TREASURE COAST ECONOMIC DEVELOPMENT … Portal/Formatted CEDS-Six...TREASURE COAST ECONOMIC...

104

TREASURE COAST ECONOMIC DEVELOPMENT DISTRICT Comprehensive Economic Development Strategy 2012 - 2017 August 13, 2012 This document was prepared under a financial assistance award (04-83-06494) from the U.S. Economic Development Administration Treasure Coast Regional Planning Council 421 SW Camden Avenue Stuart, Florida 34994 (772) 221-4060 Email: [email protected] Website: www.tcrpc.org

Transcript of TREASURE COAST ECONOMIC DEVELOPMENT … Portal/Formatted CEDS-Six...TREASURE COAST ECONOMIC...

TREASURE COAST

ECONOMIC DEVELOPMENT

DISTRICT

Comprehensive Economic

Development Strategy

2012 - 2017

August 13, 2012

This document was prepared under a financial assistance award (04-83-06494)

from the U.S. Economic Development Administration

Treasure Coast Regional Planning Council

421 SW Camden Avenue

Stuart, Florida 34994

(772) 221-4060

Email: [email protected]

Website: www.tcrpc.org

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

2

Table of Contents

Acknowledgements………………………………………………………………….

3

Preface ………………………………………………………………………………

4

Executive Summary………………………………………………………………….

5

Introduction ………………………………………………………………………….

10

STRATEGY REPORT A. Background

Part I: Economic Profile …………………………………………………………..

a. Overview

b. Demographic Trends

c. Employment, Income and Wage Trends

d. Industry Trends

13

Part II: Sustainability……………………………………………………………….

a. Overview

b. Quality of Place and Economic Development

c. Infrastructure

d. Climate Change and Energy

e. Environment

33

Part III: Cluster Industry Profile…………………………………………………..

a. Overview

b. Cluster Identification and Analysis

48

Part IV: Measuring Regional Innovation…………………………………………..

55

Part V: Regional SWOT Analysis………………………………………………….

62

B. CEDS Goals and Objectives…………………………………………………….

63

C. Community and Private Sector Participation………………………………….

65

D. Strategic Projects, Programs, and Activities…………………………………..

66

E. Action Plan ……………………………………………………………………… 70

TECHNICAL APPENDIX

A. Detailed Cluster Analysis……………………………………………………….

72

B. Performance Measures …………………………………………………………

83

C. Past, Present and Projected Future Economic Development Investments…..

84

D. Integrating the CEDS with State and Regional Economic Development

Priorities……………………………………………………………………………..

84

E. Map Series………………………………………………………………………..

85

F. Other (TBD)……………………………………………………………………… 90

G. Bibliography……………………………………………………………………...

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

3

ACKNOWLEDGEMENTS

The Treasure Coast Regional Planning Council would like to thank the members of the Comprehensive

Economic Development Strategy (CEDS) Committee for their input during the preparation of this

document.

A special thanks also to _________________ for their support during the preparation of this document.

Further information on this economic development plan may be obtained by contacting Mr. Greg Vaday,

Economic Development Coordinator, Treasure Coast Regional Planning Council at (772) 221-4060 or

email [email protected].

Contributing Committee Members

PALM BEACH COUNTY

Members Sherry Howard

Gary Hines

Tony Brown

Seabron Smith

Paul Skyers

Steve Craig

Alternates Doug Saenz

Carol Thompson

INDIAN RIVER COUNTY

Members Mark Mathes

Rich Stringer

Helene Caseltine

Randy Riley

Glenn Heran

MARTIN COUNTY

Members Tammy Simoneau

Anthony Parkinson

Tim Dougher

Pauline Becker

Linda Hake

Alternates Debbie Lewandowski

Ed Maxwell

Tobin Overdorf

Kathie Smith

Melissa Corbett

ST. LUCIE COUNTY

Members Derrik Moore

Teri Pinney

Michael Corbit

Harold Smyth

Nate Bray

Alternates Howard Fein

Larry Pelton

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

4

PREFACE

THE TREASURE COAST REGIONAL PLANNING COUNCIL, in partnership with its

local governments, businesses, nonprofit and community leadership, has developed this

Comprehensive Economic Development Strategy (CEDS) to help the Region achieve long-term

economic sustainability and regional competitiveness.

This CEDS was developed in cooperation with a standing committee comprised of organizations,

business leaders and individuals from throughout the Treasure Coast Region committed to

helping develop a sustainable regional economy. The year-long CEDS strategy development

process began with an in-depth economic analysis of the Region. This was followed by several

months of meetings to identify the salient strengths and weaknesses in the Region’s economy

and opportunities and threats that needed to be addressed to move forward. The net result of this

planning process was not only the preparation of this regional economic development strategy,

but the creation of an important regional collaborative mechanism to engage the Region’s

leadership.

The partners that have helped to create this strategy document recognize the Region’s long-term

sustainability and quality of life are tied into the larger global economy and the Region’s

economy must be focused on expanding economic diversity and enhancing innovation. This

became evident as the community’s leadership recognized how the Region’s most dynamic

industrial sectors – agriculture, tourism, construction, emerging life science, and research and

development clusters are affected not only by local economic conditions but national and

international economic trends as well. The deleveraging effects of the Great Recession have

significantly dampened per capita income, small business lending and labor mobility to the

detriment of the Region’s economic growth prospects. Simply put, the Region needs to lay the

foundations for a regionally competitive economy that produces the high demand goods and

services the world wants.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

5

EXECUTIVE SUMMARY

The Treasure Coast Region is well known for its beautiful Atlantic beaches and its high quality

of life. From Boca Raton in the south, the Region stretches 100 miles north to the Sebastian

Inlet, and from the Atlantic Ocean west to Lake Okeechobee. While recognized for its upscale

communities along the ocean, the Region’s population is primarily located in historic mainland

cities such as Boca Raton, Delray Beach, West Palm Beach, Riviera Beach, Stuart, Fort Pierce,

and Vero Beach, and in rapidly growing “suburban” communities such as Port St. Lucie, Jupiter,

Palm Beach Gardens, and Sebastian.

Although the Region houses a permanent population of 1.9 million and devotes over one million

acres to agricultural uses, it also contains a significant number of important natural resources.

Examples include the Loxahatchee National Wildlife Refuge, Lake Okeechobee, Loxahatchee

National Wild and Scenic River, the J.W. Corbett Wildlife Management Area, Indian River

Lagoon, Lake Worth Lagoon, St. Lucie River, Savannas (the largest remaining coastal

freshwater wetland on the Atlantic Coast) and St. John’s Marsh.

Robust population growth in the 1990s and the mid 2000s was the primary engine of regional

economic growth. During the period of 1990 to 2006, the Region’s average annual rate of

population growth was 2.5 percent, outpacing statewide growth of about 2.1 percent and

significantly outpacing national growth of about 1.1 percent. Equally important was the pace of

employment growth which mirrored the rate of population growth, averaging 2.5 percent per

year. The Region’s engine fueled heavily by tourism, agriculture, and the development of new

communities to meet the needs of a rapidly expanding population coupled with increasing

consumer demand for goods and services seemed a trend that would continue apace for quite

some time.

During this period of rapid population and employment growth, the Region’s leadership took

important steps to define and enhance emerging industry clusters such as aerospace/engineering,

aquaculture and marine-related industries. Significantly, in November 2003, then Governor Jeb

Bush signed into law a historic piece of legislation that laid the framework for the Scripps

Research Institute to expand its world-renowned scientific research and endeavors into Florida.

Scripps Florida, which began operations in Jupiter in 2005, became an important milestone on

the road to putting Florida and the Treasure Coast Region at the forefront of biomedical research

and development. Since the advent of Scripps, life science research institutes such as Torrey

Pines Institute for Molecular Studies, Max Planck Florida Institute and the Vaccine and Gene

Therapy Institute of Florida have significantly influenced and lead the growth and development

of the life sciences cluster in the Treasure Coast Region.

When TCRPC released its Comprehensive Economic Development Strategy 2007-2012

population and employment growth rates were expected to trend moderately lower than the high-

growth rate period of the previous ten years, landing somewhere around 2.0 percent. That CEDS

noted …. “This level of population growth should translate into healthy growth in the Region’s

local cluster industries such as retail trade, professional and business services and education and

health services…”

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

6

By the time the national recession officially began in December 2007, the relative strength of the

Region’s economy began to show softness as reflected by increases in the year over year

unemployment rate in all four of the Region’s counties and a decline for the first time since the

year 2000 in the median sales price for existing single family homes. By 2010, the Region’s

unemployment rate stood at 12.2% with St. Lucie and Indian River Counties experiencing the

highest rates of unemployment at 14.1% and 14.0% respectively.

Against the backdrop of the Great Recession and looking ahead over the next five years (2012 to

2017), this CEDS Plan attempts to gauge the existing health of the Region’s economy and its

future outlook. The analysis of data presented in the plan, along with findings from in-depth

discussions about Regional strengths, weaknesses, opportunities and threats reveals a Region

with a unique set of attributes – its industries, cities and towns and related quality of life/place,

climate, geography, talent, diversity and resources (both financial and intellectual); its growth

prospects and its innovative capacity.

All of these attributes can be effectively harnessed to put the Region on the path to economic

sustainability provided the Region’s collective leadership makes strategic investments and policy

decisions to shore up the Region’s economic base, its educational foundations, its multi-faceted

infrastructure network and most importantly, its skill base to take advantage of new and

emerging economic opportunities nationally and abroad. In terms of the growth prospect

attribute, average annual population growth rates over the coming decade (2010 to 2020) are

projected to decrease to 1.1 from a high of 1.9 percent over the previous decade (2000 to 2010).

Ethnically, the Region’s population is expected to become increasingly diverse with Hispanics

making up almost 22 percent of the population by 2030 from about 17.5 percent in 2010. The

Region’s employment growth is expected to outpace the level for the state and the nation.

However, this strong employment growth will be tempered by growth in lower wage sectors of

the economy. Currently, almost 45 percent of the Region’s employment base earns wages that

are lower than the Region’s average annual wage of $43,237. In 2007, approximately one third

of all jobs in the Region paid wages lower than the annual average wage.

The CEDS examines the Region’s physical attributes or infrastructure attributes and suggests it

is critically important for the Region to develop, expand and maintain its multi-modal

transportation systems and telecommunications infrastructure to support its economy and allow it

to link directly to global markets and opportunities. The Region’s two deepwater ports, its

twelve airports (1 commercial, 11 general aviation), its freight and passenger rail system and its

roadway transportation networks all need to become more closely integrated to serve the needs

of growing a diverse economy and to deliver the goods and services produced by the Region’s

economy to a broader world market.

From a cluster industry perspective, the Region exhibits relative specialization in three industry

clusters – Arts, Entertainment, Recreation and Visitor Industries (a foundational cluster in many

ways), Life Sciences and Business and Financial Services. Continued strong growth is projected

for the former two clusters. They are classified as “Star” clusters with Business and Financial

Services projected to transition to a “Mature” cluster. As previously mentioned, the Region also

has a number of emerging industry clusters including aerospace/engineering (incorporated in the Defense

& Security cluster); marine-related industries (incorporated in the Transportation Equipment

Manufacturing subcluster) and aquaculture (incorporated in the Agribusiness, Food Processing and

Technology cluster).

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

7

In terms of innovative capacity, this plan introduces a new web-based tool for comparing a

region’s innovation performance with that of the United States, a state or other regions. The

Innovation Index comprises two broad categories: inputs to innovation, which measure

innovation capacity, and outputs of innovation, which measure the results. The key for any

region’s economy is to translate its inputs – human capital and venture capital, for example, into

productive outcomes. The Treasure Coast Region scores ahead of the State of Florida with an

Innovation Index of 90.4 versus 86.5 but falls behind the nation by 10 percent and the State of

California by about 13 percent. It appears the Region’s lower levels of productivity affects its

overall innovation index score.

The Treasure Coast Region faces important challenges. As it slowly emerges from the negative

effects of the economic downturn and national recession – it needs to turn into a dynamic

economy. The current economy, long focused on tourism, agriculture and construction, must

now respond to the global challenge and compete in an increasingly interconnected world. The

current depression in the residential construction and tourism sectors, however temporary it may

be, highlights the importance of developing a dynamic economy to promote Regional economic

sustainability. If the Region’s leaders are truly concerned about economic sustainability and

facilitating the required transformation of the Region’s economy into one that is entrepreneurial

and innovative, that is dynamic– then regional collaboration and commitment is essential.

The Treasure Coast Region has taken important initial steps to develop an innovative economy,

but much more needs to be done. The key to the transformation is to focus on entrepreneurship

and innovation as the engine of regional competitiveness. The Region needs to re-energize its

educational foundations to ensure the future workforce can compete in a networked world and

find meaningful career opportunities and pathways. The Region’s leadership must focus not only

on smart growth, but should adopt a new paradigm of regional competitiveness. Finally, the

Region needs to form strong and sustainable networks to speed the process of innovation.

Without these actions the Region’s future is uncertain.

The TCRPC Comprehensive Economic Development Strategy 2012-2017 Plan serves as a

framework of ideas and a broad-based program of action to promote the long-term economic

sustainability of the Treasure Coast Region. It presents a comprehensive overview of our

Region’s economy illustrating significant trends in employment, wages, income and industry.

The plan examines the Region’s existing and emerging cluster industries, its economic assets and

the internal and external forces affecting its economy.

The CEDS suggests a comprehensive regional economic development strategy that is founded

upon the following vision for the Region:

The Treasure Coast Region:

Is comprised of vibrant communities with a true quality of place;

Is one of North America’s most dynamic economic regions;

Rewards innovation by starting, growing and attracting entrepreneurial firms;

Is Florida’s leading center for scientific research and development;

Provides economic opportunities to its residents;

Values its open spaces and unique natural environments; and

Has communities that are diverse, safe and prosperous.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

8

Implementing the vision for the Region rests upon three sets of strategic priorities:

1. Framework

SIX PILLARS of FLORIDA’S

FUTURE ECONOMY:

The Six Pillars program is designed to be a framework

serving as “an organizing force for strategic planning at

local, regional and state levels” to bring together

“fragmented viewpoints into a common and consistent

conversation.” The Six Pillars are:

Talent Supply and Education

Innovation and Economic Development

Infrastructure and Growth Leadership

Business Climate and Competitiveness

Civic and Governance Systems

Quality of Life and Quality Places

2. Cluster Industry Focus

To make the Region economically

competitive the collective leadership

needs to focus on the Region’s economic

drivers – its clusters.

An advanced economic development

framework that focuses on innovation

and high-quality job creation is cluster-

based economic development. In his

book, The Competitive Advantage of

Nations, Dr. Michael Porter, a noted Harvard economist, concludes that a nation’s most

successful industries are those that consist of related groups of firms rather than single,

isolated companies. Nations (and Regions within nations) succeed not in isolated industries,

but in clusters of industries connected through vertical and horizontal relationships. A nation’s

economy contains a mix of clusters, whose makeup and sources of competitive advantage (or

disadvantage) reflect the state of the economy’s development.

The National Governors Association publication, Cluster-Based Strategies for Growing State

Economies, describes the increasing importance of cluster strategies to help accelerate

regional competitiveness.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

9

3. A Regional Jobs Agenda

Sustainable economic growth and prosperity for the Treasure Coast Region requires the

development and implementation of nothing less than a regional jobs agenda. Such a regional

jobs agenda is not simply a return to pre-recession levels of employment because of

improving economic conditions but a completely new priority to establish a regional jobs

agenda by the collective leadership of the Region. McKinsey Global Institute, in its report,

An Economy That Works: Job Creation and America’s Future suggests that “…while a robust

economic recovery provides a foundation for job growth, a cyclical rebound in GDP growth

alone is unlikely to put enough Americans back to work. Job creation must become a national

priority, not a by-product of other policy decisions…failure to reverse the anemic job growth

of the past decade and to accelerate job creation in the years to come will have serious

consequences for the future of the economy and the American people. For the United States

to remain a high-income, globally competitive nation, it will need to set the conditions for

demand-driven growth and job creation.” The report suggests progress on four dimensions is

needed:

Skill: Ensuring that Americans acquire the skills that match employer needs.

Share: Helping American workers win “market share” in an expanded global

economy.

Spark: Encouraging innovation, new company creation, and the scaling up of

new industries in the United States.

Speed: Removing impediments to investment and job creation.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

10

INTRODUCTION

The CEDS is designed to guide the economic growth of the Treasure Coast Region. It is the

result of an ongoing, participatory planning process that addresses the economic problems and

potential of the Region. The strategy reflects local economic development needs and priorities

and recommends a regional approach to achieving sustainable economic development.

Ultimately, the CEDS planning process helps create livable wage jobs, fosters the growth of a

competitive regional economy, and secures the Region’s long-term sustainability.

A CEDS is required to qualify for U.S. Economic Development Administration (EDA)

assistance under its public works, economic adjustment, and most planning programs, and is a

prerequisite for designation by EDA as an Economic Development District (EDD). In December

of 1998, Council prepared its first CEDS in order to obtain designation as an EDD. In 2000, the

TCRPC produced its second planning strategy – “Treasure Coast 2010.” In 2004, Council

published “Go Treasure Coast 2004-2014.” In 2007, TCRPC released Comprehensive Economic

Development Strategy 2007-2012. This document is the fifth version of the CEDS plan and

importantly is developed in cooperation and collaboration with economic development planning

efforts going on simultaneously statewide with other regional planning councils, the State of

Florida, the workforce development boards, and other statewide economic development

stakeholders.

This CEDS planning effort is aligned with and is being conducted in concert with statewide and

regional economic development planning efforts as follows:

Florida’s 2012-2017 Statewide Strategic Plan for Economic

Development

The Florida Department of Economic Opportunity (DEO)

Division of Strategic Business Development, as outlined in

Florida Statutes, 20.60, is required to create a five year

statewide strategic plan designed to help guide the future of Florida’s economy. DEO is

developing the strategic plan in close coordination with Enterprise Florida, Workforce Florida,

local governments, local and regional economic development organizations, the business

community, educational institutions as well as other local, state and federal entities. The

framework adopted for the planning effort is the Six Pillars of Florida’s Economy developed by

the Florida Chamber Foundation.

Earlier this year (February and March) DEO held regional forums across the state in conjunction

with all eleven regional planning councils to gather insights related to the creation of Florida’s

2012-2017 Statewide Strategic Plan for Economic Development. The purpose of the forums was

to review and prioritize goals, objectives and strategies for implementation by state government

that would assist Florida’s regions with economic development and job creation. The Treasure

Coast centered regional forum was held on March 5, 2012 in Stuart and had participation from

over 115 people representing local governments, local and regional economic development

organizations, community economic development entities, workforce development boards, the

business community, educational institutions and others attended the event. TCRPC staff

presented participants an overview of the 2012 CEDS Plan at the event.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

11

Seven50

Seven50 (“seven counties, 50 years”) is a blueprint for

growing a more prosperous, more desirable Southeast

Florida during the next 50 years and beyond. The plan is

being developed to help ensure socially inclusive

communities, a vibrant and resilient economy, and

stewardship of the fragile ecosystem in what is quickly

becoming one of the world’s most important mega-regions.

Spearheaded by the South Florida and Treasure Coast Regional Planning Councils and the

Southeast Florida Regional Partnership (SFRP), a unique collaboration of more than 200 public,

private, and civic stakeholders, Seven50 is mapping the strategy for the best-possible quality of

life for the more than six million residents of Monroe, Miami-Dade, Broward, Palm Beach,

Martin, St. Lucie and Indian River counties.

The plan is being devised through a series of public summits, workshops, online outreach and

high-impact studies led by the region’s top thinkers. Seven50 has been made possible by a grant

from the U.S. Department of Housing & Urban Development’s Sustainable Communities

Initiative.

The Florida Eight

The Florida Eight initiative provides regional

teams with a variety of facilitation services

and resources to build their regional capacity

for economic development, talent

development, job retention and international

business opportunities. Through Workforce

Florida’s investment—and consistent with its

mission to strengthen the state’s business climate through talent development— this initiative

provides research, marketing and other resources to up to eight regional teams as they establish

and implement business development plans.

The Southeast Regional Business Team (covering the

seven county region extending from Monroe to Indian

River counties) has convened stakeholder meetings since

August 2011 to the present to identify the largest “Old

Economy” barriers to regional competitiveness and build a

strategic action plan to remove them. The identified focus

areas are:

Access to Capital

Logistics and Transportation Infrastructure

Licensing and Permitting/Transactions in the

Public Sector

International Diversification

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

12

STRATEGY REPORT

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

13

A. BACKGROUND

PART I: ECONOMIC PROFILE

a. Overview

The Region’s economy long-focused on tourism, agriculture and the development of new

communities to meet the needs of a rapidly expanding population is taking important steps to

enhance its economic base along the lines of high-value added cluster industries such as Life

Sciences, Transportation Equipment Manufacturing and Transportation and Logistics. The

recent establishment of the Scripps Research Institute, the Torrey Pines Institute for Molecular

Studies, Vaccine & Gene Therapy Institute of Florida, a new teaching hospital at Florida Atlantic

University and other related operations, for example, have given the Region a profound boost in

the growing life sciences arena. These research institutes, should, over time, help to generate

important spin-off businesses and provide good job opportunities for residents. At the same

time, the majority of projected, fastest-growing jobs are in relatively low-paying sectors such as

tourism, administrative support services and construction labor. The Region attracts tens of

thousands of seasonal residents and tourists, primarily during the winter months. While tourism

is a leading income producing sector of the Region’s economy, the health care and social

assistance industry is rapidly growing.

Although employment in agriculture is declining, the Region maintains a primary role in

agricultural production. Palm Beach County ranks first in the state in income from agricultural

sales, and is of national prominence in the production of sugar cane and winter vegetables. St.

Lucie County is the largest grapefruit producing county in the state, and the Region is Florida’s

largest producer of citrus.

In many important ways the Region is experiencing a transition in its industry makeup but also in

its focus on economic sustainability as the main framework for economic development planning.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

14

U.S. metropolitan areas are now home to 83 percent of American citizens, driving America’s

economy and service as incubators of innovation and entrepreneurship that can help generate

quality jobs and spur long-term, sustainable, growth. Brookings experts examine the role of

U.S. metro areas in driving the U.S. economy and how best to create a platform for U.S. cities

and metropolitan areas to boost American competitiveness in the global marketplace.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

15

b. Demographic Trends

Population

The Treasure Coast Region’s current (2011) population is 1,890,837. This population is

distributed among the Region’s Counties as indicated in Table 1 and Figure 1 below. Palm

Beach County has the largest proportion of the Region’s population at approximately 70 percent.

In 1970, Palm Beach County’s share at the Region’s population was 75 percent. St. Lucie

County is now home to about 15 percent of the Region’s population, up from about 11 percent in

1970.

TABLE 1

2011 POPULATION DISTRIBUTION

7% 8%

70%

15%

Figure 1 2011 Population Distribution

Treasure Coast Region

Indian River

Martin

Palm Beach

St. Lucie

County Population

Indian River 138,694

Martin 146,689

Palm Beach 1,325,758

St. Lucie 279,696

Region 1,890,837 Source: U.S. Census Bureau, 2010 Census and University of

Florida, Bureau of Economic and Business Research.

Source: U.S. Census Bureau, 2010 Census and TCRPC

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

16

The Region contains a large number of municipalities (50 in 2010), 38 of which are in Palm

Beach County. Owing to its phenomenal growth over the last forty years, the Region’s largest

city would clearly be Port St. Lucie. Data for the Treasure Coast Region show that the five most

populous incorporated places and their 2010 Census counts are Port St. Lucie, 164,603; West

Palm Beach, 99,919; Boca Raton, 84,392; Boynton Beach, 68,217; and Delray Beach, 60,522.

Port St. Lucie grew by 85.4 percent since the 2000 Census. West Palm Beach grew by 21.7

percent, Boca Raton grew by 12.9 percent, Boynton Beach increased by 13.0 percent, and Delray

Beach grew by 0.8 percent.

Population Growth Trends

The Treasure Coast Region’s population has changed dramatically over the last forty years.

Between 1970 and 2010 the Region’s population increased four-fold, and the Region’s 2010

population stood at almost 1.9 million from just under 500,000 in 1970.

TABLE 2

POPULATION OF THE TREASURE COAST REGION

1970 – 2010

County 1970 1980 1990 2000 2010

Indian River 35,992 59,896 90,208 112,947 138,028

Martin 28,035 64,014 100,900 126,731 146,318

Palm Beach 348,993 576,812 863,503 1,131,191 1,320,134

St. Lucie 50,836 87,182 150,171 192,695 277,789

Region 463,856 787,904 1,204,782 1,563,564 1,882,269

State 6,791,418 9,746,961 12,938,071 15,982,378 18,801,310

Nation 203,302,031 226,545,805 248,709,873 281,421,906 308,745,538 Source: U.S. Census Bureau, 2010, 2000, 1990, 1980 and 1970 Censuses

The Region’s share of the Florida population has grown steadily over the forty-year period. In

1970, 6.8% of the State’s population resided in the Region compared to 10% in 2010.

TABLE 3

REGION’S SHARE OF STATE POPULATION

Year State Share

1970 6.8%

1980 8.1%

1990 9.3%

2000 9.8%

2010 10.0%

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

17

The Region experienced its highest growth

in population by percentage (69.8) during

the 1970 to 1980 period. However, the

decade with the greatest actual or absolute

increase in population (416,878) occurred

between 1980 and 1990. Palm Beach

County has experienced the most absolute

growth since 1970 adding 971,141 persons

over the 40 year time period. While the

Region increased at a slower pace in the

subsequent decades, it significantly

outpaced the State’s population growth in

each decade from 1970 to 2010.

Percentage-wise, St. Lucie County has

experienced the most growth since 1970

with a 446 percent increase in population.

TABLE 4

POPULATION GROWTH (percentage)

1970-1980 1980-1990 1990-2000 2000-2010

REGION 69.8 52.9 29.8 20.4

Indian River County 66.4 50.6 25.2 22.2

Martin County 128.3 57.6 25.6 15.5

Palm Beach County 65.3 49.7 31.0 16.7

St. Lucie County 71.5 72.3 28.3 44.2

STATE 43.5 32.7 23.5 17.6 Source: TCRPC

Between the 2000 and 2010 Census, the Region continued to increase in population, although at

a slower pace than in the previous ten year period (1990 to 2000). Each of the Counties

experienced a population increase of between 15 and 44 percent. The Region as a whole

increased by 20.4%, compared to 17.6% for the entire State.

Trend Analysis: Based on 2020 population

projections, the Region’s population will

continue to increase but at an annual pace of,

1.1%, which is lower than the projected growth

rate for the State, 1.2% as a whole, and

significantly lower than the 1.9% growth rate,

experienced during the previous ten-year (2000

to 2010) period. From a population of just

under 1.9 million in 2010, the estimated

Regional population in 2020 is over 2.0 million,

a projected increase of 11.2%. St. Lucie County

will be the fastest growing County in the Region over this period increasing at an annual average

rate of 2.4%, followed by Indian River County at 2.0%.

Projected

Average Annual Growth Trends

County 2010-2020

Indian River 2.0 percent

Martin 0.8 percent

Palm Beach 0.7 percent

St. Lucie 2.4 percent

Region 1.1 percent

Florida 1.2 percent Source: University of Florida, BEBR, Adapted by

TCRPC

PopulationPopulation The RegionThe Region’’s population has increased s population has increased

almost fouralmost four--fold since 1970fold since 1970

0

500,000

1,000,000

1,500,000

2,000,000

1970 1980 1990 2000 2010

Year

Population of the Treasure Coast Region

Indian River

Martin

Palm Beach

St. Lucie

Region

Largest % growth – 69.8%

Largest absolute growth – 416,878

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

18

By 2035, the Treasure Coast Region is expected to reach a population in excess of 2.4 million.

In the same period, the State of Florida will reach a population of 24.9 million.

The vast majority of this projected population

growth will be attributable to an estimated annual

net migration rate of 20,700 persons per year for the

Region.

Trend Analysis: In-migration will likely be a

continuing trend for the Treasure Coast Region for

the foreseeable future, albeit at a lower rate than

previously experienced. Over the next ten years

(2010 to 2020), the Region’s population is expected

to reach 2.1 million, increasing by over 210,000

people. This projected increase will be fueled

predominantly by net domestic migration.

Strategic Finding: At the current rate of population growth, approximately 21,000 persons per

year will need to be accommodated somewhere within the Region. This equates to about 58 new

residents per day. This level of

population growth should translate into

healthy growth in the Region’s local

cluster industries such as retail trade,

professional and business services and

education and health services.

However, infrastructure systems and

resources, particularly water and

transportation systems will be

challenged by residential and economic

growth.

Age Profile: The Region’s population is

older than that of the state or the nation.

In 2010, 22 percent of the Region’s

population was aged 65 and over, compared

to 17 percent of the State’s population and

only 13 percent of the nation’s population.

The Region’s school age population (5 to

17) at 15 percent compares with slightly

over 15 percent for the State and 18 percent

for the nation.

Trend Analysis: The most striking

characteristic of the age distribution of the

Treasure Coast Region’s population is the

increasing proportion of the age cohort referred to as “baby-boomers” (born between 1946 and

PopulationPopulation By 2035, RegionBy 2035, Region’’s population is estimated s population is estimated

to reach 2.4 millionto reach 2.4 million

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

1970 1980 1990 2000 2010 2020 2035

Population of the Treasure Coast Region

1970-2035

Population by Age Group, 2010

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00%

Ages 0 to 4

Ages 5 to 17

Ages 18 to 24

Ages 25 to 44

Ages 45 to 64

Ages 65 and Older

% of Total Population

State

Region

Population by Age Group, 2000 and 2010

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00%

Ages 0 to 4

Ages 5 to 17

Ages 18 to 24

Ages 25 to 44

Ages 45 to 64

Ages 65 and Older

% of Total Population

2000

2010

Figure 2

Figure 3

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

19

1964). This age cohort can be further divided into what demographers call “empty nesters”

(aged 45-54) and “pre-elderly” (aged 55-64). From 1990 to 2010, the proportion of persons aged

45-64 grew rapidly in all counties in the Region. The senior population that is 65 years and over,

initially peaking in the year 2000, actually has started to decline as a share of each County’s

overall population in 2010.

The median age of all counties in the Region is projected to continue to increase over the next

twenty years, clearly outpacing the more modest increase in the State’s median age. This aging

of the population reflects a pattern of sustained net migration of elderly persons to the Treasure

Coast Region.

TABLE 5

MEDIAN AGE: CENSUS 2010 AND PROJECTIONS

TREASURE COAST REGION

2010 – 2030

COUNTY 2010 2020 2030

INDIAN RIVER 49.1 53.5 56.0

MARTIN 49.7 55.1 57.3

PALM BEACH 43.5 45.0 46.4

ST. LUCIE 42.4 46.8 49.0

STATE 40.7 42.2 44.0 Source: U.S. Census Bureau, 2010 Census and Florida Statistical Abstract

2010

By 2030, Martin and Indian River Counties are projected to have a median age of 57.3 and 56.0,

respectively – twelve years higher than the State’s projected median age.

Strategic Finding: A fixed older population without an increase in the prime working age cohort

will challenge the Region’s drive to change its industrial mix from population-serving industries

such as education and health services and leisure and hospitality to traded cluster industries such

as life sciences, manufacturing and information technology as these industries need talented

young professionals to grow and prosper.

Racial and Ethnic Diversity:

In line with state trends, the

Treasure Coast Region’s racial

and ethnic composition has

become increasingly diverse over

the last decade. From 2000 to

2010, the Non-Hispanic White

share of the Region’s population

decreased from 73.2 percent to

63.1 percent. During this period,

the Region’s Hispanic population

grew from 11.1 percent to 17.5

percent of the total population.

The Region’s Non-Hispanic -20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

200.0%

Indian River Martin Palm Beach St. Lucie Treasure

Coast

Percentage Change by Race and Hispanic Origin

2000 to 2010

Non-Hispanic White

Non-Hispanic Black

Hispanic (Any Race)

Figure 4

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

20

Black population has also continued to grow in size since 2000 reaching 15.5 percent in 2010

versus 12.6 percent.

Palm Beach County experienced the largest rise in Hispanic population in absolute terms

growing from 140,675 to 250,823, an increase of 110,148 or 78.3 percent. St. Lucie County

experienced the highest percentage increase in its Hispanic population, just over 102 percent.

Trend Analysis: By 2030, population projections prepared by the Bureau of Economic and

Business Research at the University of Florida suggest that the Hispanic portion of the

population will reach almost 22 percent and the proportion of the Non-Hispanic White

population to fall to 60.1 percent, down from 63.1 percent in 2010. The Non-Hispanic Black

population is also projected to increase over the next twenty year period but only slightly. By

2030, the Non-Hispanic Black population will reach about 15.8 percent of the Region’s

population up from 15.5 percent in 2010.

Strategic Finding: The increasing diversity of the Region’s population, as evidenced by the

actual and projected rise of the Hispanic population from 11 percent in 2000 to just over 17

percent in 2010, and eventual rise to almost 22 percent presents new opportunities and

challenges for the Region’s educational system. Additionally, social and cultural amenities and

opportunities within the Region’s cities will need to reflect this growing diversity. An

increasingly diverse population will also provide fertile ground for new business opportunities.

Educational Attainment: In

2010, approximately 86.5

percent of the Region’s

population 25 years and over

had a high school degree or

higher and 29.1 percent had

earned a bachelor’s degree or

higher. Nationally, 85.6 percent

of the population had a high

school degree or higher and 28.2

percent had earned a bachelor’s

degree or higher. Within the

Region, Palm Beach County had

the highest proportion of its

population earning a bachelor’s

degree or higher at 31.8 percent

and St. Lucie County had the

lowest proportion of its

population with a bachelor’s degree or higher at 16.6 percent.

Strategic Finding: The Treasure Coast Region has a slightly higher proportion of its population

over 25 years of age that earned a bachelor’s degree or higher than the state or the nation. This

should be considered an opportunity to expand upon. However, there are marked differences in

educational attainment within the Region that need to be addressed. The Region needs to do

what it can to recruit a graduate program university with a robust research and development

0% 20% 40% 60% 80% 100% 120%

Indian River

Martin

Palm Beach

St. Lucie

Treasure Coast

US

State

Educational Attainment by % of Population 25

Years and Over, 2010

High School or less High School Graduate

Some College or Associate's Degree Bachelor's Degree

Graduate or professional degree

Figure 5

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

21

capability that is internationally acclaimed and recognized. This will help to attract talented

young professionals to the Treasure Coast Region.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

22

c. Employment, Income and Wage Trends

Labor Force and Unemployment: The Region’s annual average labor force and employment

indicators stood at 867,391 and 779,483 respectively for 2011. The 2011 unemployment rate for

the Region was 10.1 percent, compared to 9.7 percent for the State and 8.9 percent for the nation.

Within the Region, Palm Beach County had the lowest unemployment rate at 9.7 percent.

Table 6

Treasure Coast Region

Labor Force Summary

2011 Annual Averages

County/Region Civilian Labor

Force

Employment Unemployment

Level

Unemployment

Rate (percent)

Florida 9,197,730 8,304,616 893,114 9.7

Treasure Coast 867,391 779,483 87,908 10.1

Indian River 62,347 55,253 7,094 11.4

Martin 62,926 56,789 6,137 9.8

Palm Beach 618,909 558,880 60,029 9.7

St. Lucie 123,209 108,561 14,648 11.9

Source: U.S. Bureau of Labor Statistics.

Strategic Finding: The Region’s labor force participation rate of 56.2 percent is lower than that

for the State at 60.4 percent and markedly lower than the nation at 64.1 percent. The perception

of the Treasure Coast Region held by many community leaders inside and outside of the Region

is that its economy is based solely upon dividends, interest and rent income. Marketing the

Region as a valuable location to establish high-paying industries is constrained in part by this

perception of the Region as a tourist and retirement haven. The Region’s leadership needs to

help change the perception of the Region.

Employment Growth: Employment growth

reflects the rate at which

the economy is creating and

filling new jobs. The

Region continued to add

new jobs to its economy

through 2006, but the 2008-

2009 national recession

hampered employment

growth and caused it to turn

negative. Recent data,

however, suggests that

growth may be turning

positive once again.

Employment Growth

2000-2011Year Over Year Percent Change

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

nation state region

Figure 6

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

23

Why is This Important?

Employment growth is an indicator of expansion in the economy and represents an increase in

the economic opportunities available to the citizens of the region. Employment growth is

generally tracked as a percentage change year over year.

How is the Region Doing?

Between 2000 and 2006, Treasure Coast’s employment growth outpaced that of the state and the

nation (3.0% vs. 2.1% and 0.90%, respectively), but then lagged the U.S. and Florida during

2006-2007. As the national recession took hold in 2008, the Region’s employment growth rate

turned negative and contracted. Employment growth shrank from 2007 to 2010. From 2010 to

2011 employment growth turned positive for the first time experiencing 1.3 percent growth.

The year over year growth was led by advances in Professional and Business Services, Education

and Health Services, Trade, Transportation and Utilities, Leisure and Hospitality and Financial

Activities and other service industries.

Source: U.S. Bureau of Labor Statistics.

Net year over year job growth was just over 4,400.

-3,000 -2,000 -1,000 0 1,000 2,000

Construction

Natural Resources and Mining

Manufacturing

Information

Unclassified

Other Services

Financial Activities

Leisure and Hospitality

Trade, Transportation and Utilities

Education and Health Services

Professional and Business Services

Year Over Year Employment Change by

Industry, 2010-2011

Figure 7

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

24

Industry Mix

In 2011, the Treasure Coast Region employed almost 642,000 people in the following industries

(see Figure 8) and accounted for approximately 10 percent of the state’s total employment.

Source: Florida Department of Economic Opportunity, Labor Market Statistics

Center, Quarterly Census of Employment and Wages Program (QCEW).

Released March 2011 and TCRPC adaptation.

The Education and Health Services sector accounted for the largest share of the Region’s 2011

non-farm employment followed by the Trade, Transportation and Utilities sector. This marks a

reversal from the previously published CEDS plan in 2007 when Trade, Transportation and

Utilities was the dominant economic industry sector by employment.

At the County level, on a relative basis, there are marked differences in the industry mix. For

example, St. Lucie County has the highest proportion of employees within the Trade,

Transportation and Utilities sector at 24% whereas Palm Beach County has the highest

proportion of employees within the Professional and Business Services sector at 17%. Martin

County has a relatively high proportion of its employment base employed in manufacturing at

5% while Indian River County has the highest proportion of employees in Education and Health

Services at 24% (see Figure 9).

Employment by Industry

2011

Construction

5%

Leisure and Hospitality

13%

Other Services

4%

Financial Activities

7%

Public Administration

6%

Information

2%

Natural Resources and

Mining

1%Unclassif ied

0%

Manufacturing

3%

Education and Health

Services

23%

Trade, Transportation and

Utilities

21%

Professional and Business

Services

15%

Figure 8

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

25

Figure 9 County Industry Mix

2011

Palm Beach County

Industry Mix, 2011

5%6%

14%

17%

20%

21%2%

4%3%

7%

1%0%

Unclassif ied Information

Natural Resources and Mining Manufacturing

Other Services Construction

Public Administration Financial Activities

Leisure and Hospitality Professional and Business Services

Trade, Transportation and Utilities Education and Health Services

Martin County

Industry Mix, 2011

5% 4%7%

5%

5%

13%12%

23%

23%2%1%0%

Unclassif ied Information

Natural Resources and Mining Manufacturing

Other Services Construction

Public Administration Financial Activities

Leisure and Hospitality Professional and Business Services

Trade, Transportation and Utilities Education and Health Services

St. Lucie County

Industry Mix, 2011

0% 3%

11%10%24%

26%

3%6%

8%

6%

2%1%

Unclassif ied Information

Natural Resources and Mining Manufacturing

Other Services Construction

Public Administration Financial Activities

Leisure and Hospitality Professional and Business Services

Trade, Transportation and Utilities Education and Health Services

Indian River

Industry Mix, 2011

6%

7%

14%10%

21%

24%0%

5%

4%4%3%

2%

Unclassif ied Information

Natural Resources and Mining Manufacturing

Other Services Construction

Public Administration Financial Activities

Leisure and Hospitality Professional and Business Services

Trade, Transportation and Utilities Education and Health Services

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

26

Table 7

Employment by Wages and Industry

2011

Table 7, above reflects average annual employment by major industry sector for both the region

and the state. Of particular note is the Region’s annual average wage of $43,237 which is higher

than the State’s average wage of $42,176. In fact, for most industry sectors, the Region’s

average annual wage is higher than that for the State.

The industry sectors that pay an average annual wage higher than the Region’s average annual

wage of $43,237 include Education and Health Services, Professional and Business Services,

Manufacturing and Financial Activities. Together, the sectors that pay more than the District

annual average wage represent approximately 55 percent of total jobs.

Trend Analysis: Employment growth in the Treasure Coast Region has generally outpaced

population growth. As population growth tends to slow over the next few years it is expected

employment growth will moderate as well. Nevertheless, the Region’s employment growth rate

should continue to exceed that of the nation and the state.

1 Wages displayed in this table do not include non-wage income (dividends, rents, interest etc.).

Treasure Coast Region State of Florida Industry Number of

Establish-

ments

Total

Employment

Employment

Share

Average

Annual

Wage1

Industry Number of

Establish-

ments

Total

Employment

Employ

ment

Share

Average

Annual

Wage

Natural

Resources and

Mining

655 7,612 1.19% $30,023 Natural

Resources and

Mining

5,291 62,085 0.88% $28,856

Construction 6,418 32,757 5.10% $40,888 Construction 57,562 341,729 4.82% $41,180

Manufacturing 1,671 21,181 3.30% $53,356 Manufacturing 17,872 311,824 4.40% $53,176

Trade,

Transportation

& Utilities

12,633 132,065 20.57% $37,679 Trade,

Transportation

& Utilities

135,962 1,532,857 21.63% $38,644

Information 894 10,992 1.71% $58,885 Information 9,885 135,063 1.91% $63,236

Financial

Activities

7,220 43,469 6.77% $63,943 Financial

Activities

62,809 478,314 6.75% $56,744

Professional

and Business

Services

15,208 97,867 15.24% $53,139 Professional

and Business

Services

132,962 1,053,593 14.86% $50,420

Education and

Health Services

7,393 146,204 22.77% $44,006 Education and

Health Services

62,060 1,529,086 21.57% $43,832

Leisure and

Hospitality

5,021 86,208 13.43% $22,574 Leisure and

Hospitality

50,087 958,688 13.52% $22,328

Other Services 6,773 26,561 4.41% $30,599 Other Services 51,369 233,234 3.29% $30,212

Public

Administration

408 37,045 5.77 $56,427 Public

Administration

5,081 449,516 6.34% $50,980

Unclassified 175 109 0.02% $27,323 Unclassified 2,465 2,361 0.03% $31,916

Total All

Industries

64,469 642,070 100.0% $43,237 Total All

Industries

593,405 7,088,350 100.0% $42,176

Source: Florida Department of Economic Opportunity, Labor Market Statistics Center, Quarterly Census of Employment and Wages Program (QCEW).

Released March 2012 and TCRPC adaptation.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

27

Strategic Finding: Almost 45 percent of the Region’s employment base earns wages that are

lower than the Region’s average annual wage of $43,237. This is a marked increase in lower

wage growth since publication of the previous CEDS plan in 2007. In 2007, one third of all jobs

paid wages lower than the annual average wage. Continued growth in low wage industry sectors

and a relative decline of job growth in the Information and Manufacturing industry sectors

suggest the Region needs to continue to focus on advancing the growth of high-wage, high-value

added sectors and reshaping the educational system to produce more engineers, scientists and

other skilled professionals.

Wages and Compensation

In 2010, the average annual wage in the Treasure Coast Region was approximately $43,300.

Average annual wages for the Treasure Coast Region have continued to outpace the average

wage levels for the State (Figure 10). However, average annual pay in the Region has been 6 to

7 percent below national wage levels. There are marked differences in wage levels within the

Region with Palm Beach County experiencing the highest and St. Lucie the lowest average

annual wages.

As illustrated in Figure 10, the Region’s average annual pay is likely to grow modestly and is

affected by the differences in wage levels within the four counties. Moreover, the continued

growth in relatively lower paying industry sectors brings down the Region’s average annual

wage as well. In a web-based report, Florida’s Job Structure, The University of Florida, Bureau

of Economic and Business Research maintains that Florida’s dependence on retirees, growth and

tourism has heavily contributed to its disproportionate share of relatively low skill jobs. Florida

is generally long on low skill jobs and short on high skill jobs.

Generally, Florida is over-represented in most types of service, leisure and hospitality, retail

trade and construction jobs. The State is under-represented in manufacturing and government

jobs which generally pay high wages. Long-term, medium-term and short-term (15 year, 5 year

and 1 year) state trends accentuate this pattern of disproportionate job growth in low wage

industry jobs with a declining share of high wage jobs.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

28

Trend Analysis: Interpolating from the trends illustrated in Figure x suggest that wage

differences between the Region’s counties will likely exist for the foreseeable future.

Strategic Finding: The Treasure Coast Region continues to experience lower average wages per

job as compared to the nation. Even as Palm Beach County’s average wage per job tracks that of

the U.S. average wage ($46,751), wages in Martin, Indian River and St. Lucie Counties in 2010

were 82 percent, 75 percent and 73 percent, respectively of the nation’s average annual wage.

Table 8

Treasure Coast Average Weekly Wage

2010

Year Geographic Area

Average Weekly

Wage*

2010 Indian River $677

2010 Martin $740

2010 St. Lucie $655

2010 Palm Beach $881

2010 Region $833

Note: * Average Annual Wage divided by 52 weeks

Source: U.S. Bureau of Labor Statistics.

In terms of average weekly wages, Palm Beach County has the highest wage in the Region at

$881 and St. Lucie County has the lowest average weekly wage at $655.

Poverty

St. Lucie County has the highest incidence of absolute poverty at 13.7 percent and Indian River

County experiences the highest percent of employed workers in poverty than any of the Region’s

counties or the State.

Average Annual Pay

2001 - 2010

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Year

Wa

ge

e

Palm Beach Martin St Lucie Indian River

Region Florida Nation

Figure 10

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

29

Table 9

POVERTY STATUS IN THE PAST 12 MONTHS OF INDIVIDUALS BY SEX BY EMPLOYMENT STATUS

Universe: CIVILIAN POPULATION 16 YEARS AND OVER FOR WHOM POVERTY STATUS IS DETERMINED

Florida Indian

River Martin

Palm

Beach St. Lucie Region

Total:

Income in the past 12 months below poverty level: 1,817,615 12,170 10,786 112,937 25,237 161,130

Employed workers in poverty (Male & Female) 537,435 3,828 3,331 34,438 7,084 48,681

Percent of employed workers in poverty 6.4% 7.0% 5.5% 5.9% 6.4% 6.0%

Poverty rate for total population 16+ 12.4% 10.8% 9.0% 10.8% 11.8% 10.8%

Poverty rate for total population, all ages 13.8% 12.6% 10.4% 12.2% 13.7% 12.3%

NOTE. Data are limited to the household population and exclude the population living in institutions, college dormitories, and other group

quarters.

Source: U.S. Census Bureau, 2006-2010 American Community Survey 5-Year Estimates.

While the Region as a whole and its four counties have absolute poverty rates lower than the

state, there are communities experiencing significantly high levels of poverty. For example, the

Glades Region in the western portion of Palm Beach County, encompassing the cities of Belle

Glade, Pahokee and South Bay and the surrounding unincorporated areas stands out. The Glades

area is mostly rural with a total population of nearly 28,000. Poverty and long-term

unemployment are significant challenges in the region. This region has a staggering poverty rate

of approximately 33.3%. At the northern extent of the Region is the City of Fellsmere which has

a poverty rate of 26.6%. Within the Region’s urbanized corridor the City of Riviera Beach has a

poverty rate of 24.6%.

Strategic Finding: The incidence of poverty among employed workers in the Region is lower

than that for the state as a whole. However, Indian River County has the highest incidence of

poverty among employed workers while St. Lucie County has the highest rate of poverty for its

overall population of all the counties in the Region. Moreover, there are pockets of extreme

poverty in areas throughout the Region. Strategic projects and programs should be developed to

help build the job base and skill levels in the Region’s most distressed communities.

Income The Treasure Coast Region had a total personal income of just over $92.2 billion in 2010. At

$48,900 the Treasure Coast Region’s 2010 per capita income is above the state and the national

averages of $38,210 and $39,937 respectively. The respective per capita income of each of the

region’s counties is presented in Table 10 below:

Table 10

Per Capita Income by County, 2010

County Per Capita Income

Indian River $49,963

St. Lucie $29,670

Martin $51,723

Palm Beach $52,526

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

30

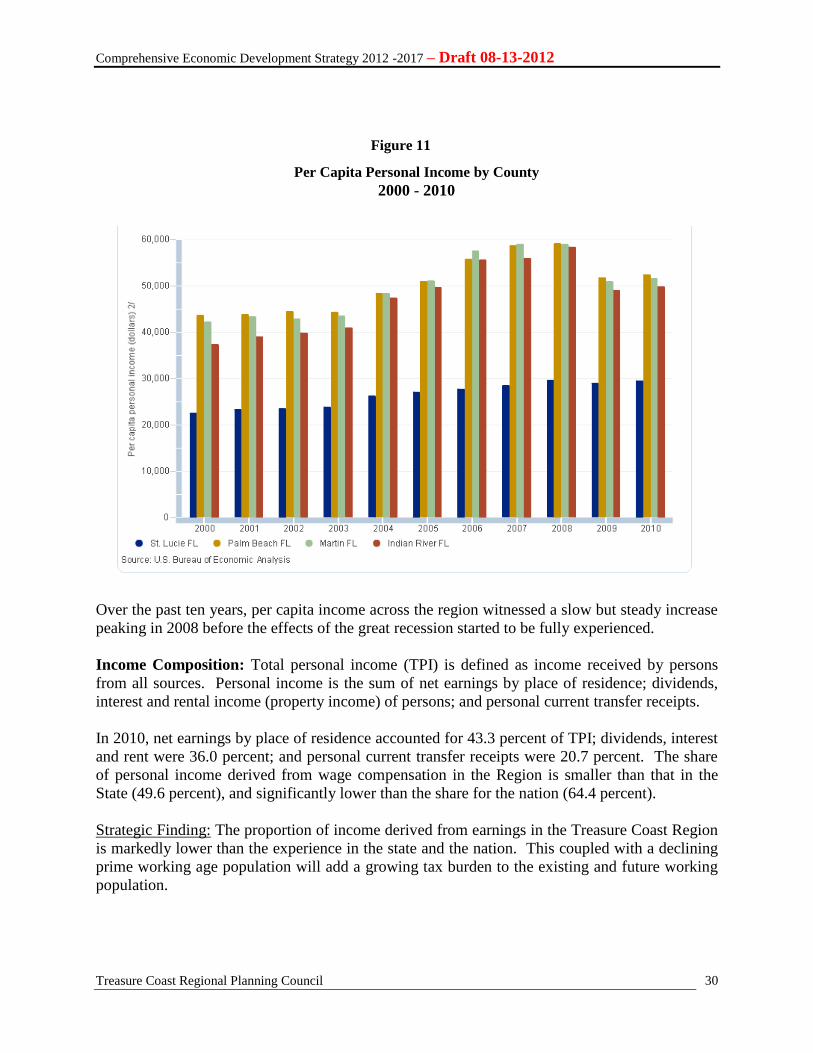

Over the past ten years, per capita income across the region witnessed a slow but steady increase

peaking in 2008 before the effects of the great recession started to be fully experienced.

Income Composition: Total personal income (TPI) is defined as income received by persons

from all sources. Personal income is the sum of net earnings by place of residence; dividends,

interest and rental income (property income) of persons; and personal current transfer receipts.

In 2010, net earnings by place of residence accounted for 43.3 percent of TPI; dividends, interest

and rent were 36.0 percent; and personal current transfer receipts were 20.7 percent. The share

of personal income derived from wage compensation in the Region is smaller than that in the

State (49.6 percent), and significantly lower than the share for the nation (64.4 percent).

Strategic Finding: The proportion of income derived from earnings in the Treasure Coast Region

is markedly lower than the experience in the state and the nation. This coupled with a declining

prime working age population will add a growing tax burden to the existing and future working

population.

Per Capita Personal Income by County

2000 - 2010

Figure 11

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

31

d. Industry Trends

Fastest Growing Industries

Over the next eight years (2011-2019), the Florida Department of Economic Opportunity

projects an average annual growth of employment across all industries in the Treasure Coast

Region of approximately 1.8 percent. This rate of growth is higher than the projected rate of

growth of population (1.1 percent) over the same time period.

Two dominant features should be noted in the illustration of the region’s fastest growing

industries: they tend to be concentrated in the services and retail trade sectors of the economy

and they are strongly correlated to population growth. Most of the industries represented in

Figure 12 are also those with average wages lower than the average annual regional wage of

$43,300.

Strategic Finding: The fastest-growing industries in the Treasure Coast are those which are

strongly correlated to projected population growth. This pattern underscores the prevailing

tendency of the Treasure Coast Region to continue to experience high employment growth in

relatively low wage industries. Except for Professional, Scientific and Technical Services and

perhaps Specialty Trade Contractors, there is an over-representation of relatively low wage

industries projected in the future.

Fastest-Growing Industries

2011-2019

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00%

Construction of Buildings

Specialty Trade Contractors

Professional, Scientific, and Technical Services

Rental and Leasing Services

Furniture and Home Furnishings Stores

Ambulatory Health Care Services

Nonmetallic Mineral Product Manufacturing

Waste Management and Remediation Service

Transportation Equipment Manufacturing

Building Material and Garden Supply Stores

Management of Companies and Enterprises

Merchant Wholesalers, Nondurable Goods

Wholesale Electronic Markets and Agents and Brokers

Real Estate

Warehousing and Storage

Fabricated Metal Product Manufacturing

Heavy and Civil Engineering Construction

Performing Arts, Spectator Sports, and Related

Publishing Industries

Motion Picture and Sound Recording Industries

Ind

us

try

Annual Change (%)

Figure 12

Source: Florida Department of Economic Opportunity, Employment Projections Data. 20

February 2012. Available at http://www.floridajobs.org/labor-market-information/data-

center/statistical-programs/employment-projections, Accessed February 20, 2012.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

32

Workforce Development Trends

One of the primary means of enhancing the innovative capacity of the Region is to ensure its

workforce has the requisite skills and knowledge base to work in the various targeted industry

clusters and to be adaptable to changing economic opportunities. The Region’s two workforce

development boards – Workforce Alliance (Region 21) and Workforce Solutions (Region 20)

closely monitor the local economy and work closely with local economic development agencies

to identify changes in industry growth and skill demands and make the necessary adjustments to

programs and services to continue meeting the needs of employers and jobseekers.

Through their partnerships with educational and economic development organizations, the

workforce boards ensure that the workforce services provided are consistent with the economic

development goals of the region and workforce funding sources are used to support the

recruitment and training needs outlined in local economic development projects. Their

partnerships with the Region’s varied educational institutions assist in developing a pipeline of

future workers with the requisite skills needed to adapt to a changing global marketplace.

In its publication, State Workforce

Investment Plan 2011-2012 Workforce

Florida, Inc. discusses the State’s skills

gaps and makes the argument that to

…Florida employers have indicated that basic

interpersonal and critical thinking skills are the biggest

gaps in the current workforce.

State Workforce Investment Plan 2011-2012

Workforce Florida, Inc.

Industries Gaining the Most New Jobs

2011-2019

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800

Ambulatory Health Care ServicesProfessional, Scientific, and Technical

Food Services and Drinking PlacesAdministrative and Support Services

Specialty Trade ContractorsLocal Government

Nursing and Residential Care FacilitiesConstruction of Buildings

Real EstateMerchant Wholesalers, Durable Goods

Management of Companies and EnterprisesAmusement, Gambling, and Recreation

Social AssistanceGeneral Merchandise Stores

Building Material and Garden Supply StoresMembership Associations and

Clothing and Clothing Accessories StoresMerchant Wholesalers, Nondurable Goods

Educational ServicesAccommodation

Annual Change (Jobs)

Figure 13

Source: Florida Department of Economic Opportunity, Employment Projections Data. 20

February 2012. Available at http://www.floridajobs.org/labor-market-information/data-

center/statistical-programs/employment-projections, Accessed February 20, 2012.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

33

compete in the national and global economies workers need basic skills like reading, writing,

math, speaking and listening. Additionally, thinking skills such as creativity, logical reasoning,

decision-making, problem-solving and visualization will need to be incorporated in the

curriculum throughout Florida’s educational system. Armed with these sets of skills combined

with technical and computer proficiency will help to assure Florida’s ability to compete in the

global marketplace.

In this region, the life sciences industry is extremely broad in scope and encompasses basic and

applied research and development, medical device design and manufacturing, medical testing

and diagnostics, pharmaceutical research and manufacturing, marine science, environmental

monitoring and testing, biohazard abatement, veterinary research and health care services.

Workers with specific science-based skills sets are needed, as are support personnel with skills in

marketing, finance, human resources, security, information technology and bioinformatics. The

life sciences industry also requires services and suppliers of equipment, chemicals, contract

research, business management and financial services.

Strategic Finding: Building a talented and creative regional workforce requires close cooperation

between the business, education and economic development communities. These partnerships

need to be strengthened and supported to enable the workforce development boards to develop a

pipeline of future workers and to upgrade the skills of the existing workforce. Helping existing

and future workers develop the skill sets required for future jobs, especially in the emerging life

sciences and research and development clusters will help the Region develop its innovation

economy.

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

34

PART II: SUSTAINABILITY

a. Overview

Economic sustainability is closely tied to the concept of creating livable regions. Livable regions

are comprised of vibrant communities that are diverse, safe and prosperous. A livable region

should offer its residents a wide variety of choices to live, work, play and visit. These choices

will include urban, suburban and rural living options; a wide range of quality employment

options and locations; high quality schooling, dynamic artistic and cultural and environmental

amenities with a true quality of place.

This section frames the concept of economic sustainability through a discussion of the

importance of qualify of life/place considerations, the importance of having well developed

infrastructure systems, an understanding of how climate change may affect the Region’s

economy and the necessity to preserve and enhance the Region’s natural environment.

b. Quality of Life, Quality of Place and Economic Development

Increasingly, economic activity is centering in metropolitan area across the country and across

the world. Place factors prominently in business and industry location decisions as does quality

of life considerations. The Treasure Coast Region as a whole is perceived as having an excellent

quality of life. While this topic is subjective to a certain degree, there are commonly used criteria

to describe quality of life components. These include the natural environment, recreation,

culture, safety, education, housing and health services.

The large amounts of open space, strong efforts to expand educational and cultural facilities,

public safety programs, and increasing health-related services, suggest that maintaining the

quality of life is a high priority in the Region. The perception of an area having a good quality of

life is critical for many businesses when determining whether or not to invest in an area. Studies

indicate that cultural and natural assets form the basis for economic development in

communities. The greatest attractions for economic growth are quality of life, natural

environment, historic legacy and cultural context. These qualities and the character of a city

influence a wide range of business and residential location decisions and can serve as either a

dampener or catalyst for tourism and other economic and cultural activities. In relocation

decisions, businesses place increasingly more value on quality of life considerations. Continuous

investment in infrastructure as well as in various amenities (museums, theaters, sports,

entertainment, recreation) are necessary to maintain a competitive posture. The arts, culture, and

historic resources are big factors in a city’s quality of life and provide it with something more

tangible - a leveraging tool. If a community wants to attract capital and investment, it must be

prepared to call attention to its diversity, identity, and individuality. In addition, a continued

effort should be made to maintain, improve and/or expand these amenities to sustain a quality of

life that is enjoyed by the Region's residents and found attractive to outside businesses.

The Region’s Strategic Regional Policy Plan suggests that renovating and creating new locations

for economic development and businesses in existing cities, towns, and villages should be of

highest priority. While it is likely that land outside these central locations will be sought for

Comprehensive Economic Development Strategy 2012 -2017 – Draft 08-13-2012

Treasure Coast Regional Planning Council

35