TRAVEL AND TOURISM - ICRA Lanka Limited

51

Prepared by And IMaCS Research & Analytics TRAVEL AND TOURISM September 2011 Industry Report on Sri Lanka

Transcript of TRAVEL AND TOURISM - ICRA Lanka Limited

i

Prepared by

And

IMaC

S R

ese

arc

h &

An

aly

tics

TRAVEL AND TOURISM

September 2011

Ind

ustry

Rep

ort o

n S

ri Lan

ka

ii

Contacts:

W Don Barnabas,

Managing Director/CEO

ICRA Lanka Limited,

#10-02, East Tower,

World Trade Center,

Colombo 01,

Sri Lanka

Telephone: +94 11 4339907

Mobile: + 94 773417517

Fax: +94 11 2333307

Email: [email protected]

www.icralanka.com

V Sriram

Chief General Manager

ICRA Management Consulting Services Limited

India

Telephone: +91 44 4596 4329

Mobile: +91 98400 88273

Email: [email protected]

www.imacs.in

Disclaimer This report is a joint initiative of ICRA Lanka and IMaCS. All information contained in this

document has been obtained from sources believed by them to be accurate and reliable.

Although reasonable care has been taken to ensure that the information herein is true, such

information is provided ‘as is’ without any warranty of any kind, and neither ICRA Lanka nor

IMaCS in particular, makes any representation or warranty, express or implied, as to the

accuracy, timeliness or completeness of any such information. All information contained herein

must be construed solely as statements of opinion, and neither ICRA Lanka nor IMaCS or any

other Group ICRA Company shall be liable for any losses incurred by users from any use of this

document or its contents in any manner. Opinions expressed in this document are not the

opinions of our holding company, ICRA, or ICRA Lanka Limited (ICRA Lanka) and should not be

construed as any indication of credit rating or grading of ICRA or ICRA Lanka for any instruments

that have been issued or are to be issued by any entity.

iii

TABLE OF CONTENTS

EXECUTIVE SUMMARY ............................................................................................................... 1

SRI LANKA TRAVEL AND TOURISM—SWOT ANALYSIS.................................................................. 3 GLOBAL SCENARIO ............................................................................................................................ 4 TOURIST ARRIVALS ................................................................................................................................ 4 RECENT TRENDS AND SHORT-TERM OUTLOOK ........................................................................................... 7 MAJOR TOURIST DESTINATIONS .............................................................................................................. 7 WORLD TOURIST RECEIPTS ..................................................................................................................... 9

SRI LANKAN TOURISM INDUSTRY ............................................................................................. 10 OVERVIEW OF TOURIST INFLOWS ........................................................................................................... 13 SEASONALITY ...................................................................................................................................... 15 CONTRIBUTION TO GDP ....................................................................................................................... 16 TOURISM – IMPORTANT SOURCE OF FOREIGN EXCHANGE .......................................................................... 17 EMPLOYMENT IN TOURISM INDUSTRY..................................................................................................... 18 INBOUND TOURISM MARKET ................................................................................................................ 20 TOURIST PROFILE ................................................................................................................................ 23 DURATION OF STAY ............................................................................................................................. 24 TRAVEL AND TOURISM ACCOMMODATION .............................................................................................. 25 KEY MARKET TRENDS .......................................................................................................................... 32 MAJOR PROJECTS PLANNED .................................................................................................................. 33 PLANNED TARGETS .............................................................................................................................. 35 MAHINDA CHINTANA ........................................................................................................................... 35

TRANSPORT INFRASTRUCTURE ................................................................................................. 36 CIVIL AVIATION ................................................................................................................................... 36 RAIL TRANSPORTATION ........................................................................................................................ 39 ROAD TRANSPORTATION ...................................................................................................................... 39

GOVERNMENT AGENCIES ......................................................................................................... 42

ECONOMIC OUTLOOK .............................................................................................................. 42

TRAVEL AND TOURISM OUTLOOK ............................................................................................. 45

iv

TABLE OF EXHIBITS

Exhibit 1: Growth in World GDP and Tourist Arrivals ........................................................................... 5 Exhibit 2: World - International Tourist Arrivals and Growth .............................................................. 5 Exhibit 3: Regional Tourist Flows .......................................................................................................... 6 Exhibit 4: Major Tourist Destinations ................................................................................................... 8 Exhibit 5: Tourist Destinations in Asia and the Pacific ......................................................................... 9 Exhibit 6: World Tourist Receipts ....................................................................................................... 10 Exhibit 7: Sri Lanka - Growth in International Tourist Arrivals ........................................................... 13 Exhibit 8: Sri Lanka - International Tourist Arrivals and Growth ........................................................ 14 Exhibit 10: Share of Tourist Arrivals by Month................................................................................... 15 Exhibit 9: Monthly International Tourist Arrivals into Sri Lanka ........................................................ 15 Exhibit 11: Travel and Tourism Revenues and Contribution to GDP .................................................. 16 Exhibit 12: GDP from Hotels and Restaurants .................................................................................... 16 Exhibit 13: International Tourism Receipts ........................................................................................ 17 Exhibit 14: Domestic Travel and Tourism Spending ........................................................................... 17 Exhibit 15: Sri Lanka - Growth in Real GDP and Domestic Travel and Tourism Spending .................. 18 Exhibit 17: Direct Employment in Sri Lanka’s Tourism Industry ........................................................ 19 Exhibit 16: Sri Lanka - Employment in Tourism Industry .................................................................... 19 Exhibit 18: Share of Direct and Indirect Employment in Travel and Tourism Industry ..................... 20 Exhibit 19: Tourist Arrivals by Region and Major Countries ............................................................... 21 Exhibit 20: Tourist Arrivals by Region and Major Countries - 1st Half ............................................... 22 Exhibit 21: Purpose of Visit (per cent) ................................................................................................ 23 Exhibit 22: Number of Visitors from India for Various Purposes ....................................................... 23 Exhibit 23: Period of Stay (Percentage Distribution) .......................................................................... 24 Exhibit 24: Duration of Stay, Tourist Nights by Major Countries and Regions ................................... 25 Exhibit 25: Accommodation Availability ............................................................................................. 26 Exhibit 26: Trends in Occupancy ........................................................................................................ 26 Exhibit 27: Trends in Guest Nights in Hotels and Supplementary Accommodations ........................ 27 Exhibit 28: Annual Occupancy Rate in Sri Lanka’s Hotels ................................................................... 27 Exhibit 29: Regional Accommodation Capacity .................................................................................. 28 Exhibit 30: Occupancy Rates .............................................................................................................. 28 Exhibit 31: Trends in Guest Nights by Tourist Destinations ............................................................... 29 Exhibit 32: Share of Various Accommodation Categories .................................................................. 30 Exhibit 33: Share of Domestic Travellers in Total Guest Nights of Hotels .......................................... 31 Exhibit 34: Distribution of Domestic and Foreign Travellers in Total Guest Nights .......................... 31 Exhibit 35: Trends in Guest Nights by Hotel Type .............................................................................. 32 Exhibit 36: Percentage Distribution of International Tourist Arrivals ................................................ 37 Exhibit 37: International Tourist Arrivals by Airlines .......................................................................... 38 Exhibit 38: Sri Lanka Airlines - Inbound Passengers Carried from Various Regions .......................... 38 Exhibit 39: Key Surface Transport Statistics of Sri Lanka.................................................................... 40 Exhibit 40: Road Network in Sri Lanka................................................................................................ 40 Exhibit 41: Road Network by Province in Sri Lanka in 2010 ............................................................... 41 Exhibit 42: Summary Economic Data on Sri Lanka’s Economy ........................................................... 43 Exhibit 43: Estimates for Sri Lanka ..................................................................................................... 44 Exhibit 44: World Bank `Doing Business 2011’ Country Table for Sri Lanka ...................................... 45

Travel and Tourism Industry in Sri Lanka 1

EXECUTIVE SUMMARY With over 1,600 km of coastline, Sri Lanka is well known for its tropical beach resorts and related

sports such as water sports, deep-sea fishing, underwater photography, scuba diving at

shipwrecks and coral reefs, and whale watching. Other major tourist attractions include ancient

heritage sites and forest resorts in Wild Life Sanctuaries.

There has been a significant improvement in Sri Lanka’s tourism with the return of peace to the

island nation, following the May 2009 declaration of conclusive victory over insurgent forces.

Since the 1980s, Sri Lanka’s tourism was adversely affected because of the ethnic conflict. Tourist

arrivals shrunk from 407,230 in 19821 to 302,000 in 1996. Since then, the tourism industry picked

up with tourist arrivals increasing to 566,200 in 2004, following the ceasefire between the Sri

Lankan military and the rebel Tamil forces in 2002, but there was a substantial decline in the later

years. In 2005, there was an adverse effect because of decline in global tourists after the Asian

tsunami of December 2004 combined with the break-down of the cease fire agreement reached

in 2002. By 2008, tourist arrivals were down to about 438,000. There was a consequent decline in

employment as well in this sector, from 60,516 in 2007 to 51,306 in 2008.

Over the course of 2010, countries in Europe and North America relaxed their advisories against

travel to Sri Lanka. In 2010, international tourist arrivals to Sri Lanka increased by a significant 46

percent over 2009 to 654,477 and hotel occupancy rates increased from 48.4 percent in 2009 to a

record 70.1 percent. Domestic travel and tourism spending by Sri Lankan citizens increased 6.5

percent, in real terms, contributing to LKR 134.6 billion, compared with a decline of 5.3 percent in

2009. These trends have continued into the first half of 2011 with a 37 percent annual growth in

international tourist arrivals.

Tourism is among the most important source of foreign exchange for Sri Lankan economy. It

accounted for 2.6 percent of foreign exchange receipts in 2009. Foreign exchange earnings from

tourism increased 49.9 percent in 2010 amounting to LKR 56.24 billion, as compared to an

increase of 1.1 percent in 2009. According to the Sri Lanka Tourism Development Agency (SLTDA),

the total number of persons employed directly in the tourism sector increased 1.5 percent, in

2009 to 52,071 persons, compared with a decline of 15.2 percent in 2008.

With the restoration of peace in the country and the promise of global economic growth, the

stage is set for several years of strong growth in Sri Lanka’s tourism arrivals and tourist revenues.

We estimate International tourist arrivals to Sri Lanka to increase 15 percent in 2011 to reach

750,000. Domestic travel and tourism spending is also expected to increase in 2011 by nearly 7

percent. Estimates by the World Travel & Tourism Council (WTTC) indicate that the Sri Lankan

1 In this document, FY means Fiscal year denoting April-March. Thus, FY2011 or 2010-11 means the period April 2010-

March 2011. Statement of year, e.g. 2010 and so on, without a prefix FY means calendar year from January-December.

Thus, 2010 or CY2010 means period January-December 2010, and so on. Q1FY (year) means quarter April-June; and so

on and 1Q (year) means quarter January-March. Thus, Q1FY2011 means April-June 2010, and so on. 1Q2010 means

January-March 2010, and so on. H1FY (year) means period April-September, e.g. H1FY2011 means April-September

2010, and so on. 1H (year) means January-June, e.g. 1H2010 means January-June 2010, and so on.

Travel and Tourism Industry in Sri Lanka 2

travel and tourism industry is expected to generate 210,000 jobs directly in 2011 (2.7 percent of

total employment). By 2015, T&T is forecast to generate 225,000 jobs, an increase of 2.3 percent

per annum over the period from 2011-15.

Sri Lanka primarily attracts tourists from India (19 percent of international tourist arrivals in

2010), UK (16 percent), Germany (7 percent), Maldives (6 percent), and Australia (5 percent).

India’s real gross domestic product (GDP) has increased at an annual average rate of 8.4 percent

during the period, FY2007 to FY2011. With real GDP growth forecast to increase at an annual rate

of over 8 percent during the period, FY2011 to FY2015 and increasing disposable incomes, the

number of Indians travelling overseas is estimated to double every decade creating strong

demand for recreational tourism, meetings, incentives and conferences. Because of its proximity

to India, Sri Lanka is better positioned to compete for this market than many other destinations

in South Asia and South-East Asia. Both the Sri Lankan Government and the country’s private

sector are aware of this strategic advantage and have begun to jointly invest in products and

promotional efforts geared to attract Indian tourists to circuits such as a `Ramayana’ sites

featured in the ancient Hindu epic. Further, with a more secure environment, Sri Lanka is also

expected to attract more tourists from North America, Asia-Pacific and Western Europe.

The Sri Lankan Government is prioritising tourism and has started taking a number of steps to

strengthen the sector. The Ministry of Economic Development in its report titled: `Tourism

Development Strategy 2011-16’, has identified the following key objectives:

Double hotel room capacity from around 23,000 rooms at present to 45,000 by 2016

Accommodate 2.5 million annual arrivals as compared with over 650,000 in 2010

Increase foreign exchange earnings from US$501 million in 2010 to US$2.75 billion in 2016

Increase tourism employment to 500,000 by 2016

Attract US$3 billion in Foreign Direct Investment (FDI) within the next five years

Position the country as one of the most attractive destination in the world

To realise its tourism potential however, Sri Lanka will have to significantly improve its

international air and domestic surface linkages and, invest substantially in improving domestic

transport, energy and telecom infrastructure.

The development of an island-wide road network at national, provincial and rural level is

essential to ensure safe and quick connectivity to the various tourist destinations. Recent Plan

projections indicate that public investment in road sector is expected to gather further

momentum with an investment of LKR 128 billion in 2011. It is planned to be increased to LKR

174 billion by 2013 and, thereafter, to be maintained at LKR 175-200 billion, annually.

The country’s overall investment requirements are not expected to be met through public funds

only. There is also an urgent need to attract both domestic and foreign investment to

substantially improve hotel accommodation capacity and quality. However, there is a perception

that the Government is sending some potentially conflicting signals about the role of the private

sector in economic development.

Travel and Tourism Industry in Sri Lanka 3

Sri Lanka has suffered from overlapping authorities from multiple government agencies, and in

the past projects stalled by litigation despite having government approvals. Investment approval

procedure needs to be accelerated, and speedy approval and procedures will have to be ensured

to accelerate the implementation of proposals and reduce start-up times. The government has

started a comprehensive process to address legal and bureaucratic barriers to investment and

the high cost of doing business in Sri Lanka. Increased transparency and improved governance

could also bolster market confidence and lead to higher investment.

SRI LANKA TRAVEL AND TOURISM—SWOT ANALYSIS

Strengths Long (1600 km) and beautiful coastline along the Indian Ocean and a

tropical climate

Significant long-term government support for the industry

Cultural orientation, religious values, respect for people and traditions,

and sacred sites

Low-cost tourist destination with proximity to Indian sub-continent

and South-East Asia

Weaknesses Limited international air connectivity

Inadequate in transport and tourism infrastructure

Overlapping authorities and excessive regulation from multiple

government agencies

Past projects stalled by litigation despite having government approvals

Economy severely impacted due to years of internal strife

Low competitiveness rankings compared to South East Asian tourism

destinations

Opportunities Focus areas: beach tourism, cultural tourism, tea tourism, Eco-tourism,

religious tourism

Proximity to India and cultural affinity with Southern and Eastern India

Potential to offer quality and exclusivity based packages owing to small

size - an offering not always available in mass-market package

destinations.

Onset of peace to attract greater numbers of tourists

Growing political and economic relationship with China

Planned new and expansion projects by international hotel chains

Major infrastructure investment programs planned for the Eastern and

Northern regions

Recent pledge by the World Bank for US$125 million in funding for

projects promoting: tourism, small and medium-sized enterprise

development, and local authority capabilities in the Northern and

Eastern regions.

Threats High Fiscal deficits (with planned expenditure reduction by the

Government) may constrain infrastructure spending

Limited air connectivity to European and American destinations could

Travel and Tourism Industry in Sri Lanka 4

result in Sri Lanka becoming the place for budget travellers from India

and South Asia

Competition from neighbouring countries

Adverse international publicity if the rehabilitation of the population in

the North is delayed

GLOBAL SCENARIO

Over recent decades, travel and tourism have been large contributors to the world economy.

International tourism has been growing at a slightly faster pace than the world economy and this

seems likely to continue in the long-term. Tourism plays a crucial role in supporting economic

growth and development, sustaining employment and generating foreign currency receipts.

The travel and tourism industry is highly labour intensive and a significant source of employment.

According to the International Labour Organization (ILO), it is among the world‘s top creators of

jobs requiring varying degrees of skills and allows for quick entry into the workforce for youth,

women and migrant workers. With regard to the indirect job creation, one job in the core

industry indirectly generates roughly 1.5 additional jobs in the related economy. In 2010, the

sector is expected to account for more than 235 million jobs, equivalent to about 8 per cent of

the overall number of jobs.

Tourist Arrivals

Over the last 20 years, international tourism – as measured by the number of tourist arrivals –

has mirrored the four downturns in the world economy, measured by global GDP, which occurred

in 1991, 1998, 2001 and 2008. During the past decade, the events of September 11, 2001

accentuated the fall in tourism at the end of that year. Despite the ensuing economic recovery,

global tourism suffered another setback in 2003, because of various factors specific to tourism

such as terrorist threats, the outbreak of the Iraq war, the Severe Acute Respiratory Syndrome

(SARS) crisis, and the spread of the avian flu in Asia and the Pacific. However, the shocks that

tourism experienced over the period had effects that were very short-lived and were rapidly

absorbed. Overall, international tourism growth was far more robust than economic growth. For

the period from 1988 to 2008, the average annual growth rate in tourist arrivals was 4.6 percent,

compared to 3.4 percent for global GDP.

Travel and Tourism Industry in Sri Lanka 5

Sources: World Tourist Organisation (WTO), International Monetary Fund (IMF), IMaCS Analysis

The global economic recession, aggravated by the uncertainty around the H1N1 influenza

pandemic, resulted in world tourist arrivals for business, leisure and other purposes declining 3.8

percent in 2009 to 882 million. Tourist arrivals had previously declined 1.8 percent in 2003,

followed by generally strong growth during the period, 2004-07. This was followed by another

slowdown in 2008.

Sources: WTO, IMaCS Analysis

440 443480 496

520541

575599 617

640687 687

707 695

765798

852

901 917882

940

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

200

300

400

500

600

700

800

900

1,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Arrivals-million (LS) Growth (RS)

Exhibit 1: Growth in World GDP and Tourist Arrivals

Exhibit 2: World - International Tourist Arrivals and Growth

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011F

GDP Tourist Arrivals

Travel and Tourism Industry in Sri Lanka 6

World tourism was variably impacted by the financial and economic crisis that hit the world

economy in 2008 and 2009.Tourism flows started to decline in the second half of 2008, and the

decline deepened at the beginning of 2009. International tourism was affected more than

domestic tourism, business tourism more than leisure tourism, hotels more than other types of

accommodation, and air transport more than other types of transport.

Following 14 months of decline, growth returned in the last quarter of 2009. The 2 percent

upswing registered in the last quarter of 2009 contrasted with the annual decline of 10 percent, 7

percent and 2 percent in the first three quarters of 2009. By 2010, worldwide, international

tourist arrivals increased 6.6 percent to 940 million. Asia, the Pacific region and the Middle East

led the recovery and were among the strongest growing regions in 2010.

A vast majority of destinations reported positive and, often, double-digit increases. Growth

varied across regions: at 8.3 percent in emerging economies, but at a lower rate of 5.1 percent in

advanced economies. Tourist arrivals in Africa increased in 2009 and 2010, and the Middle East

returned to double digit growth. Tourist flows to the Americas increased 6.5 percent in 2010,

compared with a decline of 5.6 percent in 2009. Growth in Europe also resumed, albeit at a lower

rate.

Exhibit 3: Regional Tourist Flows

Million No. Growth (percent)

2007 2008 2009 2010

2009 2010 2001-

05

2006-

10

Europe 485.4 485.2 461.5 476.6 -4.9 3.3 2.6 1.6

Northern Europe 58.1 60.8 57.7 58.1 -5.1 0.7 5.6 0.3

Western Europe 153.9 153.2 148.6 153.7 -3.0 3.4 0.3 1.6

Central/Eastern Europe 96.6 100.0 90.2 95.1 -9.8 5.4 -34.3 62.1

Southern/Mediterranean

Europe 176.8 171.2 165.1 169.7 -3.6 2.8 2.8 2.1

Asia and the Pacific 182.0 184.1 180.9 203.8 -1.7 12.7 6.9 5.8

North-East Asia 101.0 100.9 98.0 111.6 -2.9 13.9 8.1 5.4

South-East Asia 59.7 61.8 62.1 69.6 0.5 12.1 6.1 7.5

Oceania 11.2 11.1 10.9 11.6 -1.8 6.4 2.8 1.1

South Asia 10.1 10.3 9.9 11.1 -3.9 12.1 5.8 6.5

Americas 143.9 147.8 140.6 149.8 -4.9 6.5 0.8 2.4

North America 95.3 97.7 92.2 98.2 -5.6 6.5 -0.4 1.8

Caribbean 19.8 20.1 19.5 20.1 -3.0 3.1 1.9 1.3

Central America 7.8 8.2 7.6 7.9 -7.3 3.9 7.9 4.6

South America 21.0 21.8 21.3 23.5 -2.3 10.3 3.6 5.1

Africa 43.1 44.4 46.0 49.4 3.6 7.4 6.0 6.9

North Africa 16.3 17.1 17.6 18.7 2.9 6.2 6.4 6.1

Sub-Saharan Africa 26.9 27.2 28.4 30.7 4.4 8.1 5.8 7.4

Middle East 46.7 55.2 52.9 60.3 -4.2 14.0 8.5 10.7

Advanced economies 496.0 495.0 474.0 498.0 -4.2 5.1 1.7 1.9

Emerging economies 405.0 421.0 408.0 442.0 -3.1 8.3 6.1 5.1

Total 901.0 917.0 882.0 940.0 -3.8 6.6 3.4 3.3

Sources: WTO, IMaCS Analysis

Travel and Tourism Industry in Sri Lanka 7

Recent Trends and Short -Term Out look

Recovering from the recent slowdown in world economic growth, international tourist arrivals

grew by 4.5 percent in the first four months of 2011. According to the latest issue of the UNWTO

World Tourism Barometer, growth was positive in all regions except the Middle East. Some sub-

regions achieved double-digit growth: South America (17 percent), South Asia (14 percent) and

South-East Asia (10 percent).

Between January and April 2011, tourism arrivals increased 4.5 percent to 268 million. April 2011

was the strongest month with an estimated increase of 6 percent after weaker growth in

February and March 2011, both, at around 3 per cent. This reflected upon a late Easter holiday

and contrasted with a weaker April of 2010 when European airspace was closed for nearly a week

due to the ash cloud, following the eruption of a volcano in Iceland.

UNWTO expects demand to recover towards the end of 2011 in destinations currently facing

difficulties. As the peak tourist season gets underway in the Northern hemisphere, short-term

prospects remain positive. This is reflected in the UNWTO Confidence Index, a short-term outlook

based on consultations with over 350 experts worldwide. The index remains largely optimistic for

the period May-August 2011. There are however, marked differences in the confidence levels for

different regions of the world, with experts in the Americas and Europe anticipating the best

outcomes. Confidence remains high in Africa, but lower than that expected in Asia and the Pacific

region. Experts in the Middle East are the least optimistic. UNWTO has forecast international

tourist arrivals to increase 4-5 percent in 2011, slightly above the long-term average and in line

with previous assessments. Recent adverse geo-political developments in the Middle East, North

Africa and Japan are not expected to, significantly, alter the global forecast.

Major Tourist Destinat ions

Of the 940 million international tourist arrivals in 2010, France was the top tourist destination

and accounted for 8.1 percent of world tourist arrivals. The other major destinations were US (2nd

position), China, Spain (4th position) and Italy (5th position). Among the top 10 destinations, five

are in Europe, two in North America and three in Asia (including Turkey). The most significant

change among the top 10 destinations in 2010 was the rise of China to third position, displacing

Spain and having overtaken both the UK and Italy in the past few years.

In terms of receipts also China moved up to fourth position with a growth of over 15 per cent,

overtaking Italy. Hong Kong moved into the top 10 and reached the ninth position. France

continued in the third position, while US ranked first in receipts and second in arrivals. Spain

maintained its position as the second highest earner worldwide and the first in Europe. Italy

ranked fifth, Germany sixth and the UK was seventh. Turkey occupied the tenth position in

receipts.

Travel and Tourism Industry in Sri Lanka 8

Exhibit 4: Major Tourist Destinations Tourist Arrivals

(Million No.)

Receipts

(US$ million)

2007 2008 2009 2010

2007 2008 2009 2010

France 80.9 79.2 76.8 76.8 62.9 67.4 59.4

US 56.0 57.9 54.9 59.7 145.2 166.4 147.6 163.9

China 54.7 53.0 50.9 55.7 41.1 44.1 42.6

Spain 58.7 57.2 52.2 52.7 65.0 70.4 59.5 58.8

Italy 43.7 42.7 43.2 43.6 46.1 48.8 41.9 40.0

UK 30.9 30.1 28.2 28.1 48.2 46.3 38.6 39.8

Turkey 22.2 25.0 25.5 27.0 20.7 25.0 24.6 24.7

Germany 24.4 24.9 24.2 26.9 49.3 53.4 47.5 49.1

Malaysia 21.0 22.1 23.6 24.6 17.9 18.6 17.2

Mexico 21.4 22.6 21.5 22.4 14.0 14.6 12.3 12.5

Sources: WTO, IMaCS Analysis

Countries in the Asia-Pacific attracted 204 million tourists in 2010. The key destinations were in

North-East Asia, South-East Asia and Oceania. The South Asian region attracted 11.1 million

tourists in 2010, with India accounting for 5.58 million, while Sri Lanka attracted less than a

million tourists. Most destinations in the Asia-Pacific posted double-digit growth because of

strong development of local economies. Accordingly, receipts grew by 13 percent in real terms to

US$249 billion.

North-East Asia had the highest growth in tourist arrivals (over 13.9 percent) in 2010, with

double-digit increases for virtually all destinations. At 9.4 per cent, growth in China was below

average, but still represented around a quarter of the additional arrivals in the whole region.

Arrivals in South-East Asia, the only sub-region to show positive results in 2009, were further up

12.1 percent in 2010. Destinations such as Vietnam (35 percent), Singapore (22 percent),

Cambodia (17 percent), Philippines (17 percent), Thailand (12 percent) and Indonesia (11

percent) all recorded double-digit growth after a weak 2009.

International arrivals in South Asia increased 12.1 percent, with particularly strong growth in Sri

Lanka (46 percent) and Maldives (21 percent). At 8 per cent, growth in India’s tourist arrivals was

comparatively moderate.

Arrivals growth in Oceania (6 percent) was just below the world average with leading and more

mature destinations such as Australia (5 percent) and New Zealand (3 percent) showing

moderate growth after a flat 2009.

Travel and Tourism Industry in Sri Lanka 9

Exhibit 5: Tourist Destinations in Asia and the Pacific Tourist Arrivals

(Million No.)

Receipts

(US$ million)

2007 2008 2009 2010

2007 2008 2009 2010

Australia 5.64 5.59 5.58 5.89 22.31 24.76 25.38 30.10

Cambodia 1.87 2.00 2.05 2.40 1.14 1.22 1.19 1.26

China 54.72 53.05 50.88 55.67 37.23 40.84 39.68 45.81

Fiji 0.54 0.59 0.54 0.63 0.50 0.55 0.42 -

Hong Kong (China) 17.15 17.32 16.93 20.09 13.75 15.30 16.45 22.95

India 5.08 5.28 5.17 5.58 10.73 11.83 11.14 14.16

Indonesia 5.51 6.23 6.32 7.00 5.35 7.38 5.60 6.98

Iran 2.22 2.03 - - 1.68 1.91 2.01 -

Japan 8.35 8.35 6.79 8.61 9.33 10.82 10.31 13.20

South Korea 6.45 6.89 7.82 8.80 6.14 9.77 9.82 9.77

Lao 1.14 1.30 1.24 - 0.23 0.28 0.27 -

Macao (China) 12.94 10.61 10.40 11.93 13.08 16.43 17.64 -

Malaysia 20.97 22.05 23.65 24.58 14.04 15.28 15.77 17.82

Maldives 0.68 0.68 0.66 0.79 0.60 0.66 0.61 0.71

New Zealand 2.47 2.46 2.46 2.53 5.44 5.04 4.59 4.86

Nepal 0.53 0.50 0.51 - 0.20 0.34 0.37 0.39

Pakistan 0.84 0.82 0.86 0.91 0.28 0.32 0.27 0.36

Philippines 3.09 3.14 3.02 3.52 4.93 2.50 2.33 2.78

Singapore 7.96 7.78 7.49 9.16 9.07 10.71 9.36 14.12

Sri Lanka 0.49 0.44 0.45 0.65 0.39 0.34 0.35 0.58

Taiwan 3.72 3.85 4.40 5.57 5.21 5.94 6.82 8.65

Thailand 14.46 14.58 14.15 15.84 16.67 18.17 15.66 19.76

Vietnam 4.23 4.24 3.75 5.05 3.75 3.93 3.05 4.45

Total 182.05 184.06 180.94 203.84 186.31 208.60 203.10 248.66

Sources: WTO, IMaCS Analysis

World Tourist Recei pts

International tourism receipts are estimated to have reached US$919 billion in 2010, up from

US$851 billion in 2009. Growth in international tourism receipts was estimated at 4.7 percent in

2010, measured in real terms (i.e., using local currencies at constant prices in order to adjust for

exchange rate fluctuations and inflation). Thus, the recovery in international tourism receipts (4.7

percent) still lags that of international arrivals (6.6 percent). This is typical in periods of recovery

following major shocks, when volume (arrivals) tends to recover faster than income (receipts)

because of higher competition to contain prices. Tourists also tend to travel closer to home and

for shorter periods of time.

Travel and Tourism Industry in Sri Lanka 10

Exhibit 6: World Tourist Receipts Growth in

Local Currency ( percent)

Receipts

(US$ billion)

Per Arrival

(US$)

2008 2009 2010 2009 2010 2009 2010

Europe -0.9 -6.7 -0.4 410.9 406.2 900 850

Northern Europe -2.5 -4.0 -1.3 58.6 59.2 1,150 1.01

Western Europe -2.2 -7.1 1.5 143.8 142.0 980 920

Central/Eastern Europe 4.3 -8.0 -2.8 47.4 47.7 530 500

Southern/Mediterranean Europe -0.6 -6.9 -1.1 161.3 157.4 940 930

Asia and the Pacific 4.6 -0.7 12.8 203.1 248.7 1,120 1,220

North-East Asia 8.2 1.9 15.9 101.2 122.4 1,020 1,100

South-East Asia -0.8 -7.4 14.4 53.5 68.0 870 980

Oceania 3.2 5.3 -0.6 33.5 39.4 3,080 3,400

South Asia 7.7 -4.9 16.5 14.9 18.9 1,550 1,710

Americas 4.9 -9.9 5.0 166.2 182.2 1,170 1,220

North America 6.9 -124 6.2 119.2 131.2 1,290 1,340

Caribbean -3.2 -5.3 2.1 22.6 23.6 1,140 1,180

Central America 0.3 -3.4 4.1 6.1 6.8 770 850

South America 3.1 -0.3 1.2 18.3 20.6 850 880

Africa -2.5 -4.1 4.0 28.8 31.6 630 640

North Africa -3.9 -4.7 3.6 9.9 10.0 570 540

Sub-Saharan Africa -1.8 -3.8 4.2 18.9 21.6 670 710

Middle East 5.5 0.8 14.4 42.0 50.3 780 830

Advanced economies 1.8 -6.5 4.4 547 580 1,160 1,160

Emerging economies 1.5 -3.8 5.1 304 339 740 770

Total 1.7 -5.6 4.7 851 919 970 980

Sources: WTO, IMaCS Analysis

SRI LANKAN TOURISM INDUSTRY

Sri Lanka is an island south of India with a land area of 65,610 square km (sq.km.). It had an

estimated population of 20.65 million in 2010 and annual population growth rate of 1 percent.

The Western Province has the highest population size and density, followed by the Central and

the Southern Provinces. The North Central Province has the biggest land area, followed by the

Eastern and Uva Provinces.

The country’s major tourist attractions include the following: island's beaches located in the

Southern and Eastern parts of the country, ancient heritage sites located in the interior of the

country, and lush green resorts located in the mountainous regions of the country and wild life

sanctuaries in Yala and Wilpathu.

Heritage Tourism

Sri Lanka has 49 sites classified as unique attractions, 91 as rare attractions and eight world

heritage sites. The eight heritage sites are:

Travel and Tourism Industry in Sri Lanka 11

1. Ancient City of Polonnaruwa

2. Ancient City of Sigiriya

3. Golden Temple of Dambulla

4. Old Town of Galle and its Fortifications

5. Sacred City of Anuradhapura

6. Sacred City of Kandy

7. Central Highlands of Sri Lanka

8. Sinharaja Forest Reserve

Source: Compiled by IMaCS

Beach Tourism

With over 1,600 km of coastlines, Sri Lanka is known to most tourists for its tropical beach

resorts. The South Western coast is best visited from November to April and the East coast from

April to September. Some popular beach spots on the South Western coast include

Ambalangoda, Hikkaduwa and Galle. The Eastern coastal region offers numerous opportunities

for water sports, deep-sea fishing, underwater photography, scuba diving at the shipwrecks and

coral reefs off the coast, and whale watching. Popular tourist towns with sandy beaches in East of

Sri Lanka include Trincomalee, Batticaloa, Kalkudah and Nilaveli.

Travel and Tourism Industry in Sri Lanka 12

Cultural Tourism

Sri Lanka has numerous magnificent, century-old monuments and cultural relics in a number of

ancient cities. Kandy, Anuradhapura and Polonnaruwa are known as the points of the `Cultural

Triangle’ of Sri Lanka. Within the triangle, Sigiriya is considered as the base of cultural tourism.

The most important archaeological and cultural site in Sigiriya is the rock fortress built in the 5th

Century AD by King Kasyappa to fend off a feared invasion. Situated atop a 200 metre high rock,

the fortress houses famous frescoes (rock paintings) on its gallery wall.

Other highlights of cultural tours in this area include the following:

Buddhist cave temples dating to the 1st Century AD and a gigantic recumbent image of the

Buddha carved out of rock in the town of Dambulla

A manmade reservoir called, `Parakrama Samudra’ located in the medieval Sri Lankan capital

of Polonnaurwa

Sacred Shri Maha Bodhi Tree in Anuradhapura.

It is claimed that the right branch of the Bodhi tree in Bodh Gaya in India under which the Buddha

attained enlightenment was brought to Sri Lanka in the 3rdcentury BC by Princess Sanghamitta,

the daughter of Emperor Ashoka. It was planted in Anuradhapura and is venerated to this day by

the Buddhists from many countries of the world. This is the oldest recorded tree in the world

whose exact age is known.

Hill and Mountain Tourism (Up Country Tourism)

Kandy is known as Sri Lanka’s hill capital. The focal point of the town is the golden roofed Dalada

Maligawa (Temple of the Tooth), a temple that houses Sri Lanka’s most important religious

relic—the Sacred Tooth of Lord Buddha. The Esala Perahera celebrations are an annual highlight

when a replica of the shrine is carried in a procession accompanied by dancers, drummers, and

over 100 splendidly clothed and decorated elephants.

Another popular tourist destination in the hill country is Nuwara Eliya, a small town, set in the

heart of the tea country. Nuwara Eliya is also known as `Little England'. It is located at an altitude

of 1,868 m (6,128 feet) in the Central Highlands and is considered one of the most important

locations for tea production in Sri Lanka. The town is overlooked by Pidurutalagala, the highest

mountain in Sri Lanka at 2,524 m (8,281 feet). The town was founded by Samuel Baker, the

discoverer of Lake Albert and the explorer of the Nile in 1846. Nuwara-Eliya is known as the

coldest city of Sri Lanka, with a mean annual temperature of 16°C. Because of its climate, the city

became the prime sanctuary of the British civil servants and planters in Ceylon.

The Central Highlands are also home to the Adam's Peak. This is a 2,243 m (7,359 feet) tall conical

mountain located in central Sri Lanka. It is well-known for the Sri Pada `sacred footprint’, a 1.8 m

rock formation near the summit. In the Buddhist tradition it is regarded as footprint of the

Buddha, in Hindu tradition that of Shiva, and in Muslim and Christian traditions that of Adam.

Travel and Tourism Industry in Sri Lanka 13

Overview of Tourist Inf lows

At the time of its independence from British rule in 1948, Sri Lanka’s economy was considered

much more prosperous than most of its Asian neighbours. The country also inherited a highly

competitive pluralistic political system, which was characterised by regular general elections

based on universal franchise. Due to its export of primary crops, Sri Lanka’s national income per

head was also one of the highest in Asia. Along with its high income, the country’s achievements

in health and education were better than most other developing countries.

From the 1970s however, the democratic political system and the territorial integrity of Sri Lanka

came under the threat of growing political conflict. In 1971, there was an insurrection organised

by a youth group of the Sinhala community, known as the Janatha Vimukthi Peramuna (JVP) to

capture state power. The militant youth movements of the LTTE in the northern parts of the

country also started in the mid 1970s. While the Sinhala community accounts for 74 percent of

the total population, the Tamil community is the second largest ethnic group, accounting for 13

percent of the total population. The LTTE gradually entered into a guerrilla war with the aim of

carving out a separate Tamil state in Sri Lanka. Because of the outbreak of two armed conflicts in

the 1980s the island nation got separated into `war zones’ and `peaceful territories’. While the

bloody civil war in the North East resulted in a collapsed of tourism industry there, in large parts

of the `peaceful areas’ of the island, the tourism industry managed to survive.

Source: SLTDA, IMaCS Analysis

Because of the ethnic conflict since the early 1980s, tourism in Sri Lanka has generally operated

at sub-optimal levels. Further compared to other Asian markets, growth rates of international

tourist arrivals had significant yearly and monthly fluctuations. International tourist arrivals into

Sri Lanka shrunk from record levels of 407,230 in 1982 to 184,732 in 1989, a negative CAGR of

about 12 percent.

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Exhibit 7: Sri Lanka - Growth in International Tourist Arrivals

Travel and Tourism Industry in Sri Lanka 14

Thereafter, the tourism industry picked up with tourist arrivals increasing to 566,200 in 2004.

However, arrivals shrunk in 2005 because of the tsunami of December 2004 and the break-down

of the cease fire agreement reached in 2002. In FY2009, tourist arrivals declined to 440-450,000

because of the global economic slowdown.

The decline in tourist arrivals also caused a fall in employment in the industry from 60,500 in

2007 to 52,900 in 2008. The Sri Lanka Tourism Development Agency (SLTDA) reported that the

industry provided direct employment to 52,071 persons in 2009 and another to 72,899 indirectly.

Source: SLTDA, IMaCS Analysis

In 2010, international tourist arrivals into Sri Lanka increased 46.1 percent to a record tourist

inflow of 654,477. These trends have continued into the first half of 2011 with a 37 percent (yoy)

growth. The key reason for the dramatic improvement in Sri Lanka’s tourism is the return of

peace following the May 2009 declaration of victory over the LTTE.

In fact, tourism inflows began to recover from mid-2009, a reversal from the double digit year on

year (yoy) declines of January-May 2009. Further, over the course of 2010, tourism markets such

as the US, Japan, the UK and other European countries relaxed their advisories against travel to

Sir Lanka.

298318

394 392408 403

302

366381

400 400

337

393

501

566549 560

494

438 448

655

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

200

250

300

350

400

450

500

550

600

650

700

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Arrivals-thousands (LS) Growth (RS)

Exhibit 8: Sri Lanka - International Tourist Arrivals and Growth

Travel and Tourism Industry in Sri Lanka 15

Source: SLTDA, IMaCS Analysis

Seasonali ty

The peak months for arrivals are November to April. The lowest number of arrivals is usually

recorded in May. There is a secondary peak in July-August, a shoulder period in September-

October and a low season in May-June. The reason is partly the seasons of the West Coast, with

its monsoon period from late May to July, and partly because Sri Lanka has traditionally attracted

Indian and European tourists during their winter seasons. In the recent year, there has been an

increase in summer travel because the short-haul European tourists have been attracted into

taking long-haul holidays.

Exhibit 10: Share of Tourist Arrivals by Month Per cent

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 7.0 6.7 9.2 7.7 7.4 8.3 10.3 9.3 7.9 8.0 8.8 9.3

2006 9.3 9.4 9.8 8.9 7.8 7.9 9.9 9.5 6.9 6.9 6.7 7.0

2007 11.4 8.7 7.1 6.7 5.3 6.2 8.9 9.1 7.5 7.5 9.1 12.4

2008 13.0 9.2 8.7 6.8 7.1 6.4 7.5 7.0 6.7 8.0 8.4 11.2

2009 8.6 7.6 7.6 5.8 5.5 6.8 9.4 9.2 8.5 8.4 9.9 12.7

2010 7.8 8.8 8.0 5.9 5.4 6.8 9.7 8.5 7.2 8.0 11.0 12.9

Source: SLTDA, IMaCS Analysis

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000Ja

n-0

4M

ar-0

4M

ay-0

4Ju

l-0

4Se

p-0

4N

ov-

04

Jan

-05

Mar

-05

May

-05

Jul-

05

Sep

-05

No

v-0

5Ja

n-0

6M

ar-0

6M

ay-0

6Ju

l-0

6Se

p-0

6N

ov-

06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-0

7Ja

n-0

8M

ar-0

8M

ay-0

8Ju

l-0

8Se

p-0

8N

ov-

08

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9Ja

n-1

0M

ar-1

0M

ay-1

0Ju

l-1

0Se

p-1

0N

ov-

10

Jan

-11

Mar

-11

May

-11

Arrivals Growth yoy (RS)

Exhibit 9: Monthly International Tourist Arrivals into Sri Lanka

Travel and Tourism Industry in Sri Lanka 16

Contri bution to GDP

According to estimates by the World Travel & Tourism Council (WTTC), Sri Lanka's travel and

tourism industry’s direct contribution to GDP peaked at 4.3 percent in 2004, but declined

substantially to 2.7 percent in 2009. However, its contribution to GDP is estimated to have

increased to 2.9 percent in 2010, primarily, because of strong growth in tourist arrivals and

spending. This primarily reflects on economic activity generated by industries such as hotels,

travel agents, airlines, restaurants and leisure industries and other passenger transportation

services (excluding commuter services). Over the period 2011-15, while travel and tourism

revenues are expected to grow at an annual rate of 12.9 percent in local currency terms (7.9

percent in US$ terms), its share of GDP is expected to increase to 3 percent by 2015.

Exhibit 11: Travel and Tourism Revenues and Contribution to GDP LKR billion Growth

(percent)

US$ million Growth

(percent)

Share of GDP

2000 40.45 19.2 0.53 9.1 3.2

2005 92.13 1.6 0.92 2.3 3.7

2006 103.29 12.1 0.99 8.4 3.5

2007 118.17 14.4 1.07 7.4 3.3

2008 131.32 11.1 1.21 13.5 2.9

2009 134.28 2.3 1.17 -3.6 2.7

2010 161.95 20.6 1.42 21.7 2.9

2011 187.86 16.0 1.56 9.6 3.0

2015 296.60 12.9 (2011-15) 2.08 7.9 (2011-15) 3.0

2020 477.93 10.0 (2016-20) 2.83 6.3 (2016-20) 2.8

Source: WTTC

Data from Sri Lanka’s national accounts statistics indicate that `hotels and restaurants’ accounted

for 0.50 percent of Sri Lanka’s GDP in 2010. Its share has largely remained at 0.50-0.60 percent

during the period, 2003-2010, with a significant increase in 2010. In real terms (at constant 2002

prices), the share of `hotels and restaurants’ declined from 0.58 percent in 2003 to 0.37 percent

in 2008, but has thereafter increased to 0.52 percent in 2010.

Exhibit 12: GDP from Hotels and Restaurants Current Prices Constant (2002) Prices

LKR million Growth

(percent)

Share of

GDP

LKR million Growth

(percent)

Share of

GDP

2005 14,218 20.9 0.58 9,186 -14.1 0.47

2006 16,646 17.1 0.57 9,411 2.4 0.45

2007 18,367 10.3 0.51 9,199 -2.3 0.41

2008 20,611 12.2 0.47 8,741 -5.0 0.37

2009 24,988 21.2 0.52 9,901 13.3 0.40

2010 33,213 32.9 0.59 13,845 39.8 0.52

Source: Department of Census and Statistics, Sri Lanka; IMaCS Analysis

Travel and Tourism Industry in Sri Lanka 17

Tourism – Import ant Source of Foreign Exchange

Tourism is one of the most important sources of foreign exchange for the Sri Lankan economy. In

2009, tourism ranked as the sixth largest foreign exchange earner, after textiles and garments,

tea, transportation services and rubber-based products. Tourism accounted for 2.6 percent of Sri

Lanka’s foreign exchange receipts in 2009. The earnings from tourism increased 1.1 percent in

2009, from LKR 37.09 billion (US$ 319.5 billion) in 2008 to LKR 37.51 billion (US$ 326.3 million) in

2009.

Exhibit 13: International Tourism Receipts

LKR Million Growth

(percent)

US$ million Growth

(percent)

Receipt per

day

(US$)

Growth

(percent)

1999 19,297 29.8 274.9 19.3 61.4 3.2

2000 19,162 -0.7 252.8 -8.0 62.3 1.5

2005 36,377 -14.7 362.3 -12.9 74.6 3.3

2006 42,586 17.1 410.3 13.2 83.4 11.8

2007 42,519 -0.2 384.4 -6.3 79.1 -5.2

2008 37,094 -12.8 319.5 -16.9 76.7 -3.0

2009 37,506 1.1 326.3 2.1 81.8 6.6

Source: SLTDA; IMaCS Analysis

In 2010, foreign exchange earnings from tourism increased 49.9 percent to LKR 56.24 billion

because of a substantial increase in tourist arrivals. In US dollar terms, the earnings increased

52.4 percent to US$497.4 million. Thus, tourism industry became Sri Lanka’s fourth highest

foreign exchange earner in 2010. Also, the average expenditure per-day-per-tourist increased

from US$ 81.8 in 2009 to US$ 85.4 in 2010.

WTTC estimates for domestic spending by Sri Lankan citizens on travel and tourism indicate that

in real terms, expenditure increased 6.5 percent in 2010 to LKR 134.6 billion, compared with a

decline of 5.3 percent in 2009. It is expected to increase 6.5 percent in 2011 to LKR 152.5 billion.

Exhibit 14: Domestic Travel and Tourism Spending

LKR billion Growth

(percent)

US$ billion Growth

(percent)

2000 35.16 15.8 0.46 6.3

2005 72.26 14.7 0.72 15.6

2006 86.52 19.7 0.83 15.9

2007 102.72 18.7 0.93 11.5

2008 119.83 16.7 1.11 19.1

2009 119.82 0.0 1.04 -5.8

2010 134.59 12.3 1.18 13.3

2011 152.53 13.3 1.27 7.1

2015 246.72 12.9 (2011-15) 1.73 7.9 (2011-15)

2020 420.81 11.3 (2016-20) 2.49 7.5 (2011-15) Source: WTTC

Travel and Tourism Industry in Sri Lanka 18

Domestic travel and tourism spending has largely followed real GDP growth trends. Following

slow growth in 2001, it increased at high rates through 2008 and then stagnated in 2009 as real

GDP growth declined from 6 percent in 2008 to 3.5 percent in 2009. Thereafter, it increased 12.3

percent in 2010, primarily, because of strong real GDP growth of 8 percent.

Source: IMaCS Analysis

Employment i n Tourism Indust ry

The tourist industry creates employment opportunities directly in tourism related business

establishments such as hotels and other accommodation units, restaurants, travel agents and

tour operators, recreation and entertainment businesses, souvenir, handicraft and other shops.

Indirect employment is generated in businesses, which sell goods and services to the tourism

sector. In general, it has been found that indirect employment generated as a result of tourism is

much higher than direct employment. WTTC estimates that for every 100 direct jobs created in

the tourism sector in Sri Lanka there will be about 140 indirect jobs generated in the supply

sectors.

Employment in the industry largely increased up to 2007. In 2008, tourism jobs (both direct and

indirect) shrunk by 22,104, as tourist arrivals declined by 55,540. Some of the decline could be

attributed to a substantial expansion in employment during 2006-07, when the Sri Lankan tourist

industry added around 20,000 jobs. However, tourist arrivals declined for most months in 2007.

As this trend continued into 2008, the industry cut jobs and only 1,836 jobs were created in the

industry during 2009, even as arrivals increased by 9,420.

-5%

0%

5%

10%

15%

20%

25%

30%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012F

Domestic T&T Spending Real GDP

Exhibit 15: Sri Lanka - Growth in Real GDP and Domestic Travel and Tourism Spending

Travel and Tourism Industry in Sri Lanka 19

Source: SLTDA, IMaCS Analysis

Approximately 61 percent of those employed in the tourism industry are in the accommodation

and catering sectors. In 2008, employment in this segment declined at a faster rate than the

overall fall, primarily, because of hotel occupancy rates and discretionary spending by local

residents. Travel agents and tour operators accounted for 13.7 percent of direct employment in

2009, with employment in this segment growing at a faster rate in 2009. Employment in airlines

also declined substantially in 2008 and 2009.

Exhibit 17: Direct Employment in Sri Lanka’s Tourism Industry

Employment Annual Growth

(percent)

2004 2005 2006 2007 2008 2009 2008 2009

Total 53,776 52,085 55,649 60,516 51,306 52,071 -15.2 1.5

Hotels and Restaurants 34,354 33,497 36,017 39,758 31,626 31,891 -20.5 0.8 Travel Agents and Tour Operators 7,092 6,136 6,825 7,538 6,725 7,134 -10.8 6.1 Airlines 4,613 5,907 6,056 5,396 5,251 5,245 -2.7 -0.1 Agencies Providing Recreational Facilities 180 112 132 297 259 291 -12.8 12.4

Tourist Shops 3,029 2,358 2,396 1,585 1,485 1,546 -6.3 4.1

Guides 2,460 1,957 2,010 3,450 3,460 3,477 0.3 0.5

National Tourist Organisation 279 298 303 305 313 327 2.6 4.5

State Sector 1,769 1,820 1,910 2,187 2,187 2,160 0.0 -1.2

Source: SLTDA, IMaCS Analysis

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

10,000

30,000

50,000

70,000

90,000

110,000

130,000

150,000

170,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Indirect

Direct

Growth (RS)

Exhibit 16: Sri Lanka - Employment in Tourism Industry

Travel and Tourism Industry in Sri Lanka 20

The total indirect employment in the sector was estimated at 72,899 in 2009. Thus the combined

direct and indirect employment in tourism increased 1.5 percent in 2009 to 124,970 persons. The

ratio of direct and indirect jobs generated was 3.6 jobs per tourist arrival.

Estimates by WTTC indicate that Sri Lanka’s travel and tourism industry is expected to employ

210,000 persons directly in 2011 (2.7 percent of total employment). This includes employment by

hotels, travel agents, airlines and other passenger transportation services. The industry’s total

contribution to employment including wider effects because of investment, supply chain and

induced income impacts is expected to be 554,000 jobs in 2011 (7.1 percent of total

employment). By 2021, it is expected to support 602,000 jobs (7.4 percent of total employment)

with an increase of 0.5 percent pa.

Exhibit 18: Share of Direct and Indirect Employment in Travel and Tourism Industry

Direct Total

Employment

(‘000 nos)

Growth

(percent)

Share of

Total

(percent)

Employment

(‘000 nos)

Growth

(percent)

Share of

Total

(percent)

2000 196.2 6.1 2.7 328.6 -22.6 4.5

2005 242.6 -12.1 3.2 572.3 -6.7 7.5

2006 237.4 -2.1 3.0 596.6 4.2 7.5

2007 221.9 -6.5 2.8 576.1 -3.4 7.3

2008 201.1 -9.4 2.5 543.7 -5.6 6.9

2009 188.4 -6.3 2.3 521.3 -4.1 6.6

2010 200.8 6.6 2.5 537.3 3.1 6.8

2011 210.1 4.6 2.6 554.2 3.1 7.1

2015 224.7 2.3 (2011-15) 2.7 584.4 1.7 (2011-15) 7.2

2021 243.9 1.4 (2016-21) 3.0 602.2 0.5 (2016-21) 7.4

Source: WTTC, IMaCS Analysis

Inbound Tourism Market

Asia and Western Europe are the largest source market for Sri Lanka, accounting for 37.3 percent

and 39.2 percent of the total arrivals respectively, in 2010. In 2010 however, there was a

decrease in Asia's share when compared with 2008 and 2009. The other markets were Eastern

Europe (5.4 percent), Australasia (5.7 percent), North America (6.1 percent) and Middle East (5.3

percent).

As in previous years, India remained as the major producer of tourist arrivals to Sri Lanka during

2010. Tourist arrivals from India aggregated 126,882 persons, accounting for 19.4 percent of all

international tourist arrivals. However, tourist arrivals from India declined for three successive

years from 2007 to 2009.

In 2010, with the relaxation of the travel warning by many countries, there was an upsurge in the

tourist arrivals in the country, particularly, from the Europe and North America. Tourist inflows

from North America increased 61.2 percent over 2009 accounting for 40,216 tourists. This

Travel and Tourism Industry in Sri Lanka 21

included 21,213 tourists from Canada, accounting for a growth of over 98 percent and 19,093

from the US with over 34 percent growth.

Arrivals from the Western European countries increased 51 percent to 256,861. While tourist

inflow from UK increased 29.3 percent to 105,496, inflows from Germany increased 54.2 percent

to 45,727. There was a significant 97 percent increase in tourists arriving from France with 31,285

tourists.

Arrivals from East Asia have also followed an upward trend with a 41.6 percent increase in 2010.

The majority of East Asian tourists were from Japan amounting to 14,352 tourists (over 31

percent growth). The number of tourists from South Asia increased 39.2 percent to 175,694 with

majority of them being from India. While the number of tourists from India increased 51.7

percent to 126,882, tourists from Maldives increased 12.1 percent to 35,791.

Countries in Australasia have also found Sri Lanka as a popular tourist venue and the number of

tourists from Australasia increased 43 percent to 37,290. Of these, tourist arrivals from Australia

increased 44 percent to 33,456.

Exhibit 19: Tourist Arrivals by Region and Major Countries

Arrivals (thousands) Growth (percent) Share (percent)

2006 2007 2008 2009 2010 2009 2010 2005 2010

North America 35.32 28.36 24.31 24.95 40.22 2.6 61.2 8.5 6.1

Canada 14.62 11.87 10.26 10.71 21.12 4.4 97.3 3.9 3.2 US 20.70 16.49 14.05 14.24 19.09 1.3 34.1 4.6 2.9

Latin America and

Caribbean 0.78 3.96 3.74 0.62 0.62 -83.5 0.5 0.1 0.1

Western Europe 228.45 194.45 167.19 170.12 256.86 1.8 51.0 41.4 39.2

France 22.69 8.09 10.59 15.89 31.29 50.0 96.9 4.9 4.8

Germany 47.40 35.04 30.63 29.65 45.73 -3.2 54.2 8.4 7.0

Italy 12.42 11.45 9.13 7.51 11.42 -17.7 52.0 1.9 1.7

Netherlands 19.36 17.53 13.03 11.29 17.86 -13.3 58.2 2.8 2.7

Switzerland 7.73 4.92 5.33 6.33 9.43 18.9 48.9 1.5 1.4 UK 88.31 94.06 81.33 81.59 105.50 0.3 29.3 16.9 16.1

Eastern Europe 14.22 25.57 29.44 26.31 35.52 -10.6 35.0 1.7 5.4

Russia 7.99 13.62 15.80 11.83 13.28 -25.1 12.2 0.7 2.0

Middle East 10.35 13.55 16.78 23.74 37.54 41.5 58.1 1.9 5.7

Africa 3.24 2.71 2.14 1.55 2.31 -27.7 49.0 0.4 0.4

East Asia 73.35 52.85 44.94 48.33 68.43 7.5 41.6 12.7 10.5

China 16.27 11.95 9.81 8.55 10.43 -12.9 22.0 1.8 1.6

Japan 16.19 14.27 10.08 10.93 14.35 8.4 31.4 3.1 2.2

Singapore 7.01 5.69 5.80 7.81 11.88 34.6 52.1 2.0 1.8

South Asia 168.78 149.63 128.10 126.21 175.69 -1.5 39.2 27.9 26.8

India 128.37 106.07 85.24 83.63 126.88 -1.9 51.7 20.6 19.4 Maldives 24.83 29.54 31.56 31.92 35.79 1.1 12.1 4.5 5.5

Australasia 25.13 22.92 21.84 26.07 37.29 19.4 43.0 5.4 5.7

Australia 21.85 20.24 19.54 23.24 33.46 19.0 44.0 4.7 5.1

Total 559.60 494.01 438.48 447.89 654.48 2.1 46.1 100 100

Source: SLTDA, IMaCS Analysis

Travel and Tourism Industry in Sri Lanka 22

Although tourist arrivals from India declined in 2008 and 2009, they increased to a record

126,882 persons in 2010. During the period January-June 2011, tourist arrivals from India

increased 48.3 percent (yoy) to 81,757 tourists. India’s real GDP has increased at an annual

average rate of 8.4 percent during FY2007-2011. With real GDP growth forecast to increase at an

annual rate of over 8 percent during 2011-15 and greater levels of disposable income, the

number of Indians travelling abroad could double every decade, creating strong demand for

recreational tourism and also for meetings, incentives and conferences. Because of its proximity

to India, Sri Lanka is better positioned to compete for this market than many other destinations

in South Asia and South-East Asia.

Both the Government of Sri Lanka and the private sector are aware of this strategic advantage

and have begun to jointly invest in products and promotional efforts geared to attract Indian

tourists, such as a `Ramayana’ circuit visiting sites featured in the ancient Hindu classic. As a

result, more and more Indian tourists are visiting the Ramayana sites in Sri Lanka. During the

month of January 2011, there were visits by two groups, one consisting of 400 tourists and the

other 150.

Exhibit 20: Tourist Arrivals by Region and Major Countries - 1st Half Arrivals Growth (percent) Share (percent)

1H 2009 2010 2011 2010 2011 2010 2011

NORTH AMERICA 10,765 18,317 22,753 70.2 24.2 6.6 6.0 Canada 4,625 9,913 11,744 114.3 18.5 3.6 3.1 US 6,140 8,404 11,009 36.9 31.0 3.0 2.9 LATIN AMERICA AND CARIBBEAN 418 297 519 -28.9 74.7 0.1 0.1

WESTERN EUROPE 74,536 108,250 143,454 45.2 32.5 38.8 37.6 France 7,394 13,480 24,354 82.3 80.7 4.8 6.4 Germany 12,377 21,500 25,539 73.7 18.8 7.7 6.7 Italy 3,170 4,202 5,622 32.6 33.8 1.5 1.5 Netherlands 5,084 6,527 10,197 28.4 56.2 2.3 2.7 Switzerland 2,893 3,693 4,697 27.7 27.2 1.3 1.2

UK 36,148 44,987 46,662 24.5 3.7 16.1 12.2

EASTERN EUROPE 13,926 16,935 21,189 21.6 25.1 6.1 5.6

Russia 6,494 6,195 7,877 -4.6 27.2 2.2 2.1

AFRICA 708 832 1,493 17.5 79.4 0.3 0.4

MIDDLE EAST 6,755 13,652 20,445 102.1 49.8 4.9 5.4

EAST ASIA 20,523 29,466 41,340 43.6 40.3 10.6 10.8

China 4,107 4,686 8,613 14.1 83.8 1.7 2.3

Japan 4,922 6,145 7,886 24.8 28.3 2.2 2.1

Malaysia 1,735 5,757 7,307 231.8 26.9 2.1 1.9

Singapore 3,055 4,743 6,643 55.3 40.1 1.7 1.7

SOUTH ASIA 50,336 76,816 111,570 52.6 45.2 27.6 29.2

India 30,902 55,138 81,757 78.4 48.3 19.8 21.4

Maldives 14,732 15,894 19,303 7.9 21.4 5.7 5.1

AUSTRALASIA 9,762 14,087 18,775 44.3 33.3 5.1 4.9

Australia 8,783 12,582 16,660 43.3 32.4 4.5 4.4

Total 187,729 278,652 381,538 48.4 36.9 100 100

Source: SLTDA, IMaCS Analysis

Travel and Tourism Industry in Sri Lanka 23

Tourist Profi le

There are two principal reasons for travel: business and leisure. However, classifying the purpose

of travel has become increasingly difficult as travellers tend to combine pleasure with business, in

order to take time and cost advantage. Leisure trips may include elements, characteristics and

motivations of business travel and vice versa.

Based on the declaration made by tourists on arrival, visits for pleasure (holiday, recreation and

sightseeing) accounted for 80 percent of international tourist arrivals into Sri Lanka in 2009.

Combining other purposes, non-business visits accounted for 91.4 percent of tourist arrivals. The

share of business visits peaked at 17.8 percent in 2006, but declined substantially to 8.6 percent

in 2009.

Exhibit 21: Purpose of Visit (per cent)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Pleasure 90.1 89.2 85.4 80.8 78.2 69.6 67.4 67.1 73.2 80.0

Business 4.8 6.7 9.4 9.1 10.6 16.9 17.8 10.5 8.5 8.6

Visiting Friends &

Relatives 2.1 1.8 2.0 6.2 6.4 8.0 7.6 8.3 8.3 5.2

Religious & Cultural 1.7 1.2 1.0 1.2 1.5 1.0 1.7 2.8 2.6 2.0

Others 1.3 1.1 2.2 2.7 3.4 4.5 5.5 11.3 7.4 4.3

Total 100 100 100 100 100 100 100 100 100 100

The largest proportion of business visitors come from Asia, particularly, India. Western Europe

accounts for the largest proportion of visitors for pleasure (40.8 percent), followed by 36 percent

from Asia and 6.4 percent from Australasia.

Around 16.3 percent of visitors from India visit Sri Lanka for business, compared with 83.7

percent for non-business purposes. Visitors from India for business and conventions were

estimated at 18,831 in 2006. There was a substantial decline to 5,163 in 2009. Considering that

visitors from India increased 52 percent in 2010, it is likely that visitors for business and

conventions too, would have recorded a significant increase in 2010.

Exhibit 22: Number of Visitors from India for Various Purposes

2004 2005 2006 2007 2008 2009

Total 105,151 113,323 128,370 106,067 85,238 83,634

Pleasure 27,834 36,222 39,754 18,351 12,495 13,658

Business 7,950 5,343 7,943 2,883 2,129 2,268

Conventions 11,941 8,726 10,888 7,716 6,404 2,895

Visiting Friends & Relatives 6,360 2,490 5,876 7,269 6,181 4,985

Religious & Cultural 968 969 1,432 11,765 6,234 1,503

Others 50,098 59,573 62,477 58,083 51,795 58,325

Share 100 100 100 100 100 100

Pleasure 47.6 52.6 48.7 54.8 60.8 69.7

Business 26.5 32.0 31.0 17.3 14.7 16.3 Conventions 7.6 4.7 6.2 2.7 2.5 2.7 Visiting Friends & Relatives 11.4 7.7 8.5 7.3 7.5 3.5 Religious & Cultural 6.0 2.2 4.6 6.9 7.3 6.0 Others 0.9 0.9 1.1 11.1 7.3 1.8 Source: SLTDA, IMaCS Analysis

Travel and Tourism Industry in Sri Lanka 24

Duration of Stay

The duration of stay (excluding outlying years) has averaged 9-12 days over the past three

decades. In 2009, an estimated 25.7 percent of tourists stayed for 1-3 nights, while another 29.2

percent stayed for 4-7 nights. However, the proportion of tourists staying for 8-14 days,

generally, increased to 34.1 percent in 2009.

Exhibit 23: Period of Stay (Percentage Distribution)

Nights

Average

Stay

(Nights) 1-3 4-7 8-14 15-21 22-30 >31

1990 5.0 12.8 29.5 26.3 13.3 13.1 10.8

1991 4.5 12.2 26.9 23.8 15.2 17.4 11.4

1992 25.2 26.2 27.5 14.1 4.9 2.1 10.3

1993 19.6 30.0 30.6 12.2 4.1 3.5 10.6

1994 18.1 34.5 30.9 11.6 3.4 1.5 10.4

1995 20.4 38.5 27.5 8.2 3.4 2.0 10.0

1996 29.6 24.7 27.7 11.5 4.6 1.9 9.8

1997 26.1 24.4 30.8 13.0 4.5 1.2 10.1

1998 23.7 25.1 33.7 12.6 3.8 1.1 10.4

1999 20.4 27.1 37.8 11.1 2.7 0.9 10.3

2000 21.9 26.4 35.9 12.2 2.6 1.0 10.1

2001 23.3 26.8 34.5 12.0 2.5 0.9 9.9

2002 22.6 27.0 34.7 12.1 2.6 1.0 10.1

2003 23.1 27.3 34.8 11.5 2.3 1.0 10.2

2004 23.8 27.6 34.1 11.8 1.9 0.8 10.1

2005 38.5 24.3 25.3 8.1 2.6 1.2 8.7

2006 28.3 26.4 32.2 10.2 1.8 1.1 10.4

2007 24.2 29.8 33.9 8.8 2.0 1.8 10.0

2008 26.4 28.7 33.2 8.7 1.8 1.2 9.5

2009 25.7 29.2 34.1 8.1 1.5 1.4 9.1

Source: SLTDA, IMaCS Analysis

In general, West Europeans stay longer than the average. North Americans and Australians also

record above average stays. By contrast, Asians make shorter visits to Sri Lanka. The Japanese

have a particularly short average stay. A large proportion of Japanese tourists make one-night

transit stopover in Colombo en-route to and from Maldives. The tendency of Europeans to stay

on for longer also explains why India accounts for the largest number of tourist arrivals and yet

ranks second in number of hotel nights spent in Sri Lanka. Travellers from the UK cumulatively

spend the highest number of tourist nights, followed by Indians.

Travel and Tourism Industry in Sri Lanka 25

Exhibit 24: Duration of Stay, Tourist Nights by Major Countries and Regions Average Duration of Stay

(Nights)

Tourist Nights

(thousands)

2007 2008 2009 2007 2008 2009

North America 10.7 12.0 10.7 301.11 271.75 265.89

Canada 10.8 13.8 11.3 128.11 134.48 121.87

US 10.5 10.2 10.1 173.00 137.27 144.08

Latin America and Caribbean 11.5 9.8 9.9 47.20 36.47 6.59

Western Europe 11.5 10.2 10.0 2,287.65 1,739.86 1,713.46

France 13.0 9.5 9.6 124.02 101.68 155.57

Germany 12.3 10.9 10.2 430.70 331.64 302.57

Italy 10.7 9.8 9.8 122.53 89.54 70.70

Netherlands 12.3 10.3 10.0 215.64 135.75 112.97

Switzerland 12.2 10.6 10.1 56.91 55.77 63.10

UK 11.5 10.5 10.2 1,082.02 846.10 829.71

Eastern Europe 12.0 7.9 8.0 261.57 232.57 200.67

Russia 12.0 8.2 8.5 162.36 129.81 96.82

Africa 9.6 9.1 7.9 28.71 21.42 12.57

Middle East 8.1 7.6 7.5 110.06 126.93 178.66

Asia 7.8 7.9 7.8 1,640.17 1,452.29 1,403.60

China 8.0 7.6 8.0 83.30 76.11 68.59

Japan 8.5 7.7 8.6 121.33 81.45 83.08

Malaysia 8.4 8.2 8.6 55.99 41.17 30.92

Singapore 7.7 7.6 7.5 43.82 43.34 59.82

India 8.1 8.1 7.9 857.84 718.12 657.83

Maldives 9.2 9.4 9.2 271.86 295.71 292.31

Australasia 11.5 11.5 10.2 263.62 284.21 294.35

Australia 11.5 13.6 11.5 232.77 260.37 266.50

Total 10.0 9.5 9.1 4,940.08 4,165.51 4,075.80

Source: SLTDA, IMaCS Analysis

Travel and Tourism Accommodation

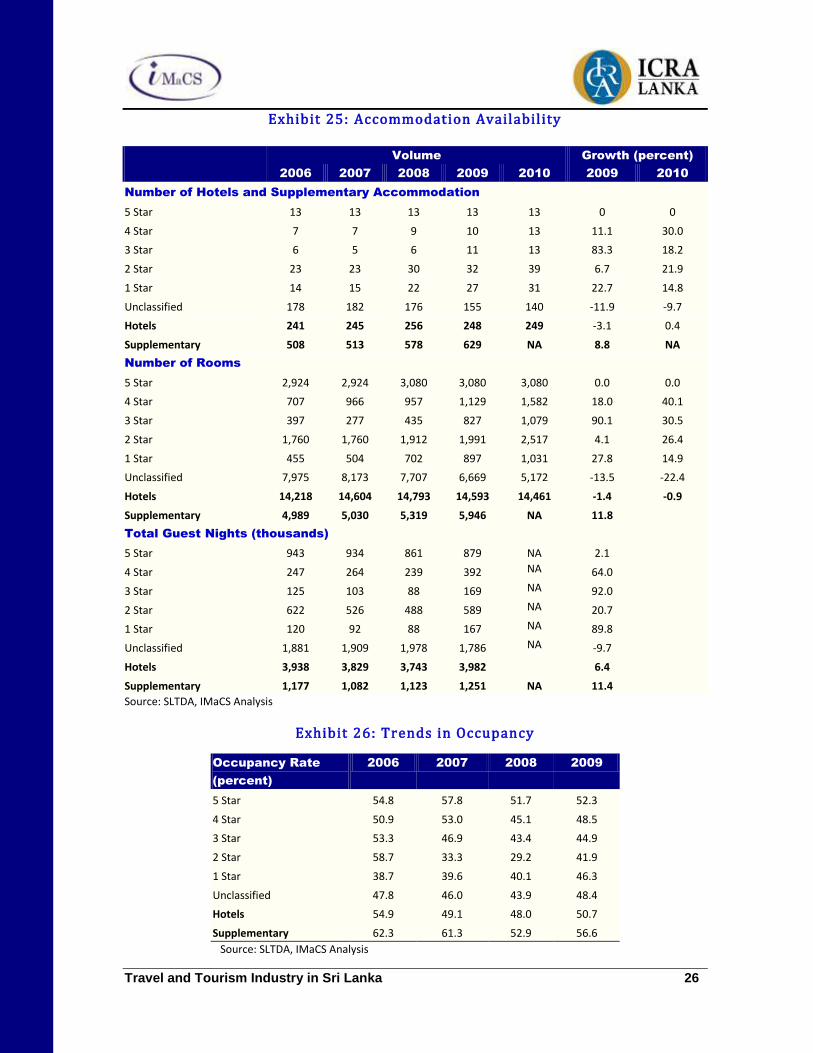

Sri Lanka offers a range of accommodation, from hotels and motels to individual guest houses,

self-catering and other forms of private accommodation. According to the SLTDA, at the end of

2010, the country had 249 registered hotels providing a total of 14,461 rooms. During 2009 and

2010, the authorities degraded a number of tourist hotel properties. However, the supply of

supplementary accommodation units such as guest-houses, motels, and inns increased by 51

additional units, from 578 in 2008 to 629 in 2009. Room occupancy rates increased 4.5

percentage points over 2009 to reach 48.4 percent.

Travel and Tourism Industry in Sri Lanka 26

Exhibit 25: Accommodation Availability Volume Growth (percent)

2006 2007 2008 2009 2010 2009 2010

Number of Hotels and Supplementary Accommodation

5 Star 13 13 13 13 13 0 0

4 Star 7 7 9 10 13 11.1 30.0

3 Star 6 5 6 11 13 83.3 18.2

2 Star 23 23 30 32 39 6.7 21.9

1 Star 14 15 22 27 31 22.7 14.8

Unclassified 178 182 176 155 140 -11.9 -9.7

Hotels 241 245 256 248 249 -3.1 0.4

Supplementary 508 513 578 629 NA 8.8 NA

Number of Rooms

5 Star 2,924 2,924 3,080 3,080 3,080 0.0 0.0

4 Star 707 966 957 1,129 1,582 18.0 40.1

3 Star 397 277 435 827 1,079 90.1 30.5

2 Star 1,760 1,760 1,912 1,991 2,517 4.1 26.4

1 Star 455 504 702 897 1,031 27.8 14.9

Unclassified 7,975 8,173 7,707 6,669 5,172 -13.5 -22.4

Hotels 14,218 14,604 14,793 14,593 14,461 -1.4 -0.9

Supplementary 4,989 5,030 5,319 5,946 NA 11.8

Total Guest Nights (thousands)

5 Star 943 934 861 879 NA 2.1

4 Star 247 264 239 392 NA 64.0

3 Star 125 103 88 169 NA 92.0

2 Star 622 526 488 589 NA 20.7

1 Star 120 92 88 167 NA 89.8

Unclassified 1,881 1,909 1,978 1,786 NA -9.7

Hotels 3,938 3,829 3,743 3,982 6.4

Supplementary 1,177 1,082 1,123 1,251 NA 11.4

Source: SLTDA, IMaCS Analysis

Exhibit 26: Trends in Occupancy

Occupancy Rate

(percent)

2006 2007 2008 2009

5 Star 54.8 57.8 51.7 52.3

4 Star 50.9 53.0 45.1 48.5

3 Star 53.3 46.9 43.4 44.9

2 Star 58.7 33.3 29.2 41.9

1 Star 38.7 39.6 40.1 46.3

Unclassified 47.8 46.0 43.9 48.4

Hotels 54.9 49.1 48.0 50.7

Supplementary 62.3 61.3 52.9 56.6

Source: SLTDA, IMaCS Analysis

Travel and Tourism Industry in Sri Lanka 27

Exhibit 27: Trends in Guest Nights in Hotels and

Supplementary Accommodations Foreign Domestic

Hotels Supplementary Total Hotels Supplementary Total

1999 3,837 211 4,047 610 263 874

2004 4,394 350 4,744 969 402 1,372

2005 2,858 392 3,249 818 474 1,292

2006 3,134 681 3,815 806 496 1,302

2007 2,778 599 3,377 1,051 497 1,548

2008 2,763 701 3,464 979 422 1,401

2009 2,818 779 3,598 1,163 472 1,635

Source: SLTDA, IMaCS Analysis

In 2010, the overall annual hotel room occupancy rates increased to a record level of 70.1

percent, representing an increase of 21.7 percentage points. This was due to the unprecedented

demand for hotel rooms, coming from both the domestic as well as foreign tourists.

Exhibit 28: Annual Occupancy Rate in Sri Lanka’s Hotels

Source: SLTDA, IMaCS Analysis

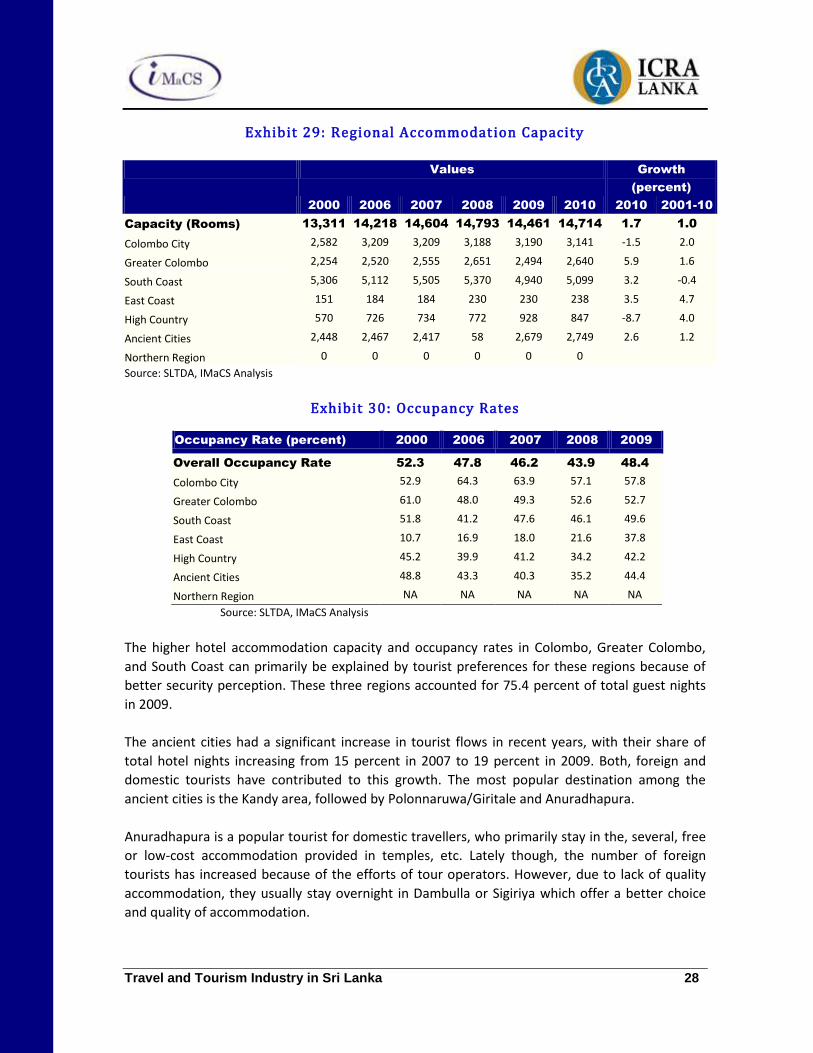

In 2009, the room capacity distribution in graded accommodations was 34.2 percent in the South

Coast region, 22.1 percent in the Colombo City region, 18.5 percent in the Ancient Cities region,

17.2 percent in Greater Colombo region, 6.4 percent in the High Country region, and only 1.6

percent in the East Coast regions. Since the 1980s, tourism in the Eastern, Uva, and North Central

region has languished, without significant investment in tourism.

57.8%

47.2%

48.4%55.3%

57.0%

56.6%

52.6%

40.3%

49.1%

52.8%

57.6%

52.3%

42.1%

43.1%

53.2%

59.3%

45.4%

47.8%

46.2%

43.9%

48.4%

70.1%

20%

30%

40%

50%

60%

70%

80%

1980 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Travel and Tourism Industry in Sri Lanka 28

Exhibit 29: Regional Accommodation Capacity Values Growth

(percent)

2000 2006 2007 2008 2009 2010 2010 2001-10

Capacity (Rooms) 13,311 14,218 14,604 14,793 14,461 14,714 1.7 1.0

Colombo City 2,582 3,209 3,209 3,188 3,190 3,141 -1.5 2.0

Greater Colombo 2,254 2,520 2,555 2,651 2,494 2,640 5.9 1.6

South Coast 5,306 5,112 5,505 5,370 4,940 5,099 3.2 -0.4

East Coast 151 184 184 230 230 238 3.5 4.7

High Country 570 726 734 772 928 847 -8.7 4.0

Ancient Cities 2,448 2,467 2,417 58 2,679 2,749 2.6 1.2

Northern Region 0 0 0 0 0 0

Source: SLTDA, IMaCS Analysis

Exhibit 30: Occupancy Rates