averts‐recession‐in‐saudi‐arabia/3005192.article. 3 Michael McMillen and John A. Crawford, Sukuk in the First Decade: By The Numbers, DOW JONES ISLAMIC

MARKET INDEXES NEWSLETTER, ISSUE 3, December 2008 (“McMillen and Crawford”), available at http://img.en25.com/Web/DowJonesIndexes/DJIM_QNL_120408.pdf. 4 The murābaha is generally used by individual banks or financial institutions to provide financing, whereas sukūk are used to obtain financing from the capital markets. Sukūk al‐murābaha and some mixed‐instrument

3

It has long been recognized that the murābaha is the most frequently used, and the most frequently

abused, structure in Islamic finance.5 It has been the staple for short‐term investment and working

capital transactions, and the primary device for revolving credit facilities. It has been used in some term

financings, although on a limited basis. It has been a significant element of sukūk issuances since the

inception of those markets.6 But, if the anecdotal and experiential observations of practitioners are any

indication, the murābaha has never before been as pervasive in sophisticated financing transactions as

at the current time.

Many finance practitioners (too many) tend to dismiss the murābaha as a simplistic structure. More

ominously, they tend to aver that the murābaha is an easy way to convert an interest‐based lending

arrangement into a Sharīʿah ‐compliant transaction. To these practitioners, it seems that the murābaha

is a lowly creature, unworthy of rigorous analysis and discussion. Sharīʿah scholars do not share that

sukūk do make use of the murābaha to access the capital markets, but are subject to restrictions. It is difficult, if not impossible, to determine the extent to which use of bank murābaha have successfully substituted for sukūk in meeting financing requirements in the current economic environment because of severe liquidity restrictions concurrently in both the commercial financing markets and the capital markets. In the sukūk markets, there has been a trend toward the use of sukūk wakāla bil istithmar, or agency sukūk, which allows for incorporation of a greater percentage of murābaha transactions in the sukūk structure. See, e.g., Adnan Halawi, The Rise of Wakala, GLOBAL SUKUK REVIEW, ZAWYA SUKUK MONITOR, August 2011, available at http://ae.zawya.com/sukuk/Story.cfm/sidZAWYA20110905081630. 5 Yusuf Talal DeLorenzo, Murabaha, Sales of Trust, and Money‐value of Time (“DeLorenzo: Murābaha”), in PROCEEDINGS OF THE SECOND HARVARD UNIVERSITY FORUM ON ISLAMIC FINANCE: ISLAMIC FINANCE IN THE 21ST

CENTYURY (1998), 145, at 147‐49, discusses the rationale and the arguments for Islamic authenticity of the murābaha, noting that the rationale is largely one of the economic function of the structure and that the authenticity, as a matter of the Qurʾān, ḥadīth and fiqh, is imprecise, inconclusive and reliant upon those indicators of legitimacy that are accorded the least weight by jurists. Wahbah Al‐Zuḥayli presents a summary of the proof of the permissibility of the murābaha in Wahbah al‐Zuḥaylī, AL‐FIQH AL‐ISLĀMĪ WA‐ADILLATUH (ISLAMIC JURISPRUDENCE AND ITS PROOFS) (FOURTH EDITION, 1997), FINANCIAL TRANSACTIONS IN ISLAMIC JURISPRUDENCE, Mahmoud El‐Gamal, translator, and Muhammad S. Eissa, revisor (2002) (being a translation of volume 5 (the translation appears in two volumes; all references are to Volume 1)) (“Al‐Zuhayli”), at 354. With respect to the approval of modern financing commodities murabāha transactions, although not the metals murābaha transactions discussed in this paper, see Al‐Zuhayli at 360‐62. Abdul‐Rahman Abdullah bin Aqeel, Shari’ah Precautionary Procedures in Murabaha and Istisna’: A Practical Persepctive (“bin Aqeel: Murābaha”), in Second Harvard Forum, 127, at 127‐28, discusses the variance of contemporary financing murābaha transactions from classical murābaha transactions, generally and with respect to a range of specific transactional and contractual elements, some of which remain matters of controversy among the Sharīʿah scholars.

In 1995, it was estimated that 70% of all financing activity of Islamic banks was conducted using the murābaha contract. See Nicholas Dylan Ray, ARAB ISLAMIC BANKING AND THE RENEWAL OF ISLAMIC LAW (1995), at 37. Many professionals active in the Islamic banking, finance and investment industry believe that the figure may not have changed significantly to date (despite the emergence of sukūk as capital market tools). With respect to sukūk issuances since the inception of the Islamic finance (“debt”) markets, see Michael J.T. McMillen, Islamic Capital Markets: Market Developments and Conceptual Evolution in the First Thirteen Years, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1781112, at 16‐29. 6 See McMillen and Crawford, supra note 3, at 4: sukūk al‐murābaha constituted 9.2% of the total volume and 18.8% of the total offerings of all sukūk issuances in the period from inception of sukūk to August of 2008. See, also, Michael J.T. McMillen, Islamic Law Forum, 42 THE INTERNATIONAL LAWYER 1017 (2008); Government sterling sukuk issuance: a consultation (November 2007), HM Treasury, United Kingdom, Debt Management Office, especially at 6‐8; and The Sukuk Market Continues to Soar and Diversify, Held Aloft By Huge Financing Needs, Standard & Poor’s, Ratings Direct, March 11, 2008.

4

view. They have long warned against excessive use of the murābaha, and, it seems, have foreseen, with

some trepidation, the current rather cavalier use of the structure.7

Still, the use of murābaha transactions is increasing markedly, and expanding to more areas of finance,

rather than retreating as desired by the Sharīʿah scholars. Part of the reason is the unfortunate

perception that it is an easy substitute for a conventional loan arrangement, particularly in its

“commodity as vector” manifestation. Increasing use has made it apparent that practitioner awareness

of murābaha fundamentals and requisites is somewhat deficient. With the re‐emergence, and

resurgence in the use, of the murābaha, there is an attendant obligation to study this device, in its

proper context as a type of sale, in all of its complexities, nuance, purpose and elegance.

For these reasons, this paper takes up the ancient, and most modern, of structures: the murābaha.

Particular attention is devoted to issues appertaining to its use in sophisticated transactions, particularly

financing transactions (although this is a quite modern use of the structure). First, general murābaha

(and sales) principles are surveyed. A case study, involving term and revolving facilities, is posited. A

survey of the “commodity as vector” approach to murābaha financings is presented. Thereafter, the

chapter surveys representative issues that arise in financings of this type, including those pertaining to

(i) the enforceability of promises to enter into future murābaha transactions, (ii) the use of variable rate

profit elements, (iii) profit elements pertaining to commitment fees, profit participations and other

accruing obligations, (iv) waivers, forgiveness and rebates of profit elements, including in early

payments, (v) conditions precedent, (vi) collateral security arrangements, and (vii) guarantees.

Quite intentionally, this paper uses a range of conventional finance terms (such as “commitment fees”)

in discussing the murābaha, and with full cognizance of their inapplicability in the murābaha itself. The

design and intention is to enhance accessibility, conceptually and linguistically, to the many

“conventional” bankers, financiers, lawyers, accountants and advisors that have entered, and will enter,

the field of Islamic finance. Those experienced in Islamic finance will understand the necessary

conceptual transformations. Those who do not understand those transformations need a place to

begin, and that beginning must proceed from their current base of reference and understanding.

GENERAL MURABAHA PRINCIPLES

Bayʿu al‐murābaha is a sale of venerable lineage under the Sharīʿah, and is acceptable to all four of the

main orthodox Sunnī madhāhib.8 In its original conception, it is a trade‐based, “cost‐plus” sale contract

7 Taqi Usmani, Murabaha, undated paper, available at http://www.darululoomkhi.edu.pk/fiqh/islamicfinance/murabaha.html (“Usmani Murābaha”). In addition to Usmani: Murābaha, this paper draws from al‐Zuḥaylī, supra note 5, Ibn Rushd, THE DISTINGUISHED JURIST’S PRIMER, VOLUME II, BIDAYAT AL‐MUJTAHID WA NIBAYAT AL‐MUQTASID (1996) (“Ibn Rushd”), and Ali Ibn Abi Bakr Burhan al‐Din al‐Marghinani, THE HEDÀYA, OR GUIDE: A COMMENTARY ON THE MUSSULMAN LAWS: TRANSLATED BY ORDER OF THE GOVERNOR‐GENERAL AND COUNCIL OF BENGAL, BY CHARLES HAMILTON (1791) (“al‐Marghinani”), Volume 2 of 4 (1791), a reproduction from the British Library, addressing the muràbaha (designated as the “Moorâbihat”) in Book XVI (Of Sale), Chapter VII (Of Moorâbihat, and Tawleeat, that is, Sales of Profit and of Friendship), at 469‐88. See, also, Taqi Usmani, Fixed Income Securities Shari’a Perspective, 3 SBP RESEARCH BULLETIN 63 (2007), at 73‐74; DeLorenzo: Murābaha, supra note 5, bin Aqeel: Murābaha, supra note 5, Mohammad Obaidullah, ISLAMIC FINANCIAL SERVICES (2005), at 68 et seq., and Muhammad Ayub, UNDERSTANDING ISLAMIC FINANCE (2007) (“Ayub”).

5

in which the cost is ascertained and expressly disclosed. And, as originally formulated, it had nothing to

do with financing; current conceptions seem overwhelming focused on financing transactions.9

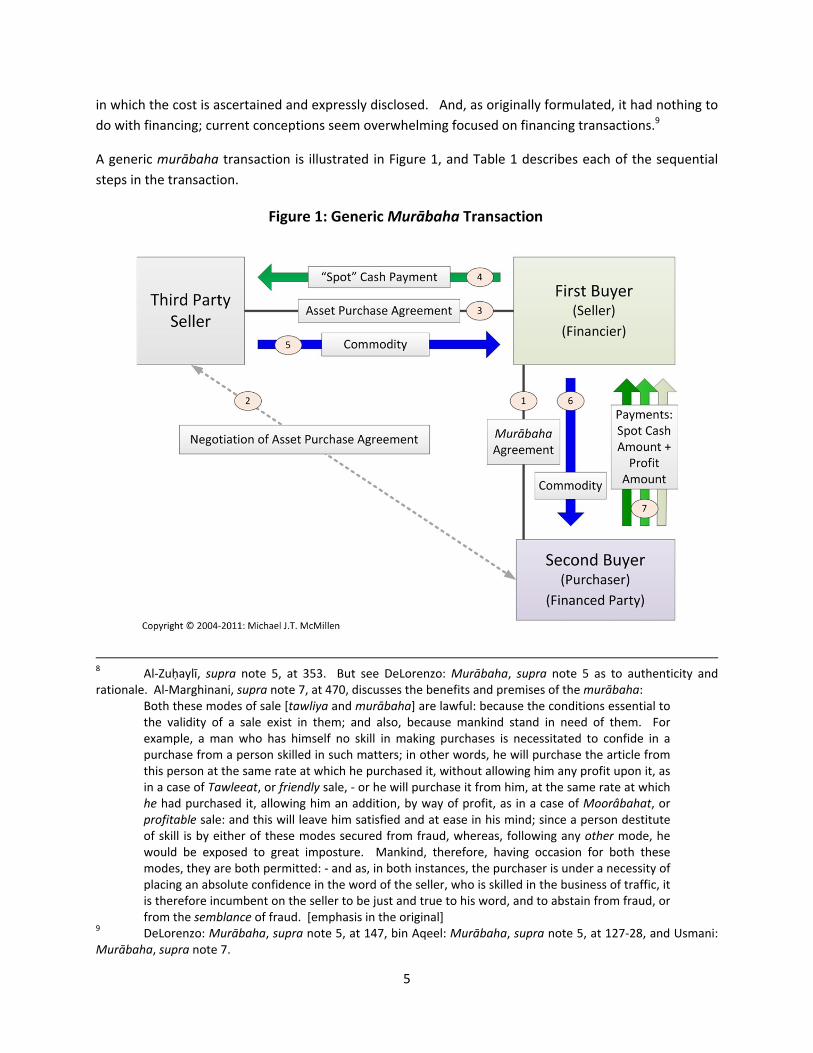

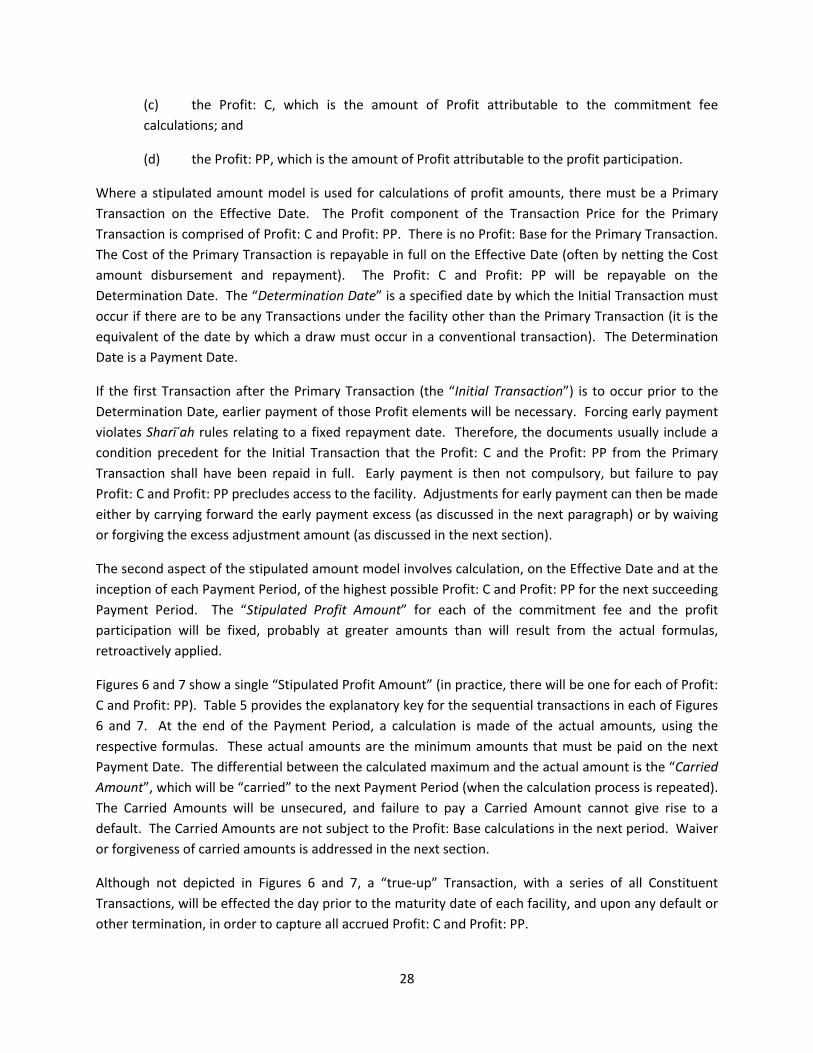

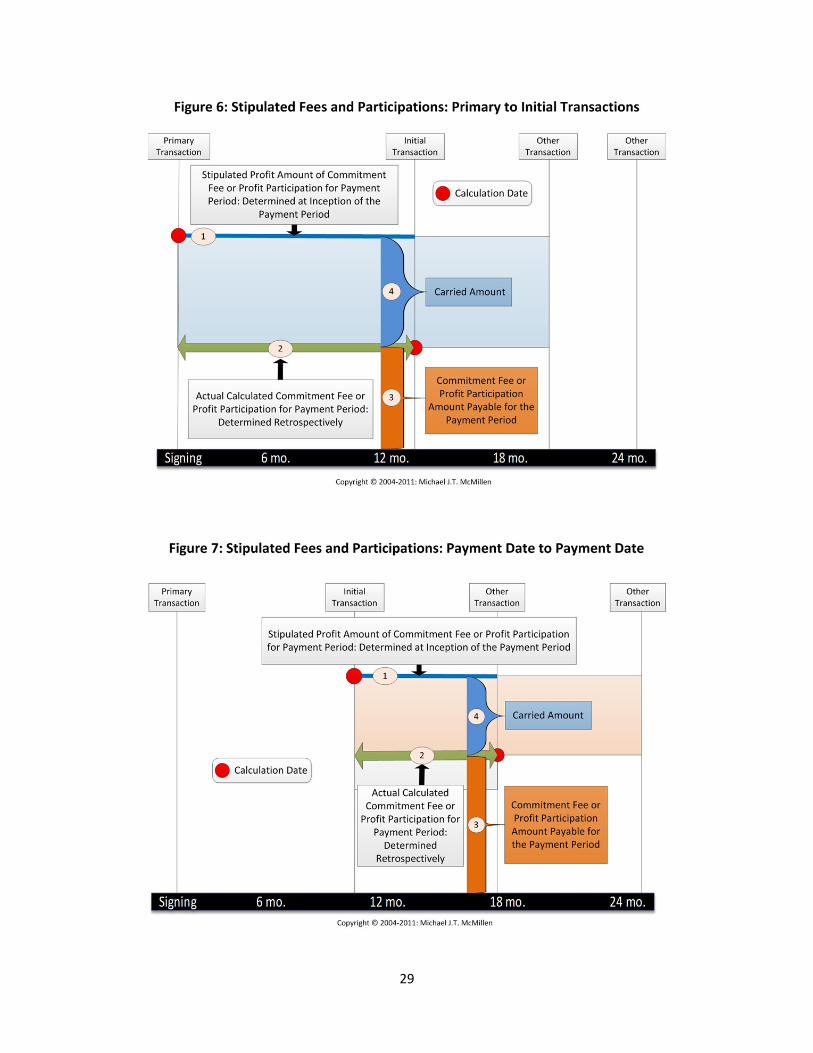

A generic murābaha transaction is illustrated in Figure 1, and Table 1 describes each of the sequential

steps in the transaction.

8 Al‐Zuḥaylī, supra note 5, at 353. But see DeLorenzo: Murābaha, supra note 5 as to authenticity and rationale. Al‐Marghinani, supra note 7, at 470, discusses the benefits and premises of the murābaha:

Both these modes of sale [tawliya and murābaha] are lawful: because the conditions essential to the validity of a sale exist in them; and also, because mankind stand in need of them. For example, a man who has himself no skill in making purchases is necessitated to confide in a purchase from a person skilled in such matters; in other words, he will purchase the article from this person at the same rate at which he purchased it, without allowing him any profit upon it, as in a case of Tawleeat, or friendly sale, ‐ or he will purchase it from him, at the same rate at which he had purchased it, allowing him an addition, by way of profit, as in a case of Moorâbahat, or profitable sale: and this will leave him satisfied and at ease in his mind; since a person destitute of skill is by either of these modes secured from fraud, whereas, following any other mode, he would be exposed to great imposture. Mankind, therefore, having occasion for both these modes, they are both permitted: ‐ and as, in both instances, the purchaser is under a necessity of placing an absolute confidence in the word of the seller, who is skilled in the business of traffic, it is therefore incumbent on the seller to be just and true to his word, and to abstain from fraud, or from the semblance of fraud. [emphasis in the original]

9 DeLorenzo: Murābaha, supra note 5, at 147, bin Aqeel: Murābaha, supra note 5, at 127‐28, and Usmani: Murābaha, supra note 7.

6

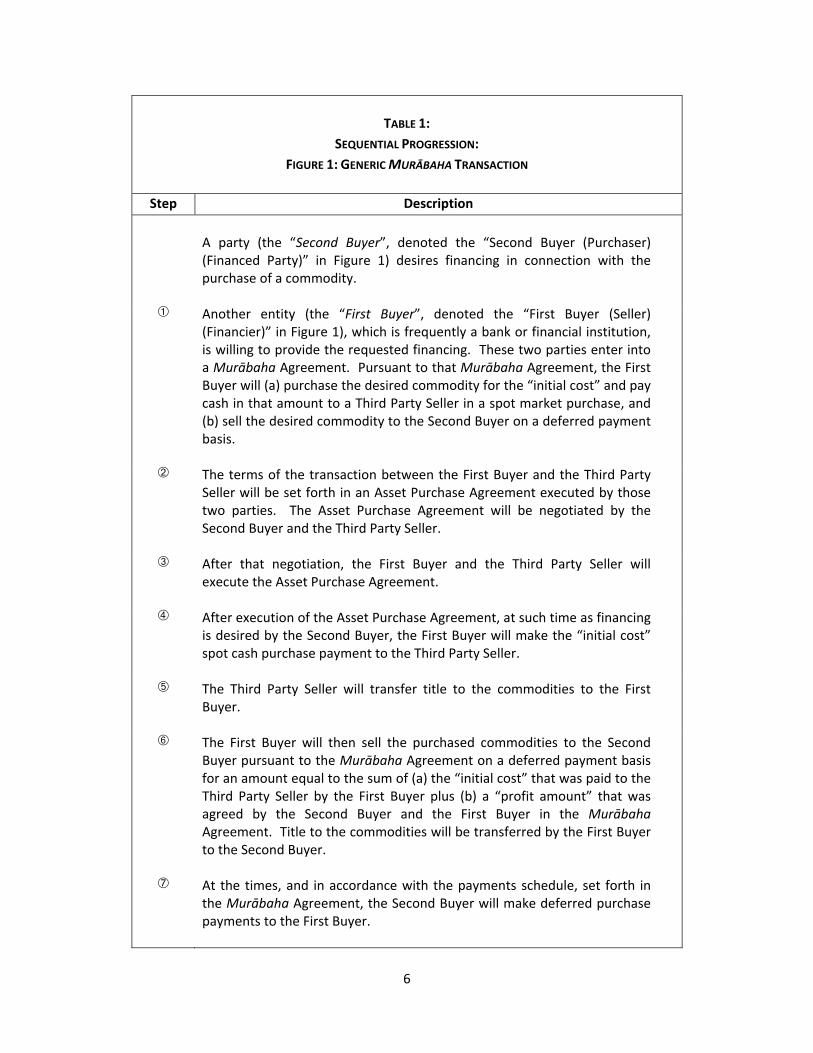

TABLE 1:

SEQUENTIAL PROGRESSION:

FIGURE 1: GENERIC MURĀBAHA TRANSACTION

Step Description

A party (the “Second Buyer”, denoted the “Second Buyer (Purchaser) (Financed Party)” in Figure 1) desires financing in connection with the purchase of a commodity.

À Another entity (the “First Buyer”, denoted the “First Buyer (Seller) (Financier)” in Figure 1), which is frequently a bank or financial institution, is willing to provide the requested financing. These two parties enter into a Murābaha Agreement. Pursuant to that Murābaha Agreement, the First Buyer will (a) purchase the desired commodity for the “initial cost” and pay cash in that amount to a Third Party Seller in a spot market purchase, and (b) sell the desired commodity to the Second Buyer on a deferred payment basis.

Á The terms of the transaction between the First Buyer and the Third Party Seller will be set forth in an Asset Purchase Agreement executed by those two parties. The Asset Purchase Agreement will be negotiated by the Second Buyer and the Third Party Seller.

After that negotiation, the First Buyer and the Third Party Seller will execute the Asset Purchase Agreement.

à After execution of the Asset Purchase Agreement, at such time as financing is desired by the Second Buyer, the First Buyer will make the “initial cost” spot cash purchase payment to the Third Party Seller.

Ä The Third Party Seller will transfer title to the commodities to the First Buyer.

Å The First Buyer will then sell the purchased commodities to the Second Buyer pursuant to the Murābaha Agreement on a deferred payment basis for an amount equal to the sum of (a) the “initial cost” that was paid to the Third Party Seller by the First Buyer plus (b) a “profit amount” that was agreed by the Second Buyer and the First Buyer in the Murābaha Agreement. Title to the commodities will be transferred by the First Buyer to the Second Buyer.

Æ At the times, and in accordance with the payments schedule, set forth in the Murābaha Agreement, the Second Buyer will make deferred purchase payments to the First Buyer.

7

At essence, (i) the “initial cost” must be disclosed to the Second Buyer (in most modern transactions, it is

also agreed by the First Buyer and the Second Buyer in the Murābaha Agreement), (b) the “profit

amount” must be disclosed to the Second Buyer (and agreed by the First Buyer and the Second Buyer),

(c) the original price must be fungible in measurement (i.e., it must be measured by weight, volume or

number of homogeneous goods), (d) when trading in goods eligible for ribā, ribā must not be effected in

relation to the original price,10 and (e) the initial contract between the First Buyer and the Third Party

Seller must be valid.11

The murābaha, in any context, is a sale, and must conform to the Sharīʿah requirements applicable to

sales.12 Therefore, it is essential to begin with some fundamental sales principles (and to consider in

greater depth the principles specific to the murābaha, as noted in the next preceding paragraph).

For the majority of fuqahāʾ, there are four cornerstones (ʾarkān) of a sale transaction (paralleling the

ʾarkān of all contracts): the seller; the buyer; the language of the contract; and the object of the

10 As a general summary of a complicated area of Sharīʿah, ribā is of two types: ribā al‐nasīʾah and ribā al‐faḍl (also referred to as ribā al‐buyūʿ). Ribā al‐nasīʾah is ribā in compensation for deferring a due debt to a new date or term (one of the two compensations in the transaction is increased because of the deferment, with no other compensation for that increase). Ribā al‐nasīʾah is forbidden in the Qurʾān and is the ribā al‐jāhiliyyah (practice of pre‐Islamic Arabia). Ribā al‐faḍl is derives from references to six goods: gold; silver; wheat; barley; salt; and dates. Ribā al‐faḍl involves an increase in the measure (weight or volume) of one of two compensations of the same genus in a sales contract not involving deferment and is applicable in transactions involving fungibles (the objects eligible for ribā). The oft‐mentioned aḥadīth pertaining to the trading of gold for gold, silver for silver, wheat for wheat, barley for barley, salt for salt and dates for dates (particularly that of ʿUbāda ibn al‐Ṣāmit) pertain to ribā al‐faḍl. Those aḥadīth provide that the foregoing sales must be in equal measure of the compensations and in immediate exchange. They further provide that these six goods may be sold in unequal measures, but must be sold “hand to hand”, without deferral of any compensation. Ribā al‐faḍl is established in the sunna. Bayʿ al‐nasāʾ (deferment sales) of two different compensations with payment of one compensation being deferred are also impermissible. See the discussions of ribā in al‐Zuḥaylī, supra note 5, at 158‐71, and Ibn Rushd, supra note 7, at 309‐52, and Justice Muhammed Taqi Usmani, The Text of the Historic Judgment on Riba, 23 December 1999, available online at http://www.albalagh.net/Islamic_economics/riba_judgement.shtml. 11 Al‐Zuḥaylī, supra note 5, at 355‐56. 12 Usmani: Murābaha and al‐Zuḥaylī, each supra note 5. The discussion of sales principles, including their elements and conditions, set forth in this paper is derived from al‐Zuḥaylī, supra note 5, at 355‐56, Ibn Rushd, supra note 7, at 153‐239, and al‐Marghinani, supra note 7, Volume 2, at 360‐550. Consider, also, Ayub, supra note 7, at 129‐52. The term bayʿ is derived from the term bāʿ, meaning ‘arm’, because one extends the arm to give or receive and/or to shake hands upon consummation of an agreement (the other Arabic language term for a sale is ṣafqa, which means, literally, ‘hand shake’).

The murābaha is one of five transactional types of sales as exchanges. The other four are: (i) bayʿu al‐musāwama (a bargaining transaction which is essentially the same as the murābaha except that the initial cost is not disclosed); (ii) bayʿu al‐tawliya (the object is resold to the second buyer for the same price as it was obtained by the first buyer/seller); (iii) bayʿu al‐ʾishrāk (the same as the bayʿu al‐tawliya, except that only part of the obtained object of sale (mabiʿ) is resold to the second buyer); and (iv) bayʿu al‐waḍīʿa (the object is sold at a known discount below the price at which it was purchased by the first buyer/seller). See al‐Zuḥaylī, supra note 5, at 353‐54, and DeLorenzo: Murābaha, supra note 5, at 146, quoting Nazih Hammad, Mu`jam al Mustalahat al Iqtisadiyah fi Lughat al Fuqaha (1995), at 351, and al‐Zuḥaylī, supra note 5, at 353.

8

contract. For the Ḥanafīs, the primary cornerstone (rukn) of a sale transaction is offer and acceptance,

which may be considered in terms of the language (ṣīgha) of the offer and acceptance and the nature

(ṣifa) of the offer and acceptance. The language of the offer and acceptance relates to the consent of

each of the seller and the purchaser. The nature of the offer and acceptance relates to the expression of

each of the offer and the acceptance and the ability of the parties to withdraw either the offer or the

acceptance in circumstances where the other of the two has not been expressed (which is agreed upon)

and where the offer and acceptance have each been expressed but the ‘session’ has not been

terminated (the ‘option of withdrawal before parting’ or khiyār al‐majlis).13

In addition, there are conditions pertaining to sales generally, and to the individual type of sale (here, a

murābaha), that must be satisfied for the sales transaction to be valid.14 Generally stated, there are four

types of conditions that a sale contract must be satisfied: (a) conditions of conclusion; (b) conditions of

validity; (c) conditions of execution; and (d) bindingness conditions.

The conditions of conclusion relate to the mental, physical and transactional capabilities of the

contracting parties (the “eligibility” (al‐rushd) of the parties in the Shāfiʿī construct), audibility and

understanding of the offer and acceptance, the correspondence of offer and acceptance, the making of

the offer and acceptance during the same session, and certain states relating to the object of the sale

(mabiʿ).

Each of the mabiʿ and the price must be in existence, with certainty, at the time of the contract and,

absent certain destruction scenarios, at the time of the sale. The foregoing statement is subject to

certain limited exceptions and to variations from one madhhab to another.15 The object of the sale

(mabiʿ) and the price paid for the object of the sale are distinct, and are treated differently under the

Sharīʿah. Al‐Zuḥaylī discusses the differential treatment as follows (the summary does not convey a full

appreciation for detail or nuance that is critical in transactional application):16

1. A condition for conclusion of sale is that the object of sale be a valued good with legitimate

uses. This condition does not apply to the price.

2. A condition for the executability of a sale is that the object of sale be in the possession of

the seller. The same condition does not apply to the price.

3. It is not valid to defer the delivery of the price in forward sales, while the deferment of the

object of sale is necessary.

13 See, for example, the discussion at al‐Zuḥaylī, supra note 5, at 10‐12. 14 The description provided in this paper is taken from, primarily, Al‐Zuḥaylī, supra note 5, at 32‐49. The organizational format of the discussion (i.e., the groups of conditions) is based upon the Ḥanafī position. The conditions of each of the four orthodox Sunni madhāhib are set forth in Al‐Zuḥaylī, at 36‐49. The Ḥanafīs prscribe twenty‐three conditions, the Shāfiʿīs prescribe twenty‐two conditions, and the Ḥanbalīs and the Mālikīs each prescribe eleven conditions. 15 See al‐Zuḥaylī, supra note 5, at 74‐76, with respect to objects not in existence and the Ḥanbalī opinion permitting the sale of items that do not exist at the time of the contract if there future existence is known according to custom, as discussed at 76. 16 See, Al‐Zuḥaylī, supra note 1, at 56‐57.

9

4. The cost of delivery of the price is borne by the buyer, and the cost of delivery of the object

is borne by the seller.

5. A sale without naming the price is defective and invalid (fāsid); whereas not naming the

object of sale, as in saying “I sold you for ten coins”, voids the contract that is thus not

concluded.

6. If the object of sale perishes after the exchange of object and price, the sale may not be

reversed. However, the perishing of the price after the exchange does not prevent the sale

from being reversed.

7. If the object of sale perishes prior to delivery, the sale is void. However, if the price perishes

prior to delivery, the sale is not void.

8. The buyer may not re‐sell movable merchandise before receiving it, whereas the seller may

use or sell the price before he receives it.

9. The buyer must deliver the price before he has a right to receive the object of sale, unless

the seller accepts otherwise.

Agreements relating to objects not yet in existence (an unborn calf, a future harvest, an

unmanufactured good) are not valid murābaha transactions.17 The mabiʿ must be an object that can be

commonly used to benefit people, a principle that, historically, has excluded the validity to sales

pertaining to dead animals (mayta) or an insignificant amount of goods (such as one grain of wheat).18

The mabiʿ must be known and clearly specified to the parties in a manner that allows its precise

identification. Of course, the mabiʿ may not be a haram object (alcohol, pork, impermissible financial

instruments, and the like). To be saleable and the subject of a valid sale contract, the mabiʿ must be an

object from which it is legal to derive a benefit. The mabiʿ must have determinable value at the time of

sale.

The mabiʿ must be privately owned by the seller at the time of the sale. A sale of a horse that is owned

by a third party is not valid, however likely it is that the third party will sell the horse to the initial buyer

so as to allow the sale to the second buyer. The sale of non‐owned public goods, uncontained water,

wildlife, sun light, air and similar items is not permitted. The sale of wine, pork or blood is

impermissible. Similarly, the price must be an existing privately owned item, and may not be wine, pork

or blood. The mabiʿ must be deliverable at the time of the making of the sales contract, even if the

mabiʿ is owned by the seller at that time (e.g., a bird owned by the seller that has flown or a camel that

has wandered away). If the mabiʿ were to reappear after the contract, the offer and acceptance would

need to be renewed.

17 In some circumstances, they may be the subject of other sales arrangements, such as an ʾistiṣnāʿ or bayʿ al‐salam. Additionally, as referenced in note 15, supra, the Ḥanbalīs permit certain sales of items not yet in existence. 18 Sales of debts are not discussed in this paper. For discussions of sales of debts, see al‐Zuḥaylī, supra note 5, at 78‐82.

10

The object must be in the actual or constructive possession of the seller (the initial buyer) at the time of

the sale. Constructive possession here means that the seller has assumed all liabilities and obligations of

ownership and possession, including in respect of destruction or “perishing”, even though the seller has

not taken physical delivery of the object. The mabiʿ must be deliverable at the conclusion of the sale.

Delivery of the object must be certain and not contingent or dependent upon conditions, events or

circumstances.

The sale must be immediate and not contingent on future conditions, events or circumstances. If not

immediate, or if contingent, it is void as a present sale and will have to be renewed and reaffirmed at

the specified future date or upon the occurrence of the contingency. Certain “customary trade usage”

conditions are permissible (e.g., the validity of a warranty), and these should be determined with the

advising Sharīʿah scholar.

There are six categories of conditions of validity relating to sales contracts generally. They relate to: (i)

ignorance or uncertainty (al‐jahāla); (ii) coercion; (iii) timing; (iv) deception and gharar (gharar al‐waṣf);

(v) harmful sales (al‐ḍarar); and (vi) corruption (al‐shurūṭ al‐mufsida).

Impermissible ignorance or uncertainty may be ignorance of the purchaser as to the mabiʿ, including in

respect of its genus, its type or its quantity. It may also exist as ignorance as to the price. The price

must be known, certain and specified. In a murābaha, the price is a function of two fully‐disclosed and

mutually agreed elements: the initial cost (also referred to as the “capital” or the “principal”)19 and the

profit. The price, including both the cost and the profit, must be determinable and fixed with certainty.

The price, once fixed, may not be increased or decreased, even if payment is made earlier or later than

the agreed payment date, including in default and early payment scenarios. Ignorance may also exist as

to the relevant time periods for the transaction. Time periods with respect to deferred prices or

conditional options (khiyār al‐sharṭ) must be known. If the price and the mabiʿ are both fungible, the

price may be deferred to a future known date. The price may not be deferred if the mabiʿ is non‐

fungible. The final area of impermissible ignorance is ignorance of the means of documentation. As an

example, this type of ignorance would exist where a condition is established that a third party guarantor

must be obtained and that third party guarantor is not specified.

Coercion that renders the sale invalid or suspended includes situations in which the seller or the

purchaser is forced to take action because of threats of death, physical harm, incarceration, beating or

other injustice. Certain types of coercion may not invalidate the sales contract, such as judicially

imposed sales.20 With respect to timing considerations, a sale must be complete and cannot be limited

to a period of time or by an expiration period. Deception as to elements of the sale transaction,

including the mabiʿ, will invalidate a sale arrangement. Similarly, uncertainty regarding the existence of

the mabiʿ (gharar al‐wujūd) will also invalidate a sale (as a result of the prohibition on selling what may

19 Note the situation discussed by al‐Zuḥaylī, supra note 5, at 358‐59, in which the initial buyer acquires at a price below actual value and then lists the actual value as a catalogue price. Disclosure of the actual below‐value acquisition cost need not be disclosed if the second buyer understands that catalogue prices do not necessarily reflect actual acquisition costs. 20 See, for example, al‐Zuḥaylī, supra note 5, at 42, discussing the Shāfiʿī conception of rightful coercion.

11

or may not exist (bayʿ al‐gharar). A sale that causes the seller losses that exceed what he, she or it is

selling also invalidates a sale. However, if the seller completes the delivery of the mabiʿ in such a

circumstance, the sale is valid. Finally, corrupting conditions that invalidate a contract are those that

benefit to a party to a sales contract and have not been specified in law as acceptable, accepted in

custom or convention, required by contract or are suitable for the transaction.21

The murābaha is a trust sale (bayʿ al‐amānah) or a fiduciary sale. Disclosure begins with the initial costs

(but, as discussed in this section, extends beyond initial cost to all essential transactional elements).

Disclosure to the second buyer of the cost to the first buyer/seller entails consideration of what

constitutes the “cost” (initial cost) to the first buyer, and thus what must be disclosed. This

determination is important in ascertaining what is entitled to earn a profit.22 Certain normal costs

associated with the object of sale (mabiʿ) which result in an increase in the value of the mabiʿ or are

“effective in the essence”23 of the mabiʿ (such as tailoring or dyeing), may be appended to the capital or

principal as “cost” for purposes of determining the cost for purposes of the murābaha transaction.

Disclosure of the initial cost must include disclosure of any financing and deferred payment

arrangements pertaining to the object or its initial purchase.24 If the object of the sale suffers damage

or defect while in the possession or under the control of the first buyer (seller) or a third party, the

damage or defect must be disclosed to the second buyer.25 If the mabiʿ is increased whilst in the

possession or control of the first buyer (seller), such as by giving birth, creating milk, bearing fruit or

growing wool), the murābaha sale may proceed, but only after disclosure of the increase.26 If the mabiʿ

was purchased by the first buyer (seller) in exchange for a debt owed by the initial third party seller to

21 Al‐Zuḥaylī, supra note 5, at 35, provides the following examples of corrupting conditions: the seller sells a care with a condition that the seller can use the car for a period of a month subsequent to the sale; the seller sells a house with the condition that the seller can reside in the house for some period subsequent to the sale; and the purchaser stipulates in the contract of sale that the seller must lend the purchaser some amount of money. 22 Particularly to the Mālikis: see Ibn Rushd, supra note 7, at 256‐57, noting that there are three categories: (i) that which is permissibly appended to the cost and also has a right to earn a profit; (ii) that which is appended to the cost but may not earn a profit; and (iii) that which may not be appended to the cost and may not earn a profit. The second category includes expenditures for activities that do not affect the essence of the mabiʿ (object of sale) and which the first buyer/seller is not capable of performing (such as transportation of the mabiʿ and renting of stores in which that mabiʿ is subsequently sold). The third category includes items and activities not within the first two categories (i.e., they do not affect the essence of the mabiʿ and the first buyer/seller is unable to undertake the activity, such as brokerage fees, fees and costs of negotiation and bargaining, and doctor’s or veterinarian’s fees). The Ḥanafīs tend to include in the capital or principal a much broader range of costs associated with the purchase and sale of the mabiʿ (essentially all such costs). 23 Ibn Rushd, supra note 7, at 256. See al‐Maghinani, supra note 7, at 471‐72, which avers, at 472, that “whatever is the cause of an increase either to the substance of the thing purchased, or to the value of it, is an addition to the capital … .” [emphasis in the original] 24 Al‐Zuḥaylī, supra note 5, at 358. 25 Al‐Zuḥaylī, supra note 5, at 358. Note the differences of opinion as to whether disclosure must be made to the second buyer where the mabiʿ is damaged as a result of ‘natural causes’: al‐Zuḥaylī, at 357‐58, and al‐Marghinani, supra note 7, at 478. 26 Al‐Zuḥaylī, supra note 5, at 358. Note the discussion of the Ḥanafī position that the increase is saleable and does not decrease the agreed price. And note that no disclosure of the increase is necessary if the object of the sale is land used for agriculture.

12

the first buyer, that information need not be disclosed to the second buyer.27 However, if the mabiʿ was

accepted as compensation for an unpaid loan, then it may not be sold in a murābaha to the second

buyer at a cost (capital or principal) equal to the amount of the unpaid loan (this is a debt forgiveness

arrangement rather than a negotiated sale).28 If a mabiʿ is purchased by the first buyer (seller) at an

amount below its value, and is then listed in a catalogue at an amount equal to its higher value, the first

buyer need not disclose the actual initial amount paid. This principle is subject to a number of

qualifications, such as the first buyer not misrepresenting that he, she or it paid an amount equal to the

higher value and the second buyer being aware that the catalogue price may not equal the amount

actually paid by the first buyer (seller).29 And, if the first buyer (seller) acquired the mabiʿ as a gift or as

an inheritance and thereafter sells to the second buyer at a fairly estimated value plus permissible

profit, the gift or inheritance need not be disclosed to the second buyer.30

Inability to determine the initial price, or unwillingness to fully disclose that price, voids the sale as a

murābaha.31 The profit may be a lump sum or a percentage.32 It may be higher if the date of payment is

more distant: consideration of time in establishing price is permissible. The price need not reflect the

current, or any future, market price. It may be different for cash and credit transactions, reflecting

different risk assessments relating to each. One of the options must be chosen at inception, and the

price then fixed. Different prices for different maturities or payment dates, leaving an option to the

second purchaser as to election of payment date, are impermissible. In deferred payment transactions

(bayʿ muj’ajjal), including most murābaha financing transactions, additional rules apply. The due date

for payment must also be unambiguously fixed and determinable at inception. It is acceptable to make

reference to a specific date or a specific period. But the date may not be fixed by reference to an

unknown or uncertain event. References to payment periods commence from the date of delivery of the

object, unless otherwise specified.

Many, if not most, Sharīʿah scholars allow for late payment and default payment charges of some type.

These are of two types: actual fees, costs and expenses (actual damages) incurred by the seller in

connection with the late payment or default, which may be retained by the seller; and penalty charges,

which may not be retained by the seller, but must be donated to charity. The latter, where permitted,33

are allowed as incentives for timely payment by the second buyer. Acceleration of the entire purchase

price upon a default is generally permissible. Collateral security for the payment and performance

obligations is acceptable.

27 Al‐Zuḥaylī, supra note 5, at 358. 28 Al‐Zuḥaylī, supra note 5, at 358. 29 Al‐Zuḥaylī, supra note 5, at 358. 30 Al‐Zuḥaylī, supra note 5, at 358. 31 See al‐Zuḥaylī, supra note 5, at 359‐60, Ibn Rushd, supra note 7, at 258‐59, and al‐Marghinani, supra note 7, at 472‐80, in connection with the various options available to the second buyer in cases of betrayal of trust, including non‐disclosure or inaccurate disclosure of price and quality characteristics. 32 Al‐Zuḥaylī, supra note 5, at 353. 33 Consider, for example, bin Aqeel: Murābaha, supra note 5, at 128 (clause “Fourth”), where the position is stated without consideration of the incentive and purification concepts.

13

Certain expenses, even though not precisely determinable at inception, may be added to the total

murābaha price. Permissible expenses are non‐recurring expenses incurred by the first buyer in

effecting the transaction: e.g, freight and transportation charges, customs duties, sales intermediation

fees, costs and expenses, feeding costs, and other normal and customary transactional costs. Recurring

business costs and expenses of the seller are not permissible additions to the sale price: e.g., employee

salaries, premises rent, normal storage and warehousing, veterinarian's costs, and the fees of herdsmen.

Consultation with the advising Sharīʿah scholar is advisable in connection with determinations as to

expenses which may be included.

For a sale to be binding on both parties, there must not exist any options that allow one of the parties to

void the contract. Examples of such options include options by condition (khiyār al‐sharṭ), description

(waṣf), price payment (naqd), identification (taʿyīn), inspection (ruʾya), defect (ʿayb) and deception

(ghubn maʿa al‐taghrīr).

Delivery and receipt of each of the mabiʿ and the price are critical elements of a valid sale.34 Receipt,

and thus possession, by the purchaser may be established in various different ways.35 If the purchaser is

provided full access and permission (al‐takhliya) to the mabiʿ and in respect of its use by the seller,

delivery and receipt will have occurred. Delivery and receipt will also have occurred if the purchaser

shall have damaged the mabiʿ while it is in the possession of the seller, as the precondition to such

infliction of damage is the ability to affect the mabiʿ and the related implication of access and

permission. Similarly, delivery and receipt are concluded if the mabiʿ suffers spoilage or a defect caused

by the purchaser while the mabiʿ is in the possession of the seller. Should the purchaser, or a third party

at the suggestion or direction of a purchaser, take possession of the mabiʿ for safekeeping or as a loan

during the pendency of the sale contract, delivery and receipt will be presumed.36 There are differences

of opinion among Sharīʿah scholars as to whether delivery and receipt have been concluded in

34 In most cases, absent deferral or other consensual arrangements, delivery of the mabiʿ and the price must be concurrent, except in the case of an exchange of non‐fungibles for fungibles. However, there are variations among the madhāhib, and variations in respect of specific exchanges. Consider, for example, al‐Zuḥaylī, supra note 5, at 62‐66. 35 See al‐Zuḥaylī, supra note 5, at 66‐70. The circumstances discussed in the text relate to the situation in which the seller is in possession of the mabiʿ. There may be circumstances in which the purchaser is in possession of the mabiʿ as a result of a receipt that antedates the sale arrangements. In those circumstances, it will be necessary to determine whether (a) the prior receipt gave rise to a responsibility of the possessor (subsequent purchaser) to another person or entity in respect of the objects received (qabḍ al‐ḍamān), as in usurpation, or (b) the recipient pursuant to the prior receipt is responsible for the objects received only if they are lost, damaged or destroyed as a result of the negligence of the possessor in safekeeping the objects (i.e., a qabḍ al‐ʾamāna), as in deposit, loan and rental arrangements. In the first case (qabḍ al‐ḍamān), (i) delivery and receipt will have been concluded if the purchaser has possession of the mabiʿ, and (ii) delivery and receipt will need to be further concluded if the mabiʿ is in the possession of another party (e.g., the seller is a pawn broker). In the second case (a qabḍ al‐ʾamāna), delivery and receipt will need to be further concluded. 36 It is necessary to carefully distinguish agreed ‘trustee’ and rahn arrangements in transactions where those elements are present.

14

circumstances where the purchaser prosecutes a third party for damages or compensation caused by

transgressions or acts or omissions of that third party.37

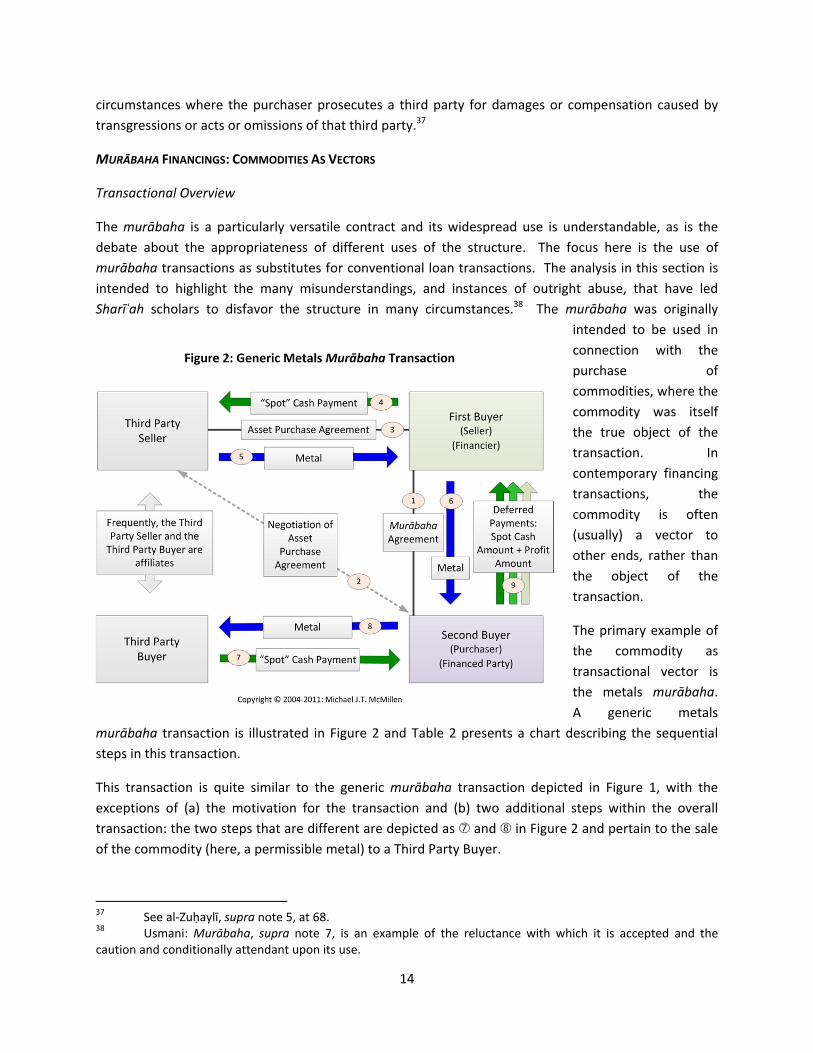

MURĀBAHA FINANCINGS: COMMODITIES AS VECTORS

Transactional Overview

The murābaha is a particularly versatile contract and its widespread use is understandable, as is the

debate about the appropriateness of different uses of the structure. The focus here is the use of

murābaha transactions as substitutes for conventional loan transactions. The analysis in this section is

intended to highlight the many misunderstandings, and instances of outright abuse, that have led

Sharīʿah scholars to disfavor the structure in many circumstances.38 The murābaha was originally

intended to be used in

connection with the

purchase of

commodities, where the

commodity was itself

the true object of the

transaction. In

contemporary financing

transactions, the

commodity is often

(usually) a vector to

other ends, rather than

the object of the

transaction.

The primary example of

the commodity as

transactional vector is

the metals murābaha.

A generic metals

murābaha transaction is illustrated in Figure 2 and Table 2 presents a chart describing the sequential

steps in this transaction.

This transaction is quite similar to the generic murābaha transaction depicted in Figure 1, with the

exceptions of (a) the motivation for the transaction and (b) two additional steps within the overall

transaction: the two steps that are different are depicted as Æ and Ç in Figure 2 and pertain to the sale

of the commodity (here, a permissible metal) to a Third Party Buyer.

37 See al‐Zuḥaylī, supra note 5, at 68. 38 Usmani: Murābaha, supra note 7, is an example of the reluctance with which it is accepted and the caution and conditionally attendant upon its use.

15

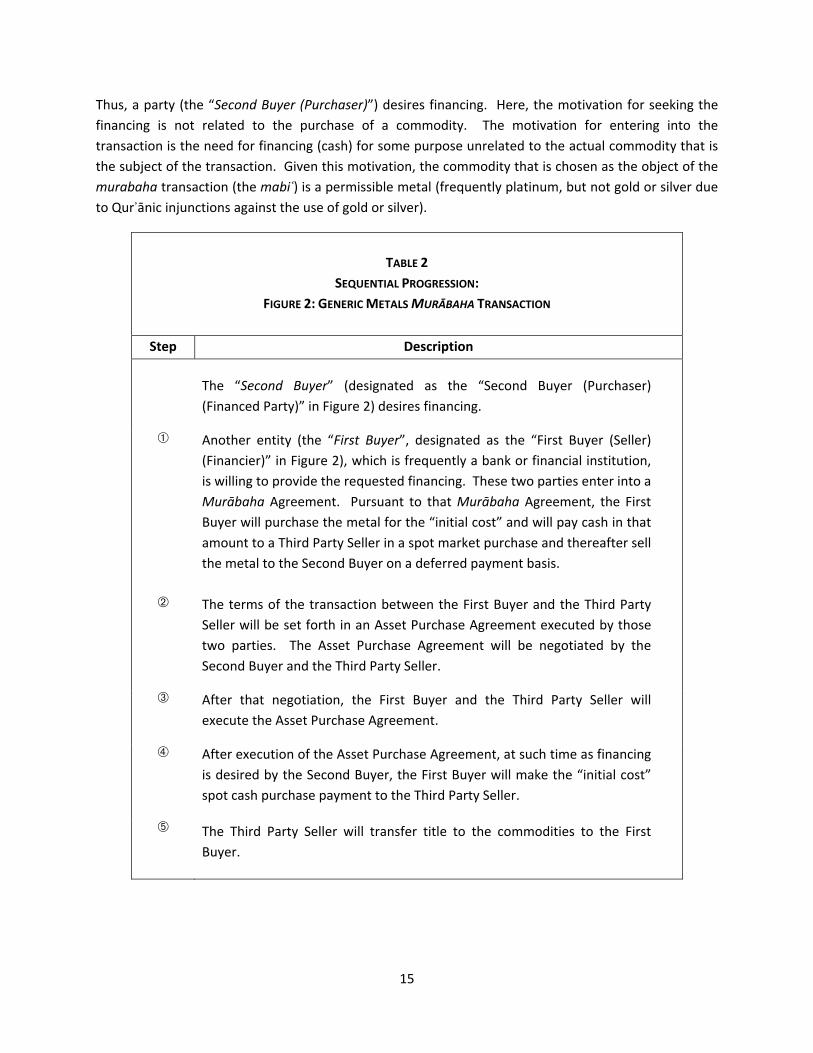

Thus, a party (the “Second Buyer (Purchaser)”) desires financing. Here, the motivation for seeking the

financing is not related to the purchase of a commodity. The motivation for entering into the

transaction is the need for financing (cash) for some purpose unrelated to the actual commodity that is

the subject of the transaction. Given this motivation, the commodity that is chosen as the object of the

murabaha transaction (the mabiʿ) is a permissible metal (frequently platinum, but not gold or silver due

to Qurʾānic injunctions against the use of gold or silver).

TABLE 2

SEQUENTIAL PROGRESSION:

FIGURE 2: GENERIC METALS MURĀBAHA TRANSACTION

Step Description

The “Second Buyer” (designated as the “Second Buyer (Purchaser)

(Financed Party)” in Figure 2) desires financing.

À Another entity (the “First Buyer”, designated as the “First Buyer (Seller)

(Financier)” in Figure 2), which is frequently a bank or financial institution,

is willing to provide the requested financing. These two parties enter into a

Murābaha Agreement. Pursuant to that Murābaha Agreement, the First

Buyer will purchase the metal for the “initial cost” and will pay cash in that

amount to a Third Party Seller in a spot market purchase and thereafter sell

the metal to the Second Buyer on a deferred payment basis.

Á The terms of the transaction between the First Buyer and the Third Party

Seller will be set forth in an Asset Purchase Agreement executed by those

two parties. The Asset Purchase Agreement will be negotiated by the

Second Buyer and the Third Party Seller.

After that negotiation, the First Buyer and the Third Party Seller will

execute the Asset Purchase Agreement.

à After execution of the Asset Purchase Agreement, at such time as financing

is desired by the Second Buyer, the First Buyer will make the “initial cost”

spot cash purchase payment to the Third Party Seller.

Ä The Third Party Seller will transfer title to the commodities to the First

Buyer.

16

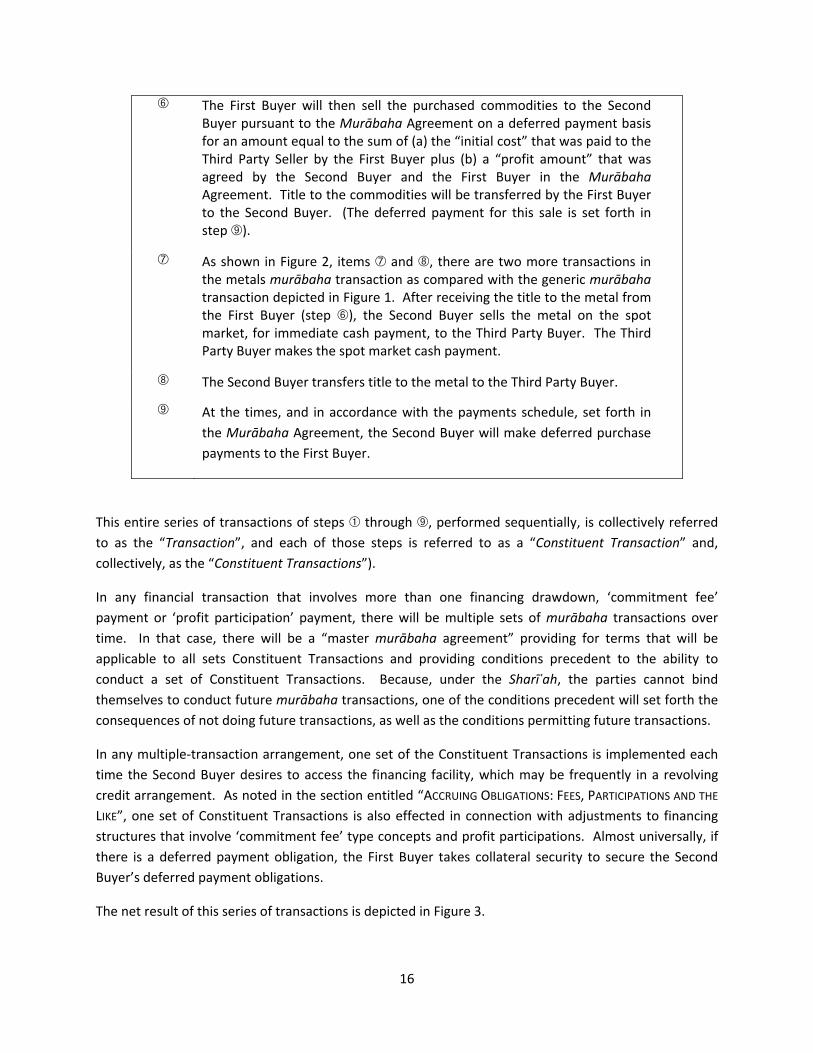

Å The First Buyer will then sell the purchased commodities to the Second Buyer pursuant to the Murābaha Agreement on a deferred payment basis for an amount equal to the sum of (a) the “initial cost” that was paid to the Third Party Seller by the First Buyer plus (b) a “profit amount” that was agreed by the Second Buyer and the First Buyer in the Murābaha Agreement. Title to the commodities will be transferred by the First Buyer to the Second Buyer. (The deferred payment for this sale is set forth in step È).

Æ As shown in Figure 2, items Æ and Ç, there are two more transactions in the metals murābaha transaction as compared with the generic murābaha transaction depicted in Figure 1. After receiving the title to the metal from the First Buyer (step Å), the Second Buyer sells the metal on the spot market, for immediate cash payment, to the Third Party Buyer. The Third Party Buyer makes the spot market cash payment.

Ç The Second Buyer transfers title to the metal to the Third Party Buyer.

È At the times, and in accordance with the payments schedule, set forth in

the Murābaha Agreement, the Second Buyer will make deferred purchase

payments to the First Buyer.

This entire series of transactions of steps À through È, performed sequentially, is collectively referred

to as the “Transaction”, and each of those steps is referred to as a “Constituent Transaction” and,

collectively, as the “Constituent Transactions”).

In any financial transaction that involves more than one financing drawdown, ‘commitment fee’

payment or ‘profit participation’ payment, there will be multiple sets of murābaha transactions over

time. In that case, there will be a “master murābaha agreement” providing for terms that will be

applicable to all sets Constituent Transactions and providing conditions precedent to the ability to

conduct a set of Constituent Transactions. Because, under the Sharīʿah, the parties cannot bind

themselves to conduct future murābaha transactions, one of the conditions precedent will set forth the

consequences of not doing future transactions, as well as the conditions permitting future transactions.

In any multiple‐transaction arrangement, one set of the Constituent Transactions is implemented each

time the Second Buyer desires to access the financing facility, which may be frequently in a revolving

credit arrangement. As noted in the section entitled “ACCRUING OBLIGATIONS: FEES, PARTICIPATIONS AND THE

LIKE”, one set of Constituent Transactions is also effected in connection with adjustments to financing

structures that involve ‘commitment fee’ type concepts and profit participations. Almost universally, if

there is a deferred payment obligation, the First Buyer takes collateral security to secure the Second

Buyer’s deferred payment obligations.

The net result of this series of transactions is depicted in Figure 3.

17

There was an immediate spot market cash

payment from the First Buyer to the Third

Party Seller in the amount of the “initial cost”.

There was an immediate spot market cash

payment from the Third Party Buyer to the

Second Buyer in the amount of the “initial

cost”. And the Second Buyer has a deferred

payment obligation to the First Buyer.

The net result is that the First Buyer (the

financier) has made a cash payment equal in

amount to the “initial cost” and the Second

Buyer (the entity needing financing) has

received a cash equal in amount to the “initial

cost”. Assume for the moment that the Third

Party Seller and the Third Party Buyer are

affiliates (as is usually the case). The affiliated group containing the Third Party Seller and the Third

Party Buyer is net zero (although it will have received two fees, one for participating in the sale of the

metal and one for participating in the purchase of the metal).

As with the generic murābaha illustrated in Figure 1, in the generic metals murābaha depicted in Figure

2, at essence, (i) the “initial cost” must be disclosed to the Second Buyer (again, in contemporary

transactions it is usually agreed as between the First Buyer and the Second Buyer), (b) the “profit

amount” must be disclosed to the Second Buyer (and agreed by the First Buyer and the Second Buyer),

(c) the original price must be fungible in measurement (i.e., it must be measured by weight, volume or

number of homogeneous goods), (d) when trading in goods eligible for ribā, ribā must not be effected in

relation to the original price, and (e) the initial contract between the First Buyer and the Third Party

Seller must be valid.

In this transaction, the Sharīʿah formalities and requisites pertaining to sales and to murābaha

transactions are observed in every particular. However, none of the parties has any substantive interest

in the commodity – the metal – that is sold and purchased in the transaction. The commodity is a vector

to facilitate the provision of financing from the First Buyer (the financier) to the Second Buyer (the party

needing financing). Compliance is technical, rather than substantive.

Why was a compliant metal chosen as the substrate commodity for this transaction? (Gold and silver,

and certain other commodities, cannot be used due to Qurʾānic prohibitions.)

There are numerous answers to that question, most of which fall under a more general response: A

compliant metal was chosen as the substrate commodity for the overall murābaha transaction because

the use of permissible metals allows satisfaction of virtually all of the Sharīʿah requisites in an efficient,

standardized, low‐cost series of transactions (including the murābaha) that takes only hours (if not

minutes) to consummate while simultaneously eliminating most, if not all, of the transactional risks for

18

the party providing the financing to the party in need of financing and the other facilitating parties

(including the third party providers and purchasers of the metal substrate).

It is worthwhile to parse that answer in some detail.

Consider, first, some matters pertaining to the third party transaction participants. The transaction is

arranged through metals dealers on international metals exchanges (such as the London metals

exchange) that have considerable familiarity with the overall series of transactions (including the

murābaha and the related purchase of the metal from the Third Party Seller and the sale of the metal to

the Third Party Buyer). The Third Party Seller and the Third Party Buyer may be affiliates, allowing for

especially close integration and cooperation. This degree of cooperation and integration eliminates

many risks in the transaction. For example, the documentation pertaining to the purchase and sale of

the metal will be harmonious, leaving no risk gaps to be covered by the party needing financing (the

Second Buyer). If the purchase and sale were with totally independent third parties, the Second Buyer

would have considerably greater risk exposure. Further, the purchase and sale prices with affiliated

companies can be established to be equal, in each case, to the “initial cost”. The possibilities of market

movements in the metal price between its purchase from the Third Party Seller and its sale to the Third

Party Buyer can be controlled (and usually eliminated). Thus, the “profit amount” payable to the

financier (the First Buyer) and the small fees payable to the Third Party Seller and the Third Party Buyer

become the only financing costs: they are fixed and certain.

In recent years, in response to the widespread use of these types of metals murābaha transactions,

companies have been formed that arrange for the entire series of transactions under discussion.39

These companies also provide all necessary documentation for the entire series of transactions. The

author has made use of some of these companies for large, complicated financings, with excellent

results. One such company, located in the Middle East, has computerized the entire process in a

manner that allows the party in need of financing, with certain integrated computerized approvals from

the party providing the financing, to control the entire series of transactions. Further, that company has

been highly receptive to accommodating the standardized documentation to the specific requirements

of complex multi‐country financings that make use of multiple murābaha transactions to effect both

revolving and long‐term multiple draw credit facilities. In one such transaction, which has both a

revolving credit facility and a long‐term credit facility, each such facility being drawn and repaid and

redrawn and repaid from time to time, dozens of murābaha transactions have been effected entirely

through the computerized system, with each transaction taking only an hour or less (approximately).

39 At least one of the companies referred to in the next preceding paragraph also has the capability to arrange for these transactions to use a commodity other than a permissible metal. The company asserts that the transactions can be arranged, using a non‐metal commodity, in such a manner as to eliminate the risk of market movements in the price of the commodity between the purchase from the Third Party Seller and the Third Party Buyer and other transactional risks (such as shipping, storage and the like). The transactions upon which the author has worked with this company all involved a permissible metal and the author does not have personal experience with other commodities in this specific type of transaction. The author has no reason to doubt the assertions of the company; they have performed in accordance with their assertions in all other related matters in metals murābaha transactions.

19

Another reason that permissible metals were chosen as the substrate commodity for these metals

murābaha transactions is the standardized nature of metals that are traded, the fungible nature of the

metals, the presence of expansive and highly developed markets for the purchase and sale of these

metals, and the existence of multiple third party sellers and purchasers

Use of permissible metals as the transactional substrate also has a number of benefits in respect of

Sharīʿah compliance. Physically, metals are customarily held, quite safely, in a cage or other confine

within a vault. Ownership is evidenced by a computer entry (the equivalent of a nameplate on the front

of a cage within a vault, if you will). Transfer of ownership is accomplished by changing the nameplate

ownership designation (accompanied, of course, by appropriate documentation); that is, changing the

name of the owner in the computerized record. There is no physical movement of the metal upon a sale

and transfer of the metal. There is actual possession by the owner, albeit through the offices of the

agent‐custodian that holds the metal in its vault. The grade and purity of the metal is maintained in

accordance with strict industry standards that are internationally recognized. Standardization pervades

the metals trading industry.

All of the foregoing is quite convenient from the vantage of Sharīʿah compliance. In fact, it is difficult to

see how the metals murābaha transaction can fail to comply with the many of the relevant Sharīʿah

principles. The foregoing also allows for the murābaha transaction to be completed on a highly

expedited basis. Thus, for example, the transfer of the metal entails no movement of the metal and is

accomplished by changing the name of the owner in a computer file. Sharīʿah issues pertaining to

ownership and effectiveness of the sale and purchase are effectively eliminated. Delivery and receipt

issues under the Sharīʿah are eliminated. In reality, there are no transportation or handling risks or

costs, no risks of loss or damage, in connection with the sale and purchase transaction. Metals do not

spoil. There are essentially no variances in quality or grade of the metal, which eliminates numerous

concerns regarding inspection of the commodity by the buyer. The transactional documentation is

easily drafted so as to place appropriately allocate risks to the bank that is providing the financing (the

First Buyer), but those risks are entirely theoretical given the nature of the commodity and the nature of

the sale and transfer. Ownership can be held by a bank or other financial institution, as the First Buyer,

and by the party needing financing, as the Second Buyer, without real risk of loss or damage for either of

those parties. The entire sequence of transactions (Third Party Seller sale to the First Buyer; First Buyer

sale to the Second Buyer; Second Buyer sale to the Third Party Buyer) can be accomplished in strict

compliance with the Sharīʿah with only a few keystrokes into a computer. Obtaining the authorizations

to make the keystrokes takes longer than the entire sequence of transactions.

Compare the risks and timing of a comparable set of transactions involving other commodities (say,

grain). At a minimum, there will be actual spoilage risks. Backing through an analysis of the other

aspects of the commodity and the transaction, it will soon become apparent that numerous issues and

considerations arise with respect to almost all other commodities: grade; quality; compliance with other

standards; spoilage; transportation and handling risks; increased transactional costs associated with the

commodity and the attendant transactions; and many others.

20

In short, metals are a nearly risk free transactional substrate for metals murābaha transactions and a

large, highly standardized, efficient market for these transactions has developed.

Use and Status of the Murābaha

The overall metals murābaha transaction (meaning, a Transaction involving a set of the Constituent

Transactions) has become the overwhelming transaction of choice for a broad range of financings. In

the earliest years of modern Islamic finance and investment, the transaction was used for commodities

transactions, working capital financings, inventory financing transactions, revolving credit transactions,

short‐term, medium‐term and long‐term term financings and virtually every other type of financing. As

other transactional vehicles were developed in the context of the modern markets, the murābaha

transaction became most closely identified with short‐term financings of different types (including

working capital transactions) and as the transactional substructure behind short‐term ‘deposits’ of

different types that was used to generate the fixed or variable returns paid do ‘depositors’. Istisnāʿ

structures came to the fore as the transactional structure of choice in many Middle Eastern construction

transactions. ʾIjāra structures rapidly became the most prominent structure for many acquisition and

operations financings of personal property and real property assets. The ʾijāra is still the transactional

structure of choice for many asset financings. Sukūk of different types took a leading position in

different sectors that desired capital markets (rather than private commercial) financing, including the

financing of financial services companies and some long‐term industrial and infrastructure projects.

With the onset of the global financial crisis in 2007, the murābaha has re‐emerged to as a transactional

structure of choice equivalent in range and coverage to its position in the early years of modern Islamic

finance and investment.

Bank regulators (such as the Comptroller of the Currency in the United States of America), using an

"economic substance" analytical methodology, have determined (in 1999) that murābaha transactions

of this type are "functionally equivalent to conventional financing transactions" and are thus permissible

bank lending transactions under relevant banking laws and regulations.40 For accounting and tax

purposes, the parties treat these murābaha transactions as loans in exactly the same manner as they

treat conventional loans in similar circumstances.

Legal, tax and accounting practitioners structure murābaha transactions based upon the conventional

loan documentation of the bank or other financial institution participating in the subject financing on a

case‐by‐case basis. Frequently, the bank's customary loan or credit agreement is the basis for drafting

the murābaha agreement, and modifications are made to the extent determined necessary to render

the agreement compliant with the Sharīʿah as determined by the Sharīʿah advisors for that specific

transaction. Thus, representations and warranties, covenants, events of default, remedies and other

provisions in the murābaha agreement are essentially identical to those in the bank's conventional loan

agreement. Many of these provisions require relatively minor modifications as included in murābaha

40 Comptroller of the Currency, United States of America, Interpretive Letter # 867, November 1999. See, also, Comptroller of the Currency, United States of America, Interpretive Letter # 806, December 1997, permitting, as lending transactions, Sharīʿah‐compliant net lease (ʾijāra) transactions involving real estate assets financed by regulated banks.

21

agreements. Significant issues arise in connection with the implementation of some of the standard

conventional loan concepts, such as commitment fees, profit participations, loan "rolllovers" and late

payment and default interest, among others. These concepts, as conventionally conceived, are

incompatible with relevant Sharīʿah principles and precepts. However, as noted below, mechanisms

have been developed to allow the inclusion of modified versions of these concepts in compliant

murābaha agreements.

A bank or other financing institution will require, as a condition precedent to funding the financing, a

legal opinion from reputable counsel to the effect that the murābaha agreement is enforceable in

accordance with its terms under applicable secular law: the "enforceability" or "remedies" opinion.41 In

order for legal counsel to render the enforceability opinion, the murābaha must be structured and

drafted to comply with applicable secular law.

In a "purely secular jurisdiction", the secular law will not incorporate the Sharīʿah to any extent.42 In

such a jurisdiction, the structuring and drafting will be performed in such a manner as to ensure that the

murābaha agreement is in fact enforceable as (usually) a loan under secular law, thereby enabling the

rendering of the legal opinion. Frequently the agreement will contain no explicit reference at all to the

Sharīʿah, although the structure and drafting of the agreement and transactional arrangements will have

been approved by the relevant Sharīʿah advisors as being compliant with the Sharīʿah. The result of that

process is that most, if not all, issues pertaining to the question of whether the murābaha agreement

constitutes a loan agreement, enforceable as a loan agreement, are never presented to a court. The

issues that are presented to a court relate to specific contractual compliance and related factual

matters. That is, the contract is accepted by the court as the governing document with respect to the

agreement of the contractual parties, and the specific dispute is considered under applicable secular

law, which treats the murābaha arrangements as conventional loan arrangements incorporating specific

agreed terms, as set forth in the murābaha agreement. Most commercial litigation of this type goes

unreported, unless it becomes subject to an appeal or is otherwise conducted in a court that reports and

publishes its opinions.

The situation is somewhat different in a jurisdiction that does incorporate the Sharīʿah to some greater

or lesser extent in the secular law of that jurisdiction. Practices vary widely from one jurisdiction to

another as to the degree of incorporation. While disputes relating to defaults under the murābaha

41 The nature, coverage and requisites of this legal opinion are discussed in Michael J.T. McMillen, Contractual Enforceability Issues: Sukuk and Capital Markets Development, 7 CHICAGO JOURNAL OF INTERNATIONAL LAW